This is a post we publish each Friday with links to articles that touch on economic inequality and growth. The first section is a round-up of what Equitable Growth published this week and the second is relevant and interesting articles we’re highlighting from elsewhere. We won’t be the first to share these articles, but we hope by taking a look back at the whole week, we can put them in context.

Equitable Growth round-up

The extreme inequality that defines the U.S. economy rendered the country more susceptible to the coronavirus recession. The incoming Biden-Harris administration will have a lot of work to do to get the economy and society on the path to recovery and ensure all Americans prosper when the economy grows. To do so, the new administration and the next Congress will need to address rampant racial and economic inequality. Corey Husak and David Mitchell compiled the best ideas from Equitable Growth’s Vision 2020 initiative and beyond to guide the new administration and incoming Congress in how to do just that. Husak and Mitchell direct readers to specific key policy categories, such as building worker power, providing universal paid family and medical leave, shoring up the Unemployment Insurance system, and addressing racial economic divides, among others. They explain how each of these proposals would work to address racial and economic inequality, implement the major structural changes needed, and ensure strong, stable, and broad-based economic growth for all Americans.

In mid-October, a group of scholars and advocates joined a webinar hosted by the Groundwork Collaborative (co-hosted by several organizations, including Equitable Growth) to discuss past policies that made the United States vulnerable to the worst impacts of the coronavirus, as well as ideas for how to promote a robust recovery from this and future downturns. The webinar, titled “EconCon presents: Building an economy that works for us all,” featured Sen. Elizabeth Warren (D-MA), Fair Fight Action Founder Stacey Abrams, and sociologist Tressie McMillan Cottom from the University of North Carolina at Chapel Hill, among others. Equitable Growth’s Shanteal Lake provides an overview of the event, which centered on the role of racial disparities and worker power in both the depth of the coronavirus public health and economic crises and the path forward for widespread economic growth.

Late last week, the U.S. Bureau of Labor Statistics released labor market data for the month of October, which showed unemployment rates declining, albeit at a slower pace than in previous months. Kate Bahn and Carmen Sanchez Cumming compiled five graphs to showcase the most important takeaways from the data and how the U.S. workforce is affected by the coronavirus. Namely, they note that the coronavirus recession is disproportionately harming less-educated workers and non-White workers—trends that must be addressed by the incoming administration as it works to ensure a broad economic recovery.

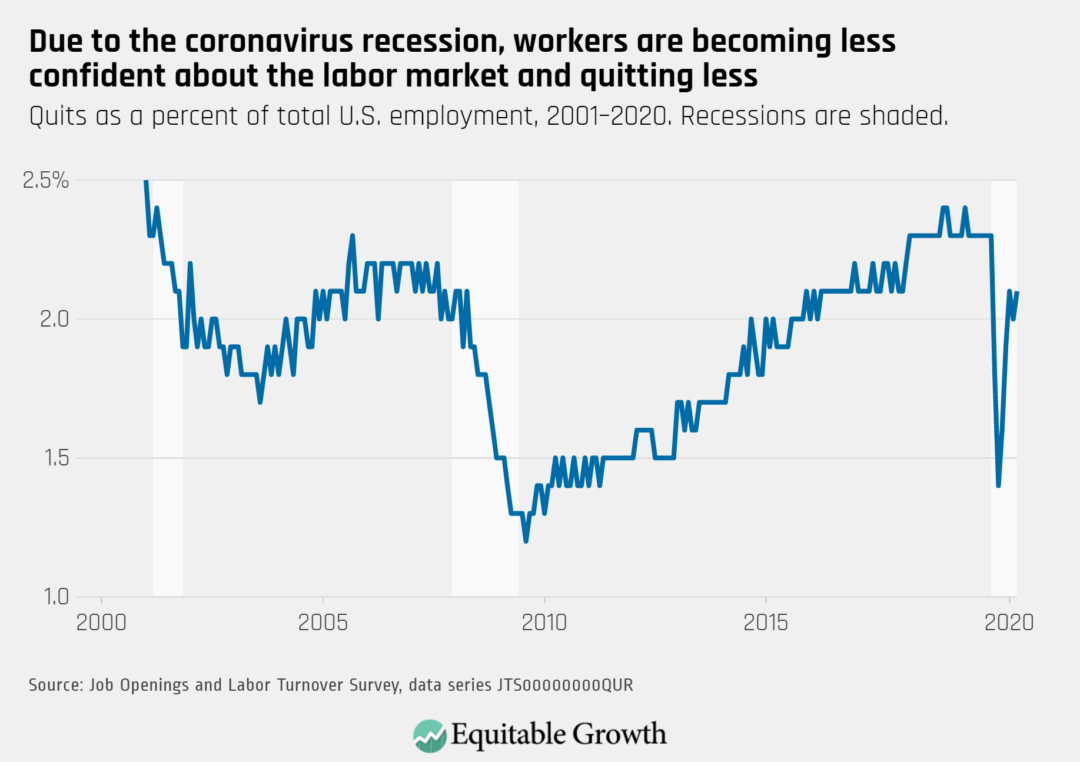

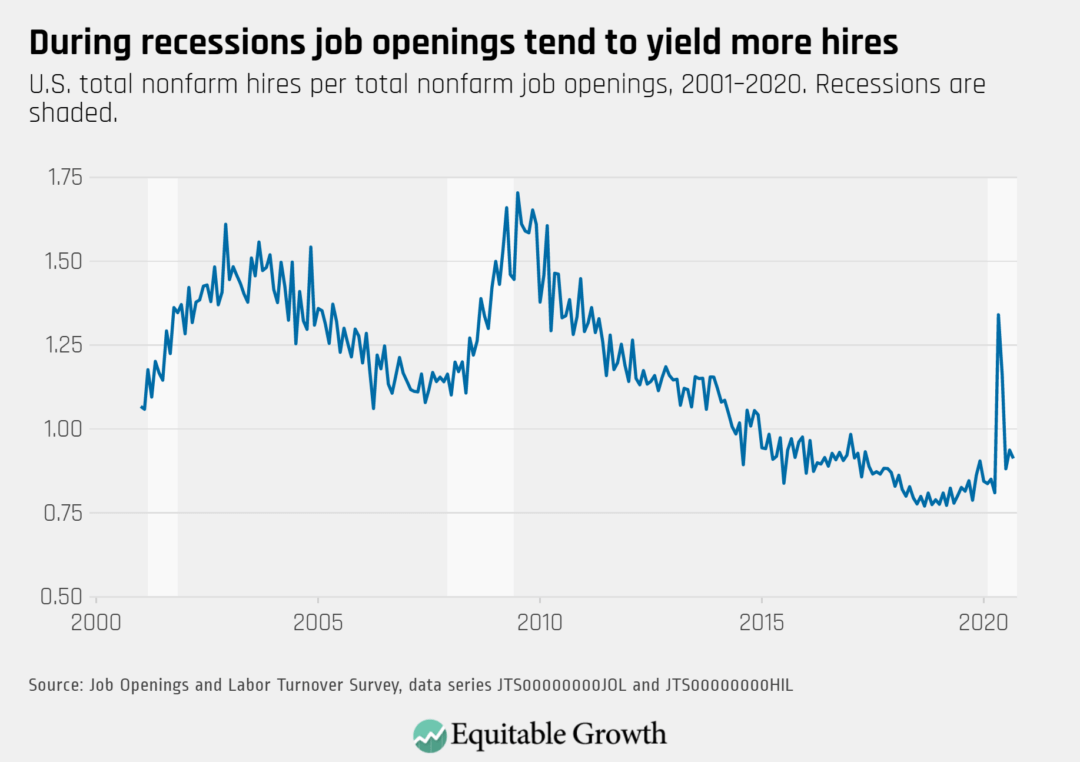

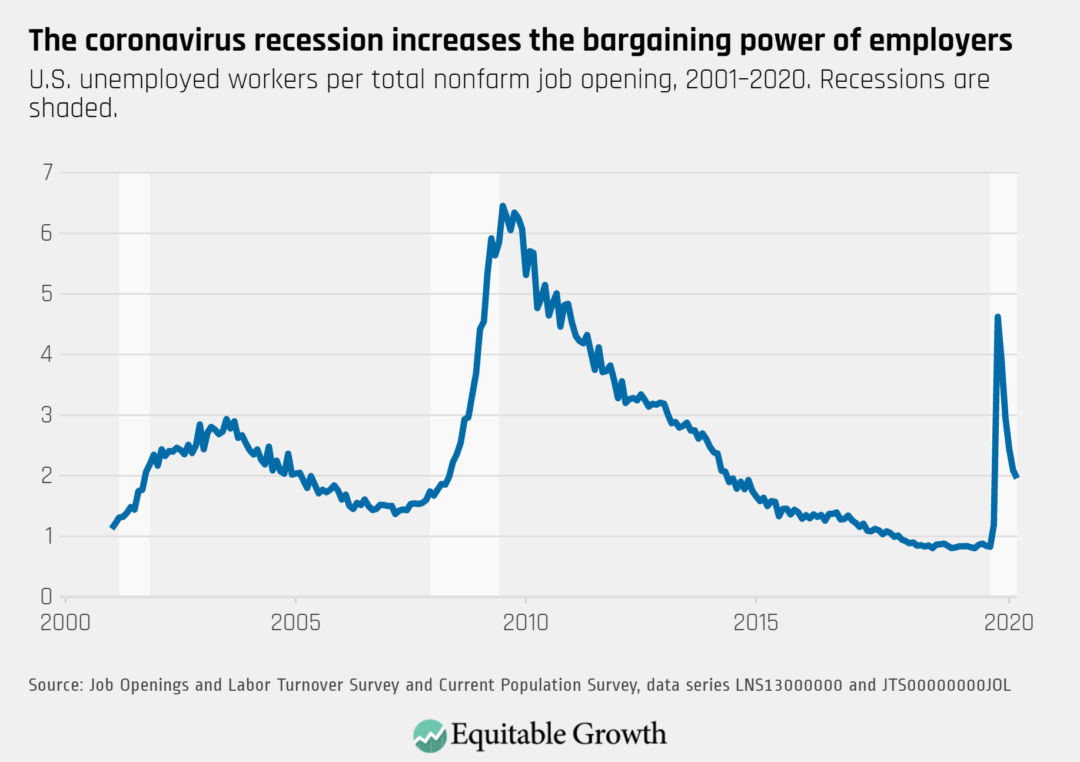

The U.S. Bureau of Labor Statistics also releases data every month on hiring, firing, and other U,S, labor market flows from the Job Openings and Labor Turnover Survey, or JOLTS. Earlier this week, the agency released the latest data for September 2020. Bahn and Sanchez Cumming put together four graphics highlighting key points in the data, including a slight uptick in the quits rate, which indicates that job prospects have stalled for many workers amid the coronavirus recession.

It is long past time to abandon the false dichotomy between saving the U.S. economy or protecting people’s health during the coronavirus pandemic. The Atlantic’s Annie Lowrey explains just how misguided this belief is by showing how the decision to prioritize the economy over workers’ health led to worse economic outcomes by sickening and debilitating our workforce. The millions of U.S. cases of the coronavirus and nearly 250,000 deaths from COVID-19, the disease caused by the virus, are hampering our economic recovery by hobbling the workers who drive the economy. The pandemic led to a huge increase in short-term disability applications and medical leave requests, and many of those who are able to recover from the worst of COVID-19’s symptoms now must deal with the long-term health impacts that prevent them from doing their jobs. All of this is made worse by the country’s lack of universal paid sick leave, which would stem the spread of the virus and reduce some of the racial, economic, and educational disparities in who gets sick. As the incoming Biden-Harris administration looks for solutions to both the economic and health crises, it would do well to enact a permanent federal paid leave program that covers all workers. As Lowrey concludes, “there is no saving the economy without saving the people who make it up.”

