Almost five months into our country’s response to the coronavirus pandemic and ensuing recession, policymakers seem to have lost the urgency that characterized the initial days of dramatic, bipartisan action. In March, four pieces of coronavirus legislation were passed and signed into law. But over the following 2 months, very little in the way of meaningful new policy action occurred. What’s worse, some congressional leaders, squinting at recent data through rose-colored glasses, are ready to declare “mission accomplished,” letting the previous legislation expire and taking no further action.

Are they right? Well, the stock market is now about even for the year. Unemployment declined by 1.4 percentage points in May, and 2.2 percentage points in June. Retail sales increased by 17.7 percent in May, the largest increase ever. And deaths per day from COVID-19, the disease spread by the novel coronavirus, have fallen by half. With the vast majority of stimulus checks delivered and cashed, and with the extra payments for the unemployed set to expire at the end of July, might the U.S. economy be able to muddle along without further support?

The short answer is no—not by a long shot. The few green shoots of improved economic data belie the fact that the health and economic crises are far from over. In fact, we are in danger of sleepwalking into economic depression.

What real-time data are telling us

A careful review of the data reveals gaping wounds caused by the coronavirus pandemic: large declines in market incomes, consumer spending, and employment, all barely propped up by the temporary government stimulus payments. To prevent economic collapse, it is urgent that policymakers take further action. Congress must continue to support unemployed workers’ incomes, send additional stimulus payments to families to keep them financially afloat and increase spending, and give aid to local and state governments so they don’t have to lay off workers.

But, most importantly, policymakers at the state and federal levels must do more to control the spread of the coronavirus, which is now growing at the rate of 70,000 cases a day.

The April Personal Consumption and Income report from the U.S. Bureau of Economic Analysis showed a historic collapse of consumption expenditures, with total spending down 13.6 percent. The decline came despite a record increase in personal income of 10.8 percent, due to the massive inflow of federal stimulus and Unemployment Insurance payments. Without these transfer payments, personal income would have declined 6.3 percent in April and spending would have collapsed even further. For every dollar of stimulus, households increased spending by 25 cents to 35 cents, according to recent estimates, while previous research shows that every dollar of Unemployment Insurance benefits leads to 27 cents of spending.

Thanks in large part to pandemic-related income support, spending recovered somewhat in May, rising 8.2 percent, but it is still down 9.8 percent from the same period in 2019. The most recent official data, the June Retail Sales report, shows that spending on retail goods has largely recovered to its level from last year, while spending on restaurants remain depressed, down 26 percent from its period last year.

While government data give the most accurate picture of the aggregate economic situation, alternative real-time data are crucially important in understanding the scale of the economic crisis and determining the appropriate government response. In a recent paper, I use real-time payment data from Earnest Research, a company that analyzes spending data from credit and debit cards, to study the latest on how consumer spending is responding to the pandemic.

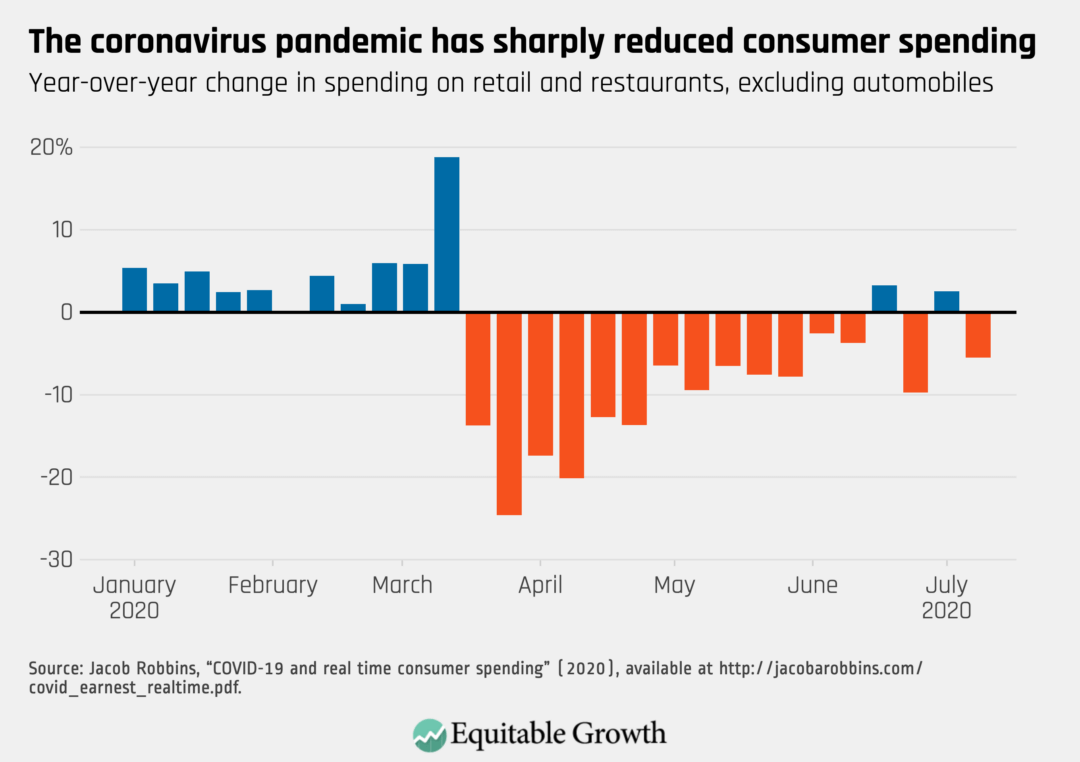

My analysis based on these data examines measures of real-time retail and restaurant spending growth, comparing weeks in 2020 with the corresponding weeks in 2019. The higher-frequency data show that the spending drop came at the end of March and beginning of April, followed by a partial recovery at the end of April. The revival stalled somewhat in May, but continued again in June, with spending in some weeks actually above 2019 levels. In July, however, there are initial signs that with Covid-19 cases spiking again, spending is declining, with retail spending down 7 percent for the week ending July 15. (See Figure 1.)

Figure 1

Restaurant spending saw a sharper decline and slower recovery: As of July 15, it was still down more than 15 percent. Aggregate service spending saw the largest decline in spending, more than 50 percent, and was still down more than 40 percent as of July 15.

The decline in consumer demand raises the specter that even if businesses are able to reopen after lockdowns end, there will not be enough demand to sustain them. A recent survey of small business owners found their biggest concern is that sales will not be high enough to justify their reopening. Layoffs—initially concentrated in sectors directly affected by the pandemic, such as restaurants and hotels—have metastasized to white-collar sectors, such as professional services, finance, and real estate.

Unemployment remains at a staggering level, with the latest jobs report showing 18 million Americans unemployed. The unemployment rate in June 2020, 11.1 percent, is the highest it’s been since the Great Depression in the 1930s, except for the previous two months. The good news in the report was that this elevated level is down 3.6 percentage points from April, driven mainly by workers who were on temporary layoffs being recalled to their jobs. The largest gains were in the leisure, hospitality, and retail trade sectors. Unemployment among Black workers declined by only 1.3 percent between April and June, about a third of the magnitude of White workers. And the data contained other worrying signs: The number of workers who have permanently lost their jobs increased to almost 3 million.

There are two additional factors that cause the headline number to understate the impact of the pandemic on employment. First, the report counts as employed an extra 2 million people who were “not at work for other reasons” and does not include the 4.6 million who have left the labor force since February. The 2 million were misclassified in error and should rightfully be counted as part of the true unemployment rate. Second, usually workers who leave the labor force are not included in totals of unemployment, but this pandemic presents a special case. Labor force participation fell substantially between February and May; a decline this large suggests that some of the people leaving the labor force may have done so temporarily due to the difficulties of looking for a job. Adjusting for these factors would increase the June unemployment rate to 13 percent.

Another worrying sign in the jobs data is government employment. State government employment declined by 247,00 between March and June, local government employment fell by a staggering 1.2 million, and federal government employment has been flat. As the coronavirus pandemic knocks a massive hole in their budgets, governments are laying off workers by the thousands. Lower consumer spending means lower tax revenue, and new coronavirus-related expenses means higher government spending. As a result, state and local governments are tightening their budgets at the worst possible moment for the economy. These government cuts have disparate impacts on Black Americans, who make up 12 percent of the labor force but 18 percent of government jobs.

The overall picture of the economy, then, is seriously troubling. Consumers are struggling, with incomes propped up by massive government stimulus and unemployment benefits. Some businesses are recalling furloughed workers but are concerned about a lack of demand. And governments are cutting employment and essential services due to unanticipated expenses and rapid declines in revenues. These fundamental issues will not resolve themselves on their own. The government acted with surprising alacrity in passing the Coronavirus Aid, Relief, and Economic Security, or CARES, Act in March, but further action is needed.

