Collective bargaining as a path to more equitable wage growth in the United States

This essay is part of Boosting Wages for U.S. Workers in the New Economy, a compilation of 10 essays from leading economic thinkers who explore alternative policies for boosting wages and living standards, rooted in different structures that contribute to stagnant and unequal wages. The authors in the new book demonstrate that efforts to improve workers’ access to good jobs do not need to be limited to traditional labor policy. Policies relating to macroeconomics, to social services, and to market concentration also have direct relevance to wage levels and inequality, and can be useful tools for addressing them.

To read more about Boosting Wages for U.S. Workers in the New Economy 20 and download the full collection of essays, click here.

Overview

Rising wage inequality in the United States means that the median wage has not kept pace with the mean wage in recent decades. Moreover, the United States has performed worse in this regard than many of its international peers. In this essay, I will first examine the decoupling of median wage growth from mean wage growth and, in turn, the decoupling from productivity growth, in the United States and in its peer countries in the Organisation for Economic Co-operation and Development.

I will then consider the role of collective bargaining institutions in these patterns. One plausible important factor underlying the greater divergence between mean and median wages in the United States, compared to other OECD countries, is the continued decentralization of wage-setting institutions such as labor unions that otherwise would empower the majority of workers to negotiate more effectively with employers for higher pay. Hence, policies that increase the scope of collective bargaining may be promising levers toward more equitable wage growth, albeit with some risk of reductions in economic performance.

Finally, I will review policies the United States could pursue that have the potential to foster more equitable wage growth. Specifically, U.S. policymakers can consider the introduction of industrywide and cross-industry wage boards to set minimum wages for workers in the middle rungs of the wage distribution, not just those on the lower rungs as happens under current federal and state minimum wage provisions. These wage-setting proposals are especially important today amid the coronavirus recession, which has led to a uniquely slack labor market among many segments of the economy and has hurt the bargaining position of many low-wage workers in particular. Without strong and sustained wage growth that is broadly distributed across the U.S. labor force, the eventual economic recovery will almost certainly take longer to reach the vast majority of U.S. workers.

The decoupling of wage growth and productivity growth: Mean vs. median wages

Growth in mean wages (the average of all wages; taking the sum of all wages earned, from the lowest-paid to the highest, and dividing that sum by the number of workers) has remained tightly linked with productivity in the United States and most OECD countries. In contrast, growth in median wages (the midpoint of all wages; if one were to rank all workers by their wage and then pick the worker ranked in the middle) has decoupled from productivity growth, as well as mean wage growth.

This divergence between mean and median wage growth reflects greater wage inequality. Together, these facts demonstrate that the distribution of income among U.S. employees has become increasingly unequal, even though on average, wages have held up well with productivity growth.

The United States experienced a more dramatic decoupling of median wages from mean wages and productivity than most OECD countries. The perhaps most extreme reflection of this decoupling is the fact that the annual compensation of chief executive officers in the United States rose by more than 1,000 percent between 1978 and 2017, compared to 11 percent for private-sector workers, after accounting for inflation.1