In an op-ed for The New York Times, economist Justin Wolfers offers the incoming administration some advice for how to deal with the economic challenges facing the country over the next 4 years—including, as a first step, getting the coronavirus under control in order to boost the economy. He, like Lowrey and many others, argues that controlling the spread of the virus is the best way to restart the economy. Wolfers suggests that President-elect Joe Biden also immediately consider a vast yet targeted stimulus package to help those struggling the most. He then turns to some medium-term solutions to protect the economy from future shocks, including automatic stabilizers that would remove the question of politics from providing aid to support those in need. Finally, Wolfers urges the Biden-Harris administration to address long-term issues such as the climate crisis, universal healthcare, and inequality—challenges that will remain long after the coronavirus recession recedes, Wolfers writes, and delaying action won’t delay their impacts.

Structural racism is behind the racial wealth divide. The legacy of slavery, segregation, and racial discrimination is what suppresses Black Americans’ wealth, writes Michelle Singletary in The Washington Post, despite where many place the blame for the disparities in wealth between Black and White families—on Black people’s spending habits. Relying on the stereotype that Black Americans would be richer if they didn’t spend “so much” on clothing, shoes, or smartphones is intellectually lazy, Singletary explains. Wealth in the United States is typically driven by owning a home—not day-to-day spending or saving behaviors—and Black Americans have long been shut out of homeownership, thanks to racist and discriminatory policies and practices dating back many decades. The American public and policymakers must acknowledge, Singletary concludes, that the difficulty many Black families face in catching up to their White peers’ wealth levels stems from these and other structural barriers to entry that hamper intergenerational transfers of wealth and mobility—not whether a family buys new sneakers for their child.

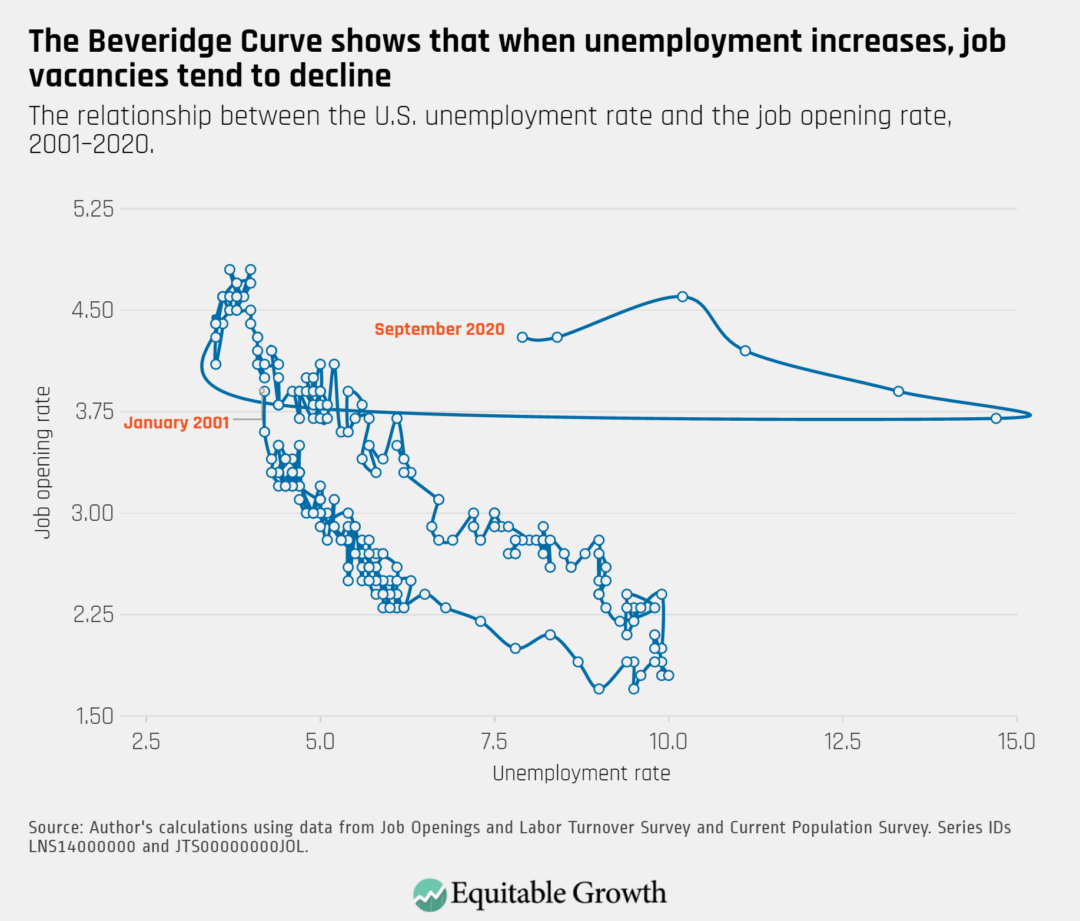

Every month the U.S. Bureau of Labor Statistics releases data on hiring, firing, and other labor market flows from the Job Openings and Labor Turnover Survey, better known as JOLTS. Today, the BLS released the latest data for September 2020. This report doesn’t get as much attention as the monthly Employment Situation Report, but it contains useful information about the state of the U.S. labor market. Below are a few key graphs using data from the report.

The quits rate increased slightly to 2.1 percent in September, signaling stalled prospects for workers.

The vacancy yield was essentially unchanged in September, as the rate of job openings stayed at 4.3 percent and the rate of hires remained at 4.1 percent. Hires decreased significantly in the federal government due to a drop in demand for 2020 Census workers, but hires also fell in retail and educational services.

Since job openings remained unchanged and unemployment declined, the ratio of unemployed-worker-per-opening dropped slightly to 1.95.

The Beveridge Curve continues to move closer to typical territory in September as unemployment declined, but job openings did not increase in the tenuous recovery.

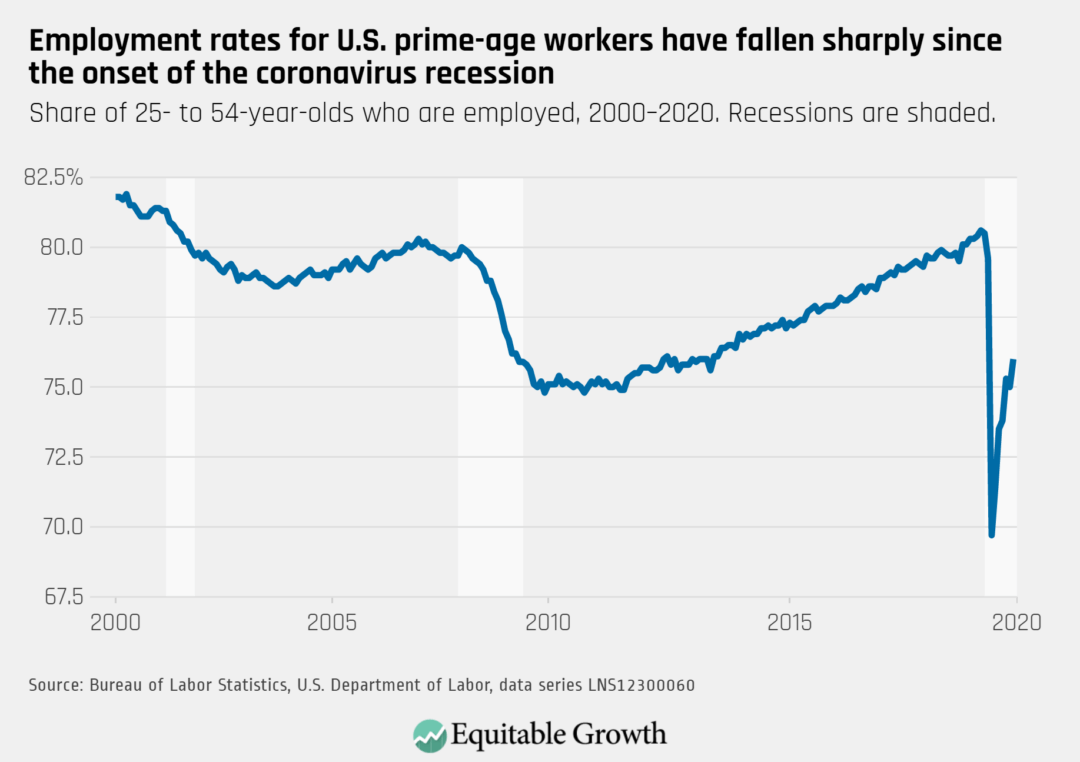

1. If you don’t have time to spend a half an hour or more plowing through the U.S. Bureau of Labor Statistic’s Employment Report, then Kate Bahn and Carmen Sanchez Cumming provide a truly excellent highlights summary. Read their “Equitable Growth’s Jobs Day Graphs: October 2020 Report Edition,” in which they write: “On November 6, the U.S. Bureau of Labor Statistics released new data on the U.S. labor market during the month of October. Below are five graphs compiled by Equitable Growth staff highlighting important trends in the data. While the employment rate of prime-age workers continued to recover in October, reaching 76 percent compared to the pre-pandemic height of 80.5 percent, the pace of its improvement has decreased since the summer.”

2. An equally good briefing on the U.S. Census Bureau’s most recent Household Pulse survey comes courtesy of Kate Bahn, Raksha Kopparam, Carmen Sanchez Cumming, and Austin Clemens. Read their “Equitable Growth’s Household Pulse graphs: October 14–26,” in which they write: “On November 3, the U.S. Census Bureau released new data on the effects of the coronavirus pandemic on workers and households. Below are five graphs compiled by Equitable Growth staff highlighting important trends in the data. Low-income families are more likely to report not being employed compared to middle- and high-income families, exacerbating financial precarity for these U.S. households amid the Coronavirus Recession.”

3. As I am less of an industrial-organization person, I tend to underestimate the importance of market structure and monopoly. But Equitable Growth is on the case. Read “Equitable Growth’s Amanda Fischer joins others in comment letter to antirust regulator on harmful U.S. banking consolidation,” which summarizes the letter: “Fischer, Steele, and Vaheesan argue that the Antitrust Division, along with banking regulators, must reverse the longstanding trend of deregulation and consolidation in the banking industry in order to promote financial stability and ensure the provision of credit to the “real economy.” The U.S. banking industry has been characterized by a long period of increasing consolidation, coinciding with an increase in income and wealth inequality for people across the United States. The top four banking organizations now control nearly 36 percent of all bank deposits in the United States, up from 9.4 percent in 1995. Likewise, these four large banks held 86.7 percent of the total banking industry’s notional amount of financial derivatives as of the first quarter of 2020. Mergers are increasingly rubberstamped.”

Worthy reads not from Equitable Growth:

1. The idea that the long-run debt costs of expansionary fiscal policy depended on the magnitude of the difference between the required rate of return lenders were demanding on government debt and the growth rate of the economy was one that Larry Summers and I had a very difficult time making progress on when trying to convince people to back at the start of the decade of the 2010s. People kept saying that there was something wrong with it—that there was, somehow, a big difference between the social-cost surface and the interest-rate surface because of the risk that demand for government debt might suddenly collapse. But it was very hard to see how that could be true for reserve-currency countries. And now we find that what was our fringe opinion a decade ago is now conventional wisdom—but, so far, only among professional economists of a technocratic (rather than a partisan or an ideological) bent. Read Gita Gopinath, “Global liquidity trap requires a big fiscal response,” in which she writes: “Vulnerable but viable firms require support, a problem that is much better addressed by fiscal policy … There is also a greater risk of currency wars in a global liquidity trap. When interest rates are near zero, monetary policy works to an important extent by weakening currencies to favour domestic producers … Fiscal policy must play a leading role … Governments should look for high-quality projects, while strengthening public investment management to ensure that projects are competitively selected and resources are not lost to inefficiencies. Many economies can lock in historically low interest rates now and keep debt servicing costs low.”

