Grubhub delivery bicycles line a New York City sidewalk in February 2020.

The Washington Center for Equitable Growth this week delivered a comment letter to Amy DeBisschop, director of the Division of Regulations, Legislation and Interpretation at the Wage and Hour Division of the U.S. Department of Labor. The subject of the letter concerns the status of independent contractors under the Fair Labor Standards Act and is in response to requests for comment on the Department of Labor proposal to change standards for determining which workers are independent contractors and which are employees.

The proposed change would make it easier and simpler for an employer to classify workers as independent contractors. In our letter, we noted that:

Compared to the current baseline, and especially compared to available alternative regulations, this rule will increase the number of independent contractors and decrease the number of future workers in employee-employer relationships. In doing so, it will have a negative effect on workers’ well-being by facilitating economic transfers from workers to employers.

The proposed rule would both rob workers of the protections of the Fair Labor Standards Act, such as the minimum wage and overtime protections, and would result in the loss of other closely associated benefits of being a formal employee, such as access to health insurance, retirement benefits, protections from discrimination, and others. Our letter presents the economic literature that establishes that this rulemaking will have harmful effects on workers, and then details well-established labor market dynamics that the Department of Labor failed to consider in its own analysis of the proposal.

We close our letter by demonstrating that the Department of Labor made an arbitrary and capricious decision not to examine the actual economic costs and benefits of this proposal, even though such costs are documented by studies cited by the department itself, and that instead, it invented highly speculative time savings to justify the proposal.

This pandemic is a time to strengthen, not weaken, crucial labor protections. Gig and contract workers have some of the lowest and most precarious earnings, and receive few protections under U.S. labor laws. Instead of making it easier for companies to pay workers less, the department should raise the standard for when it is acceptable for companies to exempt their workforce from the minimum wage, overtime rules, and child labor laws. This rule needs to be re-examined and rewritten.

Read the full letter submitted to the U.S. Department of Labor’s Wage and Hour Division.

A safe and strong banking sector is more important than ever as the coronavirus recession continues to strain individuals and families in the United States. In response to the U.S. Department of Justice’s Antitrust Division’s request for comments on its Bank Merger Review Guidelines, Washington Center for Equitable Growth Policy Director Amanda Fischer, along with Graham Steele, senior fellow at the American Economic Liberties Project and director of the Corporations and Society Initiative at Stanford University Graduate School of Business, and Sandeep Vaheesan, legal director at the Open Markets Institute, have submitted a comment letter to the Department. In the letter, Fischer, Steele, and Vaheesan argue that the Antitrust Division, along with banking regulators, must reverse the longstanding trend of deregulation and consolidation in the banking industry in order to promote financial stability and ensure the provision of credit to the “real economy.”

The U.S. banking industry has been characterized by a long period of increasing consolidation, coinciding with an increase in income and wealth inequality for people across the United States. The top four banking organizations now control nearly 36 percent of all bank deposits in the United States, up from 9.4 percent in 1995. Likewise, these four large banks held 86.7 percent of the total banking industry’s notional amount of financial derivatives as of the first quarter of 2020.

Mergers are increasingly rubberstamped by antitrust and banking regulators. The comment letter notes that since the early 1980s, merger denials by the Antitrust Division and banking regulators have been infrequent. Similarly, between 1972 and 1982, the Federal Reserve Board, which regulates bank holding companies, denied 63 proposed acquisitions on competitive grounds. From 1983 to 1994, with far greater numbers of proposals, it denied only eight. Bank merger approval rates are at historic highs, and the Federal Reserve signed off on 95 percent of merger applications in 2018—its highest approval rate since it began keeping track.

The result of this increased consolidation is decreased financial stability, exacerbation of the problem of “too big to fail,” less access to credit among small businesses and consumers, and a decline in services provided to communities, especially communities of color.

The letter’s authors conclude by arguing that the U.S. public is better served by proposals that take meaningful steps to reverse consolidation in the banking industry, and finance more broadly, so as to promote equity, efficiency, stability, and justice in the U.S. financial system. In particular, the Antitrust Division should focus its energies on the following policies:

Implementing more stringent enforcement of chartering and restrictions on banking activities

Revisiting bank ownership limitations

Imposing more stringent limits on concentration, tying, and management interlocks

Reconsidering the role of settlements in penalizing and deterring illegal and improper conduct within large banking conglomerates

To read the entire letter to the Antitrust Division of the U.S. Department of Justice, click here.

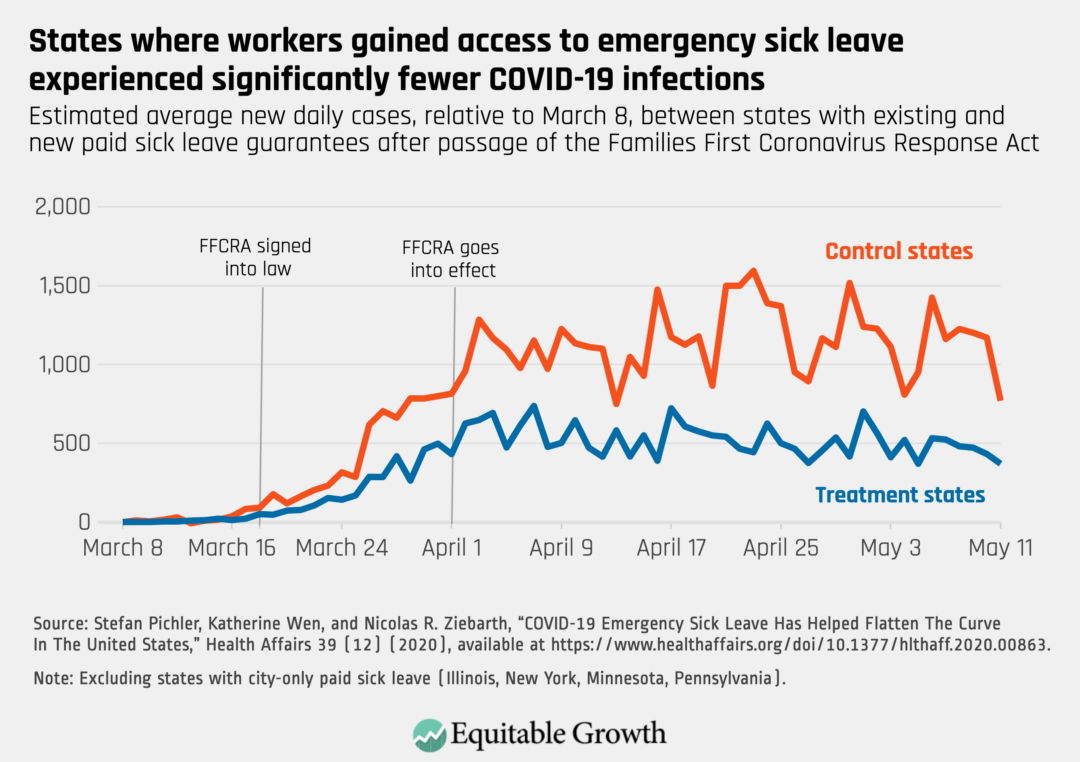

Paid sick leave is an important public health tool in the fight against COVID-19.

The United States is one of three high-income nations that does not guarantee paid sick leave for workers.1 As of March 2020, 25 percent of private-sector workers had no access to paid sick leave. This number is higher for part-time workers (55 percent) and low-income workers (69 percent).2

Without access to paid sick leave, employees who are financially constrained may show up to work sick. When that happens, they risk passing their illness to others and impose costs on employers through lost productivity.3 Several studies demonstrate how paid sick leave guarantees at the state and local level can benefit public health and improve worker productivity, with one recent study finding an 11 percent decline in flu-like illnesses in the first year after such a guarantee was enacted into law.4

When the coronavirus pandemic hit the United States, the U.S. Congress recognized that paid sick leave supports public health and economic well-being, and passed the Families First Coronavirus Response Act on March 18, 2020. The new law, part of several measures to support the economy and health of the nation against the coronavirus and COVID-19, the disease caused by the virus, allows qualified workers across the country who are affected by COVID-19 to take up to 2 weeks of sick leave at full pay.5

Now, a new study published in Health Affairs shows that the law was successful in “flattening the curve” of COVID-19 transmissions and was associated with approximately 400 fewer cases of COVID-19 per day in states where the law gave workers new access to guaranteed sick leave.6 While no one study is definitive, it offers some of the first evidence of the law’s efficacy in supporting public health.

Key takeaways

Paid sick leave is an important public health tool in the fight against COVID-19, reducing infections by 400 cases per day in states that previously had no paid sick leave guarantee.

Extending paid sick leave benefits beyond December 2020, when the current emergency benefits expire, would ensure that the United States has this necessary public health tool for the duration of the pandemic.

If more people are eligible for paid sick leave, including people employed by larger firms who are currently ineligible for emergency paid leave under the new law, then it is likely even more cases would be prevented.

About this new study in Health Affairs

Looking at the period of March 6, 2020–May 11, 2020, the researchers find that states where workers gained new access to guaranteed paid sick leave through the Families First Coronavirus Response Act saw a statistically significant 400 fewer confirmed COVID-19 cases per day.7 This translates to a 56 percent decrease in infections in these states.

To arrive at these findings, the authors compared infection rates before and after the passage of the new law in states with existing paid sick leave guarantees (the control group) and states without such a guarantee (the treatment group). The authors also controlled for state populations, testing capacities, state and local policies such as stay-at-home orders, and other geographic and temporal factors. (See Figure 1.)

Figure 1

These findings are in line with research conducted prior to the pandemic reporting similar 30 percent to 40 percent declines in influenza-like infections following the implementation of various local paid sick leave ordinances.8

These findings likely underreport the potential public health benefits of a comprehensive paid sick leave guarantee. The Families First Coronavirus Response Act does not provide sick leave benefits to workers at large firms with 500 or more employees. This provision, along with other exemptions that prevent healthcare workers and emergency responders from accessing this emergency paid leave, carved out 53 percent to 60 percent of the private-sector workforce from the law’s sick leave benefits.9 While 89 percent of workers at large firms already have access to paid sick leave through their employers, that leaves an estimated 6.5 million workers without any employer-provided sick leave.10

Policy implications

Extending access to emergency paid sick leave through 2021 would ensure that the United States benefits from this important public health tool through the expected duration of the pandemic. Currently, access to emergency paid sick days is set to expire on December 31, 2020, yet experts say the pandemic will stretch on past that date.11 Additionally, a permanent paid sick leave guarantee, such as the one proposed in the Healthy Families Act, would ensure that workers can keep these protections beyond the current public health crisis.12

Expanding access to emergency paid sick leave could yield even greater public health benefits than those identified in this latest study. Closing the coverage gap for workers at large firms would likely yield even greater public health benefits. The HEROES Act, passed by the U.S. House of Representatives on May 15, 2020, would eliminate this carve out for large businesses.13

Conclusion

Building on prior research on the public health and economic benefits of paid leave, this new study demonstrates that sick leave through the Families First Coronavirus Response Act played an important role in flattening the curve of COVID-19 transmissions in the early months of the coronavirus pandemic.14 Expanding and extending access to these benefits could have critical public health implications in 2021 and beyond.

