Fast facts

This report focuses on preliminary research surrounding the three largest income support programs totaling $1.6 trillion that were paid directly to U.S. individuals, workers, and families amid the first two years of the COVID-19 pandemic: economic impact payments, Unemployment Insurance, and the expanded Child Tax Credit. The report finds that:

- The economic impact payments were effective at increasing consumption, though changes in consumption patterns may have limited the extent to which the payments stabilized employment and the broader economy.

- Expanded Unemployment Insurance was roughly equally effective at stimulating consumption as the direct stimulus payments despite initial UI claims backlogs and concerns about fraud, though some troubling UI claims disparities by race and ethnicity and gender exist across states.

- The temporary expansion of the Child Tax Credit delivered long-run benefits for kids and parents, too, with little to no impact on the U.S. labor market.

Together, these three pandemic-related programs were effective at bolstering consumption and insuring workers against the sudden and swift loss of jobs in 2020. Yet expansions of Unemployment Insurance and the Child Tax Credit faced implementation problems that in some cases stood in the way of more equitable access and thus tempered the kick to economic growth that would have otherwise occurred.

Overview

How well did federal policy stabilize the U.S. economy and alleviate hardship during the COVID-19 pandemic? This report focuses on preliminary research surrounding the three largest income support programs that were paid directly to U.S. individuals, workers, and families: economic impact payments, Unemployment Insurance, and the expanded Child Tax Credit.

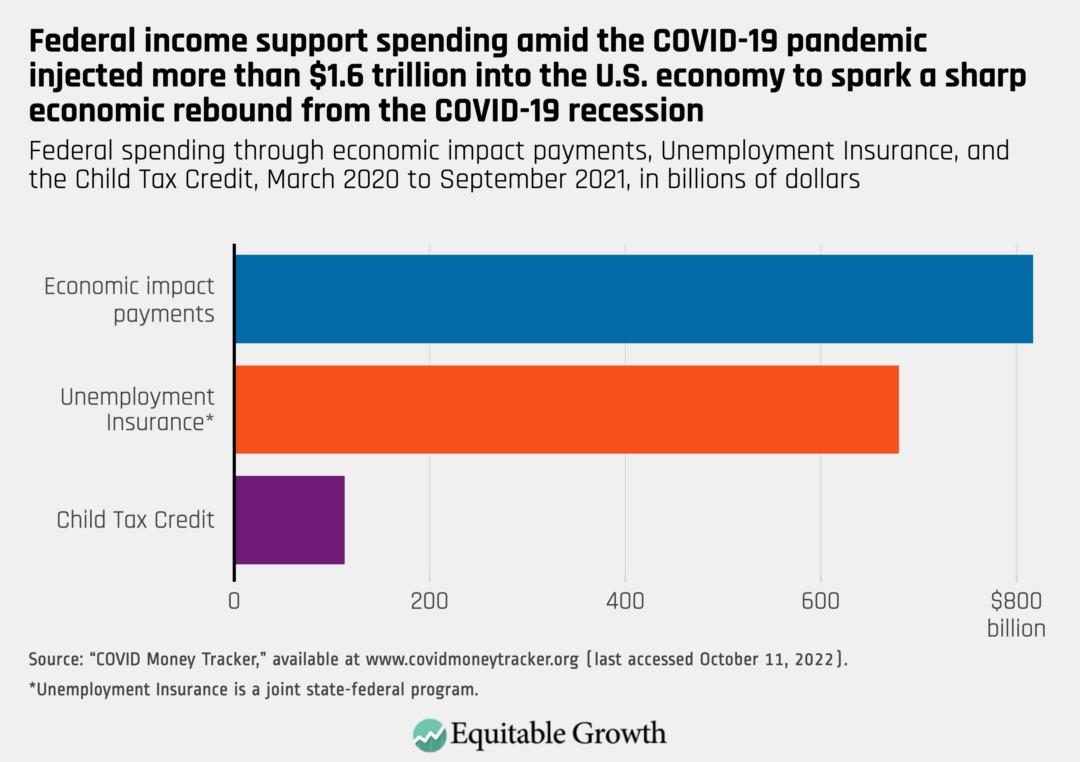

Economic impact payments were composed of three rounds of untargeted direct stimulus payments sent to most Americans and legal residents of the United States between April 2020 and March 2021, totaling $823 billion in government spending, according to current estimates by the nonpartisan Committee for a Responsible Federal Budget.1 Unemployment Insurance was temporarily expanded through September 2021, at an estimated cost of $680 billion, to include more workers, last longer, and elevate the income support levels of the program. Finally, the Child Tax Credit was expanded, at an estimated cost of $113 billion, through March 2022 to allow for near-universal eligibility and higher income support levels paid out monthly instead of annually over the course of the expanded program. Figure 1 compares spending across these three programs. (See Figure 1.)

Figure 1

Two goals motivated U.S. policymakers to support these transfers to individuals, workers, and families. They wanted to stimulate the U.S. economy by bolstering consumption. And they wanted to alleviate the hardship of those most severely affected by the onset of the pandemic and the resulting recession in 2020.

Generally speaking, recent research on Unemployment Insurance during this period examines both goals, whereas research on the pandemic stimulus payments focuses on evaluating how consumption affects economic growth, and research on the Child Tax Credit focuses on mitigating the impact of the pandemic on child well-being.

How well did the three spending programs meet these two policy goals? Preliminary research shows that the economic impact payments were effective at increasing consumption, though changes in consumption patterns may have limited the extent to which this, in turn, stabilized employment and the broader economy.

Expanded Unemployment Insurance was roughly equally effective at stimulating consumption as the direct stimulus payments. Despite initial UI claims backlogs and concerns about fraud, the rate at which income support for those out of work through no fault of their own eventually reached those who needed the financial support was very good when judged by prior benchmarks, though some troubling UI claims disparities by race and ethnicity and gender exist across states. While expanded UI benefits greatly increased take-up among the unemployed, existing evidence suggests that they had only limited negative impacts on the rate at which claimants returned to work.

The temporary expansion of the Child Tax Credit was another policy step taken to combat the COVID-19 pandemic and recession, and likely delivered long-run benefits for kids and parents, too, with little to no impact on the U.S. labor market. While a permanent expansion of the Child Tax Credit would likely entail some work disincentives for otherwise-ineligible low-income families, the gains not only to equity but also to the productivity of the next generation of workers seem likely to be considerable.

So, the preliminary research on these three pandemic-related programs indicates that, together, they were effective at bolstering consumption and insuring workers against the sudden and swift loss of jobs in 2020. Yet researchers have called into question the extent to which the consumption sparked by these three direct spending programs stabilized the U.S. economy due to shifting demand patterns caused by the public health crisis. While expansions to Unemployment Insurance and the Child Tax Credit broadened the scope of who was covered, implementation problems in some cases stood in the way of more equitable access to these two income support programs and thus tempered the kick to economic growth that would have otherwise occurred.

In the pages that follow, this report will examine each of these three programs in turn and in more detail to see what worked and explore the implementation challenges. The report will then pose some open research questions about each of the programs that still need to be researched and suggest some policymaking takeaways for each of them.

