This essay is part of Vision 2020: Evidence for a stronger economy, a compilation of 21 essays presenting innovative, evidence-based, and concrete ideas to shape the 2020 policy debate. The authors in the new book include preeminent economists, political scientists, and sociologists who use cutting-edge research methods to answer some of the thorniest economic questions facing policymakers today.

To read more about the Vision 2020 book and download the full collection of essays, click here.

Overview

Competitive markets deliver to consumers a variety of benefits: higher productivity, lower prices, better quality products, and more innovation. Yet firms have a financial incentive to restrain competition in order to obtain monopoly profits. There are three main harmful methods of limiting competition: colluding with rivals in a market, merging with rivals or potential rivals, and using anticompetitive techniques to exclude existing or potential entrants.

U.S. antitrust laws are designed to prevent these behaviors by making price-fixing, bid-rigging, and similar behavior illegal, requiring government review of mergers to prevent those that lessen competition, and prohibiting anticompetitive conduct by an incumbent with market power that tends to exclude entrants and rivals. Unfortunately, over the past few decades, these laws have not been operating in a way that generates and preserves vigorous competition in U.S. markets.

It is well understood that market power decreases innovation, productivity, and the efficient use of resources. Market power, however, also contributes to growing inequality. Shareholders and senior executives who benefit from increased market power through higher salaries and increased stock prices are disproportionately wealthier than consumers, on average. Furthermore, consumers, suppliers, and workers may be harmed by paying higher prices for monopoly products or services and receiving lower compensation for the products and services (inputs or wages) they supply to monopsonists (buyers with market power).1

Consumption, by contrast, is not nearly so concentrated. Joshua Gans at the University of Toronto’s Rotman School of Management and his co-authors report that the consumption of the top 20 percent of the wealth distribution in the United States is approximately equal to that of the bottom 60 percent, but their equity holdings are 13 times larger. Thus, if a dollar of monopoly profit is transferred to lower prices, most of that dollar moves from benefitting the top 10 percent through the value of their stock or dividends to instead benefitting the bottom 90 percent through lower costs of purchases.

Therefore, antitrust enforcement redistributes wealth without incurring the traditional shadow costs arising from taxation and, indeed, is an actively beneficial form of redistribution for the economy.2 Because antitrust enforcement both redistributes income and wealth to the bottom 90 percent of the population, as well as increases efficiency, it should be the first choice of policymakers concerned with equity. The standard for anticompetitive harm that courts use today is the protection of consumer welfare—meaning price, quality, and innovation, now and in the future. Antitrust enforcement using the best available economic tools—developed, in some cases, decades ago—generates the evidence needed to show where such anticompetitive conduct is present.

The underenforcement described below is the fault neither of this standard nor of the economic tools themselves—though they could, of course, be better. The antitrust underenforcement we see today is primarily the result of decisions made over the past 40 years in the courts.

The four policies I recommend to reverse this harmful trend are:

- Dramatically increase the budgets of two federal antitrust agencies, the Federal Trade Commission and the Antitrust Division of the U.S. Department of Justice, which would be less expensive than it might appear because the two agencies collect disgorgement and restitution awards that flow back to consumers.

- Appoint leaders of these two agencies who are committed to using the best tools available to reverse the decline in competition. Aggressive but appropriate enforcement will either lead to good results or will identify failures in the law or by the judiciary to protect competition and consumers.

- Support and pass new legislation so that Congress can make it clear to the courts how it would like federal antitrust laws to be enforced and require courts to adopt up-to-date economic learning.

- Create a new “Digital Authority” to enforce privacy laws, protect digital identities and consumer data from being monopolized by private firms with market power, and create baseline conditions conducive to competition in digital marketplaces.

This essay will first address the “hot” topics in antitrust today, such as technology markets and digital platforms, as well as important everyday markets such as agriculture, transport, and pharmaceutical products, and then turn to my recommended reforms.

