Our recent policy conference, “Equitable Growth 2021: Evidence for a Stronger Economic Future,” brought together policymakers, academics, advocates, and thought leaders to discuss the best evidence-based ideas for building a stronger economic future for all Americans. The key themes of the 2-day conference included outlining a vision for sustained public investment in structures and institutions to spur equitable economic growth, with a focus on Black and Indigenous workers and workers of color and how to recover from the pandemic while addressing the ongoing racial, climate, and care crises our nation faces. Below is Equitable Growth President and CEO Michelle Holder’s opening address to the conference.

Since its inception in 2013, Equitable Growth’s mission has been to advance evidence-backed ideas and policies that promote strong, stable, and broadly shared growth. I’ve admired Equitable Growth from afar for so long, and I’m now thrilled to take the helm as its leader to help further its mission. After all, Equitable Growth’s mission hits home for me.

As a labor economist, my research examines why some groups in the U.S. workforce hold a more favorable status, while other groups hold a less favorable one. I also look at the consequences of this stratification and how it contributes to marginalization and disempowerment—and ultimately less prosperity and slower growth.

My research is informed by my lived experience, which lies at the nexus of characteristics associated with marginalization and cuts right to the heart of the issues affecting the economy today. The economy is not an abstract system that we have no control over. It is made up of people. People like me: a second-generation immigrant, first-generation college graduate, and working mom.

The economy is also a direct result of choices that policymakers make. A new day has dawned in government, and with it comes the possibility for long-overdue structural changes to the economy. The coronavirus pandemic continues to expose deep fragilities in our economy—especially racial and gender inequities—that economic policymakers have a once-in-a-generation opportunity to address.

Broadly shared economic growth is achievable, but a stronger, more equitable future requires deliberate policy choices coupled with a better understanding of what makes the economy grow. This is why I’m so excited to lead Equitable Growth in this moment, and this is why Equitable Growth’s mission is more important and relevant than ever.

Since 2013, Equitable Growth has provided more than $7 million in grants to more than 300 researchers aiming to understand how economic inequality affects growth and stability. Just last month, we announced $1.3 million in grant funding for 2021, a new record for the organization.

And we’ve managed to maintain this growth despite some pretty intense challenges, including the coronavirus pandemic. When the pandemic-induced recession hit, Equitable Growth was prepared. Our vast body of research exploring how inequality leads to a more fragile economy when shocks occur quickly moved from abstract to concrete.

The organization was able to meet the moment, connecting scholars and their research to policymakers desperate for data and recommendations to help guide their work. The result of that collaboration—as well as tireless organizing and advocacy from groups across the country—was the largest public program of economic relief in the nation’s history. Policies that both brought immediate relief amidst the recession and helped lay the groundwork for a more equitable future.

In 2019, for example, Equitable Growth, jointly with The Hamilton Project, published Recession Ready: Fiscal Policies to Stabilize the American Economy, a collection of big ideas and proposals aimed to help policymakers navigate the next recession. We were able to quickly amplify these ideas at the beginning of the coronavirus recession to help policymakers ameliorate the recession’s worst effects.

There are other examples as well. We published the books Vision 2020: Evidence for a Stronger Economy and Boosting Wages for U.S. Workers in the New Economy, which have provided evidence-backed policy ideas for the new administration and Congress. In fact, in the session later today on social infrastructure as an engine for equitable growth, you will hear insights from one of the essayists in Boosting Wages on how the lack of social investments contributes to market failures, such as many families’ inability to find or pay for adequate child care or cushion themselves against unexpected job loss.

Our in-house policy experts have extensively promoted ideas and policies ranging from investing in the care economy, to raising wages, understanding market competition, promoting new ways of measuring economic well-being, and combating fiscal austerity.

The list goes on.

We have built a foundation of research and have engaged with policymakers about the necessity for long-term, structural changes to the economy to ensure it works for families up and down the income ladder. In doing so, we’ve helped change the narrative about what makes the economy grow.

But there is more work to be done.

In addition to the pandemic exposing deep fragilities in our economy, 2020 also brought with it a racial reckoning in this country. And we have continued to see the consequences of climate change take hold, most recently with the devastation wrought by Hurricane Ida and the fires in California.

The current moment calls for a vision of sustained public investment in structures and institutions to spur equitable economic growth, with a focus on Black, Indigenous, Latinx, and Asian American workers. The current moment also calls for addressing inequities such as the gender and racial wage and wealth divides, and for centering people in that vision who have been ignored by policymakers for far too long.

And last but not least, the current moment calls for a coherent and comprehensive vision for emerging from the pandemic stronger and more equitable, unafraid of addressing the ongoing and overlapping racial, climate, and care crises our nation faces. Public investments in these areas can spur strong, stable, and broad-based economic growth by addressing longstanding racial and income inequality, driving clean energy and creating good jobs, and jumpstarting a new era of innovation.

This is a moment we must continue to face head on if we want an economy that works for everyone, not just the few.

The Washington Center for Equitable Growth through its Dissertation Scholars Program supports pre-doctoral students from the social sciences who are studying the links between inequality and growth. With a stipend of $50,000, as well as professional support—including connections to potential mentors and collaborators in the Equitable Growth network—the program invests in the next generation of scholars pursuing research that will inform evidence-backed policy solutions.

The Equitable Growth Dissertation Scholars for the 2021–22 academic year are Lauren Russell of Harvard University and Sheridan Fuller of Northwestern University. Both Russell and Fuller have started their in-house residence virtually.

Russell is a Ph.D. student in public policy at Harvard University and a familiar face at Equitable Growth, having received a doctoral grant in 2019 to study the link between a criminal record and access to opportunity and mobility. Her research interests are in labor economics and public finance, with a focus on the intersections of poverty, race, and inequality. Her current focus is centered on understanding and addressing social inequality as it relates to housing, mobility, and criminal justice.

Russell’s research agenda has two main prongs. First, she is examining whether and how a criminal record limits access to some neighborhoods in the United States—specifically, neighborhoods with high measures of social mobility, low crime rates, and good-quality schools. Second, she is exploring whether limited or precarious access to housing leads to recidivism and the relationship between recidivism and neighborhood quality.

In Russell’s own words, her two research objectives necessarily mean a “focus on the role that structural racism has played in determining outcomes in housing, mobility, and criminal system contact for Black and Indigenous people in the United States both historically and in the current moment.”

Russell also acknowledges the importance of working with both policymakers and key stakeholders to translate her research findings into real-world policy proposals. Her hope, she says, is that “this project will push forward the conversation on racial justice in access to quality housing and provide evidence in support of a policy response.” This link to policy is a key aspect of Equitable Growth’s mission of bridging the academic and policymaking communities in order to foster evidence-backed ideas that ensure a strong and stable economy for all.

Like Russell, Fuller also understands the importance of connecting research to policy, having spent time in both fields. Before beginning his doctoral program, he was a presidential management fellow at the U.S. Department of Health and Human Services, an experience that drove him, as he explains it, to strive to “develop a toolkit that would allow me to traverse both policymaking spaces and generate research that informs those policy processes and decisions.”

Fuller’s research since starting his graduate program in human development and social policy at Northwestern University has centered on income support programs, such as the Temporary Aid for Needy Families program, and the impact of these programs on U.S. families, and especially on children. He particularly looks at how the design of income support programs can either limit or expand access to vital resources for families, with implications for children’s well-being.

His current work has two primary goals. One is to determine whether racialized welfare policies hindered families’ access to cash assistance program benefits. The other is to identify long-term effects of these programs on children’s health, educational, and economic outcomes in adulthood. Through his research, Fuller will calculate the material benefits—including the aforementioned health, educational, and economic outcomes—that Black and Latinx families lost as a result of being excluded from income support programs, particularly as relates to the 1996 welfare reform legislation that reduced families’ access to cash assistance.

Fuller hopes his research will “provide policymakers with evidence on cash assistance’s effectiveness in protecting children and families experiencing vulnerability and economic hardship” with a specific eye toward “how the racialized design of welfare policies may exacerbate economic inequality and undermine the goal of creating strong, stable growth for all Americans.”

On the value of joining the Dissertation Scholars program, both Russell and Fuller expressed enthusiasm.

“I cannot imagine another institution that is better-fitting for my research trajectory or more equipped to support me as a Black woman economist seeking to make policy contributions that combat structural racism,” said Russell.

