The U.S. labor market delivered employment gains that were far below expectations last month. According to the Employment Situation Summary released this morning by the Bureau of Labor Statistics, between mid-March and mid-April the U.S. economy added only 266,000 non-farm payroll jobs, and the share of the population between the ages of 25 and 54 that is employed—a measure economists call the prime-age employment to population ratio—increased only slightly, from 76.8 percent in March to 76.9 percent in April.

April’s Jobs report is a stark reminder that the U.S. labor market continues to be a long way from its pre-pandemic employment levels. The U.S. economy now has a jobs deficit of 8.2 million compared to February, 2020, before the coronavirus pandemic and resulting recession hit. For the millions of workers who have lost their jobs, including many young workers and those who experienced structural disadvantages in the labor market well before the coronavirus recession, this crisis may lead to long-term damage to their economic outcomes.

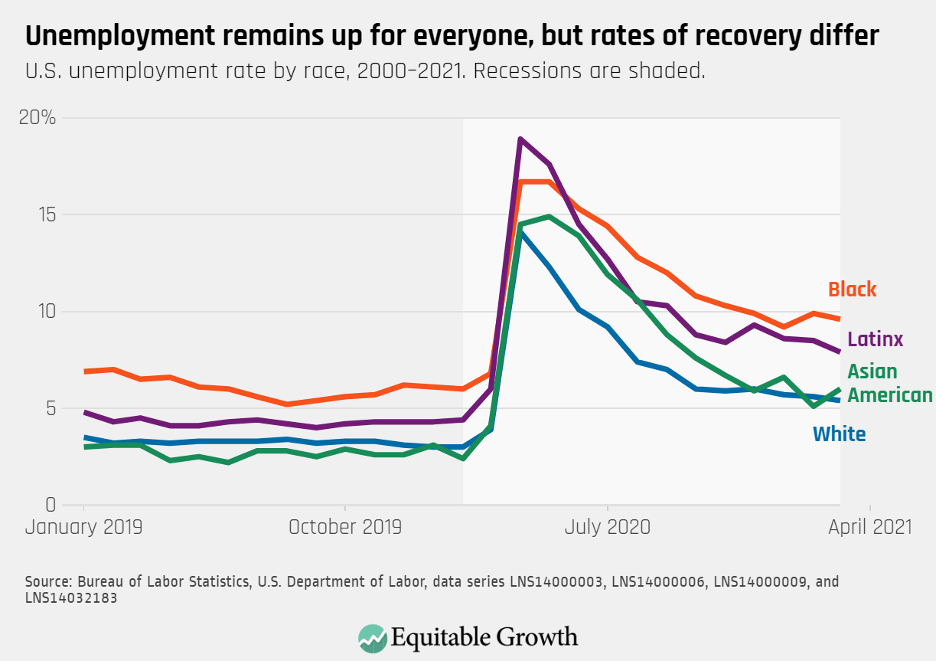

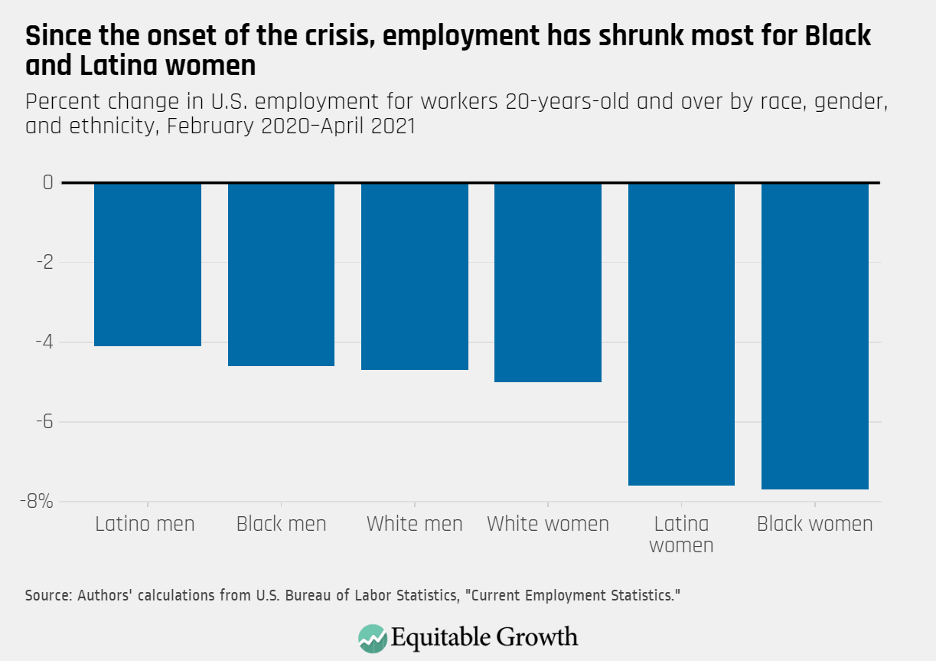

The modest net increase in employment was not spread evenly across the workforce. At 9.7 percent, the unemployment rate for Black workers is higher than for any of the other major racial or ethnic groups, followed by the jobless rate of Latinx workers (7.9 percent), Asian American workers (5.7 percent), and White workers (5.3 percent). Across race, ethnicity, and gender, Black women saw an important increase in employment, adding 135,000 jobs. Yet the number of Black women employed is still 7.7 percent below pre-coronavirus recession levels. Along with Latina women, Black women’s employment has declined more than for any other group. (See Figure 1.)

Figure 1

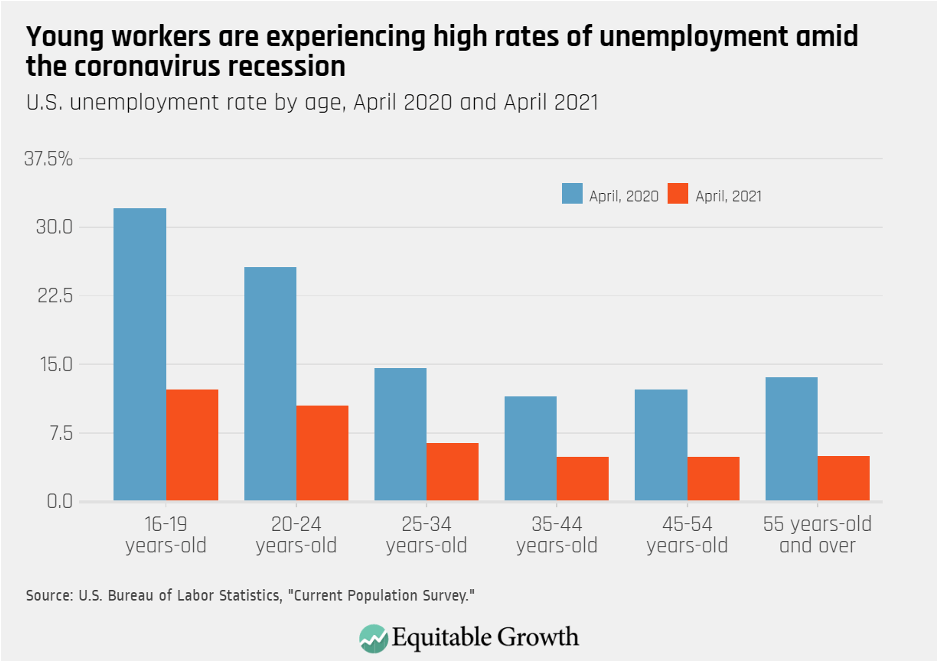

Young workers are another group that has been hard hit. As the health and economic crises hit the United States, the unemployment rate of workers between the ages of 16 and 19 skyrocketed, going from 11.5 percent in February 2020 to 32.1 percent in April 2020. For workers between the ages of 20 and 24 the jobless rate climbed from 6.3 percent to 25.6 percent during the same period. Currently at 12.3 percent and 10.5 percent, respectively, the jobless rate for the youngest subsets of workers in the U.S. economy is both above pre-pandemic levels and above the jobless rate of older workers. (See Figure 2.)

Figure 2

Research from the early months of the coronavirus recession shows that younger workers—along with workers of color, workers with lower levels of educational attainment, and women workers—experienced both particularly large decreases in hiring and particularly large employment losses. These results hold even when accounting for young workers’ occupational distribution, since they are overrepresented in positions that have been among the most exposed during this downturn, including lower-paying service jobs in the leisure and hospitality industry.

Moreover, at the height of the recession last spring young Black, Asian American, and Pacific Islander workers experienced especially high jobless rates, reaching nearly 30 percent according to an analysis by the Economic Policy Institute, compared to 24 percent among all workers between the ages of 16 and 24.

What makes younger workers so vulnerable to slack business conditions? For one, research shows that workers who first step into the U.S. labor force during a recession experience persistently harmful effects on their future labor market outcomes. Usually, early careers are periods of strong earnings growth—a process that can be disrupted by recessions. In addition, because earnings mobility has declined since the 1980s, where workers start off in the earnings distribution is increasingly important.

Research by Jesse Rothstein at the University of California, Berkeley, finds, for instance, that workers who graduated college during the Great Recession of 2007–2009 had lower employment rates and earnings than older college graduates. Likewise, research by Kevin Rinz of the U.S. Census Bureau shows that during the Great Recession, millennials (people born between 1980 and 1994), experienced especially large earnings losses that persisted even as the U.S. economy recovered.

In part, Rinz finds, these losses were driven by millennials’ lower likelihood to work for high-paying employers even as their employment rates recovered. Rinz also finds that millennials suffered from structural changes to local labor markets in hard-hit locations that caused persistent lower earnings and employment opportunities even as the overall national economy moved beyond the recession.

As the U.S. economy struggles to return to pre-pandemic levels, it is important to highlight the persistent negative economic consequences facing the hardest hit workers that could last well into the forthcoming economic recovery and exacerbate long-term trends of rising economic inequality and insecurity. A year after one of the worst months for the U.S. labor market, an important way to prevent young workers from the harmful long-term consequences of recessions is to promote healthy earnings growth through policies that increase wages, such as lifting the federal minimum wage floor and fostering unionization to offset the persistent downward pressure on wages facing these workers.

