Fast facts

- At the onset of the COVID-19 pandemic and resulting recession in 2020, maintaining inflation at the Federal Reserve Board’s 2 percent target rate took a backseat to ensuring the U.S. economy—and, by extension, the global economy—did not fall into a prolonged recession.

- Fed Chair Jerome Powell and his colleagues are now hiking the key federal funds interest rate that the Fed controls at a steady clip—and signalling they will continue to do so until inflation subsides. That is easier said than done.

- There are a number of heterogeneous factors at play around the world and in the United States affecting inflationary pressures, many of which the Federal Reserve has no control over, among them globally set oil and gas prices, the economic ramifications of Russian dictator Vladmir Putin’s invasion of Ukraine for those prices and for the cost of key agricultural commodities, and continuing global supply chain snarls.

- Once future inflationary expectations take hold in an economy, reversing them is hard to do. U.S. households react very differently to inflationary expectations by income. The income earners in these households react differently when seeking higher wages due to inflation. And U.S. businesses react differently to these wage pressures and to industry-specific inflationary pressures for the inputs they need to make the products they sell and the profit margins they seek to maintain.

- Inflationary expectations of U.S. households are, by and large, set by their consumption patterns based on their incomes—a key determinant that the Federal Reserve’s anti-inflationary toolkit is not specifically designed to tackle. And the Fed’s blunt interest rate hikes cannot account for the heterogeneous factors that go into the inflationary expectations of U.S. workers and businesses across many industries. To address these monetary policy shortfalls requires:

- Better communication by the Fed about its understanding of future inflationary expectations and what it intends to do about it

- Targeted income support for lower-income U.S. households to ameliorate inflationary pressures

- Investment incentives to U.S. businesses to build more manufacturing capacity in the United States to help resolve continuing global supply chain problems

- Improvements to the country’s social infrastructure that allow currently at-home caregivers to return to the workforce and increase the labor supply

- Above all, though, this report finds that the Fed needs to better understand the heterogeneous factors contributing to future inflationary expectations today due to the still-reverberating consequences of the COVID-19 pandemic.

Overview

The chair of the Federal Reserve, Jerome Powell, and other members of the U.S. central bank’s Federal Open Market Committee, which sets monetary policies, are keenly aware of the importance of inflationary expectations among U.S. households and businesses. That’s why they try to signal the Fed’s determination to keep inflation under control. At the onset of the COVID-19 pandemic and resulting recession in 2020, however, maintaining inflation at the Fed’s 2 percent target rate took a backseat to ensuring the U.S. economy—and, by extension, the global economy—did not fall into a prolonged recession.

Fast forward to 2022. Powell and his colleagues are now hiking the key federal funds interest rate that the Fed controls at a steady clip—and signalling they will continue to do so until inflation subsides. That is easier said than done.

This report examines why inflationary expectations amid the continuing COVID-19 pandemic could be hard to suppress. There are a number of heterogeneous factors at play around the world and in the United States affecting inflationary pressures, many of which the Federal Reserve has no control over. Think globally set oil and gas prices, the economic ramifications of Russian dictator Vladmir Putin’s invasion of Ukraine for those prices and for the cost of key agricultural commodities, and global supply chain snarls for key products due to the pandemic just as demand for those products spiked sharply over the past 2 years.

But once future inflationary expectations take hold in an economy, reversing them is hard to do. U.S. households react very differently to inflationary expectations by income. The income earners in these households react differently when seeking higher wages due to inflation. And U.S. businesses react differently to these wage pressures and to industry-specific inflationary pressures for the inputs they need to make the products they sell and the profit margins they seek to maintain.

This report examines in detail how U.S. workers and their families understand inflationary pressures across the income distribution in the United States, as well as by the race, ethnicity, and gender of those workers and their families. The main finding is that the inflationary expectations of U.S. households are, by and large, set by their consumption patterns based on their incomes—a key determinant that the Federal Reserve’s anti-inflationary toolkit is not specifically designed to tackle.

This report also looks at how the Fed can exercise influence over U.S. businesses’ investment decisions and U.S. workers’ bargaining positions, but even in these cases, the Fed’s blunt interest rate hikes cannot account for the heterogeneous factors that go into the inflationary expectations of U.S. workers and businesses across many industries. This report looks at the reasons why this is the case.

I close the paper with a brief examination of the role of recent U.S. fiscal and monetary policies in setting future inflationary expectations amid the continuing COVID-19 pandemic and then posit some open questions that economists and other social scientists could examine to better understand the root causes of inflation in the U.S. economy and society today. My concluding policy recommendations are necessarily brief, given how much academics and policymakers alike still need to understand about the heterogeneous factors that determine inflationary expectations across U.S. income and wealth divides. But these recommendations are nonetheless doable, among them:

- Better communication by the Fed about its understanding of future inflationary expectations and what it intends to do about it

- Targeted income support for lower-income U.S. households to ameliorate inflationary pressures

- Investment incentives to U.S. businesses to build more manufacturing capacity in the United States to help resolve continuing global supply chain problems

- Improvements to the country’s social infrastructure that allow currently at-home caregivers to return to the workforce and increase the labor supply

Above all, though, this report finds that the Fed needs to better understand the heterogeneous factors contributing to future inflationary expectations today due to the still-reverberating consequences of the COVID-19 pandemic.

The impact of inflation across U.S. households by demographic composition

This section of the report breaks down how consumption dynamics play out in the real economy for U.S. households. This section first looks at key heterogeneous factors that actually determine realized inflation and future inflationary expectations amid the pandemic at the level of U.S. households. This section then examines how the financial debt and assets of these different kinds of U.S. households factor into their experiences with realized inflation and their perceptions about future inflationary expectations.