The Health Affairs study presents early insight into how paid leave is supporting public health in the COVID-19 pandemic, and new data-driven evidence of the importance of paid leave, with support from the Washington Center for Equitable Growth, will enable researchers to continue studying how paid sick leave and paid family and medical leave can support workers, public health, and the economy in years to come.15

1. Humans are wired to believe that all kinds of bad things are catching, and thus you should avoid close contact with people who have them. In our modern economy, this applies to the unemployed. Most of the fear of hiring people who have been or are unemployed is not “rational” statistical discrimination, but rather this monkey brain predisposition. It is very damaging to the economy. Read Peter Norlander, “Addressing long-term U.S. unemployment requires confronting the stigma against the unemployed amid the coronavirus recession,” in which he writes: “I and … Geoff Ho … Margaret Shih … and Todd Pittinsky … examined the psychological roots of employer discrimination against the unemployed … Stigma against unemployed workers operates like other psychological prejudices and biases, is unjustifiable on productivity grounds, and occurs nearly instantaneously to workers losing their jobs.”

2. This is going to be very good. You should go to this, virtually that is. Please attend “Equitable Growth’s Antitrust Transition Report Event: “A virtual conference on November 19 to discuss the release of Equitable Growth’s antitrust transition report … Antitrust enforcement has failed to protect the competitiveness of the U.S. economy … Federal antitrust enforcers in the U.S. Department of Justice’s Antitrust Division and the Federal Trade Commission have been criticized for being too lax, and courts have been criticized for incorrectly limiting the reach of the antitrust laws. Equitable Growth’s upcoming transition report is the work of a committee of academics, legal experts, and former government officials, assessing the antitrust landscape and providing their recommendations for the next administration’s antitrust enforcement priorities to correct these failures.”

Worthy reads not from Equitable Growth:

1. Heather Boushey assesses herself as having gone five-for-five in her predictions made last March. She is right, as are her steps to deal with the coronavirus recession. Read her “Economic inequality made the U.S. more vulnerable to the pandemic,” in which she writes: “I made five predictions about the US economy in 2020. We would be hit harder … U.S. states and localities with paid sick days and family and medical leave policies would see fewer transmissions of the coronavirus … Mandated sick leave reduces the rate of seasonal flu by as much as 40 percent … Transmissions would be higher because high medical costs … would cause many workers to fear going to the doctor … The recession would be deeper and more protracted because our social support system is one of the worst among developed countries … We would experience the recession more deeply because policymakers don’t understand that the economy depends on people. The economy needs people to stay healthy so they can work and to have the resources to consume … We need to contain the coronavirus. It’s shocking that the world’s leading economy still does not have in place a comprehensive plan for testing, tracking and tracing. We also need to renew the relief for workers, families and small businesses that expired at the end of July and keep it in place until we recover fully. Plus, we need to give every worker access to a safe working environment, paid family leave, paid sick leave and health insurance.”

This is a post we publish each Friday with links to articles that touch on economic inequality and growth. The first section is a round-up of what Equitable Growth published this week and the second is relevant and interesting articles we’re highlighting from elsewhere. We won’t be the first to share these articles, but we hope by taking a look back at the whole week, we can put them in context.

Equitable Growth round-up

The coronavirus recession is resulting in millions of Americans either laid off or furloughed as businesses around the country close either temporarily or permanently due to the public health crisis. This jobs crisis is accompanied by record-setting levels of Unemployment Insurance claims—and these don’t even include the many more workers who are eligible but do not apply for benefits or wrongly believe they are not eligible. This in turn reflects the severe stigmatization in our society of joblessness and being unemployed—a stigma that threatens both our future economic recovery and the psyche of millions of capable workers let go through no fault of their own. Peter Norlander examines the effect of this stigma against the unemployed—labeling them as lazy, less productive, and personally at fault for not having a job—amid the coronavirus recession. He finds that this vilification, along with the existing faults within the Unemployment Insurance system, inhibits the delivery of jobless benefits to workers, leads to discrimination in hiring, and can have lasting damage to workers and the U.S. economy. Norlander concludes with several policy recommendations to address this stigma toward the unemployed, explaining why these suggestions would help unemployed workers re-enter the job market quickly and efficiently, and thus support the broader economy.

Student loan debt is a longstanding problem for workers, especially younger and lower-income workers, in the U.S. labor force. But an in-depth look at the Federal Reserve’s 2019 Survey of Consumer Finances reveals that this crisis ballooned in recent years—and it is likely getting even worse amid the coronavirus recession. In fact, average student debt-to-income ratios are now 0.56 among those adults who have student debt, falling most heavily on those households in the bottom 50 percent of the income distribution and especially on Black Americans, writeRaksha Kopparam and Austin Clemens. Though some debt forbearance was provided in one of the coronavirus relief packages passed in March, and other programs such as income-based repayment plans attempt to alleviate debt burdens more generally, much more is needed to fully mitigate the effects of the student loan crisis on households across the country. Kopparam and Clemens analyze the data, summarize its main findings, and conclude with the policy implications of rising student debt-to-income ratios.

New research on a German law requiring varying levels of worker representation on some boards of directors shows that this representation does no harm to revenues or corporate profits while giving workers a much-needed voice in corporate decision-making. The law was overturned for new companies in 1994 but upheld for certain businesses already in existence, providing researchers with natural setting for testing the effect of including workers on boards. Kate Bahnsummarizes the new paper, which found that when worker and shareholder representatives hold equal or near-equal power on boards, they operate by consensus rather than contention. This consensus yielded no significant impact on overall wages or employment, according to the study, alongside a slight increase in capital assets. More significantly, Bahn writes, when workers were included on boards, the study found an increase in worker productivity, with added values accruing mainly to capital and not labor, as well as a noteworthy reduction in outsourcing, with no meaningful effect on profits and revenues. This suggests that worker representation does not lead to negative outcomes for companies, such as bankruptcy.

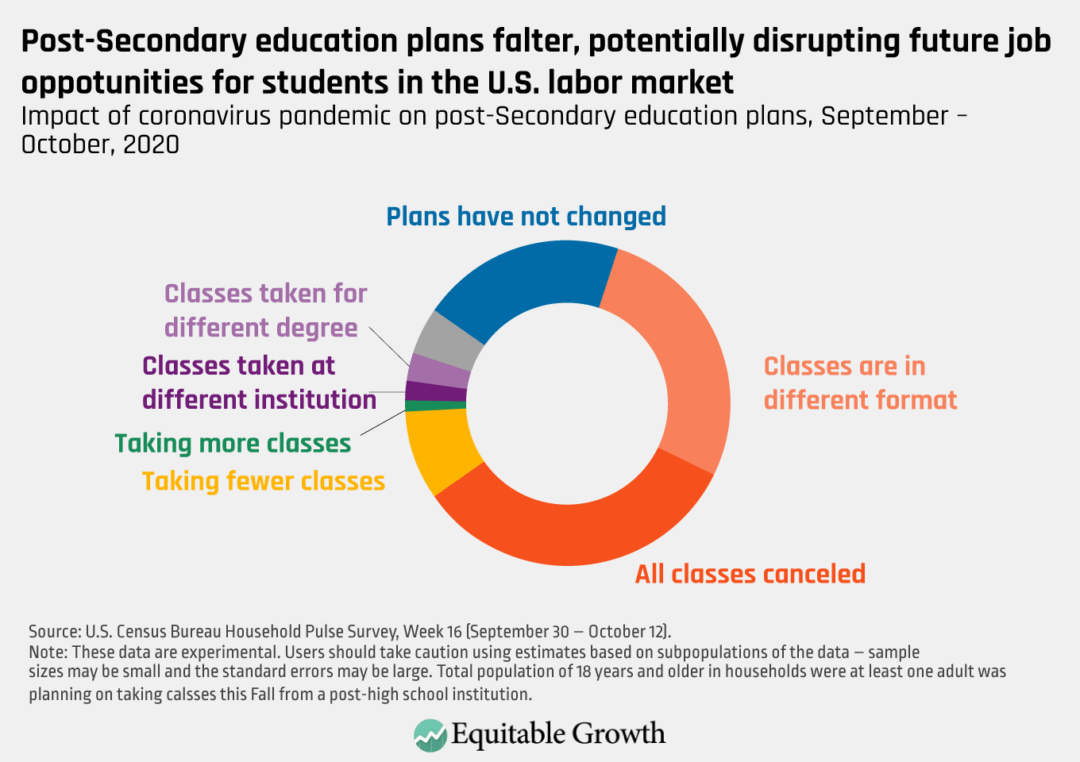

Earlier this week, the U.S. Census Bureau released new data on the effects of the coronavirus pandemic on workers and households. Austin Clemens, Kate Bahn, Raksha Kopparam, and Carmen Sanchez Cumming put together five graphs highlighting important trends in the data, including the racial disparities in food insecurity, in the ability to pay household expenses, and in loss of income since the start of the recession as well as the impact of the coronavirus on students’ postsecondary education plans.

Head over to Brad DeLong’s latest Worthy Reads, for his takes on must-read content from Equitable Growth and around the web.

Links from around the web

The majority of Americans believe the U.S. economy is rigged against them, writes Samantha Fields for Marketplace. In fact, according to a recent poll, more than 80 percent of Black Americans, 70 percent of women, and two-thirds of Americans overall feel that the economy works better for some people than it does for others—namely, the wealthy, the powerful, and White Americans while everyone else gets left behind. Fields examines the data and its implications, particularly amid the coronavirus recession as millions struggle to pay basic expenses, and compares this year’s results with those from similar polls taken in 2016. She interviews several people across the country and varying demographic groups for their takes on who is benefitting from U.S. economic growth and why some people have it better than others.

