The comment letter discusses the impact of commercial data practices on workers, labor markets, and the economy, in response to the NTIA’s questions. Specifically:

Transparency alone cannot lead to fair practices; workplace monitoring and algorithmic management can be all but impossible for most workers to avoid, both due to such practices’ ubiquity and because of the erosion of labor protections and the rise of anticompetitive labor practices that reduce workers’ ability to consent meaningfully to surveillance or bargain over these issues.

Harmful commercial data practices in the workplace undermines worker power and change the structure of jobs and work through which firms de-skill work and misclassify employees, allowing them to pay workers less, sidestep worker protections, and undermine workers’ bargaining ability, ultimately increasing economic inequality and distorting economic growth.

The consequences of workplace privacy harms are concentrated and compounded for marginalized workers due to discrimination, occupational segregation, and weaker bargaining power, exacerbating an array of economic inequalities and further preventing these workers from challenging harmful practices.

Read the full letter submitted to the National Telecommunications and Information Administration.

This dual role means that women workers face particularly significant challenges balancing professional and family responsibilities. These challenges are amplified when a woman’s partner or child becomes seriously injured or ill, impacting her ability to continue working.

Paid family leave policies, which provide workers with partially paid time off to care for a loved one, can help workers prioritize their care responsibilities without fear of losing their income or their jobs. Many studies have examined the impacts of paid parental leave, or time off to care for a newborn or newly adopted child, as well as paid sick leave, which is typically used to address one’s own short-term illness. But less is known about paid leave taken to care for an ill family member.

Our new working paper, “The Impact of Paid Family Leave on Families with Health Shocks,” builds on this literature by demonstrating how access to paid caregiving leave significantly improves job continuity among women workers whose spouses experience a health shock. We analyze the impacts of the paid family leave policies implemented in California in 2004, New Jersey in 2009, and New York in 2018 on the labor market and mental health outcomes of individuals whose spouses or children undergo a surgery or are hospitalized.

Our paper uses restricted-use data from the U.S. Department of Health and Human Services’ Medical Expenditure Panel Survey, which follows U.S. households for five rounds of surveys over a 2-year period. These surveys collect detailed information on respondents’ demographic and socioeconomic characteristics, the precise timing and diagnosis codes associated with any inpatient, outpatient, and emergency department visits, prescription drug use and medical conditions, labor market outcomes, and states of residence.

Our study then uses difference-in-difference and event-study models that compare the differences in labor market and mental health outcomes, measured in post-health-shock rounds of the survey, between individuals before and after paid family leave implementation in California, New Jersey, and New York. It also compares these differences with analogous differences in states with no change in paid family leave access over the analysis time period.

Our main finding is that access to paid family leave leads to a 7 percentage point decline in the likelihood that the healthy wives of individuals who experience a hospitalization or surgery will “[leave] a job to care for home or family” in the aftermath of the health shock. These findings are concentrated among women workers, and those with 12 years or fewer of formal education.

The impacts on men’s labor market and mental health outcomes, as well as on women’s mental health outcomes, are more mixed and less conclusive. We also do not find statistically significant impacts of paid family leave on the outcomes of working parents whose children experience a health shock. This finding is in line with other survey evidence indicating that parents of children with healthcare needs experience large barriers to actually taking paid leave, even when they have access to it.

Our findings on the labor market impacts for women are consistent with prior research about the impacts of paid family leave on new mothers. One study, for instance, shows that paid parental leave allows new mothers to more easily step away from work temporarily and then resume their professional duties once their children are a little bit older. Other studies find similar positive economic effects of paid family leave on new parents.

While more research is needed to understand how paid family leave may affect other types of caregivers—such as those providing eldercare to aging parents—our results indicate that paid family leave can have a significant impact on job continuity among women whose spouses need care. Additionally, women, and especially mothers, often face lower wages and other professional penalties that their male counterparts do not. The fact that our results are driven by women—and particularly those with lower levels of education, who may not have access to employer-provided paid leave—points to paid family leave as a policy tool that can reduce economic inequality while supporting a healthier balance between the important work done both in U.S. homes and in the U.S. labor market.

—Courtney Coile is the William R. Kenan, Jr. Professor of Economics at Wellesley College. Maya Rossin-Slater is an associate professor of health policy at Stanford University. Amanda Su is a Ph.D. student in health policy specializing in health economics at Stanford University.

To learn more about paid family and medical leave research, including three new research products funded by Equitable Growth examining the impact of paid leave amid the COVID-19 pandemic, please consider attending Equitable Growth’s upcoming webinar, “Paid leave and the pandemic: New evidence from Families First and lessons for federal policymakers.” Click here to register for the event.

For centuries, Indigenous communities in the United States have faced devastating poverty. American Indians and Alaska Natives today experience the highest rate of poverty, at 25 percent, of any major racial or ethnic group in the United States.

The current economic hardships faced by AIAN communities can be traced back to centuries of colonization and discriminatory policies, such as the Homestead Act of 1862, which took land and resources away from Indigenous tribes. In recent decades, tribal governments and community organizers have worked to rebuild their populations and promote educational and economic prosperity both on and off reservation lands.

Data on the economic state of American Indians and Alaska Natives across the country is limited, however, making it difficult for researchers and policymakers alike to assess the needs of individual tribes and communities. Additionally, while those living on and off reservation lands may experience similar socioeconomic disparities, they differ when it comes to the barriers they face to building wealth.

Housing on reservation land, for example, is scarce and poor quality, compared to nonreservation rural housing. This means that potential AIAN homeowners trying to purchase a home on tribal land might experience issues with low housing supply and quality, though they do have access to tribal-specific lending options. Yet potential AIAN homeowners looking to purchase homes outside of tribal boundaries might experience a competitive housing market and be excluded from receiving tribal grants and loans, meaning their options for homeownership might be limited.

This issue brief focuses on the unique challenges that face Native Americans trying to build wealth while living on reservations, including the lack of banking accessibility, housing supply, and high-quality jobs. It also covers a series of potential policy solutions to address these challenges and make wealth building more accessible for Native Americans.

But first, we look at the existing data on Native American wealth and what it can tell us about the disparities these communities face in the United States.

What the data say about Native American wealth

The primary source of wealth data in the United States is the Federal Reserve’s Survey of Consumer Finances. Although this survey allows respondents to identify as American Indian or Alaska Native, published results from the survey only offer summary data for White, Black, and Hispanic respondents, with all other races and ethnicities included in an “Other” category.

This level of data aggregation reflects the relatively small sample size of the Survey of Consumer Finances, which does not support disclosure of summary statistics for smaller groups. Asian Americans, Native Hawaiians, Pacific Islanders, American Indians, Alaska Natives, and people of two or more races are all included in this aggregate “Other” group, yet the economic experiences and conditions of each population and subpopulation are vastly different—meaning the data for this group have little analytical value.

State and federal statistical agencies are unable to provide disaggregated data on AIAN socioeconomic experiences and challenges, and they primarily cite small sample sizes in government surveys as the reason. One potential solution, put forth by Blythe George, an Equitable Growth grantee and professor at the University of California, Merced, is for state and federal governments to work with tribal leaders to honor tribal sovereignty and build data infrastructure designed to capture vital information about tribal citizens and the state of their reservations.