The traditional view of U.S. households’ experiences with inflation

Inflation reflects the increase in the general level of prices, typically comparing the cost of purchasing an identical bundle of consumption goods across different time periods. When inflation goes up, a dollar today purchases less than a dollar did yesterday. That’s why many U.S. workers and their families are hit hard by high inflation when their wages do not follow suit, yet the harmful consequences of inflation do not hit everyone uniformly.

In the 1980s, economists noted that aggregate consumption dynamics are best described by two types of households: low-income ones that consume 100 percent of their disposable income and those that have sufficiently high incomes so that they can save parts of it, which allows them to optimize their consumption and savings decisions over time and pull forward consumption before prices start increasing.1 In the data, the average savings rate in the United Sates increases with the incomes of U.S. households, with the highest income earners tending to have the highest savings rates.

This is why inflation makes the consumption of a bundle of goods and services more expensive for lower-income U.S. workers and their families because they are hit by inflation on 100 percent of their disposable income. In contrast, higher-income U.S. households do not feel the higher prices for consumption goods for 100 percent of their income. Similarly, most African Americans workers and their families tend to have lower savings rates because they are concentrated in lower-income groups as a result of a long history of systematic exclusion from wealth-building opportunities and hence are hit harder by inflation.

So far, we discussed how the average increase in the price level of a representative consumption bundle hits individuals differently. But, of course, not all Americans purchase identical goods all the time, and the flexibility to change consumption patterns is a well-documented way that households evade the impacts of inflation. In the data, lower-income Americans tend to spend most of their income on necessities, such as groceries, gas, and rent, whereas the share of discretionary consumption increases as individuals’ incomes rise. This pattern was exacerbated by the onset of the COVID-19 pandemic and the resulting recession—a pattern that continues to some degree amid the continuing pandemic.

The COVID-19 pandemic dramatically altered traditional U.S. household consumption patterns

Early in the COVID-19 pandemic in 2020, a large part of the increase in inflation was concentrated in goods—and especially durable goods, such as new or used cars—due to the disruption of supply chains and shortages in important intermediate inputs. Then, in 2022, a surge in energy prices and in the prices of services hit the U.S. economy, with the former hitting lower-income Americans the hardest. They spend a larger share of their budgets on gas, energy, and rent, and typically have to commute longer distances to work.

Moreover, not only do U.S. households differ in how they spend money; they also differ in where they purchase goods, whether they use coupons and discounts, and whether they purchase goods in bulk or on the spot when needed. That’s why realized inflation, as measured by the U.S. Bureau of Labor Statistics as the increase in the level of prices for a representative consumption bundle, is a rather abstract concept for many U.S. households.

Indeed, the realized inflation rate at the household level, taking into account household-specific consumption bundles and prices that households pay, might differ quite substantially from those of a representative consumer.

Consumption and its impact on inflation varies by types of households

Research finds large differences in realized inflation across U.S. households, with important roles for both differences in goods consumed and in the prices paid contributing to differences in realized inflation.2 Yet little systematic variation exists in realized inflation across the income distribution and across race in normal times.3 During the COVID-19 pandemic, though, I and my co-researchers did observe realized inflation of up to 2 percentage points higher for low-income U.S. households ,relative to high-income households, and for Black households, compared to White ones.4

What drove this large wedge in realized inflation? We find that two margins help explain this pattern. First, lower-income U.S. households and most African American households consumed goods that witnessed a larger increase in prices, compared to other goods. Second, a trading-down mechanism played a crucial role.5

Normally, higher-income U.S. households tend to purchase goods at higher-priced stores, such as Amazon.com Inc.’s high-end grocery store chain Whole Foods Market. They barely use coupons and don’t buy their groceries in bulk or when they are on sale. Hence, when a sharp contraction hits them, they can engage in a trading-down mechanism: They can switch grocers and start purchasing at lower-priced stores.

Moreover, higher-income U.S. households can start purchasing goods with coupons and in bulk to save money. Therefore, when inflation rises and reduces their disposable incomes, they can reduce the prices they pay for their consumption bundle, and realized inflation is muted.

For lower-income Americans, instead, this margin of adjustment is barely operative. Even in normal times, they are more likely to purchase at lower-priced grocers. They purchase in bulk and might drive long distances to obtain a bargain and because of food desserts. Hence, as a consequence, they witnessed substantially higher inflation during the pandemic and in other recessions and downturns. Given the spike in gas prices, the longer trips to shopping outlets by lower-income U.S. households also might no longer be feasible.

Financial debts and assets also matter for U.S. households’ realized inflation

But then, let’s consider the asset side of U.S. households’ balance sheets. Higher-income households not only save a larger share of their incomes but also are substantially more likely to save in so-called real assets, such as real estate, or financial market assets, such as stocks. Stocks are claims on real assets and similar to real estate because their value is more likely to increase in value when the price level goes up and are therefore hedges against increases in rising prices.

Of course, higher-income U.S. households are also more likely to invest in bonds, which experience negative returns in times of higher inflation and interest rates. Yet the share of savings that are invested in real assets tends to increase among higher-income households, and hence, in relative terms, higher-income households are relatively less affected on the asset side of their balance sheets.

In contrast, U.S. households earning below the median income often save (to the extent they have the means to save at all) in assets that are less protected from the impact of inflation, such as savings and deposit accounts, whose interest payments do not or only slowly increase with higher inflation. Therefore, when inflation spikes, lower-income Americans also see the value of their assets erode over time.

