This past March, as a coronavirus relief measure, Congress suspended payments on a lion’s share of federally owned student loans for 6 months. When this temporary loan forbearance expires on September 30, it should be extended—permanently.

Many borrowers will not be prepared to begin making payments that soon. But more importantly, none of these student loan borrowers should ever have to make another payment. Cancelling these debts would benefit the U.S. economy, reduce the massive racial wealth divide, and create new opportunities for a generation of college graduates whose hopes the economy has wiped out twice in a dozen years.

The Coronavirus Aid, Relief, and Economic Security, or CARES Act places federal student loans in administrative forbearance. That means debtors still owe their full debt but need not make any payments, and no interest will accrue on the loan during this period. It’s a good idea to provide relief to the more than 40 million borrowers in our country, many of whom face staggering levels of debts, not to mention helping to sustain an otherwise bleak economy by putting some money in the pockets of consumers.

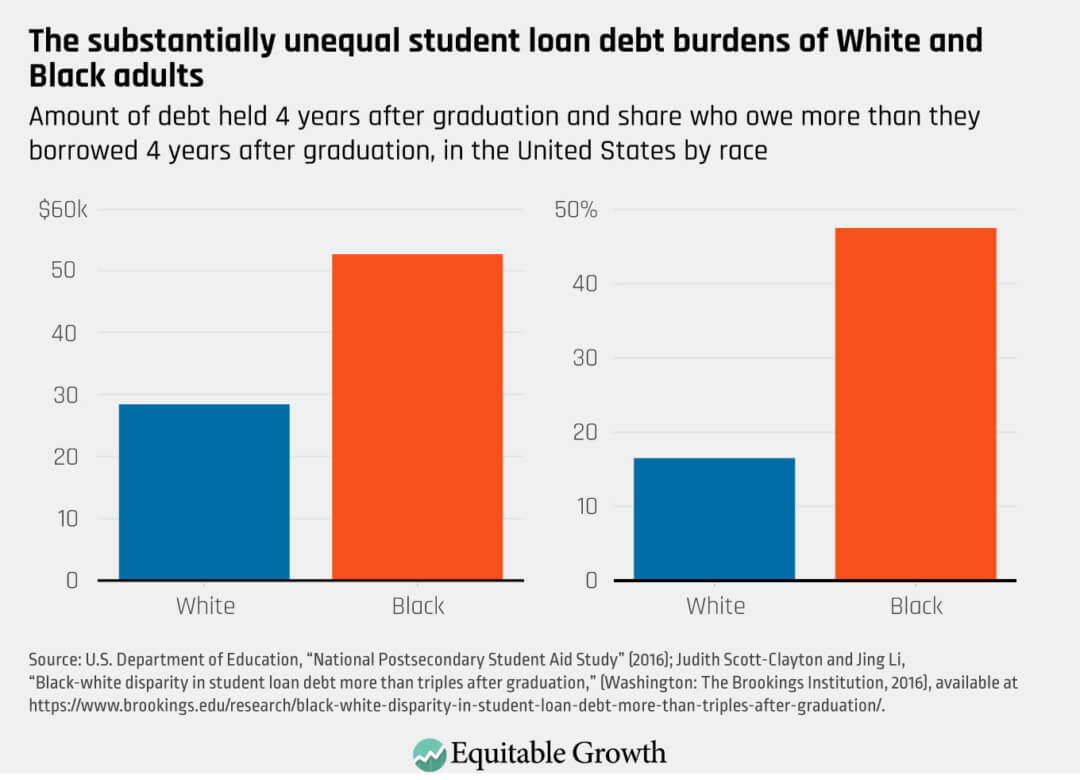

But this measure doesn’t go nearly far enough. This debt should not merely be suspended but cancelled entirely. Even before the coronavirus pandemic, federal student loan debt was crushing the financial and career aspirations of millions of borrowers. With college costs consistently rising faster than inflation and federal grant aid to students not keeping up, the aggregate amount of student debt is more than triple its level just 13 years ago—revealing the systemic nature of the trap created by a system of debtor’s education. Debt levels are especially high for Black students, who, 4 years after graduation, have an average obligation of more than $50,000, compared to less than $30,000 for the average White student. (See Figure 1.)

