The breadth of the economic impact of the COVID-19 pandemic ushered in sweeping, albeit temporary, changes to income support programs and tax policies in the United States. These changes include broadening and making more generous the Child Tax Credit—a move that, paired with other emergency programs, is credited with reducing U.S. child poverty by up to 40 percent—and expanding Unemployment Insurance to pay out at higher levels and for longer periods than before the pandemic, as well as to groups previously not eligible for UI benefits, such as gig workers.

Now, a few years later, researchers are taking a critical look at the impact of these temporary policies and what policymakers can learn for future implementation. Previous work has uncovered some drawbacks to the expansion of these income support programs, but there is no denying that they reduced poverty and hardship among U.S. workers and families because the unconditional nature of the cash allowed families to spend the money how they needed to stay afloat during the economic downturn.

This column will look first at new research on the Child Tax Credit and Unemployment Insurance amid the COVID-19 recovery, before turning to implications for future policymaking.

The expanded Child Tax Credit

Although efforts to make modest expansions to the Child Tax Credit failed in Congress earlier this year, the impact of the temporary CTC expansion in 2021 remains an active conversation in policy circles, especially as some of the 2017 changes to the credit are set to expire in 2025.

Recently, the Annals of the American Academy of Political and Social Science, a leading academic journal, published an entire publicly accessible issue on evaluating the effects of the 2021 expansion of the Child Tax Credit. Edited by Megan Curran of the Center on Poverty and Social Policy at Columbia University, Hilary Hoynes of the University of California, Berkeley, and Zachary Parolin of Bocconi University (also an Equitable Growth grantee), this issue provides a comprehensive look at several studies that assess the outcomes and impact of the expanded credit. The research in the volume examines the impact of the expanded Child Tax Credit on food insecurity, spending, parents’ psychological well-being, parents’ employment, racial and ethnic economic inequalities, and child developmental outcomes, along with estimating the effects of permanently expanding the credit.

Highlights from the issue include:

- The expanded Child Tax Credit caused food insufficiency to decrease by around 25 percent and food insecurity to decrease by 15 percent, with stronger effects for the lowest-income households and those headed by a person of color, according to a survey of research by Equitable Growth grantee James Ziliak of the University of Kentucky and his co-authors.

- The CTC expansion was associated with a narrowing of income inequality between Black and White households and between Latino and White households in the lower half of the income distribution, according to research by Equitable Growth grantee Bradley Hardy of Georgetown University and Charles Hokayem of the U.S. Census Bureau.

- Higher-income households tended to save money from the expanded Child Tax Credit, while lower-income households tended to spend the money, according to a survey of research by Equitable Growth grantee David Johnson of the National Academies of Sciences, Engineering, and Medicine, Jonathan Fisher of the U.S. Census Bureau (Equitable Growth’s former Research Advisor), and Jake Schild of the Bureau of Labor Statistics. Among families who spent the money, it was mainly used for basic household needs (food and rent) and for their children (child care and school supplies).

