Average inflation targeting by the Federal Reserve and U.S. consumer expectations

In August 2020, the Federal Open Market Committee published an amended version of its “Statement on Longer-Run Goals and Monetary Policy Strategy.” In this revised statement, the FOMC reaffirmed its 2 percent target for inflation, as first announced in January 2012, and adopted a new approach, known as average inflation targeting:

The Committee judges that longer-term inflation expectations that are well anchored at 2 percent foster price stability and moderate long-term interest rates and enhance the Committee’s ability to promote maximum employment in the face of significant economic disturbances. In order to anchor longer-term inflation expectations at this level, the Committee seeks to achieve inflation that averages 2 percent over time, and therefore judges that, following periods when inflation has been running persistently below 2 percent, appropriate monetary policy will likely aim to achieve inflation moderately above 2 percent for some time.

From this description, it is clear that the Federal Reserve adopted average inflation targeting explicitly with the goal of “anchoring” inflationary expectations. When policymakers refer to anchored expectations, they usually mean that people and financial markets are confident that future inflation will be close to target in the long run, regardless of developments in the short run. That is, when people observe a boost in inflation, they can be very sure it will be short-lived and that the Fed will keep inflation near target in the long run.

This is important. If consumers or investors believe inflation will be more permanent, then they may behave in ways that spur further inflation. Strongly anchored expectations indicate that the U.S. central bank is credible. And as the revised statement notes, the Fed believes that well-anchored expectations can help promote maximum employment.

This column provides background on the Fed’s average inflation target, details recent trends in U.S. consumers’ inflation expectations and uncertainty, and explains how the Fed could better anchor those expectations to ensure a stable U.S. economy over the course of business cycles.

Average inflation targeting at the Fed

Average inflation targeting is called a makeup strategy because it doesn’t “let bygones be bygones.” That is, monetary policymakers take past inflation into account, not only current economic conditions and outlook. A Federal Reserve Board working paper, presented to the Federal Open Market Committee as background before the adoption of this target, outlines three main benefits of makeup strategies:

First, makeup strategies naturally imply a desire to commit to a “lower for longer” path for the policy rate [the federal funds rate] in episodes when the ELB [effective lower bound, sometimes called the zero lower bound, which refers to the inability of central banks to set policy interest rates much lower than zero] significantly impairs the conduct of monetary policy and may cause extended periods of below-target inflation. Commitments to a lower-for-longer path provide more accommodative financial conditions, boosting aggregate demand and reducing deviations of inflation from its target even while the ELB binds. Second, (credible) makeup strategies foster expectations of more stable inflation, on average, thus reducing the sensitivity of inflation to transient developments. Third, the systematic materialization of stable inflation rates under makeup strategies may better anchor longer-term inflation expectations, inducing a virtuous circle.

The “lower for longer” point has received the most attention. Since inflation did run persistently below 2 percent for many years, the new average inflation targeting strategy should allow a longer period for the U.S. labor market to recover before the Fed begins to tighten monetary policy, even as inflation rises above the 2 percent target. The second and third points are again explicitly about anchoring inflation expectations. We can be sure that Fed officials will carefully monitor inflation expectations as they decide just how much “lower for longer” they are willing to go.

Fed officials are doing just that. Federal Reserve Governor Randal Quarles, for example, attributed recent above-target inflation to three factors: “the surge in demand as more services come back on line while goods spending remains robust, the emergence of bottlenecks in some supply chains, and the very low inflation readings recorded last spring dropping out of the calculation of 12-month inflation.” Quarles interpreted these factors as transitory and argued that the Fed needs to remain patient “so long as inflation expectations continue to fluctuate around levels that are consistent with our longer-run inflation goal.”

Similarly, Vice Chair Richard Clarida noted in November 2020 that “the goal of the new framework is to keep inflation expectations well anchored at 2 percent, and, for this reason, I myself plan to focus more on indicators of inflation expectations themselves—especially survey-based measures—than I will on the calculation of an average rate of inflation over any particular window of time.”