“I see [the program] as a unique opportunity to further my career as an engaged policy researcher who is prepared to bring my skills to developing and implementing policies that lead to strong, stable, and equitable growth for all Americans,” said Fuller.

We are excited to welcome Russell and Fuller to Equitable Growth, and look forward to working with both of them over the coming months.

In addition to funding the Dissertation Scholars Program, Equitable Growth awards research grants each year to scholars studying the impact of inequality on economic growth. In August, we announced a record $1.39 million in awards to the largest cohort of grantees—62 in total—in the history of the organization. These grants will go to faculty and staff at U.S. universities, as well as to several doctoral students working on their dissertations. Learn more about our grants program and click here to review the 2021 Request for Proposals.

President Joe Biden asked the U.S. Congress to consider investing $200 billion over 10 years in “a national partnership with states to offer free, high-quality, accessible, and inclusive preschool to all three- and four-year-olds, benefitting five million children.”1 This report calculates the 10-year costs and benefits of such a program. To understand the long-run implications of such a program, the analysis is then extended to a 35-year period. The key findings are:

Total costs and benefits over the first 10 years of the preschool program

A high-quality, publicly funded preschool education program will generate growing annual benefits that will surpass the more-slowly growing annual costs of the program within 8 years. Over the entire 10-year period, the present-value benefit-to-cost ratio is 1.01, which means that every tax dollar invested in the preschool program will generate $1.01 in total benefits over the first 10 years.

The benefits take the form of government budget benefits, increased wages and earnings of workers, and reduced costs to individuals from better health, less crime, and fewer incidences of child abuse and neglect.

Because the annual benefits grow more rapidly than the annual costs, in the 10th year itself, as opposed to over the course of the entire 10-year period, the present-value benefits exceed the present value costs of the program by a ratio of 1.68-to-1.

A high-quality universal preschool program will cost $6,600 per participant and could be expected to enroll about 64 percent of 3- and 4-year-olds, or just less than 5.2 million children, when it is fully phased in after 2 years.

The federal investment in the preschool program will also have a short-run stimulus effect that will boost Gross Domestic Product by $28.6 billion and create 210,200 additional new jobs during the first 2 years to help the U.S. economy recover more equitably and more sustainably from the coronavirus recession of 2020.

Government costs and benefits over the first 10 years

The present-value government benefit-to-cost ratio over the first 10 years of the preschool program is 0.47, which means that every tax dollar invested in the program will generate $0.47 in budgetary savings over the first 10 years. This means the budgetary savings of the preschool program, in the form of higher tax revenues and lower public expenditures on several public programs, will pay for almost half the total taxpayer cost of the preschool program during the first 10 years.

The margin by which taxpayer costs will exceed offsetting budget benefits declines progressively over each of the first 10 years of the preschool program. Thus, in the 10th year itself of the program, the tax-revenue increases and expenditure savings due to the preschool program pay for 68 percent of the program.

Total cost and benefits over 35 years

Over the first 35 years of the preschool program, the present-value total benefit-to-cost ratio is 4.93, which means that every tax dollar invested in the preschool program will generate $4.93 in benefits.

The annual benefits continue to grow faster than the costs. Thus, the benefit cost ratio improves with each subsequent year. In the 35th year, the final year of this analysis, the present value of the total benefits from government budgetary savings, increased compensation of workers, and reduced costs to individuals from better health, less crime, and reduced incidences of child abuse and neglect exceed the present value costs of the program by a ratio of 10.20-to-1.

By the 35th year, the long-run productivity effects of the preschool investment boost Gross Domestic Product by 0.5 percent and may generate as many as 787,000 new jobs.

Government costs and benefits over 35 years

Over the entire 35-year period, the present-value government benefit-to-cost ratio is 1.51, which means that every tax dollar invested in the preschool program will generate $1.51 in budgetary benefits over the first 35 years. This means the program more than pays for itself in budgetary terms.

Taxpayer costs initially exceed offsetting budget benefits, but by a steadily declining margin for the first 14 years. By the 15th year of the program, budgetary benefits exceed the taxpayer costs, and the program generates a budget surplus that grows every year thereafter.

In the 35th year of the program, the present-value government budget surplus amounts to $36.2 billion, with present-value government budget benefits that exceed the present-value government costs by a ratio of 2.84-to-1. This means that every tax dollar invested in the preschool program in the 35th year will generate $2.84 in budget savings, nearly triple the annual cost of the program.

Overview

The policy of investing in high-quality preschool in the United States provides a wide array of benefits to children, families, and society as a whole. Empirical research shows that all children, regardless of where their families are on the income ladder, benefit from preschool programs. In addition, the research confirms that higher-quality preschool programs provide greater benefits than lower-quality preschool programs.

Children ages 3 and 4 who participate in high-quality preschool programs require less special education and are less likely to repeat a grade. They and their families are involved in fewer incidents of child abuse and neglect, which reduces public child-welfare expenditures. And once these children enter the U.S. labor force, their incomes are higher, along with the taxes they pay back to society.

Both as juveniles and as adults, these children are less likely to interact with the criminal justice system, thereby reducing incarceration and criminal justice costs. As adults, preschool participants suffer less from depression and have lower rates of smoking, generating better health, steadier employment and income, and lower public health expenditures. And guardians of public preschool participants take advantage of the child care that, in effect, the programs provide to get a job or work longer hours and earn higher wages—and pay more in taxes.

Additionally, high-quality preschool programs provide budget benefits. High-quality preschool delivers government savings on Kindergarten through 12th grade spending, child welfare, the criminal justice system, and healthcare. High-quality preschool also increases government tax revenues. Thus, investment in high-quality preschool results in significant benefits for future government budgets, for the economy, and for society.

The economic and social benefits from preschool investment amount to more than just improvements in public balance sheets. A myriad of benefits accrue to the affected children, their families, and society as a whole. Children who participate in high-quality preschool programs fare better in school, have better home lives, and are less likely to engage in criminal activity than their peers who do not attend such programs.

The data show that participating children go on to higher achievement later in life, graduating from high school and attending college at a higher rate, and earning more once they enter the labor force. And the parents or guardians of children participating in preschool programs benefit both directly and indirectly from the services offered in high-quality programs.

Investment in young children not only has positive effects on the U.S. economy by raising incomes, improving the skills of the workforce, reducing poverty, strengthening U.S. global competitiveness, improving health outcomes, and reducing crime and incarceration rates. Given that the positive impacts of preschool are larger for at-risk than for more advantaged children, a universal preschool program will also help to reduce achievement gaps between poor and nonpoor children, ultimately reducing income inequality nationwide.

A nationwide commitment to high-quality early childhood education would cost a significant amount of money up front. But over time, government budget benefits outweigh the costs of high-quality preschool education investment—over time, high-quality preschool pays for itself. Yet our political system, with its 2- and 4-year election cycles, tends to underinvest in programs with lags between when investment costs are incurred and when benefits are enjoyed. The fact that governments cannot capture all the benefits of preschool investment may also discourage governments from assuming all the costs of preschool programs.

Although governments do not capture all the benefits of preschool investment, the economic case for making long-term public investment in preschool is compelling. Most government expenditures do not create offsetting receipts to the extent that early childhood education does. Indeed, it may be rare to find public programs that pay for themselves at the budgetary level. It is striking that a preschool program will have significant positive effects on the long-term government budget outlooks. This is why policymakers should consider a national preschool initiative as a sound investment on the part of government that generates substantial long-term benefits and not simply as a program requiring expenditures.

The evidence for long-term public investment in a nationwide public preschool program

Studies of high-quality preschool programs and their participants find that investing in the education of young children delivers a number of lasting benefits for the children, their families, and society at large, including taxpayers. Over time, these investments boost productivity, earnings, and taxes—and pay for themselves. This section of the report details the benefits to children, to families, to society, and to a more equitable economy.