Policy proposals to head off a depression

First and foremost, the extra $600 per week Unemployment Insurance payments, slated to expire on July 31, should be extended and based on automatic triggers tied to an eventual economic recovery. The benefits are not only a lifeline to the 20 million workers who have been laid off but also the thin thread by which consumer spending is hanging. The drop in income and spending from the expiration of this benefit would be catastrophic for an economy in which market income is falling and spending has collapsed. Congress must extend the benefits and not put an expiration date on them, keeping them elevated until triggered off by unemployment returning to normal.

But even this is not enough. Given the collapse in consumer spending, it is clear that more demand support is needed than additional Unemployment Insurance payments. While the $1,200 stimulus payment in the CARES Act was a good start, there is no reason for this to be a one-off benefit. Monthly payments—$1,000 would be a good start—should be made until unemployment returns to normal and/or consumer spending improves.

State and local budget deficits through 2021 might approach $1 trillion. Without additional aid, the shedding of government workers across the country will continue. This is not a short-term issue that can be solved with a one-time stimulus bill. Once again, what is needed is monthly aid to state and local governments that continues until the unemployment rate returns to normal and states’ fiscal health improves.

While each of these policies can help to deal with the symptoms of the economic collapse, the fundamental cause remains the continuing spread of the novel coronavirus and the lethality of COVID-19 uncontained. Many of the layoffs are in the restaurant, travel, and retail sector, whose customers will not come back in sufficient numbers until it is safe to do so. Even with states beginning to reopen, 78 percent of Americans say they would be uncomfortable eating at a restaurant, and 67 percent are not comfortable shopping at a retail clothing store. While the outbreak may have left the front pages of some newspapers, it continues unabated. Around 500 Americans per day are dying from COVID-19, with 70,000 new cases reported each day.

Several of the hardest-hit European countries, such as Italy and Spain, have succeeded in suppressing new cases to the low hundreds per day. They did so by following the only tried-and-true plan that has worked against the coronavirus: a comprehensive program of tracking and tracing, with massive testing and effective tracing and quarantining of those exposed to the virus. Compared with the four economic stimulus plans Congress has already passed, the cost of these public health measures is moderate. Congress has already spent more than $1 trillion on relief and recovery measures—and more will be necessary—but the cost of following the proven path these other nations have taken would run in the relatively modest tens of billions of dollars, and could save additional trillions of dollars in consequently unneeded stimulus costs down the road.

There is much to be done. The federal government, state governments, and local governments must refocus and redouble their efforts to suppress the virus. A plan by Sens. Michael Bennet (D-CO) and Kirsten Gillibrand (D-NY) would create a national test-and-trace program that would hire hundreds of thousands of people who would help carry out testing, contact tracing, and eventually vaccinating to fight the coronavirus, at the cost of $55 billion. The Medical Supply Transparency and Delivery Act of Sens. Tammy Baldwin (D-WI) and Chris Murphy (D-CT) would finally rationalize the medical supply chain, utilizing the Defense Production Act to ensure the production of critical medical supplies.

Recovery from the coronavirus pandemic and the coronavirus recession is neither close nor assured. This mission has not been accomplished. The federal government needs to act and spend aggressively to support families, workers, and states and localities, and restore consumer demand. Acting swiftly and certainly can mean the difference between a lengthy, weak recovery with unnecessary suffering by those who already suffer from economic and racial inequality, and a strong recovery that leads to stable, broad-based growth and a more equitable economy.

Equitable Growth’s 2020 Paid Family and Medical Leave Grantees

The Washington Center for Equitable Growth today announced four research grants to scholars who are pushing the frontier of knowledge on paid family and medical leave in the United States. Their research, chosen in a competitive process with vetting by outside academics and approved by our Steering Committee, will be conducted by faculty members at leading U.S. colleges and universities.

Equitable Growth supports research to better understand the channels through which inequality affects growth and to provide evidence for policies that can address inequality and ensure strong, stable, and broad-based economic growth. We’re dedicated to bridging the gap between academia and policy by making sure research is relevant to today’s policy debates and by informing policymakers of cutting-edge research.

Equitable Growth is committed to advancing academic knowledge on paid family and medical leave. Connecting this new knowledge to policymakers, employers, media, and the public is increasingly important amid the ongoing public health crisis and recession caused by the coronavirus pandemic. In our first Request for Proposals specific to a subject area, Equitable Growth sought to stimulate research in three major areas:

Medical leave. Personal medical leave is the type of leave that is most frequently accessed, yet it also is the type of leave about which the least is known.

Caregiving leave. Caregiving leave impacts the lives of both caregivers and recipients, but outcomes are understudied for both groups.

Employers and paid leave. Even when paid leave is available from the state, employers affect their employees’ interactions with the paid leave system. The responses of firms to the availability of paid leave is a key channel through which paid leave affects the broader economy.

We are pleased to announce investments in research in all three areas.

In their project “Employers and paid leave: Assessing the interdependencies between state-level mandates, medical leave, and voluntary provisions of paid leave” Nicolas Ziebarth of Cornell University, Catherine Maclean of Temple University, and Stefan Pichler of ETH Zürich will examine the effect of both state-provided paid medical leave and city- and state-level sick pay mandates on the provision of paid leave. The proposed project will use restricted-use National Compensation Survey data with geographic identifiers and a difference-in-differences approach to determine whether employers react to the mandated provision of sick leave and state paid leave social insurance programs by reducing their voluntary provision of medical leave, private group disability insurance, and other forms of paid leave such as family leave. No other study has examined comprehensively the interactions and interdependencies of state-level sick pay mandates, employer provisions of paid leave, and state-run medical leave systems.

Two projects will examine caregiving leave. Priyanka Anand and Janusz Wojtusiak of George Mason University, Laura Dauge of Texas A&M University, and Kathryn Wagner of Marquette University will identify the characteristics of individuals who lack caregiving leave but have a family member who experiences the onset of disability or health shock. The investigators also will estimate the impact of access to paid caregiving leave on the financial security and employment for this group of individuals. The research team will use data from the National Compensation Survey to develop a machine-learning classification model to determine the likelihood that individuals observed in the Survey of Income and Program Participation have access to paid leave. This novel technique overcomes limitations in existing data sources that have hamstrung previous research efforts and is poised to make a significant contribution to the small but growing body of research on caregiving leave. This team’s project is titled “Access to paid caregiving and the impact on financial security, employment, and public program use of non-elderly adults in the United States.”

Kanika Arora of the University of Iowa and Doug Wolf of Syracuse University will look at another subset of people who may have caretakers in need of paid leave: older adults. Their project seeks to understand how access to paid family leave influences the provision of eldercare and labor market outcomes among individuals in midlife and whether the effects vary by the characteristics of care providers or recipient. To examine these issues, the research team will pool data from 11 waves of the Health and Retirement Survey to examine the experiences of respondents ages 51 to 65 with at least one living parent. They will survey responses to determine the intensity of caregiving provided, as well as the intensity of labor force participation, and use a difference-in-differences approach to compare the experiences of individuals residing in states with operational paid leave social insurance programs (California, New Jersey, and Rhode Island) to those who reside elsewhere. This team’s project is titled “Paid family leave and work eldercare tradeoffs.”

In their project “Employer employee discordance in awareness and perceived accessibility of paid family and medical leave” Julia Goodman of Oregon Health & Science University and Portland State University School of Public Health and Danny Schneider of Harvard Kennedy School will examine whether and how employers and employees are aligned in understanding about the accessibility of paid leave. Their research takes advantage of a unique data source, The Shift Project at the Malcolm Wiener Center for Social Policy at Harvard Kennedy School. The project samples low-wage service-sector workers from within a set of large retail and food service employers across the United States and allows the team to match employee responses with individual employers. The research will pair quantitative analyses of Shift Project data and in-depth interviews with twenty human resources staff members at firms in the sample. This mixed-methods approach will provide important information about how employer practices may mediate awareness and take-up of paid leave benefits.

Equitable Growth’s process does not end with grantmaking. We look forward to engaging with this impressive slate of grantees through publication of their findings in our working paper series, dissemination of their findings, and continuing to build a bridge between those who make paid leave policy and those who can provide the evidence needed to do so in a way that supports an economy that works for all.

Thank you to our paid leave advisory committee, whose expertise made this round of grantmaking possible:

Chantel Boyens, Principal Policy Associate, The Urban Institute Tanya Byker, Assistant Professor of Economics, Middlebury College Christopher Ruhm, Professor of Public Policy and Economics, University of Virginia Jack Smalligan, Senior Policy Fellow, The Urban Institute Kristin Smith, Visiting Associate Professor of Sociology, Dartmouth College Alexandra Stancyzk, Researcher, Mathematica Policy Research Jane Waldfogel, Compton Foundation Centennial Professor of Social Work for the Prevention of Children’s and Youth Problems, Columbia University

Unemployment rates in the United States are currently higher than they were at height of the Great Recession, standing at 11.1 percent in June after declining from a record high of 14.7 percent in April, compared 10.6 percent at the height of the previous recession in January 2010. Amid the deepening coronavirus recession, Unemployment Insurance is critical to keeping families afloat and bolstering our economy, just as the program has been throughout economic downturns since its federal inception in the Social Security Act of 1935.