It’s no secret that the coronavirus pandemic caused a child care crisis in the United States. Many schools are operating virtually or offering only part-time in-person learning and child care centers are closing. It’s also no secret that women tend to shoulder the majority of home responsibilities, including child care. So, it shouldn’t come as a surprise that the pandemic is forcing women out of the labor force in much higher numbers than men—four times as many in September, according to the U.S. Department of Labor’s jobs report for last month. NPR’s Andrea Hsureports that this trend is hitting even the most successful women, many of whom are sidelining their hard-earned careers to take care of overwhelming household needs. This may well put many of their future promotions, earning power, and leadership positions at risk, Hsu continues, threatening a generation of gains for women in the workforce. The uncertainty surrounding the pandemic and how much longer it will continue to wreak havoc on U.S. society and the economy only adds to this rolling crisis.

New research shows that access to paid sick leave is an essential tool in reducing the transmission of the coronavirus. The study, summarized by HuffPost’s Emily Peck, looked at the impact of the emergency paid sick leave benefit in early coronavirus legislation, which provided 10 days of sick leave for workers with COVID-19 working for companies with fewer than 500 employees. It found that this emergency benefit prevented up to 400 cases of coronavirus per day per state, or roughly 15,000 cases prevented in the United States per day. Though experts say paid sick leave is not a “silver bullet,” it does slow the spread of the virus and can be extremely effective at doing so. Peck writes, however, that the emergency paid leave benefit is set to expire at the end of this year even though the coronavirus will certainly still be spreading throughout the country. What’s worse, the United States does not have a universal paid sick leave program to pick up where this emergency benefit leaves off. A universal paid leave program is long overdue: The United States is the only developed country in the world to not offer such a benefit for all workers, which some experts argue may be why case numbers in the United States have been so much higher than in other comparable nations.

Six months into a pandemic that is keeping many businesses closed across the United States, and with close to 1 million new unemployment claims continuing to be added each week, there should be widespread agreement that unemployed workers are blameless for their condition. Yet stereotypes that find fault with jobless workers are already appearing amid the coronavirus recession and are an obstacle to economic recovery that threatens to leave lasting scars on unemployed individuals.

The stigma of unemployment is an unfounded bias that views the unemployed as lazy, less-productive workers who are personally defective, worthy of contempt, and to blame for being unemployed. Prejudice against the unemployed hampers the effective delivery of benefits to millions of workers out of a job, leads to hiring discrimination against the unemployed, and can cause long-term damage to workers and the economy.

I and my co-authors Geoff Ho at Rogers Communications Inc., Margaret Shih at the University of California, Los Angeles, Daniel Walters at INSEAD, and Todd Pittinsky at Stonybrook University examined the psychological roots of employer discrimination against the unemployed in the aftermath of the Great Recession of 2007–2009.16 We find that the stigma against unemployed workers operates like other psychological prejudices and biases, is unjustifiable on productivity grounds, and occurs nearly instantaneously to workers losing their jobs.

This issue brief examines these findings in light of the importance of preventing unemployment and mitigating the downside impacts of unemployment, as policymakers address the continuing damage in the U.S. labor market caused by the current coronavirus recession. I will first examine current U.S. unemployment trends and then document how unemployed workers are discriminated against in the job market due to the stigma of being unemployed. This issue brief then details how this discrimination scars unemployed workers for the rest of their careers while sapping U.S. economic growth.

I close with some policy recommendations to address the stigma of unemployment, among them:

Reforms to the Unemployment Insurance system

Automatic stabilizers for unemployment benefits that match the distribution of benefits to the state of the economy

Work-share employment policies

Direct government jobs programs

In these ways, the stigma of unemployment is overcome by policies that help unemployed workers exit their joblessness as quickly and efficiently as possible to help them and the broader U.S. economy.

U.S. unemployment trends in the coronavirus recession

In July 2020, an unemployed Florida worker who had not received any benefits after 5 months without work said, “Gov. DeSantis, if you hear this, please, please help me get my unemployment. I’m not asking for anything that’s not mine. I’m not a lazy bum. I’ve worked my whole life.”17

This unemployed worker’s plea is emblematic of the stigma associated with being unemployed and the challenges facing a growing number of unemployed workers. Unemployment trends suggest that a lack of work is particularly likely to affect Black workers and women workers. Evidence suggests that rates of job displacement in economic downturns are discriminatory, meaning that Black workers are more likely to be laid off, all else equal, greater than what can be explained by differences in the types of sectors and jobs where Black workers are overrepresented or years of work experience.18 This contributes to the persistent 2-to-1 Black-White unemployment ratio.19

Workers’ time out of work is not only lost income during that time period, but also leads to diminished future earnings. This dynamic is especially evident among women workers who need to take time off for family caretaking.20 The disadvantage is now exacerbated in this recession alongside the public health crisis that has increased family care needs. Research on differences in outcomes by generations of Americans amid the Great Recession shows that often, the groups hit the hardest by unemployment in a downturn will take the longest to recover jobs and their earnings—even once the economy is technically in an expansion.21

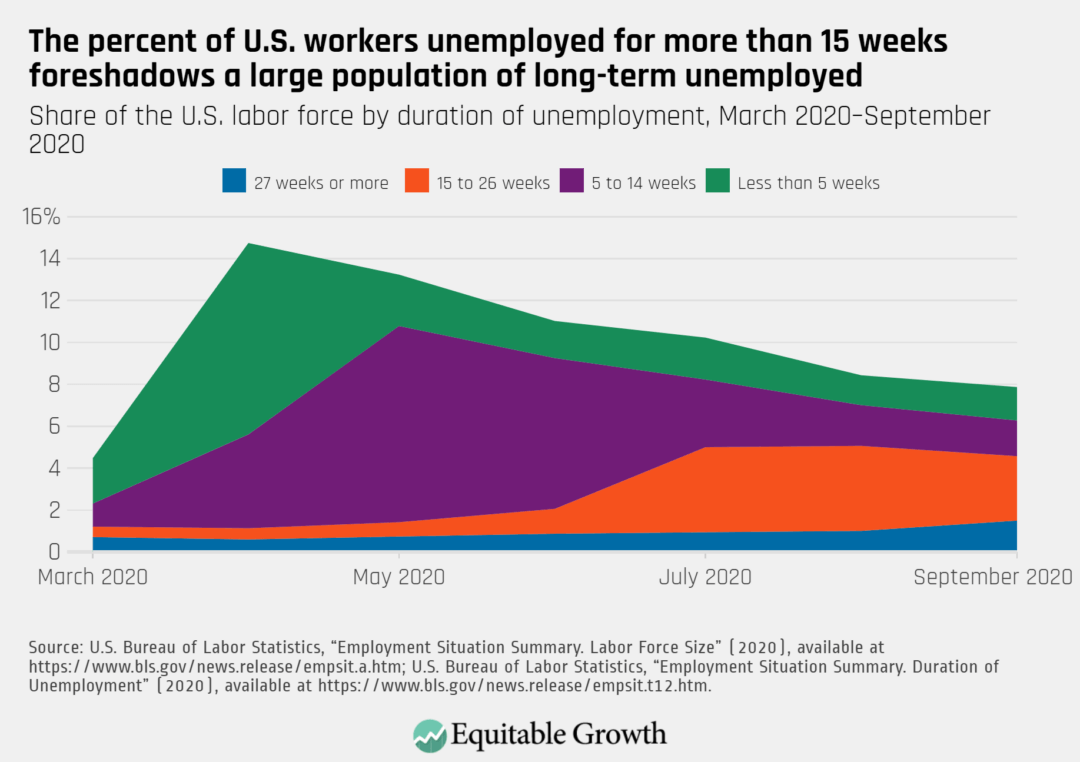

Today, the first waves of those unemployed due to the coronavirus recession are about to enter long-term unemployment, defined as being unemployed for more than 26 weeks. Almost 800,000 workers first laid off in March entered long-term unemployment in the month of September. As of September, 4.6 percent of the U.S. labor force, or 58 percent of the unemployed—7.3 million workers—are now unemployed for more than 15 weeks. (See Figure 1.)

Figure 1

For the 2.4 million long-term unemployed workers in September, and for the overall health of the U.S. economy, addressing the stigmatization of unemployment is a major challenge now and will remain so in the years ahead.

The stigma of unemployment

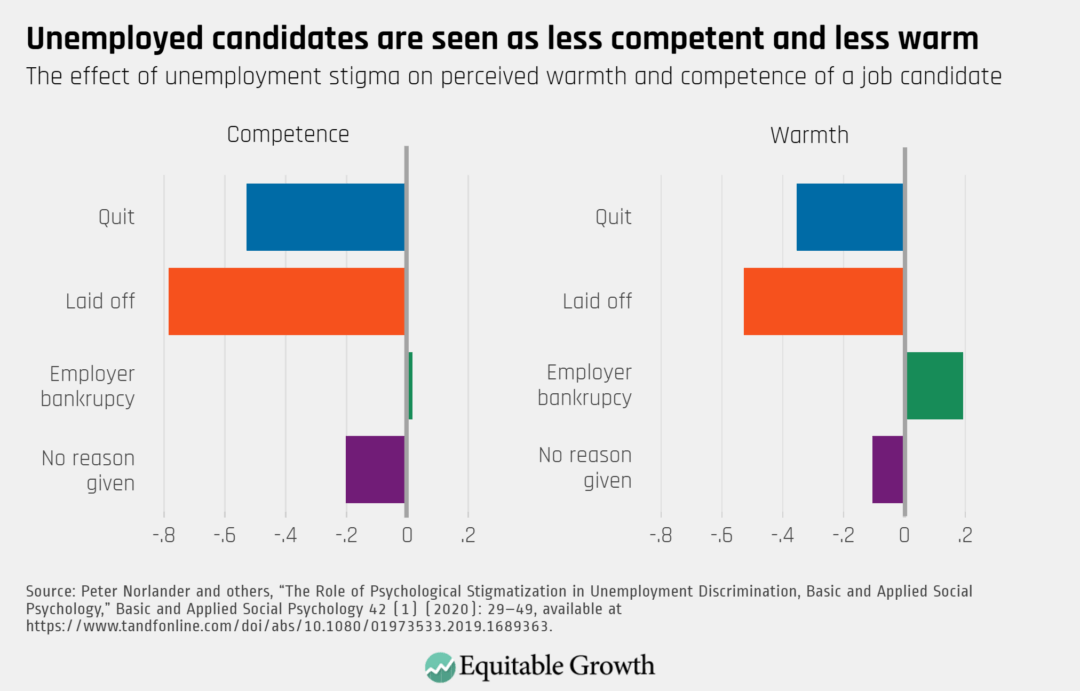

My and my co-authors’ research finds that hiring managers and HR departments often blame unemployed workers for losing their jobs, even when laid off in a severe recession. We presented online and student respondents, as well as real hiring managers and HR professionals, with different reasons for why a fictional job candidate became unemployed, including:

Lay offs

Quitting

Employer bankruptcy

No reason given

We find that an unemployed job seeker was a target of discrimination, compared to an employed job candidate. Specifically, we conducted five studies that asked participants to evaluate an otherwise-identical resume of a worker who is either unemployed or employed at the time of applying for a job. The results show that the unemployed are evaluated harshly, and not just in terms of their abilities.

