Does increasing taxes on businesses reduce private-sector investment? Most economists agree that investment in new projects and technologies is a key driver of economic growth. While the tax code plays less of a role in delivering truewelfare-enhancingeconomicgrowth than many policymakers claim, during tax policy debates the question of which policies are most likely to increase or decrease investment nevertheless looms large over how the tax code ultimately is—or isn’t—reformed.

A new study is helping to shed light on this important question. Princeton University’s Jordan Richmond, along with the U.S. Department of the Treasury’s Lucas Goodman, Adam Isen, and Matthew Smith, examine whether limiting a tax break used by highly indebted U.S. firms affects private investment and corporate debt.

The co-authors specifically investigate what is known as the 163(j) limitation on the deduction for business interest expense, which caps the amount of tax deductions firms can claim based on interest payments they make to banks and other lenders to pay off their debts. This limitation was included in the Tax Cuts and Jobs Act of 2017 and went into effect in 2018.

While the 2017 tax law is mostly—and correctly—known for the huge tax reduction it bestows on high-income businesses and individuals, there are a few provisions that raised taxes on certain businesses in an effort to constrain the bill’s total price-tag. Section 163(j) was one such provision, which was estimated at the time to bring in $253 billion in revenue over 10 years.

In addition to helping offset the cost of the Tax Cuts and Jobs Act—which still increased federal debt by more than $1 trillion—the argument for including 163(j) was that U.S. companies already have a large incentive to invest in new projects via provisions such as bonus depreciation and the research and experimentation credit. Providing a preference to firms that happen to use debt to finance those projects gives them an unfair advantage over firms that choose to finance investment by selling stock or using cash on hand.

There also is a widespread concern that the more highly leveraged, debt-laden firms there are in an economy, the greater the risk of a 2009-style financial crisis, in which defaults cascade across the economy and cause a deep recession.

The new study by Princeton’s Richmond and his co-authors, which was presented at the National Tax Association conference earlier this month, can help policymakers make sense of the conflicting claims. The new study, titled “Tax Policy, Investment, and Firm Financing: Evidence from the U.S. Interest Limitation,” uses actual (but anonymized) tax data and sophisticated methods to compare similar firms that are differentially impacted by the policy. Specifically, they look at firms with similar levels of debt but falling above and below the firm-size threshold for the limitation, being careful to control for other tax changes that affected these firms at the same time.

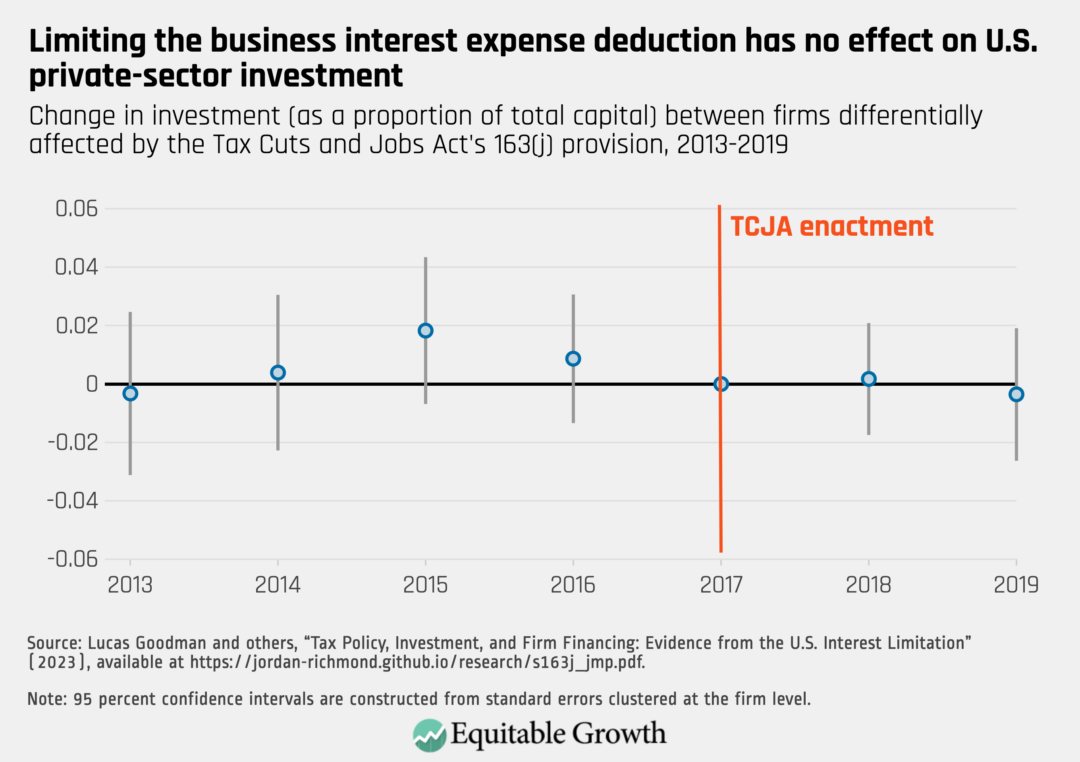

Importantly, the co-authors find that the 163(j) interest limitation did not lead to a reduction in corporate investment by the affected firms. (See Figure 1.)

Figure 1

The co-authors also find that firms do not change their use of debt or cash financing in response to the interest limitation. These results are somewhat surprising, given the classic economic assumption that an increase in the cost of a certain type of capital—in this case, loans and other debt instruments—reduces its use. But the co-authors suggest that the lack of investment changes indicates that firms may face substantial fixed costs to adjusting their capital structures—for example, retiring long-term debt early.

Whatever the mechanism, the study’s findings indicate that limiting the interest deduction is an efficient way to raise substantial revenue. Indeed, these results help argue for doing away with the interest deduction entirely—something that leading economists and legal experts have raised as a potential component of progressive tax reform.

Yet there are three important caveats around this new paper to keep in mind. First, the study excludes utility and finance firms, including private equity funds. The former are excluded because they face rate-of-return regulation, which alters their incentives relative to other similarly debt-demanding firms and thus could bias the results. Finance firms are excluded because many of them supply rather than demand capital, which, again, would muddy the analysis. Although private equity firms themselves are excluded, the sample includes the businesses in which private equity firms invest, which are often loaded up with debt and the corresponding interest deductions.

Second, the study looks at business tax returns from 2013 to 2019, which means it does not cover 2022, when a stricter version of the limitation went into effect. The study does look at 2020 in an appendix but doesn’t fully incorporate those findings into the paper because of the unique circumstances of that year: In addition to the global COVID-19 pandemic, the U.S. Congress temporarily raised the interest deduction limitation in the name of further stimulating the economy.

Third, the paper’s findings diverge from that of two otherpapers that find significant investment reductions as a result of the deduction’s limitation. These two studies, however, use financial statement data to study the impacts of the interest limitation on a smaller set of companies, yielding less precise estimates.

Given the negligible effect overall, the findings of the new study also mean that the interest deduction limitation does not seem to be reducing systemic risk in the economy—firms are still taking out just as much debt as they have in the past. If policymakers want to more narrowly address that problem, other interventions may be more effective, such as higher capital requirements at banks.

Policymakers grappling with what to do with the interest deduction limitation—especially now that businesses and some in Congress are hoping to weaken it as part of an end-of-year tax package—should take note of this new study. Despite industry claims to the contrary, it doesn’t appear that delaying, rescinding, or loosening the limitation will boost investment in any meaningful way—just as implementing it did not hamper investment significantly.

The Washington Center for Equitable Growth today announced the addition of two new members to its board of directors: Sameera Fazili, former deputy assistant to the president and deputy director of the National Economic Council, and Mary Beth Maxwell, executive director of Workshop.

Equitable Growth’s Board of Directors also includes former senior policymakers, business executives, and philanthropic leaders. Fazili and Maxwell will join Steve Daetz, president of the Sandler Foundation; Byron Auguste, CEO and co-founder of Opportunity@Work, and former deputy director of the National Economic Council in the Obama administration; and Ira Fishman, COO and managing director of the NFL Players Association.

“We are thrilled to welcome Sameera and Mary Beth to our Board of Directors,” said Daetz, Equitable Growth’s board chair. “Their extensive experience across government, academia, and advocacy make them well positioned to guide the organization as it provides policymakers with actionable, research-driven ideas and proposals to foster strong, stable, and broadly shared growth.”

One of today’s most heated debates around U.S. income support programs is about work requirements. From the removal of work requirements through the 2021 enhancements to the Child Tax Credit to the imposition of additional ones in the 2023 debt ceiling negotiations, work requirements are now a lightning rod in policy debates. The high stakes of these debates center around a question that is as normative as it is economically important: Should policymakers help people attain adequate living standards if it means they will be less likely to participate in the U.S. labor market?

But what if that tradeoff doesn’t exist? What if income supports themselves facilitate work?

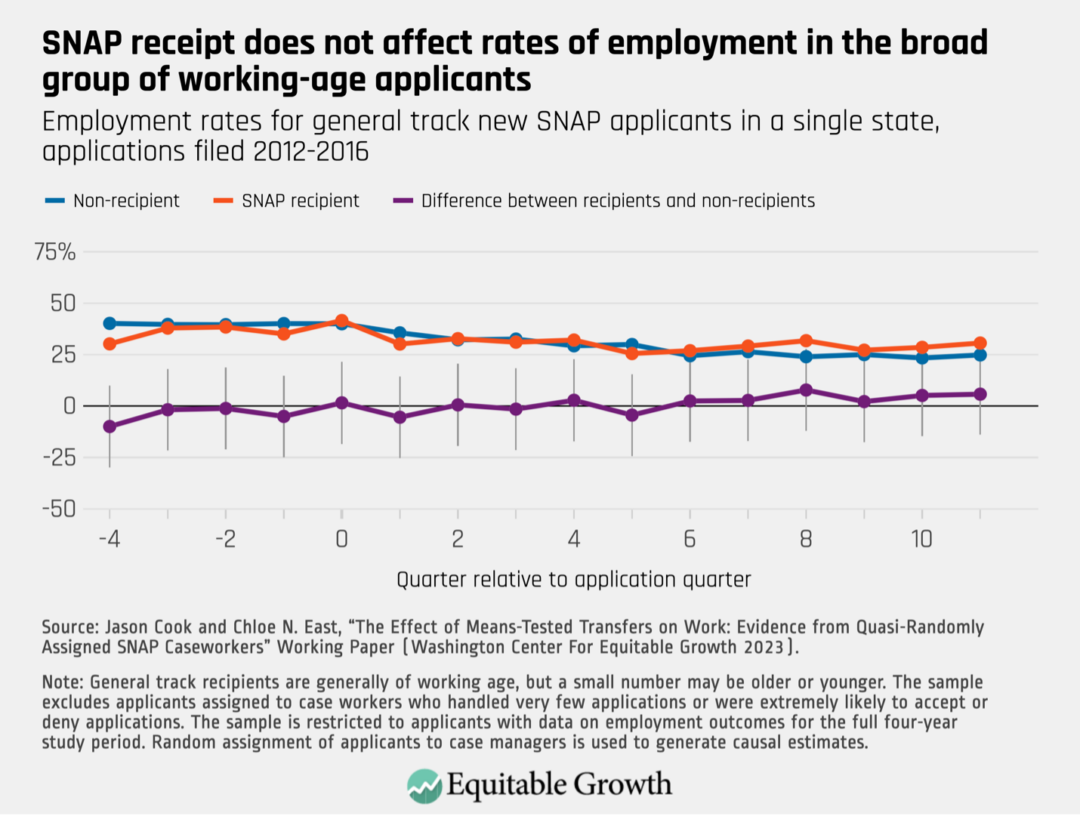

Cook and East take advantage of a natural experiment: Applicants to an unidentified state’s Supplemental Nutrition Assistance Program are randomly assigned a caseworker. Some caseworkers are more likely to facilitate successful applications for SNAP benefits than others because they provide more help with the application process than their peers. Using this random variation, the two researchers compare the labor force outcomes of similar working-aged SNAP applicants, some of whom received benefits because of the caseworker they were assigned and others who did not receive benefits because of the caseworkers they are assigned.

Their results are unlikely to be affected by work requirements because in the state they study most SNAP recipients (96 percent) have disabilities, dependents, are old or young, are already working, are in school, or have another circumstance that exempts them from work requirements.