On November 6, the U.S. Bureau of Labor Statistics released new data on the U.S. labor market during the month of October. Below are five graphs compiled by Equitable Growth staff highlighting important trends in the data.

While the employment rate of prime-age workers continued to recover in October, reaching 76 percent compared to the pre-pandemic height of 80.5 percent, the pace of its improvement has decreased since the summer.

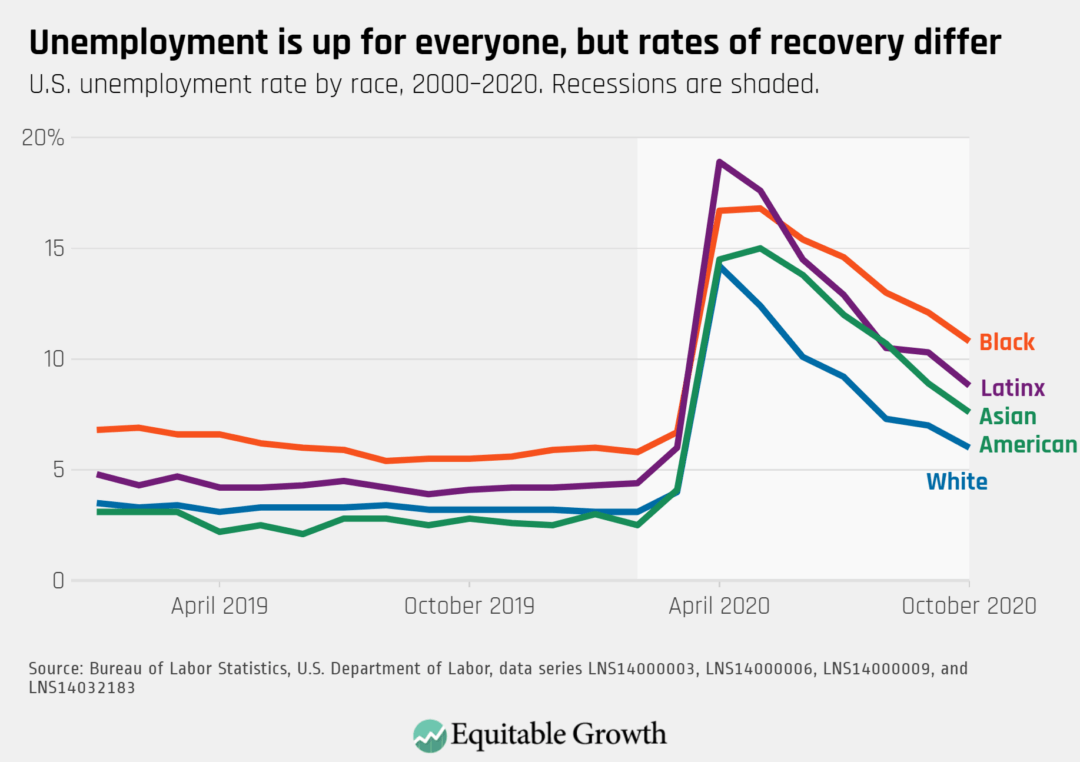

The unemployment rate fell to 6.9 percent for all workers, but was significantly higher for Black workers at 10.8 percent. The uncontrolled pandemic, occupational segregation, and labor market discrimination limit the ability of Black unemployment rates to recover and converge with other demographic groups.

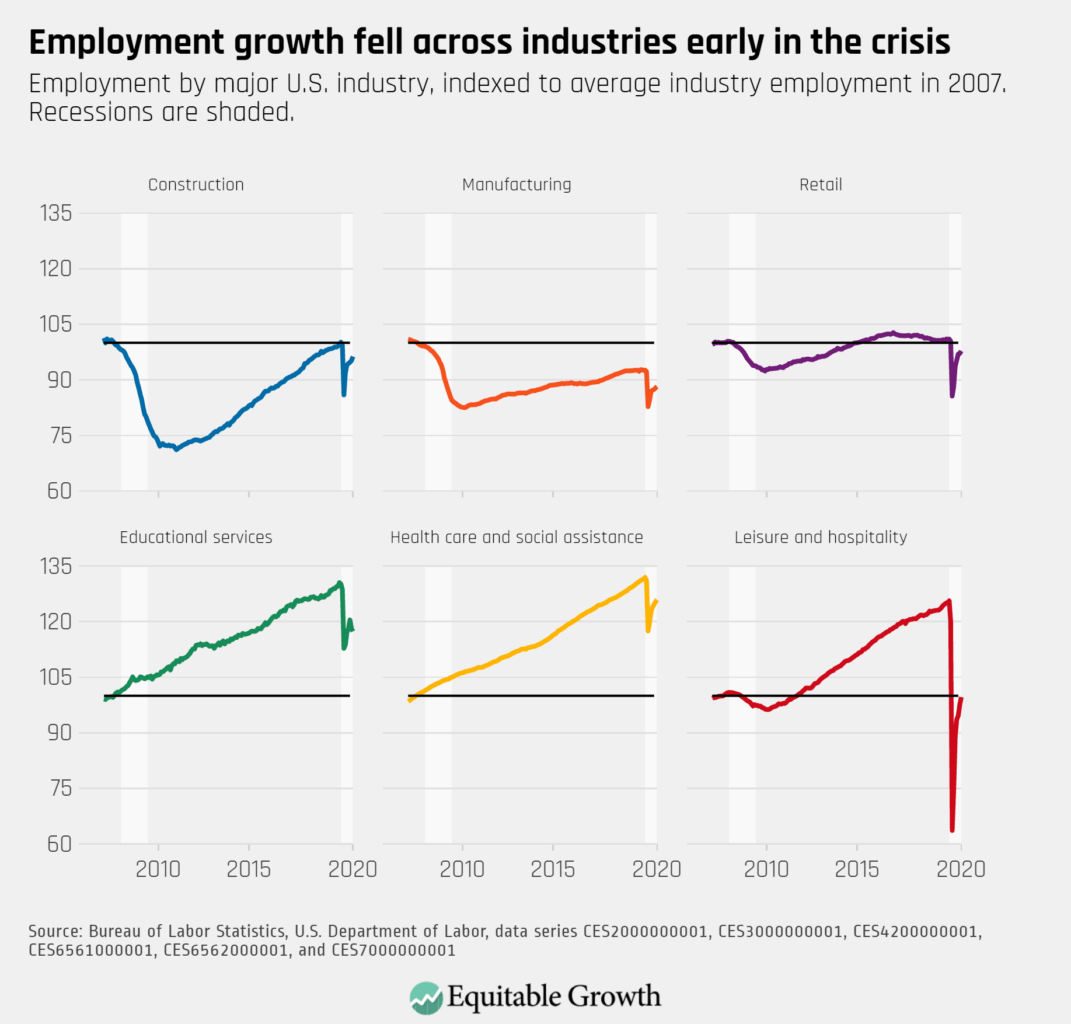

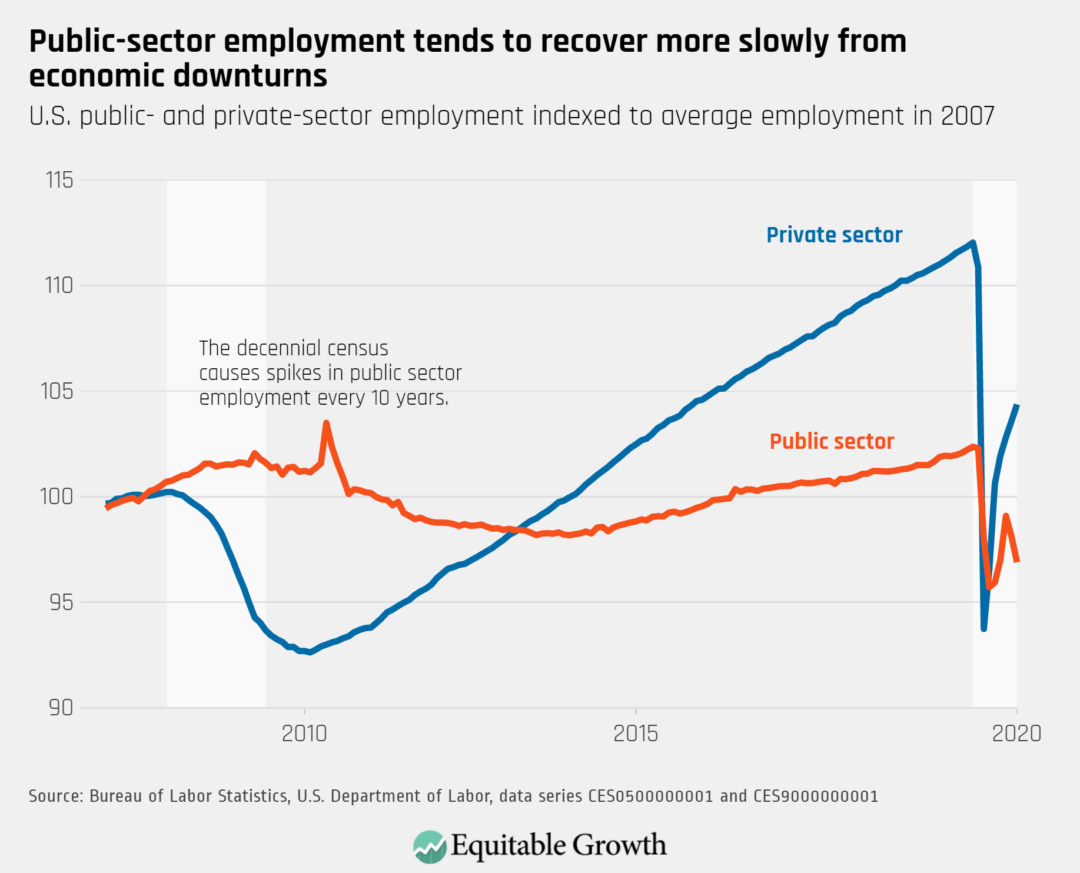

Employment growth continues to improve across the private sector, but layoffs from the end of the 2020 Census and job losses in local and state government education offset employment recovery.

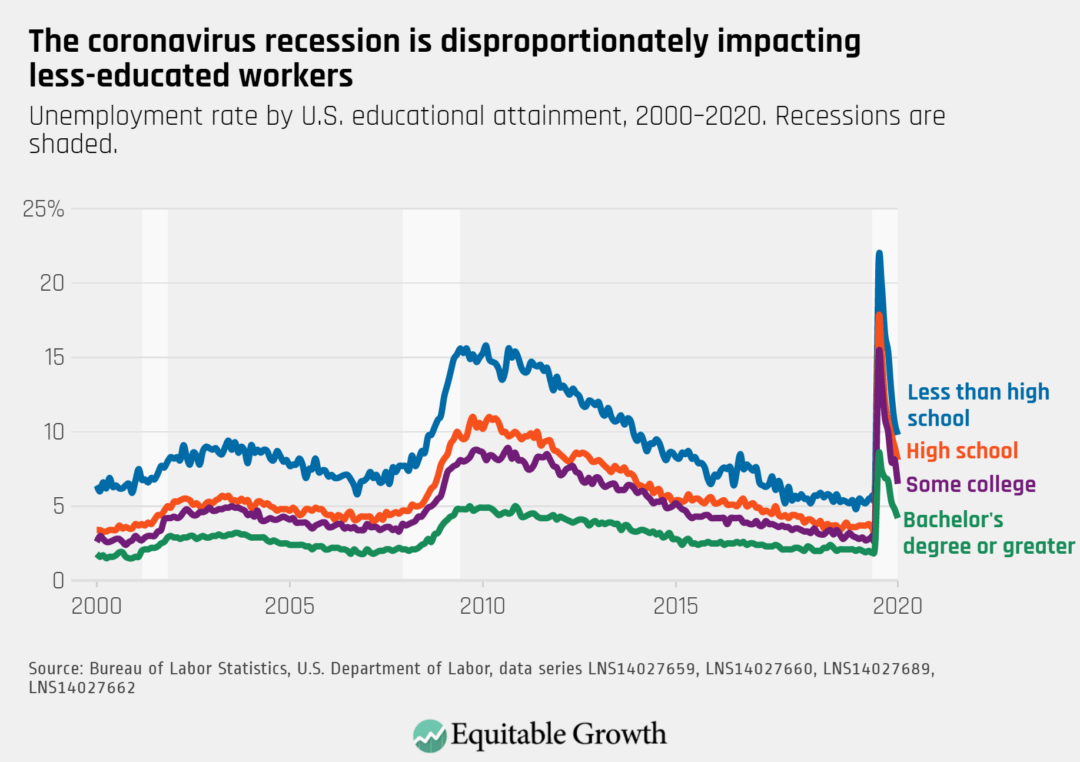

Unemployment rates continue to be significantly higher for workers with less than a college degree, who are less likely to be able to telework.