Economic impact payments

Economic impact payments were a series of three stimulus checks sent by the federal government to bolster consumption between April 2020 and March 2021. Generally speaking, the levels of each round of payments were $1,200 per adult and $500 per child in the first round, $600 per family member (adult or child) in the second round, and $1,400 per family member in the third round. The full payments were generally available to U.S. citizens and legal residents with work authorization earning less than $75,000 a year. (See Figure 2.)

Figure 2

What worked

Most of the research to date on the economic impact payments finds that they were effective at stimulating consumption. Although these payments are relatively easy to implement, two key limitations of direct stimulus payments are their lack of targeting at individuals who would be more likely spend most or all of the money and the program’s inability to zero in on discrete segments of the U.S. economy that were hardest hit by the pandemic.

Researchers find that stimulus transfers increased aggregate spending by between 10 percent and 46 percent of the total government outlay and were most effective at stimulating consumption when they reached liquidity-constrained individuals.2 Economists David Johnson at the University of Michigan, Jonathan Parker at the Massachusetts Institute of Technology, and Jake Schild and Laura Erhard at the U.S. Bureau of Labor Statistics analyzed the BLS Consumer Expenditure Survey, finding that the immediate spending response to receiving an economic impact payment amid the COVID-19 pandemic was lower than the response recorded from the 2001 and 2008 tax rebate programs, but spending responses were stronger for those who are liquidity-constrained.3 They estimate that, on average, roughly 10 percent of the payments were spent on nondurable goods and services within 3 months.

Other work estimated larger propensities to consume from the COVID-19 economic impact payments.4 Economists Ezra Karger and Aastha Rajan at the Federal Reserve Bank of Chicago analyzed data from bank accounts to estimate a marginal propensity to consume from these payments of 46 percent.5 Their estimates were higher for individuals who appear to live paycheck to paycheck (60 percent) and much lower for individuals who save more (24 percent). They find similar patterns after the second round of payments. Had payments been better targeted at individuals who live paycheck to paycheck, they estimate that the same government outlay could have increased consumer spending by nearly twice as much.

Scott R. Baker at Northwestern University, R.A. Farrokhnia and Michaela Pagel at Columbia University, and Constantine Yannellis at the University of Chicago used data from an application designed to help people save and find that economic impact payment recipients in their sample spent 25 percent to 40 percent of the payments.6 They find that U.S. households with lower income, greater income drops, and lower liquidity had stronger propensities to consume and note that liquidity was the most important of those three factors in determining the rate at which households consumed.

In their analysis of bank account transaction data, Natalie Bachas and Arlene Wong at Princeton University, Peter Ganong, Pascal J. Noel, and Joseph S Vavra at the University of Chicago, and Dianne Farrell and Fiona E. Greig at J.P. Morgan Chase & Co. also conclude that patterns suggest the stimulus payments likely played an important role in limiting spending declines from job losses at the start of the COVID-19 pandemic.7

But the extent to which increased consumer spending reached those businesses most impacted by the pandemic has been called into question. Economists Raj Chetty and Nathaniel Hedren at Harvard University, John N. Friedman at Brown University, and Michael Stepner at the University of Toronto find that the economic impact payments were effective at increasing spending for households in low-income ZIP codes but did not meaningfully increase spending for households in high-income ZIP codes.8 They find that because businesses in higher-income ZIP codes suffered greater losses in revenues near the start of the pandemic, government spending did not reach those businesses most in need and ultimately resulted in only modest gains for employment.9

Implementation challenges and demographic disparities

By virtue of this program’s untargeted design, the scope for the direct stimulus payments to cause very disparate impacts across demographic lines was limited, except insofar as the payments were available only to U.S. citizens and legal residents with work authorization. Still, even the process of distributing the economic impact payments was not without its challenges, many of which caused additional hurdles for more-vulnerable people.

Dan Murphy at The Brookings Institution chronicles the implementation challenges that arose in getting payments out in a timely fashion and in electronic form. Relative to the stimulus payments during the Great Recession of 2007–2009, payments were distributed more slowly. He reports it took almost 4 months to distribute 90 percent of the payments and 6 months to distribute 95 percent.10 This may be because even though individuals did not have to pay taxes to qualify for the payments, the IRS relied on prior years’ tax filings to automatically send payments, which were direct-deposited if the filings contained bank account information but were sent as paper checks if not. Indeed, David Johnson and his co-authors estimate that 35 million Americans and legal residents in the country were qualified for economic impact payments but did not receive them automatically.11

When preparing to make the direct stimulus payments, the IRS coordinated with other government agencies to find eligible individuals and made available an online tool for individuals who did not file tax returns to claim the benefits and supply bank information. Aside from identifying eligible individuals, however, the IRS did not always have bank account information to make the payments via direct deposit. Brookings’ Murphy estimates that as many as 10 percent of recipients may have gotten paper checks, despite having a bank account that accepts direct deposits. He estimates the paper checks may have resulted in a substantial cost paid to check-cashers—perhaps as much as $66.6 million.12 This likely would have been a cost borne disproportionately by those who were already more financially vulnerable.

Open research questions

While most research to date focuses on the consumption effects of the stimulus payments, which is generally viewed as the prime objective of the policy, less focus has been applied to other effects of the program. In particular, estimates of the effects on the supply of labor in the U.S. economy due to the direct stimulus payments would be helpful in comparing this policy to other policies surveyed in this report. This kind of research also could provide a deeper understanding of how increased consumption from the economic impact payments helped to alleviate material hardship.

Policy takeaways

The COVID-19 economic impact payments were relatively effective at bolstering consumption. Hypothetically, had they been better targeted at liquidity-constrained individuals, they could have achieved the same outcome at substantially less cost to the federal government. But because the government cannot observe liquidity (and income is not thought to be a good proxy for liquidity), there is no clear recommendation from the research community on how the direct stimulus payments could have been better targeted to increase consumption.13 The simple and untargeted nature of the payments likely also facilitated swifter passage through the U.S. Congress.

In addition, changing consumption patterns due to social distancing measures amid the pandemic likely muted the potential for this form of stimulus to stabilize the U.S. economy. Because little of the increased consumption reached the businesses hardest hit by the pandemic, the effectiveness of the funds at saving jobs was thought to be only modest.

The Child Tax Credit

Unlike many government income support programs, the Child Tax Credit is not targeted at lower-income households. Prior to the COVID-19 pandemic, the Child Tax Credit was generally unavailable to lower-income taxpayers, instead going to only those households with sufficiently high earnings. Before it was expanded amid the pandemic, the credit allowed for a reduction in tax liability of up to $2,000 per child less than 17 years of age. A maximum of $1,400 of it was refundable, meaning that a taxpayer could receive money back if the credit reduced their tax liability below $0. Refundability, however, was limited for lower-income taxpayers due to the way in which the formula was tied to earned income.