Their results are striking. Looking across the broad sample, Cook and East find no effect of receiving SNAP benefits on work. Comparing those who received SNAP benefits because of the caseworker they were assigned to those who did not receive it because of the caseworker they were assigned, they see no difference in the likelihood of working following successfully applying for SNAP. This in and of itself is notable, given that proponents of work requirements worry that receiving SNAP benefits will discourage them from working. (See Figure 1.)

Figure 1

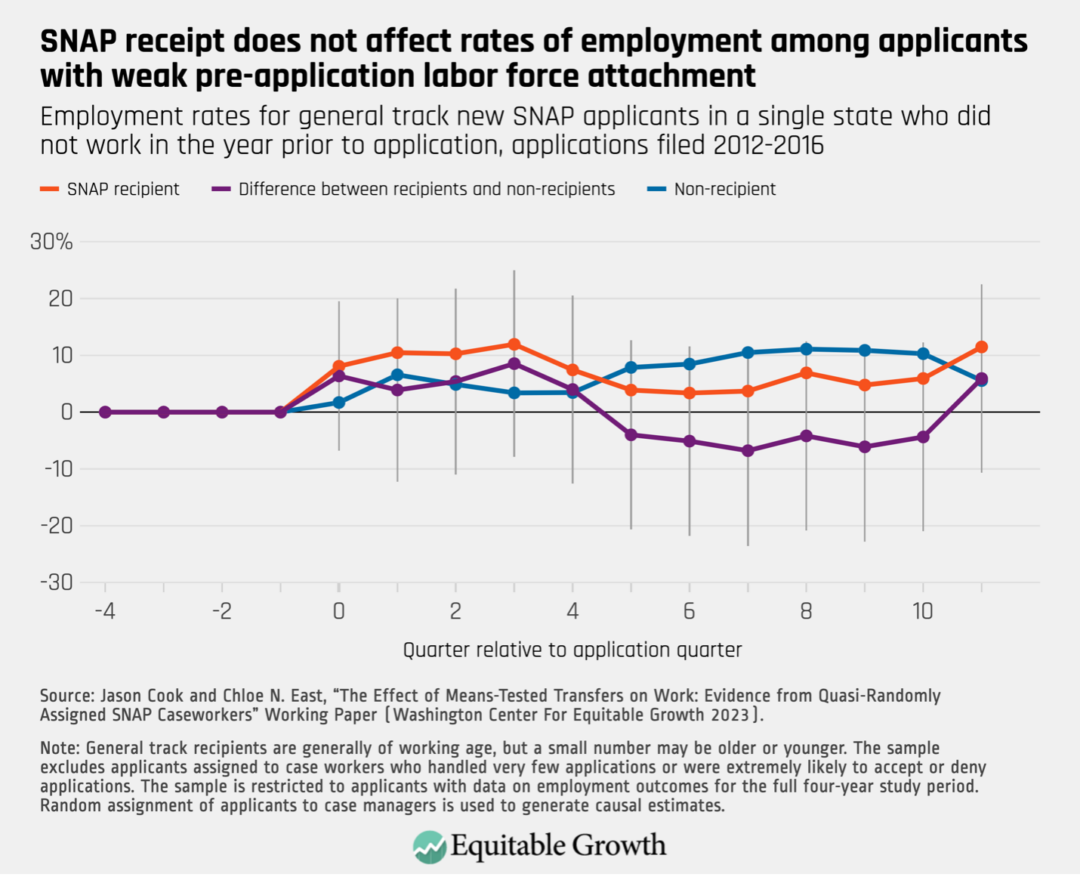

Looking closely at the data, Cook and East noticed something important: Sixty-one percent of their sample members had not worked at all in the year prior to applying for SNAP, 25 percent had worked steadily throughout the year prior, and 14 percent had worked in some of the prior quarters but not others. Looking to the 61 percent of sample members who had not worked at all in the prior to applying for SNAP, it is likely that most of them faced serious and long-lasting barriers to work: They could have young children or family members with disabilities to care for, they themselves could have a disability that makes working challenging or impossible, or they could live in an area where the labor market makes work hard to come by.

So, accordingly, the two researchers break down the sample into applicants who worked in the full year prior to applying for SNAP and applicants who did not work at all in that same year prior to application. Looking at those who had not worked, they find a similar trend to the trend in the full sample—receiving SNAP benefits does not affect one’s likelihood of working in the three years following applying to the program. (See Figure 2.)

Figure 2

This finding makes sense. Given the strong barriers to work probably experienced by this group, they are unlikely to work under any circumstances—receiving SNAP benefits does not change that fact.

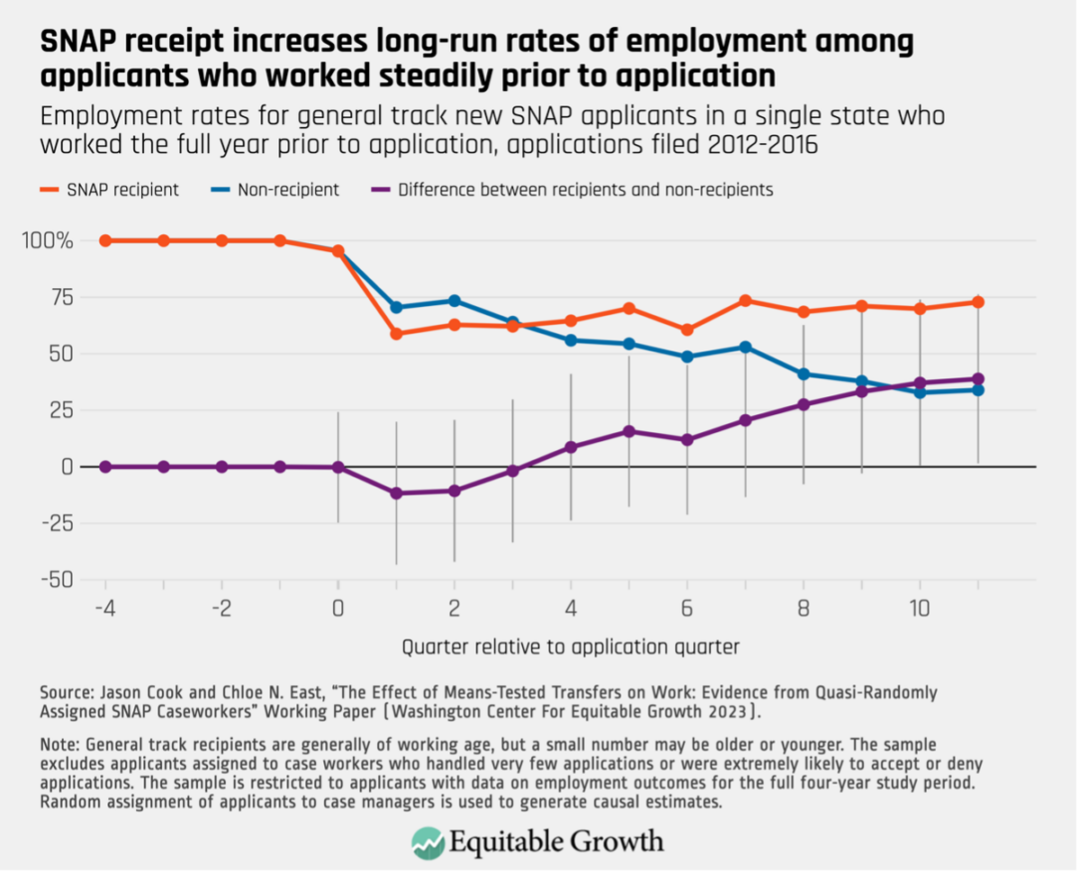

Looking to the quarter of the sample who worked the entire year prior to receiving SNAP benefits, however, we see a different story. Given their recent work history, these applicants are less likely to face the significant barriers to work that are more likely faced by the other portion of the sample. Among these applicants with a year of work history prior to application, there is a dip in their employment rates regardless of whether they received SNAP benefits. This suggests that a change (or anticipated change) in work status may have induced sample members to apply for SNAP in the first place. (See Figure 3.)

Figure 3

Looking further out in Figure 3, however, an interesting trend emerges: One year after application, if the applicants had not received SNAP because of the caseworker they were assigned, then they are actually lesslikely to work than had they instead received SNAP benefits because of the caseworker they were assigned—a trend that becomes more pronounced as time progresses. By the end of the three-year post-application observation period, SNAP recipients are a whopping 34 percentage points more likely to work than those who did not receive SNAP benefits.

What can explain this finding? It appears that SNAP applicants who had been steadily working prior to application use SNAP to cushion the blow of an employment shock, such as a layoff or a change in family or health status that affects their ability to work. When people have resources from SNAP following an employment shock, perhaps they can be more selective in their search for re-employment, leading to a better match with an employer in the long run and a longer tenure on the job. Indeed, evidence from the Unemployment Insurance program shows just this sort of dynamic.

Another possibility is that the income support from the Supplemental Nutrition Assistance Program protects people from experiencing hardships such as eviction, repossessed cars, and damaged credit that make finding and maintaining employment difficult or impossible. The results of Cook and East’s study suggest that regardless of whether income support flows from an unemployment program or a nutrition program, it can have important and beneficial long-run effects on job matching and employment status.

The finding that government expenditures on income support programs without work requirements can lead to long-run gains in employment has important implications for cost benefit analysis. Rather than assuming that the receipt of these benefits lowers employment and associated tax revenue, this research suggests that receiving them actually increases tax revenue over the long run due to increases in employment.

Indeed, the study’s co-authors write, “We find that the effect of SNAP on government revenue due only to changes in labor supply over three years is positive because the longer-run positive effects outweigh the short-term negative ones.” This finding complements a larger body of work on the long-run benefits of the Supplemental Nutrition Assistance Program, from upward intergenerational economic mobility to macroeconomic stabilization.

This paper contributes to a growing body of evidence on the way income support programs interact with work. Already, a substantial body of evidence suggests that work requirements don’t work when policymakers hope to help people attain adequate living standards through labor market participation. This paper joins a few other notable studies suggesting that the income supports themselves—without strings attached—may actually be most effective at achieving this goal.

The U.S. child care market is plagued by a math problem. Families in the United States are stretched thin, dedicating substantial portions of their household budgets to child care expenses. Yet many child care workers find themselves among the lowest earners in the U.S. labor market. And all the while, child care providers are often barely keeping their heads above water with a meager 1 percent profit margin.

How can a service cost so much without its workforce making much money? Simply put, the answer comes down to liquidity constraints faced by both parents and providers, as well as high labor costs.

Families typically incur child care costs at a moment in their working lives when their general living expenses are high but their cash flow, or liquidity, is low. This liquidity constraint limits how parents can tolerate an increase in the cost of child care before turning to other options, such as a family member or reducing their own work hours. Providers are therefore discouraged from raising their prices—and, in turn, wages and profits—too quickly.

This creates a matching liquidity constraint for those child care providers who lack the profit margins to absorb any increases in business costs without a price pass-through to families. Since labor costs—workers’ salaries and benefits—account for between 65 percent and 76 percent of child care providers’ total expenses, they have to squeeze labor costs as low as possible to keep prices tolerable to their customers.

For decades, this liquidity tug-of-war yielded low, stagnant wages in the U.S. child care market. Since the COVID-19 pandemic and recession, however, circumstances exogenous to the child care sector have upended the standard formula.