Public-sector employment declined in October, due to 147,000 Census layoffs and 159,000 job losses in education, disproportionately impacting women workers who are overrepresented in the education sector.

On November 3, the U.S. Census Bureau released new data on the effects of the coronavirus pandemic on workers and households. Below are four graphs compiled by Equitable Growth staff highlighting important trends in the data.

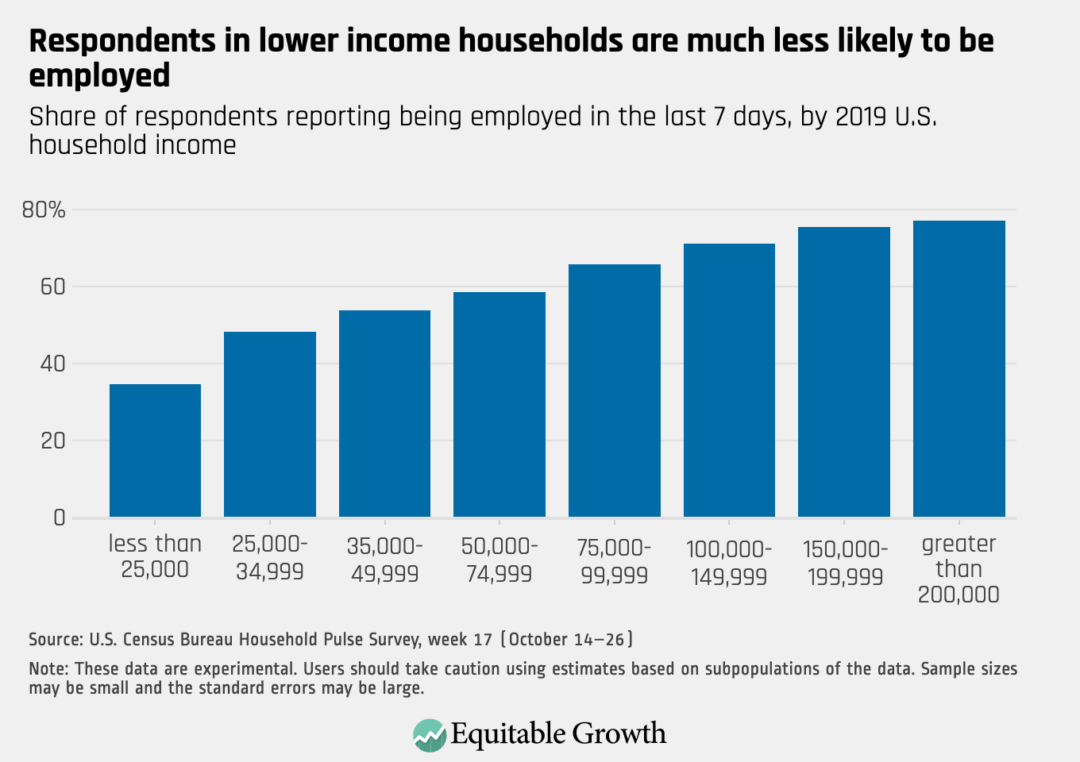

Low-income families are more likely to report not being employed compared to middle- and high-income families, exacerbating financial precarity for these U.S. households amid the Coronavirus Recession.

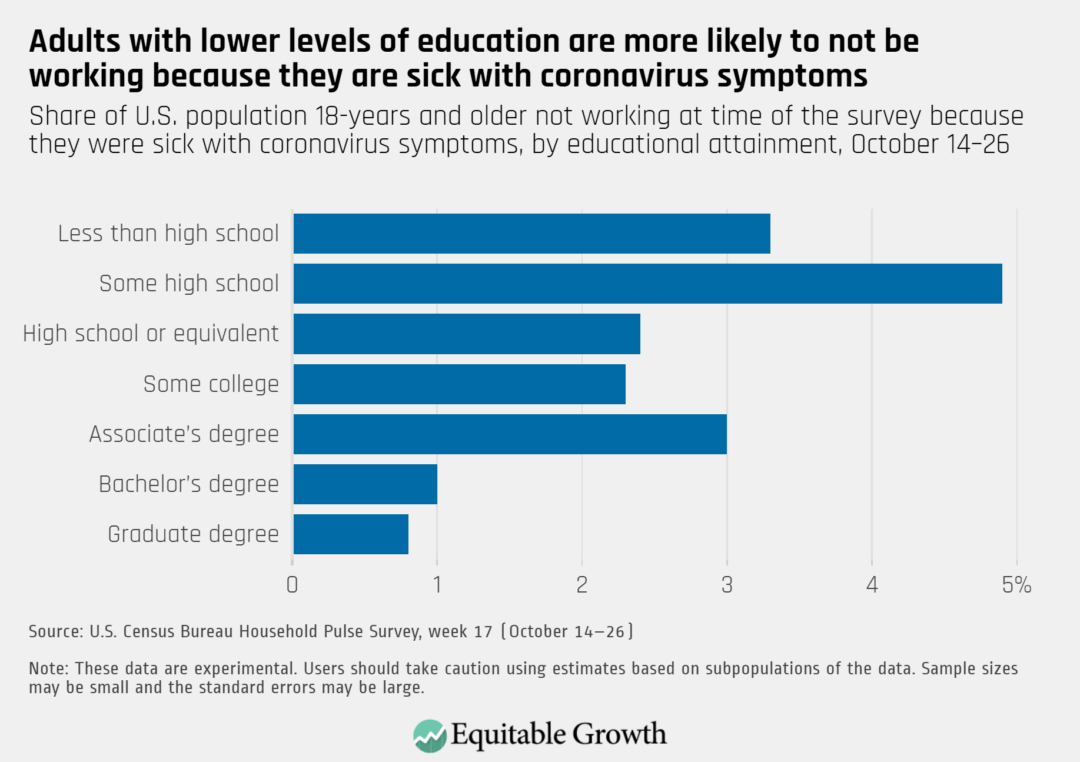

As coronavirus cases surge across the country, workers with lower levels of education are reporting higher rates of not working due to symptoms of the disease compared to those with a bachelor’s or graduate degree.

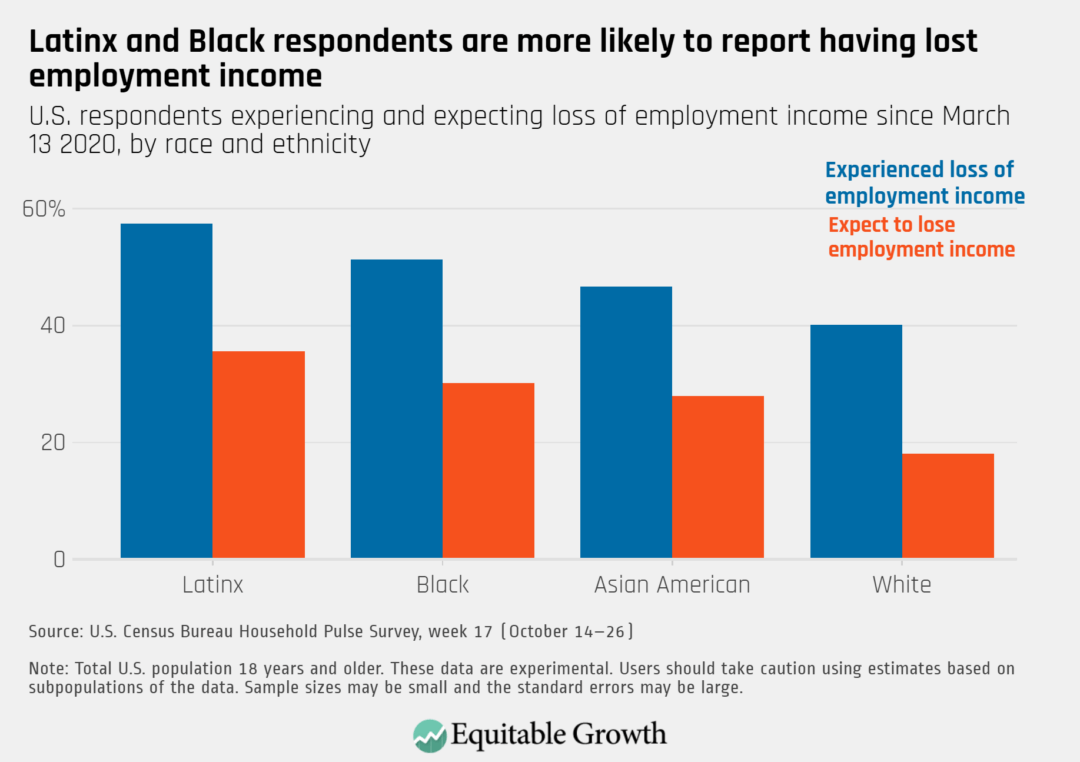

Latinx, Black, and Asian American households continue to report having already lost income during the current recession and expect to continue to lose income at higher rates compared to White households.

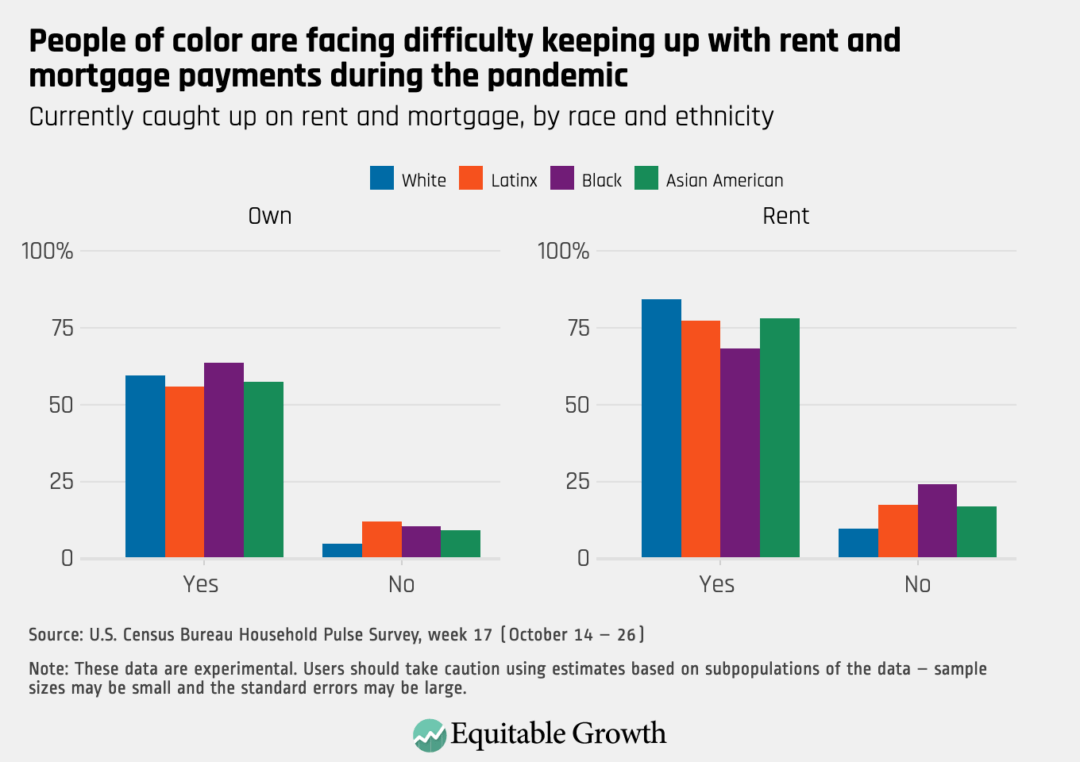

Nearly one-quarter of Black renters and one-fifth of Latinx and Asian American renters report they are not currently caught up on rent, and people of color who own their homes are more likely to report not being current on their mortgage payments compared to White homeowners.