Then and now, however, there is a common public narrative that purports generous and lengthy access to Unemployment Insurance is a disincentive to work, with people choosing to stay home and receive benefits rather than return to work. New cutting-edge research examining unemployment benefits and unemployment rates during and after the Great Recession demonstrates that was not the case then—with key implications today as Congress and the Trump administration negotiate whether and how to extend the Pandemic Unemployment Compensation program beyond the end of this month.

Forthcoming in the American Economic Journal: Economic Policy, the paper is titled “Unemployment Insurance Generosity and Aggregate Unemployment,” by Christopher Boone of Cornell University, Arindrajit Dube of University of Massachusetts Amherst, Lucas Goodman of the U.S. Treasury Department, and Ethan Kaplan of the University of Maryland, College Park. Their new research reveals that emergency Unemployment Insurance and extended benefits during and after the Great Recession did not increase unemployment rates between counties with longer access to those benefits, compared to those with shorter access. The four researchers find that overall bad economic conditions, such as those which occurred more than a decade ago and are evident again today, determine U.S. labor market outcomes more than generous access to unemployment benefits.

Prior to the steep downturn this year, the Great Recession was one of the biggest economic crises in a lifetime. Policymakers responded by instituting large increases in the duration of Unemployment Insurance, from 26 weeks to 99 weeks, but there were variations across states in both magnitude and timing. These changes were executed through the Emergency Unemployment Compensation program enacted by Congress on June 30, 2008 and modified seven times subsequently, as well as through the already-existing Extended Benefits program that provided 13 weeks or 20 additional weeks of Unemployment Insurance triggered by the level or pace of increase of a state’s unemployment rate.

Those triggers for Extended Benefits, however, are optional for states to take up, so many states opted out of providing more generous benefits in the Great Recession, resulting in variation between states in the duration of benefits available to unemployed workers. Both changes in policy over time through the Emergency Unemployment Compensation program and changes between states through the Extended Benefits program allow for what economists call a natural experiment to examine the impact of greater generosity in unemployment benefits on aggregate employment.

Boone, Dube, Goodman, and Kaplan implement what’s known as a cross-border-pair methodology—which examines differences in policy outcomes in similar regions of the economy and was pioneered by economists David Card and Alan Krueger—alongside an event study design, both with the Quarterly Census of Employment Dynamics, to test whether the long duration of unemployment benefits increased aggregate unemployment in states with more generous Unemployment Insurance. The four researchers find that the longer duration of benefits and the greater the increases to benefits result in a very small, positive impact on employment rates within those counties, with their results not statistically different than zero. While the overall employment-to-population ratio declined by 3 percentage points during the Great Recession, counties with more generous benefits may have offset this somewhat, or at least did not have worse employment outcomes.

Their paper directly challenges previous research that finds negative impacts on county employment rates as a result of longer Unemployment Insurance benefits, particularly work by Marcus Hagedorn of the University of Oslo, Iourii Manovskii of the University of Pennsylvania, and Kurt Mitman of Stockholm University. They followed a similar methodology. Boone, Dube, Goodman, and Kaplan rectify these discrepancies by noting that their paper makes use of superior administrative data in the Quarterly Census of Employment and Wages. The four researchers also critique the methodology of the previous research for using a “quasi-forward differencing” as a dependent variable based on anticipation of policy changes rather than the actual policy changes, and for examining a shorter time horizon.

Boone, Dube, Goodman, and Kaplan also address other critiques of the cross-border-pair methodology by dropping counties where employment was correlated with state levels of employment and by including county fixed effects. Their results did not change when dropping potentially spurious counties. Boone, Dube, Goodman, and Kaplan also note that their findings align with additional research using alternative methodologies that find similar insignificant impacts of duration generosity.

This cutting-edge research from the previous economic downturn demonstrates that benefit generosity in an economic crisis does not negatively impact employment levels, prolonging the labor market downturn. As the policy debate over extending more generous unemployment benefits will surely continue throughout the current recession, this new research supports the proposals included in Equitable Growth and the Hamilton Project’s Recession Ready essay compilation that calls for increased generosity in Unemployment Insurance, as well as triggers that extend the duration of benefits based on state-level unemployment rates.

The United Artists Theatres in Berkeley, CA., is one of the many venues that was forced to close at the onset of the coronavirus pandemic.

Under the Coronavirus Aid, Relief, and Economic Security, or CARES, Act,the Pandemic Unemployment Compensation program added a $600 weekly boost to Unemployment Insurance payments. Despite being one of the most effective policy responses to the coronavirus recession yet, the enhanced payments are set to expire at the end of July. The idea that Unemployment Insurance creates incentives for workers to remain unemployed has emerged as the main argument against extending the additional weekly $600, with critics arguing that generous benefits are “undermining the economic recovery.”

As this factsheet points out, current labor market indicators show jobless benefits have a negligible effect on unemployment levels. But the enhancements to Unemployment Insurance have a big impact on the economy and have set in motion a virtuous cycle that helps workers weather an economic crisis while keeping demand for goods and services from plummeting. Here are the facts.

The coronavirus health crisis—not enhanced unemployment benefits—are behind the spike in unemployment

Even after strong employment gains in May and June, the U.S. economy has lost 15 million jobs since February, and new unemployment claims have stood above their Great Recession high for 15 straight weeks. The absence of safe working conditions, a sharp drop in consumer spending, and lack of support for parents and caregivers are preventing millions from working.

More specifically:

Using real-time data from small businesses, a team of economists find that the states where benefits replace a greater portion of workers’ wages experienced the smallest drop in hours of work in March and, as of early June, the strongest recovery. Another analysis finds that receiving jobless benefits had no effect on workers’ likelihood of finding a job.

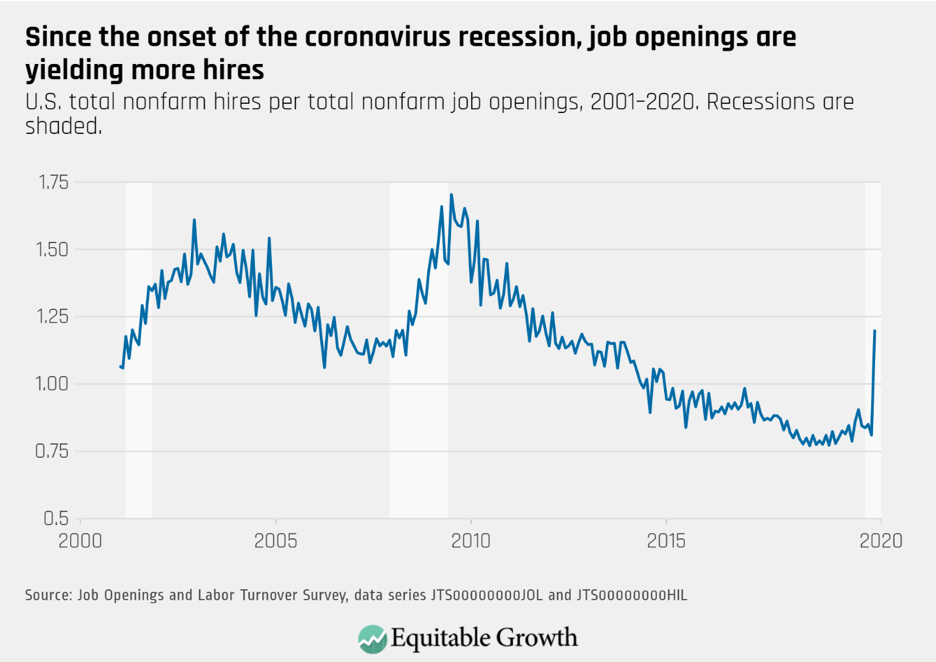

The U.S. vacancy yield, which measures the ratio of hired workers for every job opening, shows that employers are now filling open positions faster than at any point since February 2012. Lack of opportunities to work, not a disincentive to work, are keeping unemployment elevated. (See Figure 1.)

Data from Indeed.com—a widely used job-search website—show that there were 23 percent fewer job openings in early July 2020 than in the same moment the previous year. Data from the U.S. Bureau of Labor Statistics show that there are now almost four unemployed workers for every job opening.

Figure 1

Concerns about work disincentives overstate the negative impact of jobless benefits on employment and minimize the positive impacts evident in economic research

There is no academic consensus on the effect of the duration or generosity of unemployment benefits on employment. Research shows, however, that any effect these benefits might have on overall unemployment is small and likely to be weaker in downturns than in booms. Consider:

Cutting-edge research on the duration of Unemployment Insurance finds that the expansion of jobless benefits during and after the Great Recession had a negligible effect on unemployment rates. When comparing similar workers facing similar labor market conditions, states where workers could get benefits for longer did not have higher rates of unemployment.

By providing a lifeline when jobs are scarce, Unemployment Insurance can keep workers engaged in searching for jobs even when jobs are hard to find, keeping many from dropping out of the labor force altogether.