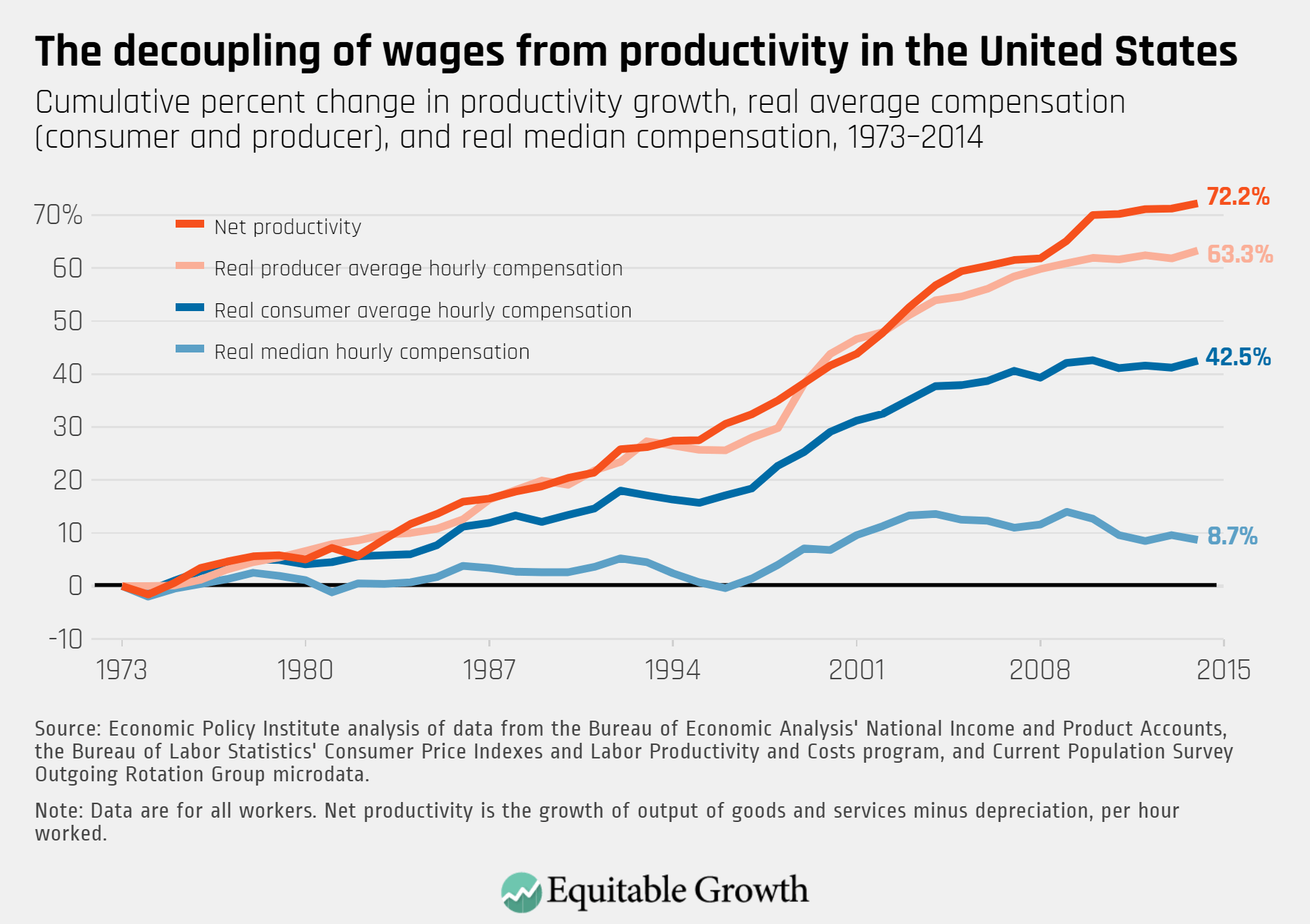

As noted above, a striking fact about the U.S. labor market is the decoupling between median wage growth and productivity growth in recent decades. U.S. labor productivity (real output per hour worked) increased by 72 percent from 1973 to 2013, yet median real wages have barely increased—by only around 8.7 percent—over the same period.2 (See Figure 1.)

Figure 1

At first glance, this divergence may suggest an increase in employer power and a decrease in workers’ bargaining power as the culprit. However, there are three observations that caution against the growth of employer power or workers’ declining bargaining power in general as the predominant culprit underlying the decoupling of overall wage growth from productivity growth.

First, a large share of the gap between wage and productivity growth is due to the different price indices used to deflate the productivity time series and the median wage. The difference between these two price indices is unrelated to wage-distribution issues.

Second, the mean wage—which reflects the wages received by all workers, rather than just the typical worker in the middle of the wage distribution—has held up quite tightly with productivity growth. The mean wage has increased by 42.5 percent, compared to only 8.7 percent for median wages. In other words, productivity increases have benefitted workers in general even as the median worker has lagged behind. This link is also evident in the tight correspondence between year-to-year growth in average labor productivity (real output per hour) and real average compensation per hour. (See Figure 2.)

Figure 2

Finally, the overall share of national income paid out in the form of labor income has fallen only modestly over the past 50-plus years. While indeed this share has fallen over the past five decades, the wage gain from returning it to the levels of the 1970s, with no offsetting effect on Gross Domestic Product growth, would entail either a moderate one-time boost to wages of around 5.8 percent or, roughly, a boost to wage growth by 0.1 percent over 50 years if spread out between 1970 and today.3 (See Figure 3.)