This is a post we publish each Friday with links to articles that touch on economic inequality and growth. The first section is a round-up of what Equitable Growth published this week and the second is relevant and interesting articles we’re highlighting from elsewhere. We won’t be the first to share these articles, but we hope by taking a look back at the whole week, we can put them in context.

Equitable Growth round-up

The minimum wage is one of the primary tools to raise the earnings of low-income workers in the United States. From the time it was first enacted in some states in the early 20th century to the times it was expanded and applied to new industries and grew to include more workers, the clear, widespread positive benefits of the minimum wage are manifest. Ellora Derenoncourt, Claire Montialoux, and Kate Bahndetail the various reforms to the federal minimum wage and its effect on earnings—specifically, its role in narrowing the racial income divide in the 1960s and 1970s, as well as its role in perpetuating that divide in recent decades as the minimum wage has not kept pace with inflation and economic growth. The co-authors explain why increasing the federal minimum wage may be critical to ensure a booming economic recovery and broad-based prosperity for all Americans following the coronavirus recession, which is currently exacerbating racial disparities in the economic security of U.S. households.

Derenoncourt and Montialoux also wrote an op-ed in The New York Times this week, on the vital role the minimum wage plays in reducing racial inequality in the United States. Their research, cited in both the issue brief on our website and in the Times op-ed, shows that raising the minimum wage would have a significant impact on the persistent earnings divide between White workers and their Black, Hispanic, and Native American colleagues. Raising the minimum wage and expanding its application to new sectors currently not covered would be an extremely effective tool in the fight for racial justice, they write, without significantly reducing the number of low-wage jobs available to workers in the U.S. economy.

The extreme inequality that has marked the U.S. economy over the past 40 years made the country more vulnerable to the worst effects of the pandemic and its recession, writesHeather Boushey on Medium. Not only does the United States have one of the world’s highest rates of death from COVID-19, the disease caused by the coronavirus, and the most cases and deaths overall, but the U.S. economy also seems likely to recover much more slowly than that of our competitors. Boushey revisits five predictions she made earlier in the pandemic about the course of the health and economic crises, and then details how policymakers can get the country back on the path to an equitable and robust recovery.

A new study confirms that access to paid sick leave reduced U.S. coronavirus infections by as much as 400 cases per day in states where workers gained access to an emergency paid leave guarantee enacted by Congress in March. Equitable Growth put together a factsheet detailing the key takeaways from the study and the policy implications for the United States—one of only three high-income nations in the world that does not already have a universal paid sick leave program in place.

Public investments in education are a vital element of broad-based, equitable economic growth that will benefit middle-class and low-income families in the United States. Not only are these investments essential for our future workforce—and some even pay for themselves in terms of long-term economic growth, tax revenues, and reduced public spending—but they also can provide a macroeconomic stimulus in the short term that will help jump-start our economy as it struggles to get out of recession. Robert Lynchsummarizes several types of public investments in education, specifically investments in school facilities and in pre-Kindergarten and Kindergarten-through-12th grade services, and how they would contribute to economic growth in the coming years and decades. Lynch analyzes the current policy considerations of these investments and explains why the current low-interest rate environment provides an opportunity to finance these investments with debt, which he argues would be better than financing via tax increases or savings from reductions in other public spending.

Equitable Growth staff submitted to two letters this week to federal government agencies seeking public comments. One comment letter, to the U.S. Department of Labor, expressed our labor market experts’ concerns about a proposed change to the standards for classifying workers as independent contractors or employees under the Fair Labor Standards Act. The change would remove important protections given to employees under the law, including the minimum wage and overtime protections, along with stripping workers of the many benefits of full-time employment, such as healthcare and retirement benefits. The other comment letter, co-signed by Policy Director Amanda Fischer, was sent to the U.S. Department of Justice’s Antitrust Division regarding its Bank Merger Review Guidelines. Fischer and her co-signatories urge the Antitrust Division to reverse the trend of deregulation and consolidation in the banking industry, and in so doing promote much-needed financial stability for U.S. households amid the current economic downturn.

This week, Equitable Growth announced changes to our Steering Committee, with the addition of Lisa Cook of Michigan State University, Hilary Hoynes of the University of California, Berkeley, and Atif Mian of Princeton University. We are looking forward to their contributions to our academic grants program and their support for the next generation of scholars studying the effects of economic inequality on growth and stability. Find out more about their research backgrounds and our Steering Committee.

Links from around the web

Even as reports abound signaling a growing U.S. economy and less unemployment, many Americans, especially Black Americans, are still struggling to find work and pay their basic expenses. The unemployment rate for Black workers remains in the double-digits, high above the rate for White workers. And Black Americans still face disproportionate risk in catching the coronavirus and dying from COVID-19. Dartunorro Clark writes for NBC News that in addition to policies aimed at lowering the Black unemployment rate, more sweeping federal action will be needed in order to address the historic levels of structural inequality in the labor market. Clark details the deep-seated inequalities that persist and the various ways they affect Black workers, particularly now, in the midst of the coronavirus recession. He also discusses the impact (or lack thereof) of the diversity and inclusion pledges many large corporations made earlier this year, alongside large donations to racial justice organizations, on racial inequality—and on the lives of Black employees.

Changes in aggregate Gross Domestic Product do not provide an accurate account of what is really happening across the U.S. economy. Neil Irwin of The New York Times’ The Upshot blog uses the apt metaphor of taking a 3-month average of a person’s health indicators before and after that person is hit by a bus to show why this week’s GDP release is not telling the full story of what’s happening to the U.S. economy. Even though the reports show a record-breaking 7.4 percent rise in GDP over the past 3 months, the data also exposes an economy in a deep recession (albeit not a complete collapse). Irwin points out that the details of the data, when broken down, reveal the areas of the economy that are beginning to recover alongside those that are still reeling from the coronavirus pandemic and recession. He highlights the importance of looking past the headline GDP numbers and diving in more depth into the data to get a better idea of where the economy is and where it might be heading.

Centuries of discrimination and injustices in the United States have robbed Black people from access to opportunities to build wealth and have crippled generations of families, contributing to the vast racial wealth, income, and mobility divides seen today between Black and White Americans, among other disparities in areas such as health, housing, and education. The Washington Post’s Michelle Singletary makes the case for a reparations program in the United States to begin healing the wounds caused by these atrocities—wounds which have repeatedly been scratched open by various actions (or inaction) and policies by the U.S. government. Rebutting several arguments put forth by opponents of reparations, Singletary shows why actions must be taken to acknowledge, redress, and provide closure for descendants of enslaved Americans and how such actions would address the structural racism that pervades every area of our economy and society.

The U.S. economy will not fully recover from the coronavirus recession without universal paid sick leave and child care. Erika L. Moritsugu and Avenel Joseph detail the importance of these two programs for workers in The Hill, explaining the impossible choice many workers have faced during the pandemic between missing a paycheck—or worse, losing their job—or keeping themselves and their loved ones safe from the virus. A paid leave program would relieve them of this burden and surely reduce the spread of the virus, facilitating an equitable recovery for all Americans. Likewise, Moritsugu and Joseph continue, providing accessible and quality child care would enable working parents—and especially working mothers—to continue to provide for their families with the peace of mind that their children are safe. While emergency sick leave provided to some workers in March did help, that program is set to expire at the end of this year. But this pandemic is not temporary, and even if it were, future crises are likely to place these issues back in the spotlight again. We need permanent solutions that provide guaranteed paid sick leave for all workers and affordable child care for all families.

Change is coming to Washington, D.C. No matter who wins the presidential and congressional elections in 2020, a new set of economic policymakers will transition into government. They will come to power at a time of immense economic turmoil. A new Trump or Biden administration, and the new Congress, should quickly implement evidence-backed policies that reduce economic and racial inequality in order to spur strong, stable, and broad-based economic growth. This post, and our entire Vision 2020 initiative, is a guide for how to do just that, especially in light of the continuing negative effects of the coronavirus recession.

In addition to new lawmakers, change is also coming from a new, diverse generation of academics studying the economy. They have a new set of diagnoses for and solutions to our economic problems. Old economic orthodoxies have left tens of millions of Americans with stagnant wages and without key pandemic- and recession-fighting tools such as paid leave, healthcare, and adequate unemployment benefits. At the same time, “free market” policies bestowed the wealthiest Americans with exploding wealth and income, rising market power, and falling tax rates. But now, a new generation of scholars, drawing on new data sources, novel methodological techniques, and their diverse experiences, are offering new structural solutions to get the U.S. economy working for all.

Worker power has declined for decades as firms amassed more control over their suppliers, contractors, and workers, wages stagnated, and unionization rates declined. Congress, state policymakers, and federal agencies such as the Department of Labor can rebalance the current anti-worker policy environment in 2021. Research suggests doing this by supporting unionization, cracking down on employer abuses, and enacting new pro-labor policies such as sectoral bargaining.

Universal paid family and medical leave could not be more critical in the current crisis. The United States is the only high-income country in the world that does not have a national paid family or medical leave program for all workers, which is one reason the coronavirus pandemic has spread so quickly through workplaces and communities. Research into states and countries with paid leave programs suggests that the federal government should establish a system with inclusive eligibility requirements, progressive wage-replacement structures, robust job protections, and adequate leave lengths.

The United States taxes income from wealth at much lower rates than income earned from working. This two-tier tax system gives preferential treatment to wealthier Americans, exacerbating inequality by income and race. Equitable Growth’s key resources and experts describe the current system and the various ways Congress could eliminate the two-tier system to make taxes, and our economy overall, more equitable.

The market power of U.S. corporations, or “monopoly power,” means consumers pay more for what they need, workers earn less, innovation declines, and small businesses aren’t as likely to succeed. Monopoly power also increases inequality by boosting the wealth of executives and stockholders. Academics and former enforcers suggest strengthening U.S. antitrust laws to counter corporate power and boosting resources for the antitrust enforcement agencies—the Federal Trade Commission and the Antitrust Division of the U.S. Department of Justice.

Unemployment Insurance is a bedrock of the social safety net, but unfortunately, policymakers at the state level built numerous problems into the system. These include fragile technical and administrative systems, coverage gaps for independent contractors and those with little work history, low benefit levels, and overly restrictive and complicated program access rules. As the coronavirus recession demonstrates, these issues cause chaos and uncertainty exactly when people most need access to benefits. Equitable Growth has compiled the readings and experts for you to understand the current system and how to fix it, so workers get the help they need.

Racial economic mobility and inequality divides are older than the republic itself but have powerfully come to the fore of late, thanks to the Black Lives Matter movement. U.S. economic mobility is declining as inequality is rising. And Black Americans not only are more likely to experience downward mobility than White Americans, but also face systemic and institutional barriers to wealth building, access to credit, and income security. This post explains economic mobility dynamics, systemic barriers for Black Americans, and how to address them.