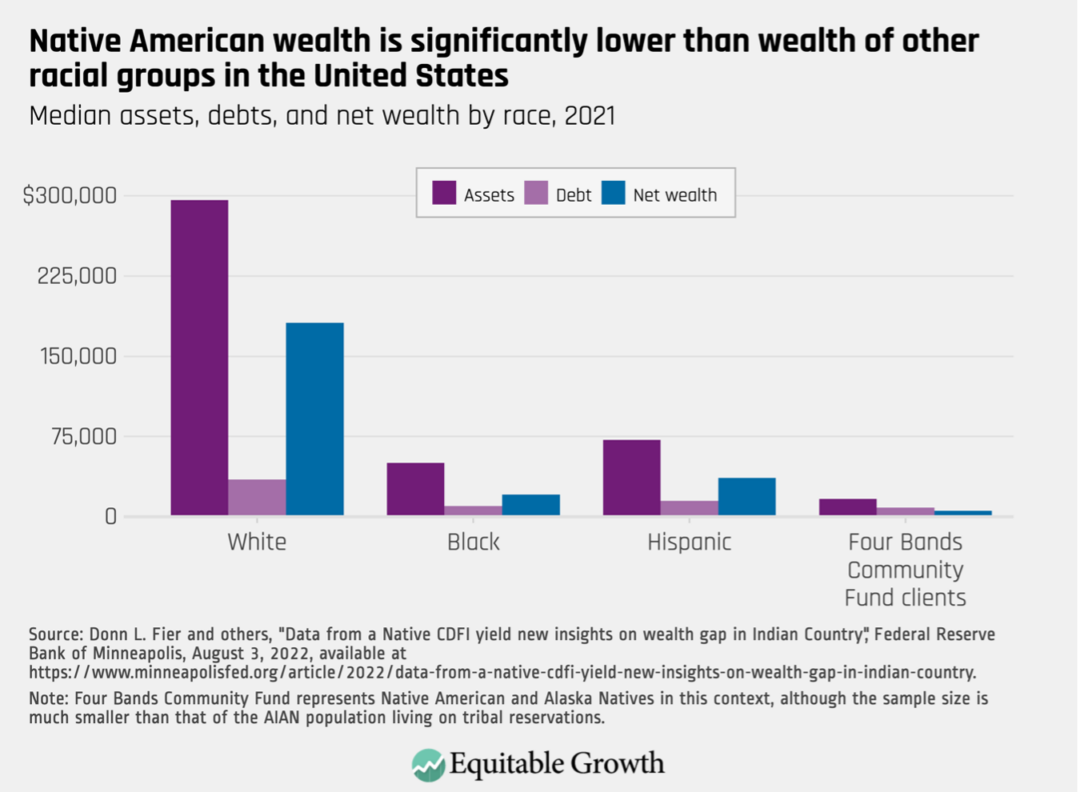

Because these gaps in the data persist, researchers also are looking into alternative metrics that can give some insight into AIAN household wealth. For instance, economists at the Federal Reserve and the Four Bands Community Fund—a community development financial institution, or CDFI, with primarily AIAN clients—looked at the assets and debts held by Native American clients living on the Cheyenne River Sioux reservation in South Dakota. Comparing these data with the wealth metrics in the Survey of Consumer Finances, the study finds that the wealth gap ratio between White Americans and American Indians and Alaska Natives is 32-to-1. The authors also find that while the median net worth of a White household is $181,440, the median net worth of the Four Bands clients is only $5,524. (See Figure 1.)

Figure 1

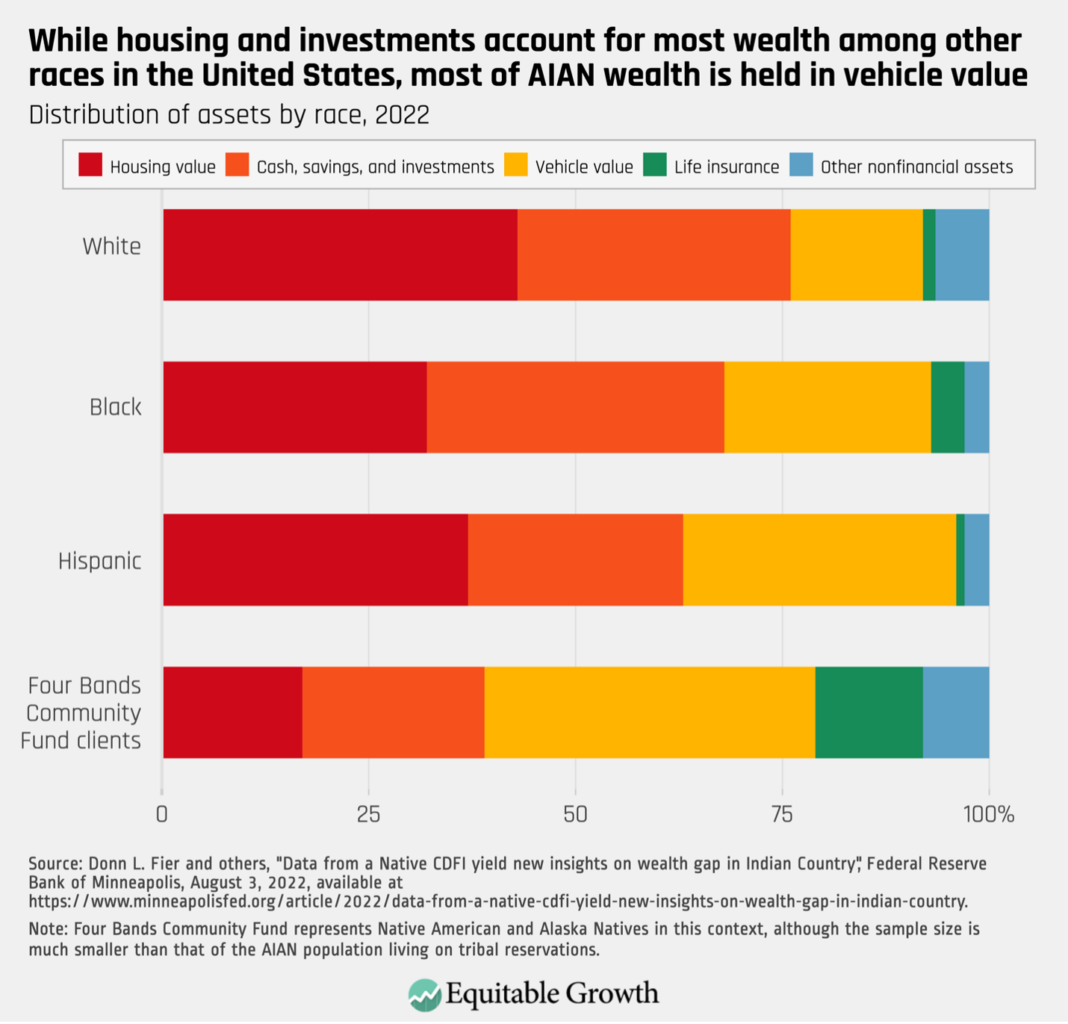

Additionally, while most U.S. households hold their wealth in homeownership, the researchers find that the value of their motor vehicles accounts for the largest component of wealth for AIAN households. (See Figure 2.)

Figure 2

While these findings are based on a limited sample of Native Americans, they indicate the difficulty that AIAN households have in building wealth.

Next, we turn to the various sources of wealth among U.S. households and the barriers to access that AIAN households face within each specific category.

Barriers to housing and homeownership wealth

Homeownership is the primary source of wealth for most U.S. households. Yet AIAN homeownership rates are considerably lower than White, non-Hispanic homeownership rates, at 50 percent, compared to 71 percent, according to the 2021 American Community Survey.

For Native Americans living on reservation land, homeownership comes with many challenges. Reservations across the country are experiencing a worsening housing crisis due to growing populations, overcrowding, limited supply, and poor-quality housing. Indeed, between 2010 and 2020, the Native American population increased by 160 percent, with a significant portion of this growth taking place on tribal reservations.

Additionally, despite funding and resources from state and federal governments, building housing on tribal land is a complex and expensive matter due to the unique challenges that their geography poses. Reservations in isolated and rural areas or those with limited infrastructure, such as roads and bridges, cannot easily receive the necessary resources to develop housing. In a 2018 U.S. Senate hearing on overcrowding in Alaska Native houses, a regional housing authority official testified that developing housing on Alaskan tribal land is expensive because every piece of hardware and materials must be flown into rural and isolated regions of Alaska.

Systemic discrimination has been a major contributor to the lack of necessary infrastructure on reservation lands. While most state and local governments can use tax-free debt obligations to build public resources, such as roads, parks, and bridges, tribal governments are blocked from using such financing due to The Indian Tribal Government Tax Status Act of 1981. This act limits the use of nontaxable tribal government bonds to “essential government functions,” which does not include road and highway infrastructure.

As part of the Great Recession stimulus package of 2009, however, a pilot program gave federally recognized tribes the authority to issue tax-exempt bonds to incentivize infrastructure development. The program was so successful that the U.S. Treasury Department has since recommended a permanent waiver to the essential government functions mandate to spur social and economic growth on reservation lands.

Because housing is so limited in supply and new housing developments are a rarity on tribal reservations, prospective AIAN homeowners currently face waiting times of 3 or more years for an available housing unit. These long waitlists mean that properties tend to face overcrowding, or situations in which there is more than one person per room in a single housing unit. In 2018, 16 percent of AIAN households on reservations experienced overcrowding, compared to the overall U.S. rate of 2 percent. Some AIAN households even report having 12 to 15 people in units measuring less than 900 square feet.

To make matters worse, many of these overcrowded housing units are low quality. Those living on reservations are “5 times more likely to live in homes that lack basic plumbing, nearly 4 times more likely to live in homes without a sink, range, or refrigerator, and 1,200 times more likely to live in homes with heating issues,” according to the National Low Income Housing Coalition.