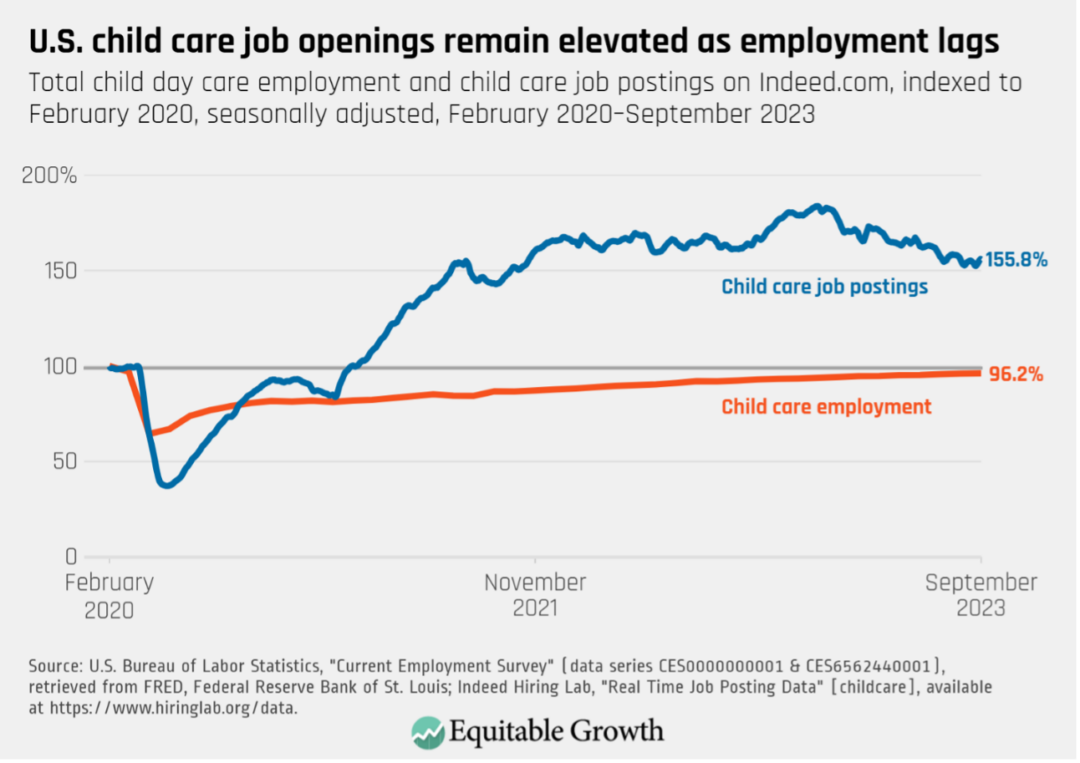

Tightness in the broader U.S. labor market—economic parlance for the excess demand for labor in the economy—resulted in rising wages across the economy. This trend put pressure on child care providers to offer better pay to attract workers back to a child care workforce that is still depressed relative to its pre-pandemic levels. (See Figure 1.)

Figure 1

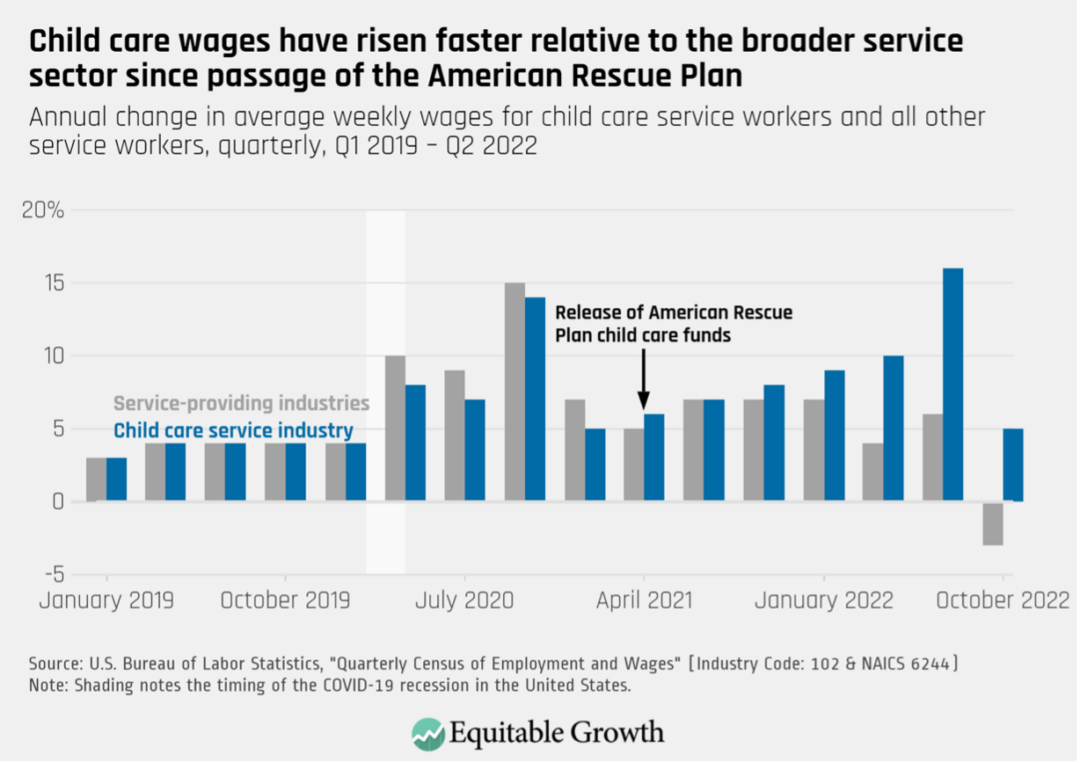

Additionally, in April 2021, the American Rescue Plan injected $39 billion in flexible funding into the child care sector. Providers could use these funds to pay workers’ bonuses or offer raises and higher pay, among other uses, likely alleviating providers’ liquidity constraints in the short term. More research is needed to identify the causal impact the law could have had on the child care sector, but early evidence suggests child care workers experienced accelerating wage increases since the American Rescue Plan funds were released. (See Figure 2.)

Figure 2

The pandemic-induced labor market tightness and the infusion of cash in child care providers’ bank accounts helped facilitate wage increases for child care workers when normal business conditions would not otherwise have done so. Yet despite these recent wage gains for child care workers, the sector may soon return to its pre-pandemic status quo.

The U.S. labor market cooled in the latter half of 2023, reducing the pressure on providers to offer competitive wages. Additionally, a portion of the American Rescue Plan funds have already expired, leaving less money to shore up providers’ books. As such, providers, workers, and parents now face new uncertainties. Will wage gains be rolled back, further straining the already-reduced care workforce? If wages gains are sustained, what will that mean for providers’ business practices and their prices?

The answers to these questions—and thus insight into the future of the U.S. child care system—may lie in a useful analogy: the minimum wage.

Minimum wage changes demonstrate how providers respond to higher labor costs

Changes to the minimum wage typically facilitate pay increases when normal business conditions fail to generate adequate wages. Likewise, child care providers emerging into a post-pandemic world—where the market rate for child care labor has increased and they are now without the cushion of emergency federal funds—face a shock to their labor costs. They therefore may behave similarly to child care providers navigating changes to their business models in the wake of minimum wage increases.

How child care providers respond to changes in the minimum wage is the subject of a recent working paper by economists Jessica H. Brown at the University of South Carolina and Chris M. Herbst at Arizona State University. The authors combine two decades of minimum wage data from the Quarterly Workforce Indicators, market-rate price surveys used to set child care subsidy levels, and Child Care Development Fund data on subsidy receipt and use. Data from the Early Childhood Longitudinal Survey and market research data allow for insights into the parameters of child care quality, while consumer reviews from Yelp allow the authors to understand parents’ satisfaction with their child care providers.

This comprehensive review of the minimum wage and the U.S. child care market yields largely positive news for child care workers. Their pay rose 1.2 percent to 2.3 percent for every 10 percent increase in the minimum wage, with no discernable impact on employment levels, consistent with other sectors. Care quality also improved, with staff turnover decreasing by 1.1 percent and workers making more human capital investments, such as taking courses and earning certifications in early childhood education. Additionally, child care workers had more high-quality interactions with children, as indicated by a 2.4 percent improvement on the Arnett Caregiver Interaction Scale, following a 10 percent minimum wage hike.

As expected from child care’s labor-intensive business model, the higher labor costs resulted in higher prices for families, with center-based market prices increasing between 4.2 percent and 8.1 percent following a 10 percent increase in the minimum wage. This price pass-through was higher than in other businesses affected by the minimum wage, such as fast-food restaurants, where labor costs are a smaller portion of overall business costs. Perhaps due to these price increases, parents’ reviews on Yelp decreased by 0.03 on a 5-point scale for every 10 percent increase in the minimum wage, suggesting that parents saw slightly less bang-for-their-buck under new pricing schemes.

In addition to price increases, child care providers adjusted their class sizes and composition to account for increased labor costs. Center-based programs saw enrollment increase by 5.6 percent and child-to-staff ratios rise 4.7 percent. Centers also accepted 12.2 percent fewer subsidized children, whose subsidies reimburse providers at a lower rate than what they charge unsubsidized families. Home-based providers, in turn, accepted more subsidized students, increasing subsidized enrollment by nearly 28 percent.

Child care providers responses to increasing labor costs after adjustments to the minimum wage offer insight into what might be expected in the months and years following the COVID-19 pandemic and the expiration of the American Rescue Plan child care funds. In the worst-case scenario, providers will respond to these higher costs with layoffs and even closures, eliminating child care slots.

Even if significant layoffs and lost child care slots do not ultimately materialize, providers may still respond to these increased costs by raising prices, adjusting class sizes, and shifting their composition of subsidized and unsubsidized students. In either outcome, child care would become less accessible and affordable for the families who need it most.

Public investment can mitigate unintended consequences while sustaining care workers’ wages

Policymakers have tools at their disposal to minimize these unintended consequences while preserving higher pay for child care workers in the United States. Supply-side grants, similar to the American Rescue Plan, or the emergency supplemental child care funding recently proposed by the White House, can ease providers’ liquidity constraints and reduce the price pass-through of higher labor costs. On the demand side, higher and more streamlined reimbursements for subsidized care—a change currently being contemplated by the U.S. Department of Health and Human Services—would help ensure that subsidized families can access the child care of their choosing.

Higher wages for child care workers are essential for the long-term health of the sector—which has long been plagued by turnover issues and staffing challenges—and consequently essential for the health of the overall U.S. economy. Without affordable and accessible high-quality child care, parents cannot be their full productive selves at work, and some may even exit the labor force if left without viable child care options.

Still, parents’ and providers’ dueling liquidity constraints provide few outlets for higher labor costs beyond rising prices and shifting classroom compositions. With or without higher worker wages, child care costs in the United States will continue to rise. Only robust public investment that treats child care as a public good—akin to the Kindergarten through 12th grade public education system—can sustain workers’ wages and ease providers’ liquidity constraints, all while shielding families from these rising costs.

What does the research say about the impact of unionization and worker strikes in the United States? Aside from well-documented benefits that are associated with unions—from increased job security and better healthcare and retirement benefits to more widespread access to paid leave and higher pay—there are other aspects of unionization and heightened worker power that may be less widely discussed. These benefits extend to union members and nonunion workers, entire communities, and the U.S. economy more broadly.

A few cases in point:

An Equitable Growth-published report by Adam Dean of George Washington University, Jamie McCallum of Middlebury College, and Atheendar Vankataramani of the University of Pennsylvania finds that unions improve worker safety and lower health inequality. They study the spread of COVID-19 in unionized and nonunionized nursing homes in the United States and find that those that were unionized registered better outcomes in terms of COVID-19 transmission and death rates among both residents and workers of nursing homes. The co-authors also find additional health benefits of unions in workplaces with greater percentages of Black workers, helping to mitigate racial health inequity in the United States.

The Economic Policy Institute finds that Black and Hispanic unionized workers have a higher union wage premium—the increase in earnings that accrues to union members, compared to nonunion workers—than their White counterparts, shrinking the racial wage gap. The think tank also finds that union members, especially Black and Hispanic workers, tend to have higher median levels of wealth than nonunion households, reducing racial economic inequality in the United States along a second dimension.

A 2021 study by Paul Frymer of Princeton University and Jacob Grumbach of the University of Washington finds that unions temper racial resentment and boost racial solidarity. The co-authors compare views on policies such as affirmative action and other programs that benefit Black Americans among White workers who are unionized and those who are not, finding higher levels of support among the union set. Further, they find that when White workers gain union membership, their levels of racial resentment fall.

Recent research from Carlos Fernando Avenancio-León at the University of California, San Diego, Alessio Piccolo at Indiana University Bloomington, and Roberto Pinto at Lancaster University shows that unions can improve overall financial stability in the economy by encouraging firms to make less risky borrowing decisions. This further reduces the risk of unemployment for both union workers and the broader workforce. The co-authors also find that firms in states with anti-union right-to-work laws are more prone to riskier borrowing practices, reducing financial stability and increasing the risk of unemployment.