Figure 1

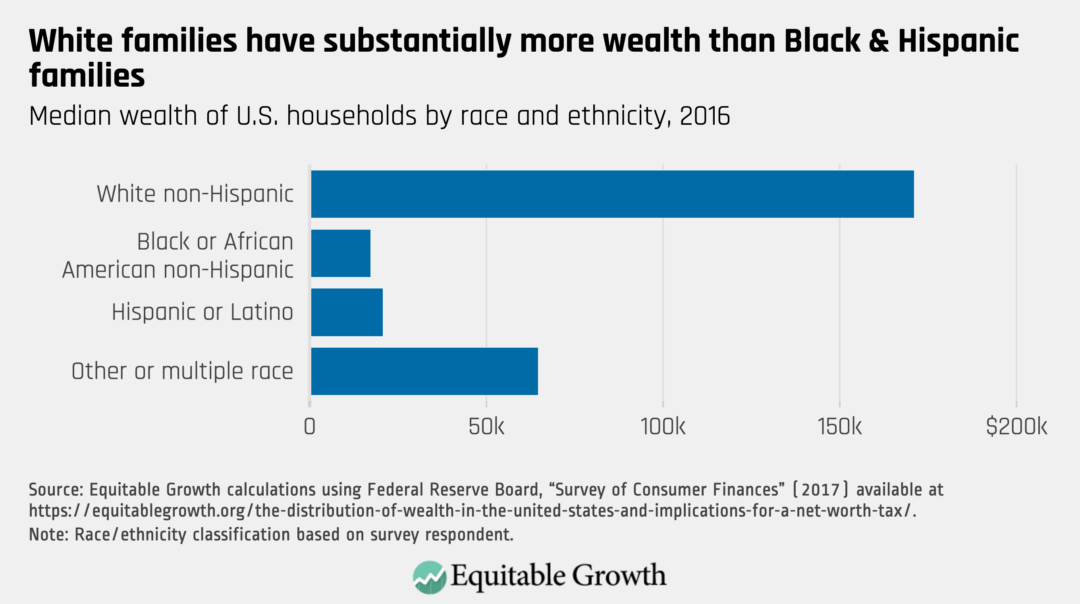

This higher debt load stems, in part, from the extraordinary gap in wealth between White and Black families. The median White household has 10 times the assets of the average Black family. (See Figure 2.)

Figure 2

Receiving less protection from parental wealth, Black students take on higher debt loads. Then, upon entering the labor market as young adults, these students face a harder time paying off their loans in a labor market characterized by racial discrimination. Evidence suggests that student debt has significant social impacts on the most vulnerable borrowers, including impeded family formation and poorer mental health. While student debt has conventionally been thought of as “good debt,” the investment generates widely disparate rates of return by race, given the prevailing social framework of unequal housing and Kindergarten through 12th grade education, predatory finance, and labor market discrimination.

The past decade and a half were especially cruel to college graduates. The scarring effect of the Great Recession of 2007–2009 is well-known. Those who graduated during that recession and immediately after will, on average, earn less throughout their careers. Yet, in part because of legislation permitting higher federal student borrowing, overall student borrowing began to skyrocket, surpassing credit card debt for the first time in 2010.

In addition, during the Great Recession, adults were encouraged to wait out the poor labor market and advance their career prospects by furthering their education. Many accrued more student loan debt but not all returned to the workforce with a degree or with the substantial improvement in earnings potential needed to pay off their debt. College costs are continuing to rise faster than overall inflation and federal grant aid is lagging, causing a significant portion of the millennial generation and its immediate successors to pursue adult lives with a millstone around their necks.

Cancelling student debt during the coronavirus recession and going forward with tuition-free universities would provide the greatest benefit to those who are suffering the most today. It is well-documented that people of color are contracting and dying from COVID-19 in numbers far out of proportion to their share of the population. Those service-sector jobs that don’t require a college degree, where Black workers and immigrants are overrepresented, are also less likely to provide access to insurance coverage or paid sick leave than other sectors. As the saying goes, when America gets a cold, Black people get the flu, but when America gets the flu, Black folks are far more likely to die. The anger we are seeing on the streets of cities across the nation is due not only to the violence imposed on Black Americans by discriminatory law enforcement but also is inextricably intertwined with social, educational, and economic injustices all created by the same society.

The concept of cancelling federal student debt is not a new one. Congress enacted loan forgiveness programs with Presidents George W. Bush and Barack Obama. The Bush program, initiated in 2007, focused on teachers and other public servants, as well as those working for nonprofit organizations, but it is exceedingly complex. Since loans became eligible for forgiveness in 2017, fewer than 3,400 borrowers have been approved for forgiveness, though nearly 200,000 have applied.

The Obama plan, which began in 2010, aimed at a far broader swath of borrowers. It enables borrowers to make payments based on a percentage of income. It also allows for cancellation of loans, but only after 20–25 years of payment. It is too early to tell how many borrowers will be aided by the cancellation element of the program, but, as with the Bush program, the Trump administration is showing that much can be done through administrative efforts to undermine this program’s intent by making it difficult for borrowers to qualify.

Cancellation of student debt was among the focal points of the recent Democratic Party presidential nomination campaigns. While some presidential candidates supported full student debt cancellation, former Vice President Joe Biden recently made a more modest proposal to forgive all undergraduate loan debt for borrowers who attended public colleges and universities, as well as historically Black colleges and universities, private minority-serving institutions, and for-profit colleges that disproportionately enroll Black students. Only those earning up to $125,000 would be eligible for forgiveness. In addition, Vice President Biden supports $10,000 in across-the-board loan forgiveness as a response to the coronavirus crisis.

There’s no question this proposal goes a long way and would cancel the loans of many millions of borrowers. Loan forgiveness, however, must be complete. Partial proposals—whether they limit the amount of cancellation, limit the source of debt to undergraduates, establish income ceilings, or distinguish between public and private institutions—leave us with the same mess of rules, income verification, and administrative burdens plaguing the previous, wildly ineffective attempts and will not protect young Black people seeking to use education as a tool for social mobility. Partial forgiveness would keep in place the unfair burden carried by this generation of borrowers, who were hit hard by higher debt and a double whammy of now-two recessions. Full cancellation is simple. It doesn’t pose administrative barriers, and it avoids the stigma associated with means testing.

Moreover, full cancellation leads naturally to what we consider to be the logical next step. Once Congress cancels all student debt, it should not stop there. Just as free public elementary education has effectively been a universal (though unevenly applied) economic right since the 19th century, free higher education should become the standard in the 21st century. Most young people have little choice but to pursue a college education if they wish to raise their socioeconomic standing beyond where they started out in life. And for many, higher education is a necessary step to earning a living wage. Providing tuition-free public higher education to all Americans would eliminate the social and psychological stigma associated with the current system of financial aid and eliminate the need for future generations to carry burdensome debts.