Only by emphasizing in the clearest way that the unemployed person was not at fault for being unemployed—by specifying that the unemployed person was out of job because their former employer went out of business—could we reverse the stigma of unemployment that blames the victim. In addition to being seen as less competent, an unemployed job candidate is seen as less warm, less trustworthy, less well-intentioned, less friendly, and less sincere, compared to employed job candidates. (See Figure 2.)

Figure 2

In the aftermath of the Great Recession of 2007–2009, long-term unemployment persisted at high levels for more than 5 years. It’s obviously too early to tell whether this same trend will play out after the end of this recession, but stigma against the unemployed can harm job candidates even if they are out of work for a short period of time. In a field study that involved sending real resumes to real job advertisements, our study finds that discrimination occurs even when a resume shows that the unemployed person was employed until the prior month. This suggests that the stigma and discrimination against the unemployed is not justified by the theory that firms discriminate against unemployed workers because of skills lost during long durations of unemployment.

Unemployment is one channel through which an individual can be marked by stigma. Research by sociologist David Pedulla at Harvard University shows that members of disadvantaged demographic groups carry stigma even before the experience of unemployment begins and thus face discrimination in the labor market regardless of an employer’s perceptions of their employment status and reason for job separation. Because Black, Latinx, and women workers already have higher unemployment rates than White males and are already subject to high levels of discrimination, there may not be much room for the level of discrimination they face to increase. Indeed, Pedulla finds that the level of stigma increases most for White males, who do not face prejudice based on their demographic group.2223

The consequences of stigma

When workers are unemployed for a long period of time, this can lead to long-lasting damage to the psychological well-being and economic future of individuals.24 Joblessness decreases self-esteem, a sense of being in control of one’s destiny, and confidence. At the same time, it increases alienation, anxiety, and depression.25 Some research shows that joblessness may impact Black workers to a greater extent, due to fewer resources available to recover from the downside effects described here.26 As described above, Black workers are laid off more frequently, have higher unemployment rates, and face greater disparities in the coronavirus recession.

In addition, research demonstrates that long-term unemployment leads to:

Targeting the unemployed for relief is an essential first step to prevent suffering and speed up an economic recovery. Unemployment Insurance benefits help mitigate the damage of unemployment by lessening wage scars, among other benefits.31 But in addition to this program, and precisely because unemployment is so stigmatized and has such long-lasting damage on individuals and the economy, efforts focused on preventing further unemployment and mitigating long-term unemployment should be at the center of recovery plans.

Policies that would prevent more workers from being stigmatized by more swiftly re-employing the unemployed are described in the following section.

Don’t let unemployment stigma get in the way of economic recovery

The Coronavirus Aid, Relief, and Economic Security, or CARES, Act provided $600 in supplemental weekly jobless benefits, which expired at the end of July. The law also extended unemployment benefits from the usual 26 weeks to 39 weeks, with that extension set to expire on December 31, 2020.32 These benefits are expiring far too soon. Economists estimate that the peak of long-term unemployment in the coronavirus recession will involve 2 million workers who will be unemployed for more than 46 weeks by early 2022.33

Already, conservatives opposed to extending these benefits seek to shift the blame to unemployed workers. Conservative commentators Stephen Moore, Art Laffer, and Steve Forbes argue that benefits for the unemployed discourage work. And Republican Sen. Lindsay Graham (SC), summing up the views of many of his conservative colleagues on Capitol Hill, termed expanded unemployment benefits a “perverse incentive.”34 This argument is based on a stigmatized view of unemployment because it assumes that workers prefer leisure to work (are lazy) and blames the victim (believing that a motivated unemployed person could find a job at any time).

Unfortunately, many unemployed U.S. workers are blocked from accessing any of these unemployment benefits due to a stigmatized Unemployment Insurance system that attempts to screen the worthy from the unworthy and is now failing these workers in their moment of crisis. Barriers to accessing unemployment, including confusing eligibility criteria, lack of awareness, and antiquated information technology systems are characteristics of a stigmatized benefits system. Meanwhile, many unemployed workers are waiting weeks to receive benefits for which they were eligible, and many never received any at all.35

The ineffective administration of unemployment benefits also likely is hampering an economic recovery because jobless workers are unable to spend at a critical moment when spending would speed a recovery. Expanding benefits by resuming the $600 weekly supplemental payment and extending benefits for as long as necessary would help. Reforms to the Unemployment Insurance system to hasten the return to full employment could include:

Increasing the federal taxable wage base and indexing it to inflation to ensure adequate funding

Designing automatic benefits extensions so that the program can respond quickly to rapid downturns, such as the current recession

Implementing a minimum benefit level that would incentivize eligible workers to apply to the program36

To counteract unemployment stigma, counteract unemployment

The best step to prevent the harm of unemployment is to prevent people from becoming unemployed. One way to do so is through direct government hiring and incentives for firms to keep people employed and hire the unemployed. Direct payroll subsidies, as in the Paycheck Protection Program, saved jobs but were too short-lived and not generous enough.

Employers in states with work-sharing programs could reduce hours without laying off workers or reducing incomes if these short-time compensation programs run through state Unemployment Insurance systems had wider participation. But short-time compensation is not adopted by enough states and has not been well-targeted toward low-wage workers in particular, despite benefits associated with maintaining a workforce during downturns. In addition, any federal aid for municipalities and states could prioritize maintaining employment levels to prevent further rounds of mass layoffs.

In future stimulus proposals, direct payroll subsidies or job creation tax credits for hiring long-term unemployed workers could be considered as well.37 Such programs would offer incentives to firms that hire unemployed workers, essentially by offering wage subsidies.

By preventing workers from becoming unemployed and hastening the return of the unemployed to work, the above policies can shorten the time to economic recovery. Such actions can also be far cheaper in the long run than having the unemployed remain idle and can prevent the damaging consequences of unemployment stigma.

— Peter Norlander is an assistant professor of management at Loyola University Chicago.

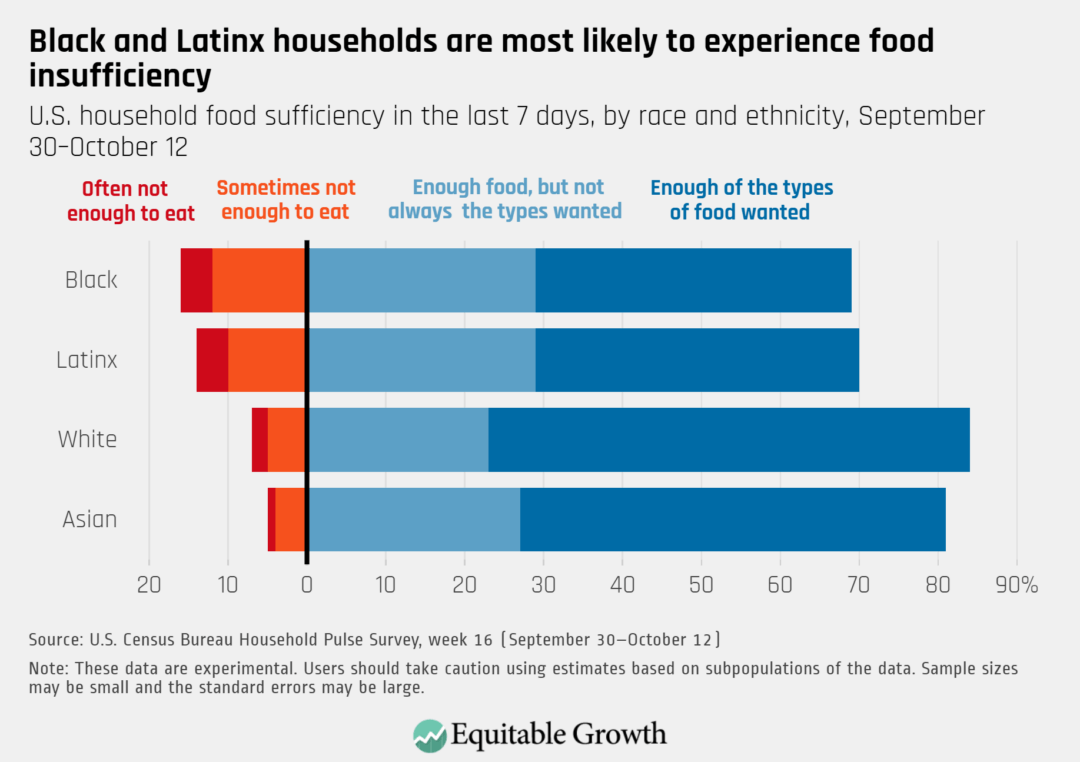

On October 21, the U.S. Census Bureau released new data on the effects of the coronavirus pandemic on workers and households. Below are five graphs compiled by Equitable Growth staff highlighting important trends in the data.

Food insecurity varies significantly by race and ethnicity. Fourteen percent of Latinx households and 16 percent of Black households report not having had enough food to eat in the prior week, compared to 7 percent of White households and 5 percent of Asian households.

As higher education plans are changed or delayed, those who are delaying education will have fewer options in the U.S. labor market now given high unemployment as well as less opportunity in the future based on credentialism.