Unemployment Insurance provides liquidity to the workers who need it the most, getting cash in the hands of those more likely to spend it. Those who have been hardest hit by the crisis—Black, Latinx, and low-income households—are less likely to have the liquid financial assets needed to maintain their consumption when their earnings suddenly go down.

Until the coronavirus pandemic and recession are under control, rolling back unemployment benefits will exacerbate the public health crisis and deepen the downturn

Under normal circumstances, Unemployment Insurance allows workers to put food on the table as they search for suitable work, supporting overall economic activity. In the context of a global pandemic and the sharp recession it sparked, providing workers with time and financial resources as they search for suitable work is even more crucial. Specifically:

Without adequate health and safety workplace standards, face-to-face jobs will put millions of workers at risk. Workers need time and resources to search for suitable work that will not jeopardize their health or public health.

In the economics literature, the concept of compensating wage differentials describes the additional earnings needed to offset the negative risks associated with some jobs. The true costs to workers of being exposed to a deadly virus in a pandemic is not reflected in the pre-pandemic wage levels used to calculate benefit amounts. Enhanced Unemployment Insurance allows workers to make decisions based on safety rather than desperation during the pandemic.

The Economic Policy Institute estimates that extending Pandemic Unemployment Compensation payments through mid-2021 would provide 5.1 million jobs by maintaining demand for goods and services.

The emphasis on work disincentives serves to exclude Black and low-wage workers and reflects racist biases against low-income workers of color

As with other safety net programs, opposition to a robust Unemployment Insurance system often acts to prevent workers of color from receiving their fair share of unemployment benefits. This is especially true for Black workers. Consider:

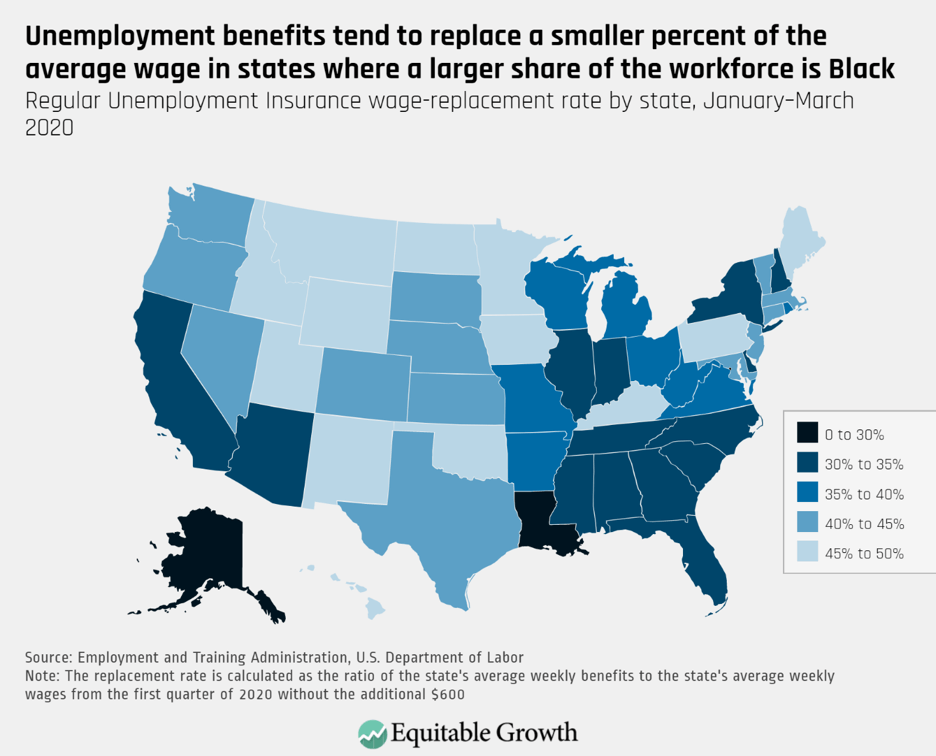

Despite applying for Unemployment Insurance at similar rates than unemployed White workers, unemployed Black workers—and especially unemployed Black women workers—have been much less likely to receive benefits. States with a higher share of Black workers tend to have less generous jobless benefits. For Black workers, an estimate shows, the average maximum weekly benefit is $40 short of that received by White workers. (See Figure 2)

Figure 2

Depending on the state, the withdrawal of the additional $600 would lead to a median cut in benefits of 52 percent to 72 percent. The drop would be of 71 percent in Arizona, 71 percent in Louisiana, and 72 percent in Mississippi.

Conclusion

As a number of states reinstate lockdowns due to the recent surge in coronavirus cases and COVID-19 deaths, the prospect of a quick economic recovery is becoming increasingly unlikely. Concerns about work disincentives fail to recognize that job displacements have consequences beyond the loss of wages. Most workers find inherent value in their work and care about benefits, career advancement opportunities, and their long-term economic security.

If Congress lets the Pandemic Unemployment Compensation program expire, then those who have already been hardest hit by the downturn—Black workers, Latinx workers, women workers, and low-wage workers—will be most affected, making the current crisis longer and more severe.

Equitable Growth is committed to building a community of scholars working to understand whether and how inequality affects broadly shared growth and stability. To that end, we have created the monthly series, “Expert Focus.” This series will highlight scholars in the Equitable Growth network and beyond who are at the frontier of social science research. We encourage you to learn more about both the researchers featured below and our broader network of experts.

The future health and stability of the U.S. economy depends on our ability address the roots of longstanding racial inequalities. Continuing the theme from last month’s installment of “Expert Focus,” we highlight Black scholars whose cutting-edge research is influencing our understanding of the historic and persistent role that structural racism plays in driving wealth and income inequality for Black Americans particularly.

Peter Blair

Harvard University

Peter Blair is an assistant professor of education at Graduate School of Education of Harvard University, where he co-directs the Project on Workforce and serves as the principal investigator of the Blair Economics Lab—a research group with partners from Harvard University, Clemson University, and University of Illinois Urbana-Champaign. He received an Equitable Growth grant in 2019 to study the impacts of state-by-state occupational licensing policies on wage and employment outcomes for individuals with a previous felony conviction. Blair’s professional interests are broad in scope—he recommends that businesses wanting to address systemic racism in hiring and management should focus on job skills, rather than continuing to privilege college degrees, and has shared his views on the importance of mentorship, particularly to support diversity in the economics profession.

Terry-Ann Craigie

Connecticut College

Terry-Ann Craigie is an associate professor of economics at Connecticut College and economics fellow at the Brennan Center for Justice. She recently joined the Opportunity & Inclusive Growth Institute at the Federal Reserve Bank of Minneapolis as a visiting scholar. She is a labor economist who studies the intersections of mass incarceration, criminal justice reform, and labor markets. Her current research examines the economic and social costs of mass incarceration within the U.S. labor market context, as well as the implications for racial justice. In her most recent study, she evaluates the impact of “Ban the Box” policies on the public employment of people with criminal records and tests whether these policies lead to discrimination against young males of color.

Ellora Derenoncourt

Princeton University

Ellora Derenoncourt recently joined the University of California, Berkeley as an assistant professor in the Department of Economics and the Goldman School of Public Policy. She was previously a postdoctoral research associate in the Economics Department at Princeton University and has received several grants from Equitable Growth, including one as a graduate student for her work, in collaboration with Claire Montialoux of the University of California, Berkeley, on the historical determinants of racial gaps in earnings and upward mobility. That research resulted in a recent working paper that found a dramatic reduction in the racial earnings divide in the United States through a reversal of racist and exclusionary wage policy. Watch her discuss her and Montialoux’s research here at the Allied Social Sciences Associations’ 2020 annual meeting.

Damon Jones

University of Chicago

Damon Jones is an associate professor at the University of Chicago Harris School of Public Policy working at the intersection of public finance, household finance, and behavioral economics. His work has provided important insights into the ongoing debates around economic security and opportunity, universal basic income, retirement, and tax. He recently testified at a U.S. House of Representatives Committee on the Budget hearing about health and wealth inequality in the United States and how health and wealth interact with the current coronavirus pandemic. His recent working paper shows that income shocks affect Black and Hispanic households more strongly than their White counterparts, as a result of the persistent racial and ethnic wealth divide in the United States.

Equitable Growth is building a network of experts across disciplines and at various stages in their careers who can exchange ideas and ensure that research on inequality and broadly shared growth is relevant, accessible, and informative to both the policymaking process and future research agendas. Explore the ways you can connect with our network or take advantage of the support we offer here.

One of the explanations for this job-quality crisis is that not enough workers have the skills required for an increasingly digital and technologically advanced jobs market, leading to a widening gap between the rising wages of the highest-paid workers and everyone else. The concept of a skills gap was likewise blamed for high unemployment after the Great Recession ended in July 2009 and is now cited as the key challenge facing low-wage workers amid the current coronavirus recession. The proposed solutions to closing this apparent gap center around education and training for low-wage workers, often with a focus on getting more workers to obtain college degrees, so they can fill these high-wage, high-demand jobs.

