When any piece of legislation is considered by the U.S. Congress, it typically goes through a budget analysis to establish its impact on the federal government’s bottom line. These analyses, performed by the nonpartisan Congressional Budget Office, look at the changes in government spending and revenue that may arise over the next 10 years as a result of the proposed bill being enacted, accounting for predicted responses to the law by individuals, firms, and local governments.

The results of these analyses are expressed as budget “scores”—a single dollar amount reflecting the total cost to the government of enacting the legislation—and they are hugely influential in the legislative debate. In fact, bills that are deemed to cost more than they bring in over the 10-year budget window often face very long odds of being enacted, for both rhetorical reasons (claims of fiscal irresponsibility, for example) and procedural ones (such as so-called Pay as You Go rules in the House and Senate, which can require super-majority vote thresholds to waive).

While these budget analyses are useful tools to allow policymakers to evaluate potential future effects on the federal budget, they are not foolproof. Indeed, our recent paper shows that CBO scores for income support programs that provide assistance to low-income families with children in particular miss the mark.

Income support programs are part of a broader network of social infrastructure that provides essential assistance to families. Social infrastructure that specifically targets families with children can take the form of direct cash or near cash transfers to children, investments in child care, early education, paid family leave, and family services, and financial support through the tax system.

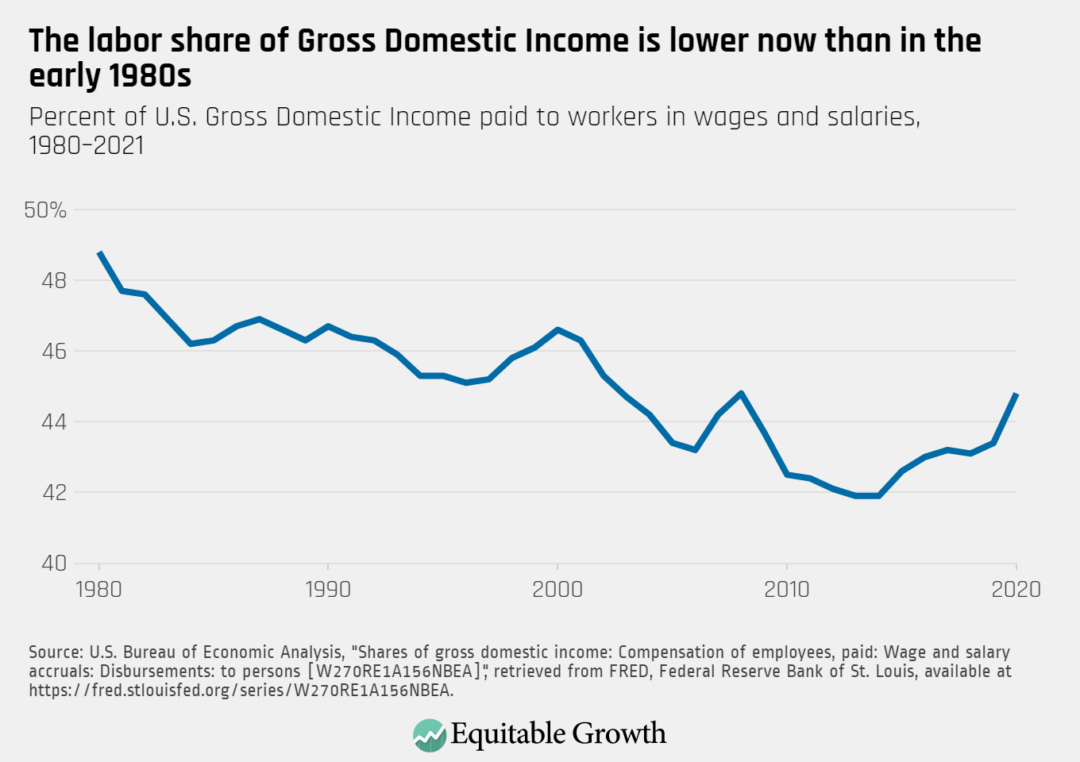

Studies show that countries that provide less of this kind of support to families with children have higher rates of child poverty. According to data from 37 countries in the Organisation for Economic Co-operation and Development, for example, the United States spends less on social infrastructure programs as a share of Gross Domestic Product than most other high-income countries. At the same time, in the same group of 37 countries, only Turkey and Costa Rica have higher rates of child poverty than the United States.