The coronavirus pandemic, the ensuing recession, and the community response to the police killing of George Floyd and far too many other Black Americans in 2020 and beyond bring into sharp focus the barriers American society places in front of today’s generation of Black students—barriers as old as our nation that continue to this day. Student loan debt exacerbates the challenges facing young Black Americans trying to establish careers and begin families. Eliminating this debt would be an important step toward reducing racial and economic inequality in the United States and bringing about the globally competitive, educated workforce that will unleash the country’s overall productive potential. As Congress and American voters facing a presidential election think about big solutions to America’s very big problems, this is one of the most important and effective actions we can consider.

The coronavirus pandemic and the ensuing economic recession have exposed and exacerbated many systemic inequalities in U.S. society, especially for Black and Latinx families. Even after a decade of growth following the end of the Great Recession in 2009, with low inflation and historically low unemployment, the U.S. economy before today’s crises was extraordinarily fragile, built upon a foundation weakened by rampant inequality.

The recovery from the coronavirus recession must be different from the previous recovery. The benefits of that recovery went largely to the wealthy and left the U.S. economy deeply vulnerable. To have a chance of emerging on a stronger footing, with less economic and racial inequality and more sustainable economic growth, policymakers need to respond with robust, evidence-based measures that attack the underlying problems causing inequality and help achieve economic security for all.

As part of our Vision 2020 initiative to ensure that the election-year economic policy debate focuses on big ideas grounded in the latest research, the Washington Center for Equitable Growth is hosting a webinar with top economic experts on June 25 to discuss the kind of bold policy initiatives that can help transform the U.S. economy. Titled “Vision 2020: Focusing on economic recovery and structural change,” the conversation will focus on how current finance, banking, and labor laws and institutions exacerbate economic and racial inequality, and what we can do to set the stage for strong, stable, and broad-based economic growth going forward.

The webinar will feature two panels. The first, “Democratizing the Economy,” will focus on the need for new or drastically reformed institutions to address how financial institutions and the Federal Reserve have exacerbated inequality. The second, “Building Power for Workers and Families,” will describe how enhanced collective bargaining rights, public benefit and social insurance programs, anti-discrimination protections, and other power-building policies can help Black, Latinx, and other workers emerge stronger from these crises.

The June 25 event is scheduled for 2:00 p.m. – 3:30 p.m. EDT. Click here to register.

After the Great Recession of 2007–2009, when the U.S. economy lost 8.7 million jobs and $12 trillion in total household net worth, one group emerged stronger than ever: the wealthiest 1 percent, who took only a few years to regain most of what they had lost. When the coronavirus crisis hit earlier this year, middle-class families were still recovering from that devastating shock 10 years earlier. To avoid a similar outcome, Boushey and Equitable Growth’s Somin Park have laid out principles for policies that can support the right kind of economic recovery. These principles, which underlie the ideas to be discussed in the upcoming webinar, are:

Recognize that markets cannot perform the work of government. As we see today, allowing markets to determine outcomes, while pretending that the rules that govern markets are always neutral and fair, has shifted economic risk toward individuals and families, especially those in communities of color, and away from wealthy institutions.

Address fragilities in our markets themselves. To prevent further corporate concentration across industries, policies must ensure the stability of U.S. small and medium-sized businesses. Black-owned businesses have been especially hard hit and urgently need support to survive.

Keep income flowing to all the unemployed workers and to small businesses now and in future crises. To strengthen the resiliency of families, businesses, and the economy, direct payments, Unemployment Insurance, small business grants and loans, robust aid to states, and emergency paid leave should be continued until the coronavirus recession passes.

Ensure those who are still employed can stay employed. To ensure that businesses do not become hotspots for transmitting the coronavirus, adopt widespread testing and tracing and provide protective gear to essential, front-line workers and others as necessary.

Produce headline economic statistics that represent the well-being of all Americans. To understand how the coronavirus recession and eventual recovery affect all Americans and make policy to ensure a broad-based recovery, measure not only average income growth or decline through Gross Domestic Product but also income changes up and down the income and wealth ladders and across demographic groups.

These principles also are consistent with the policy proposals contained in the book and conference that kicked off Equitable Growth’s Vision 2020 project, both titled Vision 2020: Evidence for a Stronger Economy. Taken together, the ideas contained in the book’s 21 chapters form the backbone of what could be an agenda for equitable growth in the third decade of the 21st century. Hertel-Fernandez, Morrissey, and Zewde authored or co-authored three of the chapters. Their proposals, which respectively address labor law reforms, early childhood care and education, and student-loan debt, will be discussed on Thursday in the context of recovery from the coronavirus recession. For summaries of those chapters, Equitable Growth is today publishing a Vision 2020 backgrounder focused on the coronavirus recession, which can be found here.

The health, economic, and social effects of the coronavirus pandemic and the ensuing recession have helped make the case for the kinds of big, bold ideas that are the basis of the Vision 2020 initiative. Join us on June 25 as some of the nation’s top scholars connect the dots between our current, multifaceted crises and the future structural change we so desperately need.