Yet this focus on individual workers misses the structural conditions that constrain workers’ options and ability to share in economic growth. This issue brief examines recent data-driven research that demonstrates the skills gap is only a small and relatively unimportant explanation for the college wage premium because it fails to account for declining worker power and the role of monopsony in the labor market. These more important explanations for the college wage premium—and its recent decline—underscore why policymakers need to improve the underlying labor market conditions for all workers, instead of shifting responsibility to those already struggling in an uneven playing field.

The college wage premium can’t explain the ongoing rise in wage inequality

A recent National Bureau of Economics Research working paper by economists David Autor at the Massachusetts Institute of Technology (and a member of Equitable Growth’s Research Advisory Board) and Claudia Goldin and Lawrence F. Katz (also an Advisory Board member) of Harvard University demonstrates how the college wage premium changed over time in response to labor market changes and policy shifts affecting worker power. While the paper itself is based in a skills-focused framework, its findings show that even this framing falls short when attempting to explain the rise in wage inequality since 2000.

The paper is part of a series of research that assumes employers’ demand for skilled labor is driven by “skill-biased technological change.” This framework holds that technological advancements—such as computers or robotics—improve the productivity of workers with the skills and education necessary to use the technology more than they improve the productivity of less-skilled workers. The result is a “race” between technology and education, where technological advancements lead employers to require more highly educated workers, but immediate shortages in the supply of educated workers result in higher wages for the college-educated candidates already in the workforce.

This framework is premised on a simplistic supply-and-demand model of the market that supposes wages are purely a result of demand for worker attributes and those attributes explain wage levels for individual workers. In framing wage distribution and outcomes in this way, it overlooks other important factors such the influence of institutions, including unions, and the relative power of workers and employers in changing labor markets.

The new paper expands on previous research, including a 2007 paper by Goldin and Katz, “The Race Between Education and Technology,” which tracked the differences in wages for workers with different education levels from 1890 to 2005. This paper combines several data sources to extend that analysis to look at the relationship between years of schooling and wages over the period from 1825 to 2017.

In line with previous research, the latest paper by Autor, Goldin, and Katz finds that when demand for educated workers is high and supply is low, such as in the late 1800s, the wage premium for educated workers—defined as the average difference between their wages and those of less-educated workers—is high. When the supply of educated workers increases, as it did over the early part of the 20th century, the wage premium falls. The definition of a relatively eduated or skilled worker shifts over time, of course, depending on eduation trends and available data sources, beginning with those who did clerical work (which generally required a high school background) prior to 1914 and then tracking those with high school and college degrees or equivalents.

Since the beginning of the 20th century, the three researchers find that a 10 percent increase in the relative supply of college-educated workers leads to a 6 percent reduction in the college wage premium. The paper argues that models using this framework can explain most of the wage premium for educated workers—but only until the 2000s, when other factors appear to play a larger role.

As the authors note, the wages of educated workers only describe one side of the education wage premium. Because wage premiums refer to the difference between earnings for educated and less-educated workers, they depend not only on the added value for educated workers but also the opportunities for workers without that educational background. The strong decline in wage premiums for high school and college educations in the 1940s probably did not happen because the supply of educated workers increased dramatically—in 1940, the reach of high school education had expanded, but only 6 percent of men and 4 percent of women had completed 4 years of college. Instead, the authors write, the lower relative returns to education in the 1940s were “likely driven by strong unions, tight labor markets, and government wage pressures during World War II.”

Likewise, the three authors find that the strength of American unions and a robust national minimum wage also contributed to a decline in the college wage premium in the late 1970s. This happened because wages improved for those in occupations that did not require a college degree.

When the three authors examine more recent wage patterns, they find that wage inequality rose at roughly the same rate between 1980 and 2000 as it did between 2000 and 2017, but also that the college wage premium could explain 75 percent of this increase in the first time period and only 38 percent in the second time period. Furthermore, wage inequality increased within college degree holders since 2000, and workers with advanced post-college degrees earned even greater wage premiums.

The authors conclude that the framework of a race between education and technology “remains relevant in the 21st century, but needs some tweaks” to fully capture the drivers behind the rising wage inequality the United States experienced since 2000.

Rising education requirements are not necessarily due to increasingly skilled work, and the returns of a college education are often less for the workers who need it most

One of the factors complicating a straightforward interpretation of the college wage premium is that employers often require college degrees for positions for reasons other than the content of the role’s duties. One way this is evident is when employers often raise job education requirements during times of high unemployment, when there are many candidates for jobs, but may also drop these requirements when the labor market tightens. Over time, as a greater share of workers earns college degrees, education requirements may continue to rise—but, crucially, not because the duties of the job require greater skill or education levels.

As a paper by Paul Beaudry of the University of British Columbia and the National Bureau of Economic Research, David A. Green of the University of British Columbia and Institute for Fiscal Studies, and Benjamin M. Sand of York University found, the decline in demand for college degrees since 2000 led many college-educated workers to take jobs that did not require a degree, which, in turn, pushed workers without degrees down into even lower-wage jobs. The Roosevelt Institute also notes that requiring unnecessary degrees drives more students to attend college, often taking on large amounts of debt in the process, because they’ve been told they can’t afford not to.

The evidence is clear that while a college degree is increasingly a requirement for middle- and high-wage jobs, it is not a guarantee of higher earnings, especially for people of color. Discrimination and occupational segregation continue to limit wages and economic opportunity for Black and Latinx workers and intersect with gender discrimination to additionally lower wages for Black women and Latinas. The new NBER working paper by Autor, Goldin, and Katz examined in the previous section of this issue brief did not break out college wage premiums by race and ethnicity, but other research shows that Black and Latinx workers with college degrees continue to earn lower wages than White workers with college degrees.

In addition, Black workers with college degrees experience higher unemployment rates compared with White workers with college degrees, as shown by economists Jhacova Williams and Valerie Wilson of the Economic Policy Institute. The two economists also find that Black workers are more likely to be underutilized in jobs that do not require a college degree.

Then, there’s evidence that shows how external factors limit the role of a college degree in driving economic mobility. As economist Brad Hershbein writes for The Brookings Institution, a college degree is still associated with higher earnings, on average, but actually benefits the wages of those from lower-income backgrounds less. Hershbein finds that college graduates from very low-income backgrounds—those from families below 185 percent of the federal povery level—see less of a relative income bump from their degree over the course of their careers than college graduates from higher-income backgrounds.

College graduates from very low-income families go on to earn 91 percent more than people from the same income background who only graduated high school, but college graduates from families with higher incomes earned 162 percent more compared with high school graduates from that income background. If the content of a college degree is the key to skilled work and greater economic mobility, then these findings should be the reverse. Instead, these findings—along with research on the role of household wealth and of student debt—show that the college wage premium is not a straightforward story.

The skills gap framing ignores the underlying dynamics of job quality and worker power

The new NBER paper by Autor, Goldin, and Katz demonstrates that the college wage premium declined when unions were strong and the real minimum wage was at its peak. The research shows that the college wage premium is less a story of supply and demand—let alone about the inherent value of a college degree—and more about other U.S. labor market factors such as the underlying dynamics of job quality and worker power. It is also the story of the opportunities for workers without a degree and the protections they have.

We see the importance of these factors in another recent NBER working paper, by Matthias Doepke of Northwestern University and Ruben Gaetani of the University of Toronto, which sheds more light on the intersection of skills, job quality, and worker protections. Comparing college differentials in the United States and Germany since 1980, the paper’s findings suggest that a major reason why the college wage premium has risen in our nation compared to Germany is that German employment protections reduce the number of worker separations from their employers and encourages employers to invest in workers.

Doepke and Gaetani’s model suggests that the very precarity and lower-quality of jobs in the United States do not allow these workers to develop skills over time in the same way that college-educated workers can. This bolsters the idea that part of the cause for the college wage premium is higher-wage workers’ bargaining power.

Ultimately, the skills-focused competitive market approach needs more than a tweak to fully capture the forces shaping earnings for workers. As Equitable Growth Labor Market Policy Director Kate Bahn explains, the idea that a skills gap is at the root of wage inequality ultimately ignores the role of unions, worker power, and the broader policy decisions affecting low-wage workers. In a recent Equitable Growth working paper by Bahn and Mark Stelzner of Connecticut College, the authors demonstrate how barriers to job search by race and ethnicity, particularly lack of access to wealth for workers of color and women workers, means that these workers face more difficulty managing their lives and job searches while being unemployed longer without earnings.

Because workers from marginalized groups can’t afford to wait for better job opportunities, employers wield a greater ability to offer lower (discriminatory) wages. Fostering worker bargaining power through pro-labor institutions, such as supporting union organizing and enforcing anti-discrimination laws, reduces the ability of employers to use their monopsony power to exploit workers by race and gender. Similarly, other research shows that raising the minimum wage directly benefits low-wage workers, reducing income inequality and narrowing racial wage disparities.