Market power has increased

The evidence for the failure of current U.S. antitrust policy is detailed in my report from May 2019 titled “Modern U.S. antitrust theory and evidence amid rising concerns of market power and its effects,” and its accompanying database.3 Economic evidence of rising market power comes from large samples of firms and industries. One widely discussed study of all publicly traded firms finds that markups (the difference between the price charged to a consumer and the cost to make an additional unit) have risen sharply since 1990 among firms in the top half of the markup distribution.4 Macroeconomists have further documented a declining share of national incoming going to workers and a rising share going to profit.5 New theories whose empirical implications are only now being explored also are possible contributors to rising market power. For instance, the huge growth in overlapping equity ownership of rival firms by diversified financial investors over the past four decades has plausibly led to less aggressive competition in many industries.6

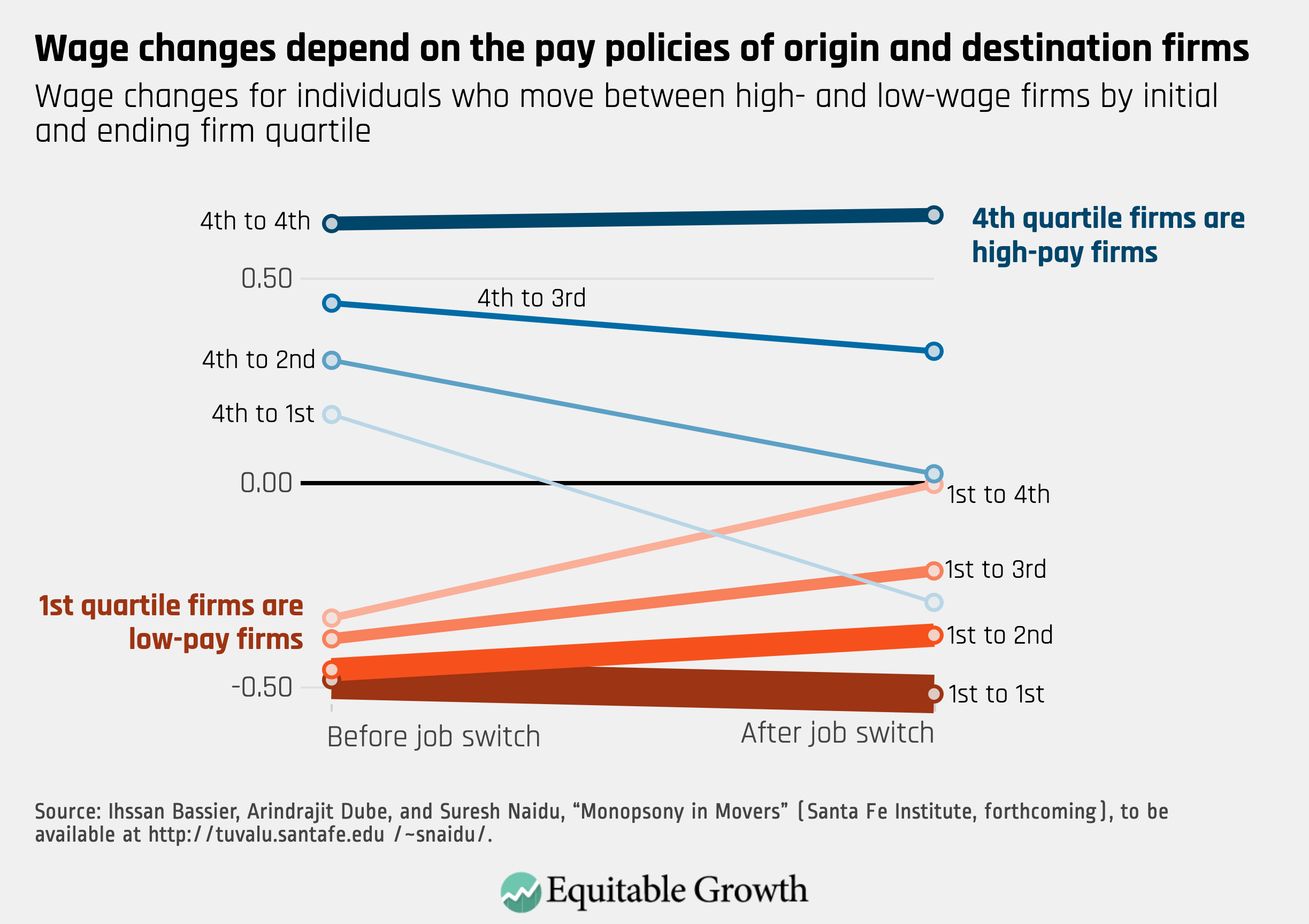

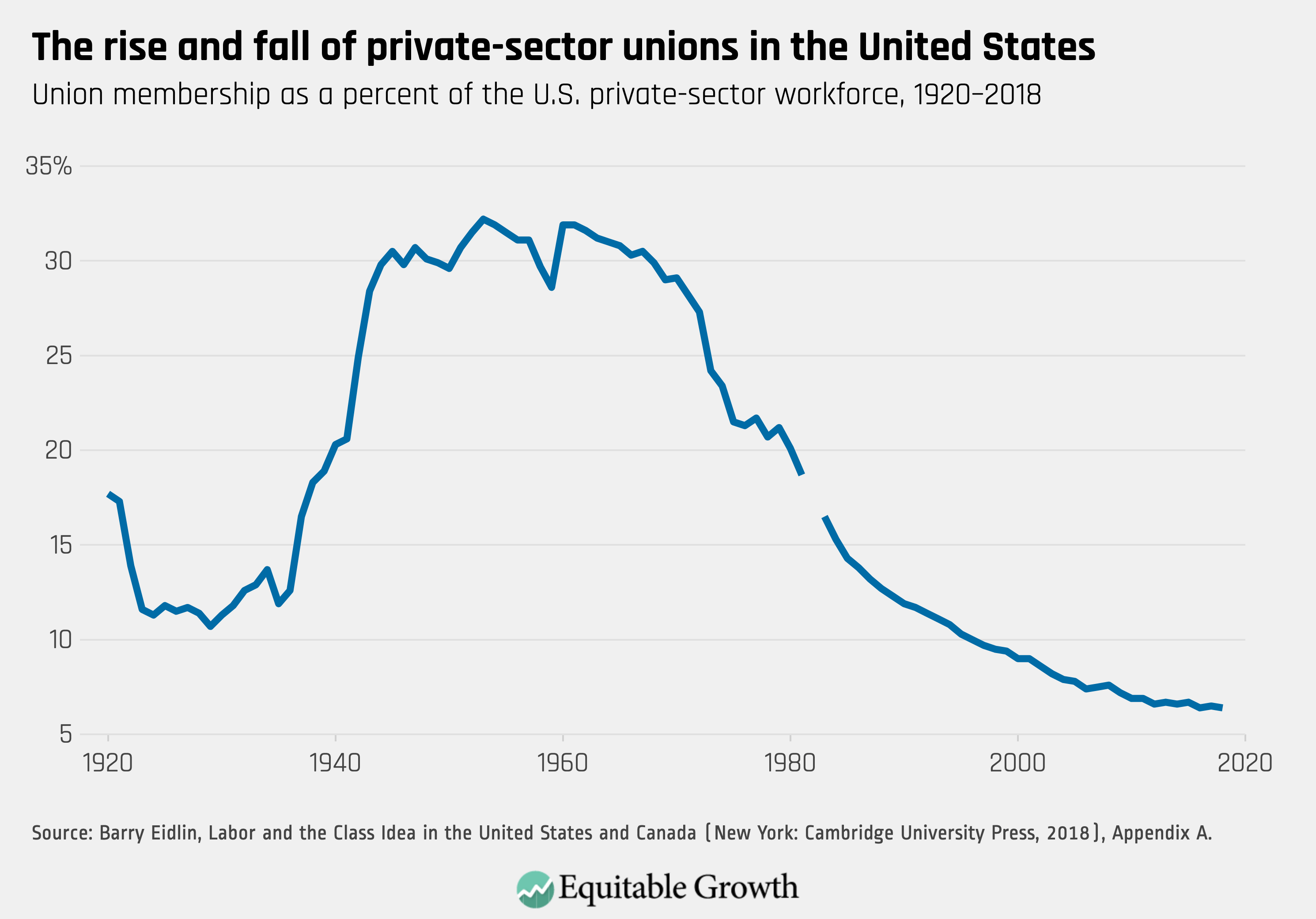

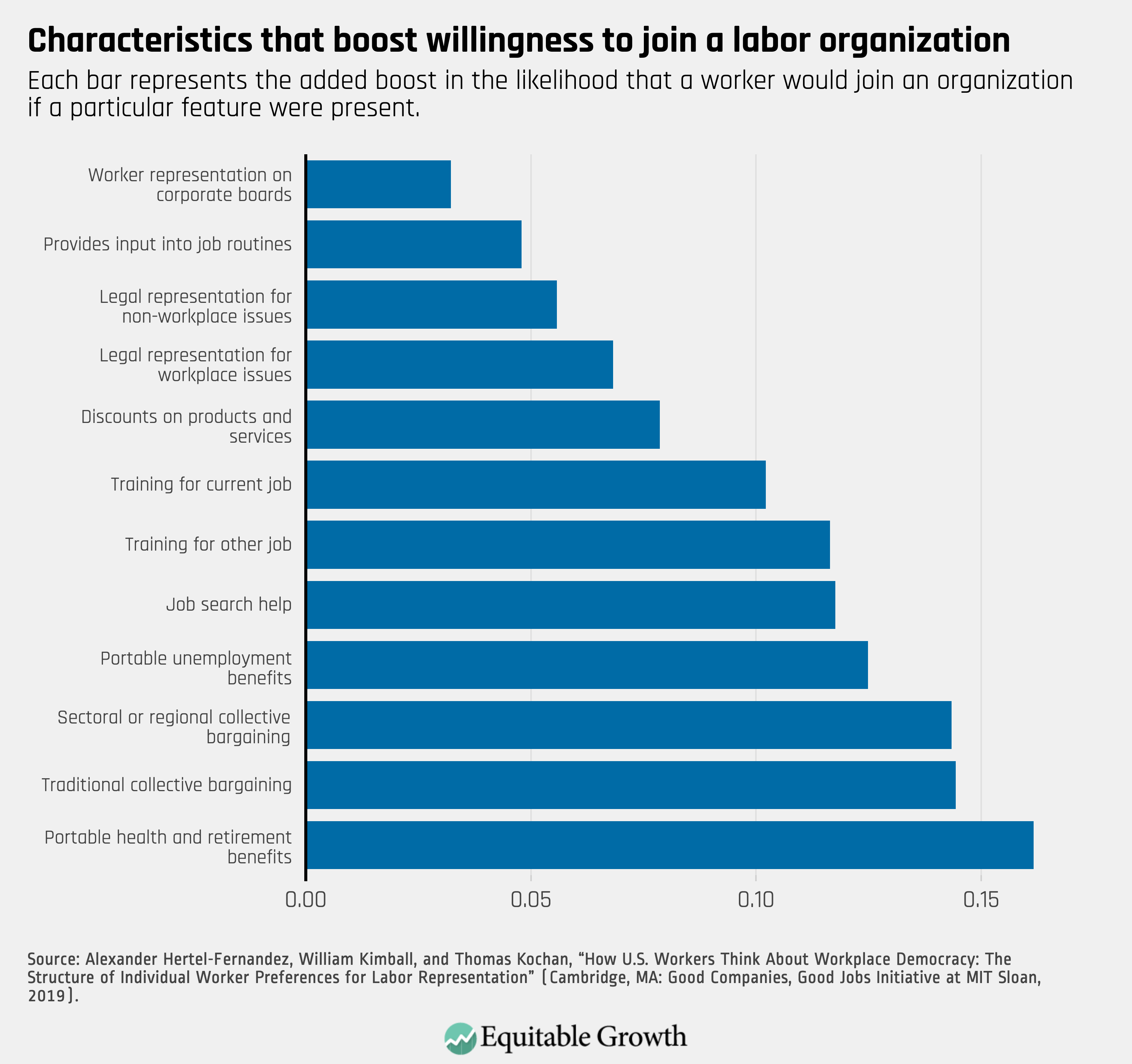

Still more evidence of market power comes from labor markets—in this case monopsony power, which is exercised by a buyer with market power (such as an employer) to pay less for its inputs (such as workers). Because workers have specialized skills and are often geographically constrained, monopsony