Lack of necessary resources, such as plumbing and heating, coupled with the issues posed by overcrowding, can mean AIAN individuals face two related hurdles in their efforts to build wealth: The value of existing properties on reservations is exponentially lower than the U.S. housing market, and resulting health issues from poor-quality housing can prevent AIAN workers from entering laborious, good-paying jobs. During the previously mentioned Senate hearing on overcrowding and its impact on Alaska Natives, witnesses cited research finding that overcrowding causes decreased sleep, increased stress, increased cases of mental health crises, and the elevated spread of illnesses. Likewise, amid the COVID-19 pandemic, researchers from Duke University found that overcrowded housing increases the risk of COVID-19 mortality.

Another element in the reservation housing crisis is the structure of property ownership on reservation lands. In an effort to reduce tribal governments’ control over the land they resided on, President Grover Cleveland signed into law the General Allotment Act of 1887, which allowed the president to “survey Indian tribal land and divide the area into allotments for individual Indians and families” and forced tribal governments to sell any land that exceeded the allotment restrictions to homesteaders or the government. From 1887 to 1934, Native American land ownership plummeted from 138 million acres to just 48 million acres.

Additionally, under the 1887 law, these allotments could be transferred to fee simple land, which gives property owners full rights over their property. Yet this transfer was only allowed on a case-by-case basis at the discretion of the U.S. Bureau of Indian Affairs. The federal government ended the allotment program in 1934, but even today individuals who own trust land still need to get approval from the agency to sell or develop their land. Having to navigate bureaucratic approval processes means that trust landowners may experience difficulties building or updating housing on their properties, which results in diminished property values.

Barriers to banking and access to capital

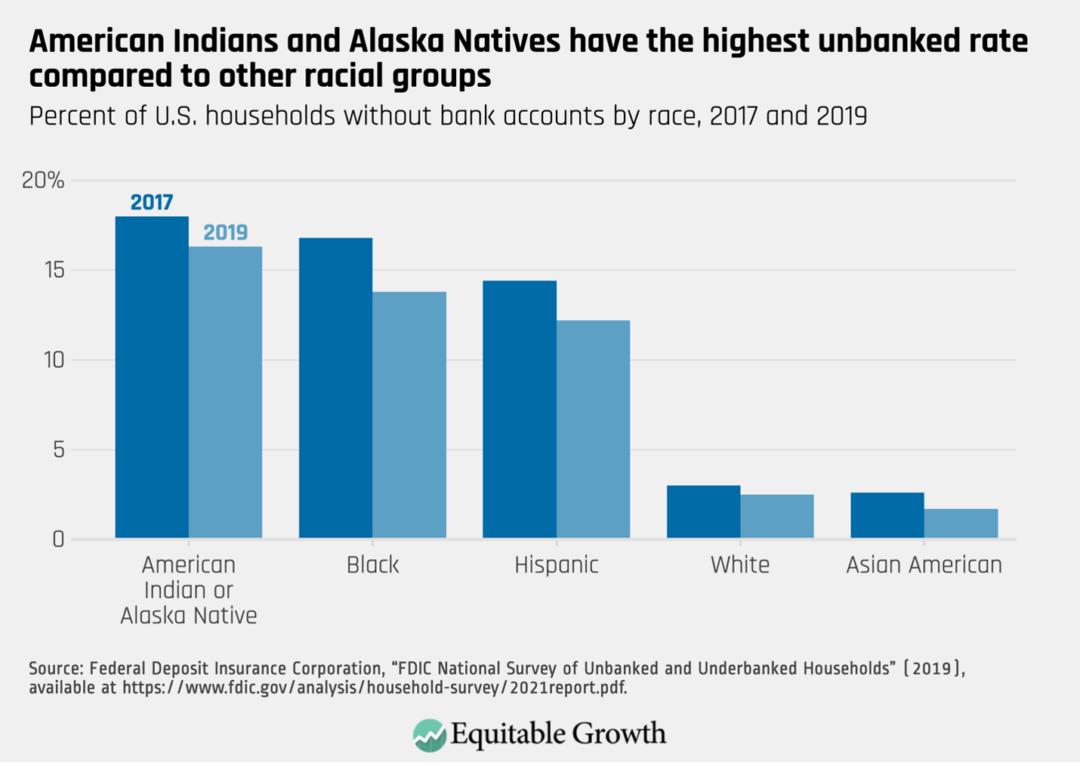

According to the Federal Deposit Insurance Corporation, Native Americans are the most underbanked racial group in the United States, with approximately 16 percent of AIAN households being unbanked as of 2019. (See Figure 3.)

Figure 3

Of those U.S. households that are banked, AIAN families had the lowest rate of bank branch visits, at 15.5 percent. Physical proximity and general lack of necessary services are the two main reasons AIAN banking rates are so low.

The average distance between Native American reservation lands and the nearest bank is approximately 12.2 miles, almost 20 times the distance between rural city centers and nearby banks. Even if a national bank is within a reasonable distance to tribal land, residents find that such banks neither have an adequate understanding of tribal finances nor provide the necessary financial resources and credit that AIAN households need to navigate investment and housing complexities.

To overcome these challenges, tribal nations have established tribal community banks and CDFIs that support tribal residents as they navigate the nuances of tribal laws and state and federal funding limitations. These financial institutions, often run by tribal nations or tribal entities, provide residents with the tools and services they require to access capital for homeownership or property improvements and other financial needs.

Additionally, researchers find that over the past two decades, Native American Financial Institutions on reservation lands are closing the gap in credit access in tribal regions and providing underserved citizens with much-needed banking resources and knowledge unique to tribal society. Native-owned banks are also seen as more trustworthy and are generally more supported by Native American tribal residents.

Barriers to income growth

At the onset of the COVID-19 pandemic, 28.6 percent of AIAN workers were unemployed, a devastating joblessness rate that is only comparable to the general rate of unemployment seen during the Great Depression nearly 100 years ago. Part of this is because Native American workers are often overrepresented in service and front-line occupations, which have experienced long-lasting disruptions since the start of the pandemic.

Yet employment challenges for Native Americans predate the pandemic. In 2020, 21 percent of single-race AIAN people were earning incomes below the federal poverty line due to the many structural barriers to employment—an improvement from almost 29 percent in 2015. Likewise, research from 2013 finds that when controlling for a number of factors, such as age, education, reservation residency, and state of residence, Native Americans had lower odds of gaining employment, compared to White workers.

These findings supplement evidence that almost one-third of Native Americans face racial discrimination when applying for employment or being considered for a promotion, while 54 percent of Native Americans living in areas with a Native majority experience institutional discrimination.

Some researchers point to educational quality and attainment as an explanation for the employment divide between AIAN workers and White workers. A 2018 study on occupational dissimilarities between AIAN and non-Hispanic White workforces, for example, finds that while AIAN workers are overrepresented in low-skilled occupations and underrepresented in high-education occupations, compared to White workers, much of that gap is closed when accounting for differences in educational attainment.

Research also shows that lower educational attainment rates among AIAN students is due to lack of wealth. In 2016, approximately 90 percent of Native American higher education students received some form of grant aid, compared to 77 percent of all students. Another survey on Native American education finds that only 36 percent of Indigenous college students completed their degree within 6 years, compared to 60 percent of all U.S. college students. Participants of the study who did not complete their degree within 6 years cited college affordability as the primary barrier to completing their degree.

Yet differences in educational attainment do not fully explain the workforce gaps between AIAN workers and White workers, suggesting there are other factors that contribute to this occupational sorting. The 2018 study does find that occupational dissimilarities between AIAN men and AIAN women exist, but also finds that when comparing AIAN women to White women and AIAN men to White men, there were not more significant differences in occupational choices than in the comparison of the two racial groups collectively.

Despite these barriers, over the past 30 years, there have been significant improvements in economic well-being among Native Americans living on tribal lands. Randall Akee of the University of California, Los Angeles credits advancements in tribal sovereignty over the past three decades for this economic growth—the best that Native Americans living on tribal land have experienced in the 500 years since contact with European colonists. His research finds that the businesses and industries that survived during the Great Recession of 2007–2009—including arts, entertainment, public administration, food, and lodging—were able to do so because establishments that were tribally owned and operated prioritized maximum employment of tribal citizens and residents over profits.

Policies to reduce barriers to AIAN wealth building

Several options exist for policymakers seeking to reduce the barriers to wealth building for Native Americans, including collecting more and better data, improving physical infrastructure on reservation lands, boosting AIAN homeownership rates, and making banking more accessible for Native Americans, among others. Below, we detail several proposals that policymakers can undertake to boost Native American wealth.

Build better data infrastructure for tribal populations and areas

Before tribal governments can tackle the barriers to building wealth, they need the necessary data to accurately assess the status of wealth and debt held by tribal citizens and residents. The Federal Reserve Board collects information on Native American wealth, but with a limited sample size, it’s difficult to confidently make any statements on AIAN wealth.