U.S. consumers’ inflation expectations and uncertainty

Fed policymakers monitor a variety of measures of inflation expectations, derived from financial markets and surveys. The Michigan Survey of Consumers, a long-running monthly survey of adults in the United States, is frequently used to gauge the expectations and sentiment of the general public (as opposed to professional forecasters or financial market participants). I developed a new method for estimating consumer uncertainty about inflation based on the forecasts in the Michigan Survey of Consumers. In particular, I show that respondents tend to provide forecasts that are round numbers—say, 5 percent, 10 percent, or 15 percent—when they are highly uncertain about their forecasts.

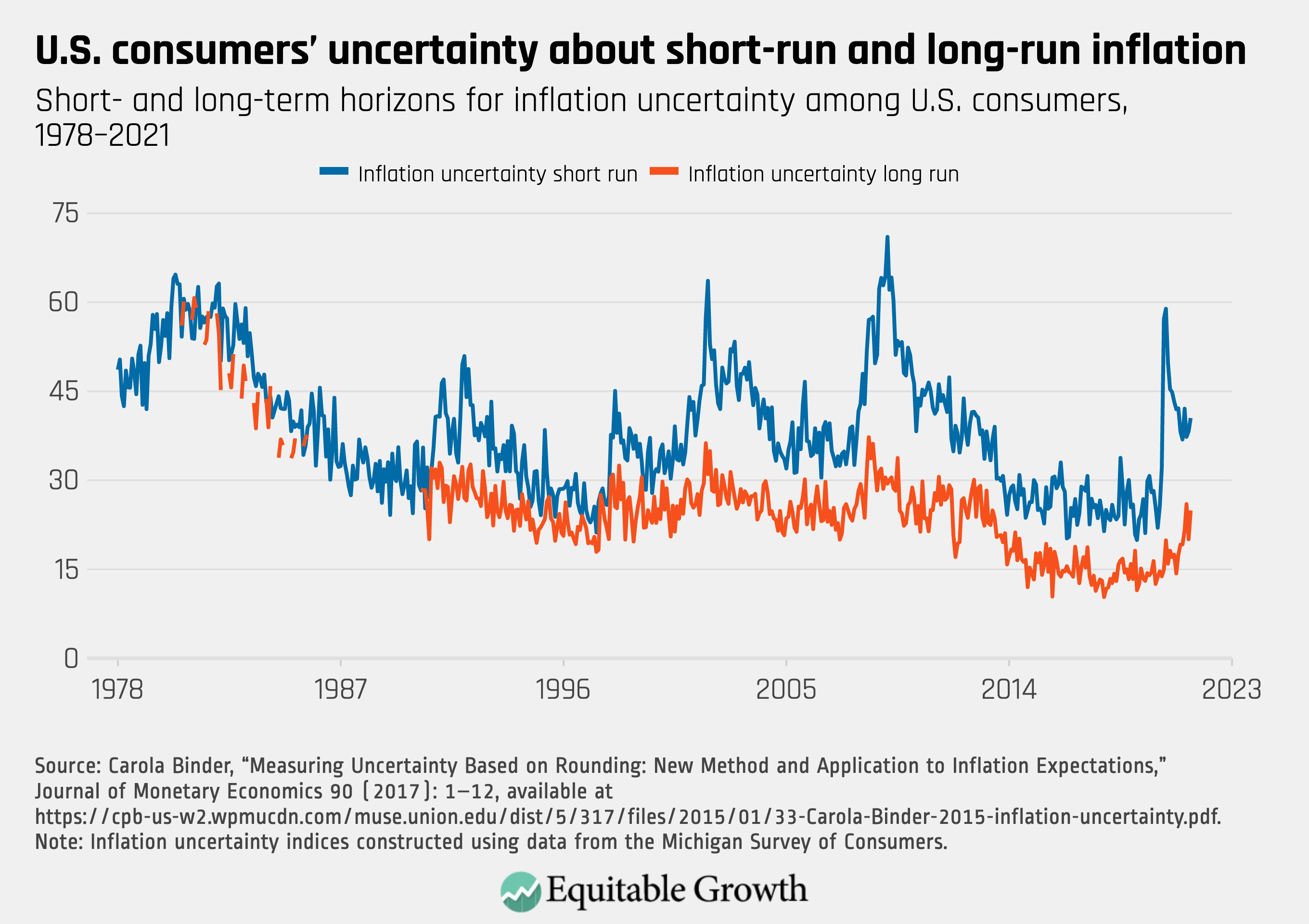

This methodology allows researchers to quantify the uncertainty associated with this rounding behavior, to create a consumer inflation uncertainty index about short-run (1 year ahead) and long-run (5–10 years ahead) inflation. The inflation uncertainty index is the estimated percent of respondents who are highly uncertain about inflation. My methodology is useful for estimating uncertainty when density forecasts are not available and has been used by an array of economists. (See Figure 1.)