To reduce wage inequality, improve conditions for all workers, not just those at the top

As Equitable Growth noted in 2014, one of the results of assuming that education differences provide the main explanation for rising wage inequality in the United States is to lead policymakers to view college as a blanket solution for inequality. But the evidence from the Great Recession shows that the apparent skills gap is often driven by greater employer power in times of high unemployment, and that a college degree does not protect workers from low-paying, low-quality job options with no bargaining power and no opportunities to learn and grow. Focusing on education as the first and leading solution to wage inequality ignores the larger issues that undercut workers’ options and further racial disparities. While education and training are often part of what workers need to access quality jobs, they will not be sufficient without worker power to ensure they share in the productivity gains their value-added inputs create.

If past trends continue, policymakers can expect employers to respond to the current record-setting unemployment levels by continuing to raise education requirements. And many policymakers will attempt to respond to this sudden skills gap with calls for more education and training. But the solution to today’s dismal jobs numbers is not tell workers to go into debt acquiring credentials only to be rehired at the same types of jobs that had not previously required a degree. Instead, policymakers need to address the structural conditions shaping jobs and wages across the board, focusing on the needs of workers at the bottom of the income ladder. This will require raising the minimum wage to improve outcomes for the country’s most vulnerable workers, actually enforcing anti-discrimination laws to reduce pay disparities by race and gender, strengthening unions to give workers a voice in their working conditions and training opportunities, and checking the rising monopsony power that prevents workers from sharing economic growth.

1. The old Chicago-school argument was that market pressures would not allow employers to discriminate—not unless their customers strongly and immediately demanded it. This was always subject to a critique: to the extent that market discipline was not immediate and absolute, market power gave running room to bad actors. Now come Kate Bahn and Mark Stelzner to point out that even good actors with market power will reflect, transmit, and amplify discrimination elsewhere in the system: Kate Bahn and Mark Stelzner, “How racial and gendered pay discrimination persists under monopsony in the United States,” in which they write: “There are many obstacles in finding a job … [that] inhibit workers from moving freely … and thus give employers monopsony power … Because these obstacles more commonly confront women and non-White workers, employers have more power over such workers, which means employers can push their wages down more compared to White men … These racialized and gendered wealth disparities reinforce discriminatory pay penalties … Greater protections for collective action and a more pro-worker National Labor Relations Board … can limit the ability of employers to exploit workers based on their gender or race and ethnic backgrounds … Wage disparities, and monopsony power more broadly, are moderated by workers’ ability to act collectively as a countervailing force, and that kind of worker power is a function of institutional supports for collective action … A variety of factors intersect to result in discriminatory wage outcomes for workers along the lines of race, ethnicity, and gender, and likewise shows that a suite of policies in tandem that address these broad constraints would lead to more efficient outcomes and higher levels of social welfare.”

2. We have a Treasury. We have a Federal Reserve. We have an Internal Revenue Service. Those financial operations that can be done at scale and do not require the incentive of profit-seeking expertise—or that are hindered by the deployment of profit seeking expertise—should all be provided by the government. Why weren’t they so provided in the case of the Paycheck Protection Plan? Amanda Fisher asks the question, and give us an answer. Read her “Did the Paycheck Protection Plan work for small businesses across the United States.”

3. Back at the end of 2008 I lobbied the Obama administration to put the unemployed at work going door-to-door treating the chronic diseases of the uninsured. Win-win. Now the same logic applies, both at the federal and at the state level, to put the unemployed at work in public health. Win-win. The states may say they have no money. But states that suppress the coronavirus will end up having much more money, even in the short run, than states that do not. Read Delaney Crampton, “The United States needs a new Works Progress Administration to overcome the coronavirus recession,” in which he writes: “Our nation needs more tracking and tracing of cases so that people can be notified and help limit the contagion of others. Unfortunately, the implementation of contact tracing programs has been uneven … At the same time, more than 44 million Americans have filed for unemployment benefits in less than 4 months. These two dire and worrisome trends—one related to public health and the other economic—also create a singular opportunity. Policymakers could place millions of people searching for work into contact tracing jobs through a modern-day Works Progress Administration … In Massachusetts, the nonprofit global health organization Partners in Health has been tapped to spearhead the state’s new contact-tracing program. Already, it has hired and trained close to 1,000 contact tracers. They are paying workers $27 an hour for their time and providing all contact tracers with health insurance. Massachusetts is taking a step in the right direction, but there are estimates that the United States will need to hire as many as 300,000 contact tracers to track and prevent the spread of COVID-19.”

4. The relative material progress of Black Americans in the United States has been stalled since the 1970s. The black shadow of slavery and Jim Crow and its impact on the wealth distribution means that any “declining significance of race” has been offset by a rising significance of class. And then we need to add in the rising ossification of America’s class structure. Those of us who are African American do not forget this. Those of us who are not African American need to recall this many times each day: when we rise, and when we lie down; when we eat, and when we drink; when we work, and when we rest. Read Liz Hipple, Shanteal Lake, and Maria Monroe, “Reconsidering Progress This Juneteenth: Eight Graphics that underscore the economic racial inequality Black Americans face in the United States,” in which they write: “In observance of Juneteenth, the Washington Center for Equitable Growth is reflecting on the perceived progress made in the lives of Black Americans and highlighting evidenced-backed policy solutions needed to reduce economic racial inequality. Eight graphics on wages, wealth, and health: Black workers, especially Black female workers, have lower salaries than White workers with similar levels of education. While the median White male worker with a college degree earns $31.25 an hour, the median Black male worker with a college degree only earns only $23.08. This is only $5 more than a White male worker with a high school degree. Some of this wage gap is due to occupational segregation, but the majority of it is “unexplained” and is attributed to discrimination.”

Worthy reads not from Equitable Growth:

1. There is every reason to hope for a rapid economic bounceback toward full employment in Japan and Europe. But as best as I can see, Dan Alpert is right here: The right economic forecast for the short run here in the United States is one of fear and terror of a snowballing depression. Read his “The government needs to step in to save American businesses or the US is going to spiral into a second Great Recession,” in which he writes: “We have now entered the post-PPP Payroll Lay Off Phase (PLOP) of the COVID-19 Pandemic Recession of 2020 in the United States. Efforts by the federal government to soften the blow to businesses and households were bold—but we can see clearly now, not sufficient. America is still hemorrhaging jobs … Workers … not being “re-employed” … but … rather being “re-payrolled”… to meet the requirements of the Payroll Protection Program (PPP) … Many of the 4.9 million borrowers under the program may not be viable as ongoing enterprises. Even more will be non-viable unless they now cut costs and jettison a good number of the workers they added back to payrolls with the PPP dollars. The evidence of this re-furloughing and resumed layoffs is rolling in now like thunder … In addition to the 50 million claims above, there have been 8,792,890 in aggregate initial claims for unemployment insurance benefits made by self-employed persons under the Pandemic Unemployment Assistance Claims (PUAC) program, over one million in just this past week alone … It would be a mistake … to conflate these persistently high initial claims numbers with the new peaks in COVID-19 cases in the Southern and Western states. The data could not more clearly illustrate the opposite to be true … The layoffs and furloughs that are behind the continuing (and soon to be growing) volume of unemployment claims are evidence of the deep recession … deeper than that of the Great Recession. The only questions are whether this Greater Recession will last longer than its predecessor and whether it will turn into an outright economic depression.”

2. In the Clinton and Obama administrations legislative proposals tended to be crafted with an eye toward gaining of the approval of at least 60 Senators. The combination of senate procedural blockages and the belief that bills many Republican senators thought were good policy would be durable victories led to that strategy. It was a catastrophic failure. Joe Biden’s staff appears to have learned from Clinton’s and Obama’s mistakes, and is drafting proposals focusing on what would genuinely be the best policy. It is very nice to see. Read Matthew Yglesias, “Joe Biden’s surprisingly visionary housing policy, explained,” in which he writes: “Joe Biden has a housing policy agenda that is ambitious, technically sound, and politically feasible, and that would—if implemented—be life-changing for millions of low-income and housing-insecure households. According to original modeling by Columbia University scholars, it could cut child poverty by a third, narrow racial opportunity gaps, and potentially drive progress on the broader middle-class affordability crisis in the largest coastal cities as well. The plan hasn’t stirred an intraparty debate or really much attention at all, which could make it politically feasible to enact …The centerpiece is simple. Take America’s biggest rental assistance program — Section 8 housing vouchers — and make it available to every family who qualifies. The current funding structure leaves out around 11 million people, simply because the pot allocated by Congress is too small. Then pair it with regulatory changes to help the housing market work better for more people. It’s the general consensus approach among top Democratic Party politicians and left-of-center policy wonks.”

3. Is it the staying at home with lots of time to think, the economic distress and uncertainty, or the heightened fear and consciousness of mortality, or just chance that turned the coronavirus spring into the Black Lives Matter spring? Barry Eichengreen believes that it is the second. Read his ‘Rage Against the Pandemic,” in which he writes: “The connection running in the other direction—from the pandemic to the demonstrations—has received far less attention …Why now? … Before Floyd, there was the police killing of Michael Brown … Eric Garner … nearly 100 African-Americans who died in police custody over the past six years. One explanation for why Floyd’s killing triggered a national uprising is … an especially horrific recording … But this answer will satisfy only those who have forgotten the equally horrific recording of Garner’s killing. A more convincing explanation must include the pandemic …The COVID-19 mortality rate is 2.4 times as high among black Americans as white Americans … [a] situation … already approaching the unbearable…because of America’s threadbare social safety net … Certain states in the South provide fewer. Indeed, some, such as Florida, have intentionally designed their bureaucracies to make applying for unemployment benefits as difficult as possible.”