Additionally, not all tribes are alike, and their experiences navigating the labor market and the broader economy are different, too. While one tribal government may benefit from comprehensive data on fishing revenue, for example, other tribes may prioritize data on gaming profits.

In a recent phone conversation with UC Merced’s George, she proposed that individual tribes work to build their own data infrastructure that captures their citizens’ unique economic experiences and conditions. Similarly, Desi Small-Rodriguez, an expert in Indigenous data infrastructure and sovereignty at the University of California, Los Angeles, argues that Indigenous people have the most insight into their tribes’ data, and by ensuring their own data sovereignty, tribal governments are able to reclaim their tribal sovereignty.

These tribe-specific data can assist state and local governments with understanding the individual needs of each tribe and creating funding opportunities that tackle the unique problems each tribe faces.

Develop physical infrastructure to boost housing supply on reservation lands

Tribal leaders and policymakers should look toward improving AIAN homeownership to boost Native American wealth. One way to do so is for state and federal governments to establish funding opportunities for tribal governments to incentivize infrastructure development on reservation lands. Better roads, irrigation, and other public-access projects will establish the necessary infrastructure to build higher-quality housing, and more of it.

Similarly, waiving the limitations of the Indian Tribal Government Tax Status Act and issuing tax-exempt bonds to develop roadway infrastructure would make rural and isolated tribal land more accessible, facilitating the delivery of the materials that are essential to housing development.

Establish funding for home upgrades and clean energy retrofits

Research shows that overcrowding and poor housing quality impact tribal residents’ quality of life and employment stability. State and federal funding to help upgrade residences and infrastructure, such as resilient electricity, plumbing, and insulation, can improve home values while also reducing the health risks associated with overcrowding on reservation lands.

The recently passed Inflation Reduction Act allocated funding to tribal nations and Native American communities to support climate resilience and adaptation, build stable clean energy systems, and make home efficiency upgrades cleaner and more affordable. With a reliable energy system and low-cost options for home improvements, AIAN households will have an opportunity to live in safe and high-quality housing.

Improve accessibility to lending and banking

Several federal agencies have launched programs and grants specifically to promote homeownership for AIAN people. The U.S. Department of Housing and Urban Development’s Section 184 Indian Home Loan Guarantee Program gives AIAN borrowers loans with low down payments that can be used to purchase existing homes, construct new homes, or rehabilitate older properties.

The U.S. Bureau of Indian Affairs’ Housing Improvement Program also provides grants to AIAN households “who have no immediate resources for standard housing” in an effort to tackle rampant homelessness on tribal land.

Support Native American Financial Institutions

While home loan programs exist to improve AIAN communities’ access to homeownership, many households have difficulty accessing these programs due to limited banking operations on reservation lands.

Federal and state governments can work with tribal authorities to establish and support Native American Financial Institutions or any financial institutions that cater to tribal residents specifically. These specialized banks are generally more trusted than national banks because they educate tribal citizens about the designated government programs for which they are eligible that can help them on their path to homeownership and wealth building. They also tend to have specialized knowledge about the tribes and areas they are serving, which allows them to better serve their communities.

Elevate tribal sovereignty to foster additional labor market growth

Academics studying AIAN labor market barriers all point to tribal sovereignty as the key factor leading to the economic growth on reservation lands since the 1980s. For instance, a 2006 paper on economic development on tribal land finds that when tribal governments have more control over community resources, it positively impacts economic growth.

Similarly, a review of academic literature on Native American credit access finds that while improved educational attainment and market access can improve economic growth, “they tend to pay off after a Native nation has been able to bring decisions with local impact under local control and to structure capable, culturally legitimate institutions of self-government that can make and manage those decisions.”

In his essay for Equitable Growth’s Boosting Wages book, UCLA’s Akee proposes tribal sovereignty and innovation of the industries currently operating on reservations as solutions to improving the employment conditions of Indigenous people living on tribal land. The Indian Gaming Regulatory Act of 1988 gave tribal governments the guidelines for developing gaming establishments on tribal land, and since then, the fast-paced boom in tribal gaming operations has been a prosperous endeavor for most tribal communities. In 2015, the tribal gaming industry brought in almost $30 billion in revenue, compared to the nontribal gaming industry’s annual revenue of about $38 billion.

The establishment of tribal sovereignty over the gaming industry is a clear example of how tribal governments’ control over economic regulations directly improves employment and economic conditions of tribal citizens for the better. Building off these successes, Akee’s research finds that federal policies that support industry innovation, restore land bases to tribal governments, and grant authorization to tribal citizens who seek to earn a living through “traditional subsistence activities” can improve employment and earnings opportunities.

As an example, he cites the Columbia River Inter-Tribal Fish Commission, a modern coalition of four tribes dedicated to promoting salmon spawning in the upper regions of the Columbia River. Efforts to improve fish passes at dams along the river and the return of water to smaller offshoots of the river have had positive impacts on the environment, society, and the economy in the region. These changes have restored water and salmon to areas once blocked off through dams, improved the availability of salmon to inland communities, and brought in new fishing revenue to tribal communities.

Conclusion

After centuries of systemic racism and discrimination, Indigenous communities on and off tribal land deserve the right to economic growth and development. Federal and state governments have been working toward this goal through a series of grants, loans, and funding programs that aim to rectify the wrongs committed against Indigenous communities. These programs, in tandem with efforts to boost housing supply and quality and access to banking and financial institutions, will go a long way to reducing the Native American wealth divide in the United States.

Yet academics and advocates find that tribal sovereignty, self-governance, and better data infrastructure also are necessary to further develop economic growth and prosperity for AIAN communities. Expanding upon three decades of tribal sovereignty by introducing tribal data infrastructure can only help AIAN groups understand their unique economic conditions, allowing them to break down the barriers to wealth building and provide sustainable economic growth for all tribal communities.

A central part of Black History Month is highlighting the accomplishments and contributions of Black Americans to U.S. society, culture, and the economy, often in the face of incredible barriers. Over the course of U.S. history, the institution of slavery, overt and violent racism and discrimination, and de facto and de jure segregation actively separated Black people from resources that could help them thrive. Yet despite these barriers, Black Americans overcame them to develop art, create inventions, and change laws—all while propping up the economy that made the United States into the country that it is today.

All aspects of Black history are important to study and learn from, but examining the economic history of Black people in the United States is especially necessary to understand modern-day racial disparities in income and wealth and the consequences for economic growth, as well as the possibility of future shared prosperity. While Black Americans have experienced important gains in education, employment, and income, that progress often lags behind that of White Americans and broader national trends. And other indicators, such as Black homeownership rates, have registered little progress.

The racial wealth gap, in short, is one of the largest and most significant economic disparities in the United States today.