Benefits for children

Assessments of well-designed and well-executed preschool programs find they provide a large variety of benefits to participating children. Preschool education enables young children to be more successful in Kindergarten and primary and secondary school, and in life after these school years, than children who are not enrolled in high-quality programs. In general, children who participate in high-quality preschool programs tend to have greater math, reading, and language abilities.2

More specifically, these children are better prepared to enter elementary school, experience less grade retention, and have less need for special education and other remedial coursework.3 They alsohavelower dropout rates, higher high school graduation rates, and higher levels of educational attainment.4 They also experience less child abuse and neglect, and are less likely to be teenage parents.5 Additionally, with the services offered in high-quality programs, they are better fed, gain improved access to healthcare services, have higher rates of immunization, and experience better health as children.6

As adults, high-quality preschool recipients boast higher employment rates, higher earnings, and lower rates of turning to public-assistance programs such as the Supplemental Nutrition Assistance Program and the Temporary Assistance for Needy Families program. Working and earning more, they pay more in taxes over their lifetimes. They exhibit lower rates of drug use and less frequent and less severe criminal behavior, engaging in fewer criminal acts both as juveniles and as adults and having fewer interactions with the criminal justice system, as well as lower incarceration rates. They also experience better health outcomes in adulthood, such as fewer episodes of depression and less tobacco use.7

In short, the benefits of high-quality preschool programs to participating children enable them to enter school “ready to learn” and help them achieve better outcomes in school and throughout their entire lives.8

Benefits for families

Parents and the families of children who participate in public, high-quality preschool programs also benefit. They benefit both directly from the services they receive in high-quality programs and indirectly from the child care provided by publicly funded preschool. In general, parents take advantage of the child care these programs provide by increasing their employment and earnings, and by investing in their own health and education.9

Mothers in particular benefit from preschool for their children. These mothers have better nutrition and smoke less during pregnancy.10 Parents with kids in preschool complete more years of schooling, have higher high school graduation rates, are more likely to be employed, have higher earnings, pay more in taxes, engage in fewer criminal acts, have lower rates of drug and alcohol abuse, are less likely to turn to public assistance programs, and are less likely to abuse or neglect their children.11

Benefits for society

Investments in high-quality preschool programs pay for themselves over time by generating benefits for participants, the nonparticipating public, and government itself. Studies of high-quality preschool programs find that they produce $2.63 or more in present-value benefits for every dollar of investment, with the programs whose subsequent benefits were studied over the longest periods generating well in excess of $7 in benefits per dollar of investment.12

The participants and their families get part of these total benefits, but the benefits to the rest of the public and government are large, too. On their own, these benefits outweigh the costs of these programs. Taxpayers benefit because preschool participants are less likely to repeat a grade or require expensive special education services or engage in crime or be incarcerated. They and their families also have less need for child welfare and public health services throughout their lifetimes. All of these are outcomes that reduce the cost of taxpayer-funded public services.

In addition, the increased lifetime earnings of the adults who receive a preschool education as children and of their parents enlarge the tax payments they make, pay for the preschool programs, and help fund other public services for society. Thus, it is advantageous even for nonparticipating taxpayers to help pay for these programs.

Benefits for a more equitable economy

Although children across the income distribution benefit from high-quality preschool education, the largest positive effects are on disadvantaged children from lower socioeconomic backgrounds.13 For mothers of preschool participants, the largest employment increases occurred among mothers without a high school degree.14 Thus, public investments in preschool reduce economic inequality.

A cost-benefits analysis of the American Families Plan’s proposal for a nationwide public preschool program

The 10-year, $200 billion American Families Plan’s investment in a nationwide preschool education program envisions a preschool program that is similar in its characteristics to the high-quality, public Chicago Child Parent preschool program. The Biden administration’s preschool proposal, for example, calls for a publicly funded preschool that will have “low student-to-teacher ratios, high-quality and developmentally appropriate curriculum, and supportive classroom environments that are inclusive for all students.”17

In addition, “educators will receive job-embedded coaching, professional development, and wages that reflect the importance of their work.” All employees participating in the preschool program “will earn at least $15 per hour, and those with comparable qualifications will receive compensation commensurate with that of kindergarten teachers.”18

So, what would be the effects of a 10-year, $200 billion public investment in a voluntary, high-quality, universal preschool program made available to 5 million 3- and 4-year-olds in the United States? To be consistent with the administration’s proposal, this analysis assumes a preschool program that is modeled on the Chicago Child Parent program. The program would operate 3 hours per day, 5 days a week, for 35 weeks a year (the school year), or a total of 525 hours.19 The program would be voluntary and available to all 3- and 4-year-old children.

The lead classroom teachers would all have bachelor’s degrees or higher, with certification in early childhood education, and would be required to pursue professional development. The teaching assistant in each class would have at least an associate’s degree. Teacher and staff pay would be high relative to most existing preschool programs, as compensation would follow the salary schedules of public schools.

For the children, the preschool program would provide health screenings, speech-therapy services, and home visitations. Parental involvement would be encouraged. The student-teacher ratio (including the assistant teacher) would be no higher than 17-to-2, and maximum class size would be 17 children. The curriculum would be comprehensive, with a focus that includes language and pre-reading skills, mathematics skills such as counting and number recognition, science, social studies, health and physical development, and social/emotional skill development.

This analysis assumes that the preschool education program would be largely housed within the existing or newly built public school infrastructure. But its services could be delivered in private care centers as well, if they meet quality standards.

A 2011 study of the Chicago Child Parent program that did not consider any short-run macroeconomic stimulus effects calculated a benefit-cost ratio of $10.83 by age 28.20 A 2015 study of the Chicago Child Parent program by the author of this report and Kavya Vaghul, then a research assistant at Equitable Growth, which focused only on the long-run productivity and behavioral impacts of the investments over 35 years, calculated that a voluntary, high-quality, public, universal preschool program modelled on that program would generate annual budgetary, health, and decreased crime benefits that would surpass the annual costs of the program within 8 years.

The 2015 study further found that within 35 years, when the first cohort of children would be in their late 30s, the annual benefits of the program would exceed the costs by a ratio of 8.85-to-1. Within 16 years, the budgetary benefits to governments alone—in the form of lower budget outlays for various programs and higher tax revenues—would surpass the costs of that program, and within 35 years, these budget benefits alone would exceed the costs by 2.37-to-1, or more than double the cost of the program.21 And these benefits would exceed the costs by a growing margin each subsequent year.

In this study, the costs and benefits of public investment in preschool, modeled on the Biden administration’s proposal, are calculated to analyze the effects of a $200 billion public investment over 10 years in high-quality preschool. Although the Biden administration’s proposal is for a 10-year program, this report assumes that the program will be renewed and become permanent. The analysis is then extended to consider the costs and benefits over a 35-year timeframe. These analyses take into account both the long-run productivity effects of preschool, as well as the immediate macroeconomic stimulus effects.

This study assumes that the program will be phased in over 2 years. The analysis considers budget effects on the federal government and the combination of state and local governments. Although responsibilities have shifted in the past and will continue to do so in the future over the 10- and 35-year timeframes used in this study, it is assumed that all levels of government will share in the costs of education, child welfare, criminal justice, and healthcare in the future in the same proportions as they do today.

Likewise, it is assumed that federal, state, and local tax rates will remain constant over the period analyzed in this study. It is assumed that federal, state, and local governments will maintain their efforts in Head Start, special education, and state preschool programs, but all additional costs attributable to the new preschool program will be paid by the federal government. However, regardless of which level of government pays the cost of the preschool program, the total budgetary benefits to all levels of government remain unchanged—only the cost burden shifts. In the case of a federally funded program, states and localities receive budget benefits without paying the additional costs of the program. And in a state-funded program, the federal government receives budget benefits without incurring the program’s additional costs.

Although the granular details of the plan are not yet all worked out, the preschool proposal currently being drafted and debated in the U.S. House of Representatives mimics the Biden proposal in many ways.22 The current House proposal seems to be designed to invest the same $200 billion in federal government money for universal preschool and enroll more children, though there is a greater expectation of the states and the District of Columbia sharing the costs and for the spending to sunset after 7 years. Assuming the program does not end after 7 years, these differences in cost sharing and enrollment do not significantly change the cost-benefit analysis provided here, although they would increase the number of children enrolled and reduce somewhat the ratio of benefits-to-costs calculated in this report.

An investment in a high-quality, publicly funded preschool program will generate annual costs and benefits that will vary from year to year. To evaluate the worthiness of the investment, we compare these annually varying costs and benefits, and calculate a benefit-to-cost ratio by using the standard economic and financial method of present value with a discount rate of 3 percent.23 Present value calculates the value in today’s dollars of future costs and benefits. If the ratio of present-value benefits-to-present-value costs is greater than 1, then the benefits of the investment exceed the costs, and it makes economic sense to undertake the investment.