power is common. Recent studies find that employers have monopsony power over college professors and nurses.7 Wages for nurses may stagnate after hospital mergers for this reason. The extensive use of noncompete agreements in employment contracts involving low-wage fast-food workers and the no-poach agreements between a number of high-tech firms over software engineers and between rail equipment suppliers over their workers, provide additional examples of anticompetitive conduct that harms workers.8

Evidence that antitrust laws are falling short is plentiful. Many cartels go undiscovered, and tacit collusion is probably even more prevalent because it is harder for antitrust enforcers to prosecute and deter.9 Anticompetitive horizontal mergers (between rivals) appear to be underdeterred.10 A variety of clever strategies used by incumbents to exclude entrants, either by purchasing them when they are nascent or using tactics to confine them to a less threatening niche or forcing them to exit have been successfully deployed in recent years, often when antitrust enforcement is late or absent.11

Each of these sources of concern can be critiqued, but together they make a compelling case. Some of the evidence may have benign explanations in part, such as the growing importance of fixed costs, for example, when creating software or pharmaceuticals that leads naturally to higher markups, or the increasing benefit of being on the same platform with other users (known as “network effects” in the case of a social media site). Firms in industries with high fixed costs or large network externalities may exhibit high profits and productivity and low labor shares, and may earn high profits because they had a good idea early and executed well, thereby getting adoption from many consumers.12 Nonetheless, the overall picture is clear that market power has been growing in the United States for decades. Moreover, even where the explanation for growing market power is benign, we must ensure that companies do not use anticompetitive tactics to protect their position.

Firms with market power need not compete aggressively to sell their products, so they tend to raise prices, reduce quality, and/or innovate less. Market power can also contribute to slowed economic growth by, for example, suppressing productivity increases.13 Theoretical and empirical economic studies convincingly show that innovation is harmed by anticompetitive conduct.14

This is why antitrust enforcement is such a terrific policy tool to strengthen competition—it does not come with an efficiency downside, as do most policies that redistribute income. Policies that enhance competition are unambiguously beneficial for efficiency, as well as inclusive prosperity, with minor qualifications.15 Other policies for addressing inequality, in particular, such as labor market and tax policies, may create disincentives or allocative efficiency losses that must be weighed against their distributional benefits. Policies to enhance competition, by contrast, offer what is close to a free lunch.16

An agenda to confront market power

An antitrust enforcement policy agenda to confront rising market power has four parts: increase enforcement resources; appoint agency leaders committed to using the best tools to combat the decline in competition; reform statutes to deter and prevent anticompetitive conduct more effectively; and use regulatory tools to foster competition. Let’s look at each of these policy components in turn.

Increase resources for enforcement

The resources expended on enforcing the antitrust laws in the United States are lower as a proportion of Gross Domestic Product than they were for most of the mid-1900s and have experienced a notable decline since 2000. Interestingly, this decline coincides with a rise in markups by firms, an increase in U.S. Supreme Court opinions protecting monopolists, and increasing policies that benefit incumbents. These patterns are consistent with the interests that favor corporate profits over consumers and those firms gaining more control of the political process to achieve all of these goals.

Approximately doubling the budget of both federal antitrust agencies would restore resources to a level where the agencies would be able to combat much more of the anticompetitive conduct present in the economy. In increasing resources, Congress should also consider whether it should provide funds to bolster the enforcement efforts of state attorneys general.