Figure 3

This is because until the 1970s, the U.S. labor share had been relatively stable, holding at around 65 percent of the national output. Over the past four decades or so, this labor share declined to just less than 60 percent. This small reduction in labor share corresponds to the small gap between productivity growth and mean wage growth at producer prices, as depicted in Figure 1.

Hence, these three observations on wage growth and productivity growth make clear that the first-order development in U.S. wages has been the decoupling between mean and median wages, reflecting a shift toward a more unequal distribution within labor—meaning between workers, rather than between labor overall and capital.

An international perspective on the decoupling of wage and productivity growth

Additional insight can be gained by taking an international perspective to gauge potential causes and mediating factors of the evolution of median and mean wages in the United States. Such an international comparison reveals that, in terms of median versus mean wage growth, the U.S. economy performed particularly unequally. (See Figure 4.)

Figure 4

Across most of the OECD economies, the median wage has not lagged behind productivity and average wages as much as in the United States. Quantifying the particularly unequal performance of labor income in the United States, Figure 4 shows that the median-to-mean ratio has widened four times as much in the United States than on average in the OECD, even as the gap between average wages and median wages has widened in many countries within the more limited time period between 1995 and 2013.

This insight is evident by plotting wage growth not just for the median wage but also for the lowest 10 percent of the wage distribution and the top 10 percent of the wage distribution. The wage growth of these segments of the earnings distribution exhibits tremendous heterogeneity between OECD countries other than the United States.4 (See Figure 5.)

Figure 5

Even though the United States experienced a very significant decoupling of top earners’ wages from median wages in recent years (as seen in Figure 5) and the most dramatic drop in the median-to-mean wage ratio, there are several OECD countries that also performed unequally in their wage growth evolution. During the same period depicted in Figure 5, Germany’s bottom percentile of wage earners witnessed its greatest decline in rates, while France’s bottom percentile actually outperformed its top-tier counterparts in wage growth.

These countries also experienced the decoupling of wages and productivity growth. While Figure 4 clarified that Germany had a more pronounced divergence of mean wage growth from median wage growth than France, that basic statistic actually masks the dramatic opposite relative evolution of wage growth at the bottom and top in these two countries. These are telling heterogeneous performances in equitable wage growth with differential evolutions of wage-setting institutions. (See Figure 6.)

Figure 6

The upshot is that the U.S. economy is not the only one dealing with wage inequality. That said, some OECD nations display less wage inequality and more wage compression than others, giving U.S. policymakers some points of comparison for potential sources and policy remedies.

The role of collective bargaining in equitable wage growth

To better understand trends in wage inequality, it is useful to introduce the concept of wage compression. At the level of a single firm, wage compression describes a situation in which wages are compressed in a way that need not reflect the distribution of workers’ productivity or market wages. Firms that pay similar wages to differently productive workers exhibit wage compression. In contrast to standard economic theories of a worker’s market wage reflecting her productivity, wage compression at the firm level is pervasive in real-world labor markets.5

Introspection makes this clear. About whom would your employer worry more: someone who is quitting and is among the highest-paid and most productive workers at your firm? Or, instead, someone who is quitting but is among the lowest-paid and least productive workers at your firm? Rather than being indifferent, as would be predicted if wages equaled one’s productivity or if both workers’ wages were higher than their respective productivity by the same amount, the answer is likely that your employer would worry more about the more productive type of worker quitting. This kind of wage compression—the deviation of wages from productivity—is usually relevant when examining microeconomic, firm-level wage-setting trends and decisions.

Wage compression can also exist at the macroeconomic level, however. In this case, wage compression does not solely reflect decisions of individual actors within specific firms, but additionally reflects broader labor market institutions, such as minimum wages or sectoral collective bargaining.

It remains an open question which factors explain the differences in the gap between the growth in mean wages and median wages across countries, and specifically which policy factors may have been mediating or causal factors. Still, formal institutional factors in wage setting have emerged in the research literature as a plausible key explanation of the heterogeneity of the evolution of this median-mean wage gap—specifically those institutional factors that lead to wage compression.