To ensure that happens, policymakers should make heavy long-term investments in the broader U.S. economy alongside economic relief to workers and families and greater access to Unemployment Insurance benefits to give affected workers a strong and stable foundation to build on during the eventual recovery. Specifically, under the current Unemployment Insurance system, self-employed workers, workers just stepping into the labor force, and workers who do not meet the minimum earnings thresholds are not eligible for regular jobless benefits, hurting both individual workers and the entire economy. To ensure the damages caused by the coronavirus recession can be overcome swiftly and sustainably, all young workers and other vulnerable workers need to be able to benefit from one of the country’s most important income support programs.

During his first 100 days in office, President Joe Biden turned core elements of his Build Back Better campaign plan into concrete policy proposals for congressional consideration. Dubbed the American Jobs Plan and the American Families Plan, his two most recent proposals are designed to complement the temporary economic boosters included in the American Rescue Plan—legislation, passed by Congress and signed by the president in March, focused on addressing the coronavirus recession.

The American Jobs Plan and the American Families Plan, though, would go further than the American Rescue Plan. President Biden’s two new plans would make large-scale, and in some cases permanent, investments in the nation’s physical and human infrastructure, combating racial, income, and wealth inequality and restructuring large parts of the U.S. economy. As 225 leading economists explained in a letter to Congress earlier this month, these proposals, if designed correctly, could promote strong, stable, and broad-based economic growth. And indeed many of the big ideas included in the two new plans are backed by extensive academic evidence, much of which has been funded and featured by the Washington Center for Equitable Growth.

Let’s walk through the major elements of the administration’s new plans, which were outlined by the president in a joint address to Congress last night, alongside the underlying academic evidence, in turn.

American Jobs Plan

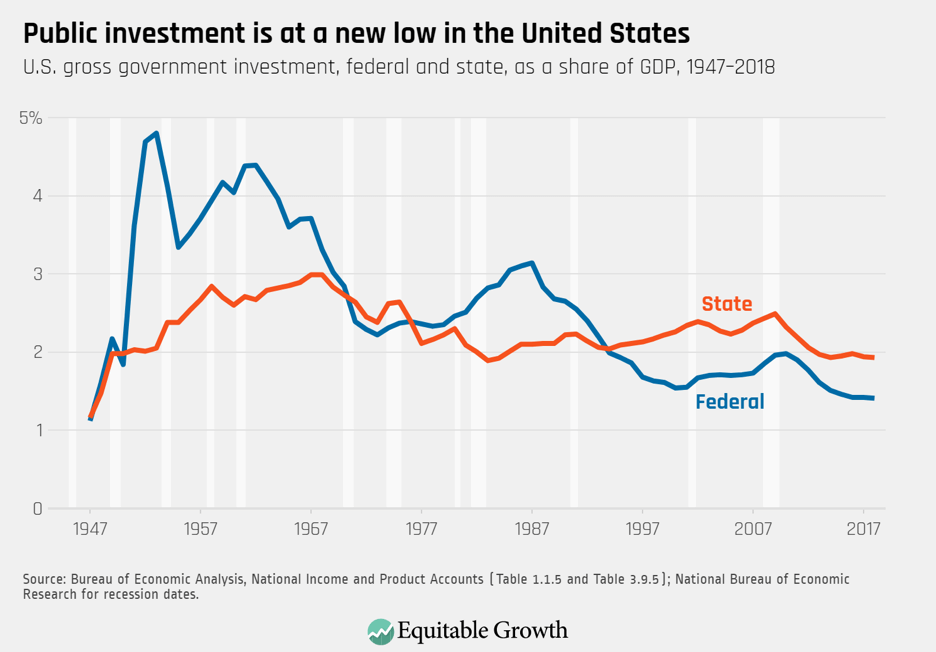

In total, this plan includes $2.3 trillion in public investments in physical and human infrastructure, science research and technological development, and climate change mitigation and environmental justice. It would begin to reverse the decades-long downward trend in government investment. (See Figure 1.)

Figure 1

We know from academic research that the decline in public investments has weakened growth and increased inequality. Specific policies in this plan to address these weaknesses include:

Nearly $1 trillion for upgraded transportation infrastructure, including roads, rail, and bridges; improved water systems; expanded broadband; and enhanced electricity grids. Black, Latinx, and Indigenous communities suffer disproportionately from long commute times, unsafe drinking water, and unreliable broadband access, so these investments will begin to address our country’s insidious racial inequities.

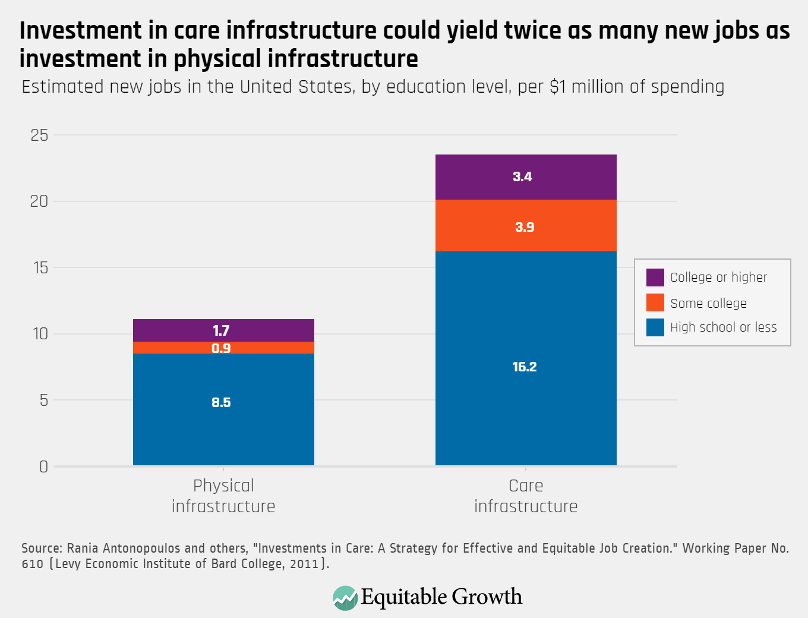

A $450 billion investment in long-term care services and supports through Medicaid. As nearly 200 social scientists wrote in a recent letter to Congress, this investment will improve care for our aging population and invest in long-term care workers, who are today largely underpaid women of color. Improving job quality for care workers helps the workers themselves, prevents patient deaths by improving the quality of care, and is good for the U.S. economy. In fact, this type of investment in “care infrastructure” boasts the potential to create twice as many new jobs as investments in physical infrastructure alone. (See Figure 2.)

Figure 2

The Protecting the Right to Organize, or PRO, Act, which would modernize decades-old labor laws to address the growing power imbalance between workers and businesses. It would make it easier for workers to organize and collectively bargain, thus ensuring that the millions of jobs created by the American Jobs Plan are high-quality positions that include fair pay, predictable schedules, and good benefits, among the other advantages of unionization.

The American Jobs Plan also calls on large, profitable firms to pay more in corporate tax to help finance these investments. Though the federal government has the fiscal capacity needed to deficit-finance the growth-enhancing investments included in the American Jobs Plan—and research shows that previous concerns about deficits and debt are overblown—many U.S. corporations have prospered throughout the coronavirus recession and received large and economically wasteful tax cuts in 2017, so raising revenue from them is both fair and consistent with strong, stable, and broadly shared growth.

American Families Plan

The American Families Plan, released by the White House yesterday, is all about human capital investments and enhancing the nation’s social infrastructure so that children are not raised in poverty, have access to high-quality pre-Kindergarten and child care, and families can better balance caregiving and work obligations. Specific policies in this $1.8 trillion plan include:

Guaranteeing all workers access to paid family, medical, and sick leave. Today, only 20 percent of private-sector workers access paid family leave through their employers, and 44 percent of U.S. workers do not even qualify for unpaid leave through the Family and Medical Leave Act. This leaves many workers with the impossible choice of caring for loved ones or keeping their jobs. And caregiving responsibilities are a significant driver of women’s exit from the labor force, which helps explain why the U.S. women’s labor force participation rate was 56.1 percent in March 2021, a 33-year low. Women of color have been hit the hardest by the collision between caregiving responsibilities and the coronavirus pandemic.

Expanding access to high-quality child care options through a $225 billion investment and a permanent extension of the enhanced Child and Dependent Care Tax Credit. Research shows that parents’ labor force participation increases when child care is more affordable and accessible. In one study, a $100 increase in the price of child care is associated with a 3.7 percentage point decrease in that neighborhood’s labor force participation rate among women. Meanwhile, high-quality early care and education can lead to long-term improvements in a child’s human capital. Children in high-quality programs demonstrate better education, economic, health, and social outcomes and fewer negative outcomes—such as deleterious involvement in the criminal justice system. These high-quality programs can help pay for themselves, generating up to a 13 percent return on investment per-child, per-year.