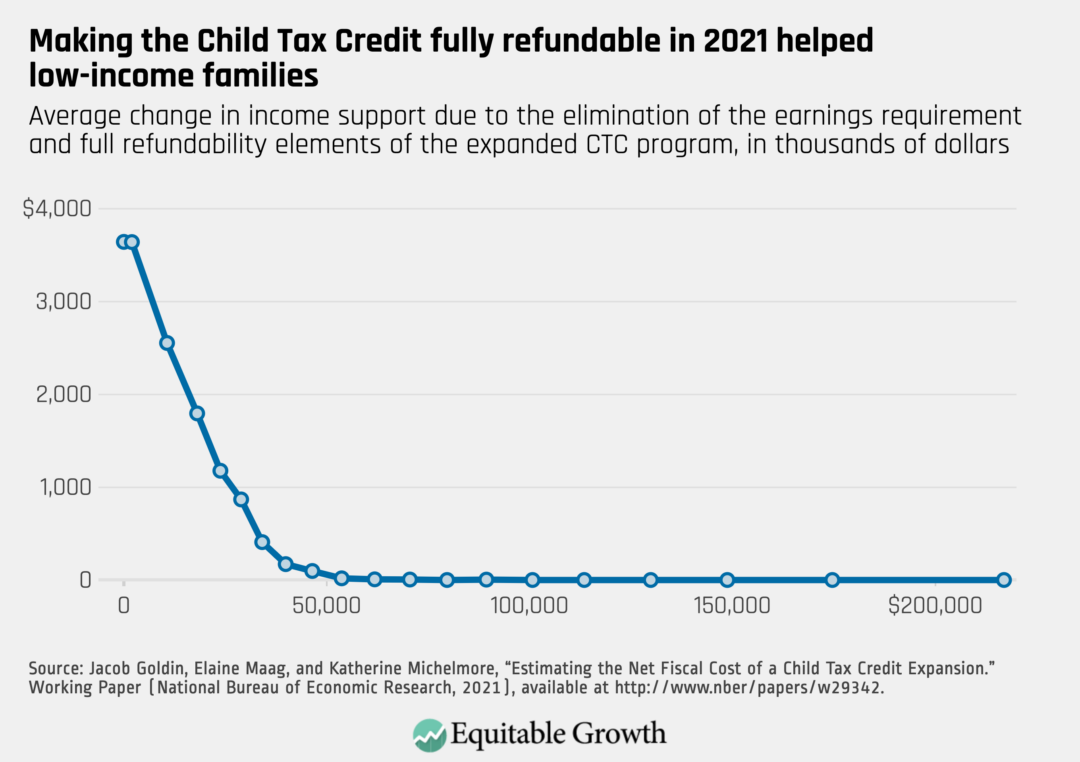

During the pandemic, three temporary changes in 2021 transformed the Child Tax Credit into what more closely resembled a universal child allowance. First, eligibility was greatly expanded because the credit was made fully refundable and the earnings requirement was dropped. Second, the maximum amount was raised to $3,000 per child ages 6 to 17 (inclusive of 17) and $3,600 per child less than 6 years of age. And third, families could receive nearly half of the credit in advance through six monthly payments during the second half of 2021 (each of $250 to $300 per child, with the remainder paid after filing 2021 taxes in 2022). All of these changes have since been allowed to expire, returning the program to its original design as described above.

Making the Child Tax Credit fully refundable and eliminating the earnings requirement primarily affected low-income households (See Figure 3), while the other changes affected families across the income distribution.

Figure 3

What worked

Early evaluations of the temporary expansion of the Child Tax Credit generally find that it increased well-being with limited or no detriment to the U.S. labor supply. Recent research by economist Zachary Parolin and his co-authors at Columbia University estimates that the CTC expansion reduced food insecurity in the United States by 25 percent and U.S. child poverty by 40 percent.14

Subsequent and more detailed research by Parolin and his co-authors compares changes in U.S. labor supply around July 2021 for households with children versus those without in the Consumer Price Survey data and the U.S. Census Bureau’s Household Pulse data.15 These findings show no consistent differences in the monthly employment outcome of these two groups around the time of the CTC expansion, offering some support to the argument that the temporary changes did not induce large labor supply effects.

While the temporary expansion may not have impacted employment, some debate exists about how to gauge the effects should policymakers consider a permanent expansion of the program. Most research on this topic simulates the effects of such a permanent policy using estimates of labor supply elasticities from the academic literature on the subject, of which there are a range. Using one set of elasticities, simulations by Jacob Goldin at the University of Chicago, Elaine Maag at The Urban Institute, and Katherine Michelmore at the University of Michigan suggest that the labor supply effects of a permanent expansion would be small.16 Furthermore, their simulations take into account that providing financial support to low-income families with young children will likely have positive effects on their labor supply in adulthood, which they benchmark to studies on the Earned Income Tax Credit, another federal income support program specifically targeting low-income workers and their families. These positive effects of the Child Tax Credit partially offset the costs of expansion in the long run.

Other simulations by Irwin Garfinkel, Elizabeth Ananat, Robert Paul Hartley, and Christopher Wimer at Columbia University also conclude that the expansion would have substantial positive returns.17 In contrast, Kevin Corinth, Bruce D. Meyer, Matthew Stadnicki, and Derek Wu at the University of Chicago use a different set of behavioral elasticities, finding that such an expansion would substantially disincentivize work—which, they emphasize, would partially reduce the effectiveness of the program at relieving child poverty.18 They conclude that other means-tested programs would be more effective.

Although recent debates center around the magnitude of U.S. labor supply effects of a proposed permanent CTC expansion, a very large and established body of literature finds beneficial effects of similar financial transfers to children. Key benefits identified are in the areas of health, education, and adulthood earnings. A thorough review of this literature can be found in the congressionally commissioned report in 2019 by the National Academies of Sciences, Engineering, and Medicine.19 Another recent review focused on weighing the costs and benefits of such programs.20

Though the expansion of the Child Tax Credit was primarily framed as a tool for alleviating hardship amid the pandemic, it is reasonable to expect that its expansion to lower-income families also benefited fiscal stimulus efforts. Research on consumption propensities from the expanded CTC program is sparse, but evidence that lower-income households had higher propensities to consume from the economic impact payments suggests that the eligibility expansion of the Child Tax Credit may have helped further fiscal stimulus goals.21

Implementation challenges and demographic disparities

While the expansion of the Child Tax Credit was effective at removing the design aspects of the program that disproportionately excluded low-income families, research during the pandemic suggests that more subtle barriers still lingered. Prior to the expansion, large disparities in eligibility existed by income and race. The University of Chicago’s Goldin and the University of Michigan’s Michelmore report that most households in the bottom tenth of the income distribution were ineligible for any of the credit, and most households in the bottom third were eligible only for a part of the credit.22

The two researchers also find that only half of Black and Hispanic children were eligible for the full credit, while the rate among White, non-Hispanic, and Asian American children was three-quarters. Because eligibility is determined by family income, they further find that many single mothers did not have enough income to access the benefit, which disproportionately impacted Black children, who are more likely to live without their fathers.23

Although the CTC expansion went a long way toward removing key structural barriers leading to the racially disparate impacts of the CTC program, researchers are still analyzing data to ascertain who was left out amid the pandemic expansion and why. Early survey evidence reported by Michelmore and her colleague at the University of Michigan’s Gerald R. Ford School of Public Policy, Natasha Pilkauskas, suggests that approximately two-thirds of very low-income families received monthly CTC payments.24 While some did not receive the payments for valid reasons—for instance, they opted for one lump sum in 2022—questions still surround why roughly 1 in 5 low-income families did not receive payments.

