What the U.S. Census Household Pulse Survey reveals about the first year of the coronavirus recession, in six charts

The U.S. Census Bureau’s new Household Pulse Survey is an invaluable and near real-time source of information for understanding how the coronavirus recession is affecting U.S. workers, families, and communities. By asking U.S. households since April 23, 2020 about their health, employment status, and spending patterns, the survey sheds light on how they are experiencing the downturn.

The results are alarming. The Household Pulse Survey data show that over the course of the pandemic, millions of workers stopped working due to slack business conditions or because they were doing unpaid care work. As many as 30 million households experienced food insecurity. And close to 90 million households struggled to afford typical household expenses and make rent or mortgage payments on time.

The survey also gathers information on access to and use of economic relief and income-support programs such as the Supplemental Nutrition Assistance Program and Unemployment Insurance. Even though access to jobless benefits has been unequal, these benefits nevertheless allowed millions of households—and especially those hit hardest—to meet their spending needs. And as the money from Economic Impact Payments reached the hands of many workers and families in need of a lifeline, relief dollars were injected back into the economy, helping the United States get on track toward a recovery.

Here is what the Household Pulse Survey tells us about this recession almost 1 year after the Census Bureau first published the results of this new survey.

The shock to the U.S. labor market falls heaviest on already-vulnerable workers and families