A study from University of Illinois at Urbana-Champaign’s Marc Doussard and Ahmad Gamal suggests that unions are a bulwark against wage theft. The authors find that states with higher rates of union membership are more likely to pass laws against wage theft, which tends to affect low-wage workers, workers of color, women workers, and non-U.S. citizen workers more than their White, citizen, and male peers.

A set of two 2021 working papers by economist David Howell explores the possibility that stagnant wages in the United States could be attributed to decades of public policies that lowered labor standards and weakened worker power rather than to globalization, market conditions, or technological advances. By comparing the United States to peer economies, Howell shows that strong unions and worker power can protect workers from wage inequality and other negative economic trends.

It’s still too early to tell what the results of the past few years of increased labor activity will be, but the early indications from several of the recent strikes—and even in some cases simply threats of strikes—seem to back up what the literature says about unions and worker power. When unions are strong and workers can bargain over wages, benefits, and other working conditions, workers come out on top and the benefits are felt across the U.S. economy.

It can be difficult for the federal government to get its fiscal response to an economic downturn just right. Too much fiscal stimulus can create excess fiscal demand and inflation, while too little fiscal stimulus can lead to a long slog out of a recession that leaves the U.S. economy weak for years. Given that the Goldilocks zone for government intervention to spark an economic recovery can be difficult to hit, how should U.S. policymakers think about the trade-off between overstimulation or understimulation?

The U.S. economy has seen both extremes in the recent past. The recovery from the Great Recession of 2007–2009 was met with insufficient fiscal policy and weak monetary policy that resulted in inflation consistently coming in below the Federal Reserve’s 2 percent target. A pivot to austerity budgeting in 2010 left the economy adrift. Only in the final 4 years of the expansion, ending in early 2020, did workers start to benefit from the recovery.

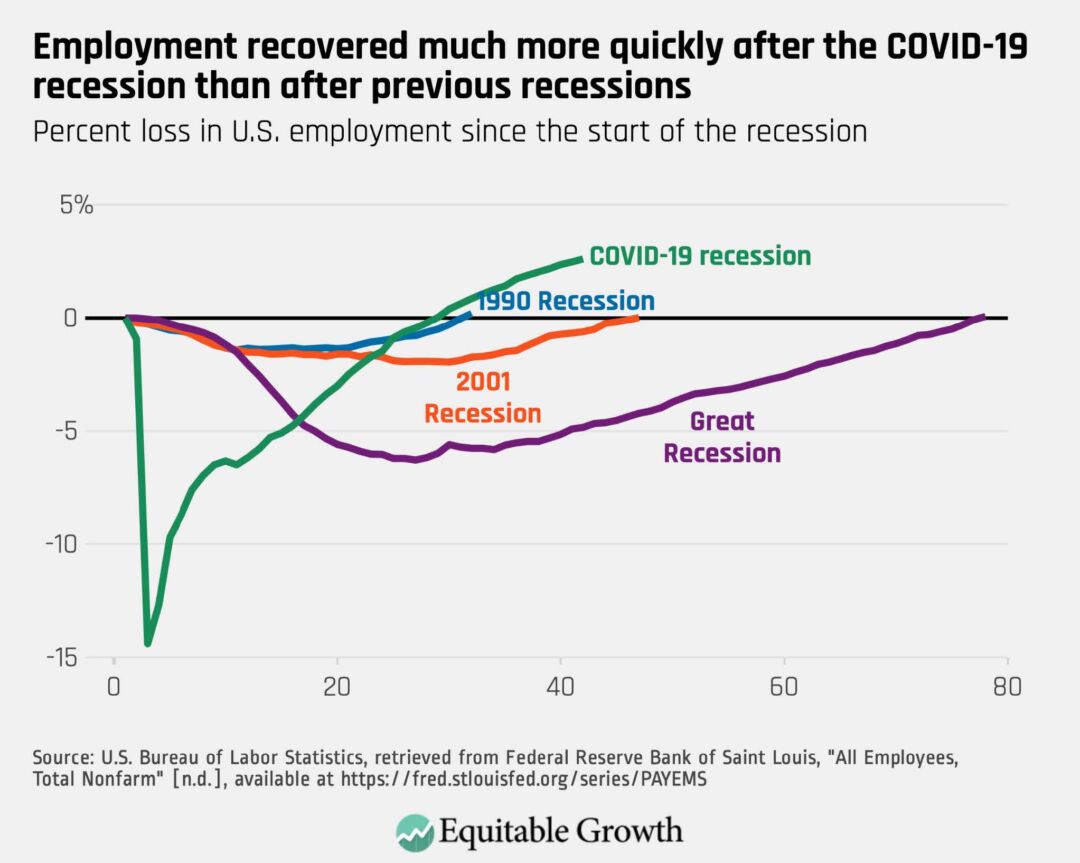

In contrast, the U.S. fiscal policy response to the COVID-19 pandemic-induced recession that began in February 2020 was among the most aggressive in the world, amounting to about 26 percent of total U.S. Gross Domestic Product while adding modestly to supply shock-led inflation. The U.S. recovery from the pandemic recession later that year has been among the strongest in the world, with GDP growth leading our Group of 7 peer nations and a U.S. labor market that bounced back to pre-recession employment levels in record time.

It is a bit too early to know what the full impact of this significant stimulus will be, but recent research suggests that overshooting the recovery, as the U.S. economy did in the pandemic recession, is preferable to the alternative. Earlier this year, Till von Wachter, a University of California, Los Angeles economist and a Washington Center for Equitable Growth grantee, and economist Hannes Schwandt at Northwestern University published a review of their recent work on the ill-effects of graduating into a recession, also known as employment scarring.

By studying new U.S. labor market entrants across a long timespan, the co-authors are able to document the short- and long-run impacts on “unlucky” graduates: those who graduate into a high-unemployment-rate economy. Research shows that these unlucky workers suffer persistent negative impacts on their earnings, but von Wachter and Schwandt additionally show that scarring can harm affected workers across a range of other outcomes.

Their research also demonstrates how persistent these impacts can be. In an earlier paper, for example, they find that for a 3 percent increase in the unemployment rate, new U.S. labor market entrants face an initial reduction in earnings of about 11 percent. Earnings remain depressed 10 years after these workers’ entry into the labor market, with significant cumulative effects.

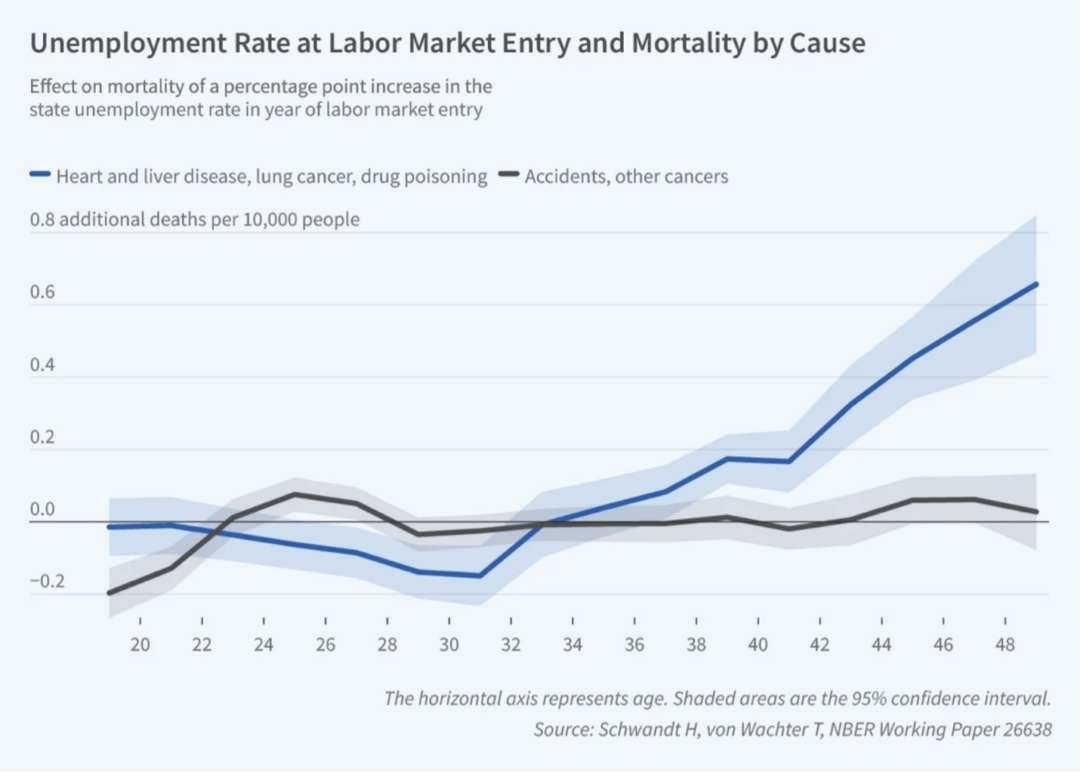

Additionally, in more recent work, von Wachter and Schwandt find that workers who graduate into weak U.S. labor markets also face higher mortality in midlife. They find that those who entered the labor market in 1982—a group who faced an unemployment rate elevated by about 3.9 percentage points—experience a decrease in life expectancy of 6 to 9 months. Moreover, they find this increase in mortality is caused by increases in the incidence of heart disease, liver disease, lung cancer, and drug overdose, suggesting that scarred workers adopt unhealthy lifestyle habits that lead to mortality in middle age. (See Figure 1.)

Figure 1

There are other life-cycle impacts on unlucky graduates. They tend to marry sooner and have children at younger ages, then face higher rates of divorce. In mid-life, they are less likely to be married and tend to have smaller families than their peers. Workers of color are more seriously impacted, suffering both higher initial earnings losses and earlier increases in mortality, compared to White workers.

This and other research in the scarring literature suggests that these consequences may be the result of workers falling behind in skills development during long periods of unemployment. But this human capital decay isn’t just a problem for these workers; reduced human capital stock is also a drag on the overall U.S. economy that reduces potential output in the long run.

This is evident in the evolution of U.S. GDP after the Great Recession. GDP increased at a similar rate after the recession as it did before, but it never made up a significant drop in the level of GDP that had occurred during the recession. In other words, the recession caused a permanent decrease in potential output, called hysteresis by macroeconomists.

The U.S. policy response to the COVID-19 recession caused mildly elevated inflation but has not resulted in a sustained wage-price spiral. Aggressive stimulus did, however, rapidly bring back a tight U.S. labor market. That strong labor market suggests that damage to new labor market entrants—and thus to their future well-being and our overall economic growth—was limited.

Research on worker scarring and macroeconomic hysteresis strongly suggests that it is better to overshoot rather than undershoot on fiscal stimulus when there is uncertainty about the proper size of the fiscal response during downturns. The differing approaches and results of the past two fiscal policy responses to U.S. recessions appear to back that up.

Our new working paper, “Minimum Wage Effects and Monopsony Explanations,” examines the effects of the boldest such policies: the near-doubling of minimum wages—to $15 per hour—in California and New York between 2013 and 2022. We find that these large minimum wage increases both raised pay for workers at the bottom of the earnings ladder and increased employment.

We focus on the lowest-wage workers—those employed in the fast-food industry and teen workers—who are often considered the most vulnerable to losing their jobs when minimum wages rise. Nonetheless, we find positive earnings and positive employment effects for both groups of workers in both states.

Our study uses data from the U.S. Bureau of Labor Statistics and the U.S. Census Bureau to study 47 large and mid-sized counties from these two states. Average wages in these counties span the distribution of average wages in counties across the United States. Our findings therefore contain lessons that are likely to apply to the entire country.

We compare each of these counties to a matched combination of counties that had similar wage and employment trajectories before 2013 and are in the 20 states where the minimum wage has remained at $7.25 since 2009. This state-of-the-art estimating strategy—which we call a stacked county-level synthetic control—is especially suited to studying the effects of a series of repeated policy events, such as annual minimum wage increases, in multiple locations.

We find substantial earnings increases and positive employment impacts. We also find that the employment effects are concentrated largely just below and above the new $15 minimum wage, with no significant effects for those higher up the earnings ladder. This result gives us confidence that our methods are not generating spurious positive employment effects.