A remaining barrier may be that families who wouldn’t ordinarily file taxes may not have known about their newfound eligibility. Indeed, families with little or no earnings had substantially lower rates of receiving the expanded Child Tax Credit in the first several months of the expansion. Language barriers may also have imposed barriers. Pilkauskas and Michelmore find lower rates of receipt among respondents who took the survey in Spanish, despite high rates of tax filing.25

Open research questions

Many open questions still surround the recent CTC expansion. There is room for more research to estimate the labor supply effects of the temporary expansion. Empirical estimates of the actual impact of these payments on consumption would be helpful in planning future fiscal stimulus programs, particularly given early survey evidence that parents were primarily planning to save the payments for emergencies.26 Although similar income supports have been shown to increase the well-being of children, there is scope to better understand the short- and long-term effects of the Child Tax Credit itself on the well-being of kids and their parents, including in the domains of health, foster care, and crime.

Given the near-universal coverage of the Child Tax Credit that would continue if the expansion were made permanent, attention also should be given to assessing whether existing estimates of the benefits of financial support for children on their well-being are as large when applied universally as opposed to a small number of families—taking into account so-called general equilibrium effects. These effects are economic parlance for the notion that increasing everyone’s qualifications might not benefit a particular person as much increasing just that person’s qualifications. Finally, more research is needed to understand how potential labor supply effects of an expanded Child Tax Credit would interact with other pieces of the federal tax code, as well as means-tested programs outside of the tax code.

Policy takeaways

Research broadly supports a permanent expansion of the Child Tax Credit. There seems to be a consensus that such a policy would improve welfare, with the remaining debate concerning whether expansion of other social programs would be even more efficient. The trial expansion of 2021 did not seem to cause parents to work less. Most simulations of a permanent expansion suggest that labor disincentives would be small, though some researchers point out that expanding other social programs, such as the Earned Income Tax Credit, would impact labor supply by even less.

Indeed, the primary argument for not expanding the Child Tax Credit is that it would allow low-income parents to work less, which would work against the program’s goal of reducing child poverty. Still, a large body of evidence on financial transfers to children makes a strong case that despite potential reductions in parents’ participation in the U.S. workforce, these policies tend to improve children’s short-term welfare, as well as socioeconomic outcomes in adulthood, thus boosting economic productivity and growth over the long term.

Unemployment Insurance

Federal policymakers expanded the Unemployment Insurance system in three key ways during the COVID-19 pandemic: They increased the level of income support, lengthened the duration of that support, and expanded eligibility for this joint federal-state program.

The level of income support was increased by weekly added supplements. All states determine the size of UI support as a function of prior wages up to some cap, and the cap varies greatly from state to state. Prior to the pandemic, maximum benefit levels ranged from $840 in Washington state to only $235 in Mississippi.27 The first of the pandemic supplements, called Federal Pandemic Unemployment Compensation, added $600 of weekly benefits for most weeks of unemployment until the end of July 2020. As a result of this step, for the first few months of the pandemic, about 76 percent of claimants qualified for UI benefits that exceeded their prior wages, with a median replacement rate of 134 percent.28

Subsequent rounds of added benefits were lower, at $300, but were also similarly determined as a flat rate, per claim week, rather than as a share of prior income or base benefits. While the flat-rate benefits were administratively easier to implement, they also had a substantial equalizing impact not only across people of different income levels, but also across states with drastically different base levels of UI income support.

Benefit durations were increased through a series of extensions referred to as Pandemic Extended Unemployment Compensation. In most states, UI claims pay out for no more than 26 weeks. But substantial variation across states exists. Prior to the pandemic, maximum durations ranged from 30 weeks in Massachusetts to just 12 weeks in North Carolina and Florida. Pandemic Extended Unemployment Compensation added 53 additional weeks for claimants in all states, effectively covering most claimants for the entire timeframe from the onset of the pandemic until the federal expiration of the expanded program at the start of September 2021. Several state governments, however, ended the program as early as June 2021, citing concerns about slowdowns in workers’ return to the labor force.

UI eligibility also was expanded through Pandemic Unemployment Assistance, which was in effect at the same time as Pandemic Extended Unemployment Compensation. The PUA program covered workers who did not have the wage history to ordinarily be covered by Unemployment Insurance. This includes self-employed and “gig” workers and young or new workers with limited wage histories. The program also covered workers who were essentially misclassified by their employers as being self-employed so that the employer can avoid paying payroll taxes on their wages, including those taxes that explicitly fund states’ UI systems.

While the federal government expanded UI income support level, duration, and eligibility, important changes also occurred at the state level. Most states suspended, in whole or in part, the job-search requirement, which demands applicants to be actively looking for a job in order to be eligible for UI benefits, during the first year of the pandemic. States also commonly waived their statutory waiting periods, though delays due to UI claims backlogs were exceedingly common.

In addition to the federally legislated Pandemic Extended Unemployment Compensation, a preexisting program called Extended Benefits was in place to automatically “trigger on” in each state, providing up to 20 additional weeks of benefits when economic conditions warranted. During 2020, Extended Benefits triggered on in every state except South Dakota.29

What worked

Most evaluations to date focus on the effects of the increases in UI income support and the extended duration of the support, with relatively little known yet about effects of the Pandemic Unemployment Assistance program. The bulk of research so far suggests that the distortions caused to the U.S. labor market by these expansions were relatively small and probably smaller than might have been extrapolated from evaluations of prior policy changes. Existing research highlights the benefits to workers of increased UI income support, and newer research is investigating the role of similar programs in reducing virus transmission during the pandemic.

Existing research finds the added UI benefits had small effects on U.S. labor supply but substantial benefits for stabilizing consumption. Leveraging data from anonymized bank records, the University of Chicago’s Ganong and his co-authors conclude that the increased benefits raised spending by 2 percent to 2.6 percent while decreasing employment by only 0.2 percent to 0.4 percent.30

In relation to the existing academic literature on the subject, the authors estimated an elasticity of unemployment duration with respect to benefit levels of 0.02, which is substantially lower than all pre-pandemic estimates of 18 studies reviewed in 2016 by economists Johannes F. Schmieder at Boston University and Till von Wachter at the University of California, Los Angeles, which are centered around 0.35. (An elasticity of 0.35 means that increasing benefit levels by 10 percent causes workers to stay unemployed 3.5 percent longer). Ganong and his co-authors estimate that claimants consumed between 29 percent and 43 percent of their benefits.

Analyzing data from an online job platform near the start of the pandemic, economists Ioana Marinescu at the University of Pennsylvania, Daphne Skandalis at the University of Denmark, and Daniel Zhao at Glassdoor Inc. find that the UI supplements had a small negative impact on job applications.31 But they conclude that the pandemic-induced fall in job vacancies was so drastic as to justify the decreased job applications (and thus decreased “congestion” among applicants) as welfare-improving.