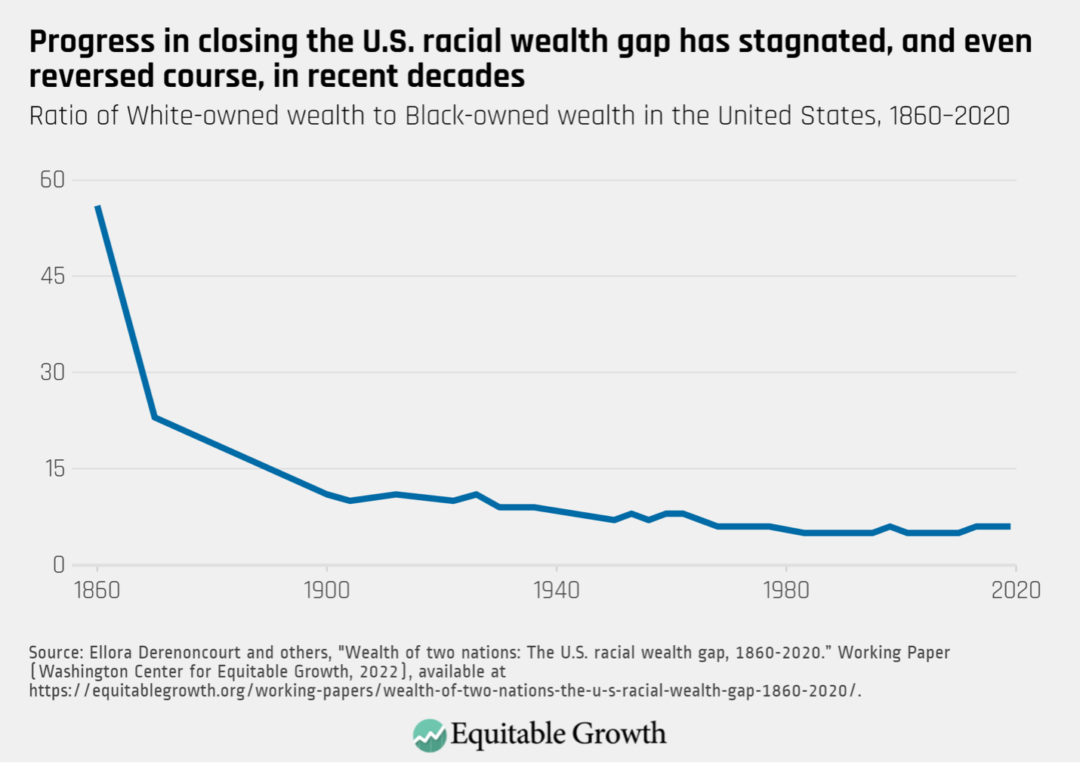

A new working paper seeks to provide more historical insight into the U.S. racial wealth divide. In a first-of-its-kind paper, Princeton University’s Ellora Derenoncourt and her co-authors, the University of Bonn’s Chi Hyun Kim, Moritz Kuhn, and Moritz Schularick, study changes in the racial wealth gap since the end of slavery in the United States. While there have been several studies that look at land-holding and wealth accumulation in specific U.S. states in the late 1800s and early 1900s, this paper is the first to provide historical data that compare Black and White wealth at a national scale.

The four co-authors model cash savings rates and capital gains for Black and White Americans to determine how these factors shape racial differences in wealth over time. One of the paper’s key insights is that while the U.S. racial wealth divide declined dramatically in the immediate decades following the end of the Civil War in 1865, that pace of decline then stagnated for much of the 20th century—and even increased beginning in the 1980s. (See Figure 1.)

Figure 1

The authors find that after the Civil War, during the period of Reconstruction and even in its aftermath in the late 19th century and early 20th century, the White-to-Black per capita racial wealth gap fell from 60-to-1 in the mid-1860s to 10-to-1 by 1920. The initial drop following the end of the Civil War was driven in large part by the substantial relative increase in asset ownership by formerly enslaved Americans, who previously owned little to nothing.

In the decades following, Black people began to secure steady jobs, start businesses, and own land, all of which contributed to the decline in the racial wealth gap as well. Even with the substantial headwinds of the rise of Jim Crow and de jure segregation in early 20th century—as well as the eventual onset of the Great Depression in the 1930s—the racial wealth gap still generally continued to fall.

In the post-World War II era, as the U.S. economy expanded rapidly and the U.S. middle class grew alongside it, wealth accumulation for Black and White families progressed at similar rates. But that move to parallel progress in the mid-20th century also marked the beginning of a long period of slowing, and eventual stagnation, in the convergence of the wealth gap between White and Black Americans, only going from around 8-to-1 in 1940 to around 6-to-1 by 2020—a noticeably smaller drop than over the 80 years before 1940 that the paper examines.

The bulk of contemporary studies of the wealth of Black and White families generally start their analyses in the 1960s, due to the availability of these data. Yet the longer timeframe in this new paper shows that most of the progress in closing the U.S. racial wealth divide actually preceded the 1960s.

Additionally, Derenoncourt and her co-authors spot a disheartening trend starting in the 1980s: Within the past few decades, not only did the historical convergence between rates of Black-owned wealth and White-owned wealth slow and stop, but the White-Black racial wealth gap actually began to widen. This widening is consistent with other contemporary analyses of wealth disparities, but the full range of historical data in this paper paints a stark picture of little progress toward wealth parity since the 1940s—even during periods of dynamic social change and economic growth.

Yet, counterintuitively, these advances were not accompanied by sustained progress on closing the U.S. racial wealth gap. Derenoncourt and her co-authors attempt to clarify why. First, they find, starting in the 1980s, Black income growth started to slow relative to White income growth, which contributed to relatively weaker wealth accumulation among Black workers through savings. This period of time is also when broader U.S. income inequality began to grow.

Homeownership builds wealth for both Black and White households, and in the absence of equity from stocks, homeownership may have led to a greater convergence between Black and White household wealth. But the substantial capital gains registered in stocks since the 1980s enabled White households to experience much greater relative wealth accumulation, given their relatively larger ownership of financial assets.

Interestingly, the authors also model what the racial wealth gap would be if wealth accumulation rates had been equal for Black and White people since the 1860s. They find that even if savings and capital gains rates had been the same since the Civil War, the racial wealth gap would still be half as big as it is now—a significant improvement, but still a large gap, at about 3-to-1.

They argue that because the wealth divide was so large 160 years ago, it is not possible, under current conditions, for Black American families to save or invest their way more wealth parity. In fact, they write, parity is possible at this point only via reparations.

In the absence of reparations, a shift toward greater wealth equity would require dramatic reductions in, or elimination of, racial differences in essential wealth accumulation tools: income, savings, and capital gains. Yet multiple studies, including the one covered here, find that even after equalizing these accumulation factors, it would likely take up to 100 years, if not more, to close the racial wealth gap.

This economic history is critical not just to our understanding of the enduring racial wealth divide, but also to the full accounting of the impact of contemporary economic conditions going forward. While many individuals achieve upward mobility across generations and go on to earn more than their parents did, that mobility is less common now than in the past—particularly among Black Americans.

U.S. economic history also shows that progress can be made, although it is far from guaranteed. As times change, policy solutions should be updated and improved to adjust for changed economic and social conditions. Among the household-level tools available to build wealth, creating stronger pathways to higher-earning jobs for Black people is essential. Homeownership also will continue to be important for wealth building, but would be better if considered alongside a more diversified portfolio of assets—from financial assets held in and outside of retirement accounts, to business ownership, or even possibly social wealth.

But the racial wealth divide will not close from household-level efforts alone. Larger-scale policy interventions—from baby bonds to reparations—must also be seriously considered.

The research is clear: Increased racial equity substantially contributes to U.S. economic growth and to our society’s shared common prosperity. As time goes on, unchecked and growing racial inequalities in the United States continue to cost us in more ways than one. Addressing these disparities that persist from the past to the present is critical, not just for the justice owed to impacted communities, but also because of the limitations these inequities create for current and future opportunity and economic growth.

When a worker gets a new job, it is normally a cause for celebration and not litigation. Yet noncompetition clauses in employment agreements, and a veil of other threats buried in employer paperwork, weaken workers’ freedom to shop their skills in the U.S. labor market. To end unfair competition and boost the productivity of the U.S. economy, the Federal Trade Commission is currently asking the public to comment on a new rule that bans noncompete clauses that some firms force employees and independent contractors to sign as a condition of employment.

My latest research project illuminates a greater scope, prevalence, and variety of anticompetitive practices than has previously been described. “New Evidence on Employee Noncompete, No Poach, and No Hire Agreements in the Franchise Sector” reports the results of an analysis of 17,785 franchise disclosure documents and suggests that rulemaking and enforcement efforts might miss anticompetitive practices that currently lie in the shadows—buried in millions of pages of documents already in the public domain.

My paper raises the concern that research and policy seeking to address anticompetitive practices could be limited by the so-called streetlight effect, or focusing only on the problems that have already been exposed to the light. The FTC rule, for example, cites lawsuits and media reports that have, to date, been a main source of information. While these sources provide substantial evidence regarding noncompete clauses, other methods of unfair competition that are similar to noncompetes remain in the shadows.

There is still time to better describe practices that effectively are noncompete agreements covered by the FTC rule. The agency, on January 8, invited comments and indicated that no poach rings, no hire agreements, nondisclosure, trade secret, proprietary, and confidential information clauses can also be used to threaten and block workers from gaining a different job at a competing firm. More than 12,000 comments from members of the public have already been received, and additional comments are welcome until March 20.

This column details new methods used to pinpoint anticompetitive language in a massive document collection and illuminates some of the lesser-known clauses that can have the same effect as noncompetes.

Open-source machine learning and natural language processing tools can track noncompete clauses and other anticompetitive practices

The findings in my new research paper are the result of a years-long effort to acquire a massive collection of contracts that are already in the public domain and online but which are unable to be researched or analyzed due to inaccessible websites, unsearchable text document formats, unstable links, and a lack of clear software tools or methods to analyze a collection of documents. The evidence gathered includes more than 157,000 documents obtained from websites from the states of California and Minnesota, with a variety of technical challenges overcome along the way.

My paper uses and develops new natural language processing and machine learning methods to count and identify a variety of clauses. Graduate and undergraduate research assistants helped develop and validate “context rules” that are matched with the text. A machine learning model and knowledge tools that can automate the identification of new, unseen cases of anticompetitive conduct are now available as open-source replication materials.