Automatic stabilizers are economists’ favorite tools to combat recessions. These policy designs ramp economic support programs up and down as economic conditions, such as the unemployment rate, rise and fall. Making more economic aid “automatic” means quicker, more sustained support for families in need and less politicization of the crisis. A body of experts outline a suite of six ways Congress could expand automatic stabilizers for this recession and those to come.

Small businesses are suffering during the coronavirus recession and need new policies to prevent a wave of bankruptcies. The Paycheck Protection Program enacted earlier this year failed to prevent layoffs and bankruptcies among the smallest employers and did not provide enough assistance to the hardest-hit areas or to businesses owned by people of color. Research suggests restructuring business aid so that small firms can be rescued with the same speed as big businesses and building up public financial systems to improve economic resilience.

The current economic status quo—a devastating recession and underlying fragilities due to sky-high economic and racial inequality—is untenable. Maintaining the status quo is a choice we can no longer afford to keep making. No matter who is in power in 2021, major structural changes are needed. Equitable Growth’s deep bench of policy ideas and experts, highlighted in the above policy guides, can guide the way.

The coronavirus recession took root in a U.S. economy already characterized by profound economic and racial inequality, deeply inadequate public investment, and significant holes in support systems for families. At an October 19 webinar sponsored by the Groundwork Collaborative and several other organizations, including the Washington Center for Equitable Growth, speakers and panelists described past policies that prepared that fertile ground for the spread of the coronavirus, and proposed a series of ideas for recovering from the pandemic and the recession while laying the foundation for a thriving, inclusive economy.

The event, titled “EconCon presents: Building an economy that works for us all,” brought together leading scholars and advocates in two panels to discuss the policies that enabled the spread of coronavirus and COVID-19, the disease caused by the virus, as well as the path forward. The event opened with remarks by Sen. Elizabeth Warren (D-MA) and Stacey Abrams, founder of Fair Fight Action, and closed with a keynote address by sociologist Tressie McMillan Cottom of the University of North Carolina at Chapel Hill.

Sen. Warren set the tone for the event in her introductory remarks. She described the current state of the country in graphic terms: “Our country is taking one gut punch after another,” she said. “More than 200,000 Americans have died from an infectious disease that is still out of control. Our economy is being squeezed to the breaking point. And families are being pushed off an economic cliff as they lose their jobs and struggle to pay their bills. Black and Brown Americans have been hit the hardest.”

“Right now,” she continued, “our nation has a serious choice to make about how to recover from this economic crisis. … We could decide to prioritize making this recovery a racially just recovery. And it starts by reframing what we think a strong economy looks like.” Pointing to racial economic disparities in employment, housing, and wealth, she added, “We have to stop allowing the economic well-being of people of color to be expendable as long as White folks are doing OK and the stock market is doing OK.”

Abrams told the virtual audience that economic recovery depends on the ability of all people to spend and support their families. “We need to rebuild our economy, but we need to learn from past failures and current calamity as we do it,” she said. “Fundamentally, the economy does well when we all do well. We have the power to reshape the economy because we are the economy.”

Past policies that paved the way for economic disaster

The first panel, titled “How decades of conservative policies and narratives paved the way for economic disaster,” featured economist Ioana Marinescu of the University of Pennsylvania, author and former President of Demos Heather McGhee, and Mehrsa Baradaran, professor at the University of California, Irvine School of Law and a member of the Equitable Growth board of directors. New York Times columnist Jamelle Bouie served as moderator.

The panel agreed that the coronavirus recession revealed the weaknesses of the U.S. economy and society. “This crisis could not have done more to reveal and expose some of the mythologies at the heart of our economy,” Baradaran said, adding that “people’s lives came up against the economy and a lot of policymakers chose economic growth versus people’s lives.”

Marinescu and McGhee pointed out that that the recession showed the weakness of U.S. social systems. “One of the things that characterizes U.S. social policy as compared to many other rich countries, including Europe … is the paucity of its social protection system,” Marinescu said. “We have rolled back a lot of the social protection programs that we had, we have limited the amount, and more and more made them conditional on work.” The recession, she added, “exposes the holes in our system in terms of being able to ensure an income for all in a time of crisis like today.”

McGhee focused on the role of the public health system. “We don’t have a really universal form of guaranteed health insurance, but even beyond that, we also don’t have a robust public health system,” she said. “We have a fragmented, for-profit health system.” She said that the public was shocked that nurses could not obtain adequate personal protective equipment at the beginning of the pandemic, and that half of hospitals in low-income areas had no ICU beds to spare. She blamed the weakness of the system on cutbacks in public health in the latter part of the 20th century.

The panel placed racial animus at the center of the narrative of why liberal economic policies prior to the 1980s failed to support progress for Black Americans, and why low- and middle-income White Americans have been willing to support political leaders over the past four decades whose conservative policies hurt them as well as Black Americans.

Baradaran argued that conservative economic policies were a direct response to the civil rights movement’s push for economic equity. She said this led to the rise in the political strength of libertarian, anti-government policies, after an era when the government’s role had been seen as critical. The argument that government did not have a role to play in addressing people’s economic problems succeeded as it had not before. “The damage has been across society,” she said, but has hurt Black communities the most.

McGhee said that in the New Deal and beyond, many of the policies enacted to help people were developed and implemented “with an asterisk, which is a Whites-only basis.” “The American Dream got so much harder to attain just as the formal barriers to the American Dream were stripped away for Black and Brown people,” she said. McGhee related a story that occurred in many communities around the country when civil rights enforcement began, where formerly segregated public swimming pools were drained and closed to avoid integration. She said this story illustrated how White people resisting integration and civil rights turned against government action. “It was racism, and the link between government action and government action to address civil rights” that made conservative ideas “common sense” for White voters, she said.

Marinescu noted that research shows that countries with more ethnic diversity have poor welfare systems because of racism. She said this had played out in the concept of welfare reform, which was fed by the myth of the “welfare queen,” and cut benefits and made them more contingent on work. She said that policies that provide cash to families, such as a universal basic income, support the economy.

Bouie noted that the $600 weekly supplemental payment that was added in March to Unemployment Insurance benefits by the Coronavirus Aid, Relief, and Economic Security, or CARES, Act has now expired, but also that the additional money did not discourage people from working. He asked if the success of this benefit, as well as the $1,200 payment to all families that was also provided early in the pandemic, might lead to similar policies in the future.

The panel expressed varying degrees of optimism in their responses.

Marinescu expressed hope that this has “opened the window.” She said images of the “undeserving poor” were giving way to “a much bigger sense of solidarity.” She pointed out that “everybody knows that there’s a reason why, through no fault of their own, people have come to suffer economic hardship.” She said this could increase understanding of the need to support families when they face economic difficulties.

McGhee noted that beyond cash benefits, a long-term, broad-based recovery would require support for state and local governments and other priorities. “If you get $600 [a week], that is fantastic, but you also need a school to send your kids to, you also need a hospital that is highly functioning, you also need clean water.” Given these and other crises facing communities across the country, she expressed concern about recent calls for austerity that could stand in the way of needed investments.

And Baradaran said, “I’m not as optimistic about people being convinced that if it’s a benefit to the economy, it’s going to change anyone’s mind.” She pointed to the power that the wealthy exert in politics and society. “The way that our democracy is tilted now,” she said, “it doesn’t matter that this benefits the majority of people … because the people getting the benefits [of this economy] have a larger voice.”

The panel discussed ideas for moving forward to produce a broad-based recovery. McGhee called for reinventing the New Deal era of shared prosperity “without the racial asterisk” and that it depends on “whether or not White people are willing to be part of a multiracial democracy.” She said that the public does not support conservative economic policies, and that White voters need to decide between racial issues and addressing economic policies that are to the right of their own views.

Baradaran pointed to the need for electoral and judicial reform. She noted that the U.S. Constitution gives greater power to White and more conservative voters because of the Electoral College and the make-up of the U.S. Senate. She expressed concern that, in fact, White voters may still vote on the basis of race instead of on the basis of economic policies that would benefit them.

Marinescu raised the question of how to pay for necessary programs and pointed to the possibility of a wealth tax. It’s “often maligned by conservatives as punishing the rich,” but it should be seen as providing “the symbolic value that we’re all pitching in and those who have more pitch in more because they can, and it’s not about punishing you.” She noted that racial wealth inequality is far greater than income inequality. “Being able to make progress on wealth equality is so important for having a more equal society.”

Building a multiracial, post-neoliberal economy

The second panel was titled “Where we need to go: Building a multiracial, post-neoliberal economy.” The panelists were Jess Morales Rocketto, executive director of Care in Action and civic engagement director for the National Domestic Workers Alliance, Abdul El-Sayed, a physician, epidemiologist, activist, and educator, and former Deputy Secretary of the U.S. Department of the Treasury Sarah Bloom Raskin. The panel was moderated by the President of Demos K. Sabeel Rahman.

Rahman began by acknowledging the current calamitous time, noting that “we are in a moment where these intersecting crises—of systemic racism, of the pandemic, of the economic collapse before us—have all combined to produce such a severe moment of crisis for our communities.”

El-Sayed ushered in the conversation about the fragility of the U.S. economy by examining the state of the nation prior to the pandemic. As he explained, “We know that if you look at the pathophysiology of the coronavirus, that among people with preexisting conditions, the risk of a serious course of illness and even death is substantially higher.” Consequently, “among societies with preexisting conditions, the course of this disease and the risk of serious outcomes is higher, and our economic circumstances are a preexisting condition.”

Raskin then pointed to income and wealth inequality as one of the greatest longstanding conditions plaguing the U.S. economy. She explained that the nation has “had a very fragile heterogeneity of income and wealth, where we have essentially gutted the middle class,” leaving the nation with “this barbell which actually does not poise the economy or … households well in terms of being hit by exogenous shocks.” She explained that we went into this set of crises with an unaddressed set of fragilities that have created greater dispersions in income and wealth, and “set us up for a very hard shock that came our way via the pandemic and will make it exceedingly challenging to get out of.”

Rocketto described the plight of domestic workers during a time of unprecedented challenges. She explained how workers in this industry, particularly women, are more susceptible to negative consequences of wealth and income inequality. She said that “we still have the vestiges of the past in that industry, and so it is an exploited and marginalized sector of the economy. And that is because it is directly related to slavery and racism and patriarchy around women’s work and working inside the household.”

All three panelists agreed this deep structural crisis developed over the course of the nation’s history. And they concurred that if the country does not respond, not only will we fail to meet the current crisis but conditions are likely to get even worse over the next few years—or even over the next decade. Rahman pointed out that one of the consistent themes of U.S. history has been “the systematic bypassing or even our continued extraction from people of color, women workers, and the essential workers of our economy” of the income and profits from economic growth. Rahman add that these workers have been the engine of our wealth and stability but have not been part of the social compact. When asked how to ensure that the United States builds an economy that centers these communities that have historically been cut out, the panelists placed addressing workers’ needs and advancing worker power at the forefront of policy priorities.

Raskin said policymakers must “put the worker’s experience at the heart of economic policy. It has to be central to every single policy decision that goes forward.” She explained that there is a disconnect between workers’ experiences and current policy. While there have been major policy changes as a result of the pandemic, she said, many of those changes are still falling short.

Rocketto said that “workers themselves have a lot of clarity about what’s really needed” and that understanding workers’ experiences and how they interact with the labor market is essential to policymaking. She also argued that workers need to have a seat at the policymaking table and that they should be considered experts in terms of setting standards in their industries. Rocketto explained that workers themselves are already experiencing those changes that policymakers are understanding only at a theoretical level, “so it just makes sense to listen to the people who have the experience right now and can influence and shape that, even as we are thinking about the larger, macro-level changes that we are trying to apply.”