Earlier analyses by other researchers compared employment rates across states and did not detect any impacts of the $600 Federal Pandemic Unemployment Compensation program on U.S. labor market conditions. Studies in this vein include University of Massachusetts Amherst economist Arindrajit Dube’s 2020 analysis of U.S. Census Bureau’s Household Pulse data, as well as a 2021 analysis of payroll data from Pioneer Works Inc.’s small business work schedule management unit Homebase by Yale University economists Lucas Finamor and Dale Scott.32

The impact of extended UI income support on the U.S. labor supply was also at most modest. The early turn-off of most of the federal UI expansion programs in 22 states yielded a natural point of comparison from which economists have measured the impacts of the benefits on states’ labor markets. In general, the early terminations pertained to all UI expansions, so it is difficult to separately parse the impacts of each program from this design. Analysis of data from financial services company Earnin, however, finds that ending the expanded benefits increased employment by 4.4 percentage points but decreased the share of unemployed workers who received benefits by 35 percentage points and substantially reduced consumption—by 52 cents per dollar of benefits lost.33

Analyzing survey data from the U.S. Census Bureau’s Current Population Survey, economists Harry Holzer at Georgetown University, R. Glenn Hubbard at Columbia University, and Michael Strain at the American Enterprise Institute detected small effects of the early termination of the benefit expansions on the rate at which unemployed workers became employed.34 To benchmark the magnitude of the distortion, they estimated that if all states had withdrawn from expanded benefits in June 2021, this might have induced only 3 out of every 1,000 jobless workers back to work.

Implementation challenges and demographic disparities

Policymakers faced two sets of challenges in implementing the array of existing and expanded UI programs in the first 2 years of the COVID-19 pandemic. One set was composed of the backlogs of claims in the UI systems, fraud, and overall outdated systems. And the other set was demographic disparities, old and new. Let’s consider each in turn.

A host of barriers to implementation occurred at the state level when federal policymakers took swift action to expand Unemployment Insurance. Many problems can be viewed as exacerbations of preexisting issues during a period of stress, while others were more novel to the pandemic.

Unprecedented backlogs of claims characterized Unemployment Insurance during the early months of the pandemic because reliance on the system itself was unprecedented. Reports across the country indicated that slow payments and jammed phone lines caused hardship for many jobless workers for several months past the onset of the pandemic.

In California, where some of the most granular UI claims data are available to researchers, initial claims during the final week of March 2020 were 10 times higher than even during the worst week of the Great Recession of 2007–2009. Yet analysis of later claims payments data indicates that the vast majority of workers who were unemployed during the first several months of the pandemic did eventually receive compensation for those weeks.35

UI fraud also was substantial during the pandemic. Facing inadequate resources to rein in the backlog, states were forced into a balancing act between screening for fraud and distributing funds to workers in crisis. Some of the countermeasures that states deployed to combat fraud probably also introduced barriers to access for more-vulnerable workers, such as identity verification systems centered around smartphones.

There is no consensus on the amount of UI fraud that occurred. In June 2021, the CEO of the identity verification company ID.me was quoted as estimating that UI fraud could have been as high as $400 billion.36 A recent report by the U.S. Department of Labor finds a rate of improper payments of 18.71 percent, which would put the dollar value of improper payments at $163 billion.37 But those estimates do not yet include the Pandemic Unemployment Assistance program, which was likely more susceptible to fraud.38

The strain of the pandemic likewise exposed other problems in the UI system that were largely dormant. The Extended Benefits system is designed to be an automatic stabilizer that kicks in when either the unemployment rate or UI claims levels are sufficiently high. But a counterintuitive modification introduced during the Reagan administration for the first time kicked in en masse to terminate the extension program in most states within the first year of the pandemic—in many cases as UI claims were still surging upward.39

Simulations by economists Gabriel Chodorow-Reich at Harvard University, the University of Chicago’s Ganong, and Jonathan Gruber at the Massachusetts Institute of Technology have also highlighted the value of reforming the federal Extended Benefits program to provide more sensible automatic stabilization.40

Another set of longstanding problems with the UI system exacerbated during the pandemic concern the equity of access. The pandemic magnified preexisting disparities in accessing Unemployment Insurance, while also introducing new challenges. Many of these disparities were compounded by the toll that the pandemic took on more-vulnerable populations, including workers of color in the service sector and working mothers impacted by school closures.

Many longstanding racially disparate aspects of the UI system were amplified by the strain of the pandemic. Economists Christopher J. O’Leary and Stephen A. Wadner at the Upjohn Institute and William Spriggs at Howard University and the AFL-CIO note that for the 20 years prior to the pandemic, the rate at which Black workers received Unemployment Insurance has been lower than all other racial or ethnic groups.41 Economists Eliza Forsythe and Hesong Yang at the University of Illinois, Urbana-Champaign use survey data before and during the pandemic to confirm that disparities in access along demographic lines were largely perpetuated, with only a modest reduction from CARES Act policies.42

A key driver of national disparities is differences in state-level policies, which tend to be more restrictive and less generous in Southern states. Recent research using administrative data from U.S. Department of Labor confirms that during the pandemic, differences in state-level policies continue to account for much of these systematic disparities.43

Using claim-level records from California, these studies also find evidence suggesting that more nuanced obstacles, such as the digital divide and language barriers, play a part in limiting access.44 Qualitative evidence also highlights some of these more subtle barriers to accessing Unemployment Insurance that arise, including stigma and the digital divide, as well as workplace context.45

Due to the chaotic implementation of UI expansions across states with limited federal oversight, little is known about how these programs contributed to or mitigated racial disparities at a national level. Newly released data show that in California, the average weekly benefit paid to Black claimants was almost $50 less than what White claimants received, which is an indicator that the fixed-level added benefits played more of an equalizing role than additional benefits tied to prior earnings would have.46 Evidence suggests the extensions also likely helped mitigate racial disparities in UI durations. Still, in California, 29 percent of Black claimants exhausted all UI benefits available to them, compared to only 23 percent of White claimants.47

While many racial disparities in Unemployment Insurance grew out of longstanding concerns, the pandemic brought about a unique shift in labor market disparities by gender. Relative to prior economic downturns, social distancing measures caused a disproportionate collapse in sectors with high shares of women, and school closures massively increased the child care needs and responsibilities of working mothers.48 Literature summarized by Harvard University economist Stefanie Stantcheva also finds that women had larger negative income shocks from the pandemic than men.49

Recent research also shows that in California, 34.6 percent of the state’s female labor force filed a claim for Unemployment Insurance during the pandemic, compared to 28.3 percent of male workers, which underscores the pandemic’s disproportionate impact on women in the U.S. labor force.50 The U.S. Department of Labor does not release national gender breakdowns of claimants for the Pandemic Extended Unemployment Compensation or the Pandemic Unemployment Assistance programs. But recently published data indicates that in California, the average weekly benefit amount of women was approximately $50 less than that of men.51 The extensions also benefited more women than men in California: 52 percent of extension claimants were women and 48 percent were men.52

Open research questions

While substantial evidence exists regarding the effects of the Federal Pandemic Unemployment Compensation weekly benefit top-up and Pandemic Extended Unemployment Compensation extensions, there is a dearth of research on the Pandemic Unemployment Assistance program. One sphere of questions surrounds take-up: How well did the PUA program—designed to bring a broader group of workers into eligibility—insure otherwise-vulnerable workers? Another core set of questions surrounds the effects of the program, both in terms of labor supply and job outcomes.