Total costs and benefits over the first 10 years of the preschool program

A high-quality, publicly funded preschool education program will have both long-run productivity effects and a short-run stimulus effect on the U.S. economy that will generate growing annual benefits that will surpass the more-slowly growing annual costs of the program within 8 years. That is, over the first 7 years, the present-value costs will exceed the present-value benefits, but in the last 3 years, the benefits will be greater than the costs. Over the entire 10-year period, the present-value benefit-to-cost ratio is 1.01, which means that every tax dollar invested in the preschool program will generate $1.01 in total benefits over the first 10 years.

As noted above, the annual benefits grow more rapidly than the annual costs. Thus, in the 10th year alone, the present-value benefits—in the form of government budget benefits, increased wages and earnings of workers, and reduced costs to individuals from better health, less crime, and fewer incidences of child abuse and neglect—exceed the present value costs of the program by a ratio of 1.68-to-1.

The high-quality universal preschool program would cost $6,600 per participant and could be expected to enroll about 64 percent of 3- and 4-year-olds, or just less than 5.2 million children, when it is fully phased in after 2 years. As a result, the program would have a “gross” cost of about $34.3 billion annually when it is fully phased in. Some of this money, however, is already being spent on existing public preschool programs of mixed quality.24

A fraction of the funds used to finance these existing programs—equal to the ratio of children who would attend the new, high-quality preschool instead of the existing programs—would be used to fund the new preschool program. To avoid double-counting these expenditures, they are subtracted from the costs of the new program.

The bottom line is that the proposed high-quality universal preschool program would require approximately $19.1 billion in additional annual government outlays once it is fully phased in. The annual outlays for the program will then grow with inflation and the slowly growing population of children that it serves.

The federal investment in the preschool program during the first 2 years will also have a short-run stimulus effect that will boost Gross Domestic Product by $28.6 billion and create 210,200 additional new jobs to help the economy recover from the current recession.25

Government costs and benefits over the first 10 years

The present-value government benefit-to-cost ratio is 0.47, which means that every tax dollar invested in the preschool program will generate $0.47 in budgetary savings over the first 10 years. In other words, the budgetary savings of the preschool program, in the form of higher tax revenues and lower public expenditures on several public programs, will pay for almost half the total taxpayer cost of the program during the first 10 years.

For each of the first 10 years of the universal preschool program, taxpayer costs will exceed offsetting budget benefits but by a progressively declining margin. Thus, in the 10th year of the program, the tax revenue increases and expenditure savings due to the preschool program pay for 68 percent of the program.

The offsetting government budget savings begin small but grow over time. Budget savings in the first two years of the program will manifest themselves as reductions in child welfare expenditures as fewer children will be the victims of child abuse and neglect. In addition, some parents will take advantage of the universal pre-Kindergarten program for some of their child care needs, allowing them to work more and, thus, pay more in taxes.26

When the preschool participants enter the K-12 public school system, additional government budget savings will begin to appear, as these children will be less likely to repeat a grade or need expensive special education services. When the first cohort of children turns 10, further budget savings will begin to be realized as lower juvenile crime rates will require less public expenditure on the juvenile justice system.

The government budget deficit in the 10th year is based on a cash analysis that compares the impact of net government expenditures on the program to the additional taxpayer costs engendered by the program. Thus, the estimate that the government budget benefits pay for 68 percent of the cost of the preschool program considers all the additional costs due to the program but only the additional government budgetary benefits of the program—thereby ignoring the compensation, health, crime, and other social benefits of the program that accrue to the general public.

Once these other benefits of the program are taken into account, the universal preschool program, as noted in the previous section, pays for itself. In fact, the nonbudgetary benefits in the 10th year of the preschool program are, by themselves, equal to the costs of the program. Consequently, the budget benefits could be seen as bonuses that are in addition to the other nonbudgetary benefits that justify the investment.

It would similarly be unwise to judge the merits of investments in preschool solely in terms of their 10-year effects because many costs and benefits (both to the government and the public) manifest themselves only after 10 years and are a function of the long-run productivity effects of high-quality preschool.27 Among the other quantifiable costs and benefits of preschool investment are its impact on the future costs of K-12 education, the earnings of, and taxes paid by, preschool participants, their improved health, and their fewer interactions with the criminal justice system.

To capture these longer-term effects, we extend the analysis of costs and benefits to a 35-year framework, assuming that investment in preschool continues to grow with inflation and the population of 3- and 4-year-olds grows to maintain a 64 percent enrollment rate.

Total cost and benefits over 35 years

The present-value total benefit-to-cost ratio is 4.93, which means that every tax dollar invested in the preschool program will generate $4.93 in total benefits over the first 35 years.

The annual benefits grow faster than the costs. Thus, the benefit-cost ratio improves with each subsequent year. In the 35th year, the final year of this analysis, the present value of the total benefits from government budgetary savings, increased compensation of workers, and reduced costs to individuals from better health, less crime, and reduced incidences of child abuse and neglect exceed the present-value costs of the program by a ratio of 10.20-to-1. Thus, by making this investment, we will be leaving our children and grandchildren an enormous inheritance.

By the 35th year, the long-run productivity effects of the preschool investment boost Gross Domestic Product by 0.5 percent and may generate as many as 787,000 new jobs.28

Government costs and benefits over the first 35 years

Over the entire 35-year period, the present-value government benefit-to-cost ratio is 1.51, which means that every tax dollar invested in the preschool program will generate $1.51 in budgetary benefits over the first 35 years.

Taxpayer costs exceed offsetting budget benefits but by a steadily declining margin for the first 14 years. By the 15th year of the program, budgetary benefits exceed the taxpayer costs, and the program generates a budget surplus that grows every year thereafter. In the 35th year of the program, the present-value government budget surplus amounts to $36.2 billion, with total present-value government budget benefits that exceed the present-value government costs by a ratio of 2.84-to-1.

What explains this pattern of slowly growing budgetary costs and more rapidly growing budgetary benefits? On the cost side, after the first 10 years, the costs of the preschool program continue to grow as a result of inflation and the modestly increasing population of 3- and 4-year-olds that it serves. In addition, there are increases in government expenditures due to the increased educational attainment of preschool participants who drop out of high school at lower rates and complete more years of high school and go on to public colleges and universities at higher rates.

On the benefits side, the benefits identified during the first 10 years continue to manifest themselves. There are reductions in child welfare spending due to lower rates of child maltreatment. There are increased tax revenues generated from the earnings of parents who can now work due to the newly available child care. Public education expenditures diminish due to less grade retention and less need for expensive special education. And governments experience lower judicial system costs due to less juvenile crime, starting when the first cohort of pre-Kindergarten participants reaches age 10.

What’s more, there are significant additional budgetary benefits that manifest themselves after the first decade of the program. After a decade and a half, the first cohort of children begins entering the workforce, resulting in sharp increases in earnings and tax revenues because participants in high-quality preschool earn significantly more than nonparticipants. In addition, when the first cohort turns 18, governments experience lower judicial system costs due to less adult crime and lower public healthcare costs because preschool participants have fewer episodes of depression and lower tobacco usage.

Timing of phase-in

This analysis assumes a 2-year phase-in of the proposed preschool program. For political purposes, however, such as the need to secure enough votes to enact the program, it may be necessary to have a longer phase-in period. In addition, for practical reasons, such as the recruitment and training of teachers and staff and the establishment of appropriate locations, the preschool program may have to be phased in over a longer period. A longer phase-in would push back both the costs and benefits of the program and would reduce the 10- and 35-year benefit-to-cost ratios.

Omitted benefits of universal preschool

The various benefit-to-cost ratios of preschool investment are understated in our estimates because the analysis is limited to considering only benefits for which it was possible to obtain monetary estimates. Perhaps most important in terms of omitted benefits is the potentially positive effects on the children born to preschool participants who, as parents, will have higher earnings and employment, lower incarceration rates, and better health outcomes, which were not calculated.

Preschool is an investment in the parents of the future, who, as a result of that early childhood education, will be able to provide better lives and better educational opportunities to their own children. Hence, the children of preschool participants may be able to earn more and lead better lives. If this intergenerational effect were properly accounted for, then the benefits of preschool education may be substantially larger than those estimated in this analysis.

Other benefits that could not be monetized—such as the financial savings to families who would place their children in the publicly funded program but who, in its absence, would have paid the costs of private preschool—were left out.29 Since about one-quarter of all families with 3- and 4-year-old children place their children in private preschool programs, the savings to families from the use of publicly funded preschool are potentially very large.