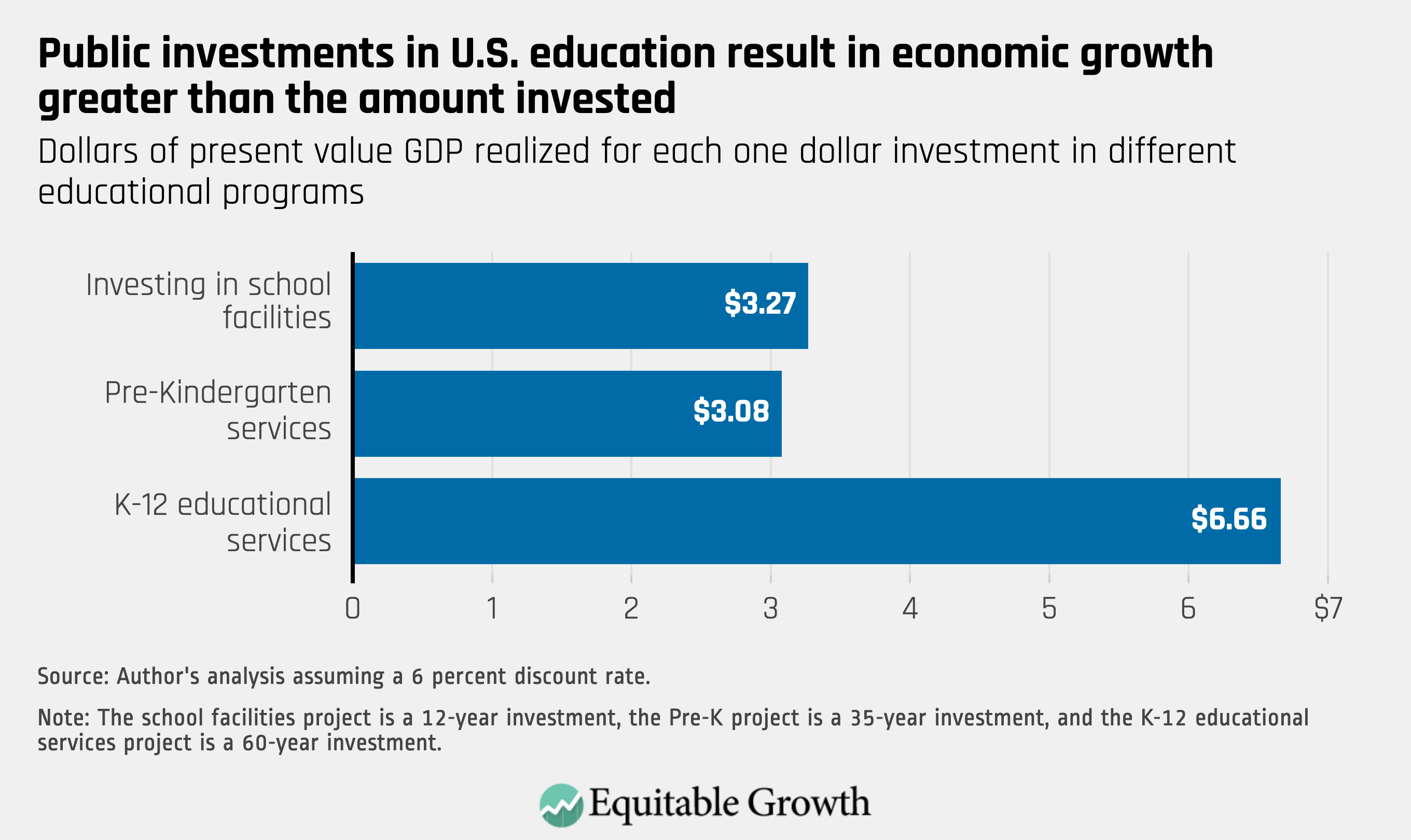

$200 billion of investments in universal pre-kindergarten. Academic research finds that pre-K programs can spur growth, create jobs, and ultimately pay for themselves. (See Figure 3.)

Figure 3

A four-year extension of the enhanced Child Tax Credit that was included in the American Rescue Plan enacted in March. Sometimes described as a “child allowance,” the evidence shows that this policy would pay dividends not just for low- and middle-income families, but the economy as a whole.

The use of automatic triggers, based on economic conditions, to extend the length and amount of Unemployment Insurance benefits, some of which are currently scheduled to expire in September. The plan does not outline a vision for revamping the Unemployment Insurance program writ large, but ensuring that program enhancements turn on and off based on objective economic indicators rather than arbitrary and politically-negotiated dates is a major step in the right direction.

The United States has the fiscal space to finance these investments with deficits, but President Biden proposes to finance this package with taxes on the income and wealth of the richest Americans. The top 1 percent of income earners now enjoy the fruits of a historically outsized share of the nation’s economic growth. The American Families Plan envisions raising the top income tax rate from 37 percent to 39.6 percent for individuals making more than $400,000 a year, equal to the top marginal rate in 1997 (and for much of the 1990s and between 2013 and 2017). In the United States, wealth is even more inequitably distributed than income, so the American Families Plan wisely proposes to raise revenue by taxing the investment income from capital gains of Americans making more than $1 million per year. This would equalize the rates paid by people who earn income through work and those who earn it from investments. Raising revenue from the rich in this way could raise even more revenue than traditional estimates assume, especially because it proposes to end a loophole called “stepped-up basis,” which allows some capital gains to never be taxed at all. The proposal also includes new enforcement resources for the IRS, which will allow the federal agency to target tax evaders in the top 1 percent of income earners, who research shows hide 20 percent of their income from tax collectors.

Conclusion

The top fiscal policy priority for U.S. policymakers should be to make long-overdue public investments in physical and human infrastructure, which evidence shows will pay long-term dividends in the form of strong, stable, and broadly shared economic growth. These investments should be focused on the areas that are most holding back the U.S. economy—and that were so exposed by the coronavirus pandemic—namely combating racial discrimination and injustice, mitigating the effects of climate change, empowering workers, and expanding social insurance protections. The key elements of the American Jobs Plan and American Families Plan, as described by President Biden in his joint address to Congress last night, would represent a huge step toward those goals.

Attention now turns to Congress, which must work with the administration to fill in the details and craft legislation that can pass both chambers. Some concerns raised by some members of Congress, such as those around deficits and economic “overheating,” are not well-founded and should not stand in the way of action. But there remain legitimate questions about which elements of the president’s plans should be included or excised, and which policies that were left out by the president—such as instituting mark-to-market capital gains taxation, cancelling student loan debt, and improving the way we measure the economy—should be added back in by Congress.

In answering these questions, our hope is that policymakers follow the compilation of academic evidence that Equitable Growth and others have assembled and capitalize on this opportunity to make structural economic change that spurs strong, stable, and broad-based growth.

Critics of President Joe Biden’s $1.9 trillion American Rescue Plan and further public investments financed through a combination of tax increases and deficit spending—such as his administration’s proposed American Jobs Plan, at roughly $2 trillion, and the forthcoming American Families Plan—often argue that the U.S. economy will “overheat” if policymakers pump too much support into the U.S. economy too quickly.

Yet plans for further public investments should be judged primarily on the merits of those investments. Arguments that the U.S. economy will overheat ignore the need for additional investments in the economy and rely on the possibility of future policy errors to argue against needed investments today.

This factsheet explains how economists and policymakers colloquially use the term overheating, why it’s not really a concern, and why it distracts from the more important debate about the kind of investments required to create a more equitable and sustainable economic recovery coming out of the coronavirus recession.

What is overheating?

The term overheating refers to an economy in which the actual level of goods or services produced, or the Gross Domestic Product, exceeds potential GDP.

What is potential GDP?

Potential GDP is a theoretical quantity. It is the estimated amount of output that would be produced assuming full utilization of inputs. In this situation, unemployment is low and reflects only transitions between jobs or new entrants to the labor force.

Importantly, potential GDP is a theoretical quantity that cannot be directly observed. Economists can estimate potential GDP, but they will never know with certainty what it is. As a result, policymakers never know for sure whether GDP is above or below potential. One part of the debate about whether the Biden administration’s policies could cause overheating is a debate about what potential GDP is.

Why is potential GDP important?

The Congressional Budget Office’s estimates of potential GDP are highly influential, but critics argue, with substantial justification, that CBO analysts have been unduly pessimistic about the capacity of the economy in recent years, and thus overstate the risk of overheating.

As economists Adam Hersh at the University of Massachusetts Amherst’s Political Economy Research Institute and Mark Paul at the new College of Florida point out, these estimates also include assumptions that embed racial disparities into their forecasts of the “natural rate of unemployment,” which is an estimate of the level of unemployment where potential GDP is reached. The Congressional Budget Office, for example, estimates that the “natural rate” of unemployment for Black workers, at 10 percent, is more than double that of White workers (4.4 percent), and the “natural rate” of unemployment for Latinx workers (6 percent) is more than one-third higher than that of White workers.

Can potential GDP be misleading?

The implications of the Congressional Budget Office’s assumptions about potential GDP and the natural rate of unemployment can be misleading. These assumptions would mean that the Black unemployment rate—which reached a record low of 5.5 percent in August 2019 without any inflationary consequences—would never be expected to fall below the overall peak unemployment rate during the Great Recession, at 10 percent. Moreover, these assumptions would also mean that the Latinx unemployment rate—which reached a record low of 4 percent in September 2019, again without any inflationary consequences—would never be expected to fall below 6 percent.

Notably, the CBO’s baseline deficit projections assume that current law is unchanged, just as CBO’s estimates of potential GDP assume current law and regulation. But changes in law and regulation can change potential GDP. This is particularly important when evaluating policies that aim to invest in the productive capacity of the economy in the future, including investments in people or physical infrastructure.

The U.S. economy has 10 million fewer jobs today than it likely would absent the coronavirus pandemic and resulting recession. This is why now is not the time for concern about overheating. The prominence of the concern, in fact, reflects the scale of the policy response to the pandemic and the recession, especially the recently enacted $1.9 trillion American Rescue Plan.

Even so, it is difficult to state with confidence how the actual level of GDP will compare to potential GDP in the near future. Wendy Edelberg and Louise Sheiner of The Brookings Institution estimate that legislation of approximately the scale of the American Rescue Plan would restore actual GDP to potential GDP after the third quarter of 2021, cause GDP to exceed potential GDP temporarily by a modest 1 percent in the fourth quarter of 2021, and then allow GDP to roughly match its potential path in the middle of 2022.

If potential GDP is higher than Edelberg and Sheiner estimate or the American Rescue Plan causes less spending than they project, then the U.S. economy will be less likely to overheat. If potential GDP is lower or the American Rescue Plan causes more spending, the economy would be more likely to overheat.

Then, there are the two forthcoming public investment packages from the Biden administration. The president’s American Families Plan will be unveiled later this week, but there are enough details about his American Jobs Plan for some early analysis. A projection by Mark Zandi and Bernard Yaros of Moody’s Analytics implies the American Jobs Plan may set the real GDP (after accounting for inflation) on a path that modestly exceeds the Congressional Budget Office’s pre-pandemic projections for potential GDP. Yet the general macroeconomic benefits—such as long-term employment gains and fully recovered labor force participation among women and workers of color—significantly outweigh any concern for possible overheating.