The role of all three UI expansions in promoting racial equity is still not well understood at a national level. Many questions remain about how claimants’ access, experience, and outcomes varied by demographic groups. Increased data availability from the U.S. Department of Labor and states’ UI offices about claimants in these programs disaggregated by demographics would foster research in this area.

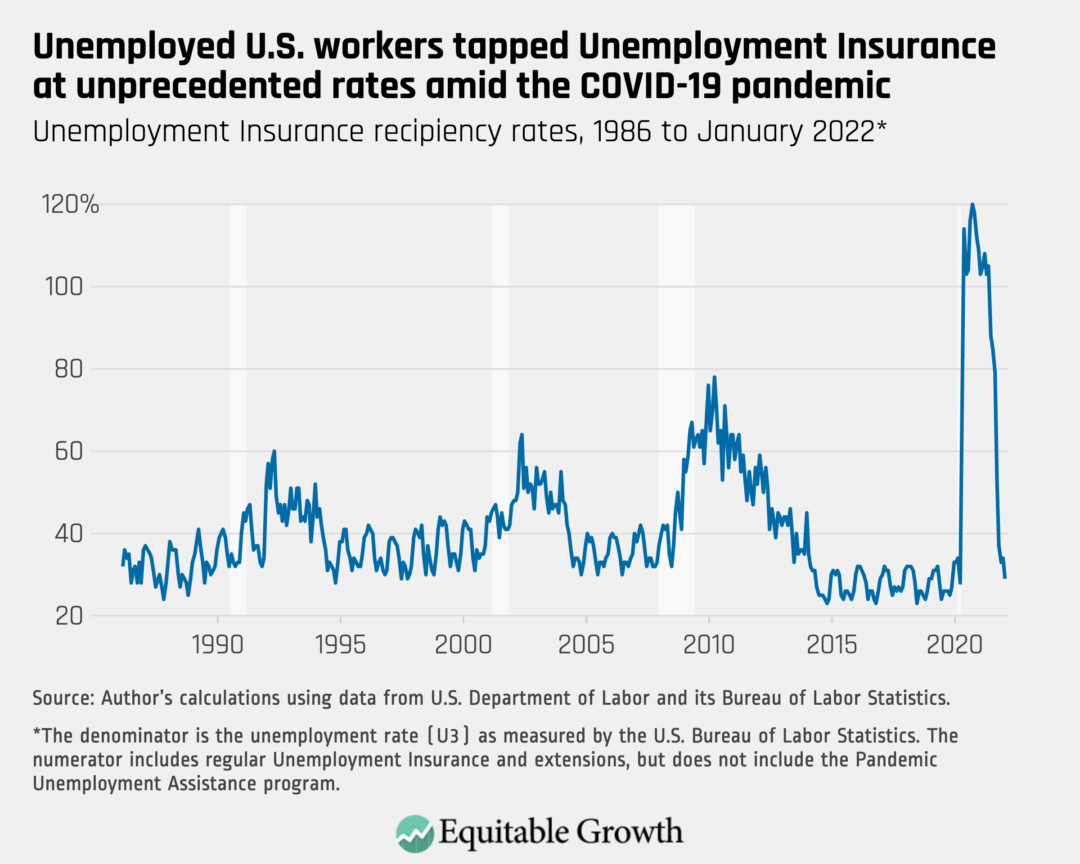

Several other novel aspects of Unemployment Insurance during the pandemic merit more research. By standard metrics, the rate at which jobless workers claimed their UI benefits during the pandemic was twice as high as that of the Great Recession and higher still than at any point in at least two decades. State-level suspensions of job-search requirements were substantial policy shifts that merit research—in particular, their impacts among women with child care responsibilities.

New questions have also emerged about the overall benefits of Unemployment Insurance, including the public health consequences of these income supports during the pandemic. The exact mechanisms driving the surge in UI claims over time amid the pandemic are still not well understood, but they were substantial. (See Figure 4.)

Figure 4

The unusually low labor supply elasticity estimates that have so far emerged from the pandemic have also revived longer-standing questions about the role of Unemployment Insurance during recessions. Building on a wave of research following the Great Recession, the empirical literature has been divided on whether it is more or less distortionary to labor supply during periods of downturns. If labor supply responses indeed were smaller during the pandemic, then researchers will need to explain whether this was a function of labor market tightness, liquidity infusions from other stimulus programs, the perceived temporary nature of the added benefits, or some other driver. Although it is reasonable to suspect that workers’ job searches might respond differently to an added benefit of $600 for several weeks versus permanently, the literature contains little empirical or conceptual precedent from which to draw.

Policy takeaways

The expansion of UI income support via the Federal Pandemic Unemployment Compensation program and the expanded UI duration via the Pandemic Extended Unemployment Compensation program alleviated the hardships faced by suddenly unemployed workers and their families amid the COVID-19 pandemic, with notably small impacts on the rate at which UI claimants returned to work. Current estimates of the work disincentives of these policies near the start of the pandemic are substantially lower than would have been predicted from extrapolations based on prior studies of more marginal changes.

Some economists believe this is because jobs were already so scarce relative to available workers for much of the pandemic that there were few employment opportunities from which Unemployment Insurance could deter workers. Liquidity infusions to U.S. households from other government spending programs also may have dampened both labor supply effects and unemployed claimants’ propensities to consume the benefits. Still, existing estimates of the effect of both the added income support levels and the extended duration of the UI program suggest they each had relatively large benefits to stimulating consumption. Less is known about the effectiveness of the Pandemic Unemployment Assistance program, largely for want of data.

Aside from the three novel expansions to Unemployment Insurance, the pandemic also brought to light three other longstanding problems with the UI system that merit policy action. First, federal action is needed to harmonize and modernize states’ UI systems. An outdated patchwork of systems across the states led not only to backlogs but also to disparate impacts for racially marginalized groups.

Second, the current federal system of automatic UI stabilizers is in need of an overhaul. The current Extended Benefits program is not just woefully inadequate, but also proved itself to be counterproductive in dozens of cases by automatically terminating federal funds to states when they most needed it.

Finally, the U.S. Department of Labor should modernize the way that it reports UI statistics. While unprecedented claims backlogs contributed to inaccurate reporting of UI claims counts near the start of the pandemic, lack of transparency surrounding the racial and ethnic data that claimants report to states continues to limit the extent to which policymakers can learn about the racially disparate impacts of pandemic-related UI expansions.

Conclusion

This report focuses on three distinct pandemic spending programs, but important interactions occurred across these programs. Many U.S. households that received funds through one program also benefited from others. For instance, the final round of economic impact payments was disbursed in March 2021, which also when federal extensions of Unemployment Insurance were still in place and shortly after monthly advance payments of the Child Tax Credit began to go out. It is likely that many households that received funds from multiple programs spent less of their payments from each one than they would have in the absence of the others, but research has not yet tested this hypothesis.