The fact that the United States spends so little, compared to peer countries, on social infrastructure can be explained in part by a previous emphasis on the immediate behavioral effects of these programs on parents (such as impacts on labor supply decisions), rather than a focus on the vast returns these investments in children and their human capital yield down the road. In other words, economists and policymakers alike have paid too much attention to costs in the short term and not enough to the benefits over the long run.

This focus led to a bias toward austerity and away from public spending on important programs that support children and boost their outcomes in adulthood. As a result, U.S. income support programs in particular have largely shifted from unconditional cash transfer programs to conditional transfers based on parental work requirements. This change in policy has been driven by policymakers seeking to avoid certain behavioral effects—for instance, parents staying out of the labor market or delaying marriage in order to remain eligible for certain targeted programs—that could arise from various design elements of income support programs, such as who the aid targets, how it is delivered, and whether there are any conditions for eligibility.

The evidence is mixed on whether this policymaking strategy has succeeded in affecting these behaviors. But what is clear is that it means families have more difficulty accessing the programs they need, and these programs are not working at their full capacity to keep U.S. children out of poverty. Likewise, this short-sighted policy approach ignores the many long-term benefits to children—and to society and the broader economy—of income support programs.

To be fair, economic research also largely tended to focus on the short-run costs of income support programs. Our recent paper finds that of 239 articles examining such programs since 1968, only 40 percent looked into the benefits of programs such as the Earned Income Tax Credit, Medicaid and the Children’s Health Insurance Program, Temporary Assistance for Needy Families and its predecessor, Aid for Families with Dependent Children, or the Supplemental Nutrition Assistance Program. Prior to 2010, that number was less than 27 percent.

Often, when researchers did examine benefits, they were in the short term, such as the impact of Medicaid on infant mortality or the link between access to SNAP during pregnancy and the birth weights of newborns. It wasn’t until research began to examine the long-run outcomes for children attending high-quality preschools—such as the Perry Preschool or Abecedarian programs and, later, Head Start—that economists broadened both their time horizons and how they define human capital benefits.

These studies changed how researchers evaluated income support programs, from the timeframe and types of outcomes studied to the incorporation of noncognitive benefits. This, combined with studies examining declining economic mobility in the United States, spurred researchers to look more closely at how economic conditions in childhood shape future outcomes in adulthood.

Newer studies are better able to examine the long-term benefits of income support programs on children, and many find that the most effective interventions are those that children receive between birth and age 5. These research projects look at such impacts as college admission and completion rates, future neighborhood quality and homeownership rates, reliance on income support programs and poverty levels as adults, income and earnings in adulthood, connection to criminal justice system, and even physical and mental health outcomes. Studies also now find that programs that target children deliver very large returns on investment for the government, and even pay for themselves in the long run, compared to programs that target adults.

This research boom over the past decade—in which 2.5 articles examining benefits have been written for every article on disincentives—should signal to policymakers that their fixation on the short-term costs rather than long-term benefits isn’t giving them the full picture they need to properly evaluate the impact of social infrastructure policy. The Congressional Budget Office limit its budget analyses to 10-year periods—a timeframe that clearly does not capture the adulthood outcomes of a program delivered to a child before age 5 but does capture the short-term costs to the government of implementing such programs. And that 10-year window is an extremely narrow view of what outcomes constitute human capital gains.

While this focus on the short-run costs is explainable—it is indeed easier to understand the effects of a policy using data available in the moment than it is to estimate benefits that won’t be fully known for two or three decades—it ignores the fact that these programs are more than income supports that bolster consumption in the current moment. These programs represent investments in our children’s human capital—and the returns on these investments should be measured well into the future and using a variety of metrics.

post

post

post

post

Our paper shows that researchers have already begun to widen their lens when it comes to examining the benefits of income support programs. We suggest ways they can offer further support, including by improving our understanding of why the estimated impacts of various programs on children differ across populations and environments, and whether it’s possible to use evidence on short-term impacts to predict long-term outcomes.

The COVID-19 pandemic led to a temporary shift away from austerity in income support programs. But the policies providing extra assistance to U.S. families over the past 2.5 years have largely expired, erasing many of the gains that were achieved in that period, such as the drastic cut in child poverty from the expanded Child Tax Credit. Research shows these measurable short-term gains for children, if sustained, would have long-term benefits.

Policymakers, alas, have yet to make adjustments to their budget scoring practices. Congress would do well to act, adopting longer timeframes when performing budget analyses on programs that affect children or finding another way to consider the long-run benefits of these programs. Without a shift, these vital investments in our future workforce will continue to be pushed to the back burner because an incomplete picture of their effects on society and the broader U.S. economy minimizes what our nation truly has to gain from these programs.