This is a post we publish each Friday with links to articles that touch on economic inequality and growth. The first section is a round-up of what Equitable Growth published this week and the second is relevant and interesting articles we’re highlighting from elsewhere. We won’t be the first to share these articles, but we hope by taking a look back at the whole week, we can put them in context.

Equitable Growth round-up

The coronavirus recession and the current debate surrounding reopening the U.S. economy shine a blinding light on the role of child care in supporting our economy. In fact, writesSam Abbott, rarely before has it been so obvious how important various forms of child care—from schools to daycare to summer camps—are to the state of the economy and its ability to recover. A national set of safety standards must be developed by scientists and public health officials, he argues, and until that happens any plans to reopen schools and child care facilities will remain patchwork and random, shaped largely by uncertainty about the coronavirus pandemic and its impact on children and how it is spread by children. Likewise, Abbott says, policymakers should ensure that child care is affordable and accessible to all American families—an already daunting challenge made more formidable because the child care industry has suffered devastating layoffs and closures since the onset of the pandemic. Abbott reviews some pre-coronavirus trends in child care options and parental preferences, and why those choices could limit the post-pandemic child care industry without thoroughgoing reforms.

Now that some U.S. small businesses are attempting to reopen, and policymakers are still considering how to stabilize the economy while protecting public health, it is as good a time as any to look back at the Paycheck Protection Program and examine its efficacy in achieving its goals. The program was designed to help small businesses keep employees on payroll and avoid bankruptcy during the pandemic. While early research shows it did provide a liquidity backstop for some firms during lockdowns, Amanda Fischerexplains that studies also show that PPP loans did not go to small businesses in the country’s hardest-hit areas and that the program itself did not have a statistically significant impact on preventing layoffs. Fischer goes through the various studies that analyze the program and reveal its flaws, and then proposes several policy recommendations and alterations that could address these shortcomings in future iterations of the program.

New research from Kate Bahn and Mark Stelzner shows how employers have more power over—and thus can push wages down more—for women and non-White workers compared to White men workers. The co-authors look at how workers search for jobs to show how racial and gender wealth disparities reinforce discriminatory pay penalties. They find that workers with greater wealth (who, in the United States, tend to be White workers) are better equipped to weather drops in income levels during job search periods and can thus hold out for a job that pays well and fits their skillset, while workers with less wealth and less of a financial cushion (who tend to be workers of color) take jobs that pay “just enough” out of necessity. Similarly, women workers tend to have more household responsibilities and thus are constrained by geography in their job searches, reducing their job prospects and allowing employers to take advantage of that constraint. The co-authors also show how workers’ ability to act collectively limits employers’ monopsony power, or the ability to set wages, of employers and reduces exploitation of workers based on gender and race and ethnicity. Bahn and Stelzner then propose several policies that can strengthen worker power, reduce wealth inequality, and boost family economic security.

Head over to Brad DeLong’s latest Worthy Reads to get his takes on recent must-read content from Equitable Growth and around the web.

Links from around the web

Until now, there has been very little acknowledgement of how truly vital child care and schooling is to the functioning of the U.S. economy—or the impact a broken child care system has on workers and their families. Vox’s Anna North gives us a deeper look at the numbers, providing an easy-to-grasp framework for looking at the impact of the current child care crisis on our economy and how important it will be to solve this crisis for our future economic recovery. North looks at data points such as the number of workers with children under age 18 who have lost their child care due to the pandemic, the impact of this loss on income, wages, and hours worked, and how differently this affects women and men workers, as well as two-parent and single-parent households. North then reviews the impact of the coronavirus pandemic and resulting recession on the child care system and its workers, and, in looking at the Trump administration’s failure to provide guidance in this area, concludes with an assertion that we must change how we value care work and education in order to carve out a path forward.

Eventually, the overall U.S. economy will recover from the coronavirus recession, but not before leaving a lasting impact on how many Main Streets across the United States are structured, writes James Kwak in The Washington Post. It’s likely that many small businesses will not survive, that “chain stores will replace mom-and-pop businesses, some storefronts will remain vacant, and cash that once went into local hands will be redirected to Amazon and Walmart.” In other words, the pandemic and the resulting recession are likely to amplify the two major trends that have been reshaping our economy in recent years: consolidation and inequality. Kwak explains the effect these two economic trends have had thus far, and how they will only be exacerbated by the hardships many small businesses and local economies are likely to face in the coming months and years.

Before federal aid lapses at the end of this month, policymakers in Washington DC must ensure that Unemployment Insurance benefits are extended until people can actually find new jobs and return to work safely, writesThe New York Times’ Editorial Board. Automatic stabilizers would work to increase support for those in need during this and future crises and wind down automatically when normal economic conditions return, the Board continues, thus guaranteeing that politics don’t play a role in helping vulnerable communities facing layoffs. The extended unemployment benefits provided in the Coronavirus Aid, Relief, and Economic Security, or CARES, Act in March have played an outsize role in stabilizing household finances and keeping families out of poverty. The end-of-July expiration date was placed on these extended benefits because policymakers hoped the pandemic would be under control by now. Because this is obviously not the case, the Editorial Board urges Congress to act swiftly to extend these benefits further and incorporate an automatic stabilizing element to ensure workers receive needed aid in the best, smartest, and most timely way.

By now, it is no secret that parents across the United States are struggling. Adapting to life during the coronavirus pandemic has been difficult for nearly everyone, but parents—particularly those with young children—are facing day-in, day-out work-life conflicts with no end in sight. Whether they are continuing to work from home, unemployed, or still working outside the house, providing for their children without the support of schools, daycare, camps, or even help from grandparents is taking an emotional and economic toll. Rarely has the role of child care in supporting our economy, by freeing up parents’ time and minds to focus on work, been more self-evident.

For weeks, experts and parents alike have been warning that child care will be essential in any economic recovery from the coronavirus recession. Without it, many parents, particularly women, will have to weigh dropping out of the labor force or reducing their work hours if their caregiving responsibilities remain incompatible with their work responsibilities. Still, plans to reopen schools and child care facilities remain scattershot, largely driven by uncertainty about how coronavirus infections spread in such environments, how children may contract or spread the virus to adult staff, and how susceptible children themselves are to COVID-19, the disease spread by the coronavirus.

How to provide child care safely is primarily a question for scientists and public health experts, but policymakers and social science researchers have their own role to play in this ongoing crisis. First, the coronavirus pandemic must be treated as the workplace safety issue that it is. This involves developing a national set of safety standards—along with the appropriate education, training, and funding to enact those standards—so that parents and staff can be confident that their care is as safe as it can be. Without such standards, each facility will have to fend for itself with limited knowledge and potentially disastrous consequences.

Also important are policies designed to make child care accessible and affordable even in the midst of a pandemic. Recent research suggests that the child care market will be unprepared to provide care in a post-pandemic environment without significant public investment. If parents are shifting their preferences as a result of the pandemic and ensuing economic crisis—either by desiring smaller providers or working more nonstandard hours—then the policy challenges of providing high-quality and affordable care will only grow.

More research on what child care services families need and what the child care industry is poised to provide will help target the policy response supporting families as they return to work and fuel the economic recovery.

Child care priorities prior to the coronavirus pandemic limit our post-pandemic options

The United States does not have a universal child care system, so many families rely on a patchwork of polices, including tax credits, licensing standards, and subsidy programs, to access high-quality child care. These policies help some families afford much-needed care, but they are largely insufficient in meeting the variety of care options that families need. What’s more, these policies underpin a child care system that lacks the flexibility necessary to meet the shifting needs of families in response to the current pandemic.

As the coronavirus and COVID-19 continue to spread through communities, larger child care centers, where dozens of children are together in one building, may be more prone to spreading both the virus and the disease. Already, some communities are reporting alarming transmission of COVID-19 in child care centers, though some studies suggest the disease is less likely to spread among children.