Finally, the debt side of U.S. households’ balance sheets is possibly the bright side of higher inflation. Fixed debt payments imply that the real value of debt payments erodes when inflation increases after debt contracts are signed.6 Simply speaking, when inflation increases, the future dollars to make interest and principal payments are worth less. Of course, this statement assumes that increases in payments or debt balances do not increase with inflation (or in advance of possible inflation). Mortgages are the most important debt position of most Americans, with 30-year fixed-rate mortgages the most prevalent type of mortgage in the United States. Other popular fixed-rate debt instruments include auto loans and student loans.

Yet interest owed on mortgages does go up when inflation rises for holders of adjustable-rate mortgages. In the distribution of mortgage holders, lower-income U.S. households and Black households are more likely to hold adjustable-rate mortgages and therefore do not benefit through lower real debt payments following higher inflation.

Other forms of consumer debt carry either variable interest rates—think credit cards or home equity loans—or higher interest rates, such as auto loans or loans for durable goods. These forms of debt generally do not protect the holders of this debt from the impact of inflation, compared to 30-year fixed-rate home mortgages. In general, holders of debt instruments whose payments do not fluctuate with inflation tend to be better off from surprise inflation.

Finally, low-income seniors are mostly protected from inflation because of Social Security cost-of-living increases. And young people, to the extent they are more likely to be paying down a fixed-interest mortgage, can actually benefit from inflation.

Understanding the different factors that contribute to inflation and future inflationary expectations across U.S. households and U.S. firms

For monetary policymakers at the Federal Reserve and central banks across the globe, more important than who is experiencing what level of inflation is what different types of households and businesses expect will happen with inflation going forward. This section will explain why that is, what different Americans are currently thinking about future price trajectories, and how the Federal Reserve might effectively keep inflation expectations “anchored” at its target annual rate of 2 percent.

One important observation to make before delving into the details, however, is that the academic literature in inflation overall finds that U.S. firms form their inflation expectations almost identically to U.S. households. I note situations where this is not necessarily the case, such as among financial market participants, but, by and large, the heterogeneous factors determining future inflationary expectations hold true for U.S. households and businesses alike.7

Why the Fed cares about the views of U.S households and U.S. firms on inflation and future inflationary expectations

Federal Reserve Chair Jerome Powell, in 2021, said that “Inflation expectations are terribly important. We spend a lot of time watching them.”8 Why would these expectations be so important? The traditional policy view is that inflationary expectations—the broad public’s sense of how quickly prices will rise over the next several years—help central banks and other institutions predict future inflation rates and hence feed into the production of economic forecasts, one of the main tasks that monetary policy institutions perform. And, indeed, the survey-based inflationary expectations of U.S. business and finance professionals and U.S. households have been shown to help the Fed forecast future inflation.

Traditionally, macroeconomic researchers also have stressed an important role for inflationary expectations among a specific group of agents—financial market participants—because such expectations have been shown to affect asset prices, such as stock prices, and interest rates. These traditional roles of inflationary expectations, however, are not the ones central bankers such as Chair Powell have been emphasizing since after the Great Recession of 2007–2009. In their view, the key reason why subjective inflationary expectations matter is that they affect the prices and wages that firms set, as well as the consumption-saving decisions of households. This view does not focus on the expectations of financial-market participants or professional forecasters—of which most firms and most households are barely ever aware—but on the subjective inflation expectations of ordinary economic agents, such as U.S. workers and their families and U.S. firms.

The president of the St. Louis Federal Reserve Bank, James Bullard, laid out this logic clearly in 2016. Explaining why inflationary expectations are important, he stated, “Firms and households take into account the expected rate of inflation when making economic decisions, such as wage contract negotiations or firms’ pricing decisions.”9 Why would U.S. households and firms take their subjective inflationary expectations into account when making fundamental economic choices? To this, I now turn.

U.S. households and firms gauge inflation and future inflationary expectations very differently

In theory, how rapidly U.S. households and firms expect prices to increase in the future should matter for how they allocate their spending over time. For instance, expectations of much higher prices in the future should induce households to purchase more goods today while prices are still relatively low—which, in economic parlance, is known as intertemporal substitution. Also, in normal, noninflationary times, prices and wages change only infrequently, but when high rates of inflation arise, they swiftly erode the value of previously sticky prices and wages—a feature firms and workers alike take into account when setting prices, as well as when bargaining over wage increases.

Subjective inflationary expectations also shape expectations of how expensive it will be to repay loans with future dollars. These expectations are crucial to firms’ investment decisions, which typically require external financing, as well as households’ choices about how to finance the purchase of large ticket items, such as houses, cars, and other durable goods. This is why higher inflationary expectations today shape current U.S. consumer spending and investment decisions by firms, and thus aggregate demand in the U.S. economy. Inflationary expectations also have a direct impact on realized inflation via the so-called New Keynesian Phillips curve, which relates realized inflation to inflationary expectations and slack in the economy.

The role of inflationary expectations for the effectiveness of U.S. monetary policy and realized inflation was recently questioned by Jeremy Rudd, an economist at the Federal Reserve Board, who claims that little evidence exists that inflationary expectations matter for realized inflation and questions whether U.S. households and U.S. firms take their inflationary expectations into account when making economic decisions.10 Yet mounting empirical evidence shows that inflationary expectations at the individual U.S. household level are important determinants of their consumption and savings choices, and hence of aggregate demand and realized inflation.11 Moreover, direct evidence using household expectations shows that the New Keynesian Philips curve is a good description of realized inflation.12

Let me expand a bit on the growing body of work studying how ordinary U.S. workers and their families form their inflationary expectations and how these expectations, in turn, shape their decisions. The conventional narrative argues that inflationary expectations are well-anchored, so that changes in the Federal Reserve’s benchmark interest rate transmits one-for-one to real interest rates via the Fisher equation, which equates nominal rates with the sum of real interest rates—rates after inflation is factored in—and expected future inflation.