Appoint leaders committed to using the best tools available to enforce competition rules

Effective antitrust enforcement requires the appointment of enforcers who will vigorously protect consumers using modern economic tools. This will inevitably require litigation in the face of hostile legal rules, and possibly losses. Yet aggressive but appropriate enforcement will either lead to good results or identify failures by the judiciary to protect competition and consumers.

Leadership at the two agencies that is committed to reversing the decline in competition could take full advantage of existing antitrust laws. The game theory revolution (creation of tools to understand strategic interactions) in microeconomics beginning in the 1980s and the development of empirical techniques from the 1990s onward provide underutilized tools to identify and quantify harmful practices that can be attacked under the current antitrust rules.17

The enforcement agencies already use econometric methods, sophisticated simulations, bargaining theory, and other tools to identify harmful conduct and choose which cases to bring to court, yet in some instances, courts have trouble understanding these tools and resist accepting them as state of the art. Too often, court decisions, such as in the merger of AT&T Inc. and Time Warner Inc., reject modern economic ideas.18 Rather than change strategies, enforcers must continue to rely on the best arguments and evidence even if there is a chance that in the short run a court will not understand. Sound economics is critical to this approach: It shows where there is harm to consumers and explains how that conduct is harming consumers. Over time, the economic arguments can educate all of society, both the public and the courts. This is not an easy task but generates broad-based benefits.

The history of pharmaceutical pay-for-delay litigation amounts to a long string of losses in court for the Federal Trade Commission against drugmakers, eventually followed by success.19 This history shows that the agencies are capable of convincing courts to change their views when they rely on sound economics and persevere. Moreover, publicly demonstrating the harm through an ultimately unsuccessful court challenge can clarify to the public and to Congress when a court is ideologically opposed to protecting consumers from that harm.

One of today’s significant challenges is convincing courts to do more to protect potential competition from anticompetitive conduct.20 When markets become more concentrated because of network effects or economies of scale, the primary locus of competition shifts from competition in the market to competition for the market. In that setting, consumers rely on competitors who are about to enter, could potentially enter, or who are nascent competitors in the market to put pressure on oligopolists or dominant firms, making potential competition a critical source of consumer welfare.

While antitrust enforcers have had some success in attacking conduct by a monopolist that excluded nascent competition, as in high-profile litigation involving Microsoft Corp. two decades ago, doing so is particularly challenging when the excluded product poses a future competitive threat but has not yet had substantial marketplace success.21 The next leaders at the antitrust agencies must understand the need to bring cutting-edge cases to protect potential competition even in the face of legal hurdles.

Reform antitrust statutes to deter and prevent anticompetitive conduct more effectively

Increasing resources and more aggressive enforcement alone will not solve the problem. Judicial decisions interpreting the antitrust laws have significantly crippled antitrust enforcement. These decisions reflect, at best, an archaic economic understanding of competition or, at worst, simply bad economic reasoning.

Under a series of U.S. Supreme Court decisions over the past decade, for example, it is doubtful that the government could have successfully broken up AT&T’s phone monopoly in the 1980s. That break up, arguably the government’s most successful monopolization prosecution, focused on AT&T’s refusal to allow MCI, a long-distance competitor, to connect its long-distance service to local phone monopolies. In Verizon Communications v. Trinko, the Supreme Court dramatically expanded a monopolists’ ability to avoid antitrust liability when it refuses to deal with competitor or potential competitor, and also implied that antitrust concerns are subordinate in an industry subjected to the regulation.22 More recently, the Supreme Court misapplied basic economic reasoning in a case that, under some interpretations, has the potential to almost exempt technology platforms from antitrust enforcement: Ohio v. American Express.23 Since technology platforms comprise an ever-increasing share of economic activity, this situation is of grave concern.24

Even where the antitrust plaintiffs have been successful, the difficulty and cost of those successes suggest systematic underweighting of the benefits of competition and deference to the desire of the corporation for increased market power. The government’s long battles over stopping pay-for-delay deals and anticompetitive hospital mergers are notable examples of this misalignment, as is the approval by the government of the Sprint-T-mobile merger. In all of these cases, the corporations did not seek that market power on the merits, but through regulation (Trinko or state-supervised hospital mergers), exclusion (pay for delay and American Express), or merger (AT&T-TimeWarner or Sprint-T-mobile).