The project initially began as a search for nonsolicitation, or no poach, clauses, but additional language in the franchise documents also carries anticompetitive implications. Based on exact matches with rules that define a no poach clause, 44 percent of franchise filings had a no poach clause from 2011–2022. In addition, 25 percent had a no hire clause that bars franchisees from hiring a worker at another franchise in the same franchise chain. Twenty-six percent had language that approves of or requires franchisees’ use of noncompete clauses.

Language found in the disclosure documents also reveals that despite aggressive enforcement efforts by the Washington state attorney general’s office, approximately 10 percent of disclosure documents in 2022 contained language that bars firms from soliciting or hiring another firm’s workers within the same franchise chain.

The ability to conduct this research is enabled by software called Context Rule Assisted Machine Learning. The open-source method enables researchers to find any concept in any document collection and was developed at Loyola University Chicago’s Quinlan School of Business. My paper compares results between hand-coded data, exact matching with rules, and a machine learning approach that identified a larger number of suspect clauses. A separate paper provides additional methodological details on the construction of the no poach machine learning classifier that can rapidly identify suspected clauses in documents, and is co-authored by me and Stephen Meisenbacher at the Technical University of Munich.

DocumentCloud/Muckrock, a nonprofit organization, now hosts the corpus collected in this research project on its website, where documents can be linked to, annotated, and searched. This research project also received generous support from the Economic Security Project’s Anti-Monopoly Fund, the Loyola Rule of Law Institute, the Loyola Quinlan School of Business, and Loyola University Chicago.

Many more barriers to job mobility exist than just noncompete clauses

In my paper, I caution against regulatory and scholarly focus on only the noncompetition clauses that are known about today. As one practice is blocked, new barriers for workers may emerge. As illustrated above, many ordinary U.S. workers are also required to sign documents of debatable legality that require them to maintain “absolute confidentiality” of “trade secrets” and “proprietary information.” Workers can even face dubious threats upon joining another firm if they have learned new skills and professional methods while on the job.

At Godfather’s Pizza chain restaurants, “information, processes, or techniques” that are generally not considered confidential information are nonetheless covered by nondisclosure agreements if workers learn the information on the job while working for a franchisee. Russo’s New York Pizzeria Restaurant chain requires franchisees to pay costs and expenses for hiring managers from other franchisees and requires management personnel receiving training to sign confidentiality covenants.

With the strongest U.S. labor market in decades, employers can retain workers either with better employment practices or through attempts to limit workers’ freedom to quit. As a stream of research by Evan Starr at the University of Maryland’s Smith School of Business and other work by Matthew S. Johnson at Duke University’s Sanford School of Public Policy, Kurt Lavetti at The Ohio State University, and Michael Lipsitz at the Federal Trade Commission shows, limiting the use of noncompetes and other anticompetitive practices is likely to increase workers’ opportunities in the labor market, boost wages, and increase the number of new firms in the market. When people and knowledge flow more freely and firms compete to attract and retain workers, then the overall U.S. economy can grow faster.

An important 2020 report on competition by the Washington Center for Equitable Growth describes how the federal government can do much more to address growing market power. A whole-of-government approach to labor and antitrust serves the aims of ensuring U.S. workers have good labor market opportunities. The FTC rule is one prime example of this, but other efforts across the government could include using the federal government’s buying power to limit the use of anticompetitive practices.

At the state level, for example, all procurement contracts in Illinois bar firms from restricting employee mobility through noncompetition clauses and ban them from contracting with other firms to “prohibit said independent contractor, subcontractor, or employee from competing, directly or indirectly, in any way with the Vendor.” Such state rules, along with the new FTC rule, illustrate the potential for a wide range of government action to improve the competitiveness of labor markets and protect workers’ fundamental right to quit sand accept better opportunities.

Income support programs transfer cash or other goods, such as food or housing, to workers and families to relieve pressure on household budgets, effectively freeing up income for other needs. These programs are powerful tools to reduce the severity of recessions, help stabilize the broader economy, and ameliorate income volatility by providing income for people with low earnings or replacing income for those who experience a temporary dip in earnings.

The COVID-19 crisis exposed longstanding and deep inequalities in access to U.S. income supports, especially along the lines of race and gender. The executive branch can work to reverse these persistent barriers to access and explore more opportunities to expand the U.S. system of income supports.

The Biden administration and agencies such as the U.S. Department of Labor and U.S. Department of Agriculture can utilize research opportunities to suggest improvements to income support programs and better understand the gaps that remain due to lack of congressional action. Indeed, such action would build on steps that have already been taken, such as implementing and evaluating a navigator program for Unemployment Insurance, studying the implementation of paid leave programs at the state level, and tracking access to the Supplemental Nutrition Assistance Program during the COVID-19 pandemic.

Below, we detail a suite of possible executive actions the administration can take to improve U.S. income support programs and thus better support workers and strengthen the broader U.S. economy. The actions listed here aren’t exhaustive but would go a long way to providing much-needed support to U.S. workers and their families, both in times of economic crises and beyond.

Study the impact of boosting SNAP benefits for children under age 5

Lots of research has alreadybeenreleased on the Supplemental Nutrition Assistance Program and its effects on reducing child hunger, supporting healthy eating, boosting the overall U.S. economy, and lessening the extent and severity of poverty. Research shows that access to SNAP benefits before age 5 leads to large reductions in the incidence of health issues later in life, such as obesity, high blood pressure, heart disease, and diabetes, as well as improving long-term earnings and educational attainment and reducing mortality rates.

Research also suggests that more can be done to amplify the program’s positive impacts by increasing investments in very young children. Hillary Hoynes of the University of California, Berkeley and Diane Schazenbach of Northwestern University propose the creation of a “young child multiplier,” which would increase maximum SNAP benefits by 20 percent for households with children between the ages of 0 and 5. The program has the biggest return on investment for children in this age range because these families tend to need more income support and because investing in children at a pivotal developmental stage can help ensure they are productive, healthy adults.

Because the young child multiplier is a relatively new idea, the Biden administration can introduce a randomized control trial through the U.S. Department of Agriculture, which runs the Supplemental Nutrition Assistance Program, to study its effects on both short- and long-term outcomes with regard to food security, labor force participation, and child and adult health, well-being, and educational attainment.

Conduct an evidence review on the efficacy of different paid leave programs

The United States is the only developed economy without a federal paid family and medical leave social insurance program or guaranteed paid sick days. Yet preliminary research shows that U.S. individuals and employers, as well as the U.S. economy as a whole, can benefit from instituting such a policy. U.S. employees who had access to paid sick leave, for instance, experienced significantly fewer COVID-19 infections and had lower job turnover rates. Research also demonstrates that paid leave programs can increase labor force participation (particularly among women), lead to improvements in child well-being, and increase parents’ time helping children with reading and homework.

The U.S. Department of Labor has tools at its disposal that can help us better understand the main takeaways from research on paid sick days and paid family and medical leave. The department’s Clearinghouse for Labor Evaluation and Research—which assesses the quality of research looking at the effectiveness of policies and programs and makes that research more accessible—can establish paid family and medical leave and paid sick time as topic areas to assess the burgeoning evidence base. This would not only inform the conversation around these policies but would also provide policymakers and stakeholders with important information that could guide further evidence-based improvements.

Create a commission to explore improvements to Unemployment Insurance

Unemployment Insurance acts as an automatic stabilizer when the U.S. economy goes into a recession, reduces poverty rates, stops home mortgage foreclosures, improves health outcomes, and improves job matches between workers and employers. The U.S. Department of Labor has already taken several steps to improve the program, from implementing a new navigator program to establishing equity grants and helping states improve the functionality of Unemployment Insurance applications. Yet more can still be done to improve this vital income support program that helps millions of people every year, despite the many discrepancies in how individual states run this joint federal-state program.

To get a better sense of which improvements would have the most impact, and which states have been most successful in running the program, the U.S. Department of Labor should form an advisory commission similar to those created by Congress. As Equitable Growth’s Alix Gould-Werth and her co-authors suggest, this commission could look into the effects of increasing UI benefit levels and duration, updating minimum standards for eligibility requirements, and reforming financing mechanisms. Another area the commission could explore is improving the collection and dissemination of data related to Unemployment Insurance. This would help policymakers and other stakeholders get a more nuanced understanding of the program and additional gaps that may exist.

This commission would provide federal and state policymakers and stakeholders with a greater understanding of the program and its impact across demographics, particularly as relates to inequity in access to Unemployment Insurance. It also would ensure Congress has the information it needs to design future substantive, evidence-based improvements. Importantly, the commission should include a diverse range of stakeholders—including directly impacted workers and the groups that represent them to center workers in UI policy evaluation and development.