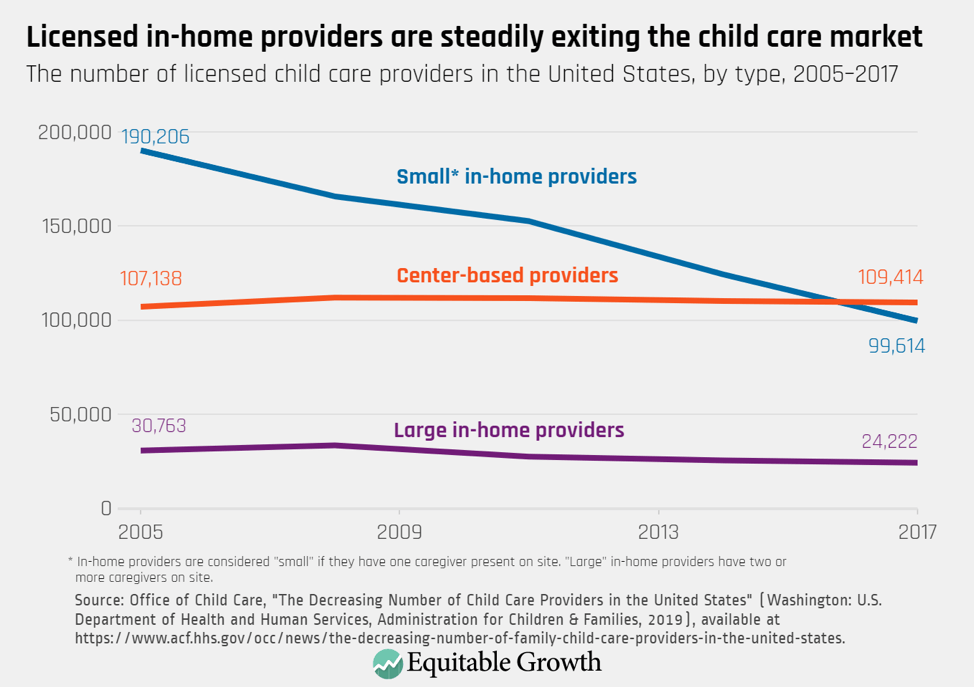

While wealthy families can hire nannies or babysitters to limit exposure, middle- and lower-incomes parents may be driven to seek in-home care. This type of care, also called home-based care, typically occurs in the provider’s home, where only a handful of children are present. It may be reasonable to assume these less-crowded settings are a safer alternative for families concerned about the safety of their kids and themselves. But the number of licensed in-home providers has rapidly declined over the past two decades. (See Figure 1.)

Figure 1

As some of these in-home providers exit the market, others may be transitioning to an “underground” market of unlicensed providers. These providers, which may be legally unlicensed depending on state statute, do not necessarily provide lower-quality care. But regulators cannot oversee the quality of care in these settings to the same extent that they can with those that are licensed. Parents who prefer in-home care over child care centers may be left with a difficult trade-off between accessibility of care and their confidence in a provider’s quality. Unfortunately, even parents who find an acceptable in-home provider could lose out on the subsidies that made their previous care arrangements affordable.

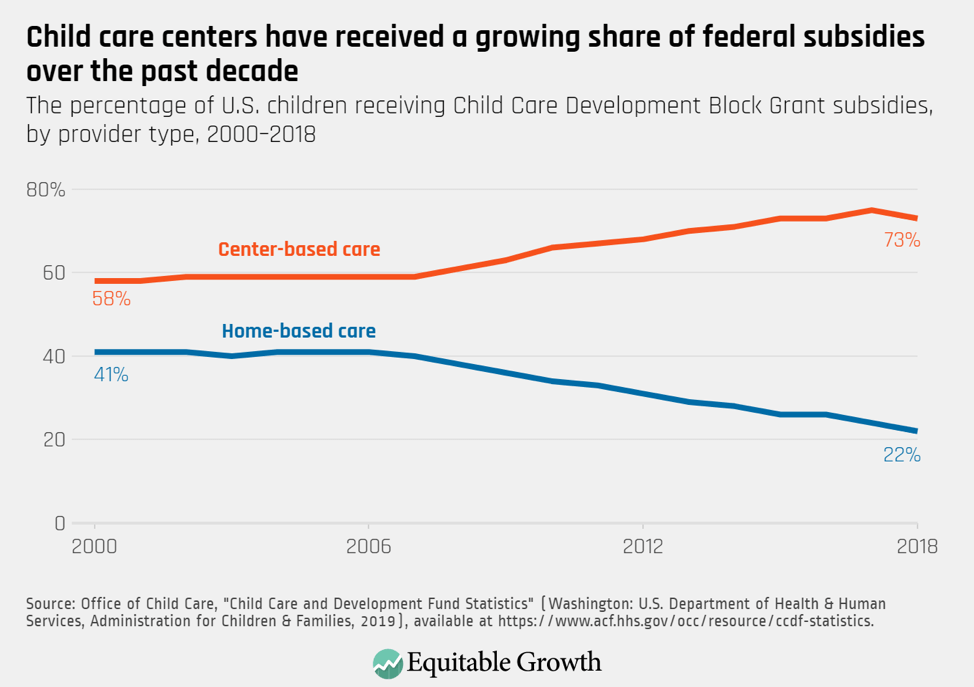

Child care can be incredibly expensive, even exceeding the cost of college in some states. Many families rely on some combination of tax credits or subsidies to help cover the cost. The Child Care Development Fund is the primary child care subsidy program for low-income families in the United States. When the program was reauthorized in 2014, it included important health and safety requirements for eligible child care providers but did not guarantee sufficient additional funds for states to enact these requirements. Experts say this has inadvertently advantaged child care centers, where states are better positioned to provide oversight and training.

Centers care for about 40 percent of preschoolers with a regular, nonrelative child care arrangement but serve more than 70 percent to 78 percent of similarly aged children receiving Child Care Development Fund subsidies. Conversely, in-home care serves 34 percent of similar preschoolers but around 18 percent to 25 percent of those receiving subsidies. This disparity in funding has dramatically widened in the previous decade. (See Figure 2.)

Figure 2

Reshifting subsidies toward these in-home providers is not a simple task. States will need to devote significant resources supporting in-home providers, particularly those that are exempt from licensing, to meet quality standards. Experts already worry that quality standards are too geared toward center-based providers and do not reflect the relative strengths and opportunities of in-home care. This could present an opportunity for high-level rethinking of what defines “quality” for these settings—a task for researchers as much as it is for regulators and policymakers.

Information on the spread of the coronavirus and COVID-19 and their effects on the economy changes rapidly. In the coming months, many families will be continuously reassessing their child care needs and what levels of risk are acceptable. The child care system, and the policies that help make it accessible to more families, must be flexible enough to meet parents’ needs without sacrificing quality or affordability. Unfortunately, these may be longer-term fixes in a system facing immediate shortfalls.

The supply of child care amid the pandemic is down, but parents are still searching for the care they need

These challenges in the U.S. child care market are longstanding, but they are now exacerbated by the coronavirus pandemic and COVID-19. More research is needed to understand how larger structural changes—such as additional subsidies or adjusted licensing standards—can be accomplished. In the meantime, the child care industry also faces an immediate critical shortage of providers who can care for the nation’s children once parents return to work.

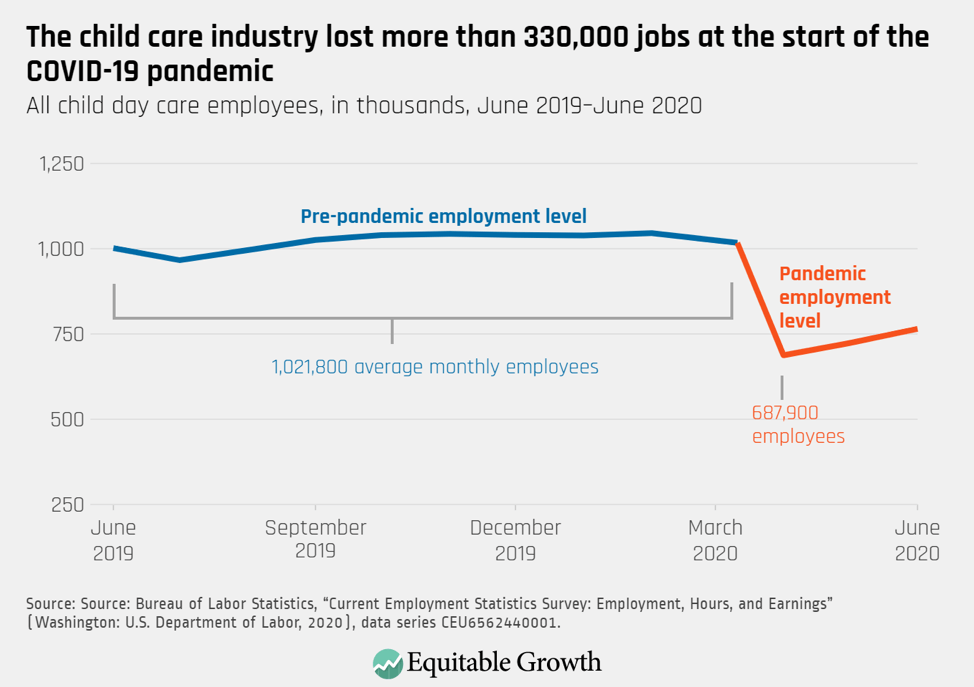

Like many industries, the coronavirus pandemic and resulting public health measures were shocks to the child care market. An April poll by the Bipartisan Policy Center found 60 percent of licensed providers shut their doors amid lockdowns and stay-at-home orders. More than 330,000 jobs were lost in the child care sector in only a few short weeks. (See Figure 3.)