Other examples of omitted benefits include the value of lower drug use and fewer teenage parents, the intrinsic value of the increase in the knowledge, skills, and literacy of participants, and the potentially greater levels of happiness and job satisfaction that preschool participants will experience as adults.

If the ultimate aim of public policy is to promote the well-being of individuals, families, communities, and the nation, then investment in high-quality preschool is an effective strategy. Investing in high-quality preschool can help us achieve a multitude of social and economic objectives, including:

Strengthening economic growth

Increasing incomes

Creating jobs

Reducing poverty

Tempering inequality

Improving education

Reducing crime

Ameliorating health problems

Improving public balance sheets

Moreover, high-quality preschool helps to create the conditions that enable people to achieve their potential, live lives of dignity, and maximize their well-being.

A high-quality, nationwide commitment to universal preschool would cost a significant amount of money up front, but it would have a substantial payoff in the future. Our political system, with its 2- and 4-year election cycles, tends to underinvest in programs with lags between when investment costs are incurred and when benefits are enjoyed. The fact that governments cannot capture all the benefits of preschool investment may also discourage them from assuming all the costs of preschool programs. Yet the economic case for public investment in preschool is compelling.

The economic and social benefits from preschool investment amount to more than just improvements in public balance sheets. Investing in young children has positive implications for the current generation of children, for future generations of children, and for earlier generations of children. The current generation of children will benefit from higher earnings, higher material standards of living, and an enhanced quality of life. Future generations will benefit because they will be less likely to grow up in families living in poverty. And earlier generations of children, who are now working or in retirement, will benefit by being supported by higher-earning workers who will be better able to financially sustain our public health and retirement benefit programs such as Medicaid, Medicare, and Social Security.

In short, strengthening the economic and social conditions of our youth will simultaneously help provide lasting economic security to future generations, as well as to all of us, including our elderly.

Investing in young children has positive effects on the U.S. economy by increasing economic growth, improving the skills of the workforce, reducing poverty, and strengthening U.S. global competitiveness. Crime rates and the heavy costs of incarceration to society will be reduced. Health outcomes improve as well. Additionally, given that the positive impacts of preschool may be larger for at-risk than for more advantaged children, a universal preschool program will help to reduce achievement gaps between poor and nonpoor children, ultimately reducing income inequality nationwide. In other words, investment in high-quality preschool promotes equal opportunity and widely shared economic growth.

The long-term nature of the benefits of preschool investment suggests that policymakers should not impose the costs of the investment (through lower public services or higher taxes) only on the current generation of beneficiaries. Instead, they should spread them over the lives of the current and future generations of beneficiaries of the programs.

Public investments in the quality and quantity of education are important determinants of productivity, growth, and international economic competitiveness. They are also central to human well-being. Investing in the education and skills of our people—our most valuable resource—can immediately boost the economy, create jobs, and help lift us out of our current economic malaise, while simultaneously laying the groundwork for future growth. Investments in the cognitive skills of our people help create pathways for more rapid future growth by enhancing long-run productivity, and they reduce economic disparities by providing ladders of opportunity for all.30

The evidence is clear that one of the most effective ways to promote faster and more widely shared economic growth is to raise academic achievement and narrow socioeconomic-based achievement gaps. Investment in universal high-quality preschool does both. By raising academic achievement, it will improve well-being now and for future generations of Americans, and it will encourage long-term economic growth.

—Robert G. Lynch is the Young Ja Lim professor in economics at Washington College and was a visiting scholar at Equitable Growth from 2014–2015.

1. The stakes involved in pushing the U.S. congressional reconciliation bill to the goalposts are very large indeed. Read Alix Gould-Werth and Sam Abbott, “Congressional investments in social infrastructure would support immediate and long-term U.S. economic growth,” in which they write: “President Joe Biden’s Build Back Better agenda … boasts the potential to reshape the U.S. economy … [by] supporting workers and families with investments in care infrastructure, including a comprehensive paid family and medical leave program and increased investment in early care and education, as well as income supports, such as a permanent fully refundable Child Tax Credit and structural reforms to the Unemployment Insurance program. Common sense, as well as a robust body of research, suggests these investments would improve workers’ and families’ personal well-being, especially for families of color. …. But policymakers should not lose sight of the economywide impact these investments will have as well.”

2. This will, I think, be Equitable Growth’s best policy conference yet—if only because the United States now has huge amounts of running room given the chaos caused by the coronavirus pandemic and by the ongoing disruptions to U.S. politics I believe its aftermath is likely to bring. Read Maryam Janani-Flores, Kate Bahn, and Carmen Sanchez Cumming, “Equitable Growth’s 2021 policy conference features key speakers and panelists discussing inclusive U.S. economic growth after the coronavirus recession,” in which they write: “More expansive, more transformative, and more equitable economic policies have helped power a far more rapid recovery, compared to the years following the Great Recession. … Our virtual policy conference … [features] pathbreaking leadership and cutting-edge scholarship that recognizes how a stronger economic future is built on the linkages between racial justice, climate resilience, access to care and family economic security, financial stability, and rebalancing power, so that all can share in the gains of economic growth. Headlining the conference in a series of fireside chats and remarks are the new Equitable Growth President and CEO Michelle Holder, U.S. Secretary of Labor Marty Walsh, U.S. Rep. Hakeem Jeffries (D-NY), Michigan State University economist and Equitable Growth Steering Committee member Lisa Cook, University of California, San Diego assistant finance professor Carlos Fernando Avenancio-León, and Marketplace host and correspondent Kimberly Adams.”

Worthy reads not from Equitable Growth:

1. That technological disruption affects U.S. workers already in declining industries but does not harm the prospects of future entrants may be a durable lesson from the past of technological disruption and change. Read James Feigenbaum and Daniel P. Gross, “Automation and the Future of Young Workers: Evidence from Telephone Operation in the Early 20th Century,” in which they write: “Telephone operation, one of the most common jobs for young American women in the early 1900s, provided hundreds of thousands of female workers a pathway into the labor force. Between 1920 and 1940, AT&T adopted mechanical switching technology in more than half of the U.S. telephone network, replacing manual operation. Although automation eliminated most of these jobs, it did not affect future cohorts’ overall employment: the decline in demand for operators was counteracted by growth in both middle-skill jobs like secretarial work and lower-wage service jobs, which absorbed future generations. Using a new genealogy-based census linking method, we show that incumbent telephone operators were most impacted by automation, and a decade later were more likely to be in lower-paying occupations or have left the labor force entirely.”

2. The point of Critical Race Theory: don’t make African Americans poor and excluded from networks, keep them poor and excluded from networks, then discriminate against the poor and those excluded from networks, and claim that you are not then discriminating on the basis of race. Read Noah Smith, “The Negro Subversive on Critical Race Theory,” in which he writes: Critical Race Theory’s founders sought to understand how a society that had officially disowned racism managed to continue being racist. … To understand how law impacts society, we must understand how law exists in society, which means applying insights from … the social sciences. … What all three social objects under the name “Critical Race Theory,” have in common is the idea of politicizing the allegedly apolitical. … The social sciences … rose in the midst of various national projects and served to justify them. Their (very incomplete) transition away from this heritage has traced an arc similar to their growth toward greater objectivity. The legacy of this transition continues, as the social sciences both reflect and condition how the public thinks about society. The fault lines of the critical race theory “debate,” reflect the fault lines early social science practitioners faced as they developed their disciplines out of “social philosophy,” into social science. Recognizing that these faults still condition our thinking about the social world is crucial to recognizing what’s at stake right now.”

This is a post we publish each Friday with links to articles that touch on economic inequality and growth. The first section is a round-up of what Equitable Growth published this week and the second is relevant and interesting articles we’re highlighting from elsewhere. We won’t be the first to share these articles, but we hope by taking a look back at the whole week, we can put them in context.