In March, the federal government passed the Coronavirus Aid, Relief, and Economic Security bill, more commonly known as the CARES Act. The law aims to provide relief for businesses and Americans struggling due to the coronavirus pandemic and the resulting economic recession. It also had the potential to accelerate the fight against another crisis—climate change—by funding a green stimulus to accelerate the clean energy transition.

The coronavirus and climate change are, unfortunately, linked. Air pollution from dirty energy infrastructure makes people much more likely to die from COVID-19, the disease caused by the coronavirus. And those dying in the United States are more likely to be people of color, perhaps in part because of environmental injustices that expose communities of color to much higher pollution levels.

We do not have to use dirty energy that damages peoples’ lungs to power our societies. The CARES Act could have helped protect Americans’ health during this pandemic by moving us away from polluting fossil fuels. Yet rather than supporting clean energy, the law is being used to bail out the dirty fossil fuel sector.

If we continue along this terrible path, the accelerating climate crisis will disrupt employment, cause property damage, and destabilize the financial system. Why use the rescue programs from the current crisis to subsidize the industry most likely to cause the next one?

This issue brief examines how the CARES Act was deliberately misapplied to the fossil fuel industry, which was already on the ropes before the coronavirus recession. We also examine how future stimulus funds could be targeted toward clean energy, which would create more and better-paying jobs to power our economic recovery. This approach would not just help us tackle the coronavirus recession, but the climate crisis as well.

The fossil fuel industry was in crisis before the coronavirus hit

Many fossil fuel companies were already struggling before this economic crisis. Since President Donald Trump entered the White House, 11 coal companies have declared bankruptcy. To try to buck this trend, the Trump administration has found creative new ways to distort power markets to advantage coal.

Similarly, shale gas and oil companies have been struggling under high debt levels and underperforming investments. The massive global petroleum glut has only added to their woes. These hard times led carbon-intensive companies to seek refuge in bailouts when the coronavirus recession hit.

Unfortunately, the CARES Act is funding corporate welfare for polluters. The law allows the Federal Reserve to lend money to companies. In theory, these companies should be doing well enough that they are able to pay the government back. But for oil and gas companies, this may not be the case. Given very low oil prices, these companies do not have a clear pathway toward profit. Many are highly leveraged and were already struggling with credit-rating downgrades by the end of 2019. This debt burden would have initially made many oil and gas companies ineligible to receive Federal Reserve loans.

Yet after taking comments, including from the fossil fuel industry, the Federal Reserve watered down their requirements for lending. Oil and gas companies, even with their pre-existing debt, have become newly eligible. In addition, the maximum lending amount was raised from $150 million to $200 million.

Notably, U.S. Secretary of Energy Dan Brouillette said in mid-April that lending would need to be “closer to $200 or $250” million to help the fossil fuel sector, after he met with representatives from the industry. While the Trump administration has been meeting regularly with fossil fuel groups, it has not done the same for the renewable energy industry.

Some commentators have called for federal government ownership or equity stakes to be a conditional requirement for lending to the oil and gas industry, even though the CARES Act prohibits the federal government from exercising any voting power if a government financial investment takes the form of an equity stake. This clause needs to be amended to enable the federal government to influence these corporations, ideally helping to put them on a path toward reducing their fossil fuel extraction and carbon emissions. The Trump administration, however, has clarified that it has no intention of taking ownership stakes in fossil fuel companies.

Instead, fossil fuel companies have been using the coronavirus recession to try to secure immunity against lawsuits for their decades promoting climate denial. In response, 60 members of the U.S. House of Representatives recently wrote a letter opposing liability relief. These disturbing developments are not just happening federally. Across the country, fossil fuel companies and state and local governments are using this crisis as an opportunity to weaken environmental regulations.

What’s more, publicly traded coal companies have received more than $31 million as part of the law’s Paycheck Protection Program, which is designed to go to small businesses, not publicly traded companies capable of other ways of raising cash. The coal industry was initially left out of the package but successfully persuaded the Trump administration to list it as essential. Similarly, Marathon Petroleum Corporation has received more than $400 million from the CARES Act.

Environmentalists have criticized these loans as throwing good money after bad because the coal industry was already struggling financially in recent years. They’re right. These are bad economic investments. Bailing out fossil fuel industries will not yield as many jobs as investing in clean energy would.

A green stimulus can lead an economic recovery

Every dollar spent propping up a dying industry is a dollar that can’t be invested into new careers, training, opportunity, and equitable growth in the clean energy sector. Increasingly, even banks recognize this, as more and more are pulling out of fossil fuel investments that are yielding poor returns.

According to recent research from Heidi Garrett-Peltier, an assistant professor at the University of Massachusetts Amherst, for every $1 million invested in renewable energy or energy efficiency, almost three times as many jobs are created than if the same money were invested in fossil fuels. Investing more money in the fossil fuel industry will not address high and growing unemployment rates. Indeed, the Federal Reserve is not even requiring companies to keep workers as a condition for getting loans.

The seeds of an even more perniciousargument are already sprouting. Some conservative members of Congress are raising concerns about rising federal debt levels and threatening to stop further spending on relief amid the still-deepening recession. This would be the worst of both worlds. With $1.8 trillion in direct spending, the CARES Act is larger than Vice President Joe Biden’s 10-year climate plan. Clearly, the United States is able to spend more money addressing climate change if we treat it as the crisis it is.