What happens if the economy overheats?

From many perspectives, an overheated economy is a strong economy. Unemployment is very low, and it becomes much easier for workers to find jobs, and especially better-paying jobs. It is harder for employers to discriminate and may have disproportional positive effects on traditionally excluded workers such as Black Americans. Low unemployment may also create wage pressures, especially for low-wage workers who generally face much greater competition for jobs.

Concerns about an overheated economy typically focus on a set of potential consequences that could arise if it remains overheated for a long time. If an economy remains overheated for many years, then that could lead to higher inflation. If the Federal Reserve, in response to that inflation, pushes the U.S. economy into recession by pushing up interest rates, then that could cause widespread harm.

Yet this concern is less about overheating specifically, and more about extended overheating followed by a bad policy response. There is no obvious reason to believe that a short period during which GDP exceeds potential GDP will lead to this set of outcomes. This is the case because concerns about overheating often rely on analyses of what has happened in prior periods of U.S. economy history, such as the inflationary years of the 1970s, which were followed by the disinflation and recessions engineered by then-Fed Chair Paul Volcker. But there are important ways in which the economy has changed since then.

Indeed, the rise of economic inequality over the past six decades makes the experience of the 1970s less relevant for forecasting the future. There also is no compelling reason to view narrowing the scope of policy ambition now as a superior approach to avoiding these theoretically adverse outcomes before they might possibly happen. A better approach is for the Fed to change the nature of its response down the road or for Congress to change its fiscal policy response if inflation were to emerge.

Should policymakers be focused on overheating?

Concerns about overheating are offered as a reason to scale back the scope of forthcoming economic recovery legislation, specifically the Biden administration’s approximately $2 trillion American Jobs Plan and forthcoming American Families Plan. These concerns, however, are more about the scale of the tax increases on higher-income families and corporations needed to pay for these investments, as well as the smaller amount of deficit financing envisioned in these two legislative packages, compared to the recently enacted American Jobs Plan.

In fact, this factsheet details why overheating is of relatively little direct concern. Much of the actual concerns about overheating could be better addressed down the road should the symptoms of possibly arise.

Conclusion

The entire conversation about overheating distracts attention from where economic policymakers should be focused. They instead should be focused on the investments in the two forthcoming legislative packages—whether the proposed investments are a good idea, regardless of how they are financed. The primary case against investments is that they may be unwise or perhaps unmerited, not that they are financed by higher taxes and more deficit spending.

The primary case for these large public investments is that they are valuable and important. Debates about investments should focus more on that question and focus less on overheating.

The United States is the only advanced economy in the Organisation for Economic Co-operation and Development that does not guarantee any paid family and medical leave to its entire workforce. Though 10 U.S. states and localities have currently implemented or have begun to implement programs for their residents, there is no nationwide paid family and medical leave plan that covers all workers across the country regardless of where they live or work.

As a result of this policy choice, U.S. workers, their families, and their employers often lack the resources and support they need during a family transition or health shock, including the arrival of a new child, an aging parent, a diagnosis of an illness, and personal injuries. When paid leave from work to deal with and adjust to these moments is needed but not available, workers are forced to choose between their responsibilities at home and earning a paycheck, which can have far-reaching implications for families, employers, and the broader economy.

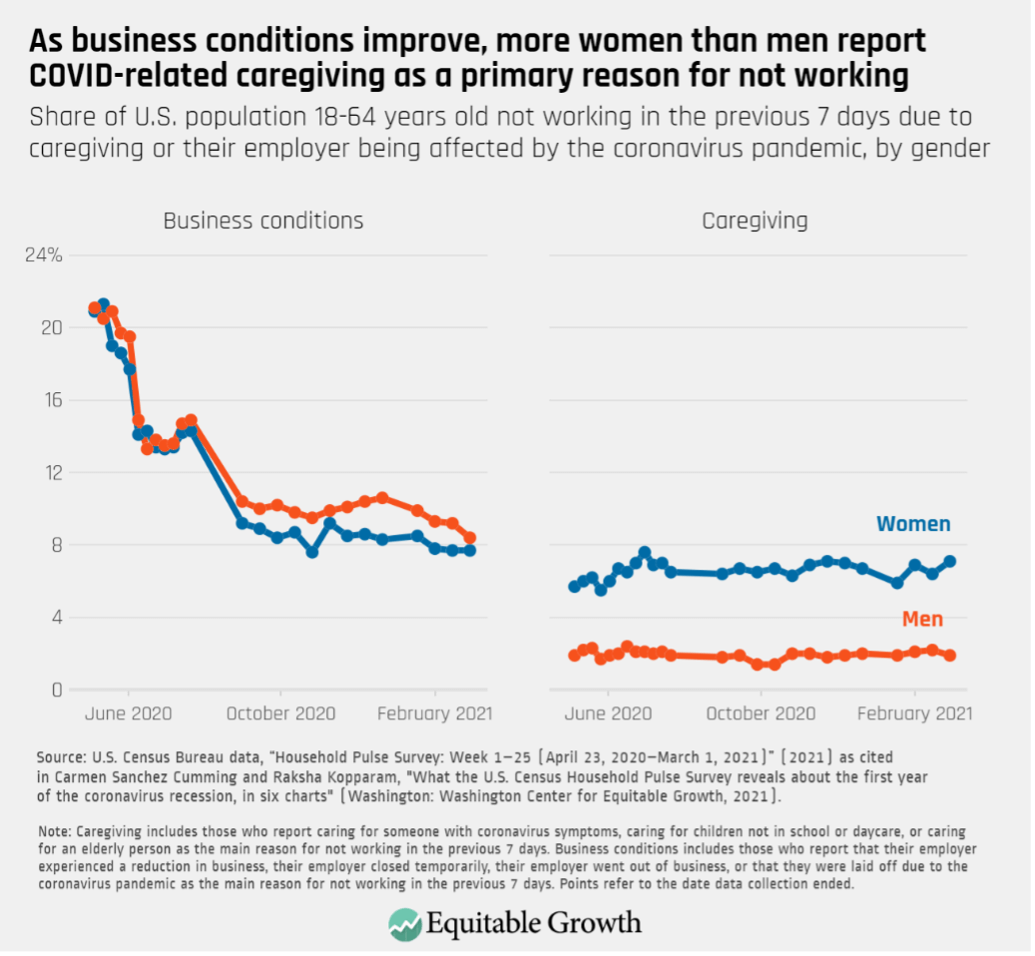

The coronavirus pandemic and recession exacerbated these longstanding caregiving and work-life conflicts for U.S. workers. As the nation emerges from the greatest health, economic, and caregiving crises in a generation, though, policymakers preparing for the post-pandemic economy are proposing investments in U.S. physical and caregiving infrastructure—including paid family and medical leave, child care, and home-based health services. Inequities in the recovery from the coronavirus recession point to the importance of these investments. In March 2021, for instance, U.S. women’s labor force participation rate was 56.1 percent, a 33-year low, and women of color have been hit the hardest.

Meanwhile, emerging research confirms what many families already knew: Caregiving responsibilities are a significant driver of women’s exit from the labor force. Investing in U.S. care infrastructure will help ensure women can reenter, stay, and thrive in workplaces; that work and caregiving responsibilities are more equitably distributed; and that the country is equipped to handle both national crises, such as a new pandemic, and the personal crises that too often leave workers and their families in economic peril.

This factsheet looks at research on—and lessons learned from—state-provided paid family and medical leave programs in the United States. Building on this evidence and these lessons in establishing a national paid leave guarantee would address one of the most pressing deficiencies in the nation’s caregiving infrastructure.

Paid leave programs increase labor force participation, particularly among women

Evidence indicates that under California’s paid leave law, new mothers are estimated to be 18 percentage points more likely to be working a year after the birth of their child. During the second year of their children’s lives, mothers’ work hours increase by 18 percent, and their weeks at work increase by 11 percent, relative to their peers prior to the implementation of the state’s paid parental leave policy.1

Recent research corroborates these findings, indicating that in California, mothers with access to paid leave demonstrate an approximately 20 percent increase in the probability of labor force participation during the year of their child’s birth. This increase remains significant up to 5 years later.2

Research using administrative data in California and New Jersey finds that paid parental leave in both of these states is associated with increased labor force participation for women around the time of birth, and this finding is driven nearly exclusively by the increased labor force attachment of less-educated women.3

Research analyzing women’s labor force participation for different cohorts also suggests those on paid leave have higher employment rates after pregnancy, compared to those who do not have paid leave. Those on paid leave have a participation rate of 82 percent after 10 years—considerably higher than those who quit their job during pregnancy, who have a 64 percent participation rate after 10 years.4

Though much of the public conversation has focused on paid leave to care for a new child, paid leave to care for one’s own serious medical condition and paid leave to care for a noninfant family member with a serious medical condition are also important components of the program. Specifically:

A synthesis of related research suggests that paid medical leave could reduce household income volatility, facilitate reemployment, improve business productivity by reducing presenteeism—that is, the act of attending work while sick—and increase labor supply.5

Research from California finds that following the introduction of California’s paid leave law, the labor force participation of unpaid caregivers increased from 66 percent to 73 percent, in comparison to a smaller increase (68 percent to 70 percent) in other states. Additionally, while the percentage of unpaid caregivers engaged in part-time work fellover this time period in other states, it nearly doubled in California, rising from 10 percent to 19 percent.6

Paid leave to care for a child improves child well-being and strengthens the human capital of the next generation

In studying the mental and physical health outcomes of elementary school students exposed to paid leave in California, researchers find lower rates of attention deficit/hyperactivity disorder, obesity, ear infections, and hearing problems. These benefits are most apparent in children from families with lower socioeconomic status, which is consistent with the theory that paid leave provides additional benefits for those families that previously could not take leave due to access or affordability concerns.7

Following the implementation of paid leave in California, researchers saw a significant reduction in hospital admissions for pediatric abusive head trauma, indicating that paid leave decreases rates of child abuse and maltreatment.8

Paid leave also may allow for more bonding between parents and their child. In fact, state paid leave policies are shown to increase rates of breastfeeding, a parenting activity with a strong, evidence-based link to long- and short-term health benefits for babies.9