Commit to fight for a more just, equitable, and prosperous economy

The conference concluded with a keynote by Tressie McMillan Cottom from the University of North Carolina at Chapel Hill. She tied the day’s key takeaways together by reminding the audience that no matter the outcome of November’s elections, it is important to be committed to fighting for a more just, equitable, and prosperous economy.

Cottom framed her remarks around “the powerful progressive ideas and narratives that have shaped economic policy … and delimited our imagination about what is possible.” She discussed the idea that she said has animated all of her work and considers “probably the most powerful idea outside of slavery in all of United States of America folklore … the idea that there is a clear path for upward social mobility and economic security, and we have solved the puzzle and that puzzle is deeply embedded in our belief in markets, in liberalism and free speech and civil liberties.”

Focusing on the prospects for women, particularly Black women, in a post-coronavirus economy, Cottom explained that the narrative that describes getting ahead in the United States as being a matter of working hard in school, delaying childbirth, and then going to college not only excludes women from the American Dream, but also is “an unrealistic road map for social mobility.”

Cottom described the considerations that Black women in particular must face when trying to chart a path for socioeconomic growth. She pointed to “sexist public policy wrapped around things such as child care and racist labor market discrimination [that] expose Black women to poorer job quality and lower occupational mobility … bad jobs, and no promotions, no opportunity.” She also explained that “if you are a Black woman sitting at that intersection [choosing between college and entrepreneurship], it makes absolute rational sense for you to do what everybody tells you, you need to do. Which is to go out on your own.”

For those who choose entrepreneurship, Cottom makes it clear that “racist economic policy exposes Black women to poor credit terms and lower wealth basis for investment,” and that “ideas about Black women’s inherent deviance makes them keen to expose themselves to the risks of entrepreneurship on predatory terms.” Citing Janelle Jones, the policy and research director at The Hub Project, and others, she said, “The female recession is … best understood as … one where putting Black women first may just save us all from economic disaster.”

Stating that some progressives have helped to write an unrealistic narrative, Cottom noted that progressive politics face “a special challenge that conservative politics simply does not have when it comes to the stories we tell about society, the stories we tell about the social contract, the stories we tell about humanity.” She said that progressive politics, in order to be progressive, have to be based in reality.

She stated that “politics based in nostalgia simply do not have the same responsibility to reality or material conditions” as politics based on current conditions. “The challenge for progressives is that we have to tell a story that is at least marginally related to reality.” Cottom cautioned progressives, “When it comes to the story then that we tell about opportunity and progress—go to school, get a degree, get a good job—we have a reality problem.”

For Cottom, the great risk is that the pandemic, having pushed women back out of the paid labor market, “is going to legitimize our historical desire to obscure women’s economic lives so that we can get back to the ‘real work’ of economic policy.” She cautioned listeners further that “going to college and hanging out your own shingle will not solve that crisis. That is a deeper more protracted crisis.” It does not benefit us, she added, “to focus so narrowly on the institutions of the mid-20th century—college and entrepreneurship—for solving decidedly 21st century economic problems.”

Cottom concluded, “We have got to be ready, I think, to write a better progressive metaphor at this moment in time, and a progressive metaphor is one that has to tell the truth about our economic realities while also allowing for a development of a set of tools ready to push for better.”

High school students, union activists, and fast food workers rallying in New York City to demand a $15/hour federal minimum wage, April 2015.

Overview

The minimum wage is one of the primary tools for raising the wages of low-income workers. This was the case at its inception in some states in the early 20th century, as a key federal component of the New Deal reforms during the Great Depression, and today, amid the coronavirus recession. Importantly, though, reforms in the 1960s turned the minimum wage into a critical tool for decreasing the wage divides between Black and White workers because Black Americans were overrepresented among low-wage workers who were not initially covered by the federal minimum wage. Yet those reforms six decades ago are now increasingly unable to address racial income inequality without keeping pace with inflation and economic growth.

Indeed, the coronavirus recession demonstrates how persistent disparities in economic security by race and ethnicity are exacerbated in a crisis. Black and Latinx households today are more likely to report a loss in income and difficulty paying expenses. And the tenuous partial recovery of the U.S. labor market since the start of the current recession now appears to have stalled, leaving Black and Latinx workers with significantly elevated unemployment in the double digits.

Research from previous economic downturns highlights how these racial income disparities will not be alleviated by market forces in the eventual post-pandemic recovery. Centering racial justice in economic policy is critical to ensuring broadly shared growth in the future.

This issue brief shows how minimum wages were and remain an important tool for racial justice. We first examine the role of minimum wages today in perpetuating the current racial income divide. We then review who was covered historically by minimum wages, and how the changing real value of minimum wages over time and across geographic divides reflect continued structural racism. We then close with an analysis of what it would mean for economic security of Black and Latinx families to increase the federal minimum wage closer to a living wage.

Low minimum wages and the racial wage divide

The racial wage divide is one of the most persistent features of the U.S. labor market. Yet a greater proportion of specific wage gaps between Black men and White men and Black women and White men are “unexplained” by the so-called human capital model or are interpreted by economists as the result of overt discrimination, compared to the gender wage gap between all men and all women workers, which is explained to a greater extent by differences in occupational segregation.

What is clear is that the wage gap between Black and White workers persists across the wage distribution and is larger at the top of end of the wage distribution, where Black workers are excluded from high-wage jobs. One of the primary reasons this racial wage divide is less severe at lower wage levels is because of the minimum wage. By design, minimum wages boost the pay of workers who are among the lowest-paid in the U.S. labor market. And Black workers have the highest share of those who are paid the minimum wage among all major racial and ethnic groups in the United States.

Increasing the minimum wage to $15 an hour, for example, would increase the earnings of 38.1 percent of Black workers, compared to 23.2 percent of White workers. This calculation is based on a combination of workers in states whose minimum wage is determined by the current federal minimum wage of $7.25 per hour, workers in states with a state minimum wage below the federal minimum, and workers in all other states who are currently earning less than $15 per hour.

Black and Latinx workers also are more likely to experience wage theft, where they are paid less than the statutory minimum wage by their employers, because of the ineffective enforcement of minimum wage standards. According to new research by Rutgers University labor market researchers Janice Fine, Jenn Round, Daniel Galvin, and Hana Shepherd, Black workers are 50 percent more likely than White workers to experience a minimum wage violation, and Latinx workers are 84 percent more likely to experience this serious labor market problem. Black women who are not U.S. citizens are 3.7 times—370 percent—more likely to experience a minimum wage violation, compared to White male U.S. citizens.

The upshot is that the level of minimum wages, who they apply to, and how well they are enforced all play a role in offsetting racial wage inequality and working toward racial economic justice.

How historical exclusions and expansions to minimum wages influenced racial wage inequality

The minimum wage played an important role in driving more equitable U.S. labor market outcomes since it was first introduced in individual states beginning in 1912 and federally as part of the Fair Labor Standards Act of 1938. When the Fair Labor Standards Act first came into effect, the federal minimum wage was mandated in sectors such as transportation, finance, manufacturing, and wholesale trade, covering about 54 percent of the U.S. workforce. Due to opposition from Congress, however, the initial legislation excluded sectors in which Black workers represented a large share of the workforce—even though President Franklin D. Roosevelt intended it cover the entire U.S. economy.

In particular, both state-level minimum wages from 1912 to 1923 and the Fair Labor Standards Act of 1938 played into highly racialized and gendered conceptions of work that excluded Black workers and in particular Black women as “Neither Mothers Nor Breadwinners.” Early state-level minimum wages that were passed between 1912 and 1923 during in the Progressive Era both adopted the rhetoric of protecting vulnerable women while also excluding farming and domestic services industries where Black women were overrepresented. Then, in 1923, the Supreme Court case Adkins v. Children’s Hospital ruled that minimum wage laws covering women workers violated their freedom of contract.

With the passage of the Fair Labor Standards Act in 1938 as part of the New Deal, the focus was to promote and maintain the breadwinner status of male heads of household. Yet congressional compromises over the federal minimum wage excluded male and female workers in industries in the South that were disproportionately Black. Thus, despite Progressive Era and New Deal legislation intended to improve the conditions of work, Black workers, and Black women in particular, were largely left out.

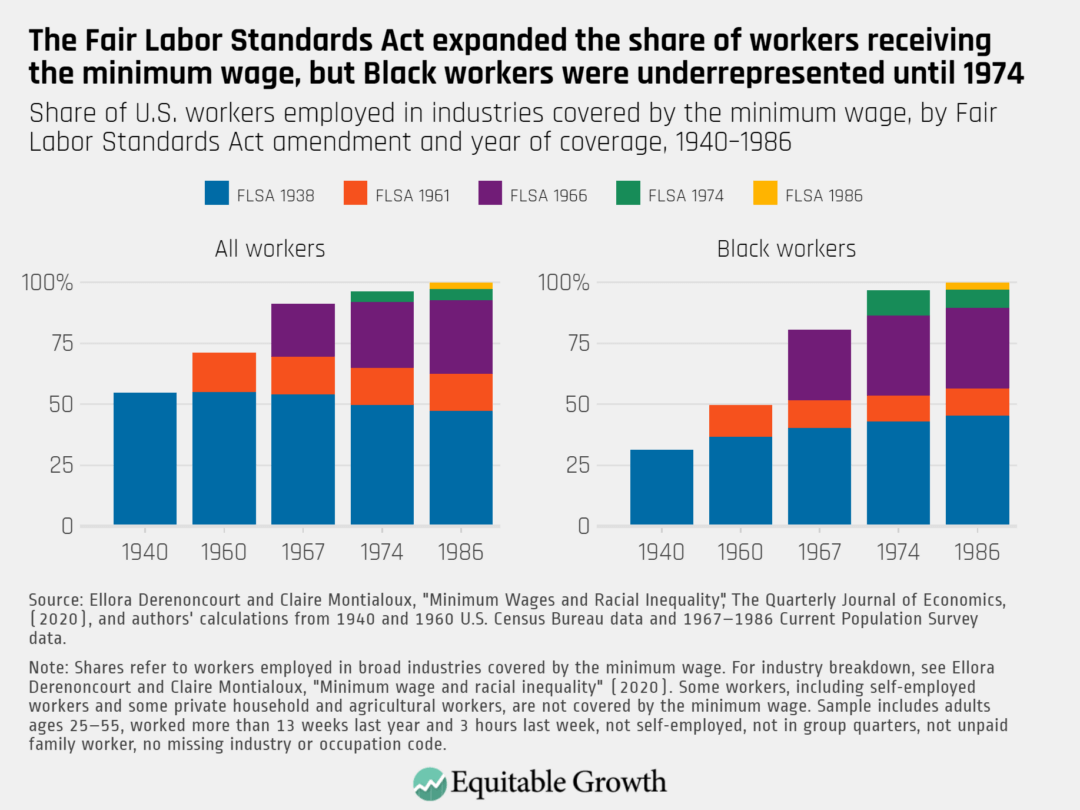

Over the following decades, the Fair Labor Standards Act was modified to cover a larger share of the U.S. workforce. The 1961 amendment introduced the minimum wage to workers in some retail trade and construction establishments, and the 1966 Fair Labor Standards Act—the largest expansion of the minimum wage—provided coverage to workers in agriculture, nursing homes, laundries, hotels, restaurants, schools, and hospitals. The year the new legislation came into effect, approximately 8 million workers, or a fifth of all U.S. prime-aged workers, were employed in the newly covered sectors. It was not until this expansion that the majority of Black workers had access to the federal minimum wage.

In 1966, the Fair Labor Standards Act also was amended to introduce a $1 wage floor to sectors such as agriculture, schools, nursing homes, and restaurants. As the legislation came into effect in 1967, earnings growth in the newly covered sectors jumped, relative to earnings in the sectors that had been covered by the initial Fair Labor Standards Act of 1938. The positive effect of the minimum wage expansion was almost twice as large for Black workers than for White workers, according to new research by two of the authors of this issue brief, Ellora Derenoncourt and Claire Montialoux. This is because the newly covered sectors employed about a fifth of the U.S. labor force, or almost a third of all Black workers. Even more importantly, the legislation had an especially large effect on workers whose previous wages were below $1, among whom Black workers were also overrepresented. (See Figure 1.)