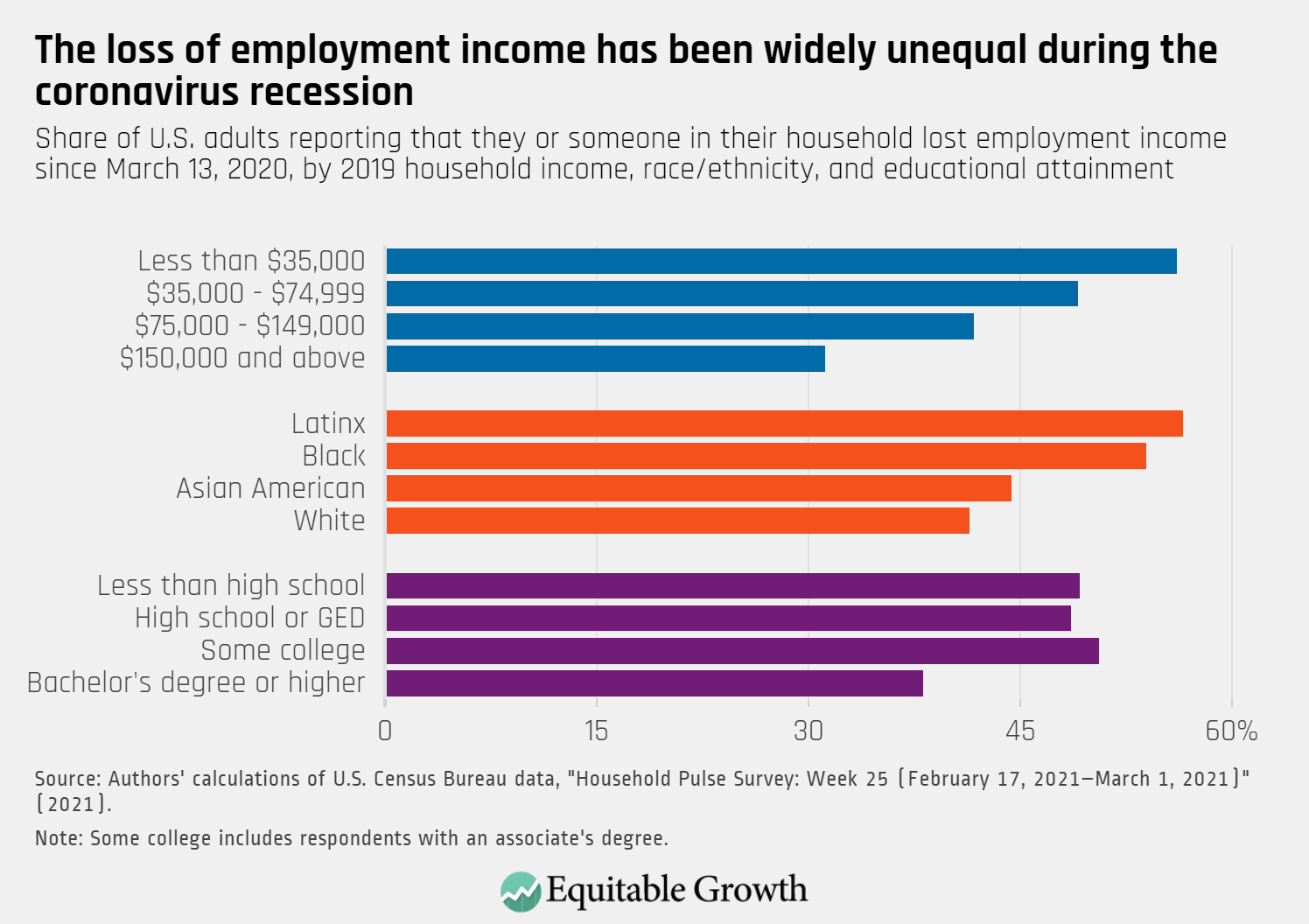

Between mid-February and early March 2021, almost half of U.S. adults reported that they themselves or someone in their household lost employment income since March 2020, but lower-income workers, workers of color, and workers without a college degree were especially likely to experience losses. For those facing multiple disadvantages in the labor market, that number can be much higher.

Case in point: More than 6 in 10 Black adults with a 2019 household income of less than $35,000 report losing labor income since the recession hit. As such, the Household Pulse data reflect what is a defining feature of this crisis: The workers most exposed to job losses and wage cuts are some of the same workers least likely to have a buffer of savings to weather an income shortfall. This trend is not only deepening longstanding disparities in the labor market but also risks holding back the economic recovery. (See Figure 1.)