Several key findings of the growing literature on pandemic income support programs bear significance for policymakers as they consider how to prepare for future recessions. Despite all the media attention that fraud in UI systems has received, policymakers should note that research to date has found the UI expansion programs were roughly as effective of a fiscal stimulus as the untargeted economic impact payments. Future rounds of stimulus payments should consider whether liquidity-constrained individuals can be better targeted.

Of course, future UI expansion programs should focus on limiting fraud through investments in information technology and data sharing across government agencies, while remaining vigilant to avoid introducing new access barriers for claimants that could widen the disparate impacts of accessing these critical income supports. If experiences during the pandemic can be extrapolated to subsequent downturns, concerns about the purported work disincentives of Unemployment Insurance may not be first-order.

The temporary expansion of the Child Tax Credit also demonstrated the power of tax policy to restore equity in the U.S. economy. This program worked not only to bolster an economic recovery but also to lay the foundation for more broad-based and thus more sustainable economic growth, while also making investments in children that will lead to a more productive workforce in the future and more long-term equitable growth.

While this report has sought to highlight open research questions as they pertain to each program, some important questions are broader. Studies that span multiple programs to analyze their interactions are few and far between. A better understanding of these interactions would help guide policymaking. A more thorough review and synthesis of the recent literature is needed to compile and compare estimates of marginal propensities to consume from these novel programs, which will help guide stimulus policy in future recessions.

Similarly, careful attention is needed to assess how lessons learned during the COVID-19 public health crisis will generalize to other contexts. How these programs contributed to inflation is clearly another question of growing importance.

Additionally, with few exceptions, these stimulus funds were designed not to reach people living in the United States without work authorization. More research is needed to understand how this exclusion disproportionately impacted the fiscal stimulus that certain vulnerable communities received and how that channel, in turn, slowed the recovery of certain segments of the U.S. economy. Future research should investigate the extent to which fiscal stimulus can be more effective by including undocumented residents, who may have higher-than-average propensities to consume due to barriers in accessing liquidity.

One final point. Although the scope of this report focuses on only the three largest pandemic spending programs to U.S. individuals, workers, and families, a number of other important programs in this vein also came about during the pandemic. Salient among those are the expansion of the Supplemental Nutrition Assistance Program and the pause on college student loan payments. The rental eviction moratorium, although not a direct transfer to families, was another important government program aimed at families amid the pandemic. These three programs, and their interactions with the major pandemic spending programs, deserve more evaluation by researchers.

About the author

Alex Bell is a postdoctoral scholar at the California Policy Lab at the University of California, Los Angeles. Prior to joining CPL, he earned a Ph.D. in economics from Harvard University. At CPL, Bell is part of a team focused on labor and employment. His research documents unequal experiences of workers in the labor market and the implications of these inequalities for society as a whole. Bell’s research has appeared in top economics publications, including the Quarterly Journal of Economics and American Economic Review. His research has also been featured in media outlets, including The New York Times, Vox, and The Economist, as well as in the U.S. Patent and Trademark Office’s 2019 report to Congress on underrepresented groups in innovation.

Acknowledgments

Shusheng Zhong and Matthew Forbes provided outstanding research assistance for this report.

End Notes

1. Current cost estimates are from the nonpartisan Committee for a Responsible Federal Budget. See “COVID Money Tracker,” available at www.covidmoneytracker.org (last accessed October 4, 2022).

2. Most evaluations of the stimulus payments reviewed here focus on comparisons of consumption around payments issued April 15, 2020.

3. Jonathan A. Parker and others, “Household Spending Responses to the Economic Impact Payments of 2020: Evidence from the Consumer Expenditure Survey.” Working Paper 29648 (National Bureau of Economic Research, 2022).

4. These discrepancies have not yet been fully resolved but may be accounted for by differences in the populations studied, how transactions are measured, and statistical uncertainty.

5. Ezra Karger and Aastha Rajan, “Heterogeneity in the Marginal Propensity to Consume: Evidence from Covid-19 Stimulus Pay” (Federal Reserve Bank of Chicago, 2020).

6. Scott R. Baker and others, “Income, Liquidity, and the Consumption Response to the 2020 Economic Stimulus Payments.” Working Paper 27097 (National Bureau of Economic Research, 2020).

7. Natalie Bachas and others, “Initial Impacts of the Pandemic on Consumer Behavior: Evidence from Linked Income, Spending, and Savings Data.” Working Paper 27617 (National Bureau of Economic Research, 2020).

8. Raj Chetty and others, “How Did COVID-19 and Stabilization Policies Affect Spending and Employment? A New Real-Time Economic Tracker Based on Private Sector Data.” Working Paper 27431 (National Bureau of Economic Research, 2020).

9. Ibid.

10. Dan Murphy, “Economic Impact Payments Uses, Payment Methods, and Costs to Recipients” (Washington: The Brookings Institution, 2021).

11. Parker and others, “Household Spending Responses to the Economic Impact Payments of 2020: Evidence from the Consumer Expenditure Survey.”

12. Survey data analyzed by Brookings’ Murphy indicates that 3 percent of economic impact payment paper-check recipients accessed the funds through a check casher, and an additional 6 percent used retail or convenience stores. Given the average value of the stimulus checks and rough estimates of check-cashing percentage fees and caps, Murphy arrives at $66.6 million in check-cashing fees. See Murphy, “Economic Impact Payments Uses, Payment Methods, and Costs to Recipients.”

13. Although targeting lower-income families is not thought to be beneficial for achieving fiscal stimulus goals, such targeting may help achieve redistributional or equity goals.

14. Zachary Parolin and others, “The Initial Effects of the Expanded Child Tax Credit on Material Hardship.” Working Paper 29285 (National Bureau of Economic Research, 2021); Zachary Parolin and others, “Monthly Poverty Rates among Children after the Expansion of the Child Tax Credit” (New York: Columbia University Center on Poverty and Social Policy, 2021).

15. Elizabeth Ananat and others, “Effects of the Expanded Child Tax Credit on Employment Outcomes: Evidence from Real-World Data from April to December 2021.” Working Paper 29823 (National Bureau of Economic Research, 2022).

16. Jacob Goldin, Elaine Maag, and Katherine Michelmore, “Estimating the Net Fiscal Cost of a Child Tax Credit Expansion.” Working Paper 29342 (National Bureau of Economic Research, 2021).

17. Irwin Garfinkel and others, “The Benefits and Costs of a U.S. Child Allowance.” Working Paper 29854 (National Bureau of Economic Research, 2022).

18. Kevin Corinth and others, “The Anti-Poverty, Targeting, and Labor Supply Effects of Replacing a Child Tax Credit with a Child Allowance.” Working Paper 29366 (National Bureau of Economic Research, 2021).

19. National Academies of Sciences, Engineering, and Medicine, “A Roadmap to Reducing Child Poverty” (Washington: The National Academies Press, 2019).

20. Anna Aizer, Hilary Hoynes, and Adriana Lleras-Muney, “Children and the US Social Safety Net: Balancing Disincentives for Adults and Benefits for Children,” Journal of Economic Perspectives 36 (2) (2022): 149–74.