Some of the 47 counties we study implemented higher local minimum wages on top of the state-level $15 mandate; a few others had relatively higher wages than almost all other U.S. counties. In both groups, the effects of the state-level $15 minimum wage are likely to be very small, which could lead to biased estimates of the effects of the state-level increases in more typical counties. When we remove these outlier counties from our sample, we find a larger and statistically significant positive effect on employment.

Using simple back-of-the-envelope calculations, we estimate that the higher minimum wage in California and New York resulted in 39,000 more employed fast-food workers.

How it is possible that an increase in the cost of labor could result in greater employment, rather than less? The answer is that the competitive market model of Econ 101 textbooks does not fit the reality of many low-wage labor markets. Indeed, our results are consistent with a growing body of research on what economists call monopsony power.

Monopsonistic employers face less vigorous competition from other employers. They therefore can—and do—pay workers considerably less than if they faced such competition in the labor market. Lower wages, in turn, cause employees to quit their jobs more often and make the jobs less attractive to other workers. As a result, low-wage employers typically have large numbers of unfilled job vacancies.

Higher wages decrease this churn and reduce the number of open positions at any given time—in other words, increasing the number of filled jobs. Our study finds that the higher minimum wages in California and New York did indeed reduce employee quits, demonstrating how minimum wages can increase employment.

We also examined how profit margins at McDonald’s restaurants in the 47 counties reacted to the minimum wage increases. In theory, lower wages allow monopsonistic firms to make higher profits; higher minimum wages would reduce those profits. We find that profit margins at McDonald’s did indeed fall when minimum wages rose—another indication that the new minimum wage policies worked to overcome employer power.

Our study indicates that a $15 minimum wage does not cause negative employment effects in these monopsonistic environments. Rather, it can raise living standards and employment rates among low-wage workers, creating a more equitable U.S. labor market and generating more equitable economic growth.

Many of these benefits also extend to nonunionized workers in what are known as spillover effects, such as nonunion firms offering higher wages or improved working conditions in order to remain competitive with their unionized peers. Similarly, unions have been shown to benefit the broader community in other ways, with increased civic participation and racial solidarity among those who are part of a union.

Yet the direct effect of unions on wages and work equity may actually understate the broader economic benefits of unions. In new research, we show that stronger unions have the unintended benefit of improving overall financial stability in the economy by prompting firms to make less risky borrowing decisions. This is because the collective bargaining process pushes firms to take fewer financial risks, thereby reducing the prospects of firms going bankrupt or undergoing layoffs.

This is an often-overlooked aspect of the role of unions in the economy: Union-induced financial stability can reduce the risk of unemployment for both unionized workers and the broader workforce alike.

In other words, firms care about having financial flexibility, and they make safer borrowing choices if their workforce is unionized and there is a possibility of having to ride out a strike. These safer financial choices help firms endure not only strikes, but also any potential economic adversity, including periods of economic recession—which affect all workers in the economy.

Crucially, our research also reveals that the adoption of so-called right-to-work laws, which weaken the power of unions, lead to significant increases in risky borrowing by firms because of the reduced need for firms to stay financially flexible. We document that firms in states that passed such laws reduced safer long-term borrowing by these firms and instead increased their use of riskier short-term debt—a difference in borrowing patterns that matters in times of economic turmoil.

During the financial crisis in 2007–2008, for example, we find that for each additional percentage of a firm’s total debt that was held long term, firms reduced employment by around one-third of a percent less than otherwise-similar firms, even after accounting for each firm’s total level of borrowing. Other academic work similarly documents that these differences in borrowing patterns mattered both during the Great Recession of 2007–2009 and the Great Depression of the 1930s.

The passage of right-to-work laws might therefore have additional adverse effects for workers, outside of undermining unions, in terms of an increased risk of unemployment—which, during the Great Recession, for instance, would have added to the increase in the unemployment rate by about 0.68 percent. That is equivalent to more than 1 million additional unemployed workers at the end of the Great Recession in June 2009.

As U.S. workers continue to exercise their right to strike and demand livable wages from their employers, these findings on unionization and financial stability can shed light on how firms behave to endure labor actions and protect themselves from the financial impacts of strikes. This could shape how unions approach contract negotiations and define strategies for strikes.

Carefully considering the relationship between unions and financial stability also should be an essential part of the discussion on right-to-work laws and U.S. labor policy more broadly. It is well-known how empowering workers to unionize, bolstering existing unions, and supporting labor organizing and strikes improve outcomes for all workers, but these new findings may well extend those benefits to the stability of the broader U.S. economy—which could be extremely relevant when the next economic downturn hits.

Shayna Strom Washington Center for Equitable Growth

Testimony before the Senate Budget Committee Hearing on “Reducing Inequality, Fueling Growth: How Public Investment Promotes Prosperity for All” September 20, 2023

Introduction

Chairman Whitehouse, Ranking Member Grassley, and members of the committee, thank you for the opportunity to testify today.

I am the President and CEO of the Washington Center for Equitable Growth, a nonprofit research and grantmaking organization dedicated to advancing evidence-backed ideas and policies that promote strong, stable, and broad-based economic growth. Since 2013, Equitable Growth has provided more than $9.6 million in grants to more than 350 academic researchers aiming to understand how economic inequality—in all its forms—affects growth and stability.

Today, I want to make two important points: First, high levels of economic inequality are detrimental not only to the millions of people left behind economically, but they are also detrimental to strong, stable, and broad based economic growth. Second, the economic policies pursued by the federal government since the start of the pandemic—especially significant public investments and income supports—had a notably positive impact on many of those obstacles to growth and have resulted in strong economic outcomes.

Historical Trends in Inequality

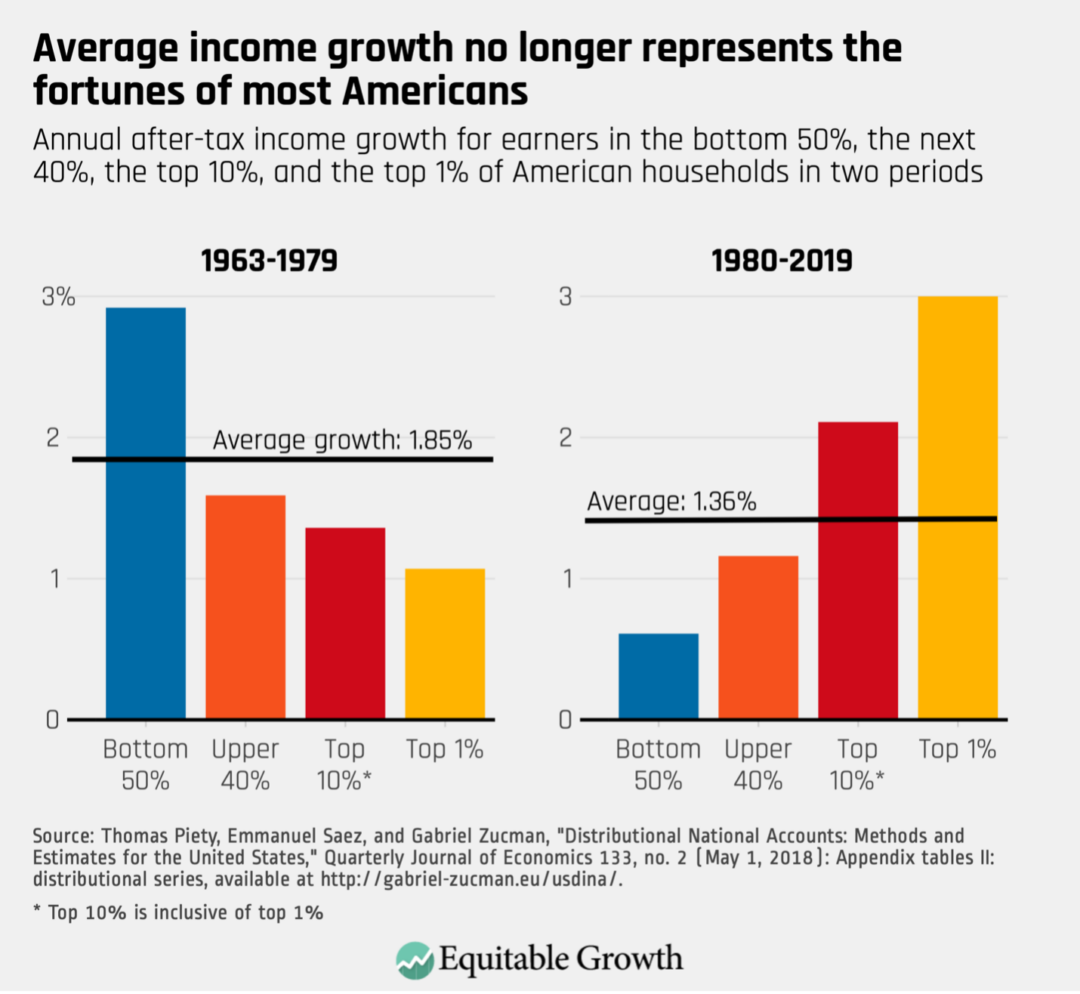

For context, I want to start by discussing historical trends in inequality. According to one estimate, 70 percent of national income in 1979 was earned by the bottom 90 percent of individuals. But by 2019, the share of income earned by that group had fallen by 9 percentage points, to just 61 percent of national income. Nine percentage points of all national income represents an enormous transfer of income from working- and middle-class families to those at the top.

This rapid increase in income inequality had negative impacts on Americans who were left behind. Economists studying generational mobility find that a child born in 1940 had a 90 percent chance to earn more income than their parents by the time they were age 30. But a child born in 1980, whose adult earnings are observed in 2010, had just a 50 percent chance to do the same. Contrary to the ideal of the American Dream, it is now more difficult for a young person to achieve upward mobility in the United States than it is in some high-income European countries.

Inequality Harms Economic Growth

Unfortunately, the fortunes of the rich did not trickle down as promised but simply resulted in stagnant pay for everyone else. Average economic growth was lower in the recent decades when inequality was increasing than it was in recent decades when inequality was falling. (See Figure 1.) This finding has been corroborated by evidence from other historical and international examples. In the international context, researchers associated with the IMF find that lower inequality is positively related to economic growth. The same researchers additionally find that nations with lower inequality enjoy longer spells of growth, leading to more durable and sustainable improvements in incomes.

Figure 1

There are a number of reasons that high levels of inequality are detrimental to strong, stable, and broad-based economic growth and prosperity. I would like to highlight two of them in particular:

1) Marginal Propensity to Consume

Low- and middle-income consumers spend more out of each dollar they earn as compared to higher-income consumers. That additional consumption is good for the economy—it creates demand that encourages businesses to invest in further production. The economist Alan Krueger once estimated that because of increasing inequality between 1979 and 2007, aggregate consumption was about $480 billion lower every year than it would have been if lower-income consumers had grown more prosperous.

This finding undermines the trickle-down argument that is often used to justify high-income tax cuts. The theory behind this argument is that if wealthy individuals can keep more of their income, they will invest it back into the economy, leading to higher supply and more goods produced. But supply requires a buyer, and if low- and middle-income individuals do not see increases in their earnings, they will not increase consumption. Without greater demand, businesses have little reason to expand production, leaving fewer places for the rich to invest.

2) Human Capital

There is an enormous amount of evidence that inequality prevents people who are low-income or who are discriminated against from building and deploying their human capital and that this is a significant drag on economic growth. Human capital includes all the qualities of a person that make them a more valuable contributor in the workforce. It includes education, training, and hands-on experience.

This is one of the reasons that investing in children, including low-income children, is so powerful and can ultimately also boost incomes and grow the economy. Hilary Hoynes, who is on Equitable Growth’s academic Steering Committee, has found that early childhood programs have huge economic returns. SNAP benefits, for example, have $62 dollars in benefit to society for every dollar of federal money spent, if you account for other positive benefits SNAP has, such as lower infant mortality, increased chance of going to college, and increased earnings.