Figure 1

Many U.S. workers stopped working, but reasons why vary among groups

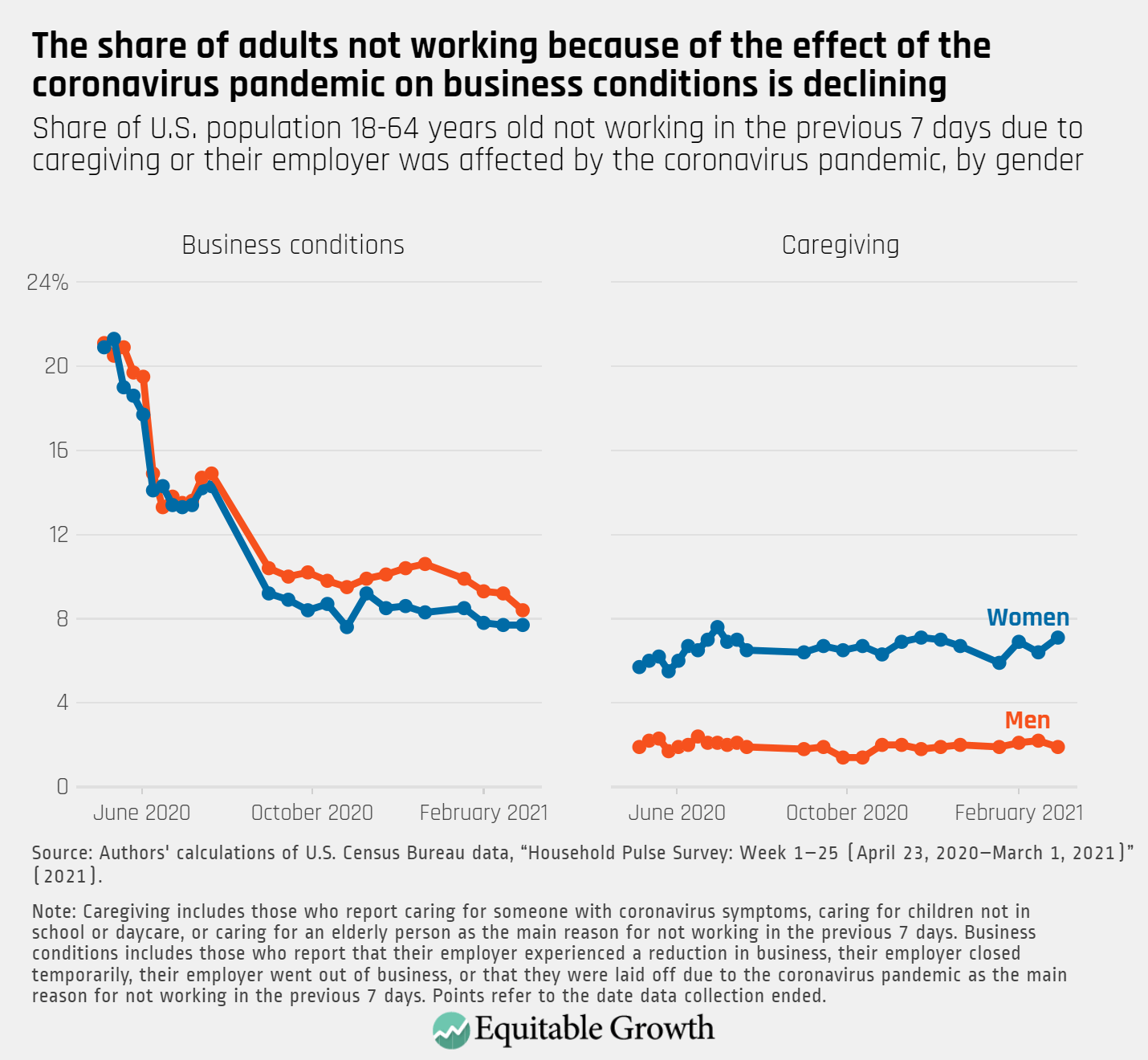

As the recession hit the U.S. economy, more than 20 million workers lost their jobs between February and April 2020. As the Household Pulse Survey published its first estimates for the last week of April and the first week of May 2020, 1 in 5 working-age adults reported being out of work due to a layoff or because the coronavirus pandemic affected their employers’ businesses.

Disaggregating the data by gender shows that while slack business conditions affected women and men in roughly the same way, the share of adults not working for pay because they are caring for someone with coronavirus symptoms, an elderly person, or a child not in school or daycare hovered at around 6 percent for women and around 2 percent for men throughout most of the recession. (See Figure 2.)

Figure 2

By early March 2021, more than 7 million working-age women were not working for pay due to these caregiving responsibilities. Research shows that women—and especially women of color and women with children—are experiencing particularly tough labor market outcomes during this recession as they assume the lion’s share of the unpaid work of caring for their households and communities. For instance, another survey finds that of the 11 percent of women with young children who reported quitting their jobs due to the pandemic, half pointed to the closure of school or daycare as one of the reasons why.

Because women are disproportionately hit by the coronavirus recession, the gender gaps in employment outcomes could widen further, dampening the economic growth resulting from women’s greater attachment to the labor market.

Millions of U.S. households, especially low-income households and households of color, struggled to pay their bills