One piece of evidence for the important role of these institutions is the dramatic decoupling in Germany, which arguably reflects the contemporaneous decline in sectoral bargaining toward an environment with more decentralized wage setting.6 In Germany, firms increasingly opted out of or did not opt into collective bargaining agreements. This argument is consistent with the increased dispersion in the wages that different firms pay to similar employees in Germany, which has accounted for a large share of the increase in pay inequality.7

In contrast is the French experience, where median wages have held up well, with average wages and productivity trends more tightly linked, arguably due to policy choices that have maintained sectoral collective bargaining.8 Similarly, a recent OECD report substantiates these international insights, documenting that more centralized wage setting is associated with lower wage dispersion, and also documenting an association with the link between wage growth and productivity growth.9

Taking a broader view, the University of Massachusetts Amherst economist Arindrajit Dube reviews the Australian context, where collective bargaining covers around a third of the workforce. For around a quarter of the Australian workforce that is otherwise not covered by collective bargaining, wage floors are still set predominantly by industry, skill, and experience group, with some set by occupation. Dube presents a fascinating graph that shows that Australian mean and median wages grew strikingly similarly.10 (See Figure 7.)

Figure 7

Given the rarity of macroeconomic experiments, empirical evidence at the macroeconomic level on its own must often remain tentative. Yet microeconomic empirical evidence at the level of individual firms or workers sheds light on how centralized wage setting affects wage setting across the broader economy and may specifically further wage compression, which could realign median wages with productivity and mean wages. Importantly, survey evidence and case studies indeed suggest that unions establish fairness norms and pursue wage compression.11

A fascinating puzzle piece to the role of collective wage setting in wage compression is the new study of a unique 2011 reform of public school teachers’ collective bargaining agreements that decentralized wage setting in Michigan.12 Focusing on the gender pay divide, economists Barbara Biasi of the Yale School of Management and Heather Sarsons of the Chicago Booth School of Business document a sharp increase in wage inequality on this gender dimension, reflecting an increase in bilateral, flexible bargaining that resulted in a greater pay gap between male and female teachers with the same credentials, especially among younger teachers.

Central bank economist Ernesto Villanueva at the Banca de España also reviews the evidence on extensions of collective bargaining agreements to otherwise uncovered firms and highlights the effect on more equal wages.13 He finds extending collective contracts reduces wage inequality and reduces gender wage gaps, as otherwise uncovered firms are mandated to raise their wages to the mandated minimum wages set by the collective bargaining agreement.

A cost of compressing wages through collective bargaining is the potential negative effect on employment. Researchers have attributed the time series of Germany’s growing employment rate to the decline in collective bargaining (and the associated increase in wage inequality), compared to other European countries that traded low employment for more wage compression.14 Pedro Martins at Queen Mary University of London has drawn on quasi-experimental evidence to document that extending collective bargaining agreements to more firms in Portugal came at the cost of lower employment.15

Other researchers link regional disparities in employment rates with nationally binding collective bargaining agreements, a geographical dimension of wage compression across regions in which productivity may be very different.16 This finding indicates that rigid nationwide contracts contribute to regional imbalances and have greater aggregate costs to workers’ earnings and employment levels, compared with systems that allow more local-level bargaining.

Banca de España’s Villanueva also discusses the trade-off between wage compression from more centralized wage setting in the form of extended collective bargaining agreements.17 He finds that while collective contract extensions benefit job quality and wages, they can lower overall employment, particularly in otherwise-uncovered, low-wage firms. Indeed, other research finds that extended collective bargaining agreements can be used as anticompetitive measures by dominant firms to drive out competitors.18

Potential policy routes for the United States

A U.S.-focused discussion of the role of collective bargaining to foster more equitable wage growth is difficult. Indeed, collective bargaining receives relatively little attention in recent labor economics research. One case in point is the Chicago Booth IGM Forum, which frequently polls prominent economists on a diverse and large set of economic policy debates and has not featured any instances of questions on collective bargaining, unions, and centralized wage setting.

Indeed, the reality of the U.S. context is the continued decentralization of wage setting in the form of the decline of unionization.19 This trend is accompanied by an increase in between-firm wage inequality.20 These two factors broadly mirror the trends in countries where the decentralization of wage setting is believed to have played a crucial role in the growth of wage inequality, such as in Germany.

Moreover, the firm-specific effects on wages of firm-level unionization that characterize U.S. industrial relations suggests no, or no large, wage gains on average.21 Indeed, there is little empirical evidence for any firm-specific form of worker organization to measurably raise firm-level wages, reduce wage inequality, or raise the share of profits going to workers at the firm level.22

Overall, then, rather than firm-level bargaining, pursuing progressive wage compression through above-the-firm-level collective bargaining—such as at the sector level or regional level—may be the most effective focus for labor policymakers in the United States who are interested in policies that achieve wage compression.