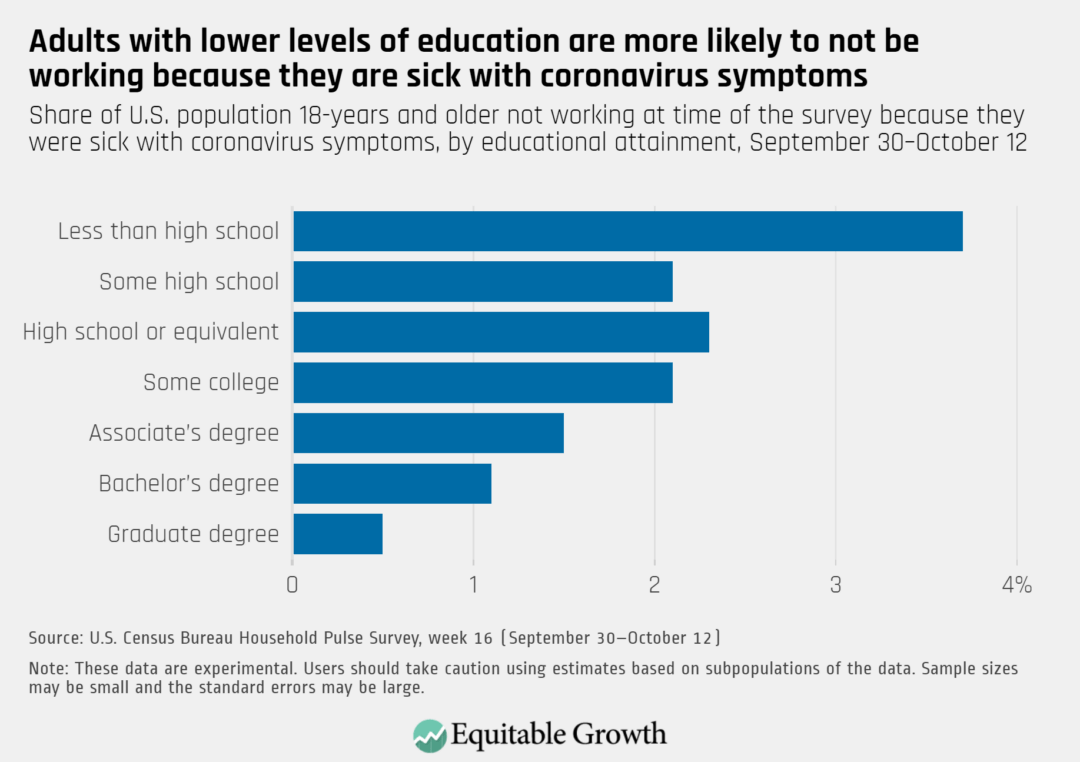

The spread of the coronavirus has impacted the employment of workers with less than a college degree, more of whom report they are not working due to being sick with coronavirus symptoms compared to those with an associate’s degree or greater.

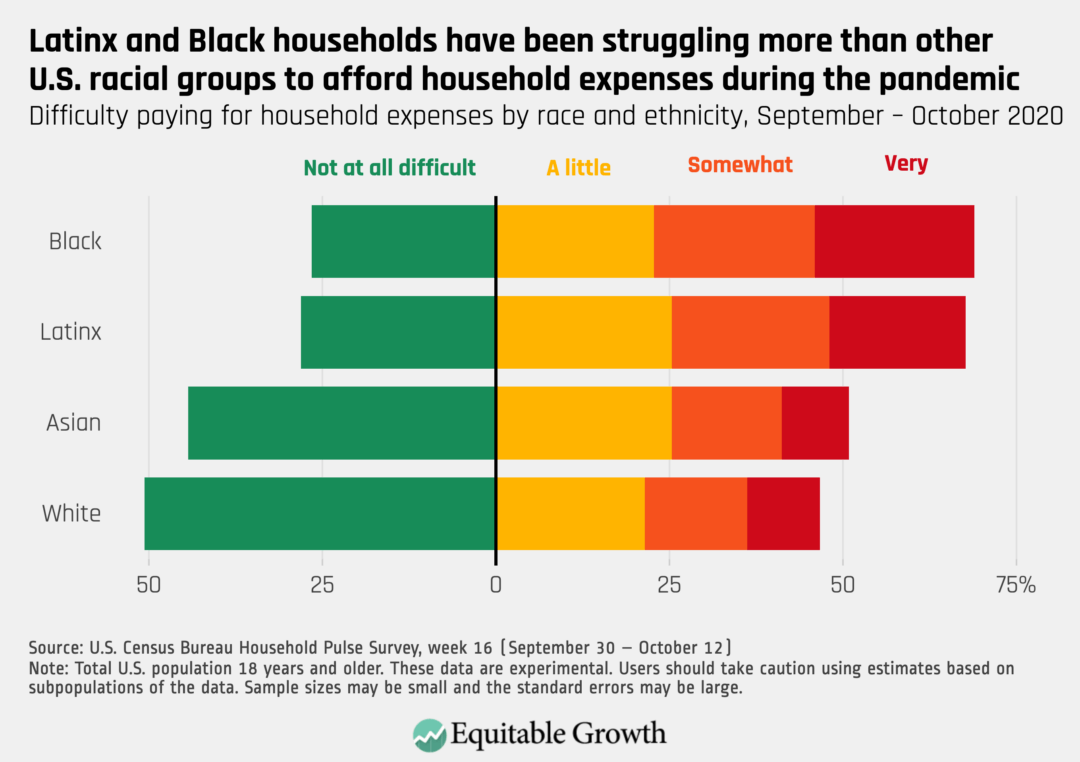

More than half of all households reported having difficulty affording household expenses over the past month, with more than two-thirds of Latinx and Black households reported having difficulty with expenses.

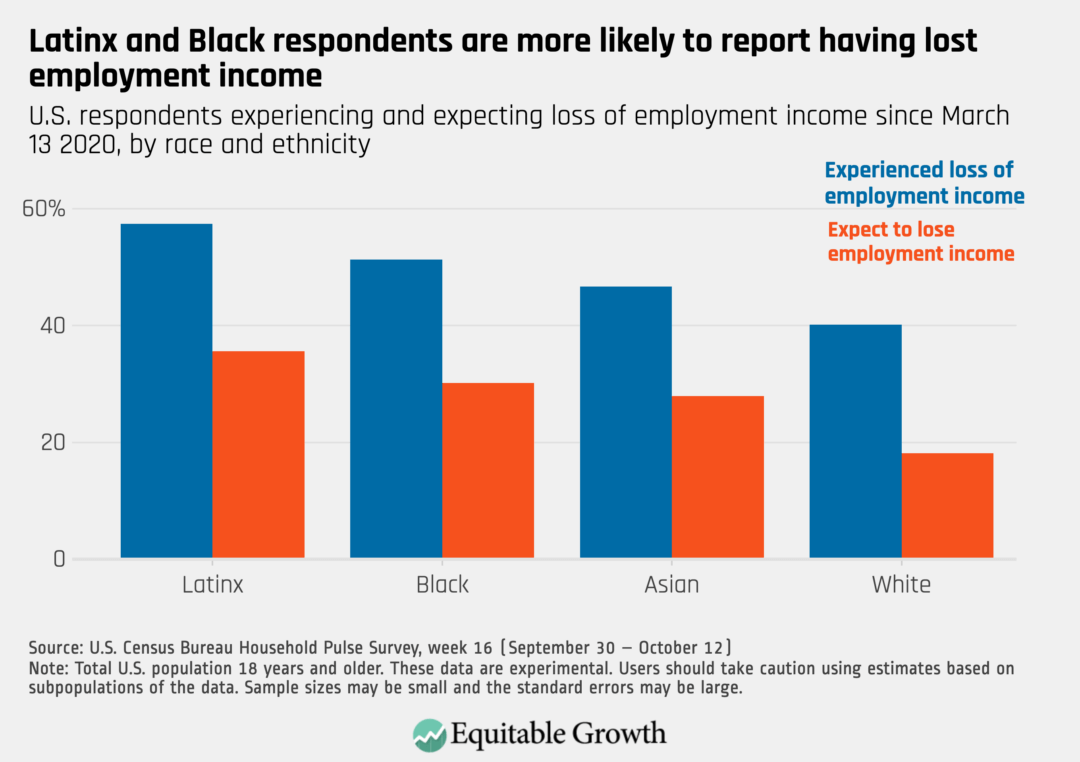

More than half of Latinx and Black respondents report experiencing losses to their employment incomes since the start of the coronavirus recession, with more than one-fifth of all respondents saying they expect to lose income over the next four weeks.

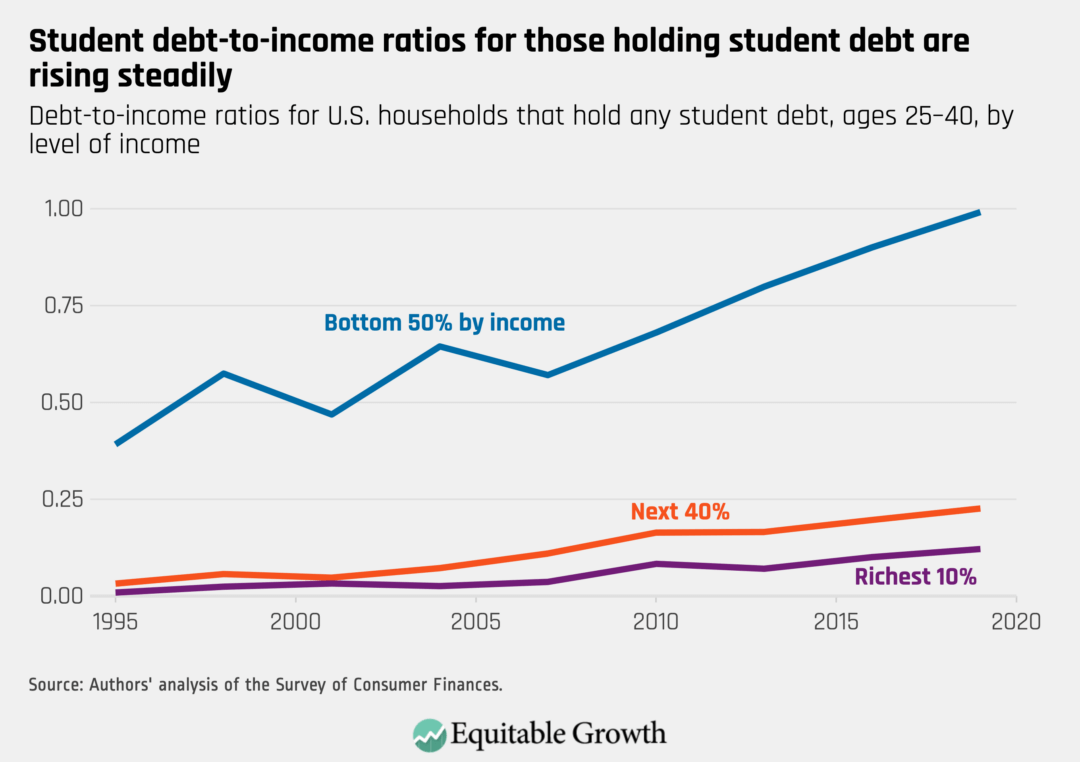

Today, about 43 million adults in the United States collectively hold $1.5 trillion in federal student loan debt and an additional $119 billion in private student loans not backed by the federal government. Student loan debt is an issue for many U.S. households, but it is becoming an especially acute problem for heads of households who are low-income, Black, or Hispanic. The Federal Reserve’s 2019 Survey of Consumer Finances shows that student debt-to-income ratios are rising, saddling millions of U.S. households with a persistent drag on their incomes that could last 20 years.