One of the most frequently cited studies in this literature analyzes U.S. patent holders and finds that when children are exposed to innovation at a young age, they are far more likely to file their own patents in later life. But because disadvantaged youth tend to grow up outside innovative areas and without innovative role models, they patent at rates that are much lower than what school test scores would predict. The research team calls these children “lost Einsteins” and finds that the economic impacts of this loss are high. If children from disadvantaged communities and low-income families invented at the same rate as White men of similar aptitude, we would have four times as many inventors in the economy. Innovation is a key driver of economic growth. This failure to cultivate the talent of people in the U.S. economy and match them to jobs where they can effectively apply their skills is costing the U.S. economy an enormous amount of money. By one estimate, it cost the economy $23 trillion over 30 years.

Yet beyond education and training, human capital also includes the ability to deploy these advantages. A good education is not as useful in the labor market, for example, if a person is not healthy enough to work, has to provide full time care for an elderly parent, cannot afford transportation to get to work, or is being discriminated against. One set of researchers finds that closing the gap in patenting rates between men and women, which is at least partly driven by discrimination, would increase GDP by 2.7 percent. Similarly, Federal Reserve Board member Lisa Cook and her co-author Yanyan Yang find that if more women and African Americans were involved in the initial stages of the innovation process, GDP per capita might rise by between 0.6 percent and 4.4 percent. A different team of researchers finds that expanded opportunity for women and disadvantaged groups accounts for at least 20 percent of growth in per capita output between 1960 and 2010. The empirical economics literature makes it clear that more equitable access to opportunity for all Americans, but especially those who have historically been discriminated against due to gender or race, would yield significant economic benefits.

Public Investments Help Roll Back Inequality and Spur Growth

The good news is that we are now starting to see some real progress to reduce inequality and strengthen the economy. Social supports provided to families during the pandemic contributed to keeping them on firmer financial footing, finding higher-quality jobs, and thereby stabilizing and growing the economy. The economic investments that the federal government is currently making will lay foundations for stronger, broad-based growth for decades to come.

I will discuss public investments in people and public investments in new products and industries in turn, before describing the impact of public investment on the economy.

Investments in People

Increasingly, economists are finding that investments in people can be as important as investments in physical infrastructure, such as roads or bridges. By investments in people, I mean the services and supports that make it possible for people to develop their human capital and participate fully in the labor market. This includes programs that help children and adults develop in-demand skills, care infrastructure that allows people to participate fully in the labor market even while they care for others, and income supports that allow people to maintain the standard of living necessary to be able to search for and maintain good employment.

A large body of empirical research documents the ways that investments in people strengthen the economy. For example, programs such as Head Start, paid leave for new parents, and our federal nutrition programs all provide essential support to babies and young children as they develop the human capital they will need as the workers of tomorrow. These programs keep children safe, healthy, and ready to learn. Research on early care and education programs finds that every dollar in spending generates roughly $8.60 in economic benefits in the long term.

Another important area for investment is the care economy, which not only helps care recipients but also helps others remain in the workforce. The literature suggests that when low-cost child care is widely available to parents, the labor force participation of mothers rises. Similarly, when people can access paid family and medical leave, they are more likely to remain in the workforce while they have a young child or when their spouse experiences a health problem.

Similarly, when people’s living standards are too low—when apartments are not heated, bellies are empty, or medical prescriptions are unfilled—people struggle to obtain high-quality jobs and bring their full productive capacity to work. This is where a crucial piece of our public infrastructure, income supports, comes in. By providing the income people need to maintain an adequate standard of living while they search for work, programs such as Unemployment Insurance help people to match with jobs that best use their skills, benefiting workers, employers, and the broader economy. Early evidence from guaranteed income pilots suggests that when families receive a modest guaranteed income, adults increase their work effort. Moreover, evidence from abroad shows that when low-income workers can meet their economic needs at home, they are more productive at work.

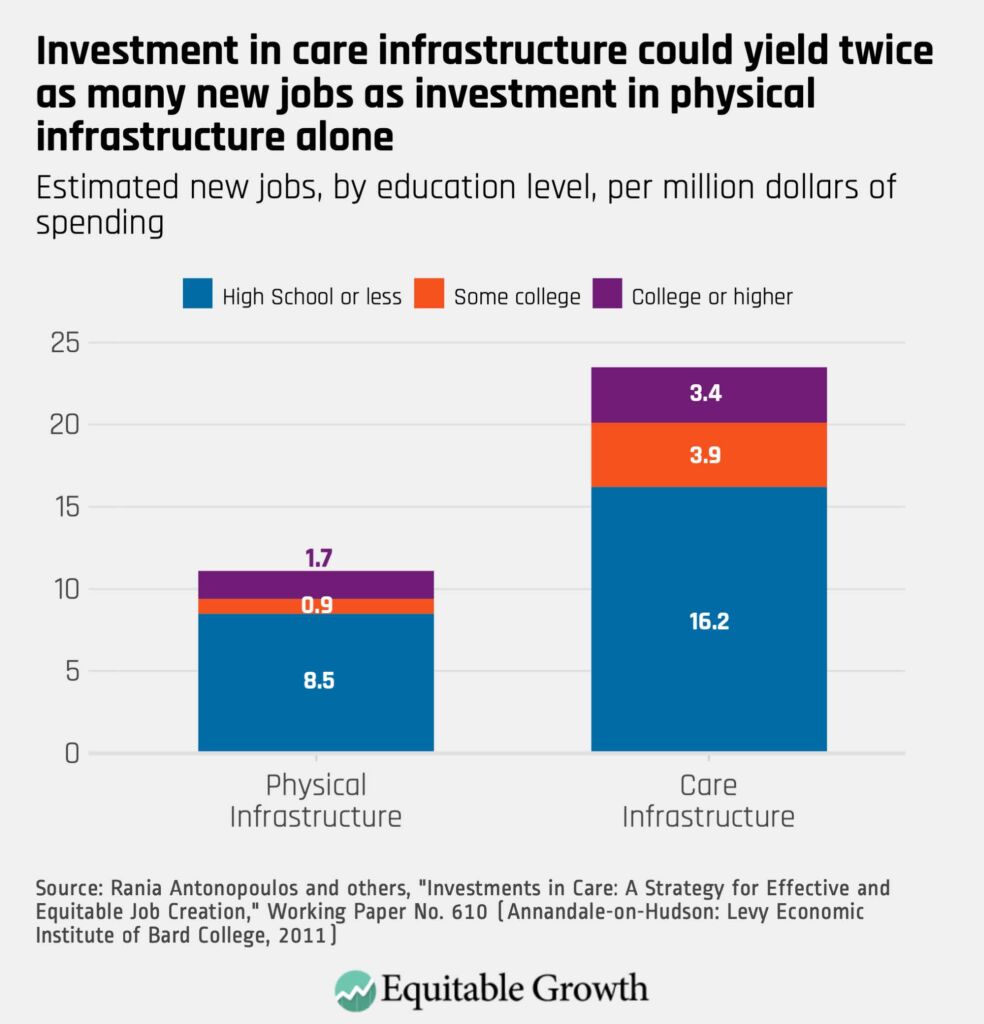

As you would now expect, given the relationship between reducing inequality and growing the economy, sustained government investment in people can create jobs and stabilize the macroeconomy. For example, Rania Antonopoulos and co-authors find that investment in early childhood development and home-based healthcare after the Great Recession could have created 23.5 new jobs per $1 million spent, compared to 11.1 jobs from physical infrastructure investments. (See Figure 2.) Unfortunately, recent Congresses have mostly failed to invest in this area, holding the economy back. To drive down inequality and encourage growth, we have to continue to invest in people.

Figure 2

Investing in New Products and Industries

In addition to passing the Bipartisan Infrastructure Law, the previous Congress also enacted the CHIPS and Science Act and the Inflation Reduction Act, both of which are large public investments meant to spur equitable growth. Although it is too early to know the full impact of these bills, there is evidence that government-led investment in the products and industries of the future can help ensure the economy meets its full productive potential.

One reason for this is that the basic research and development that ultimately leads to technological breakthroughs is hard for the private sector to monetize. Historically, federal research and development investment, especially in the areas of defense and health science, has helped build technologically advanced industries, such as computer hardware and software, aerospace, and pharmaceuticals. In a study from 2019, Aaron Kesselhim and colleagues examined all new drugs approved in the United States from 2008 to 2017—excluding biologics, or those drugs produced from living organisms as opposed to drugs produced through chemical synthesis—and found that publicly supported research in nonprofit institutions or spin-off companies that had their origins in public-funded research made important late-stage intellectual contributions to at least 1 in 4 of these new drugs. By far the most prominent recent example is Operation Warp Speed, the public-private partnership that delivered millions of life-saving doses of COVID-19 vaccines across the country and world. Congress appropriated $18 billion to the successful effort.

In her book, The Entrepreneurial State: Debunking Public vs. Private Sector Myths, University College London economist Mariana Mazzucato highlights the role of government investment at the heart of major technological breakthroughs, noting that Apple and other successful private companies owe much of their value to government-supported research and development. Nearly all the technologies in the iPhone, for example—including GPS navigation, voice recognition, and touchscreen capabilities—were developed through government investments, while Alphabet’s Google search engine algorithm was funded by the National Science Foundation.

Other, non-R&D types of public investment can also be good for equity and growth. It is well understood, for example, that investments in manufacturing played a large role in driving U.S. economic growth in the 20th century. At the moment, investments in semiconductors are especially strategically important. As the pandemic made clear, the private sector alone cannot ensure that supply chains—both for semiconductors and other vital products—are resilient enough to overcome substantial disruptions. The CHIPS and Science Act of 2022 will invest $52.7 billion in U.S.-based semiconductor research, development, manufacturing, and workforce development. Such public investments can also help reduce racial and geographic inequality by funneling public resources to regions and communities that have previously been neglected.

Ultimately, long-term economic growth will be significantly hampered if we do not address the consequences of climate change, which the Office of Management and Budget projects could reduce federal revenues by $2 trillion annually by 2100. But there is ample evidence that the transition to a green economy, if managed correctly, will be good for workers. According to Heidi Garrett-Peltier, for every $1 million invested in renewable energy or energy efficiency, almost three times as many jobs are created than if the same money were invested in fossil fuels. And in a recent paper, E. Mark Curtis of Wake Forest University and Ioana Marinescu of the University of Pennsylvania develop a measure of green jobs—specifically, occupations in the solar and wind energy fields—and find these jobs tend to be in occupations that are about 21 percent higher-paying than the average in other industries—including fossil-fuel extraction—with the pay premium being even greater for green jobs with low educational requirements.

We therefore have reason to expect that the Inflation Reduction Act’s historic investment in green energy will pay long-term dividends in the form of strong, stable, and broadly shared growth. Indeed, according to a recent paper by Costas Arkolakis and Conor Walsh, the IRA is projected to generate around $970 billion of additional GDP as a result of the transition to renewable energy, due largely to cheaper power prices both in the United States and around the world.

Public Investment Has Led to Significant Improvements in the Economy

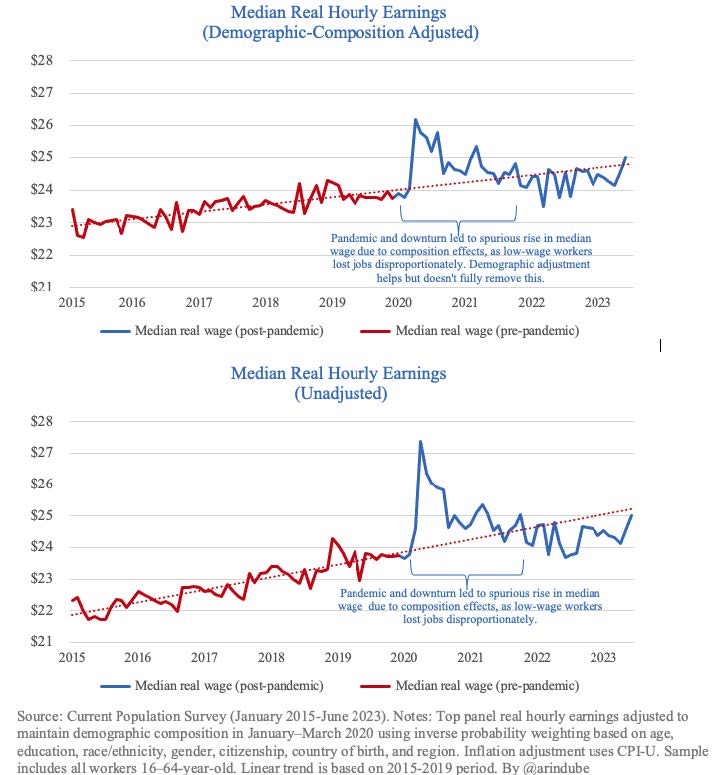

Public investment in the economy is reaping rewards. New metrics published by the U.S. Bureau of Economic Analysis show that between 2019 and 2021, the share of disposable income earned by the bottom half of U.S. households rose nearly 2 full percentage points—the highest level of income for that group since BEA’s first year of data in 2000. And as inequality has come down, the U.S. economy has soared. Employment recovered faster than in any of our previous three recessions, prime-age employment is at a 20-year high, and median real wages, adjusted for inflation and demographic changes, are right back on the upward path they were on in 2019. (See Figures 3 and 4.)