Despite the government’s success in some merger litigation, this success only occurs in transactions that most clearly violate the law.25 The fact that the two antitrust agencies must litigate cases that are clearly anticompetitive—rather than the parties not even considering the deal in the first place or abandoning it after the government makes its concerns known—speaks to the limitations of current antitrust legal doctrine.

It would likely take decades to reverse this body of accumulated legal doctrine, even if every future case that was litigated were decided with perfect accuracy. Fortunately, Congress is the final arbiter on competition law and can change it to reflect the desire of society for competitive markets. Congress has not substantively amended those laws in more than 60 years. A broad foundation of economic research supports retooling our antitrust laws for the 21st century and restoring the vigor that was originally intended. Although legislation can take many forms, successful antitrust reform legislation should accomplish four goals:

- Overturn Supreme Court precedent that has inoculated exclusionary conduct from antitrust scrutiny even when it harms competition by eliminating or harming competitors

- Prohibit courts from assuming that some aspect of a market is competitive or will become competitive rather than assessing the evidence in the case

- Create simple rules (known as presumptions) that will lower the resource cost of enforcement for conduct and acquisitions that economic research shows are likely to raise competitive problems

- Clarify that the antitrust laws are designed to protect competition that may manifest itself across a broad range of outcomes such as higher prices, reduced quality, harm to innovation, lower input prices, and elimination of potential competition

Lastly, Congress could consider two ways to raise the expertise level of judges. One is to require the court to hire its own economic expert in an antitrust case, paid by the parties. The neutral expert’s task would be to help the court understand the economics presented by each side. A second option is to create a specialized trial court to hear cases brought under the federal antitrust laws.26 Doing so would allow antitrust cases to be heard by judges with experience in evaluating complex economic evidence. A sophisticated judge would encourage litigants to rely on the best economic arguments and modern economic tools applied to the facts in the case, improving the accuracy of judicial decisions and discouraging judicial acceptance of the erroneous general economic assumptions that have supported relaxed antitrust enforcement.27 A term on such a specialized court should be of relatively short duration to limit the possibility of capture or entrenchment.

Download FileReforming U.S. antitrust enforcement and competition policy

Complementary regulation that promotes competition: Create a federal digital authority

There is a real need for federal agency to regulate digital businesses. This new agency could create a baseline level of competition in an area that lacks it. Regulations under its purview could enhance competition by, for example, facilitating digital-data portability that would allow a consumer to take her own data in a usable format from one provider to a competitor (such as moving purchase history from Amazon.com to Jet.com).

A new agency also could define and regulate “interoperability” in the digital arena; for example, a Verizon phone can call an AT&T phone because they are interoperable. A digital authority could ensure social media sites were also interoperable so that a person who uses Snap, for example, could follow her friends who post content on Instagram or another site. And it could consider the creation of open standards that promote competition, such as a standard for micropayments. These payments in fractions of a cent cannot practically be made today because the transaction cost is higher than the amount being paid. But micropayments may be critical in compensating consumers for their attention, may be an important dimension of competition between platforms, and may aggregate to significant benefit to consumers. By creating one system, a regulator could enable price competition in attention markets.

In addition, this new regulator could be tasked with enforcing somewhat stricter antitrust laws for those digital platforms or sectors that Congress felt required additional scrutiny and speed, or where competition was particularly valuable for society. This would allow a faster, more specialized agency to protect small entrants into digital marketplaces from exclusion or discrimination by the incumbent platform. It would also allow for review of even the smallest acquisitions when those small firms are being acquired by the largest incumbents. In general, the agency could have a mandate to protect and facilitate entry to address competition problems in the digital sector.

—Fiona M. Scott Morton is the Theodore Nierenberg Professor of Economics at the Yale University School of Management. (This essay draws on ideas developed in prior work jointly with Jonathan Baker, a research professor of law at American University Washington College of Law.)