The new data show that student debt-to-income ratios crept up over the past two decades and now average 0.56 among adults who have any student debt. In this issue brief, we report mean (average) income divided by mean (average) debt to reduce the influence of large outliers and look at people between the ages of 25 and 40 to roughly capture the generation that has been most affected by climbing college costs while excluding those who are just starting out their careers and therefore have especially low incomes. Excluding older households also addresses, in part, known weaknesses of using SCF data to analyze student debt. Although we think this age restriction is a reasonable frame for analyzing the data, removing it or using different age brackets does not substantially change the results we give here.

Our analysis demonstrates that the student debt burden in the United States falls most heavily on those U.S. households in the bottom 50 percent of the income distribution—and even more on Black American households. Measures to alleviate these student debt burdens—via income-based repayment plans and one-time forbearance policies enacted by Congress amid the coronavirus recession—mitigate these burdens only on the margins. We detail these findings from the new 2019 Survey of Consumer Finances and conclude with some analysis of student debt forgiveness programs based in these data.

Student debt burdens are on the rise

Disaggregating households by their income, the data show that adults in the bottom 50 percent of the income distribution with any debt have an average debt-to-income ratio of 1.03—more than double the ratio of 0.5 that same group held in 2001. Debt ratios are also rising for those in the next 40 percent of individuals by income, indicating that student debt is a problem of growing significance for a broad swathe of working- and middle-class households. Notably, these trends are for households that hold student debt and have therefore attended some college, so the trend is not being driven by increased college attendance. (See Figure 1.)

Figure 1

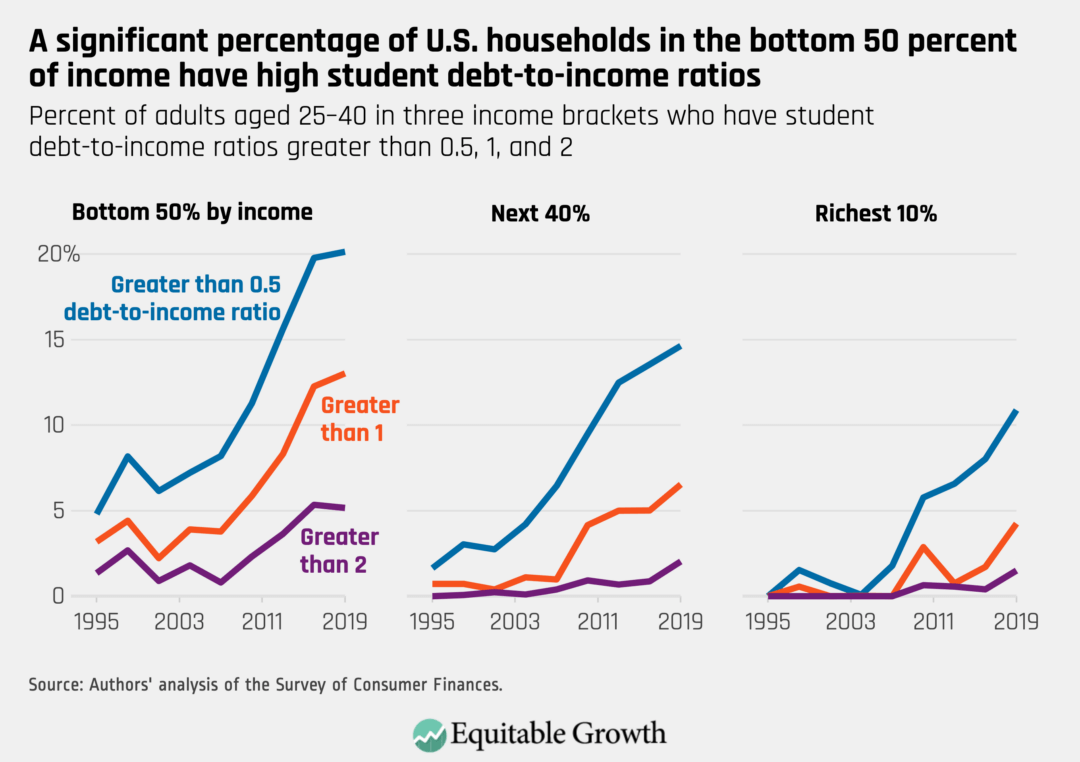

Heightened levels of student debt are often downplayed. Analysts point out that many of the largest balances are accrued by doctors and lawyers who will find high-paying jobs and have no trouble paying down their debt. But there are a large number of workers with relatively low balances on the student debt they owe who are nonetheless struggling to pay because they are stuck in low-income jobs. In fact, about 500,000 U.S. households with heads between the ages of 25 and 40 in the bottom 50 percent of the income distribution have a debt ratio greater than 1, and 2.5 million have a debt-to-income ratio greater than 0.5. Twenty percent of all households in this age group in the bottom half of the income distribution have a debt-to-income ratio of 0.5 or greater, not just those who have any student debt. (See Figure 2.)

Figure 2

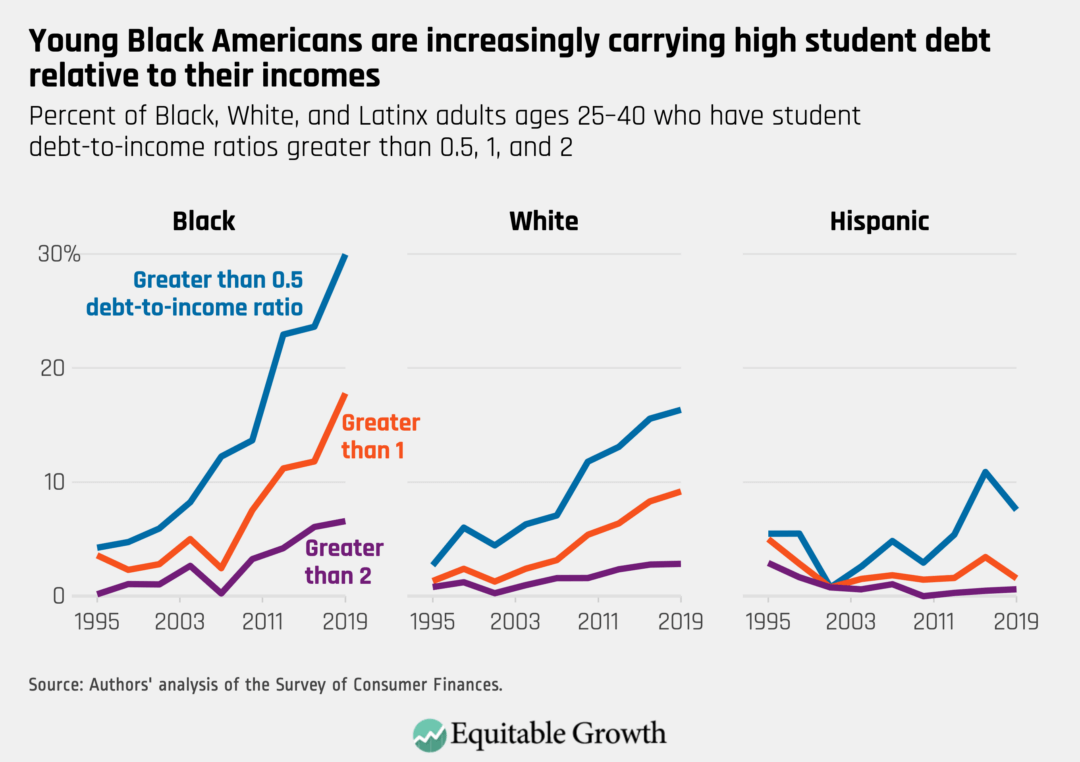

Black borrowers are struggling most

Because the U.S. labor market continues to discriminate against Black Americans, the result is Black student debtholders are likely to have lower-paying jobs than their White peers. Black student loan borrowers also have less family wealth to draw on to pay for college, leaving them with higher debt balances too. The result is that nearly 30 percent of Black Americans between the ages of 25 and 40 have a student debt-to-income ratio exceeding 0.5. Latinx student loan borrowers are less likely to have high debt, although this is in part because they are less likely to have attended college than other groups. (See Figure 3.)

Figure 3

A contributing factor to these trends is that more Black Americans are now attending college. But if we confine our analysis to only those who have attended at least some college, the results are very much the same. In 2001, about 5.5 percent of Black Americans who attended at least some college had a debt-to-income ratio greater than 1. In 2019, it was a whopping 24 percent.

Other data points echo our findings here. Analysis by the Institute for College Access and Success based on voluntary reporting by colleges found that Black recent graduates have the highest difficulty (about 40 percent of Black respondents) making federal student loan payments 12 months after graduation. Racial wealth divides between Black and White households mean that Black college graduates may not have a secure financial safety net in the event of financial crises, such as the one our nation is experiencing currently.

Institutional racism and discriminatory financial practices up until the 1970s suppressed the growth of household wealth among non-White families, with long-lasting implications for today’s non-White millennial and zoomer students. Today, without the same financial cushion of generational wealth that is available to average White households, college graduates in Black and Latinx households may run the risk of defaulting on their student debt when the U.S. economy faces shocks, such as amid the current coronavirus recession and future economic downturns.