Recent work finds that paid family leave also increases the amount of time mothers spend in child care activities, including reading, talking, homework help, and other activities that are important for children’s human capital development.10

One study that examined paid leave in California finds that mothers earn less and are less likely to work under the program, though there are questions about the study’s generalizability. Still, the researchers also find that first-time mothers who took up paid leave in response to the policy change spent more time reading to their children, taking them on outings, and eating breakfast as a family, compared to similar mothers not exposed to the paid leave policy change. If this finding holds, it complements the larger body of work on the human capital benefits of paid leave to care for a new child, and suggests that paid leave should be coupled with additional care infrastructure, such as an effective and affordable child care system, to allow families to both parent intensively and prosper financially.11

Paid leave programs protect workers from health and economic shocks

Family incomes generally dip substantially around the birth of a new child,12 but research shows that the introduction of California’s paid leave program was tied to a 10.2 percent decrease in the risk of families with new children dipping below the poverty threshold.13

Time off to deal with one’s own serious medical condition is associated with better health outcomes. Having access to paid sick leave is associated with a significantly lower risk of mortality across a wide range of conditions, including heart disease and unintentional injuries.14

Administrative data from California and Rhode Island show that state paid leave programs were responsive to the onset of the COVID-19 pandemic, with rates of claims between February 2020 and March 2020 increasing 43 percent in California and 300 percent in Rhode Island.15

Paid leave is an important support for small businesses

While some might argue that guaranteed paid leave for workers creates burdens for businesses, analysis of California administrative data finds no evidence that employee turnover at firms increases or that wage costs rise when paid leave-taking occurs.16

Research on employers in Rhode Island similarly finds limited effects of the state paid leave policy on businesses, with employers noting few significant impacts on business productivity and related metrics.17

Survey research finds that 63 percent of small- to medium-sized employers in New Jersey and New York report that they support or strongly support paid family and medical leave programs.18

In a 2010 survey of 253 California employers on the state’s paid family and medical leave program, a large majority said the law has “no noticeable effect” or a “positive effect” on productivity (88.5 percent), profitability (91 percent), turnover (92.8 percent), and morale (98.6 percent).19

New research shows that the introduction of paid leave in New York both improved employer’s reports of how easy it was to accommodate employee absences and increased rates of leave-taking among employees. In the 3 years following implementation of the program, a majority of businesses support the program, while a small minority—less than 10 percent—say they are opposed.20

Paid leave boosts macroeconomic growth

In concert with other care infrastructure policies, paid leave could help raise the labor force participation rate of U.S. women to be comparable with the rate for women in peer nations, which could increase Gross Domestic Product by as much as 5 percent.21

McKinsey analysts estimate that implementing policies such as paid leave that advance gender equality prior to the pandemic’s end could add $2.4 trillion to U.S. GDP and create near gender parity in the U.S. labor force by 2030.22

Paid leave is a sustainable investment in the vibrancy of our economy

While some critics argue that a federal paid leave program is too expensive, a recent policy analysis concludes that the Biden administration and Congress could enact a new self-financed paid leave program without increasing overall average taxes for workers earning less than $400,000 a year.23

By allowing family members to provide care, paid leave may also result in budgetary savings for government programs. One study finds that California’s paid leave program is associated with an 11 percent decline in nursing home usage among older adults, which is associated with substantial decreases in Medicare and Medicaid spending.24

Conclusion

This factsheet presents some of the research and evidence on paid family and medical leave as it relates to families’ economic security, human capital development, employer experiences, and U.S. economic growth. For more information on specific paid leave provisions or other aspects of the care economy, see Equitable Growth’s other factsheets on paid caregiving leave, paid medical leave, paid leave policy design, and our most recent factsheet on care infrastructure investments more broadly.

The United States is emerging from the greatest health, economic, and caregiving crises in a century. Many policymakers are looking for ways to jumpstart the economy and, recognizing the tie between infrastructure and economic growth, have turned their sights on investments in U.S. physical and care infrastructure.

In March 2021, President Joe Biden proposed the American Jobs Plan and American Families Plan, a multipart proposal that would boost federal spending on the nation’s care and physical infrastructure. (See textbox for details.) Investments of this kind could help the U.S. economy recover from the coronavirus recession and lead toward sustainable, broad-based economic growth in the future.

Care infrastructure includes the policies, resources, and services necessary to help U.S. families meet their caregiving needs. Specifically, care infrastructure describes high-quality, accessible, and affordable child care; paid family and medical leave; and home- and community-based services and support.

This factsheet presents some of the research and evidence on America’s care infrastructure as it relates to families’ caregiving needs, the care workforce, and U.S. economic growth.

The current state of U.S. care infrastructure

Caregiving is an important component of the economy. Research suggests that adequate care infrastructure can promote labor force participation, particularly among women; boost the human capital of care recipients; and support broad-based macroeconomic growth. Yet the evidence also suggests that U.S. care infrastructure is in need of greater investment, and current caregiving policies and resources may not be sufficient for the nation’s caregiving needs. For example:

Child care costs more than in-state public college in 30 states, and more than half of all families live in so-called child care deserts, where the supply of licensed child care slots is insufficient for the number of children in that area. Despite these high prices, child care providers run on razor-thin profit margins, making them particularly vulnerable to changes in macroeconomic trends. Meanwhile, the median wage for a child care worker is only $25,460 per year.25

The U.S. Department of Health and Human Services estimates that today’s seniors will incur an average of $137,800 in future long-term services and supports costs, half of which will be financed out of pocket—an unaffordable amount for many. And while COVID-19 outbreaks were particularly devastating to nursing home residents, waitlists for home- and community-based services through Medicaid waivers remain long. In 2018, more than 800,000 Americans were on such a waitlist—approximately 45 percent of the total population already receiving these services.26

For workers living in the 44 states that do not currently have an active paid family and medical leave system, finding time to focus on caregiving can be a challenge. Only 20 percent of private-sector workers access paid family leave through their employers, and 44 percent of U.S. workers do not even qualify for unpaid leave through the Family and Medical Leave Act, or FMLA.27

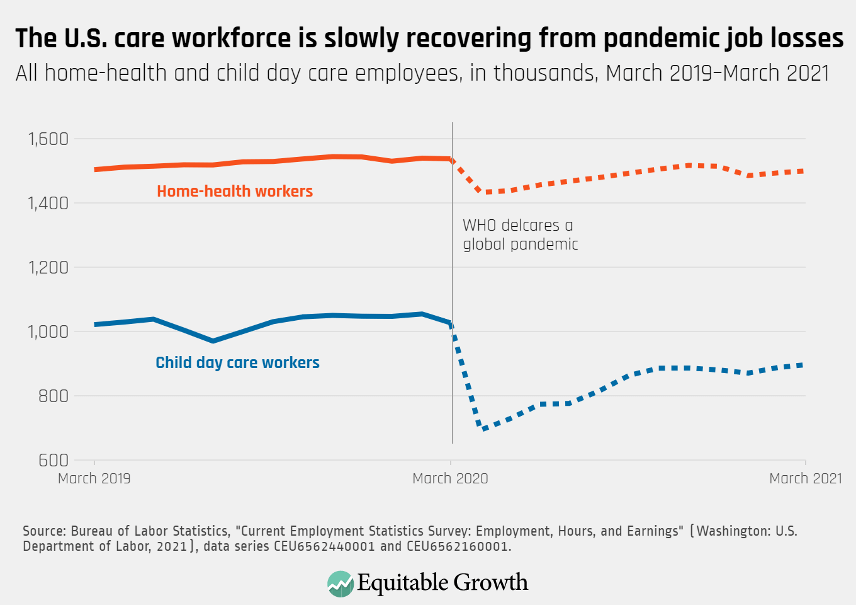

The COVID-19 pandemic and recession exposed preexisting flaws in the nation’s care infrastructure and further weakened an already-fragile system. Employment in the child care and home-health sectors remains depressed, suggesting the care economy could struggle to meet demand as the nation reopens, blunting the economic recovery. (See Figure 1.)

Figure 1

Insufficient care infrastructure constrains the U.S. economy and worker well-being

Paid caregivers earn less than workers in noncare jobs with comparable skills, employment characteristics, and demographics. Research demonstrates that professionals in the caregiving industry receive wages that are 20 percent lower than comparable professionals in other industries. Managers face a similar 14 percent penalty. These penalties translate to higher turnover, lower consumer spending, a smaller tax base, and reduced economic security than if care workers were valued the same as comparable noncare employees.28

Turnover and disruptions in paid caregiving arrangements are burdensome for family caregivers. Recent research finds that the COVID-19 pandemic disrupted more than half of family caregiving arrangements. Family caregivers who face a caregiving disruption demonstrate increased anxiety and depression, and are 13.9 percentage points more likely to also experience permanent job separation or furloughs during the pandemic, compared with noncaregivers.29

Informal caregiving may constrain the economy through lost productivity, wages, and benefits. In data collected by Gallup Inc., 24 percent of family caregivers report that caregiving keeps them from working more, and 30 percent report missing 6 or more days of work in the prior year due to caregiving duties. These productivity losses are estimated to cost the U.S. economy more than $25 billion per year. A 2011 study by the Metlife Mature Market Institute estimates that aggregate cost to the U.S. economy from lost wages, pensions, and Social Security benefits for these family caregivers is nearly $3 trillion.30

Caregiving concerns may have driven millions of women out of the workforce in the COVID-19 pandemic. Research shows that caregiving concerns contributed to more than 2.3 million women exiting the labor force between February 2020 and February 2021. By March 2021, the labor force participation rate for women was 56.1 percent, the lowest rate since May 1988. The gap between men’s and women’s labor force participation widened in communities where school closures exacerbated caregiving needs. Time out of the workforce has long-term implications: Research shows that 13 percent of the gender pay gap can be ascribed to time spent outside of the labor force caring for others.31

Investments in care infrastructure boost economic growth, labor force participation, and worker well-being

Investments in care infrastructure have the potential to create twice as many new jobs as investments in physical infrastructure alone. In the wake of the Great Recession a decade ago, researchers estimate that investment in early childhood development and home-based healthcare could have created 23.5 new jobs per $1 million spent, compared to 11.1 jobs from physical infrastructure investments. Approximately 85 percent of new jobs from both care and physical infrastructure investments would reach workers with lower levels of educational attainment.32 (See Figure 2.)