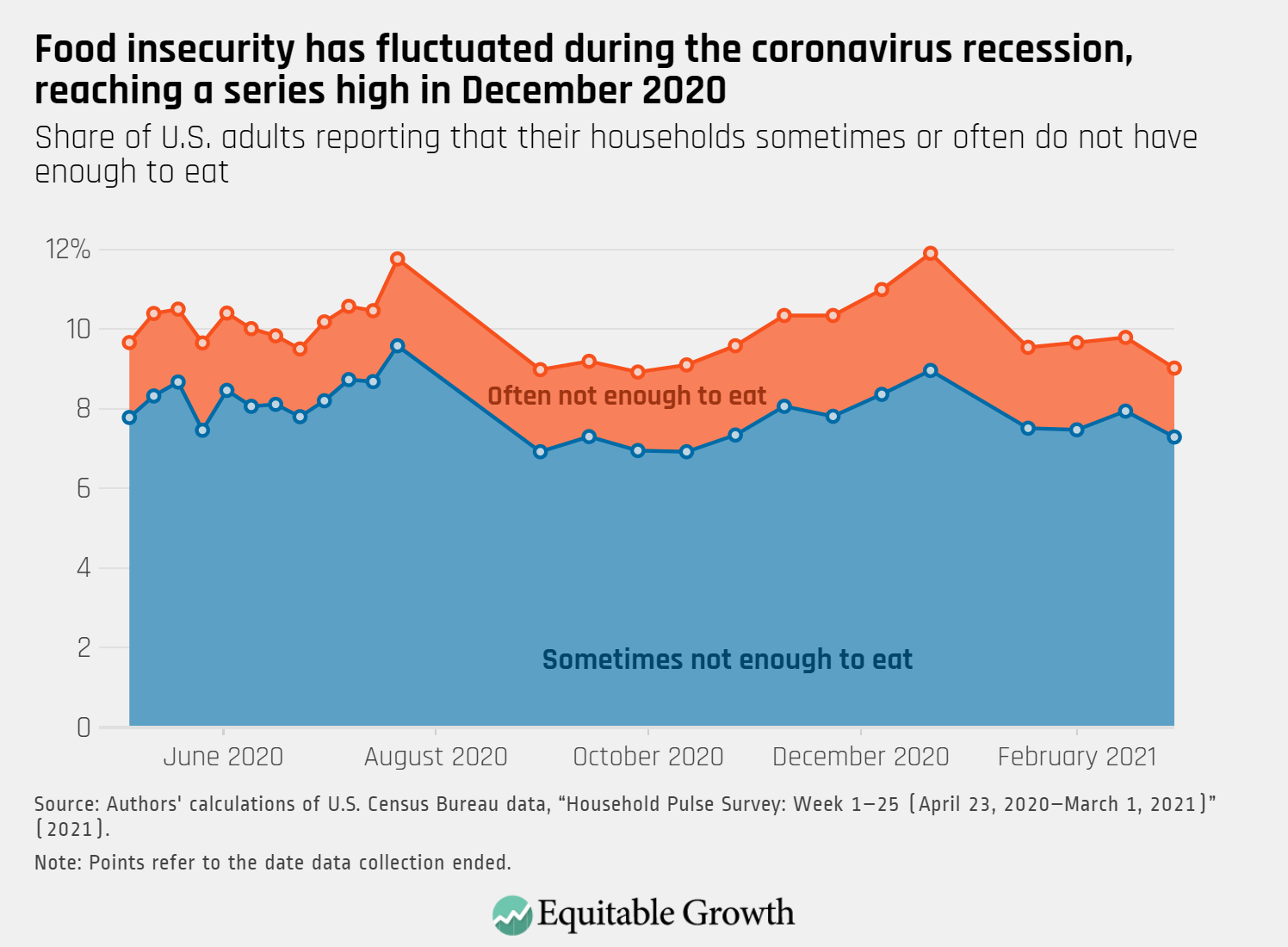

Overall, the share of working age-adults between 18 and 64 years of age reporting they did not work during the previous week declined from 39 percent in early May 2020 to 34 percent in early March 2021. Alarmingly, however, the improvement in the U.S. labor market did not prevent many households from having a hard time buying essential goods or keeping up with their bills.

In late December 2020, 12 percent of U.S adults—almost 30 million people—lived in a household that either sometimes or often did not have enough to eat. As many households struggle to put food on the table, some states and localities reported big spikes in applications for Supplemental Nutrition Assistance Program benefits, highlighting the role of the program in both protecting families’ economic security and as a mechanism to stabilize the entire economy by helping cash-strapped households keep up their spending. (See Figure 3.)