Figure 3

Figure 4

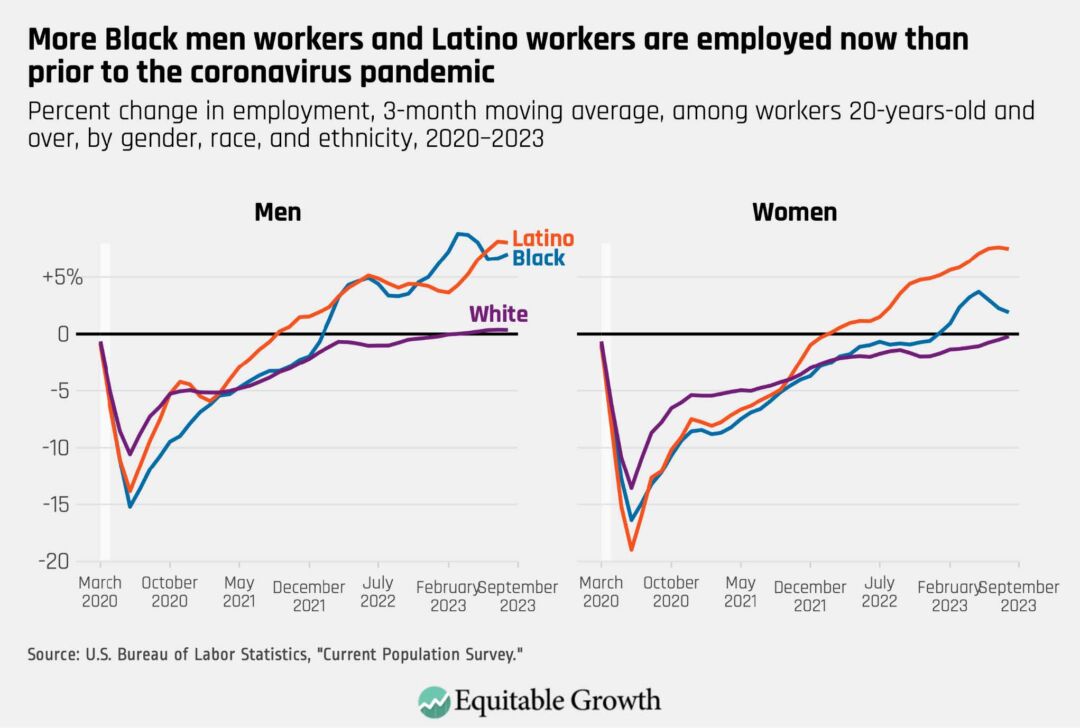

Even groups that have historically been left behind, and were especially hard hit by the pandemic, are benefiting from today’s tight labor market. As of August 2023, Black workers, White male workers, and Latino and Latina workers have surpassed their pre-pandemic employment levels. (See Figure 5.)

Figure 5

While inflation did spike in 2021 and 2022, price growth has now moderated considerably. Since the beginning of this year, annual PCE inflation fell from about 5 percent to about 3 percent. Over the same period, the economy added more than 1.4 million new jobs, and the unemployment rate stayed roughly flat and is still below 4 percent today. At the same time, wages have risen particularly quickly at the bottom of the income spectrum, helping to compress inequality—a stark contrast with recent business cycles in which the rich quickly recovered while low- and middle-class workers experienced persistent labor market dislocation or “scarring.”

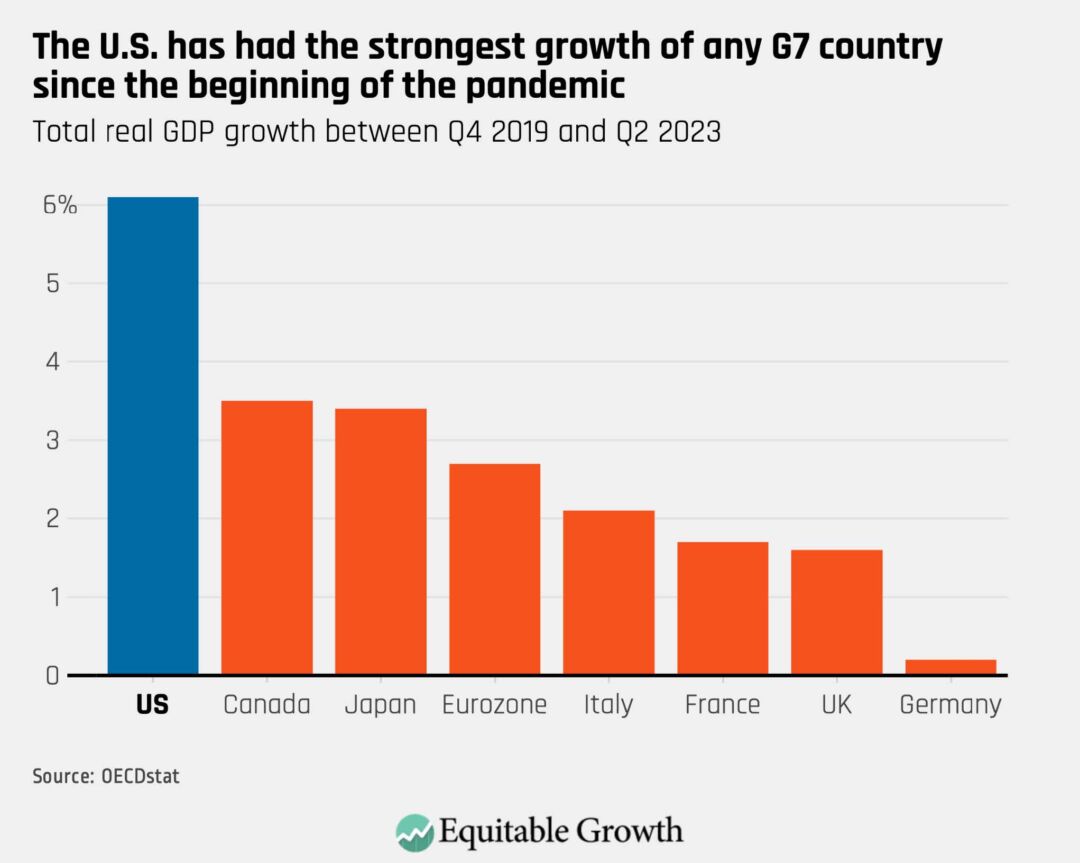

There is now growing evidence that a “soft landing” is within reach. If inflation had primarily been driven by excess demand, bolstered by government spending, economic theory predicts that significant increases in unemployment would have been required to control it. But inflation is now largely declining and the labor market remains tight, which is yet more evidence that the inflation we experienced was not primarily related to excess aggregate demand. Instead, a significant factor in the spike inflation was supply-side shocks sparked by the global pandemic and the war in Ukraine. That is why we saw inflation affect all advanced economics, regardless of their demand side policies. Indeed, the U.S. economy has emerged from the pandemic-induced recession in an enviable global position, with better growth and lower inflation than virtually all of our peers. (See Figure 6.)

Figure 6

I attribute much of this success to the significant investments you and your colleagues made in the American people during and in the aftermath of the pandemic. The expanded Child Tax Credit (CTC), boosted SNAP benefits, and enhanced Unemployment Insurance helped stabilize household finances during the pandemic. Expansion of the CTC, for example, lifted 2.1 million children out of poverty, and last week’s Census Income and Poverty Report showed that child poverty rose sharply after the expiration of the expanded CTC.

These investments were not just good for U.S. families. Economists credit these programs for keeping consumption in the economy afloat during the pandemic. For example, one study found that weekly Unemployment Insurance supplements increased consumption among jobless workers by more than 20 percent, preventing a crash in demand that would have significantly slowed our economy.

Moreover, compare today’s economic recovery to the last one. After the Great Recession, it took about 7 years to get unemployment back to where it had been before the recession began. This time, it took only 2 years, even though unemployment spiked much higher.

Conclusion

As I close, I would like to reiterate my two key takeaway points: First, high levels of economic inequality are detrimental not only to the millions of people left behind economically, but they are also detrimental to strong, stable, and broad based economic growth. Second, the economic policies pursued by the federal government since the start of the pandemic—especially significant public investments and income supports—had a notably positive impact on many of those obstacles to growth and have resulted in strong economic outcomes.

As you consider the 2024 appropriations bills, I would urge you to continue to protect these investments in our economy. Economic inequality in the United States remains elevated, but by investing in people and in our infrastructure, we can achieve strong, stable, and broad-based economic growth that will lift up everyone in the country.

The increasing impact of private equity firms upon large swaths of the U.S. economy in recent decades is drawing more attention to the tax treatment of these firms as they engage in their business of buying, operating, and selling companies. Today, private equity deals account for more than one-third of all merger and acquisition activity in the United States, with total annual deal value in 2021 and 2022 of more than $1 trillion, comprising about 9,000 deals each year.1 These deals benefit from certain tax policies.

Since the 1990s, there have been efforts to remove one key advantage, which is the taxation of private equity profits at a relatively low capital gains rate. Private equity firms have effectively opposed such measures by arguing that the low rate enables them to finance smaller enterprises, which are crucial for the economy, while generating necessary returns for institutional investors such as pension funds.

In this issue brief, we shed light on this debate by laying out the facts about U.S. tax policy and private equity. We begin by providing an overview of the private equity business model and the incentive structure it creates. Broadly, we show how these firms raise funds from institutional investors and high-net-worth individuals, then invest those funds in companies across the U.S. economic landscape, manage them to increase cash flow while they own them, and then sell those companies, usually when individual private equity funds near their usual 10-year lifespan.

We then describe the tax benefits that are relevant to the private equity industry. The most important are:

The taxation of carried interest at the capital gains rate. This means that the primary compensation of general partners (who manage private equity funds) is taxed at 20 percent rather than at higher personal income tax rates.

The tax deductibility of interest paid on debt. This creates tax shields that boost returns.

Private equity firms also benefit from fee waivers, qualified business income deductions, depreciation allowances, real estate benefits, and exemption from the new corporate minimum tax.

In a more speculative discussion, we then explore the possible impacts of these advantages on the investment community, on the companies that private equity firms acquire, and on society more broadly. Ultimately, we present policy recommendations and assess the potential costs and benefits associated with tax reform.

Specifically, although there is a need for more research, we believe it is unlikely that taxing the income of private equity managers at the same level as other professional services—rather than at the capital gains rate—would have major deleterious impacts on the private equity industry or its benefits to the U.S. economy. Policymakers should balance the interests of investors in private equity with the broader public interest and consider the potential positive impacts of tax reform.

We believe it is unlikely that taxing the income of private equity managers at the same level as other professional services—rather than at the capital gains rate—would have major deleterious impacts on the private equity industry or its benefits to the U.S. economy.

The tax advantages wielded by private equity firms bear increased scrutiny because of their implications for business and society. These firms typically generate high returns and contribute to economic growth, but tax benefits can lead to reduced public revenue, widening income inequality, and short-term investment strategies. Thoughtful tax reform could promote equitable access to economic opportunities and enhance positive contributions to the economy and society.