In other words, well-anchored inflation expectations are those that assume the Federal Reserve is willing and able to set interest rates at the level that will achieve the Federal Reserve’s inflation target, which is currently 2 percent. Unanchored inflation expectations, in contrast, can become a self-fulfilling prophecy, since families and businesses will start making decisions under the assumption that prices—and interest rates themselves—will continue to rise.

Yet when I and my co-authors Olivier Coibion at the University of Texas at Austin and Yuriy Gorodnichenko at the University of California, Berkeley asked 25,000 individuals in a 2018 survey what they thought the average inflation rate was that the Federal Reserve tried to achieve over longer periods of time, less than 20 percent of the respondents answered a number of around 2 percent, whereas almost 40 percent reported a number larger than 10 percent.13 At the time, the actual rate of inflation was around 2 percent.

In short, not only do most ordinary U.S. households not have well-anchored inflationary expectations, but they also typically overestimate future inflation relative to realized inflation in a certain future period of time.

The gender gap in U.S. households’ inflationary expectations

What’s more, there is a clear gender gap in U.S. households’ understanding of inflation and future inflation. Using data from the New York Federal Reserve’s Survey of Consumer Expectations, I and my co-authors find that men, on average, expected an inflation rate of around 4 percent over the next 12 months during a sample period between 2011 and 2018 when realized inflation averaged below 2 percent, whereas women, on average, expected a rate of more than 6 percent.14

To dig deeper into the possible driving forces of this “gender gap” in inflationary expectations, I and my co-authors fielded our own survey on the Nielsen homescan panel, which allowed us to survey male and female U.S. heads of household at the same time.15 This within-household analysis made it feasible to keep constant many things that typically vary across survey participants, such as housing tenure, savings, and other determinants of inflationary expectations. But even within households, we find that women, on average, expect higher inflation than men.

Yet when we split households based on the distribution of grocery duties across female and male heads of household, we find that the gender gap was only present in “traditional households,” in which the male household head declared to never do any grocery shopping. In households in which the male household head instead stated that he at least occasionally went grocery shopping, the gap disappeared because the male household heads also had higher inflationary expectations. Hence, exposure to the volatile price changes during grocery shopping trips appears to manifest itself in elevated inflationary expectations of those who do the grocery shopping.

To better understand why this association appears in the data, my co-authors and I fielded another survey in which we directly asked survey participants which sources of information were most important to households when forming inflationary expectations.16 Consistent with the seminal 1972 Lucas island model—named after Nobel laureate economist Robert Emerson Lucas Jr., who argues that individuals use not all available information to form expectations, but rather information which they can easily attain—we find that households rank “own grocery shopping experiences” as by far the most relevant source of information, before “family and friends,” “TV and radio,” “newspapers,” or other sources.17

To directly establish a link between price changes observed while grocery shopping and inflationary expectations, we then levered the Nielsen homescan panel that allowed us to observe, at a weekly frequency for 50,000 households, the goods these households bought, where they bought them, which prices they paid, and whether they purchased these goods on discounts or used coupons. We then followed data published by U.S. government statistical agencies to create a so-called chained Laspeyres price index, which weights price changes by expenditure shares in a base period, but using household-specific consumption bundles and prices instead of the bundle of a representative household as usually employed to calculate a price index.

U.S. households with the highest realized inflation at the household level, on average, expected an overall Consumer Price Index inflation rate that was higher by 0.7 percentage points than U.S. households with the lowest realized inflation rate over the previous 12 months, consistent with an extrapolation from personally experienced inflation in personal shopping bundles to overall U.S. inflation expectations. We can directly rule out that all of these U.S. households might be forecasting their own actual experience with current rates of inflation and extrapolating them forward because we can observe their future realized household-level inflation rate as it comes to pass after 12 months. This means that U.S. households witnessing current higher inflation in their own consumption bundles result in higher forecasts for overall inflation 12 months later.

In that same Nielsen panel, my co-authors and I only observe around 25 percent of the overall consumption bundle for the average household. The fact that we can find a strong association between realized inflation at the U.S. household level for this subset of the bundle and overall inflationary expectations suggests that grocery prices have a strong impact for how individuals think about inflation. At the same time, this finding also suggests that not all price changes are created equally for households.18