Figure 2

Spending in the care economy would strengthen women’s employment and reduce the gender employment gap. Ananalysis of care spending in seven OECD countries, including the United States, estimates that an investment in the care economy equal to 2 percent of Gross Domestic Product would raise the employment rate for U.S. women and men by 8.2 percentage points and 4 percentage points, respectively. This would reduce the gender employment divide by 4.2 percentage points.33

Accessible and affordable child care can facilitate labor force participation and support economic growth. Research shows that parents’ labor force participation increases when child care is more affordable and accessible. In one study, a 100-slot increase in the supply of child care in a community is estimated to raise women’s labor force participation for the entire community by 0.3 percentage points. Conversely, every $100 increase in the price of child care is associated with a 3.7 percentage point decrease in that neighborhood’s labor force participation rate among women.34

Meanwhile, high-quality early care and education can lead to long-term improvements in a child’s human capital. Children in high-quality programs demonstrate better education, economic, health, and social outcomes and fewer negative outcomes—such as involvement in the criminal justice system. These high-quality programs can help pay for themselves, generating up to a 13 percent return on investment per-child, per-year.35

Much of the research evidence shows paid leave has a range of positive outcomes for caregivers and care recipients. A growing body of research suggests that paid parental leave can improve a range of childhood outcomes, including infant mortality, low birth weight, preterm birth, breastfeeding rates, and pediatric head trauma, as well as later-in-life outcomes, including lower rates of attention deficit disorder and obesity. Additionally, evidence from California suggests paid caregiving leave can reduce nursing home occupancy among the elderly patients, likely due to enhanced access to family caregivers. And while research on paid medical leave is still comparatively scant, research on related programs indicates such leave can lead to positive health and economic outcomes, as employees have more time and resources to focus on their own well-being.36

Paid leave may also improve labor market outcomes for caregivers. The bulk of the research finds positive associations between paid leave and women’s labor force participation, though the relationship remains nuanced. Evidence from California indicates that under the state’s paid leave law, new mothers are 18 percentage points more likely to be working the year after the birth of their child, compared to mothers without paid leave access. Recent research corroborates these findings, indicating an approximately 20 percent increase in the probability of labor force participation during the year of a child’s birth. This increase remains significant up to 5 years later.37

Patients transitioning from institutions to lower-cost home- and community-based services experience better quality of life and fewer unmet needs. Research shows that patients who transition from institutional care to home-based care express greater life satisfaction (66 percent compared to 83 percent) and fewer unmet care needs (18.3 percent compared to 7.6 percent), compared to their time in institutions. In the same analysis, patients transitioning from nursing home facilities demonstrate 18 percent to 24 percent declines in healthcare spending in their first year in home- and community-based care.38

Home-based care may be particularly valuable for patients without access to family caregivers. Research demonstrates that higher levels of state home-health spending is associated with a significant reduction in the risk of nursing home admission among childless patients.39

Conclusion

Inefficiencies in the nation’s current care infrastructure—paid family and medical leave, child care, and home-based services and supports—constrain economic growth, and leave families and businesses vulnerable to unexpected health and caregiving shocks. Caregiving work is undervalued, and many U.S. workers across the economy face a financial penalty for engaging in care work, which can lead to high turnover and caregiving instability. When care workers are not available or not affordable, family members take on new caregiving responsibilities, exacerbating work-life challenges. If family caregivers cannot resolve these challenges, then many are forced out of the workforce—costing the economy trillions of dollars in lost productivity and compensation.

Alternatively, research suggests that investments in care infrastructure could create significantly more new jobs than investments in physical infrastructure alone, boosting GDP growth and reducing the gender employment divide. Research on the individual components of the care economy likewise support further investment.

Accessible, affordable, and high-quality child care is associated with employment gains for parents in the short term and human capital improvements for children in the long term. Likewise, a preponderance of the evidence on paid leave indicates positive labor market outcomes for caregivers and health and well-being outcomes for care recipients. Finally, patients who transition out of institution-based long-term care report better quality of life, fewer unmet care needs, and lower healthcare costs.

Altogether, the bulk of the research and evidence suggests investments in care infrastructure are a promising tool to boost U.S. economic growth, productivity, and well-being. Policymakers looking to jumpstart the U.S. economic recovery from the coronavirus recession, ensure broad-based future economic growth, and provide much-needed support to U.S. workers and their families must prioritize investment in both physical and care infrastructure.

The United States faces four converging and overlapping challenges—a public health crisis and resulting economic one, a reckoning over structural racism, and the worsening effects of climate change—all of which require substantially greater public investment to overcome. Indeed, a growing body of research finds that declining public investment is damaging to U.S. communities and the overall strength of the economy because older infrastructure depreciates, and economic and social challenges go unaddressed.

The debate over the size and reach of recently proposed investments to restore and transform the U.S. economy is shaped, in part, by the nation’s weak and unequal recovery from the Great Recession more than a decade ago. There is ample evidence that the inadequacy of the recovery legislation enacted in 2009 and in later years contributed to slow employment growth, stagnant wages, and the long-term scarring experienced by many workers during the 2010s despite record-long economic expansion, and that concerns about federal budget deficits and U.S. debt levels are overblown.

Having learned these lessons from the past recession, Congress, in March 2021, passed the $1.9 trillion American Rescue Plan Act, which provided targeted support to those hit hardest by the coronavirus recession. Legislators will soon begin working on the next relief package: the $2.3 trillion American Jobs Plan, which directs large, targeted investments to infrastructure and clean energy, and a third, soon-to-be-announced plan to support families. But already, there are voices in Congress and elsewhere claiming that these measures are too big and far-reaching, that the United States cannot afford these investments, and that they would inappropriately increase the size and scope of government.

To elevate research about the need for increased public investment, the Washington Center for Equitable Growth and the Groundwork Collaborative hosted a virtual event on April 6 titled “Investing in an equitable future.” The webinar, a relaunch of Equitable Growth’s Research on Tap series, featured Cecilia Rouse, the chair of the White House Council of Economic Advisers, who was interviewed by Washington Post reporter Tracy Jan, as well as a discussion on the need for structural changes among a panel of economic and social policy experts—Jhumpa Bhattacharya, vice president of programs and strategy at the Insight Center for Community Economic Development; Joelle Gamble, a special assistant to the president for economic policy on the White House National Economic Council; and Saule Omarova, a Cornell University law professor—that was moderated by Equitable Growth’s Policy Director Amanda Fischer.

The speakers explained that markets and the private sector are ill-equipped on their own to make the kind of investments needed to address long-term challenges and produce strong, broadly shared economic growth. They agreed that there were fundamental structural problems before the pandemic caused by massive income, wealth, and racial inequality, even if topline economic indicators, such as the overall employment numbers, suggested the U.S. economy was strong. The goal of policymakers, they said, should not be to return to the pre-pandemic economy but to build a stronger, more equitable future in which prosperity is broadly shared.

Genuine recovery means transformation, not a return to March 2020

For the short term, Rouse drew a contrast between recovering from the Great Recession and the coronavirus downturn. “The Great Recession was caused by a problem in our financial market,” she said. “It had a true economic cause … This recession was caused by a public health emergency … We had to basically power down the economy … This time, fundamentally we’ll be able to come back more quickly.”

She then pointed to the inequality in the economy that existed despite the fact that the economy was generally healthy before the pandemic. This “inequality baseline … was exacerbated by the pandemic … On many dimensions, this crisis … for many of us, was what I would call an inconvenience … and for others, it’s been completely devastating.”

As she explained, addressing this disparity is key to full economic recovery: “We recognize that there are those who have really been harmed by this pandemic, and we believe that you need some assistance,” she said. “We are committed to keeping in place some of that assistance for the lowest-wage workers, those who are the least advantaged in our society … Improving our safety net is one way in which we as a society will come out of this better.”

Moreover, she said, policies such as the American Jobs Plan are designed “to ensure that investments in infrastructure are widely shared.” The bulk of the jobs created, she said, will be for workers without a college degree, who are disproportionately workers of color. She said that there also needs to be a focus on providing training for workers who do not have the necessary skills.

“We can be investing in the workforce at the same time that we’re investing in our economy and in the economic infrastructure,” she said. “We want to try to have not just any old jobs through these investments but we’re looking for the high-value-added jobs, those jobs that actually will pay well, that provide better economic security for the workers.”

Rouse also called for the federal government to invest more in its statistical agencies in order to improve data collection. She emphasized the importance of being able to increase sample sizes in order to better understand the impact of economic trends and federal programs on people up and down the income ladder and across racial and ethnic groups, including Black Americans, Native Americans, and subgroups of Asian Americans.

Joelle Gamble made clear that there is still much work to be done to achieve economic recovery, despite some bright spots. “We are at an important inflection point,” she said, noting that the number of jobs in the U.S. economy is approximately 4 million below the high point prior to the pandemic, and dramatic disparities continue. There is significantly higher unemployment for people of color, and the wide gap between Black and White unemployment persists.

Pointing to numerous long-term structural problems in the U.S. economy, Gamble said, “We have to think broadly about what it means to actually have an economic recovery. It means we have to think broadly about what it means to invest in infrastructure, and broadly about what communities in which this country has perennially underinvested—people of color, women, tribal communities—need to be able to be a part of ongoing economic growth.”

She then asked, “Was February 2020 actually the baseline we want to get back to? Is that sufficient for saying we have an equitable economy and that we have an equitable recovery? I would say no. There’s been a disconnect for decades between wage growth and productivity growth.”

This recession has the added challenge of being, as Gamble termed it, “a female recession.” During the worst of the downturn, women’s labor force participation rate hit a 30-year low, in part because the jobs that were lost were disproportionately held by women, and many women were forced out of the labor market due to caregiving responsibilities.