Unlike in many OECD countries, the U.S. labor relations system lacks a formal mechanism for sectoral collective bargaining or to mandate the extension of existing collective bargaining agreements to an entire labor market.23 The main tool for wage-setting regulations are federal and local minimum wage legislation. Yet by their very nature, minimum wages are unsuitable to tackle wage stagnation among the majority of U.S. workers because they affect, at most, the bottom fifth of wage earners.

In contrast, consider the “30,000 minimum wages”—the title of the aforementioned paper by Queen Mary University of London’s Martin—for those workers even in the middle of the wage distribution that are provided by sectoral collective bargaining agreements, such as in Portugal.24

In an intriguing essay, U-Mass Amherst’s Dube sketches the economics of a wage-setting institution for the United States resembling the Australian setup of wage “awards,” discussed above.25 Dube’s proposal would extend granular wage floors by industry, skill, and experience level to workers otherwise not covered by collective bargaining agreements. In a 2020 essay for the Washington Center for Equitable Growth, Dube further details why “wage boards” are a U.S. institution that may mimic these functions, with five states—Arizona, Colorado, California, New Jersey, and New York—already featuring the legislative basis for such occupation/industry-specific wage floors, though with little use so far.26

Dube estimates how this policy would affect the U.S. wage distribution. He simulates the scenario in which occupation-industry-region cells’ wages were to be raised to the 35th percentile of that cell’s median wage, which Dube shows would bind for 31 percent of workers. He finds a sizable, 10 percent to 20 percent wage boost of workers in the middle percentiles of wages, which would close a significant portion of the median-mean wage gap.

Still, even this intervention would leave a significant gap between productivity and mean and median wages, albeit much larger than the boost to wages that would result from increasing the labor share of GDP, as described above. The overarching point, however, is that the growing wage inequality experienced by workers in the United States leading to ever-growing income inequality cannot be easily remedied without policy experiments in the ways that other nations have tackled this problem. Perhaps those five U.S. states with some rudiments of wage boards on the books can form the basis for a federal policy debate on wage compression.

—Benjamin Schoefer is an assistant professor of economics at the University of California, Berkeley.

Acknowledgments

End Notes

1. Dean Baker, Josh Bivens, and Jessica Schieder, “Reining in CEO compensation and curbing the rise of inequality” (Washington: Economic Policy Institute, 2019), available at https://www.epi.org/publication/reining-in-ceo-compensation-and-curbing-the-rise-of-inequality/.

2. For prominent use of this striking graph, see Josh Bivens and others, “Raising America’s pay.” Briefing Paper 378 (Economic Policy Institute, 2014), available at https://www.epi.org/publication/raising-americas-pay/.

3. A progressive distribution of the labor share may lead to a higher wage boost for low earners and median wages. I do not know of research that has linked the labor share decline with wage reductions in specific pockets of the labor income distribution.

4. Alice Kügler, Uta Schönberg, and Ragnhild Schreiner, “Productivity growth, wage growth and unions” (Frankfurt: European Central Bank, 2018), pp. 215–247.

5. For a recent study of wage compression guiding firm-level wages, see Emmanuel Saez, Benjamin Schoefer, and David Seim, “Payroll taxes, firm behavior, and rent sharing: Evidence from a young workers’ tax cut in Sweden,” American Economic Review 109 (5) (2019): 1717–63.

6. Ibid.

7. David Card, Jörg Heining, and Patrick Kline, “Workplace heterogeneity and the rise of West German wage inequality,” The Quarterly Journal of Economics 128 (3) (2013): 967–1015.

8. Kügler, Schoenberg, and Schreiner, “Productivity growth, wage growth and unions.”

9. Organisation for Economic Co-operation and Development, Negotiating Our Way Up: Collective Bargaining in a Changing World of Work (Paris: OECD Publishing, 2019), available at https://doi.org/10.1787/1fd2da34-en.

10. Arindrajit Dube, “Using Wage Boards to Raise Pay,” Economics for Inclusive Prosperity 4 (2019), available at https://econfip.org/policy-brief/using-wage-boards-to-raise-pay/. For an empirical study of the Australian awards system, see James Bishop, “The Effect of Minimum Wage Increases on Wages, Hours Worked and Job Loss,” Reserve Bank of Australia Research Discussion Paper RDP 2018-0.