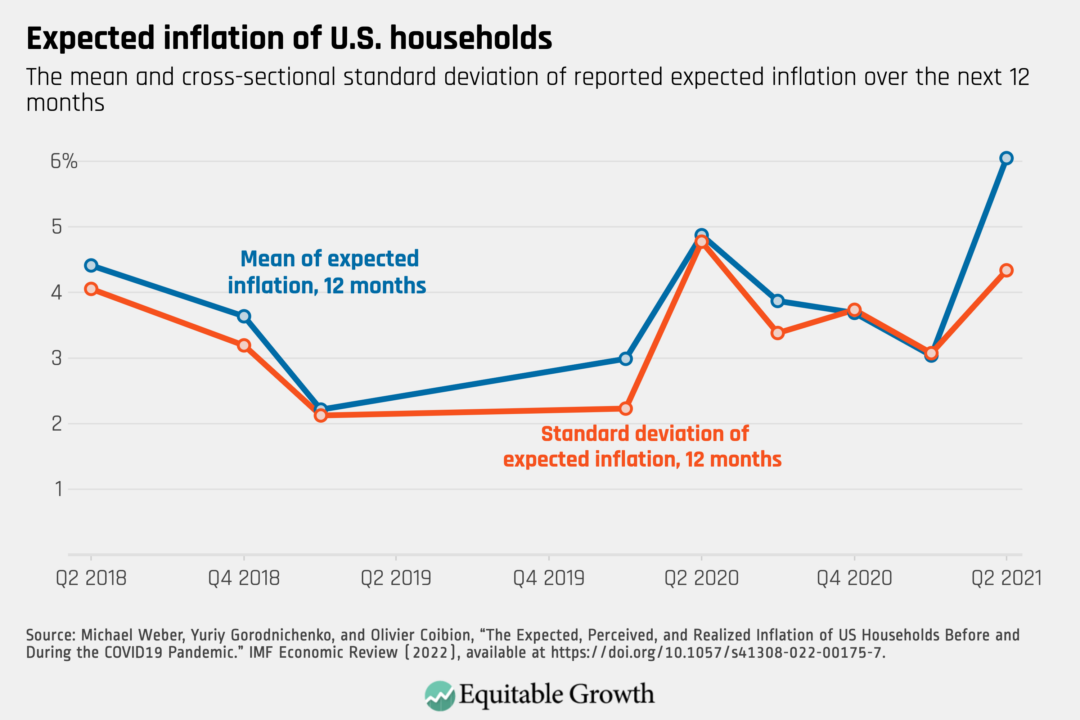

When we then weight price changes by frequency of purchases rather than the share of expenditures, we find that this “Frequency CPI” drives the association between realized inflation and inflationary expectations. In addition to putting larger weight on the price changes of frequently purchased goods, U.S. households also overweight upward price changes, relative to equal-sized downward price changes. These results can also explain why U.S. households immediately updated their inflation expectations in the summer of 2021, when the Federal Reserve and most central banks still sang the gospel of temporary inflationary pressures in narrow categories. (See Figure 1.)

Figure 1

If these initial prices spikes occur in categories that are salient to consumers, such as groceries, travel, and rental cars, then we can witness immediate increases in overall inflationary expectations. This is what happened beginning in 2021, as the COVID-19 pandemic reverberated through the U.S. labor market and workers in the United States immediately either began bargaining for higher wages or changed jobs, and sometimes even professions, in search of higher pay and less onerous pandemic-related work—which they often were able to do, given their higher bargaining power amid tight labor markets in many areas and industries.

These findings, however, also imply that even if the Fed were successful in curbing realized inflation in the near term, household inflationary expectations would still take time to come down again because ordinary consumers pay less attention to price cuts, compared to price hikes.

Because many low-income households, particularly low-income Black households, in the United States had higher realized inflation during the COVID-19 pandemic, it follows from the findings above that they would also have higher expectations for future inflation, which is, in fact, what we find.19 As previously discussed, higher inflationary expectations imply lower perceived real interest rates, which makes savings less profitable and increases current consumption and spending.

Hence, one reason why these groups save less and accumulate less wealth for retirement is due to the higher inflation rates they experience in their daily lives that then transmit into higher inflationary expectations and lower wealth in the long run, which might amplify wealth inequality. So far, no direct evidence exists showing the relative contribution of inflationary expectations to wealth inequality over the the long term, but this is definitely a new field of inquiry for academic researchers.

Possible explanations for the recent surge of inflation in the U.S. economy

Higher inflation beginning in the second half of 2021 is a global phenomenon. The global nature of the rise in inflation is prima facie evidence of global shocks being important determinants of recent inflationary pressures in the United States. One of these supply-side factors is COVID-19-induced supply chain bottlenecks, such as shutdowns of important producers of intermediate goods or backlogs in harbors around the world. Another important global determinant of inflation around the world is the spike in energy and food prices, largely due to the Russian invasion in Ukraine.

But there is evidence that inflationary factors unique to the United States are also in play. This then begs the question: What is unique about the U.S. economy that might have fueled the recent surge in inflation? In this section of the report, I look at several factors.

Fiscal policy

The deep and swift fiscal response of the federal government to the onset of the pandemic in 2020, alongside additional fiscal programs in 2021, might have played a role in driving core inflation in the United States beginning in mid-2021. Many of the COVID-19 emergency fiscal programs enacted in the United States provided a necessary lifeline to struggling Americans, but they also fueled demand amid the pandemic just as sharply reduced supplies of goods and services emerged due to the global problems mentioned earlier.

This rise in demand certainly induced price increases across many parts of the U.S. economy. At the same time, higher predicted future budget deficits tend to raise the inflationary expectations of everyday U.S. workers and their families.20 Interestingly, households barely react in their inflationary expectations to current levels of federal debt, but news about large future increases results in sharp increases in inflationary expectations of ordinary Americans.

Monetary policy

Many commentators also blamed ultra-lax monetary policies amid the pandemic as an important driver of U.S. inflation. Yet monetary policy in the United States has been very expansionary since the housing crisis that began in 2007 and the Great Recession of 2007–2009. And these same commentators had predicted hyperinflation then that did not materialize for more than a decade.