We need green stimulus investments because it’s a smart way to spend money. Investments in the clean economy will provide significant returns. As Nobel prize-winning economist Joseph Stiglitz argues, alongside other colleagues, renewable energy and energy efficiency investments typically have high multipliers, delivering even greater returns over time. They also create more jobs, including ones that can’t be taken offshore, such as those in home energy retrofits.

At the end of 2019, Congress had an opportunity to put extensions for basic supports of the green energy sector into place, among them the Investment Tax Credit and the Production Tax Credit, in the year-end budget bill. But Congress decided against it. Congress then could have put these extensions in the CARES Act, but both President Trump and Senate Majority Leader Mitch McConnell (R-KY) opposed it.

This lack of support immediately before and during the coronavirus recession leaves the the renewable energy sector struggling. This quarter, for example, residential solar installations are likely to fall by half. In March alone, the clean energy industry lost more than 100,000 jobs. In wind energy alone, $43 billion in investments are at risk. Despite the terrible state the industry finds itself in, Congress is doing very little to support clean energy jobs.

Conclusion

Despite a complete economic shutdown, global carbon pollution has only declined 5.5 percent so far this year. It may fall as much as 8 percent by year end, marking the largest annual decline on record. But to limit global warming to 1.5 °C (2.7°F), emissions must fall by that amount every year for the next decade. This will not happen without concerted government policy.

Instead, U.S. policymakers could power an economic rebound and prepare to meaningfully address climate change by investing stimulus funds in the renewable energy sector. If the Great Recession of 2007–2009 is any indication, temporary emissions reductions from economic contractions quickly reverse themselves. We should learn a lesson from the previous recession and the current one—ignoring a crisis does not make it go away, be it the coronavirus pandemic or the growing climate threat.

Leah C. Stokes is an assistant professor at the University of California, Santa Barbara. Her recent book,Short Circuiting Policy, examines the clean energy transition.

Matto Mildenberger is an assistant professor at the University of California, Santa Barbara. His recent book,Carbon Captured, examines carbon pricing and climate policy.

The coronavirus pandemic has placed the opportunities and challenges of our intensely integrated world economy in stark relief. The movement of people across borders generates fear of contagion. And the reliance on foreign countries for crucial medical supplies needed in the United States creates fears of dependence. Yet these fears can be managed without forsaking the substantial benefits that arise from global cooperation, trade, and the flows of knowledge and people across national boundaries.

The challenges of global pandemics require preparation, not isolationism.

It is unquestionable that the United States is dependent on medical supply chains that stretch across countries. We both import and export large quantities of pharmaceuticals, medical equipment, and medical supplies. Worldwide, the United States is the largest importer of medical products and the second-largest exporter of medical products.

In general, trade in these goods is spread across many countries. Germany and China account for about 11 percent and 9 percent, respectively, of our imports of these goods, and many other countries play important roles. Still, there are some products, such as personal protective equipment, where trade is more concentrated. In 2019, China, Germany, and the United States together accounted for nearly half of the world supply of protective face masks.

The coronavirus pandemic has brought forth impressive international collaborations. But it has also resurrected misguided policy instincts, exposing three important fallacies.

Export restrictions will not protect the United States

One fallacy is that export restrictions will keep important medical supplies in the United States. The problem is that the United States, alongside about 70 countries, all have sought to protect their own access to medical supplies by prohibiting exports of medical equipment and supplies. Just one case in point: The Trump administration threatened to cut off Canada and Latin America from mask supplies through the authority of the Defense Production Act before the administration and U.S. conglomerate 3M Company eventually negotiated the ability of 3M to serve both U.S. and export markets.

Indeed, many countries have banned crucial medicine and personal protective equipment exports, disrupting the supply of key products that are needed everywhere and reducing lifesaving gains from trade that would otherwise be possible due to the variation across countries in peak need. Export restrictions during pandemics are a near perfect example of a prisoner’s dilemma. From one country’s perspective, it may be optimal to restrict your exports, regardless of what your trading partner does. Yet if every country restricts exports, then it reduces the gains from trade for everyone—and risks humanitarian disaster in the many countries without native medical supplies industries.

As we’ve learned through recent experience with the Trump administration’s trade wars, retaliation to protectionist trade measures is nearly inevitable. As the United States levied tariffs on our trading partners, other countries responded in kind, generating disruptive shocks that negatively impacted workers throughout the U.S. economy. Further, the United States entered this crisis with large tariffs in place on medical equipment, including PPE (those tariffs were not removed until March 17), a severely weakened rules-based international trading system, and a sense of distrust and wariness among key allies. This was not a good starting point.

The United States does not need to pursue self-sufficiency

Undeniably, the United States is also an importer of important medical equipment and supplies, and like other countries, we are dependent on others. But the answer to dependency is not self-sufficiency, which risks cutting off the United States from the benefits of specialization and trade.

Instead, the United States should prepare for future pandemics and other disasters by identifying key medical products and stockpiling sufficient supplies to guard against supply interruptions or spikes in demand. This would also enable our nation to help other countries when disasters befall them—of course, replenishing the stockpile with an eye toward the future. Preparation is wise, yet responding with protectionism or “buy America laws,” such as those contemplated by the Trump administration, risks weakening the U.S. medical industry.

These measures are rightly protested by patient advocacy groups. The U.S. medical industry will best thrive by meeting the test of global competition, employing the cost effectiveness of global supply chains, diversifying supply chains as needed to ensure resilience, and benefitting from the ideas of the world’s scientific community. An open system best serves the health of the U.S. medical and pharmaceutical industries and the future of the world’s scientific progress.