The private equity playbook

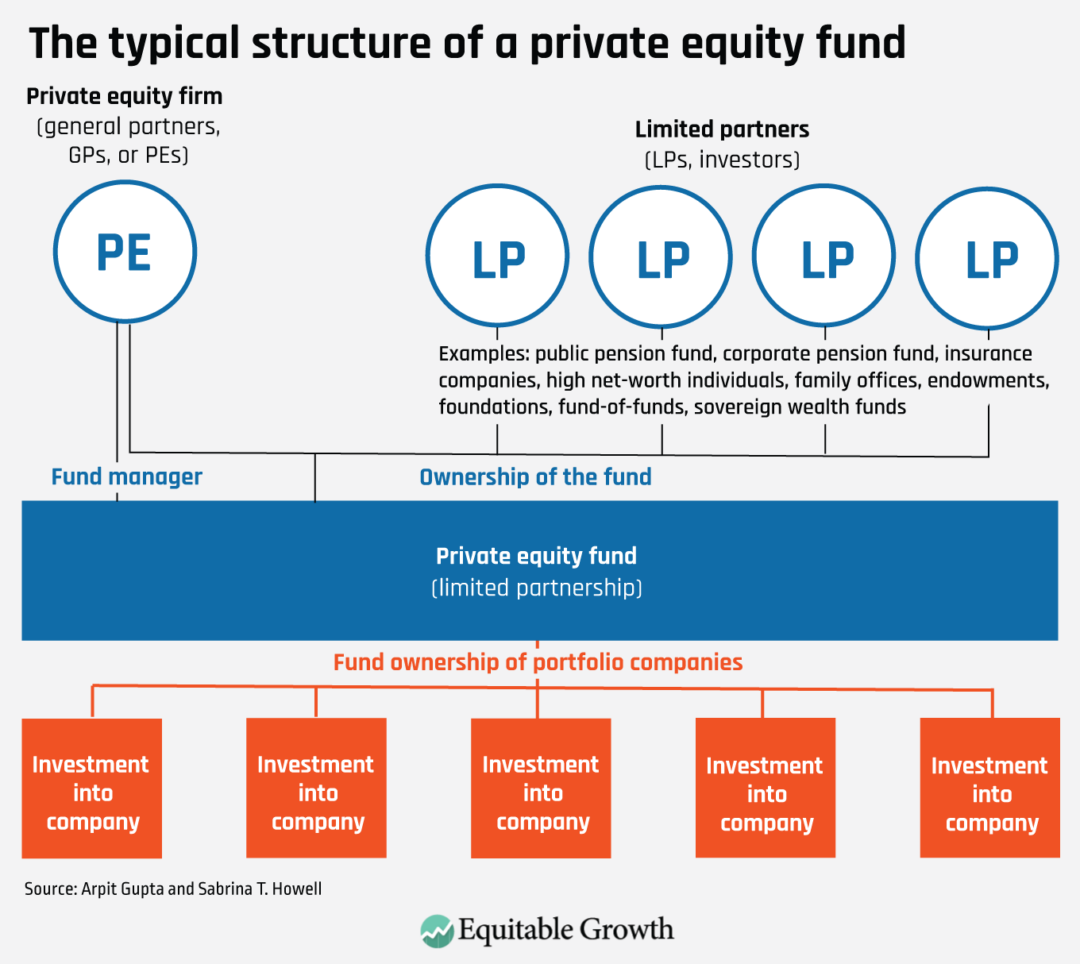

Private equity firms are financial intermediaries who connect investors, known as limited partners, with investment opportunities in the portfolio companies amassed by these firms. The private equity firm uses funds raised from these limited partners to acquire interests in portfolio companies, though the limited partners do not invest directly in the private equity firm. Rather, the managers of the private equity firm, or general partners, set up a fund vehicle, which typically has a 10-year lifespan, in which to invest the limited partners’ money and return profits. (See Figure 1.)

Figure 1

The general partners are responsible for the day-to-day operations of the fund, including the full lifecycle of a portfolio company, from its acquisition to its sale. They identify promising targets, negotiate deals, operate the company for a period, and then sell (or otherwise liquidate) the investment to deliver stock or cash profits to themselves and the limited partners.

The investment in a portfolio company may be a partial stake, a strategy common in the “growth equity” flavor of private equity—a strategy most common among venture capital firms, a subset of the private equity sector of the U.S. financial services industry that we do not include in this analysis. When institutional investors or other financial industry players think of private equity, they expect these firms to be engaged in acquiring full ownership of companies, an approach referred to as a “buyout.”

In this report, we will focus on a central deal type in private equity: the leveraged buyout. In this type of transaction, the target firm is acquired primarily with debt financing, which is placed on the target firm’s balance sheet after its acquisition, and a small portion of equity. A useful framework for conceptualizing how private equity generates value for investors via leveraged buyouts involves three core activities:

Financial engineering

Governance engineering

Operational engineering

Financial engineering refers to the use of debt—and its tax benefits—to increase private equity fund returns.2 The reliance on debt is the first of three concepts we introduce in this section that is crucial to understanding the tax policy discussion in the remainder of this report. The consequence is that private-equity-owned companies tend to have much higher leverage ratios (the proportion of debt relative to equity or overall firm value) than other types of companies. High leverage creates incentives for risk-taking behavior and necessitates the allocation of a substantial portion of the company’s cash flows to cover interest payments on that debt.3

Governance engineering refers to the common strategy of introducing new management and modifying compensation structures for executives—and, in some cases, employees—to ensure that their incentives align with those of the firm’s new ownership.4 These management changes and incentive structures reward strategies that maximize both the short-term recurring profits of heavily debt-laden companies, as well as investments to attract potential purchasers of these portfolio companies within the typical 10-year life of a private equity fund.

Operational engineering refers to those specific strategic changes that the new owners implement at the company. This can include cost-cutting, the sale of real estate assets of the acquired firms, investments in new technology, expansion of productive assets, and the downsizing of unproductive assets.5

Private equity ownership leads to different financial incentives and business strategies than other types of for-profit ownership, such as independent private firms or publicly traded firms. Compared to other for-profit owners, private equity owners have higher-powered incentives to maximize firm value. This is because the general partners are compensated through a call-option-like share of the profits, employ substantial amounts of leverage, usually aim to liquidate investments within a short timeframe, and do not have existing relationships with target firms’ other stakeholders, such as employees, customers, or suppliers.

Since most private equity funds have 10-year time horizons to return cash to investors, assets are typically held for 3–7 years. A modern private equity deal is typically not successful if the business continues as-is because of the objective to produce substantial returns on investment to general and limited partners. This means private equity firms invest with plans to motivate aggressive and short-term value-creation strategies. In contrast, a traditional business owner running the firm as a long-term operation with less leverage may prefer lower but more stable profits.

Understanding the compensation structure of general partners in a private equity firm is the second concept that is crucial for considering tax reforms for private equity. General partners are compensated primarily from the right to a share of profits, usually 20 percent, from increasing the value of portfolio companies between the time of the buyout and an exit, when the company is sold to another firm or taken public. The 20 percent share of profits is called “carried interest.”

General partners and the funds they manage also have other sources of income. First, general partners earn management fees of 1.5 percent to 3 percent of limited partners’ committed capital (usually 2 percent) each year. These fees are earned regardless of performance, and they add up.

Consider a simplified example. If a fund has $1 million in committed capital and a 10-year life with the standard 2 percent annual management fee, the general partners will earn $200,000 (or 20 percent of all the limited partners’ investment) over the life of the fund. This leaves $800,000 to invest. In order to generate a reasonable rate of return on the fund overall net of these high fees, general partners must target high returns on each deal.

In addition, the private equity fund charges the portfolio company two types of fees. The first one is a transaction fee as part of the initial purchase, which is usually about 2 percent of the transaction value. The second one is a monitoring fee, which is typically between 1 percent and 5 percent of a portfolio company’s Earnings Before Interest, Taxes, Depreciation, and Amortization, or EBITDA, a widely used measure of a company’s financial health, with the exact percentage depending on company size. These fees do not serve an obvious incentive alignment purpose and appear to be simply ways for the fund to earn revenue.6

Finally, the third concept that is important because of its connection to tax policy is the use of real estate sales. Private equity owners often sell a portfolio company’s real estate assets shortly after the buyout to generate cash that can be returned to investors. This burdens the target firm with the additional cost of paying rent on their previous real estate assets, which becomes a regular cash outflow in addition to the new interest payment obligations.

One reason that general partners seek to sell real estate is that in many cases, especially for “old economy” firms such as retailers, the real estate is the most valuable part of the business, and by separating it, they can increase the value of the sum of both parts. A second reason is that the sale generates an early cash flow in the deal’s lifecycle, which boosts ultimate returns for the fund under a key metric by which private equity managers are evaluated, the Internal Rate of Return, or IRR, which is used to evaluate the profitability of budget decisions and real estate sales over time.

The impact of private equity ownership on their portfolio firms

A central consideration for policymakers evaluating tax subsidies for private equity investors is the extent to which private equity ownership produces positive or adverse effects on the acquired firms. There is a vast literature in financial economics on this question, most of which examines a particular outcome in a specific industry.

Our interpretation of this literature is that context matters. The incentive structure for investing in specific individual industries and then operating in them determines whether the actions that lead to profits earned by private equity investors are aligned with benefits to the customers, employees, and, in the case of subsidized industries, taxpayers. We expand on this point by briefly summarizing a small part of the literature.

One dimension upon which the literature is largely in agreement is productivity and operational efficiency. This is clear from studies starting with the pioneering work by Steven Neil Kaplan at the University of Chicago’s Booth School of Business,7 and more recently including work by his colleague at Chicago Steven J. Davis and his co-authors.8 This body of research details how private equity ownership has substantial positive effects on these outcomes across a broad range of sectors. This stems, in part, from better management.9 Looking at leveraged buyout acquisitions of publicly traded companies, Harvard University’s Josh Lerner and his co-authors find evidence that innovation at these companies improves post-buyout.10

When it comes to benefits to particular stakeholders such as employees and customers, the evidence is more mixed and is more sector-specific. In the context of global airports, for example, one of the co-authors of this issue brief (Sabrina T. Howell) and her co-authors show that, relative to both government and non-private-equity private ownership, private equity ownership yields large improvements to a private-equity-acquired airport, including more flights, more capacity, more passengers, and better airport amenities.11 They show that some of this reflects superior negotiation, such as extracting more revenue from airlines.

Similarly, in fast-food restaurants, Shai Bernstein at Stanford University and Albert Sheen at Harvard Business School find that private equity ownership causes health score improvements.12 And in grocery stores, Cesare Fracassi at the University of Texas at Austin, Alessandro Previtero at Indiana University, and Harvard Business School’s Sheen show that private equity owners increase product offerings and expand geographically.13

The literature finding positive effects has primarily studied settings with low information frictions (economics and finance parlance for environments in which customers can easily observe product characteristics) and little in the way of government subsidies. In contrast, there is evidence of negative effects on consumers in the contexts of nursing homes and for-profit colleges.14 Tong Liu at the University of Pennsylvania’s Wharton School of Business finds that private equity buyouts lead to large increases in prices and health care spending at hospitals, with no evidence of quality improvements.15

A recent report from the Washington Center for Equitable Growth, the American Antitrust Institute, and the Petris Center at the University of California, Berkeley, finds similar outcomes in the area of physician practices.16

These sectors feature severe information frictions and misaligned incentives, stemming from features such as intensive government subsidies that separate the revenue from the consumer. Quality is also opaque in these settings, leading to benefits from reallocating care resources towards marketing.

More broadly, high-powered incentives to maximize profits may be misaligned with stakeholder interest in sectors that typically have an implicit contract to contribute to some objective of social interest. Michael Ewens at Columbia University and the two co-authors of this issue brief show that private equity buyouts of local newspapers, for instance, lead to fewer reporters and editors and less content about local government—which, they document, is associated with a decline in civic engagement and, in particular, citizen participation in local elections.17 Private equity owners may be more willing to take advantage of new opportunities for value creation that would violate preexisting implicit contracts.

When it comes to employees specifically, there are also nuanced findings. Perhaps the most important body of work in this area is from Stanford University’s Davis and his co-authors John Haltiwanger at the University of Maryland, Kyle Handley at the University of California, San Diego, Ben Lipsius at the University of Michigan, Harvard’s Lerner, and Javier Miranda at Friedrich-Schiller University, and Ron Jarmin at the U.S. Census Bureau.18 These papers merge leveraged buyout data with U.S. Census Bureau data to show that private-equity-owned firms tend to increase employment at productive facilities and during periods of credit expansions but reduce employment at less productive facilities and during credit contractions. Overall, there is, if anything, a small net negative effect on employment.