Tight labor market

Then, there is the question of wage dynamics for realized inflation. For decades, economists hypothesized that the decline of organized labor in the form of unions in the United States over the past several decades makes it unlikely that substantial wage pressures could fuel inflation, especially in more labor-intensive industries and in the service sector. Yet evidence is growing that tight labor market conditions upon the reopening of the U.S. economy after highly effective COVID-19 vaccines became more widely available are important contributors to wage pressures in the United States. The Atlanta Fed’s wage growth tracker shows that average wage growth has been more than 4 percent since September 2021 and, in August of this year, was at 6.7 percent—the highest number on record since collecting the data began in 1983.21

Contributing to tight labor market conditions is the wave of early retirements amid the pandemic, paired with a drop in the labor force participation rate, alongside the fast recovery of the U.S. economy. The resulting disappearance of slack in the U.S. labor market and low unemployment rates paired with a high number of unfilled vacancies increased some workers’ wage bargaining power with their employers.22

In this situation, many U.S. workers bargained for higher wages, either with their current employers or by finding new and better-paying jobs. The Atlanta Fed tracks these dynamics and finds that workers who conduct on-the-job searches for new employment opportunities are the key driver of higher wage pressures faced by firms.23 Yet nominal wage growth is still running below inflation—though even below-inflation-level nominal wage gains by workers increases marginal costs for their employers, who include these costs in price increases that they then pass on to the consumers of their goods and services.

The tighter U.S. labor market and the more spot-bargaining nature of the U.S. labor market in recent decades can explain why individual worker—even without the help of unions as they declined in reach and power beginning in the 1980s—were able to trigger some wage increases from their employers, who, in turn, passed on those labor costs to their consumers.

Unanchored expectations

Another big concern remains whether the currently higher inflationary expectations are becoming entrenched, possibly resulting in ever-increasing wage bargaining and wage pressures that will result in higher costs of production for firms and ultimately higher output prices—and hence, high and sustained inflation.

The reduced prices at the gas pump have helped lower inflationary expectations of households and the sequence of interest rate increases and announcements of additional hikes in the future have rippled through financial markets and increased many interest rates that most households see in their daily lifes, such as on credit cards and mortgages. Taken together, the action of the Federal Reserve and the reduced level of energy prices make inflationary-expectations-induced wage-price spirals unlikely.

Corporate concentration

An additional inflationary concern is the increase in concentration that many industries in the United States have witnessed over the past several decades. There are good theoretical reasons why higher concentration results in higher prices. A common theory of imperfect competition suggests that firms set prices as a mark-up over their marginal cost of production. This mark-up is typically higher for firms with higher market power. What’s more, many of these same firms exercise increasing monopsony power over their local labor forces, which means these firms can keep wage pressures down while also boosting prices.

This theory can only explain why industries would have one-time increases in levels of prices, but it would not be able to explain why we should observe sustained higher rates of changes in the price level—that is, higher inflation rates. Higher market power can result in a higher pass-through of input-cost increases into output prices and hence, higher price levels. But what seems to be missing today for this kind of margin-price spiral to take hold is how the higher prices feed back into higher marginal costs to keep the spiral going. Wages directly impact the marginal costs of firms. But for output prices, the economic literature on multisector modeling, in which the output of some firms enter as inputs in the production of other firms, is not conclusive.

Demographics

Another possible aspect that can shape inflationary pressures in the United States is demographic trends and an aging society. Charles Goodhart at the London School of Economics and Manoj Pradhan at the independent macroeconomic research firm Talking Heads Macro argue that the decrease in the U.S. working age population and an increase in the dependency ratio—the fraction of U.S. society that consumes and doesn’t produce, both young and old—can put upward pressure on inflation.24

Goodhart and Pradham write that a higher dependency ratio results in higher inflation, given that demand for labor outstrips the supply of workers under these conditions. While clearly an important argument, it cannot explain the recent sharp increase in inflation.

Open questions

To better understand what is causing the recent surge in inflation and how policymakers should react, I’ve identified a number of open questions for future research. Among them:

- How can monetary policy actions curb inflationary pressures and lower the risk of wage-price spirals when supply-side factors are an important driver of inflation?

- How do households adjust their decisions to move in and out of the U.S. labor market, and what are their wage expectations?

- How do the tightness of the U.S. labor market and labor market structures mediate this nexus?

- Do workers adjust their labor supply on the intensive or the extensive margin? That is, do they adjust the hours they work, or do they decide whether to work at all?

- Do firms have higher effective pricing power when consumers expect high inflation to begin with?

- Can firms’ increased pricing power result in wage-price spirals or profit-price spirals because the output of firms higher up in the production chain are the input goods of firms downstream in the production process?

Then there’s the consumer Euler equation, named after 18th century Swiss mathematician Leonhard Euler, which relates consumption growth, nominal interest rates, and inflationary expectations. The Euler equation today predicts that higher expected inflation increases current consumption compared to future consumption. But are higher inflationary expectations resulting in increases in aggregate U.S. demand, and thus increasing realized inflation, too?

U.S. society also is experiencing a growing degree of political polarization. Does the increased polarization matter for inflationary expectations and realized inflation? Recent work suggests that narratives about the macroeconomy matter a great deal.25 And political leanings shape the overall outlook for the economy.26 How has the pandemic exacerbated these trends, and how will those trends play out over the course of the pandemic and in the future, and amid any future public health crises that cascade into the U.S. economy?

Researchers and policymakers alike clearly need a better understanding of how monetary policy affects different U.S. households and firms differentially, as this report highlights, but particularly in light of the differential impact of the COVID-19 pandemic on them.

For U.S. households, a better understanding of their current labor incomes and their net nominal positions—that is, the exposure of their household balance sheets to inflation alongside the return on their assets—as monetary policy plays out to combat inflation would be good. Also important would be more research on understanding how U.S. households form their expectations about the macroeconomy jointly—that is, how do they adjust their other expectations when they adjust their inflation expectations?

Conclusion: Policy recommendations

Of course, policymakers cannot wait for the answers to all, or even some, of the questions above. They must act now, despite having only incomplete information. Given that, here is what I would recommend to monetary and fiscal policymakers.