Figure 3

A report by the U.S. Federal Reserve shows that in October 2019—just a few months before the recession hit—28 percent of U.S. adults did not expect to pay their bills in full or would not be able to do so if faced with an unexpected $400 expense. And indeed, when the COVID-19 crisis ripped through the U.S. economy, more than 32 percent of adults reported having a very difficult or somewhat difficult time paying for typical expenses such as food, rent or mortgage payments, student loans, and medical bills.

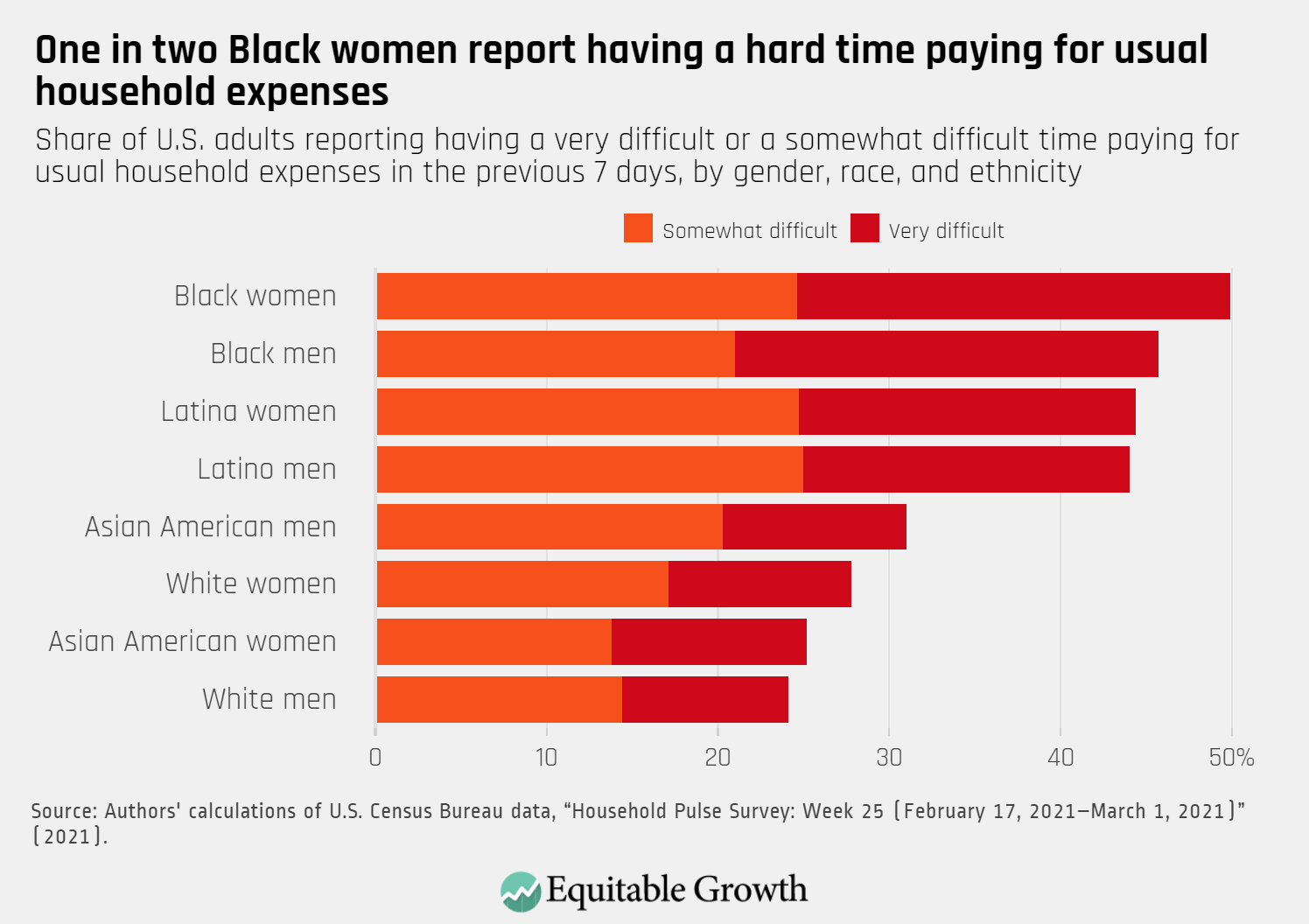

The Household Pulse Survey points to disparities across demographic groups. It shows that Black and Latinx respondents face the most difficulties paying their bills, with half of Black women reporting a very difficult or somewhat difficult time paying for essentials. This dynamic mirrors trends in the labor market, as it was precisely Black women who suffered the deepest employment losses in the first year of the recession. (See Figure 4.)

Figure 4

Economic relief is a lifeline to millions of workers and families, but disparities remain

In their initial response to the economic and health crises, U.S. policymakers in March 2020 ramped up and expanded eligibility for Unemployment Insurance—one of the country’s most important income-support programs. Amid this recession, jobless benefits not only protected millions of workers from a deep income shortfall but also helped stabilized the broader U.S. economy by allowing jobless workers to spend and contribute to maintaining demand for goods and services.

The recession, however, also exposed longstanding disparities embedded in the Unemployment Insurance system. For instance, access to jobless benefits is unequal along the lines of race and ethnicity, with analyses showing that states with a greater share of Black workers replace a smaller portion of workers’ lost wages. The Household Pulse data also show that among those who applied for Unemployment Insurance, Black and Latinx workers were least likely to actually receive benefits. For instance, of the 3.3 million Black men who applied for the program, almost 1 million—29 percent—did not receive jobless benefits. (See Figure 5.)