This column is the second in a series by guest authors examining systemic racial, ethnic, and gender inequities in the U.S. economy and in access to government social infrastructure and income support programs—inequities that hinder the full growth potential of our economy and the well-being of our society.

The use of personal care beauty products that contain harmful chemicals impacts the quality of life and life expectancy of women of color and femme-identifying people of color across the United States. The perpetuation of Eurocentric standards of beauty also encourages many of these same individuals to purchase expensive products to lighten their skin and straighten their hair.

These beauty products and cultural expectations that contribute to their use perpetuate health and other socioeconomic inequalities in ways that are emblematic of enduring racial, ethnic, and gender discrimination in the U.S. economy. Yet new data-driven evidence of these broader health and socioeconomic harms for women of color and femme-identifying people of color who use these types of personal care beauty products is sparking new research and new policymaking.

What’s more, these initial policy steps to end traditional Eurocentric beauty standards in U.S. workplaces, alongside increasing demand for natural hair and skin products, may well lead to safer beauty care for women of color and femme-identifying people of color. But before detailing these recent developments, let me first share some important context about the role of dangerous beauty products in these communities.

For us in the Black community, relaxers—products designed to “straighten” curly hair—are a way of chemically straightening hair by breaking down our hair’s protein bonds. A lot of people may choose to relax their hair for different reasons. For some, it’s simply to have a different style. Others say it is easier to handle and work with.

But many in the Black community think it changes how others view them. Straight hair has been celebrated in movies, television, art, and other forms of media that reflect life and culture. As a result, some women straighten their hair because of this influence and ideal that has been perpetuated. In a recent study from the Columbia University Mailman School of Public Health and in close partnership with WE ACT for Environmental Justice, almost half of survey participants who identified as women of color or femme-identifying folks believed that others perceive straight hair as more beautiful, wealthy, and professional.

For me, when I scan the streets for a beauty store that I hope will carry my favorite brand of conditioner to make my kinky 4c hair healthy, I often find a couple of shea-butter-based conditioners from popular brands that don’t really create products for Black hair—a product that promises a glossy finish but looks and smells like pea soup. Now, I’ve always had a tough relationship with my hair. As a child who was tender-headed because of a sensitive scalp, I hated getting my hair done.

While I identify today as nonbinary, I have the experience (and honor) of being socialized as a Black girl. I have so many memories of leaning over the sink, feeling water splash all over my face as I felt the relief of the burning relaxer subside. I got relaxers up until college but also have had braids, twists, and perms—hairstyles containing ingredients and chemicals that can be risky to human health. And in 2014, I transitioned my hair to going natural, deciding to participate in what the Black community calls “the big chop.”

Having spent copious amounts of time in Black hair salons, I looked through many large books of hairstyles that expanded my mind around the possibilities of Black hair. I have also witnessed my mother and other women in my family go through all of the hair changes and styles that have defined the time of Black women—the Bundt, jheri curl, blowouts, and micro braids, all of which also use ingredients and chemicals that are not well-regulated for safety.

As recently as the 1990s, women of color mostly had no clue about the harmful health impacts of relaxers, conditioners, and other personal care beauty products. Today, however, there is so much more information available about the dangers of these beauty care products. Most recently, researchers from the U.S. National Institutes of Health find that women who use chemical hair straighteners and relaxers may have a higher risk of uterine cancer. This new research is worrying because Black women already are at higher risk for pregnancy-related deaths and heart failures throughout the United States. Additional health dangers for Black women linked to harmful beauty products are uterine fibroid tumors and hormone disruption.

These health dangers intersect with the harmful consequences of climate change and existing environmental degradation in many communities of color, leaving women of color facing elevated health disadvantages that are already multiplied by historical health discrimination. Communities of color overall have been disenfranchised, divested, and deprived of critical financial and natural resources due to systemic racial and wealth-based oppression. Many of these communities also have been harmed by environmental hazards that create a cumulative impact on health. All of these factors create a cumulative impact on health that leave women of color with a lower life expectancy.

Then, there are the broader socioeconomic consequences of Eurocentric standards of beauty in the workplace. Former First Lady Michelle Obama, for example, did not feel she could present her natural hair until she had left the White House due to her work as part of the Obama administration. And she is by no means alone in this belief—not least because workers of color still experience pervasive income inequality and job precariousness. In 2020, for example, Hispanic women earned 57 cents on the dollar, compared to cisgender White men, with Black women earning 64 cents, and Asian American and Pacific Islander women earning on a spectrum of 52 cents to 95 cents on the dollar, depending on ethnicity.

As the director of environmental health and education at WE ACT for Environmental Justice, I now spend much of my time collaborating with my colleagues to advocate for the improvement of health outcomes for women of color, specifically as relates to beauty justice, which focuses on safer access to beauty products. In our work, we often find that there are many health issues that can be linked to specific chemicals or products, but changing the behavior of using products is another task.

The cosmetics companies that market their products to women of color and femme-identifying people of color use colorism and Eurocentric white-washing standards to fuel consumerism from their biggest customers. This is an effort to perpetuate and manipulate harmful social standards that will get these groups to buy more personal care beauty products. Black women spend almost $54 million a year on haircare, which is culturally important and necessary for their communities. Latina/o/x communities are also one of the fastest-growing consumers of haircare and other personal care products.

European standards of beauty have penetrated all racial groups and encouraged skin whitening and hair straightening, which poses long-term health problems and worsens health disparities, such as higher rates of breast cancer alongside the other cancer dangers detailed above. By creating looks that are aligned toward these standards, we change the way women, girls, and femme-identifying people of color at large see themselves.

In 2020, WE ACT for Environmental Justice, in collaboration with environmental health scientists Ami Zota and Lariah Edwards at Columbia University’s Mailman School of Public Health, completed a Harlem-focused study of 296 women of color and femme-identifying people of color. When asked about perceptions of straight hair and light skin, 52 percent of participants believed that light skin makes them more beautiful, and 50 percent of participants believed that straight hair makes women look more professional.

In addressing the continuing influence of colorism and Eurocentric standards in these communities, many organizations have taken to creating campaigns that focus on natural hair. Although not exempt from greenwashing, natural hair products and practices offer a healthier alternative to the use of relaxers, chemical straighteners, and other harmful products. In a recent report completed by Grand View Research, the natural hair market is expected to increase by almost 5 percent by 2027 across the gender binary.

Policy is likewise focusing on these issues now. One case in point is the introduction of the CROWN Act, which seeks to prevent hair discrimination specifically for those who do not fit Eurocentric standards.

The message here is clear: The quality of life and the health of women of color and femme-identifying people of color is not for sale. Policies that support holistic and enriching hair and personal care beauty products is the only way to protect these groups of people, who have historically been marginalized in the economy and society.

Signs and demonstrations at the People’s Climate March, Washington, D.C., April 2017.

Addressing climate change is a crucial—and sizeable—economic task. Ensuring equity in every dimension of climate mitigation and adaptation is critical to redressing ongoing harms and environmental injustices. Tracking the implementation of signature climate legislation such as the Inflation Reduction Act and the Infrastructure Investment and Jobs Act, both of which include federal investments to bolster the U.S. clean energy economy, and studying how these laws affect local communities and industries differently is one essential way to ensure equitable outcomes.

U.S. climate policy must also ensure that green infrastructure and jobs are “just,” in that they support front-line communities both historically and currently exposed to the negative consequences of an inequitable system, as well as those workers transitioning from employment in extractive industries who are especially vulnerable to economic risk in the transition. Many of the incentives in the two aforementioned laws will serve to create hundreds of thousands of new green jobs in the U.S. economy—as many as 912,000 per year over the next decade, according to some estimates. A recent study also shows that these jobs tend to be higher-paying than fossil-fuel jobs and tend to be plentiful in communities with fossil fuel extraction industries, two encouraging findings.

Similarly, we need more research and data to better understand the impacts of climate change on labor outcomes, such as employment, job quality, and workplace hazards, as well as on mortality, health, and well-being—and we need more and better data that looks at all of these outcomes across racial and ethnic groups, industries, and geographic regions. This multidisciplinary work can inform policy responses and debates across the environmental, energy, and climate justice movements, as well as within the economics and industrial policy fields.

Climate policy also has the potential to spur economic growth and ensure the U.S. economy remains competitive and resilient. That is why Equitable Growth is committed to fostering more research in this important area that will continue to dramatically shape the U.S. economy and labor market, as well as worker and family well-being, in the coming years and decades. Climate economics is a burgeoning area of interest for Equitable Growth, which has and will continue to fund research on the various economic impacts of climate change and also recently brought on a visiting scholar, environmental economist R. Jisung Park of the University of Pennsylvania, to help expand our work in this space.