Figure 1

Since the disinflation engineered by then-Fed Chair Paul Volcker in the early1980s, long-run uncertainty has typically been lower than short-run uncertainty, consistent with well-anchored expectations. Even when people are uncertain about what will happen with prices over the next year, they are more certain about what will happen in the long run. Figure 1 shows that at the start of the coronavirus pandemic, short-run uncertainty spiked from 25.7 in February 2020 to 57.2 in April 2020, peaked in May 2020, and has since been declining.

The recent behavior of long-run uncertainty is much different. Long-run uncertainty barely changed at the start of the pandemic but began to rise later, indicating that the pandemic itself is not likely the cause of the recent rise in long-run uncertainty; neither the presidential election nor President Joe Biden’s inauguration were associated with notable changes in uncertainty at either horizon. The rise in this trend is especially noteworthy because it reverses a years-long trend of declining long-run uncertainty.

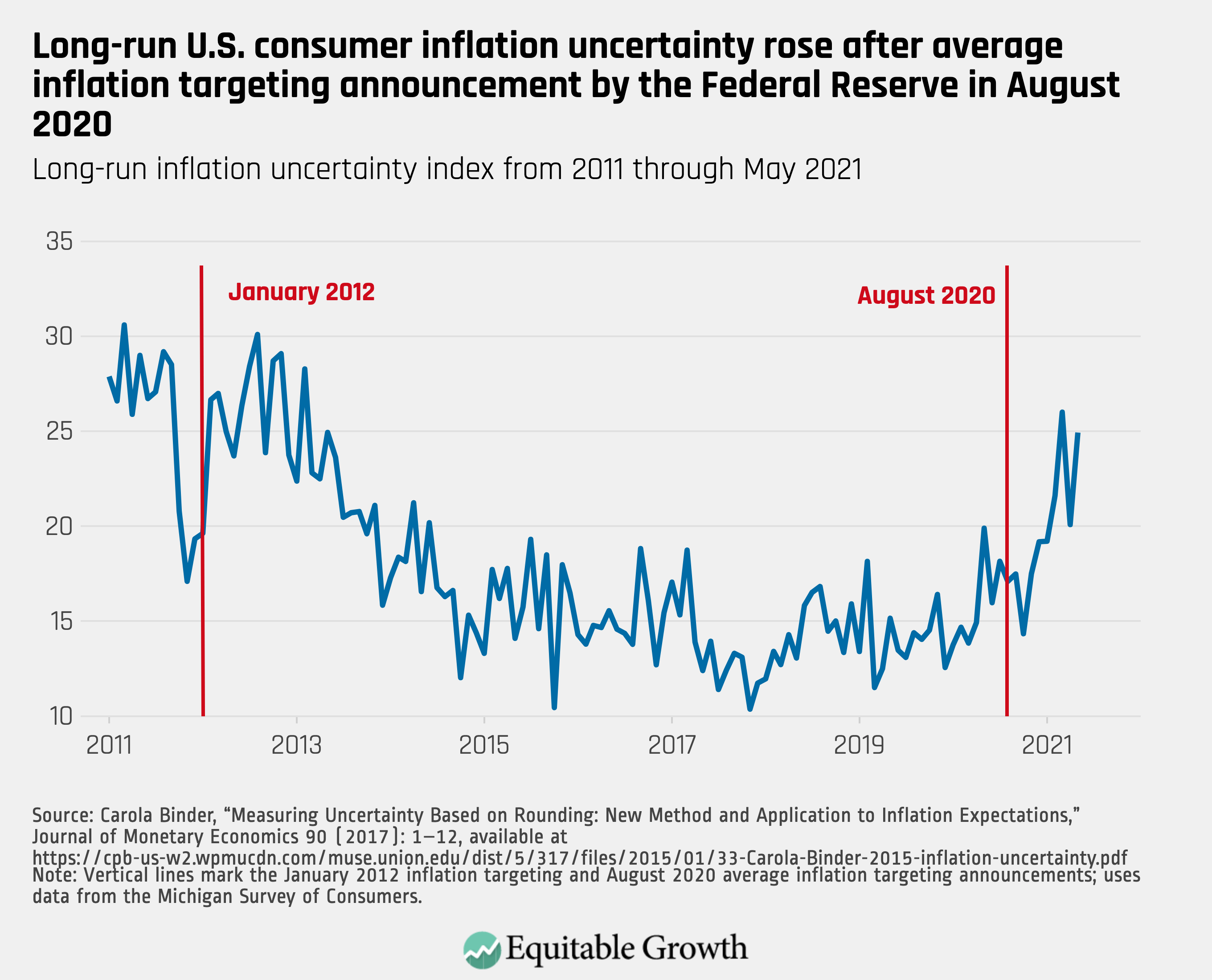

Long-run uncertainty declined following the 2012 average inflation targeting announcement, from an average of 25.7 in 2011 to 14.1 in 2019. In March 2021, long-run uncertainty rose to 26—the highest it has been since February 2013. It remains similarly high as of May 2021, the most recent month for which data are available. (See Figure 2.)