Equitable Growth round-up

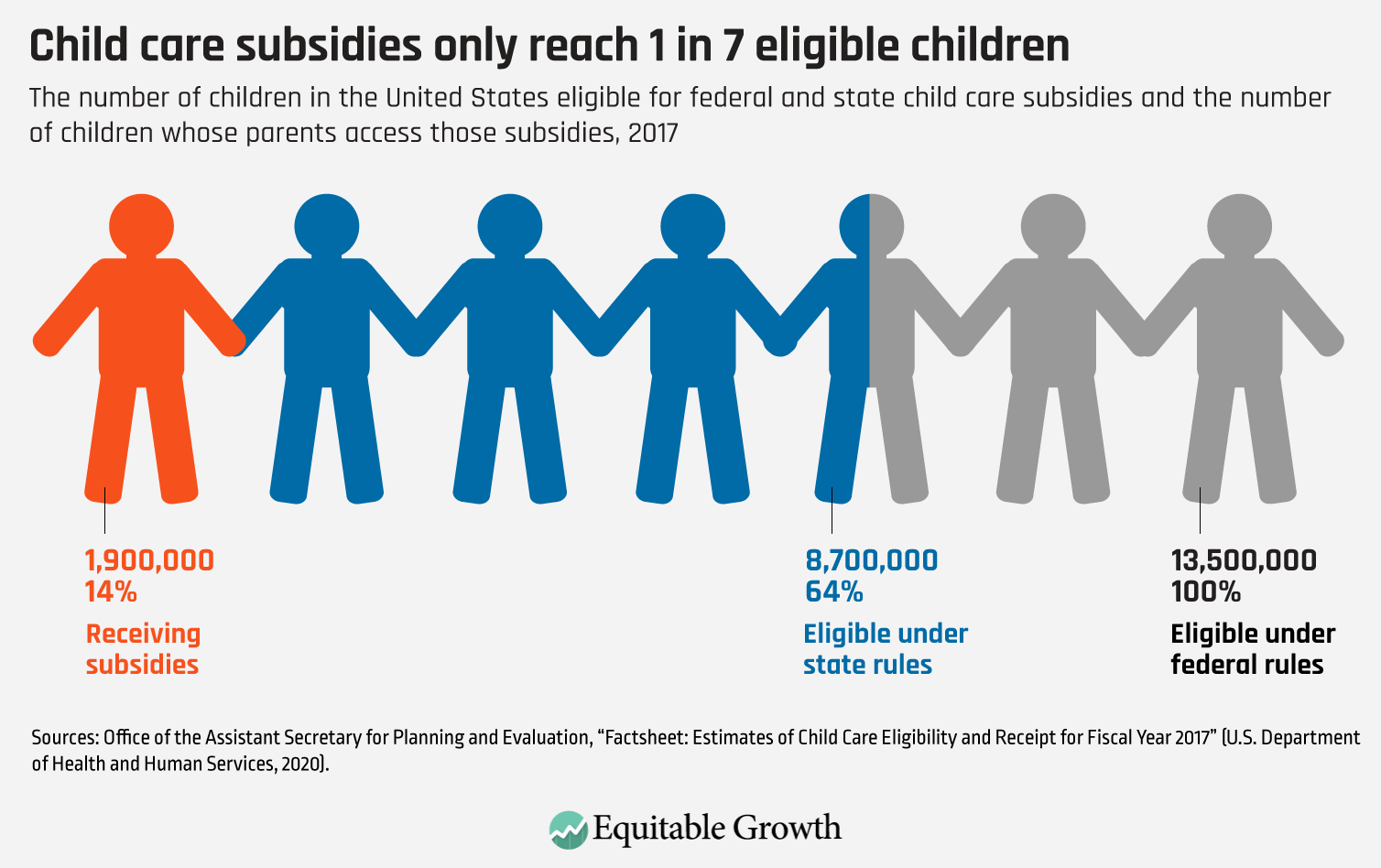

Despite the essential role that child care plays in the lives of U.S. workers and their families, the current child care market in the United States is not meeting families’ needs. This not only impacts families themselves, but also the overall economy, as high-quality care has far-ranging impacts on economic activity and growth. Sam Abbott explains why public investments are needed in early care and education to support immediate and long-term economic growth, as well as bolster human capital development in the next generation of workers. He then details how public investments in particular can offset deficiencies in the private child care market and support child care workers, who play a vital role in the U.S. economy. These investments, he concludes, are some of the best bets policymakers can make, with research showing that every dollar in spending on early care and education generates more than $8 in economic activity. Accompanying Abbott’s report is a factsheet laying out what the economic research has found about the impacts of child care and early childhood education on the U.S. economy.

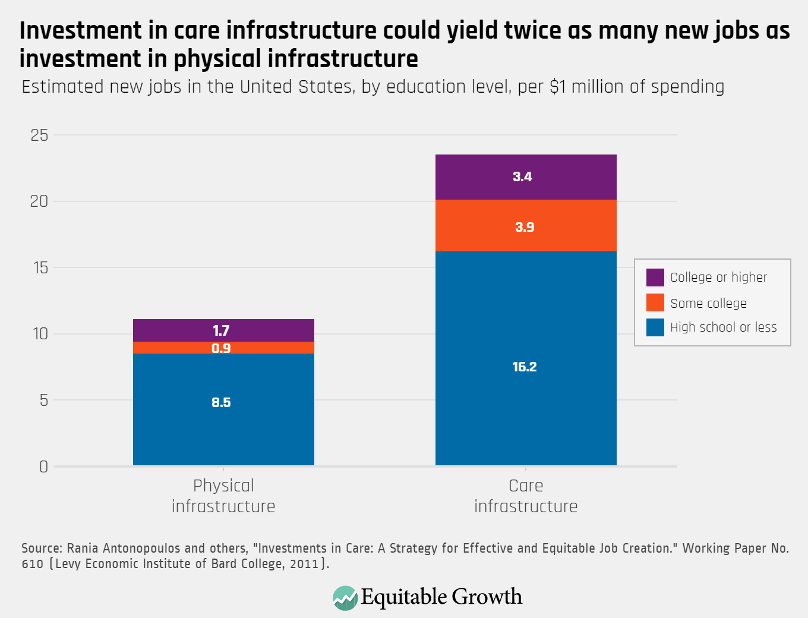

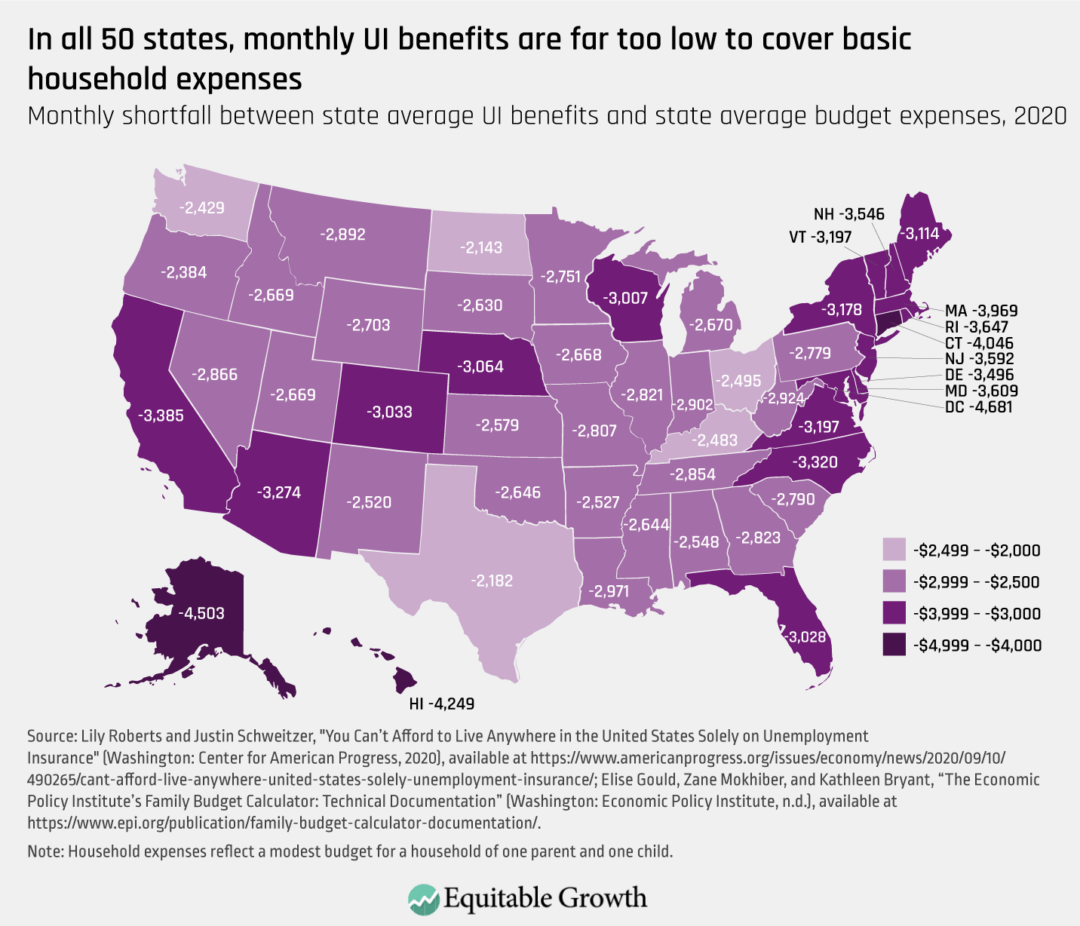

Policymakers should also seize the opportunity in the current 2022 budget reconciliation negotiations to invest in U.S. social infrastructure, Abbott and Alix Gould-Werth write. Much like investments in early care and education, they explain, increasing spending on other social infrastructure and income support programs would give a much-needed boost to the overall economy in addition to supporting those workers and families most in need. The co-authors detail recent economic findings about the role of care infrastructure, paid family and medical leave, early care and education, and income supports in ensuring strong, stable and broadly shared economic growth. As the United States emerges from the greatest health, economic, and caregiving crises in decades, they conclude, Congress should boost public investments in these critical programs to correct years of neglect and underinvestment.