11. Richard Freeman and James L. Medoff, “What do unions do,” Industrial & Labor Relations Review 38 (1984): 244; Bruce Western and Jake Rosenfeld, “Unions, norms, and the rise in US wage inequality,” American Sociological Review 76 (4) (2011): 513–537.

12. Barbara Biasi and Heather Sarsons, “Flexible Wages, Bargaining, and the Gender Gap.” Working Paper w27894 (National Bureau of Economic Research, 2020), available at https://www.nber.org/papers/w27894.

13. Ernesto Villanueva, “Employment and wage effects of extending collective bargaining agreements,” IZA World of Labor (2015), available at https://wol.iza.org/articles/employment-and-wage-effects-of-extending-collective-bargaining-agreements/long.

14. Christian Dustmann and others, “From sick man of Europe to economic superstar: Germany’s resurgent economy,” Journal of Economic Perspectives 28 (1) (2014): 167–88.

15. Pedro Martins, “30,000 Minimum Wages: The Economic Effects of Collective Bargaining Extensions,” British Journal of Industrial Relations (forthcoming).

16. Tito Boeri and others, “Wage equalization and regional misallocation: evidence from Italian and German Provinces.” Working Paper w25612 (National Bureau of Economic Research, 2019), available at https://www.nber.org/papers/w25612.

17. Villanueva, “Employment and wage effects of extending collective bargaining agreements.”

18. Justus Haucap, Uwe Pauly, and Christian Wey, “Collective wage setting when wages are generally binding: An antitrust perspective,” International Review of Law and Economics 21 (3) (2001): 287–307.

19. Henry Farber and others, “Unions and inequality over the twentieth century: New evidence from survey data.” Working Paper (National Bureau of Economic Research, 2018), available at https://www.nber.org/papers/w24587.

20. Jae Song and others, “Firming up inequality,” The Quarterly Journal of Economics 134 (1) (2019): 1–50, available at https://doi.org/10.1093/qje/qjy025.

21. John DiNardo and David S. Lee, “Economic impacts of new unionization on private sector employers: 1984–2001,” The Quarterly Journal of Economics 119 (4) (2004): 1383–1441. Cross-sectional evidence continues to suggest a relatively large union wage premium at the worker level of around 10–20 log points (Farber and others, “Unions and inequality over the twentieth century: New evidence from survey data”), which does not cover equilibrium spillovers on the wage structure, including uncovered firms and workers, but also captures positive worker selection.

22. For example, Jäger and co-authors review a large series of existing empirical estimates of firm-level rent sharing elasticities, finding a small elasticity of around 10 percent no matter the country or time period. See Simon Jäger and others, “Wages and the Value of Nonemployment,” The Quarterly Journal of Economics 135 (4) (2020): 1905–1963. I do not know of estimates of whether U.S. firm-level unionization may boost rent sharing elasticities. Moreover, recent proposals of shared governance in the United States (giving workers the right to elect their own board representatives to participate in company-level decision-making), as proposed in the Accountable Capitalism Act, may have little effect on wages, as suggested by studies in the context of Germany and Finland. See Simon Jäger, Benjamin Schoefer, and Jörg Heining, “Labor in the Boardroom,” The Quarterly Journal of Economics (forthcoming); Jarkko Harju, Simon Jäger, and Benjamin Schoefer, “Voice at Work.” (Working paper, 2021).

23. Villanueva, “Employment and wage effects of extending collective bargaining agreements.”

24. Martins, “30,000 Minimum Wages: The Economic Effects of Collective Bargaining Extensions.”

25. Dube, “Using Wage Boards to Raise Pay.”

26. Arindrajit Dube, “Rebuilding U.S. labor market wage standards” (Washington: Washington Center for Equitable Growth, 2020), available at https://equitablegrowth.org/rebuilding-u-s-labor-market-wage-standards/. For a thorough review of the legal aspects of this potential institution, see Kate Andrias, “The New Labor Law,” The Yale Law Journal 126 (1) (2016): 76, available at https://www.yalelawjournal.org/article/the-new-labor-law. For a more policy-focused report discussion, see David Madland, “Wage Boards for American Workers: Industry-Level Collective Bargaining for All Workers” (Washington: Center for American Progress, 2018), available at https://www.americanprogress.org/issues/economy/reports/2018/04/09/448515/wage-boards-american-workers/.