Figure 2

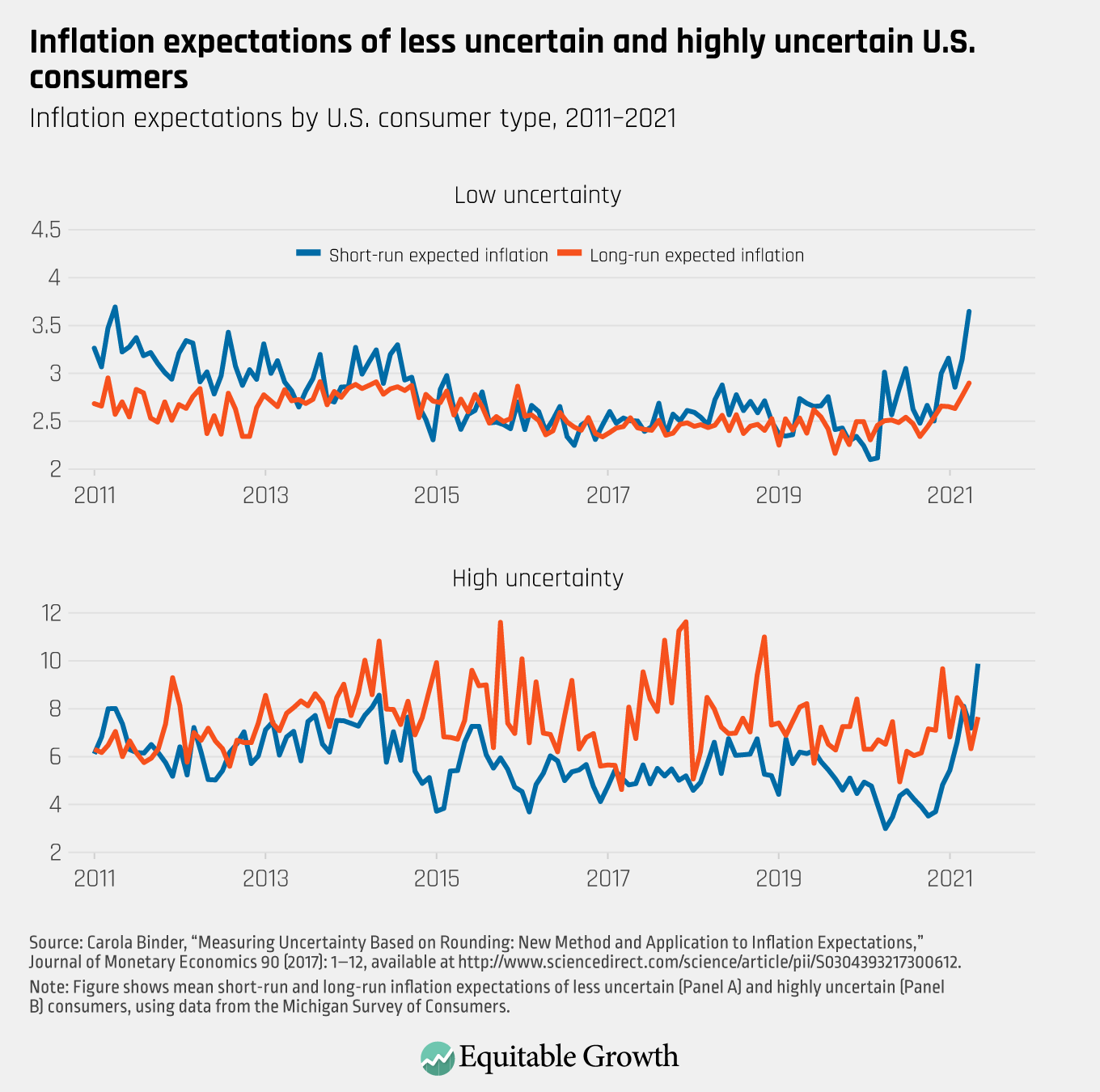

Another useful feature of my methodology is that it allows me to compute the mean (average) inflation expectations each month for the “less uncertain” and the “highly uncertain” consumers. Since the expectations of the highly uncertain consumers tend to be very noisy and high—because these consumers give round number forecasts such as 5 percent, 10 percent, and even 25 percent—focusing on the less uncertain consumers gives a clearer signal of how expectations are evolving.

As of May 2021, short-run and long-run inflationary expectations for these consumers are 3.6 percent and 2.9 percent, respectively, or about two standard deviations higher than they have been over the past decade. (If I had not separated the two types of consumers, then we would observe expectations of 5.7 percent for the short horizon and 3.5 percent for the long horizon.) (See Figure 3.)

Figure 3

The rise in short-run inflation expectations makes a lot of sense because consumers have noticed rising prices and reasonably expect higher inflation over the next year. The rise in long-run inflationary expectations implies that they (also reasonably) think that at least some of the new inflationary pressures are nontransitory.

Addressing long-run inflationary uncertainty

This rise in U.S. households’ long-run inflation expectations is not necessarily a problem at this point—after all, one point of average inflation targeting is to boost long-run inflation expectations so they don’t fall below target after years of too-low inflation. Moreover, the Michigan Survey of Consumers does not specify that respondents should provide expectations of personal consumption expenditures, or PCE inflation, which the Fed targets. Indeed, the respondents to the Michigan survey may be reporting expectations for something more like Consumer Price Index inflation, which tends to be around half a percentage point higher. So, the increase to 2.9 percent could be a move from “too low” to “just right,” rather than from “just right” to “too high.”