Figure 5

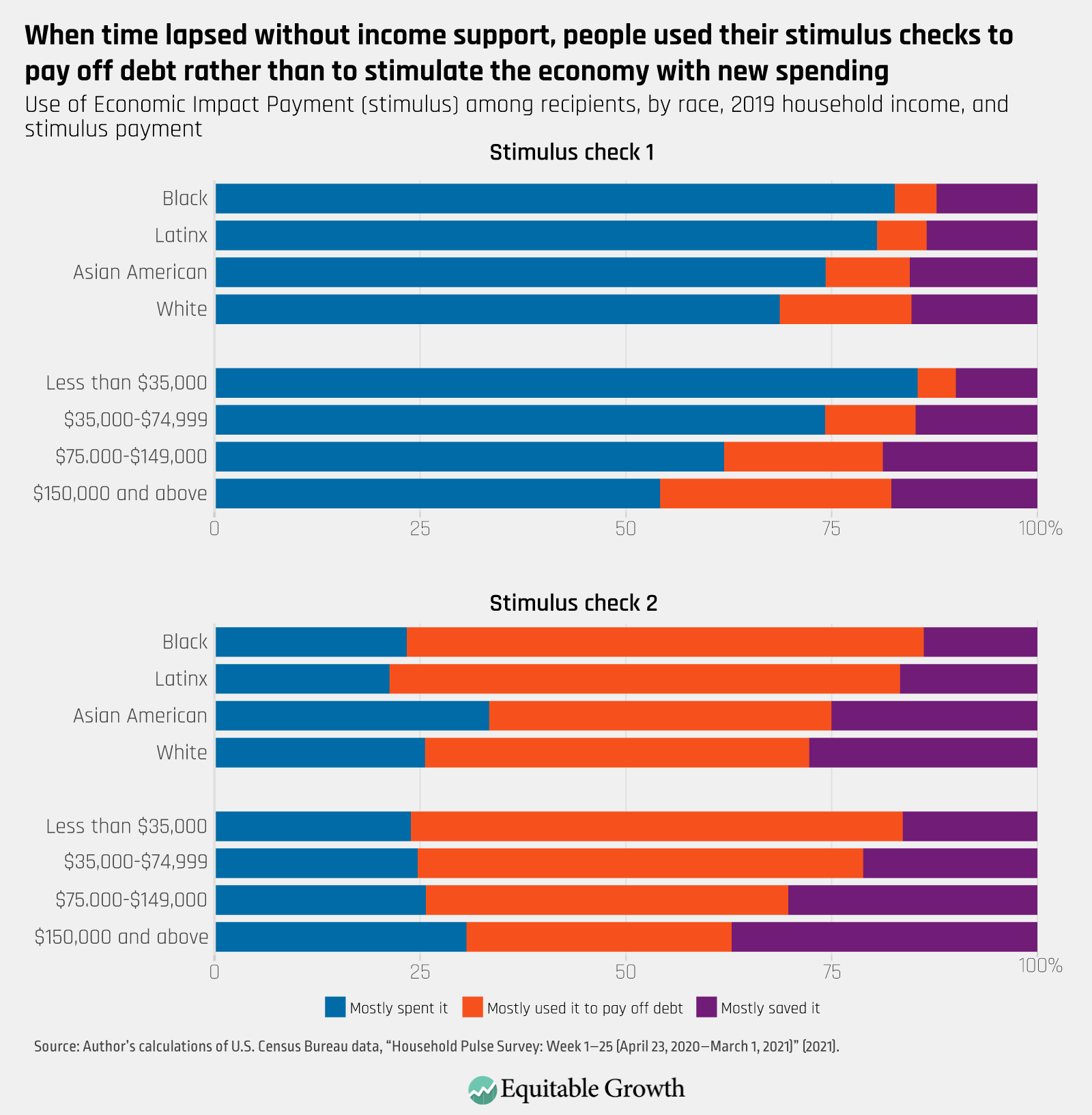

In addition to jobless benefits, the U.S. government provided most U.S. households the first Economic Impact Payment of $1,200 as a key provision in the Coronavirus Aid, Relief, and Economic Security, or CARES, Act, with research showing that consumer spending picked up immediately after the payments arrived. A greater share of Black and Latinx households—between 83 percent and 81 percent, respectively—spent their first stimulus check on expenses such as food, household supplies, and utilities, compared to Asian American (74 percent) and White (67 percent) households.

Eight months after the CARES Act was enacted, a second $600 Economic Impact Payment was sent to most U.S. households. By this time, multiple waves of coronavirus cases damaged employment opportunities and the general livelihood of many U.S. workers and their families. One of the results was more debt: Approximately 30 percent of adults reported having increased credit card debt, taking out loans, or asking for financial help from friends and family between June and December 2020.

When the $600 stimulus payments arrived, households across all races and income groups—but especially Black, Latinx, and low-income households—used this money to begin paying off the debt they had accumulated rather than spending it on household expenses. The disparities in use of the two stimulus payments highlight the importance of providing timely relief to the most economically vulnerable households in order to drive a faster and more equitable recovery. (See Figure 6.)

Figure 6

Conclusion

More than a year after the onset of the coronavirus recession, many low-income families and families of color remain more exposed not only to the continuing health crisis and economic shocks but also to entrenched and longstanding disparities in the U.S. labor market. These intertwined risks can hold back an overall U.S. economic recovery. When suffering earnings losses, workers and households with fewer savings and liquid assets cut back on their spending more than those who have more robust financial cushions.

The coronavirus recession continues to hit workers whose consumption is especially sensitive to income shocks, triggering a vicious cycle where demand for goods and services declines, hurting businesses and putting other jobs at risk. Yet empirical evidence also shows economic relief works as a buffer and helps stabilize the entire economy. Fiscal policy proposals that mistakenly champion austerity measures and concerns about the national debt should not be the priority. Rather, U.S. policymakers should focus on eliminating the disparities embedded in the U.S. labor market and social insurance programs, allowing the entire economy to recover more swiftly and be better prepared the next time a downturn hits.