21. Bachas and others, “Initial Impacts of the Pandemic on Consumer Behavior: Evidence from Linked Income, Spending, and Savings Data”; Baker and others, “Income, Liquidity, and the Consumption Response to the 2020 Economic Stimulus Payments”; Chetty and others, “How Did COVID-19 and Stabilization Policies Affect Spending and Employment? A New Real-Time Economic Tracker Based on Private Sector Data.”

22. Jacob Golden and Katherine Michelmore, “Who Benefits From the Child Tax Credit?” Working Paper 27940 (National Bureau of Economic Research, 2020).

23. Ibid.

24. Natasha Pilkauskas and Katherine Michelmore, “Families with Low Incomes and the Child Tax Credit: Who is Still Missing Out?” (Ann Arbor: University of Michigan Poverty Solutions, 2021).

25. Ibid.

26. Leah Hamilton and others, “Employment, Financial and Well-Being Effects of the 2021 Expanded Child Tax Credit: Wave 1 Executive Summary” (St. Louis, MO: Social Policy Institute, 2021).

27. Alex Bell and others, “Disparities in Access to Unemployment Insurance During the COVID-19 Pandemic: Lessons from U.S. and California Claims Data” (Los Angeles: California Policy Lab, 2022).

28. Peter Ganong, Pascal Noel, and Joseph Vavra, “US Unemployment Insurance Replacement Rates during the Pandemic,” Journal of Public Economics 191 (2020).

29. Alex Bell and others, “Why Extended UI Benefits Were Turned Off Prematurely for Workers in 33 States” (Los Angeles: California Policy Lab, 2021).

30. Peter Ganong and others, “Spending and Job Search Impacts of Expanded Unemployment Benefits: Evidence from Administrative Micro Data.” Working Paper 2021-19 (Becker Friedman Institute, 2021).

31. Ioana Marinescu, Daphné Skandalis, and Daniel Zhao, “The Impact of the Federal Pandemic Unemployment Compensation on Job Search and Vacancy Creation,” Journal of Public Economics 200 (2021).

32. Arindrajit Dube, “The Impact of the Federal Pandemic Unemployment Compensation on Employment: Evidence from the Household Pulse Survey (Preliminary).” Working Paper (2020), available at https://www.dropbox.com/s/q0kcoix35jxt1u4/UI_Employment_HPS.pdf?dl=0; Lucas Finamor and Dana Scott, “Labor Market Trends and Unemployment Insurance Generosity during the Pandemic,” Economics Letters 199 (2021).

33. Kyle Coombs and others, “Early Withdrawal of Pandemic Unemployment Insurance: Effects on Employment and Earnings,” AEA Papers and Proceedings 112 (2022): 85–90.

34. Harry J. Holzer, R. Glenn Hubbard, and Michael R. Strain, “Did Pandemic Unemployment Benefits Reduce Employment? Evidence from Early State-Level Expirations in June 2021.” Working Paper 29575 (National Bureau of Economic Research, 2021).

35. This conclusion is based on recipiency rates constructed from California claims data. See Alex Bell and others, “Increasing Equity and Improving Measurement in the U.S. Unemployment System: 10 Key Insights from the COVID-19 Pandemic” (Los Angeles: California Policy Lab, 2022). Due to the backlog and inaccurate reporting of data by the U.S. Department of Labor, surprisingly little is known about the rate at which unemployed workers in other states managed to collect benefits during the first several months of the pandemic.

36. The company later clarified that the $400 billion figure included state spending on Unemployment Insurance during the pandemic outside of the federal expansion programs, which they estimated brought total UI spending during the pandemic to $1 trillion. See Blake Hall, “Calculating the Road to Losing $400 Billion Dollars,” ID.Me Insights blog, January 20, 2022, available at https://insights.id.me/article/calculating-the-road-to-losing-400-billion-dollars/.

37. “OIG Oversight of the Unemployment Insurance Program,” available at https://www.oig.dol.gov/doloiguioversightwork.htm (last accessed October 4, 2022). The U.S. Department of Labor states that its estimate of fraud applies to $872.5 billion in UI payments authorized under the Coronavirus Aid, Relief, and Economic Security, or CARES, Act.

38. The susceptibility of Pandemic Unemployment Assistance to fraud may partly be a fault of a lack of information sharing across government agencies: While states’ UI offices receive quarterly wage data against which they can verify workers’ reported prior wage earnings, the UI offices typically do not have access to information that state or federal tax authorities collect about self-employment earnings records.

39. Extended Benefits “trigger on” in a state when a large enough share of workers claims UI benefits. However, extension claimants are excluded from this calculation. As long-term unemployment surged, more workers had exhausted state benefits and were covered by UI extensions. As a result, this counterintuitively caused the Extended Benefits program to terminate. See Bell and others, “Why Extended UI Benefits Were Turned Off Prematurely for Workers in 33 States.”

40. Gabriel Chodorow-Reich, Peter Ganong, and Jonathan Gruber, “Should We Have Automatic Triggers for Unemployment Benefit Duration And How Costly Would They Be?” Working Paper 2022-12 (Becker Friedman Institute, 2022).

41. Christopher J. O’Leary, William E. Spriggs, and Stephen A. Wandner, “Equity in Unemployment Insurance Benefit Access,” AEA Papers and Proceedings 112 (2022): 91–96.

42. Eliza Forsythe and Hesong Yang, “Understanding Disparities in Unemployment Insurance Recipiency” (Champaign, IL: University of Illinois, Urbana-Champaign, 2021).

43. Kathryn A. Edwards, “The Racial Disparity in Unemployment Benefits,” The RAND Blog, July 15, 2020, available at https://www.rand.org/blog/2020/07/the-racial-disparity-in-unemployment-benefits.html; O’Leary, Spriggs, and Wandner, “Equity in Unemployment Insurance Benefit Access”; Bell and others, “Increasing Equity and Improving Measurement in the U.S. Unemployment System: 10 Key Insights from the COVID-19 Pandemic.”

44. Ibid. They find particularly low levels of benefits receipt in Hispanic communities, though the extent to which this is due to ineligibility is unclear. To collect UI benefits, a person must have work authorization; thus, UI benefits are not open to undocumented workers, and the pandemic expansions to eligibility did not change this.

45. Monee Fields-White and others, “Unpacking Inequities in Unemployment Insurance” (Washington: New America, 2020); Alix Gould-Werth, “Workplace Experiences and Unemployment Insurance Claims: How Personal Relationships and the Structure of Work Shape Access to Public Benefits,” Social Service Review 90 (2) (2016): 305–52.

46. Bell and others, “Increasing Equity and Improving Measurement in the U.S. Unemployment System: 10 Key Insights from the COVID-19 Pandemic.”

47. Ibid.

48. Titan Alon and others, “The Impact of COVID-19 on Gender Equality” (Cambridge, MA: National Bureau of Economic Research, 2020).

49. Stefanie Stantcheva, “Inequalities in the Times of a Pandemic,” Economic Policy 37 (109) (2022): 5–41.

50. Bell and others, “Increasing Equity and Improving Measurement in the U.S. Unemployment System: 10 Key Insights from the COVID-19 Pandemic.”

51. Ibid.

52. Ibid.

Related

Explore the Equitable Growth network of experts around the country and get answers to today's most pressing questions!