But the rise in long-run inflationary uncertainty is more clearly problematic. Uncertainty about long-run inflation makes it more difficult for households to plan for the future. They need to know, for example, how much to save for education or retirement, or to make good decisions about things like taking out a mortgage. These decision can be inherently stressful. This stress hits lower-income households hardest.

Inflation uncertainty is consistently two to three times higher for respondents in the bottom 30 percent of the income distribution, compared to the top 30 percent. Inflation uncertainty also is higher for women and for people without a college degree.

The trends of rising long-run inflationary expectations and rising long-run inflationary uncertainty, especially if these trends continue, should prompt U.S. monetary policymakers to further refine their approach to their average inflation target. Indeed, Fed Chair Jerome Powell, in a speech following his average inflation target announcement in 2020, explained that “we are not tying ourselves to a particular mathematical formula that defines the average.” What’s more, the Fed has not announced the time horizon over which they will compute average inflation. This gives the Fed a great deal of flexibility and discretion but comes at the cost of greater uncertainty.

Conclusion

By making its approach to average inflation targeting more explicit and transparent, the Fed could alleviate at least some of the recently growing uncertainty and keep expectations better anchored as inflation begins to rise. This would enable the Fed to facilitate a stronger U.S. labor market recovery before beginning to tighten.

Greater transparency about average inflation targeting would also make it easier for the U.S. public to hold the Fed accountable, which could improve the Fed’s credibility and democratic legitimacy. And if monetary policymakers have a little less discretion, that should put more impetus on elected officials to pursue sound and equitable economic policies, such as automatic stabilizers, rather than relying too heavily on the Fed to ensure a stable and sustainable U.S. economy over the course of business cycles.

—Carola Conces Binder is an associate professor of economics at Haverford College.