Clearer guidance from the Fed

One aspect in which monetary policy could have been handled differently both in the United States and abroad was communication during 2021. The Federal Reserve changed its monetary policy framework at its Economic Policy Symposium that year from strict to average inflation targeting. The new policy framework suggested that after a period of low inflation, the central bank will tolerate some higher inflation, so that inflation on average hits the target.

Hence, after a decade of below-target inflation, the Federal Reserve was likely hesitant to increase its policy rates to curb inflationary pressures because doing so would have called into question its commitment to its new policy framework. Indeed, part of the Fed’s “communication” problem in 2021 was that it wasn’t clear about the time period over which it would try to hit that average inflationary target.27

Moreover, when inflation is due to short-run supply-side pressures, such as oil price shocks, central banks typically look through them under the assumption that inflationary expectations are well-anchored to core prices changes rather than volatile energy markets. Yet, as discussed above, it seems unlikely that the expectations of U.S. households are well-anchored when the price of gas jumps sharply and their utility bills increase suddenly. One could argue that expectations can deviate from the Federal Reserve’s inflation target in the short run due to temporary shocks but will not move in the same direction in the long run, given that people have high trust in the Fed today to take the necessary actions to bring inflation back to target.

So, one policy recommendation would be better monetary policy communication by the Federal Reserve amid the continuing COVID-19 pandemic. The Fed should send simple and consistent messages, not purely rely on the media as a means of communication, but explore more direct means. Also, the identity of the messenger matters: Women and Black Americans react more to identical messages sent by female and Black policymakers.28

Targeted income supports

Then, there’s the differential impact of inflation on different parts of the U.S. population, which calls for targeted programs supporting those hit hardest by the rise in inflation. A higher price at the gas pump hits many Americans hard, but attempting to lower the price of gas by subsidizing Americans’ gas expenditures not only provides a windfall to many high-income Americans who do not require a subsidy, but also sends the wrong pricing signal to consumers overall. Higher prices lower demand, which is likely a good idea in times of reduced energy supply.

So, a second policy recommendation would be for the Biden administration and the U.S. Congress to consider providing targeted support that low-income U.S. workers and their families can use to purchase goods according to their own preferences. Given that many families spend most of their budget on necessities, the expanded Child Tax Credit could be reinstituted as an appropriate policy intervention.29 It’s also worth noting that building government’s ability to make these kind of targeted fiscal transfers could help deliver a more focused and efficient countercyclical response in future recessions—and, in fact, would have been useful in 2020 and 2021.

Government investment in output capacity

Moreover, given the importance of supply-side factors, the federal government should support physical investments in domestic manufacturing capacity and local production, which higher benchmark interest rates by the Fed partially reduce by making it more costly to finance them. To overcome this problem, another policy recommendation would be for U.S. fiscal policymakers to offer investment tax credits or accelerated depreciation schedules to foster more domestic manufacturing investment and more reshoring of their overseas manufacturing operations.30

Another key supply-side factor ripe for investment is in social infrastructure. The Biden administration and Congress can tackle spiralling child care costs by enacting universal child care and pre-Kindergarten programs, alongside universal guaranteed paid leave, and other care infrastructure that allow currently at-home caregivers to return to the workforce, increase the labor supply, and reduce overall wage pressures.31

About the author

Michael Weber is an associate professor at the University of Chicago Booth School of Business. He is also a faculty research fellow at the National Bureau of Economic Research in the Monetary Economics and Asset Pricing groups, a member of the Macro Finance Society, and a research affiliate at the CESifo Research Network. His research interests include asset pricing, macroeconomics, international finance, and household finance. He has published in leading economics and finance journals, such as the American Economic Review, the Journal of Political Economy, the Review of Economic Studies, the Journal of Financial Economics, and the Review of Financial Studies. Weber earned a Ph.D. and an M.S. in finance from the Haas School of Business at the University of California, Berkeley.

End Notes

1. John Y. Campbell and N. Gregory Mankiw, “Consumption, Income and Interest Rates: Reinterpreting the Time Series Evidence.” In Olivier Jean Blanchard and Stanley Fischer, eds., NBER Macroeconomics Annual, vol. 4 (Cambridge: MIT Press, 1989).

2. Greg Kaplan and Sam Schulhofer-Wohl, “Inflation at the Household Level,” Journal of Monetary Economics 91 (2017): 19–38.

3. David Argente and Munseob Lee, “Cost of Living Inequality During the Great Recession,” Journal of the European Economic Association 19 (2) (2021): 913–952; Xavier Jaravel, “Inflation Inequality: Measurement, Causes, and Policy Implications,” Annual Review of Economics 13 (2021): 599–629.

4. Michael Weber, Yuriy Gorodnichenko, and Olivier Coibion, “The Expected, Perceived, and Realized Inflation of U.S. Households before and during the COVID19 Pandemic.” Working Paper 29640 (National Bureau of Economic Research, 2022).

5. Nir Jaimovich, Sergio Rebelo, and Arlene Wong, “Trading Down and the Business Cycle,” Journal of Monetary Economics 102 (2019): 96–121.

6. Matthis Doepke and Martin Schneider, “Inflation and the Redistribution of Nominal Wealth,” Journal of Political Economy 144 (6) (2022), available at https://www.journals.uchicago.edu/doi/abs/10.1086/508379; Adrien Auclert, “Monetary Policy and the Redistribution Channel,” American Economic Review 109 (6) (2019): 2333–67.

7. Evidence in several recent papers that I and my co-authors summarized in the Summer 2022 issue of the Journal of Economic Perspectives. See Michael Weber and others, “The Subjective Inflation Expectations of Households and Firms: Measurement, Determinants, and Implications,” Journal of Economic Perspectives 36 (3) (2022): 157–184, available at https://pubs.aeaweb.org/doi/pdfplus/10.1257/jep.36.3.157.