Global integration did not make the coronavirus pandemic worse

A third fallacy is that global integration made this crisis worse. Pandemics easily cross borders in times of economic isolationism, war, and in much more domestically oriented economies. The 1918–1919 “Spanish” flu is one famous example, in which these factors amplified the pandemic.

Today’s coronavirus pandemic will be far less deadly than those of a century ago because of the myriad benefits of global knowledge accumulation and scientific progress. Importantly, movements of people are an essential part of scientific discovery. Cutting-edge research teams operate across national borders, and flows of international scholars spread ideas. Of the Nobel prizes in scientific fields in recent decades, a majority were earned by United States-based researchers, but a majority of those winners were foreign-born U.S. residents.

While temporary travel restrictions are a necessary step to slow the spread of the coronavirus, these restrictions should not become the new normal. Both sender and receiver countries have too much to lose if we stem international flows of students, scholars, researchers, and migrants. While the Trump administration has taken the present crisis as yet another opportunity to lash out against immigrants, they remain a substantial source of strength for the U.S. economy.

The right way to deal with the coronavirus pandemic and global trade

So, what can we learn from this crisis? The failures of the present situation illustrate three lessons vividly.

First, international organizations such as the World Health Organization and the World Trade Organization have a crucial role to play in overcoming international collective-action problems, sharing information, and promoting cooperative solutions. These institutions should be nurtured, not threatened. It was stunning to witness the collaborative efforts of the WHO, the Gates Foundation, and the European Commission, announcing a global vaccine effort that would not prioritize any particular country at the very same time that the U.S. government was not just absent from world leadership, but conspicuously suspending financial contributions to the World Health Organization.

Second, even (and especially) in a pandemic, global flows of people and goods generate widely shared benefits. Global talent flows enhance international discovery and scientific progress. The gains from trade can be lifesaving during a pandemic. And, preparation can protect us from the vulnerabilities that these international flows may generate. People flows may need to be curtailed during a pandemic, but scaling up testing and tracing techniques will allow people movements to resume more swiftly after the pandemic ebbs, and we can learn from other countries that have done just that. Possible vulnerabilities due to disruptions in supply chains can be countered by stockpiling key supplies and taking steps to make sure that any crucial items are provided by multiple sources.

Of course, as I’ve written for in both Equitable Growth’s Vision 2020 project and elsewhere, while international markets come with immense benefits, we should also be careful to respond to the downsides that affect U.S. workers. Both during and after the crisis, U.S. policymakers need to put workers at the center of our policy efforts, pursuing progressive reforms to our tax system, our trade agreements, and our safety net.

Third, and most important, this crisis illustrates the primary importance of quick, serious domestic actions and responses. Threats to our nation’s public health must be monitored and responded to on a timely basis. The full authority of the federal government is needed to ramp up production and testing. And a fully functioning federal effort is required to better coordinate the movement of resources to the areas with the greatest need. So far, among U.S. states, the lack of effective federal coordination has increased prices and worsened shortages.

In all of these areas, the inaction of the Trump administration as the coronavirus spread demonstrates the dangers of ill-prepared leadership. Future crises require better leadership, and they also require a spirit of international collaboration and openness. This coronavirus pandemic is not the only serious crisis that crosses borders. Confronting climate change, nuclear proliferation, and other serious threats requires a strong network of alliances, well-functioning international organizations, and rules-based systems for handling disputes. In all of these areas, the United States can do much better in the years ahead.

When U.S. policymakers seek to restore the U.S. economy in the wake of the coronavirus recession, what will constitute success? Returning the economy to its prepandemic state is not sufficient. It’s not even desirable. Yes, unemployment was low, and job growth was strong. But that economy was also characterized by pervasive economic inequality, low productivity, and inflated asset prices. That economy was being kept afloat mainly by the Federal Reserve’s policy of maintaining a historically low rate of interest.

The Fed was forced into keeping interest rates low by years of misguided fiscal policy. When it was convenient, the need to control budget deficits was made the highest priority and used as an argument against the kind of investments that build a strong economy. Yet the deficit became irrelevant when tax cuts, especially tax cuts for the wealthy, were on the table. As policymakers seek ways to recover from the coronavirus recession, we will need to do more than just provide healthcare and replace lost incomes until the economy is “back.” The focus of fiscal policy during this recovery should be to invest—and invest a lot—in human capital, infrastructure, and scientific research.

When the coronavirus hit the U.S. economy hard in March, conventional wisdom had it that the economy was as strong as it had been in generations, with low unemployment and a thriving stock market, and that it took a global pandemic to bring it down. Some leaders, and too often the media, use the stock market as a proxy for the strength of the economy. But that is a symptom of what was wrong with our economy and economic policymaking before the new coronavirus hit our shores, spreading the COVID-19 disease in its wake—and what we need to avoid in policymaking going forward.

The new U.S. economy that policymakers should aim for also should feature low unemployment, achieved through higher productivity created by public and private investments powering broad-based growth. The new economy should create well-paying jobs with strong benefits for the many, not the few. The gap in benefits such as paid sick days and family leave is clearly evident amid this continuing public health crisis. The new economy should be stronger and more resilient than anything we saw in the decades leading up to this crisis, providing policymakers understand their past mistakes and do things differently going forward.

What, specifically, do policymakers need to do to achieve this new economy? First, some context.