As part of the effort to push this research and policy agenda forward, Equitable Growth organized and hosted a panel session on the economic impacts of climate change at the Allied Social Science Associations’ annual conference in early January. The session looked at the existing literature and areas for future research on variation in exposure to climate risk by geographic region, demographic group, and industrial sector, among others, as well as climate change’s potential role in exacerbating economic inequality or hampering economic growth. It also reviewed climate policy options that account for or can address inequality.

The panel was moderated by Park and featured presentations and discussion from Jonathan Colmer at the University of Virginia and the Environmental Inequality Lab (an Equitable Growth grantee), Gregory Casey of Williams College (also an Equitable Growth grantee), Tamma Carleton of the University of California, Santa Barbara and the Climate Impact Lab, and Catherine Hausman at the University of Michigan. Each panelist presented their research on a specific aspect of climate economics:

UVA’s Colmer discussed the work of the Environmental Inequality Lab and his research on how administrative microdata can reveal the impacts of climate change on economic opportunity and environmental justice—especially beyond the place and demographic cells most widely studied to date. Because researchers are constrained by what they can measure and the data that are available, Colmer’s team is working with the U.S. Census Bureau to develop a new microdata infrastructure that looks at individual-level climate effects, rather than place-based effects. As such, they are able to provide new evidence and preliminary findings on the distributional effects of hurricanes in the United States in co-authored research that was funded in part by Equitable Growth. They are also working to estimate the impact that the transition to a clean energy economy will have, not just on census-defined places, but also on individuals within those fine-grained geographic measures.

Williams College’s Casey presented his working paper, co-authored with Arizona State University’s Stephie Fried and Williams College’s Matthew Gibson and funded in part by Equitable Growth, which examines macroeconomic impacts of climate change on economic inequality and growth. Specifically, the co-authors looked at how climate change affects consumption and investment productivity differently, with a focus on sectors most exposed to climate change, and why it’s important for future research to differentiate between the two. The framework they develop in the paper allows for this differentiation, which, in turn, allows for more accurate predictions of future economic damages from climate change. This is not just abstract: Much of the climate adaptation that theory predicts will be crucial to future economic growth requires investments produced by the construction sector, which is among the most exposed to climate-related productivity losses.

UCSB’s Carleton discussed her research on accurately measuring inequalities and damages that result from climate change, at both the global and local levels. Her presentation touched upon her work at the Climate Impact Lab, which seeks to collect local-level data on climate harms, particularly mortality, that can inform and properly target adaptation and mitigation policies. She also discussed how these local data are being applied in California, which has seen a rise in equity-focused climate change adaptation policy and the development of a Climate Vulnerability Metric to show which areas of the state are more at risk of experiencing climate damages. Carleton also discussed how local-level data can improve estimates of the social cost of carbon, or the monetary costs of emitting one ton of carbon dioxide into the atmosphere.

University of Michigan’s Hausman presented her research on market structure and equity considerations for climate change mitigation and adaptation efforts. She discussed some of the existing market failures that exacerbate inequality and injustice, and then reviewed some questions that future researchers can take up in the area of climate policy and environmental economics, such as how energy market failures interact with preexisting sources of injustice and inequality, how racial injustice manifests in the climate space, and how to incorporate harms felt by local communities into both research and policy. Her research points to cascading effects of climate change into markets with equity concerns, a theme that came up repeatedly in this session.

The presentations were followed by a question-and-answer discussion with the audience. Notably, the panelists discussed the limited opportunities for input from nongovernmental researchers in federal climate policy design and implementation—exacerbated by the challenge of working with existing public data amid important privacy restrictions. They also touched upon the importance of economists collaborating outside of the traditional economics space, such as with engineers, experts in racial inequality, and Indigenous scholars, when studying environmental economics and industrial policy.

The panel provided Equitable Growth an opportunity to elevate the need for an equitable response to the climate crisis—one which centers the distributional impacts of mitigation and adaptation policies, especially on groups already vulnerable to climate harms or already facing environmental injustice. We look forward to continuing to engage on this issue both in our grantmaking and academic conference engagement, as well as with policymakers seeking to address climate change and transition to a green economy.

The decisions families make about child care are hugely consequential for each individual child and family, as well as for the U.S. economy as a whole. Yet despite its importance, the child care system in the United States is failing to meet the needs of working families.

The COVID-19 pandemic only exacerbated these problems. Emergency pandemic investments helped keep the child care industry afloat, but those investments did not address many of the underlying issues that have plagued the sector for years. As a result, the COVID-19 recession in 2020 led to a decline in child care workers, and the child care industry is still recovering more slowly than the overall U.S. economy.

But the pandemic is only a piece of this story.

Child care has been systematically disinvested in and deprioritized for decades. This remains the case today despite research showing that investing in child care would have positive reverberations throughout our economy. Such investments would allow parents to reenter the workforce, support positive development among children, and improve working conditions and pay for millions of low-income child care workers.

Below, we detail some executive actions the Biden administration can take to help facilitate the process of providing better child care and boosting the overall economy. The actions listed here aren’t exhaustive, but they would make strides toward providing better support for U.S. children, families, and caregivers, in turn boosting broad-based economic growth and well-being.

Convene state policymakers, practitioners, and experts to review outcomes from the American Rescue Plan’s child care provisions

The American Rescue Plan Act marked a historic, albeit temporary, investment in child care following the COVID-19 recession. Billions in supplemental Child Care Development Fund money and stabilization grants allowed states to develop the policies and infrastructure that could support future, more permanent public investments in child care.

Some states are experimenting with navigator pilot programs similar to Unemployment Insurance to help unlicensed child care providers become eligible for relevant government resources. Colorado and Minnesota have launched their own licensing incentives that make use of navigators providing assistance to caregivers to help them meet licensing requirements. These experimentations are a step in the right direction, but they remain an underutilized tool.

Such lessons and experiments could pave the way for federal pilot programs replicating local success on a national scale. The White House should convene state policymakers, scholars, child care providers, and other policy experts to discuss opportunities for further research and evaluation of lessons learned from this unique investment in child care. Holding such a convening would help key stakeholders learn what works, what doesn’t, and what could be replicated on a broader scale in the future.

Indeed, other policies and ideas could emerge to help improve the supply of child care in the United States. Participants could examine state-level experiments that address the nonfinancial costs of expanding supply and tailored incentives that address unique constraints faced by different providers—both of which have been examined by Gina Adams at the Urban Institute. Relevant data catalogued by Alycia Hardy at the Center for Law and Social Policy, Katherine Gallagher Robbins at the National Partnership for Women & Families, and Clare Waterman at Child Care Aware of America could also be used to help inform discussions.

Convene a summit or create a federal commission on child care deserts

The term “child care desert” has been popularized by researchers, such as Rasheed Malik at the Center for American Progress, to describe areas of the United States with so few child care providers or available slots that there isn’t enough capacity to meet demand. More specifically, this term can be defined as an area where there are more than three young children for every one licensed child care slot.Just more than half of families across the country live in child care deserts, pointing to an urgent deficiency in the supply of child care.

How child care deserts develop, and how they can be eliminated, requires further research and a multidisciplinary approach. Yet due to privacy considerations, independent researchers cannot always access accurate geographic data on home-based or unlicensed child care providers. And while high-quality data can help identify where child care deserts exist, the experiences of current providers, former providers, and families themselves can shed light on how they form in the first place.

Federal agency support can bolster research on this important topic. Through the development of a commission on child care deserts, the U.S. Department of Health and Human Services can convene advocates, researchers, child care professionals, and families to share their expertise and experiences on this topic. These key stakeholders can provide insight into how to best support researchers working with states to collect comprehensive data and recommend solutions to expand the supply of care. A commission also would formalize the concept of a child care desert and, in turn, could help policymakers better target federal resources.

Require the U.S. Census Bureau to provide descriptive child care information and ongoing updates to baseline data on families’ child care arrangements

An accurate understanding of the scope and types of child care arrangements that families use in the United States is crucial, as it allows the government to assess and identify trends among families and across time. Such descriptive data analyses, including updating prior research, can be cost- and time-intensive for independent researchers, but it is invaluable for advocates and policymakers.

The U.S. Census Bureau’s “Who is Minding the Kids?” report, for example, was a great tool for providing information on families’ child care arrangements, but the analysis was most recently conducted in 2013 and used even older data. The Census Bureau should reinvest in this type of research to help provide baseline data on the variety of U.S. child care arrangements. This would not only help stakeholders better understand the lay of the land but also help government agencies cater programs more effectively and better identify needs among families.