She cited what she views as three lessons from the past economic recovery. First, there are significant risks from “going too small” in terms of a fiscal response by the federal government, including scarring effects on those who face prolonged unemployment. Second, equity in a recovery is not guaranteed, and if policymakers do not focus on it, the recovery can exacerbate inequality. This is one reason that there must be active investment in quality, good-paying, union jobs, as well as strong labor standards, including in sectors such as the care economy. Third, to improve U.S. competitiveness, there should be a focus on transformational infrastructure projects, as well as “shovel-ready” ones.

Saule Omarova emphasized the importance of not relying only on large one-time appropriations of federal funds. She said that investments and policies need to be ongoing, and they need to represent structural, institutional change. Amanda Fischer noted, as an example, that Equitable Growth has focused on the need to strengthen automatic stabilizers, such as Unemployment Insurance, to combat a recession by triggering significant increases when data indicate a recession has likely begun and establishing off-trigger mechanisms that ensure increases remain in place as long as they are needed.

Care work is infrastructure

Participants addressed the contention of some opponents of the American Jobs Plan that care work should not be included in the bill because, they claim, it is not “infrastructure,” as currently conceived. “I beg to differ,” Rouse said. “I can’t go to work if I don’t have someone who’s taking care of my parents or my children.” Moreover, she added, “That workforce, which is largely female and women of color, is really poorly paid.” Part of the care work funding, she said, seeks to ensure that they are paid better and have better-quality jobs.

Bhattacharya said that infrastructure is “the things that we need to uphold a healthy, sustainable society and economy … We have traditionally divorced care from the conversation about infrastructure and the conversation about public goods.”

Citing a forthcoming Insight Center report that calculates the rapidly rising costs of child care in California, she blamed costs on overreliance on the private sector. “Child care is enormously expensive,” she said, “because we have no public infrastructure to back it up.”

Bhattacharya contrasted workers with jobs that pay enough to afford these costs with those who do not. “If you’re working a minimum wage job or even a middle-wage job, it is really hard to show up at work and be present and do what you need to do constantly stressing about child care.”

She noted that these workers are disproportionately women of color. “When we’re talking about creating an equitable infrastructure, an equitable economy or society,” she added, “we have to bring care into the conversation and consider it a public good.” Bhattacharya also noted that care work has historically been devalued, largely because it has traditionally been performed by women and people of color. This work has always been underpaid, she added, due to the intersecting challenges of misogyny and structural racism.

Reforming the financial system to steer investments equitably

Omarova focused on the need for greater federal involvement in the financial system to ensure that the benefits of infrastructure and other investments are equitably distributed. “You cannot divorce … the structural imbalances in the financial system from the broad structural imbalances in the economy,” she said. “The two are just two sides of the same coin.”

“We really need to focus more specifically and concretely on how we can change the financial system,” she added, “because the financial system is that key link that connects the big plans President [Joe] Biden … puts out on the one hand and what actually will happen in the years to come. Will those people that we care about the most actually get the benefits of these great plans and great investments? What we need to focus on is the structure of the financial system, those channels that allocate capital to specific uses.”

Omarova described the financial system as a public-private structure, in which the private sector generally makes decisions about the uses of capital while the federal government is supposed to back it up, providing the regulation and discipline when markets need correction, as well as the broader infrastructure of society that enable the system to operate.

“That system was working okay until 40 to 50 years ago, when it started falling apart,” she said. Now, “Wall Street, the financial sector, is not really allocating financial flows … to productive economic enterprise. It doesn’t care all that much about what actual companies and the real economy are getting. Instead, they would rather channel incredible amounts of private capital into speculative trading.”

She continued, “The government, on the other hand, has been gradually and quite dramatically exiting from controlling the background economic conditions … And without that public perspective constantly guiding private markets … our government basically lost its institutional muscle as an economic actor, and now we’re living through the results of it, because private actors … don’t have that view of the economy as a whole … We need public actors … with long time horizons, focused on public benefits and public resources to … channel resources” into areas of public need, such as clean public transit, housing, and a clean environment, particularly in disadvantaged communities.

Gamble amplified this point, noting that public-sector investment complements private-sector investment. Rather than it “crowding out” the private sector, it can “de-risk opportunities” for critical investments by private funds, particularly those representing nonprofit institutions, such as pension funds and university endowments. The public and private sectors, she said, are both critical to U.S. competitiveness.

Omarova called for a National Infrastructure Authority to become part of a “three-legged stool” along with the Federal Reserve and the U.S. Department of the Treasury to manage the process of guiding capital to public purposes. The authority would “step into the financial markets … competing with those types of investors that channel capital away from disadvantaged communities, away from job creation in the United States, toward speculative investments … but do it in a thoughtful, and comprehensive, and programmatic way.”

Now is the time to go big

Bhattacharya perhaps best captured the spirit of the webinar. “Any economy that has such vast stratification of wealth and income … and race and gender is not a healthy economy,” she said. “This is a space where we can start talking about shared prosperity and design an economic structure that allows for shared prosperity … Dream big. Now is the time to do it. If we don’t, we’re just going to be in the same boat 5 years from now, 10 years from now.”

More than 200 scholars call on Congress to support ‘robust and sustained investment’

During the event, Fischer announced that more than 200 prominent U.S. scholars have signed a statement urging Congress to prioritize “robust and sustained investment in physical and care infrastructure along with science and technology” in the infrastructure legislation currently under debate. Emphasizing that “the private sector alone is not capable of making the large-scale investments needed to address the overlapping structural challenges facing the country,” they urged “a clear break from the recent history of declining public investment.”

In addition to the leaders of the effort—Hilary Hoynes of the University of California, Berkeley, Trevon Logan of The Ohio State University, Atif Mian of Princeton University, and William Spriggs of Howard University—the signers included former Federal Reserve Board Vice Chair Alan Blinder of Princeton University, former Secretary of Labor Robert Reich of the University of California, Berkeley, and former Chair of the Council of Economic Advisors and Director of the National Economic Council Laura Tyson of the University of California, Berkeley.

When the COVID-19 pandemic eventually wanes and economic conditions improve, many Americans will be able to safely resume familiar activities that have been curtailed amid the health and economic crises. For many, particularly those who are unemployed, underemployed, or telecommuting, this will mean physically going back to a workplace. But after more than a year of layoffs, school and daycare closures, and new as well as preexisting caregiving responsibilities, many Americans do not have the support they need to return to work.

For one thing, not everyone is sharing in the recovery. While the aggregate data may indicate a strengthening economy, women’s labor force participation is at a 33-year low. Job losses among Black and Latina women—who comprise a significant portion of the care workforce—have been particularly stark. Meanwhile, caregiving concerns due to the pandemic continue to disproportionately keep women from work. (See Figure 1.)

Figure 1

Policymakers looking to jumpstart the U.S. economy are expressing renewed interest in the nation’s infrastructure because economic growth and infrastructure are inherently linked. Spending on infrastructure creates good-paying jobs for workers across the wage spectrum. Roads and bridges help employees travel safely to work and allow producers to ship their goods to customers. Electrical grids keep the lights on, and all the various tubes and servers that power the internet keep office workers connected.

To fully recover from the coronavirus pandemic and recession, however, Congress must also address the care economy in any forthcoming infrastructure legislation. Care infrastructure is just as important as physical infrastructure in boosting the U.S. economy and ensuring strong, stable, and broad-based growth. If there is no one to watch children or to care for a sick relative at home while parents are at work, then workers—especially women workers, who take on the majority of home caregiving responsibilities—will remain trapped in the work-life conflict that has come to exemplify the pandemic economy. Without infrastructure that covers the care economy, roads and bridges will remain unbuilt, workers will continue to be stretched too thin, and the recovery from the coronavirus recession will stall.

The American Rescue Plan makes an important down payment on the care infrastructure needed to reduce the spread of the coronavirus and right the economy. Flexible aid to child care providers will help stabilize a precarious market, and the extension of tax credits to cover COVID-related paid leave ensures that this critical public health tool remains accessible to participating businesses.

Even with the passage of this historic legislation, however, there are longstanding structural deficiencies in the nation’s care economy that require a longer-term fix. Fortunately, history and research tell us that investing in our care infrastructure is not only possible, but also has potential for economic benefits that will last for decades to come.

When care was infrastructure: World War II and the Lanham Act

Including “care” as a type of infrastructure may sound unusual to our modern ears, but it was a concept well-understood in the 1940s. Among women whose husbands were in the U.S. armed forces, labor force participation rates shot up from 15.6 percent in 1940 to 52.5 percent in 1944. In preparing the armed forces and production lines to respond to World War II, Congress also mobilized an army of caregivers to support this wartime realignment of the economy. With fathers off at war and mothers off to the factory line, child care became a matter of national importance.

The public response, according to historian William M. Tuttle Jr.’s review of 1940s child care policy, was a mix of moral panic and uncertainty in the country’s ability to meet this need. In response to these concerns, advocates and organizers engaged in practical, grassroots planning to address the child care crisis, including calls for a national nursery school system. In the following years, as Tuttle Jr. describes, the country embarked on a bold public and private expansion of care infrastructure to support mothers involved in the war effort.

In many respects, the child care system that emerged in the 1940s looked like the patchwork system of today. Most mothers relied on informal caregiving from family members, and private care centers opened across the country, often operated by firms engaged in wartime production seeking to attract new female workers. By 1942, the Children’s Bureau (now under the jurisdiction of the U.S. Department of Health and Human Services) began issuing local grants for Extended School Services, which used communities’ existing infrastructure to provide afternoon care for school-age children.

But the federal government’s boldest action—and the biggest departure from today’s child care system—was a short-lived experiment with universal, federally funded child care centers. Using funds from the Defense Housing and Community Facilities and Services Act of 1940—popularly known as the Lanham Act—the U.S. government funded care centers in more than 650 communities with defense industries across the country.