Policy implications

U.S. policymakers should be concerned by these trends. Income-based repayment plans enable some of these student loan borrowers to manage the repayment burden month to month. And many of these borrowers will be able to get forbearance from the U.S. Department of Education so they can pay $0 during periods where they are unemployed or have suffered serious declines in income. But even modest payment amounts (income-driven repayment plans cap out at 10 percent of discretionary income) are a drag on the ability of these individuals to buy houses, start families, become entrepreneurs, and engage in other activities that previous generations took for granted.

This drag, no matter how modest, was not faced by previous generations of college graduates and their families. Student debt will continue to weigh on the balance sheets of these households for 20 years in most cases. And although the overall ratio of debt payment-to-income has not increased in the way the ratio of debt balances-to-income have, this reflects, in part, the fact that debt has actually become more burdensome, and many students are in forbearance or are more likely to use income-based repayment than in the past.

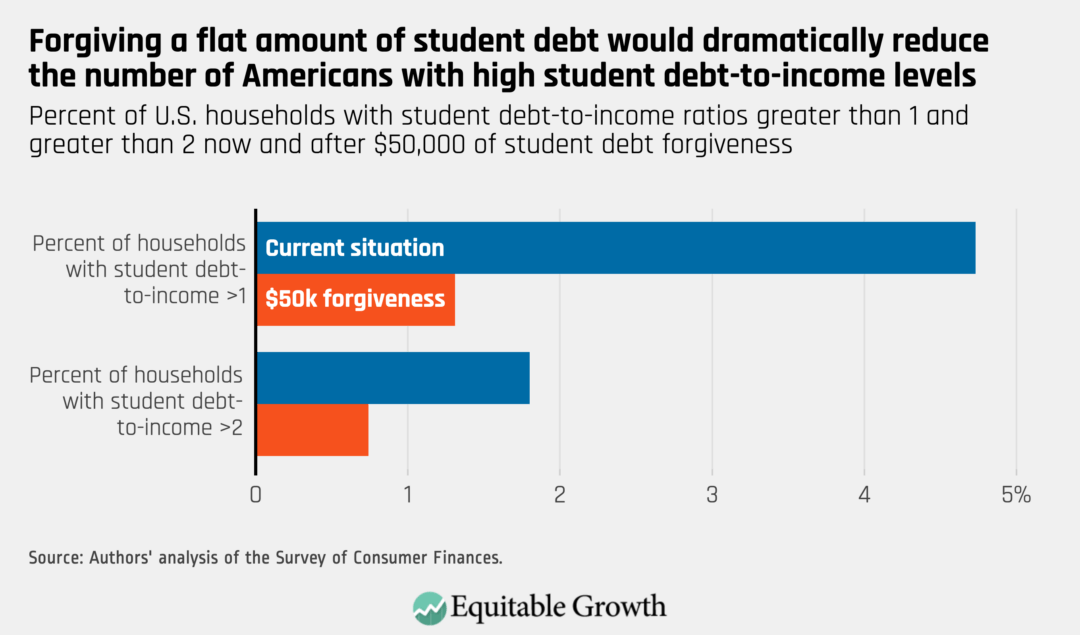

One-time student debt forgiveness, proposed by both policymakers and academics, is one way to reverse the trends discussed above. As economist Darrick Hamilton at The New School and social scientist Naomi Zewde at the City University of New York’s Hunter College argued earlier this year, full forgiveness of all existing student debt would significantly reduce the Black-White wealth gap, because Black households face higher balances and are far more likely to struggle to pay those balances back. It also has the significant advantage of being relatively simple to carry out, at least relative to proposals that include complicated eligibility requirements. These kinds of requirements have been problematic in the past. The Public Service Loan Forgiveness program, for example, approved only 3,400 out of 200,000 applicants for forgiveness in 2017, because the requirements proved complicated, and borrowers did not fully understand the program.

Other proposals have focused on forgiving a flat, across-the-board sum. Sen. Elizabeth Warren (D-MA), in her 2020 presidential campaign, for example, proposed eliminating $50,000 of debt. This would dramatically reduce the number of households with high student debt-to-income ratios. (See Figure 4.)

Figure 4

One-time debt forgiveness of any sort, however, is not a sufficient solution to the broader problem of increasing college costs. To prevent a recurrence of the creeping debt situation happening now, a college education needs to be made affordable for lower- and middle-class households. As demand for college has risen, per-student funding provided by states to public universities has fallen. Whereas tuition once accounted for just a bit more than 20 percent of revenue at public institutions, in 2017, it accounted for almost half of all revenue. Cuts in state budgets as a result of the Great Recession also exacerbated the issue, with some states still funding far less than they did before the crisis. States likely do not have the ability to reverse this trend themselves. To make college affordable, the federal government will have to step in and jointly fund public institutions with states.

As of fiscal year 2017, ending in September 2017, only 2 percent of the federal budget was allocated toward higher education. Since 2007, there has been no growth in federal and state education expenditures. In order to curb rising student loan debt, policymakers at both the state and federal level should invest in affordable and accessible higher education, especially 2- and 4-year programs. Prioritizing need-based student financial aid over merit-based aid benefits students who grow up in communities with poorly funded public Kindergarten through 12th grade education, allowing these students to experience economic mobility without the heavy burden of student loan debt after graduation. The Debt-Free College Act is an example of one bill that would implement some of these recommendations.

Much of the analysis of student loan debt fails to acknowledge that even when the burden of student loans is modest, it is a drag on income that previous generations did not face. The creeping increase in student debt-to-income ratios is evidence that the problem should be tackled now, before the student financial aid system becomes more dysfunctional. Federal support would ensure that no one is unable to get a college education due to their parents’ financial circumstances, and that the nation continues to build a well-educated workforce.

Under U.S. law, corporate boards of directors represent the interests of companies’ shareholders. This is reflected in the typical composition of boards, composed almost entirely of people from the business world, with some from the nonprofit sector and other elements of the private sector mixed in. Because boards of directors oversee the management of companies, they have fiduciary responsibilities to look at corporate strategy, hiring, and other decision-making through the lens of how these corporate activities affect the interests of the corporation, which, in recent decades, generally means the shareholders.

One group that boards do not look out for are the workers whose labor creates value for companies. Workers matter to boards only as they affect shareholder interests. That is not to say that boards don’t care at all about the health, safety, and well-being of workers. For one thing, they are obliged to follow the state and federal laws affecting workers. But generally, their interest in workers—how many there are, what they are paid, how they are treated—is confined to how such decisions affect shareholder interests, such as stock prices and fulfilling firms’ legal responsibility for workplace protections and rights.

It does not have to be this way. Building an economy with broadly shared growth can include corporate policy that considers a broader range of interests, including the voices of the workers, who make companies operate day-to-day, in decisions about both short- and long-term priorities. It’s possible that federal law can be changed, as it has been in more than a dozen European countries, to require corporate boards to represent the interests of workers, as well as shareholders.

How would this affect companies and workers? New research on Germany, funded by the Washington Center for Equitable Growth, by grantees Simon Jäger of the Massachusetts Institute of Technology and Benjamin Schoefer of the University of California, Berkeley, along with Jörg Heining of the German Institute for Employment Research, seeks to answer these questions. The co-authors examine how changes to so-called co-determination laws (corporate governance speak for worker participation at the board level) affected employment and earnings. Despite predictions by business interests that giving workers more voice may run contrary to sustainable corporate strategy, the three researchers find that companies with co-determination perform well, do not have any significant changes to wage levels, and are less likely to outsource business functions.

Policies such as co-determination are increasingly relevant to the United States, where wages have remained essentially stagnant for decades, despite a long-term increase in productivity, which suggests that workers are creating value but are not reaping any of its benefits. As the U.S. labor market becomes increasingly fissured, with rising domestic outsourcing over time, workers find fewer opportunities for advancement, and declining unionization rates decrease workers’ voices. Furthermore, wage stagnation was largely resistant to more than a decade of economic recovery and a historic drop in unemployment until the recent coronavirus recession.

As U.S. policymakers consider how to address this problem, serious thought is being given to how corporate structures might be changed to take workers’ interests into greater account—on the assumption that this could help workers get a larger share of the corporate pie. Clean Slate for Worker Power, a project of Harvard Law School’s Labor and Worklife Program, is advancing an agenda of U.S. labor law reforms designed to restore worker power, including requiring worker representation on corporate boards. And legislationis before Congress to establish such a requirement.

To help policymakers understand these proposals, it would be helpful to know what effect such reforms might have on wages and employment, as well as investment and capital stock, corporate profits, and the long-term success of individual businesses. Research by Jäger, Schoefer, and Heining begins to answer these questions.

It might be difficult for people in our nation to think of corporate boards representing anybody but shareholders since this is part of American corporate culture and precedent going back to the 1970s. In fact, boards are very different in some countries. A case in point is Germany, where, for nearly 70 years, the law required workers to be represented on some corporate boards. While that mandate existed in some form going back to 1951, it was abruptly abolished in 1994 for new firms. But the mandate remained, and remains, for firms that existed before that date.

This sudden change in German law created a so-called quasi-experiment that allowed Jäger, Schoefer, and Heining to examine how labor representation in corporate governance affects workers and companies. Operating side-by-side in Germany are companies still under the mandate and companies free of it. This raises numerous questions. How do they compare? Does having workers on the board result in higher wages? Lower capital stock? Reduced profits? More bankruptcies? That is what conventional economic theory might suggest. The researchers’ working paper, “Labor in the Boardroom,” examines these questions, with some very interesting conclusions.

First, some background. Like many other European countries, Germany has a two-tier board system, a supervisory board and an executive board. The executive board is equivalent to the senior management of a U.S. company, with day-to-day operational responsibilities. The supervisory board operates much like U.S. boards of directors, with responsibility for the selection, monitoring, auditing, compensation structuring, and dismissal of the executive board. It is involved in strategic planning, large financial decisions, and other fundamental decisions about the company.

Between 1951 and 1976, Germany passed a series of laws that mandated supervisory boards of companies—other than privately held firms or limited liability corporations—be made up of varying levels of workers’ representatives, depending on the size and type of company. By 1976, the largest corporations and smaller companies in the mining, coal, and steel industries were required to have workers’ representatives comprising one-half of their supervisory board membership. Other companies had one-third worker representation. Workers elected their own representatives, who were always workers, except in the largest companies, where workers were permitted to elect outsiders to supplement workers.