Though some policymakers are fearful of making these investments due to overblown fears of increasing the national debt, University of California, Berkeley’s Barry Eichengreen urges them to ignore the deficit fearmongering on Capitol Hill. Detailing arguments from his new co-authored book, In Defense of Public Debt, he shows how governments throughout the years have issued public debt to address emergencies and pressing social needs, and makes the case that our current conditions demand similar action. Not only is our current physical infrastructure crumbling due to decades of underinvestment and the heightened threat of climate change, but social infrastructure programs are also far behind where they should be. Eichengreen effectively rebuffs the critiques of President Joe Biden’s Build Back Better agenda and encourages policymakers to pass it while they have the chance.

Equitable Growth is hosting its biennial policy conference on Monday and Tuesday. The virtual event, “Equitable Growth 2021: Evidence for a Stronger Economic Future,” will gather policymakers, academics, activists, and thought leaders to discuss pressing economic issues and policy solutions. (Click here to register.) The first day of sessions will feature a keynote address from U.S. Secretary of Labor Marty Walsh and a conversation between Equitable Growth President and CEO Michelle Holder and Michigan State University’s Lisa Cook. Maryam Janani-Flores, Kate Bahn, and Carmen Sanchez Cummingdetail the sessions on day 2, and highlight speakers who will participate in panel sessions on topics such as envisioning a new economic future, rebalancing Big Tech’s grip on the economy, boosting aggregate demand and managing debt burdens, and social infrastructure as an engine for economy growth. The September edition of Expert Focus—Equitable Growth’s monthly series highlighting scholars at the forefront of economic and social science research—also showcases featured speakers from this year’s policy conference.

New research examines the value of racial and gender diversity at the Federal Reserve. As the Federal Open Market Committee meets next week, the 12-member body should consider the findings of a working paper published this week by Francesco D’Acunto at Boston College’s Carroll School of Management, Andreas Fuster at the Swiss Finance Institute, and Michael Weber at the University of Chicago’s Booth School of Business. The co-authors study the influence that the race and gender of FOMC members has on public perception and trust of their opinions on inflation and Unemployment Insurance. They find that Black men and women, as well as White women, are more likely to align their economic expectations with those of FOMC members from diverse backgrounds, while White men and Hispanic respondents trusted FOMC members regardless of race or gender. The research highlights the importance and salience of diversity and representation at the highest levels of policymaking and decision-making—as well as the current and historical lack of non-White male economists at the Fed and within the field more broadly.

Links from around the web

A new U.S. Treasury Department report says that the nation’s child care system is failing families, reports CNBC’s Ylan Mui, finding that market failures keep high-quality and affordable care out of reach for many families. Similar to the Equitable Growth report released this week, the Treasury report details the challenges many families face in finding affordable, accessible, and quality care options for their children and examines the often poor working conditions that many child care workers experience, from low pay to high stress. The Treasury report also recommends policymakers pass President Biden’s Build Back Better agenda. Mui runs through the details of the Treasury report, interviewing several policymakers and previewing the next steps in Congress.

Unions can play a major role in wealth building and bridging the wealth divide between families of color and their White counterparts, write Aurelia Glass and David Madland in an op-ed published in The Hill. They detail the findings of a recent analysis they and a co-author, Christian Weller, performed on Federal Reserve data from the Survey of Consumer Finances. While unions alone are not a silver bullet, they allow families to make significant gains in growing wealth and establishing more financial security. Their study finds that “the median union family has over double the wealth of the median nonunion family” and that “the wealth gap between white families and Black and Hispanic families was significantly smaller for union households compared to nonunion households.” This, they explain, has significant implications for President Biden’s plan to rebuild the middle class, which is currently shrinking and out of reach for many U.S. households.

The coronavirus pandemic has disrupted the trajectories of millions of college students in the United States. Men make up the majority of drop-outs, according to some estimates—but, Kevin Carey writes in The New York Times’ The Upshot, women are still playing catch up in the U.S. economy. The college gender imbalance is not a new phenomenon, as women have outnumbered men on campuses for decades. Carey details the data on gender disparities in college and beyond, noting that despite higher female enrollment at universities, the gender pay gap is still pervasive across the U.S. labor force.

Inflation is on everyone’s mind. NPR’s Scott Horsley reports that high meat prices are contributing to inflation and that concentration in agriculture and meatpacking could be to blame. Horsley details the Biden administration’s efforts to target what they call “Big Meat,” in their campaign against anticompetitive behavior and market dominance. The administration’s goal, he writes, is to restore competition in the U.S. meatpacking and processing industry—in which more than 80 percent of beef is slaughtered and processed by just four companies—which would work in consumers’ favor by lowering prices.

The coronavirus pandemic and resulting historic economic and societal shock revealed underlying systemic fragility driven by longstanding economic inequalities and structural racism. More expansive, more transformative, and more equitable economic policies have helped power a far more rapid recovery, compared to the years following the Great Recession of 2007–2009. But now, the coronavirus pandemic is surging anew while most of those underlying structural fragilities exacerbated by the coronavirus recession, as well as ongoing consequences of climate change, remain exposed and raw.

These economic policy challenges provide an opportunity for policymakers to rebuild a more resilient and inclusive U.S. economy and society. In a nutshell, this is what is on our agenda at our virtual policy conference, “Equitable Growth 2021: Evidence for a Stronger Economic Future,” on Monday and Tuesday, September 20–21.

The Washington Center for Equitable Growth, over the course of these 2 days, will examine the progress to date in building a resilient and inclusive economy and the needs for the future by bringing together policymakers, academics, advocates, and thought leaders. The remarks and sessions at the conference will highlight pathbreaking leadership and cutting-edge scholarship that recognizes how a stronger economic future is built on the linkages between racial justice, climate resilience, access to care and family economic security, financial stability, and rebalancing power, so that all can share in the gains of economic growth.

Headlining the conference in a series of fireside chats and remarks are the new Equitable Growth President and CEO Michelle Holder, U.S. Secretary of Labor Marty Walsh, U.S. Rep. Hakeem Jeffries (D-NY), Michigan State University economist and Equitable Growth Steering Committee member Lisa Cook, University of California, San Diego assistant finance professor Carlos Fernando Avenancio-León, and Marketplace host and correspondent Kimberly Adams. Notable panelists are featured in our four panel sessions, taking place in two concurrent blocks on the second day of the conference, focused on the key economic questions of the day.

Equitable Growth 2021: Evidence for a Stronger Economic Future

Below is a preview of the second day of conference and our featured panelists and moderators in the upcoming sessions, as well as their relevant work and experience that will be brought to bear during these discussions. And here is a complete agenda and details about attending the conference.

Concurrent sessions: Block 1

Envisioning a new economic future: What’s next?

Tuesday, September 21, 2:05 p.m. – 2:50 p.m.

As U.S. communities and the economy recover from the coronavirus recession, there is an opportunity to build a new economic future defined by investment centered on racial equity and climate mitigation and adaptation. This requires re-envisioning industrial, labor, and macroeconomic policies and redefining economic success beyond aggregate statistics. Panelists will discuss how to leverage deficits to invest in a green future and build broadly shared and sustainable economic growth while ensuring Black, Latinx, Indigenous, and Asian American, Native Hawaiian, and Pacific Islander communities can fully benefit from any such investments.