It is important to note that the Lanham Act was not designed as a child care bill. It was a public works initiative intended to help localities shore up the housing and infrastructure needs of communities engaged in the national defense. The federal government, however, understood that parents could not productively contribute to the war effort if they did not have someone to care for their children. Policymakers recognized that child care is as important as a roof overhead or a road connecting homes to factories and responded accordingly. Families were eligible to send their children to these Lanham Act centers, regardless of income, for a small fee. Adjusting for inflation, the cost to families was less than $11 per day.

Of course, not every child who needed care had access to a Lanham Act center, and centers were only available for a short time, from 1943 to 1946. When soldiers, sailors, and marines returned home from the war, many reclaimed their old jobs and women were pushed out of the workforce—and the perceived need for universal, accessible child care went with them. This perception would prove untrue in the ensuing decades, which were marked by rising labor force participation among women.

Despite the limitations of the program, however, a 2013 study identified both short- and long-term benefits. Using U.S. census data, Arizona State University researcher Chris Herbst found that communities with access to high levels of Lanham center funding were associated with greater labor force participation for women and improved education and employment outcomes for their children in the decades following the war.

The lessons from the U.S. wartime commitment to the care economy are threefold. First, it is politically and economically possible to develop a care infrastructure that supports capital infrastructure. Second, a solid care infrastructure supports short-term labor force gains and long-term human capital developments. And lastly, letting the care infrastructure fade with the crisis—as policymakers did at the end of World War II—only undoes these gains and ensures families remain trapped in a work-life conflict for decades longer than necessary.

Nearly 50 years after the end of the war, historian Tuttle Jr. closed his review of child care policy in the 1940s with this critique: “The tragedy of the Second World War experience is how little carry-over value it had in the decades since 1945, even in the face of the country’s mounting need for child care.”

Policymakers responding to the COVID-19 pandemic and recession have similarly demonstrated necessary support for the care economy and income-support programs in the midst of the crisis. Whether their support carries over to the post-pandemic economy will have important implications for the speed of the economic recovery, as well as the economic security of workers for years to come.

Building the infrastructure of an equitable post-pandemic U.S. economy

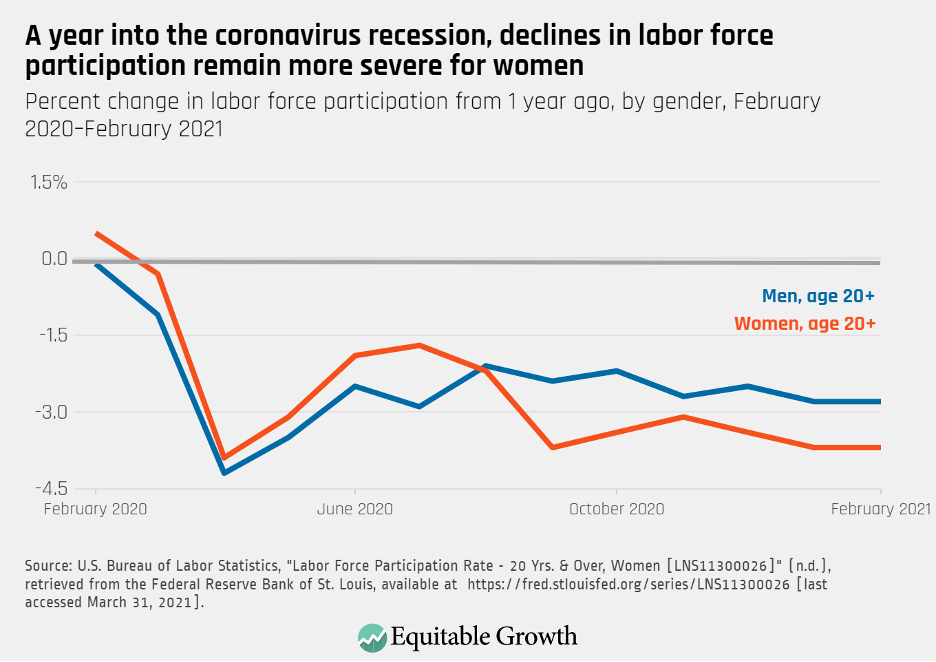

Cracks in the nation’s care infrastructure worsened the economic toll of the coronavirus pandemic and recession, particularly among women. More than 2.3 million women exited the labor force in 2020, and many who remained were less productive and overworked. Even as the economy continues to reopen, women are not rejoining the labor force at the same rate as their male counterparts. Among the civilian workforce, women’s labor force participation in February 2021 remains 3.7 percent below the pre-pandemic rate in February 2020, compared to a 2.8 percent decline for male workers. (See Figure 2.)

Figure 2

Research confirms what many families already know: Caregiving responsibilities are major contributors to women’s exit from the workforce. Though the American Rescue Plan makes a significant step toward improving and modernizing the nation’s care infrastructure, policymakers must do more to facilitate parents’ return to the workforce and to create a permanent network of care supports that help families manage work-life conflicts and prepare the next generation of workers. This means significant and creative investments in the child care marketplace and the long-overdue guarantee of paid family and medical leave for workers with their own health needs or caregiving responsibilities.

Such an investment in our nation’s care economy makes good economic sense. Indeed, investments in care can generate more economic activity and twice as many jobs as investments in physical infrastructure alone. Research shows that accessible and affordable child care can improve parents’ labor force participation. Similarly, the bulk of the research evidence suggests paid family and medical leave has positive effects on labor force participation and workers’ health and economic security. More parents and family members working means higher household incomes, increased consumer spending, and a larger tax base to help pay for these infrastructure investments.

Caregiving plays a significant role in the nation’s economy, as it did during World War II. At its core, the original Lanham Act was an infrastructure bill designed to improve the nation’s internal war-making capacity, but it had far-reaching effects that bolstered the country’s care infrastructure and supported the wartime effort by supporting working parents.

Currently, Congress and the White House are eyeing their own infrastructure package to guide spending for the post-pandemic economy. Infrastructure spending can be a valuable stabilizer for an economy in recession, but it should not be limited to roads and bridges. If child care and paid leave are not readily available when the pandemic subsides, then the U.S. economy could be constrained for years to come.

These policies comprise the infrastructure that supports the human capital powering the rest of our nation’s economic activities. Investing in care infrastructure will provide families and businesses with the tools needed to reduce the spread and impact of the coronavirus and emerge from the current recession to a more healthy, productive, and equitable economy.

According to the latest Employment Situation Summary by the U.S. Bureau of Labor Statistics, the U.S. economy added 916,000 jobs in March, the biggest month-to-month jump since August of last year. Other measures on the health of the U.S. labor market also point to a recovering economy as the public health crisis begins to abate and Congress proactively enacted continued economic relief.

The latest Jobs Day report shows that share of U.S. workers in their prime working years at ages 25 to 54 who currently have a job —also known as the prime-age employment-to-population ratio—climbed from 76.5 percent in February to 76.8 percent in March, and the national unemployment rate fell from 6.2 percent to 6.0 percent. The Jobs report also shows that last month’s gains were not as strong for all groups of workers.

The jobless rate for Asian American workers was the only one to increase last month, climbing from 5.1 percent in February to 6 percent in March. The unemployment rate for Black workers fell from 9.9 percent in February to 9.6 percent in March, but it remained higher than its January level of 9.2 percent and it continues to be the highest among the major racial and ethnic groups. For Latinx workers, the jobless rate stands at 7.9 percent and for White workers at 5.4 percent. (See Figure 1.)

Figure 1

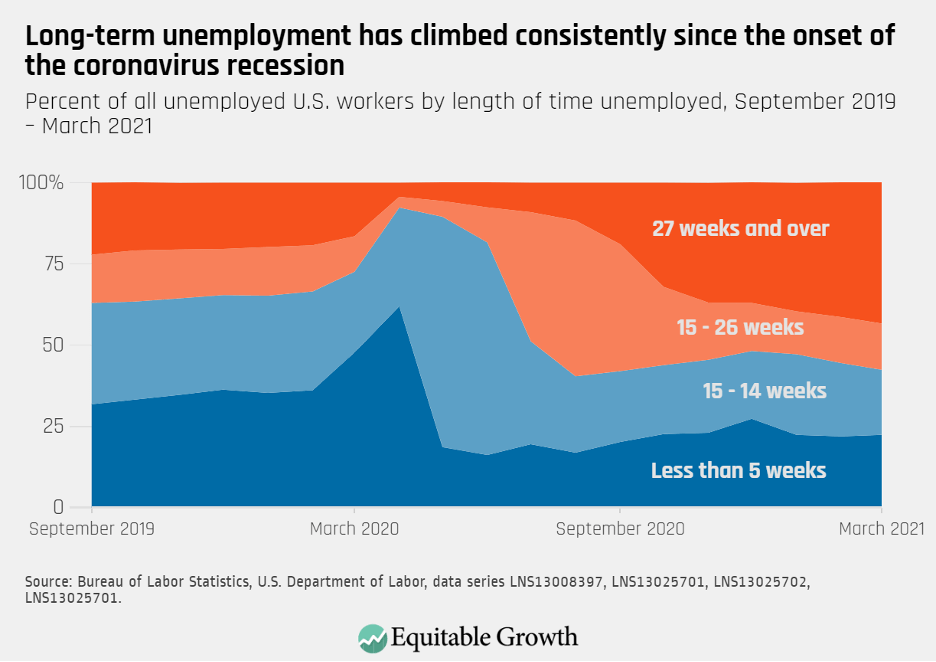

In addition to these uneven gains, the latest Jobs Day report points to another warning sign in the U.S. labor market. Even as the overall jobless rate has declined consistently since reaching a post-Great Depression high of 14.8 percent in April of last year, an increasing number of workers are experiencing long-term unemployment.

In March, the share of jobless workers reporting being out of work for 27 weeks or more reached 43.4 percent, a 1.9 percentage point increase from the previous month and a massive 26.9 percentage point increase with respect to March 2020. In total, 4.2 million workers have been jobless for more than 6 months, the largest number since August 2013. (See Figure 2.)

Figure 2

Long spells of unemployment not only hurt workers’ present earnings but also have economic, social and health effects that can ripple for decades. Research shows that being jobless for long stretches of time is associated with poorer physical and mental health outcomes, leads to a decline in workers’ chances of finding another job, and lower earnings even after re-employment.