The Federal Reserve lowered interest rates at the onset of the Great Recession and has kept rates near zero for most of the time since. In fact, the Fed discount rate has not been this low for a sustained period in about 70 years. This is partly due to market trends and partly a result of explicit monetary policy. Keeping in mind that interest rates are essentially the price of borrowing money, downward pressure on rates was a result of slow productivity growth, which reduces the demand among businesses for credit so they can invest, and an aging population, which increases the supply of saving. These two factors have a number of important implications, including:

The Fed’s traditional weapon for combatting recessions—lowering interest rates by several points—is depleted. Practically speaking, you can’t lower interest rates much below zero.

The return to risk-free saving was reduced. This affected individual savers seeking to secure their retirement savings, as well as institutional investor funds that support guaranteed pension benefits and other forms of annuities. These investors were forced to take greater risks to get positive financial returns or save even more, both of which pose challenges to the economy.

Lower interest rates reduced borrowing costs for corporations, and they took on excessive debt, including to enrich their shareholders by buying back corporate stock. Stock prices (and other asset values) were overvalued using conventional measures such as the Buffet Ratio, and thus were highly vulnerable to shocks.

While financial markets exerted downward pressure on interest rates, the Fed was forced, before the coronavirus recession, to accommodate that downward pressure to keep the economic recovery on course. And the reason was wrongheaded U.S. fiscal policy. Better fiscal policy, emphasizing federal investment over tax cuts, would have led to higher productivity and a stronger economy. This would have made it possible for the Fed to conduct better monetary policy, meaning the Fed could achieve full employment and stable inflation—the U.S. central bank’s “dual mandate”—without the inherent financial market valuation issues and instability associated with artificially low interest rates.

Since the 1980s, the narrative that has governed U. S. fiscal policy has been that budget deficits are bad for the economy, and they are caused by excessive spending. Tax cuts are always good for the economy. And what about the deficits they create? Deficits caused by tax cuts are okay, and anyway, tax cuts pay for themselves—or so goes the supply-side argument. As we know, the latter argument has been disproven time and time again.