8. Federal Reserve Board, “Transcript of Chair Powell’s Press Conference,” September 22, 2021, available at https://www.federalreserve.gov/mediacenter/files/FOMCpresconf20210922.pdf.

9. James Bullard, “Inflation Expectations Are Important to Central Bankers, Too,” Regional Economist (2016), available at https://www.stlouisfed.org/publications/regional-economist/april-2016/inflation-expectations-are-important-to-central-bankers-too.

10. Jeremy B. Rudd, “Why Do We Think That Inflation Expectations Matter for Inflation? (And Should We?)” Finance and Economics Discussion Series 2021-062 (Board of Governors of the Federal Reserve System, 2021).

11. Weber, Gorodnichenko, and Coibion, “The Expected, Perceived, and Realized Inflation of U.S. Households before and during the COVID19 Pandemic”; Francesco D’Acunto, Daniel Hoang, and Michael Weber, “Managing Households’ Expectations with Unconventional Policies,” The Review of Financial Studies 35 (4) (2022): 1597–1642, available at https://doi.org/10.1093/rfs/hhab083; Francesco D’Acunto and others, “IQ, Expectations, and Choice,” Review of Economic Studies (forthcoming).

12. Olivier Coibion and Yuriy Gordodnochenko, “Is the Phillips Curve Alive and Well after All? Inflation Expectations and the Missing Disinflation,” American Economic Journal: Macroeconomics (2015), available at https://www.aeaweb.org/articles?id=10.1257/mac.20130306.

13. Olivier Coibion, Yurly Gorodnichenko, and Michael Weber, “Monetary Policy Expectations and Their Effects on Household Inflation Expectations,” Journal of Political Economy 130 (6) (2020), available at https://www.journals.uchicago.edu/doi/abs/10.1086/718982.

14. Francesco D’Acunto, Ulrike Malmendier, and Michael Weber, “Gender roles produce divergent economic expectations,” Proceedings of the National Academy of Sciences 118 (21) (2021): 1–10.

15. Ibid.

16. Francesco D’Acunto and others, “Exposure to Grocery Prices and Inflation Expectations,” Journal of Political Economy 129 (5) (2021): 1615–1639.

17. Robert E. Lucas Jr., “Expectations and the Neutrality of Money,” Journal of Economic Theory 4 (2) (1972): 103–124.

18. D’Acunto and others, “Exposure to Grocery Prices and Inflation Expectations.”

19. Francesco D’Acunto, Ulrike Malmendier, and Michael Weber, “What do the Data Tell us about Inflation Expectations?” Working Paper 29825 (National Bureau of Economic Research, 2022).

20. Olivier Coibion, Yuriy Gorodnichenko, and Michael Weber, “Monetary Policy Communications and their Effects on Household Inflation Expectations.” Working Paper 25482 (National Bureau of Economic Research, 2019).

21. “Wage Growth Tracker,” available at https://www.atlantafed.org/chcs/wage-growth-tracker (last accessed November 29, 2022).

22. Olivier Coibion, Yuriy Gorodnichenko, and Michael Weber, “Labor Markets During the COVID-19 Crisis: A Preliminary View.” Working Paper 27017 (National Bureau of Economic Research, 2020).

23. “Wage Growth Tracker.”

24. Charles Goodhart and Manoj Pradhan, The Great Demographic Reversal: Ageing Societies, Waning Inequality, and an Inflation Revival (Berlin: Springer Nature, 2020).

25. Peter Andre and others, “Narratives about the Macroeconomy.” Working Paper 18/21 (Social Science Research Network, 2022).

26. Olivier Coibion, Yuriy Gorodnichenko, and Michael Weber, “The Cost of the Covid-19 Crisis: Lockdowns, Macroeconomic Expectations, and Consumer Spending.” Working Paper 27141 (National Bureau of Economic Research, 2020).

27. Carola Binder, “Average inflation targeting by the Federal Reserve and U.S. consumer expectations” (Washington: Washington Center for Equitable Growth, 2021), available at https://equitablegrowth.org/average-inflation-targeting-by-the-federal-reserve-and-u-s-consumer-expectations/.

28. Olivier Coibion, Yuriy Gorodnichenko, and Michael Weber, “Monetary Policy Communications and Their Effects on Household Inflation Expectations,” Journal of Political Economy 130 (6) (2022), available at https://doi.org/10.1086/718982; Francesco D’Acunto, “Effective Policy Communication: Targets versus Instruments.” Working Paper No. 2020-148 (University of Chicago Becker Freidman Insitute for Economics, 2020), available at https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3712658; Francesco D’Acunto, Andreas Fuster, and Michael Weber, “A Diverse Fed Can Reach Underrepresented Groups.” Working Paper 21 (LawFin, 2022); Washington Center for Equitable Growth, “The value of racial and gender diversity at the Federal Reserve” (2021), available at https://equitablegrowth.org/the-value-of-racial-and-gender-diversity-at-the-federal-reserve/.

29. Alex Bell, “Early evidence on federal government income support for American individuals, workers, and families during the COVID-19 pandemic” (Washington: Washington Center for Equitable Growth, forthcoming).

30. Susan Helper, “Transforming U.S. supply chains to create good jobs” (Washington: Washington Center for Equitable Growth, 2021), available at https://equitablegrowth.org/transforming-u-s-supply-chains-to-create-good-jobs/.

31. Ibid.

Related

Explore the Equitable Growth network of experts around the country and get answers to today's most pressing questions!