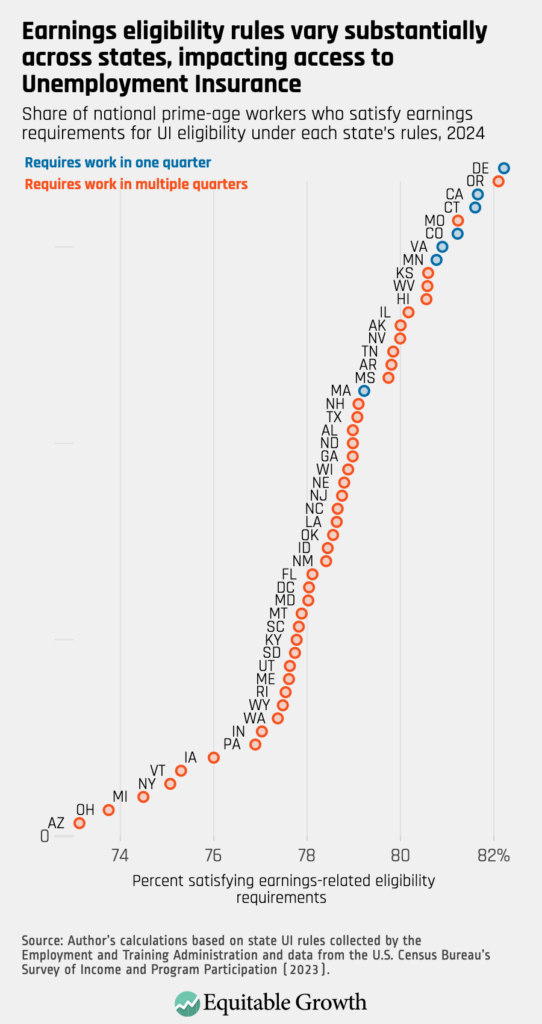

Expanded Unemployment Insurance

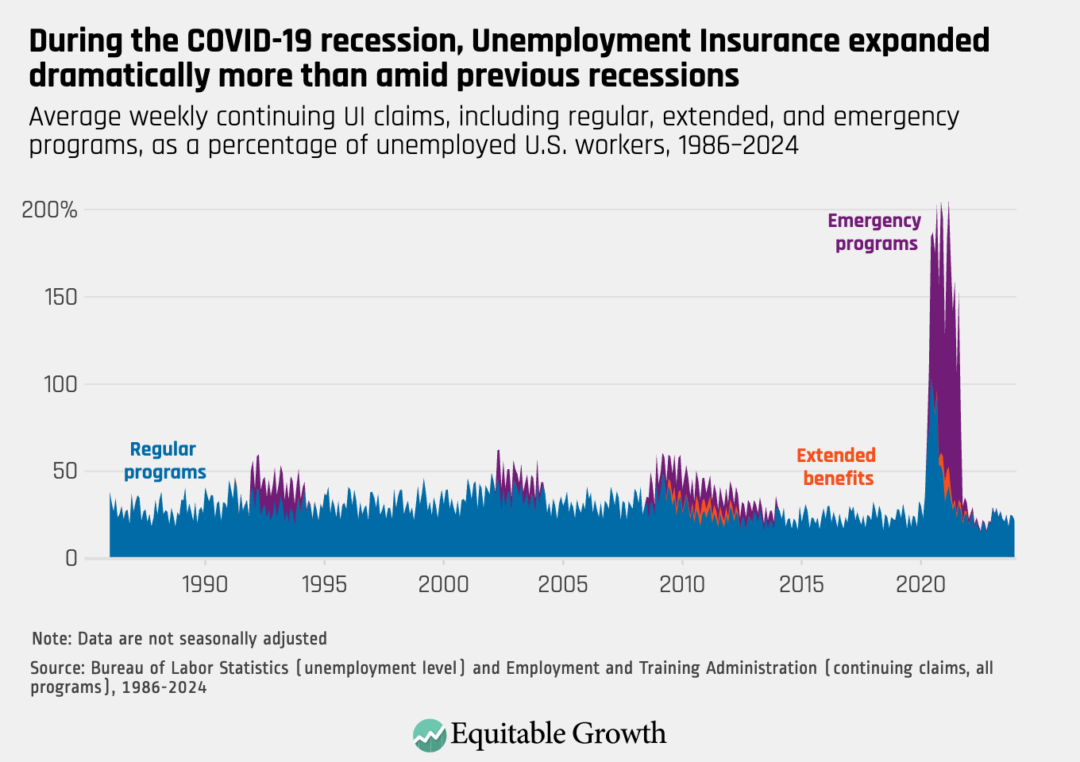

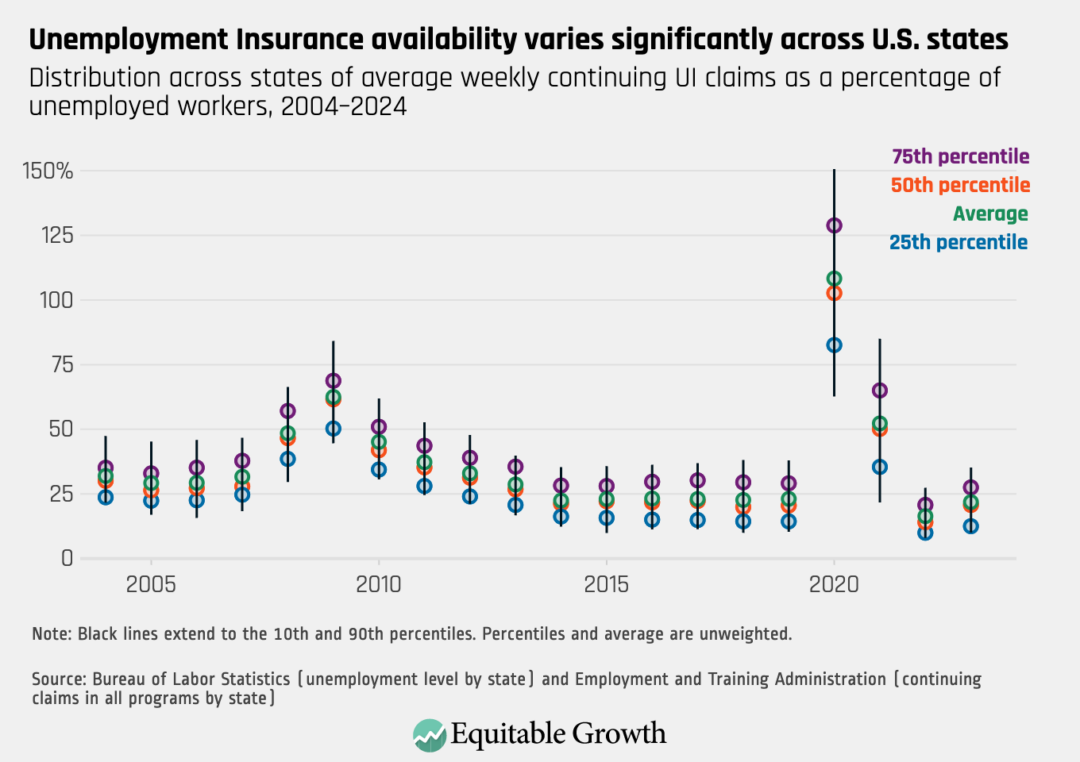

In response to the massive job losses early on in the COVID-19 pandemic, Congress passed several expansions to Unemployment Insurance benefits, including increased benefit amounts—a $600 per week increase from April 2020 to July 2020 and a $300 per week increase from late December 2020 through early September 2021—and expanded eligibility to self-employed and gig workers, who previously were not able to access this program.

Research by Equitable Growth grantees and University of Chicago professors Peter Ganong and Pascal Noel, along with their co-authors, finds that these expanded benefits had a significant impact on spending among unemployed households. While receiving the $600 supplement, for instance, unemployed households’ spending increased relative to when they were employed.

At the same time, the paper finds that the Unemployment Insurance expansion had a minimal impact on those workers finding employment because the benefits were temporary and were distributed in the context of a difficult job market. According to the researchers, these findings imply that countercyclical supports such as these should be considered during future economic downturns as a way to boost consumer spending.

Challenges with disentangling the impact of COVID-19 policies

Given the overlapping time periods of the expansions of the Child Tax Credit and Unemployment Insurance, along with three rounds of Economic Impact Payments in 2020 and 2021, disentangling the impact of these policies is challenging. It is hard to discern whether an improved outcome is the result of one policy alone or a combination of the expanded programs.

For example, Bruce Meyer of the University of Chicago and his co-authors contend in their recent study that some of the significant decrease in poverty in 2021 has been misattributed to the expanded Child Tax Credit. They argue that although the CTC expansion played a role, expanded Unemployment Insurance and the stimulus checks had a bigger impact on improving well-being among U.S. workers and families.

Conclusion

While it may be important when designing future policies to know exactly which COVID-era policy had the most impact for struggling Americans, the fact remains that overall U.S. poverty, and especially child poverty, decreased significantly in 2021 (using the Supplemental Poverty Measure) and increased again after the expiration of these programs in 2022. The common link is that each of these programs provided unconditional cash to families, which they were able to use for household necessities or to enrich their children’s lives, pay down debt, or save for future emergencies.

Research on both the expanded Child Tax Credit and guaranteed income programs (see, for example, findings from Stockton, California), indicates that unconditional cash has a significant impact on families’ well-being. Whatever the specific contours of future anti-poverty proposals that policymakers consider, this research shows that unconditional cash should be a key focus.

Did you find this content informative and engaging?

Get updates and stay in tune with U.S. economic inequality and growth!