The panelists are:

Olivier Blanchard, the Robert Solow professor emeritus at the Massachusetts Institute of Technology and the Fred Bergsten senior fellow at the Peterson Institute for International Economics. He is a macroeconomist and has worked extensively on issues including monetary and fiscal policy, labor markets, and the recent global financial crisis. When the coronavirus pandemic hit, French President Emmanuel Macron asked Blanchard, as a leader in the field of macroeconomics, along with Jean Tirole, to chair a commission and write a report on the major structural challenges societies will face in the aftermath of the pandemic, as well as policy solutions to address them. These challenges include climate change, economic inequality and insecurity, and economic disruptions stemming from demographic changes.

Dania Francis, an assistant professor of economics at the University of Massachusetts Boston. She studies the structural causes behind racial and socioeconomic achievement divides. Francis’ work includes analyses and research-based policy recommendations for implementing a reparations program for the descendants of enslaved African Americans, economic inequality and the digital divide, school racial segregation,and the link between racial, mental health, labor market, and educational disparities. Her work demonstrates how addressing racial divides are core to addressing the structural challenge imposed by economic inequality.

Brenda Mallory, the chair of the White House Council on Environmental Quality. She has worked alongside academics and in a number of senior roles in public office to advance environmental protections for low-income and communities of color. In her current role, Mallory advises President Joe Biden on policies that foster public health, environmental justice, and the resiliency of U.S. communities to the effects of climate change and natural hazards such as floods and sea-level rise and hurricanes, as well as the best practices to develop carbon capture, utilization, and sequestration projects.

Michelle Holder, president and CEO of the Washington Center for Equitable Growth, will moderate the panel.

Rebalancing Big Tech’s grip on the economy

Tuesday, September 21, 2:05 p.m. – 2:50 p.m.

From digital marketplaces to invasive worker surveillance, tech companies play an outsized role in the everyday lives of U.S. workers and their families while evading sufficient scrutiny and providing few consumer and worker protections. Dominant tech platforms stifle innovation and hinder entrepreneurship opportunities, and ubiquitous and invasive management tools risk exacerbating longstanding inequities for workers. Panelists will discuss how sound policy, coupled with a strong, organized advocacy strategy, are needed to manage technological integration so the gains from these advancements are fairly distributed, spurring competition and broadly shared economic growth.

The panelists are:

New York Attorney General Letitia James, who is at the forefront of tackling anticompetitive behavior in the technology industry. James will provide opening remarks to the panel. She has led multipleantitrustsuits that allege monopolistic behavior by tech giants, including the acquisition of smaller rivals and other activities that limit competition by other players in the ecosystem.

Antoine Prince Albert III, the government affairs policy counsel at Public Knowledge, a tech-focused think tank. He examines what policymakers are doing and can do when it comes to fostering online platform governance and competition, as well as addressing privacy concerns, with a recent detailed piece on how Congress is approaching these issues. Albert has explored questions related to how technology functions within Black, Latino, and Indigenous communities in the United States, which helps illuminate how technology integration and oversight influences different communities and interacts with people’s social and economic lives.

Ryan Gerety, a senior advisor to United for Respect, an advocacy organization for retail workers. She focuses on the economic and political implications of new technology and its impact on structural inequality. Gerety has also explored the issue of workplace technologies, such as face recognition, worker surveillance, and just-in-time scheduling, as worker monitoring and discipline tools that disproportionately harm Black, Indigenous, and other people of color.

Fiona Scott Morton, the Theodore Nierenberg professor of economics at the Yale University School of Management. She is renowned for her research on competition in the areas of pricing, entry, and product differentiation. In a piece for Equitable Growth, Scott Morton wrote about the importance of antitrust enforcement for economic redistribution and proposed policies for the U.S. Congress and the Biden administration to adopt that confront market power, including in the technology industry. She also has explored the importance of an interoperability remedy in the technology industry to address entry barriers created by network effects.

Lydia DePillis covers economic policy for ProPublica and will moderate the panel.

Concurrent sessions: Block 2

Boosting aggregate demand amid decreased debt

Tuesday, September 21, 2:55 p.m. – 3:38 p.m.

The relief and recovery efforts following the coronavirus recession offset the financial hardship that families in the United States often face in economic contractions and averted a long-term aggregate demand shock. But the sharp recession and ongoing pandemic came after decades of rising income inequality, featuring wealthier households saving more while most households leveraged debt to sustain demand. This session will dive deep into who takes on debt and how different households along the income distribution spend and save, influencing aggregate demand and U.S. macroeconomic stability. Coming out of a unique economic crisis featuring broad-based relief to families, but against a backdrop of inequality and a continuing pandemic, panelists will discuss the opportunities that will lead to a more stable future for families and the U.S. macroeconomy.

The panelists are:

Kristen Broady, a fellow at the Brookings Institution’s Metropolitan Policy Program and professor of financial economics on leave from Dillard University in New Orleans. Her research includes an exploration of mortgage foreclosure risk, and she recently wrote that, with the expiration of the Centers for Disease Control’s rental eviction moratorium, a looming eviction crisis will hit Black-majority neighborhoods the hardest. She has also explored how the Black-White wealth gap, coupled with labor market disparities, left Black households more vulnerable to the pandemic’s economic shocks, which provides insight into the path forward for maintaining aggregate demand through centering policymaking on the economic well-being of historically excluded communities.

J.W. Mason, an associate professor at John Jay College, City University of New York and fellow at the Roosevelt Institute. He has written on issues of government debt and household debt. In his paper titled, “Income Distribution, Household Debt, and Aggregate Demand: A Critical Assessment,” he finds that income inequality, household debt, and aggregate demand were closely linked during the housing boom period of 2002–2007, but that those linkages are not as clear following the post-1980 rise in household debt.

Atif Mian, the John H. Laporte, Jr. Class of 1967 professor of economics, public policy, and finance at Princeton University and director of the Julis-Rabinowitz Center for Public Policy and Finance at the Princeton School of Public and International Affairs. Mian, a member of Equitable Growth’s Steering Committee, has proposed a theory of indebted demand, resulting from rising income inequality and financial deregulation, that leads to lower aggregate demand. This research follows the argument in his book, House of Debt, co-authored with Amir Sufi at the University of Chicago, which finds that a significant increase in household debt and then drop in household spending caused the Great Recession and Great Depression.

Bharat Ramamurti, the deputy director at the White House National Economic Council. He focuses on financial reform and consumer protection and also has worked on pandemic support for smallbusinesses, as well as assessing the consequences for consumers from consolidation in the meat processing industry. Ramamurti previously served as the chief economic advisor and senior counselor on banking to Sen. Elizabeth Warren (D-MA), with a focus on the financial reforms that came out of the Great Recession.

Social infrastructure as an engine for equitable growth

Tuesday, September 21, 2:55 p.m. – 3:38 p.m.

Policy debates on infrastructure spending following the coronavirus pandemic pushed forward our collective understanding of the importance of social infrastructure investments such as child care and the Child Tax Credit, early education, community-based services and support for older adults and people with disabilities, paid sick time, paid leave, and Unemployment Insurance. These social infrastructure programs are core to the health and stability of the U.S. economy. Investments in social infrastructure reap benefits for the families of today and into the future, especially families of color. Panelists will explore potential economic impacts of these investments with a focus on the specific policy levers that will yield significant increases in labor force participation and productivity.

The panelists are:

Hilary Hoynes, a University of California, Berkeley professor of public policy and economics. Her research focuses on social infrastructure programs, including food and nutrition programs, as well as government tax and transfer programs for low-income families, which form the floor of our social infrastructure. She has authored research that shows that social infrastructure is a long-term investment in our children, based on an evaluation of the food stamps program from 1961 to 1975. She has also written about strengthening the Supplemental Nutrition Assistance Program as an automatic stabilizer in economic downturns, in the Equitable Growth-Hamilton Project co-published book Recession Ready.

Shilpa Phadke, special assistant to the president and deputy director at the White House Gender Policy Council, which covers a range of issues, including economic security, with a focus on gender equity and equality. In her work, Phadke has written about the pandemic’s impact on economic inequality and the caregiving crisis, particularly experienced by women of color, who felt the brunt of the shock of the pandemic, highlighting anew the need to invest in social infrastructure that centered the role of caregiving and gender equality as a priority for a new economic policy agenda in the recovery.