In the United States, one might expect co-determinant boards to be contentious, but in practice, in Germany, when worker and shareholder representatives hold equal or near-equal power, they tend to operate by consensus. One reason might be the existence of works councils, which have extensive consultation, information, and co-determination rights in areas such as work hours, safety, and organizational or staffing changes, and can directly negotiate with the employer. Works councils do not exist in the United States, but they have a purview similar to that of labor unions in the United States, except that they participate in setting principles of wage setting rather than engaging in direct negotiations over wage levels, as U.S. unions do.

Only roughly 9 percent of workplaces in Germany have works councils, but they are overrepresented at larger workplaces. This means they cover 42 percent of employees in the former West Germany and 35 percent in the former East Germany. In part as a result of these structural differences, with works councils present at many larger businesses, there tends to be, in general, greater cooperation between labor and management in Germany.

In 1994, all this changed abruptly. The German federal parliament, the Bundestag, passed legislation exempting all new corporations from the worker representation mandate while maintaining it for existing companies. The rationale for treating old and new companies differently was that existing companies had already become accustomed to shared governance. Researchers Jäger, Schoefer, and Heining, however, say this was a legislative compromise between those who wanted to retain the status quo and those who wanted to abolish the mandate entirely. (The new law made no changes in works councils.)

To understand the effect of this change and to estimate the impact of co-determination on company and worker outcomes, Jäger, Schoefer, and Heining measured a number of metrics for companies incorporated 2 years before and 2 years following the change in law. This creates a sample of companies created under more or less similar economic conditions and average productivity levels, but incorporated under different legal frameworks. Thus, all the firms were incorporated between August 10, 1992 and August 10, 1996. Those incorporated before August 10, 1994 were subject to the mandate; those incorporated after that date were not.

To ensure the robustness of their findings, the researchers tested a number of factors to ensure that nothing about that particular time period distorted the results. So, they also compared these firms with publicly held companies that were subject to the mandate and then released from it in 1994, and with limited liability corporations, which were never subject to the mandate. This helped to ensure that any changes post-1994 were not due to overall changes in the economy or other outside factors affecting business more generally. Jäger, Schoefer, and Heining did additional testing of other potential factors as well to ensure that changes were likely due to the boardroom legislation and not other issues.

It’s also important to note that the legislative compromise was unanticipated, and that it was implemented literally the day after it was both announced and enacted. So, there was no gap in incorporations just prior to the change in the law, which might have suggested deliberate avoidance of the mandate. And there was no rush to incorporate immediately following it, which might have suggested the same.

Generally, Jäger, Schoefer, and Heining found no significant impact on overall wages or employment. In fact, they found a slight increase in capital assets and significant upward movement in capital share, not labor share, due primarily to an increase in worker productivity. In other words, under shared governance, the same number of workers being paid essentially the same amount produce more value per worker, and that value is accruing to capital, not labor.

There does appear to be a significant reduction in outsourcing as a result of co-determination. Outsourcing is credited with decreasing average labor standards and worker outcomes across an economy. But for firms and their shareholders, the bottom line is that there is a slight increase in capital assets, and neither revenues nor profits appear to be significantly affected.

This also suggests that giving workers a voice in corporate decision-making does not lead to deleterious outcomes, such as bankruptcy, due to workers’ potential differing priorities. Important, too, is that corporate policy doesn’t affect only shareholders’ bottom lines. Companies also employ the workers and provide goods and services to the consumers who are both the bedrock of our economy.

Research like this can only speculate as to the reasons for these results and how they might differ if shared governance on corporate boards were adopted in the United States. Shared governance has existed in Germany for nearly seven decades, so the management and workers of firms that remained under the pre-1994 mandate had essentially known nothing different. Results could be different if new corporate governance rules were enacted for U.S. companies unused to shared governance.

More research could give policymakers, workers, and corporate leaders alike a stronger basis for projecting possible outcomes. But this new research by Jäger, Schoefer, and Heining does suggest that workers being given a greater voice in the workplace does not lead to the negative economic outcomes purported by anti-labor critics, such as unsustainable levels of pay or workers embracing luddite-like resistance to technological change.

Their findings also might reflect the more cooperative labor relations that are prevalent in Germany, although it may be that those cooperative relations are partly a result of shared governance. The consensus nature of supervisory boards in Germany suggests that shared governance—over the long run—can produce good results for workers, companies, and the economy. Here in the United States, researchers could look at the experiences of worker-owned companies or companies with significant employee stock ownership plans (so workers are essentially shareholders) to see whether parallels with the German experience are germane.

1. Unless we know where we are, we will be unable to figure out where we need to go. And we do not know where we are. Thus one of our very top priorities should be oversampling minorities to help us figure out exactly how far away we are from equal opportunity. Read Austin Clemens and Michael Garvey, “Structural racism and the coronavirus recession highlight why more andbetter U.S. data need to be widely disaggregated by race and ethnicity,” in which they write: “This issue brief details the steps Congress and executive branch agencies can take to improve our understanding of economic and social outcomes for all communities of color. There are many ways the economic statistical agencies could improve data collection, provide more analysis of racial economic divides, and alter the presentation and publication of statistics to better inform policymakers on the needs of marginalized communities. This issue brief focuses on three concrete policy actions that could be taken now with a focus on oversampling in existing federal surveys.”

2. A guide to five excellent scholars who should definitely be on your reading list. Read Christian Edlagan, Aixa Alemán-Díaz, and Maria Monroe, “Expert Focus: The consequences of economic inequality among Latinx groups in the United States,” in which they write about: “Carlos Fernando Avenancio-León … on how political empowerment through protecting the right to vote had a positive impact on U.S. labor market inequality … Eduardo Bonilla-Silva … on how economics can better adopt a racial equity lens by drawing from outside the discipline … Adriana Kugler… on the benefits of UI extensions to improve the quality of job matches for women, non-White workers, and less-educated … Juliana Londoño-Vélez… on the feasibility of wealth taxation in developing countries … Marie Mora … on the lack of access to capital Latinx groups face.”

3. This is a great paper—and I find the identification completely convincing. It is very hard to argue that enforcement of the Voting Rights Act of 1965 was stronger in places where other factors were already rapidly closing the Black-White wage differential. Yet it was in places where the Voting Rights Act of 1965 was most strongly enforced that saw the greatest relative wage gains for American Blacks. Read Abhay Aneja and Carlos Fernando Avenancio-León, “Voting rights equal economic progress: The Voting Rights Act and U.S. economic inequality,” in which they write: “The Voting Rights Act of 1965, a signature measure of the civil rights era, narrowed the wage gap between Black and White men in the areas where it was most strictly enforced. Specifically, between 1950 and 1980, the gap between the median wages of Black and White workers in the South narrowed by approximately 30 percentage points. And our study, which builds on existing research on the economic benefits of voting rights legislation, shows that the Voting Rights Act was responsible for about one-fifth of that reduction.”

Worthy reads not from Equitable Growth:

1. Once again, the shadow left by Harry Dexter White’s victory at Bretton Woods over John Maynard Keynes, and the consequent insistence that the burden of adjustment lie in such a way as to force deflation, damages us. What the International Monetary Fund should be saying is, echoing Keynes: “What we can do, we can afford.” As long as interest rates remain this low, governments should spend whatever is necessary to employ their people. And if interest rates start rising rapidly? Governments then need to constrain that rise by incentivizing people to hold safe assets so that 2008 does not come again, and so limit the rise in interest rates: Read the IMF’s “Fiscal Monitor: Policies for the Recovery,” in which the international financial institution writes: “Governments’ measures to cushion the blow from the pandemic total a staggering $12 trillion globally. These lifelines and the worldwide recession have pushed global public debt to an all-time high. But governments should not withdraw lifelines too rapidly. Government support should shift gradually from protecting old jobs to getting people back to work and helping viable but still-vulnerable firms safely reopen. The fiscal measures for the recovery are an opportunity to make the economy more inclusive and greener.”

2. The 2007–2008 financial crisis, the Great Recession of 2007–2009, and the subsequent botched economic recovery in the global north was a large element in the global north’s relative decline—it stood still, economically and socially, for half a decade while East Asia grew. Now it is starting to look as though the coronavirus pandemic and subsequent recession will be a similar lost half decade, or more—but this time for pretty much everyone outside of East Asia with its successful (so far) virus-control policies. Read the Financial Times Editorial Board, “the global economic recovery is dramatically uneven,” in which they write: “The IMF said in its World Economic Outlook, which was released on Tuesday, that the global economy will shrink by 4.4 per cent this year—an awful figure … [with] prospects of recovery … are far from even … China, buoyed by strong export sales and a reduction in caseloads that has enabled an economic reopening, is set to grow by 1.9 per cent this year … The US and European economies, meanwhile, are still set to experience sharp contractions as a result of not being able to fully remove restrictions on movement …The US, where the Federal Reserve and the Treasury acted swiftly to shore up financial and labour markets, will perform much better than Europe. Its economy is seen as shrinking by 4.3 per cent, compared with a deeper contraction of 8.3 per cent in the eurozone. The UK economy, meanwhile, is forecast to shrink by 9.8 per cent … Divergences within the major emerging markets are stark, too … India … is expected to see its economy shrink by 10.3 per cent over the course of 2020. In Latin America, the outlook for Mexico remains bleak … Recovery will depend largely on countries’ ability to contain the virus … If the disease lingers and becomes more difficult to contain, the IMF rightly advises countries to spend whatever it takes … The focus for now must be on mitigating the impact of Covid-19 … The IMF’s forecasts suggest the best means … lie in mitigating the spread of the disease through successful track-and-trace policies that will enable economies to reopen more quickly, too. The virus first became widespread in China; the lead set by it and other east Asian countries in controlling it offers the best way out for the global economy.”

3. Looking back at economic history and then the policy mistakes that led to the Great Depression, Doug Irwin calculates that half of the damage from deflation was a result of the misguided policies of the French government. Has orthodoxy, austerity, and deflation ever worked. Read Douglas Irwin, “Did France Cause the Great Depression?,” in which he writes: “A large body of research has linked the gold standard to the severity of the Great Depression. This column argues that while economic historians have focused on the role of tightened U.S. monetary policy, not enough attention has been given to the role of France, whose share of world gold reserves soared from 7 percent in 1926 to 27 percent in 1932. It suggests that France’s policies directly account for about half of the 30 percent deflation experienced in 1930 and 1931.”