Employment scarring research suggests benefits for aggressive U.S. fiscal policy in response to recessions

It can be difficult for the federal government to get its fiscal response to an economic downturn just right. Too much fiscal stimulus can create excess fiscal demand and inflation, while too little fiscal stimulus can lead to a long slog out of a recession that leaves the U.S. economy weak for years. Given that the Goldilocks zone for government intervention to spark an economic recovery can be difficult to hit, how should U.S. policymakers think about the trade-off between overstimulation or understimulation?

The U.S. economy has seen both extremes in the recent past. The recovery from the Great Recession of 2007–2009 was met with insufficient fiscal policy and weak monetary policy that resulted in inflation consistently coming in below the Federal Reserve’s 2 percent target. A pivot to austerity budgeting in 2010 left the economy adrift. Only in the final 4 years of the expansion, ending in early 2020, did workers start to benefit from the recovery.

In contrast, the U.S. fiscal policy response to the COVID-19 pandemic-induced recession that began in February 2020 was among the most aggressive in the world, amounting to about 26 percent of total U.S. Gross Domestic Product while adding modestly to supply shock-led inflation. The U.S. recovery from the pandemic recession later that year has been among the strongest in the world, with GDP growth leading our Group of 7 peer nations and a U.S. labor market that bounced back to pre-recession employment levels in record time.

It is a bit too early to know what the full impact of this significant stimulus will be, but recent research suggests that overshooting the recovery, as the U.S. economy did in the pandemic recession, is preferable to the alternative. Earlier this year, Till von Wachter, a University of California, Los Angeles economist and a Washington Center for Equitable Growth grantee, and economist Hannes Schwandt at Northwestern University published a review of their recent work on the ill-effects of graduating into a recession, also known as employment scarring.

By studying new U.S. labor market entrants across a long timespan, the co-authors are able to document the short- and long-run impacts on “unlucky” graduates: those who graduate into a high-unemployment-rate economy. Research shows that these unlucky workers suffer persistent negative impacts on their earnings, but von Wachter and Schwandt additionally show that scarring can harm affected workers across a range of other outcomes.

Their research also demonstrates how persistent these impacts can be. In an earlier paper, for example, they find that for a 3 percent increase in the unemployment rate, new U.S. labor market entrants face an initial reduction in earnings of about 11 percent. Earnings remain depressed 10 years after these workers’ entry into the labor market, with significant cumulative effects.

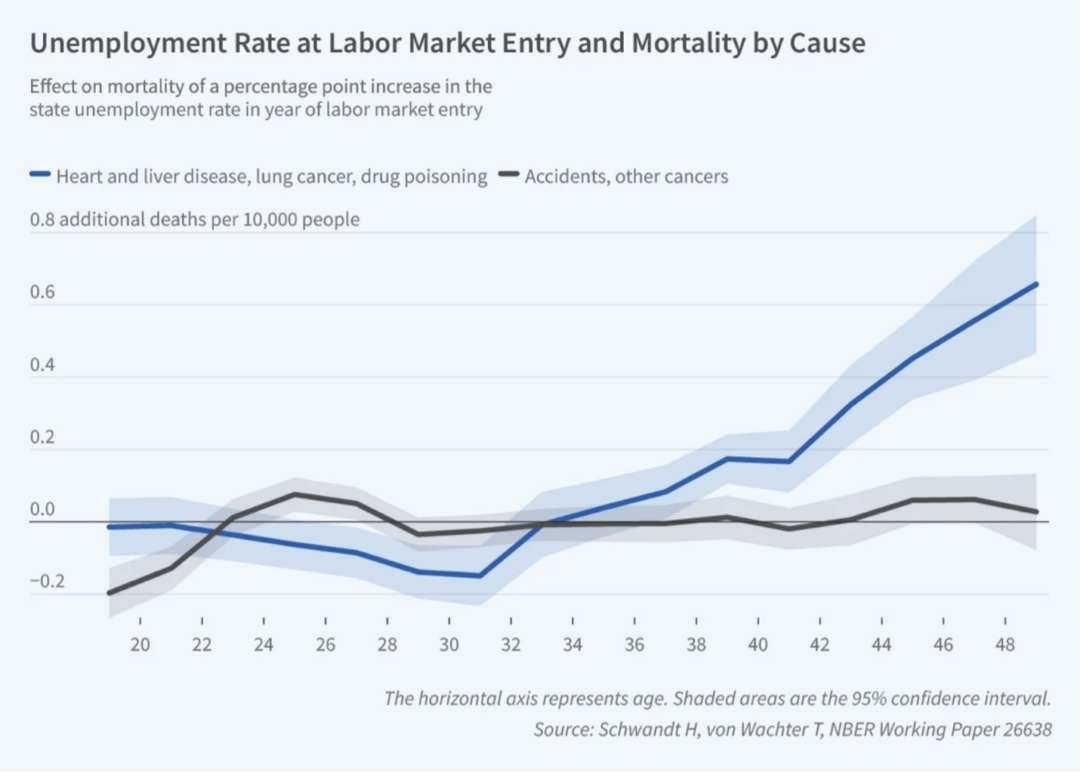

Additionally, in more recent work, von Wachter and Schwandt find that workers who graduate into weak U.S. labor markets also face higher mortality in midlife. They find that those who entered the labor market in 1982—a group who faced an unemployment rate elevated by about 3.9 percentage points—experience a decrease in life expectancy of 6 to 9 months. Moreover, they find this increase in mortality is caused by increases in the incidence of heart disease, liver disease, lung cancer, and drug overdose, suggesting that scarred workers adopt unhealthy lifestyle habits that lead to mortality in middle age. (See Figure 1.)

Figure 1

There are other life-cycle impacts on unlucky graduates. They tend to marry sooner and have children at younger ages, then face higher rates of divorce. In mid-life, they are less likely to be married and tend to have smaller families than their peers. Workers of color are more seriously impacted, suffering both higher initial earnings losses and earlier increases in mortality, compared to White workers.

This and other research in the scarring literature suggests that these consequences may be the result of workers falling behind in skills development during long periods of unemployment. But this human capital decay isn’t just a problem for these workers; reduced human capital stock is also a drag on the overall U.S. economy that reduces potential output in the long run.

This is evident in the evolution of U.S. GDP after the Great Recession. GDP increased at a similar rate after the recession as it did before, but it never made up a significant drop in the level of GDP that had occurred during the recession. In other words, the recession caused a permanent decrease in potential output, called hysteresis by macroeconomists.

post

post

Testimony by Shayna Strom before the Senate Budget Committee

September 20, 2023

post

post

Unemployment insurance reform: a primer

October 31, 2016

The U.S. policy response to the COVID-19 recession caused mildly elevated inflation but has not resulted in a sustained wage-price spiral. Aggressive stimulus did, however, rapidly bring back a tight U.S. labor market. That strong labor market suggests that damage to new labor market entrants—and thus to their future well-being and our overall economic growth—was limited.

Research on worker scarring and macroeconomic hysteresis strongly suggests that it is better to overshoot rather than undershoot on fiscal stimulus when there is uncertainty about the proper size of the fiscal response during downturns. The differing approaches and results of the past two fiscal policy responses to U.S. recessions appear to back that up.