Figure 1

Derenoncourt and Montialoux also document the effect of the 1966 Fair Labor Standards Act on employment. They find that the minimum wage expansion did not lead to large disemployment effects for either Black or White workers. As a result, the 1967 minimum wage expansion also led to a decline in the racial income divide. Overall, the introduction of a $1 minimum wage floor explains more than 20 percent of the fall in both the racial earnings and income divides experienced between 1965 and 1980.

Previous studies had alternatively credited improved educational outcomes for the Black population (in terms of both number of years of school and quality of education) and federal anti-discrimination policies for the decline in the racial earnings gap during the civil rights era and immediately afterward. But it’s clear now that the 1967 expansion of the minimum wage to previously uncovered sectors of the U.S. economy also made a significant contribution.

A higher federal minimum wage would help regional wage dispersion and reduce the racial wage gap

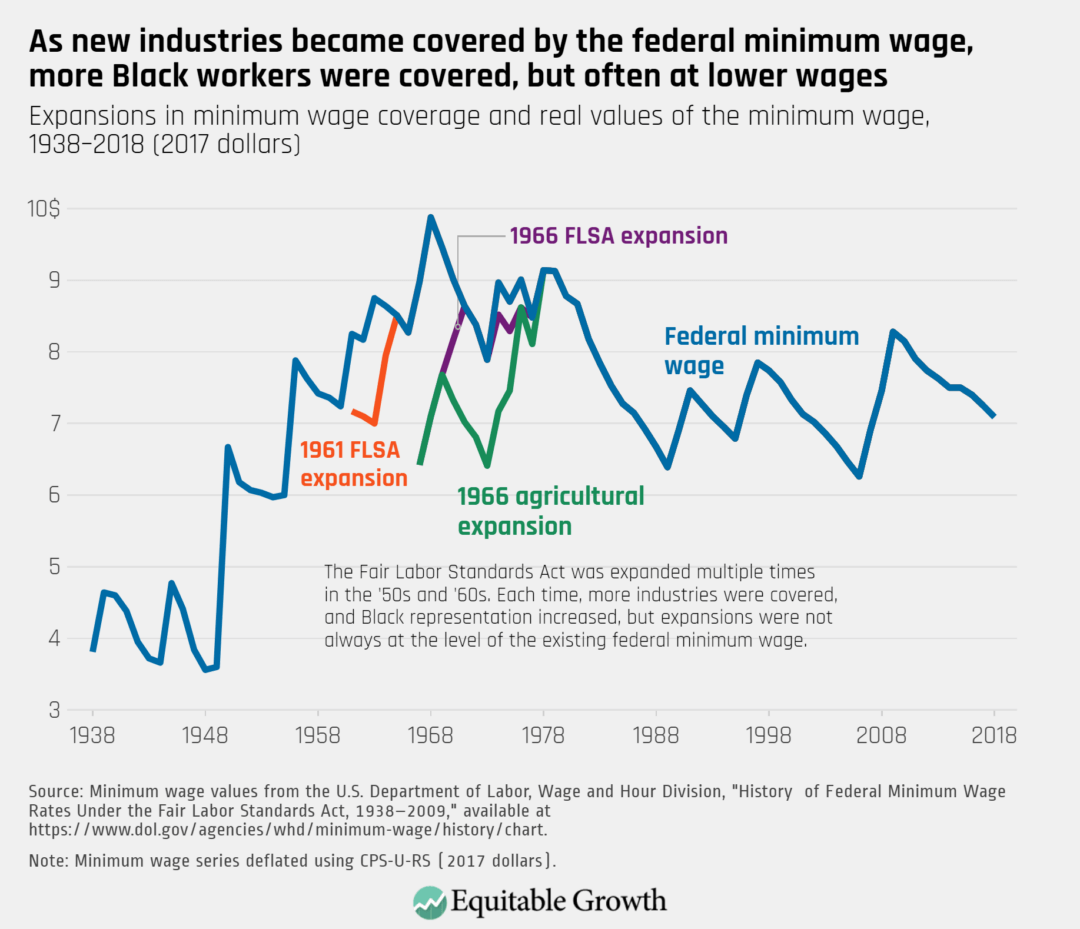

In the United States, earnings across states and territories range from the highest median wage of $35.74 in the District of Columbia to $15 in Mississippi to the lowest median wage of $10.13 in Puerto Rico. This is due to a wide variety of factors, including differences city and state minimum wage statutes above the federal minimum wage and industrial composition between states that influence median earnings in those states.

Twenty-nine states boast minimum wages today that are higher than the current federal minimum wage of $7.25 per hour, and 48 localities have adopted minimum wages higher than their state minimum wage or the federal minimum wage. Wages are also lower in states that have so called right-to-work laws and have lower union density. These states also tend to have more resistance to minimum wage increases. A higher federal minimum wage would help establish a floor across the nation, rather than institutionalize regional wage dispersion.

Variations in wages across states and regions immediately lead to arguments over whether a higher federal minimum wage will actually harm workers in states with lower median wages, since the increase to the minimum wage would be a more substantial relative increase, compared to states that have independently raised their minimum wages above the federal floor. But as Derenoncourt and Montialoux’s research on the history of the federal minimum wage increase in 1967 shows, a significant national wage increase may be sustainable since the expansion of minimum wages to previously uncovered industries was, in effect, an infinite increase above the prior minimum of $0.

The ability to significantly increase minimum wages without roiling U.S. regional labor markets is further supported by additional research. This research finds that increases of nearly 40 percent in the federal minimum wage, which would be similar in magnitude to the increases in the minimum wage that Seattle enacted between 2013 and 2016, would likely not have had a disemployment effect at the time on a national scale while also alleviating the worst earnings losses experienced during the Great Recession of 2007–2009 and afterward.

This finding points to the conclusion that a higher minimum wage would be an effective tool for mitigating the racially disparate negative economic consequences of the coronavirus recession, too.

A higher federal minimum wage would reduce poverty rates for Black and Latinx families

Black and Latinx workers are significantly more likely to be paid poverty-level wages than White workers. This is why minimum wage levels are an especially important tool for raising the earnings and decreasing the economic precarity of the working poor. And it is no surprise that states with the highest poverty rates are also among those that have not independently increased their minimum wage above the federal floor.

Amid the coronavirus recession, millions of families fell into poverty after the financial relief provided by the Coronavirus Aid, Relief, and Economic Security, or CARES, Act largely diminished with the expiration of the $600 plus-up in unemployment benefits at the end of July. These patterns will persist unless robust and inclusive economic policies, including an increased federal minimum wage, are part of the efforts to rebuild the economy centering racial justice.

Furthermore, the real value of the federal minimum wage declined beginning in the late 1970s to the late 1980s, just as the convergence of the racial wage gap began to stutter. Currently, the minimum wage has not been increased since 2009, when it rose from $6.55 per hour to its current level of $7.25 per hour. In fact, the highest value of the minimum wage was at the time of the 1967 expansion. At that time, the federal minimum wage was nearly $10 per hour in 2017 dollars. (See Figure 2.)

Figure 2

The U.S. economy, of course, is much larger and more productive than it was in the 1960s, yet low-wage workers are not sharing in those gains. Had the 1968 minimum wage kept up with inflation and productivity growth, it would actually be $24 per hour today. Raising the minimum wage would turn back the declining real value of the minimum wage, reduce racial wage gaps as long as Black and Latinx workers are more likely to be low-wage workers, and reduce the higher likelihood of poverty for Black and Latinx families.

Conclusion

This past August was the 57th anniversary of the historic March on Washington for Jobs and Freedom. Raising the federal minimum wage would help achieve the vision of racial justice outlined in the march: One of the 10 listed demands in the organizers’ platform was extending the federal minimum wage to previously uncovered workers, which was accomplished in the years following with the extensions of the Fair Labor Standards Act. Civil rights leaders more than half a century ago knew that the minimum wage was a critical tool for addressing racial wage gaps and higher poverty levels by race. The coronavirus recession now brings into stark relief how structural racism still influences economic outcomes of workers and families, elevating calls once again to raise the minimum wage as an important tool for racial justice that will foster broadly shared economic growth in the post-pandemic recovery.

Equitable Growth welcomes three new Steering Committee members.

The Washington Center for Equitable Growth announced today that three distinguished economists—Lisa D. Cook of Michigan State University, Hilary Hoynes of the University of California, Berkeley, and Atif Mian of Princeton University—have joined its Steering Committee to help guide the organization’s efforts to study economic inequality and its impact on economic growth and stability, and to build a new narrative about what makes the U.S. economy grow. As Steering Committee members, they will advise on the organization’s growing academic grants program and help strengthen connections to (and among) our academic community, especially in supporting the next generation of scholars.

“We’re thrilled that this trio of leaders in their fields are joining our Steering Committee,” said Equitable Growth President and CEO Heather Boushey. “As we continue to enhance our academic engagement, they will help us to identify the most pressing research questions related to inequality and economic growth, as well as the rising stars engaged in advanced, innovative scholarship. With their extensive engagement with the policy process, they also exemplify Equitable Growth’s mission to bring together researchers and policymakers seeking to advance evidence-based agendas to address national problems.”

Lisa D. Cook, who has been a member of the Equitable Growth Research Advisory Board since its launch, is a professor in the Department of Economics and in international relations (James Madison College) at Michigan State University. Among her current research interests are economic growth and development, financial institutions and markets, innovation, and economic history. She has served as a senior economist at the president’s Council of Economic Advisers and a senior advisor at the U.S. Department of the Treasury. Cook was the first Marshall Scholar from Spelman College, where she earned her B.A. She received a second B.A. from Oxford University and her Ph.D. in economics from the University of California, Berkeley.

Hilary Hoynes is a professor of economics and public policy and holds the Haas distinguished chair in economic disparities at the University of California, Berkeley, where she also co-directs the Berkeley Opportunity Lab. Her research focuses on poverty, inequality, food and nutrition programs, and the impacts of government tax and transfer programs on low-income families. She was previously awarded an Equitable Growth academic grant, and she served on the National Academy of Sciences Committee on Building an Agenda to Reduce the Number of Children in Poverty by Half in 10 Years. Hoynes received her Ph.D. in economics from Stanford University and her undergraduate degree from Colby College.

Atif Mian is the John H. Laporte, Jr. Class of 1967 professor of economics, public policy, and finance at Princeton University and director of the Julis-Rabinowitz Center for Public Policy and Finance at the Princeton School of Public and International Affairs. A co-author with Amir Sufi on House of Debt, a book that describes how debt precipitated the Great Recession of 2007–2009, Mian’s work examines the connections between finance and the macroeconomy. He earned his B.A. and his Ph.D. in economics from the Massachusetts Institute of Technology. He was also previously awarded an Equitable Growth academic grant.

The Equitable Growth Steering Committee comprises leading academics and former senior policymakers, including Nobel Laureate Robert Solow, former Federal Reserve Board of Governors Chair Janet Yellen and Vice Chair Alan Blinder, former White House Council of Economic Advisers Chair Jason Furman, former Treasury Department chief economist Karen Dynan, former White House Chief of Staff and Equitable Growth co-founder John Podesta, and Equitable Growth President and CEO Heather Boushey. After 7 years on the committee, founding members Emmanuel Saez of the University of California, Berkeley and Janet Currie of Princeton University are departing. Other founding members included Harvard University economist Raj Chetty, former Director of the White House Domestic Policy Council Melody Barnes, and former Chair of the White House Council of Economic Advisers and now UC Berkeley economist Laura Tyson.