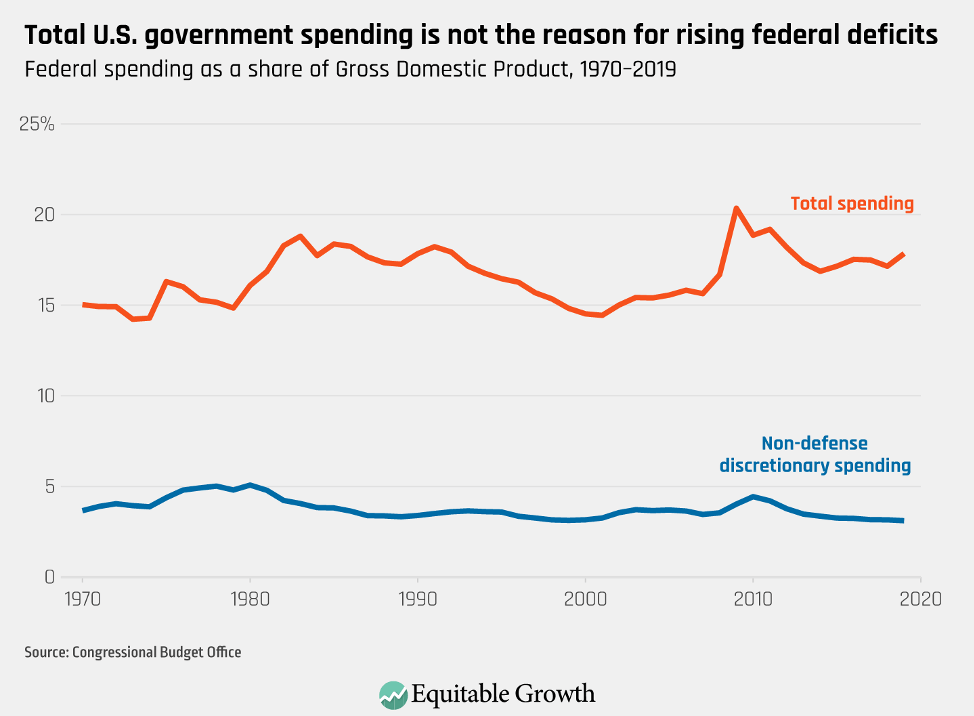

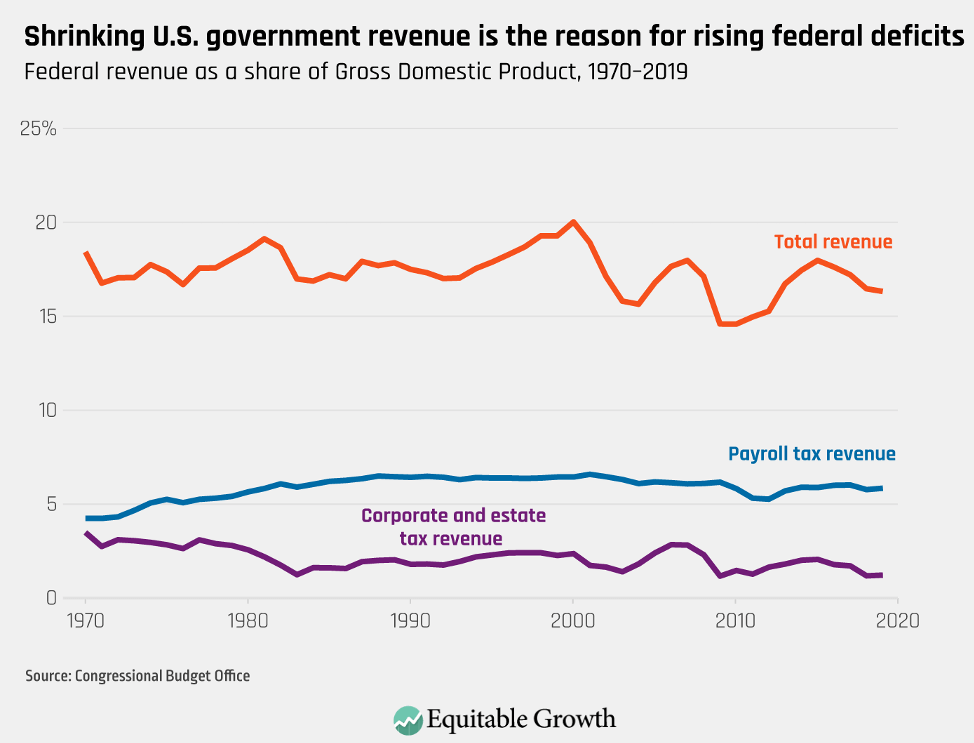

Indeed, examining the composition of federal spending and the composition of federal revenues relative to Gross Domestic Product over the past few decades provides a high-level, evidence-based perspective on this mistaken supply-side narrative. The data clearly reject that narrative that increased government spending is the primary reason for rising government deficits in recent years. Total spending, at about 20 percent of GDP in 2019, is close to its 50-year average. (See Figure 1.)

Figure 1

In contrast, total federal revenue relative to GDP, at 16.5 percent in 2019, is historically low. The previous time the economy was comparable to what we experienced in 2019, at the end of the 1990s, revenues were 20 percent of GDP. (See Figure 2.)

Figure 2

A closer look at the composition of spending in Figure 1 cuts further against the mistaken narrative about rising government spending. The component of spending associated with direct government intervention in the real economy—nondefense discretionary spending—has fallen as a share of GDP in recent decades. The fastest growing categories of outlays are for programs such as Social Security, Medicare, and Medicaid, all of which are generally financed by payroll taxes on the same low- and moderate-wage earners who are the primary beneficiaries.

The increase in payroll taxes used to fund these programs is evident in Figure 2. Thus, another crucial takeaway from this high-level perspective is that the overall decline in total revenues relative to GDP is because corporate, estate, gift, and income taxes have fallen even more than payroll taxes have increased. Deficits are primarily the result of the wealthy and corporations paying less in taxes, not due to workers receiving social insurance benefits for which they are not paying.

Most analysis of fiscal policy focuses on the economic effect of deficits, without regard for why the deficits were created. The trends in the composition of U.S. spending and revenue shown above suggest that all deficits are not created equal. A deficit created by increased nondefense discretionary spending focused on investments in human capital, scientific research, and infrastructure has positive effects on aggregate demand and boosts productivity. Such policies have the potential to reverse the downward pressure on interest rates.

A deficit generated by reducing taxes on capital incomes, in contrast, has only short-run effects on aggregate demand, mostly through increased asset prices. Indeed, the effect of such fiscal policies is to reinforce a low-interest-rate equilibrium because the after-tax return from owning stock is higher. Yet experience with those sorts of policies over the past two decades shows they do not lead to the sorts of investments that will make the U.S. economy grow and help alleviate the downward pressure on interest rates.

Most of the policy discussion about taxes in the United States involves the negative consequences of taxing some positive outcomes, but policymakers need to remember that those positive outcomes are sometimes, in large part, the payoff on public investments. Our federal tax system is increasingly allowing those who have benefitted the most from public investments in science and technology to pay less in taxes. Simply restoring the tax system to where it was a little more than two decades ago, as proposed by Owen Zidar of Princeton University and Eric Zwick of the University of Chicago, would allow us to make the sorts of investments we need to make without deficits.

The recent history of U.S. fiscal and monetary policies suggests that bad fiscal policy and constrained monetary policy increasingly reinforced each other in recent decades. This mutual reinforcement contributed to a slowdown in overall U.S. economic growth before the coronavirus recession alongside rising income and wealth inequality and financial instability. Fiscal policymakers have abdicated their responsibility to make the investments in people, technology, and infrastructure that private investors cannot and will not make.

So, what now? When we restore the economy from the ravages caused by the coronavirus recession, we should be guided by the lessons we’ve learned in recent decades and build an economy characterized by strong, stable, and broad-based growth. If U.S. policymakers had been investing properly, for example, then right now there would be federally funded infrastructure projects in place for workers to get back to once the threat of COVID-19 diminishes. Instead, many of the infrastructure investments we might commit to now will take months or years to get underway. They’re still worth doing, but earlier investments could have supported a more speedy economic recovery now.

Today, policymakers need to focus on spending to support healthcare, maintain incomes, and keep businesses alive—and, as businesses start operating again, restore aggregate demand. But to get to the kind of strong, stable, and broad-based economic growth our nation needs, the federal government needs to invest. We need to invest in human capital—in quality childcare and early childhood education, in Kindergarten through 12th grade education, in vocational and higher education, and in programs to alleviate hunger and poverty.

We need to invest in infrastructure—in maintaining, repairing, and building our roads and bridges and mass transit systems, in enhancing the quality and security of our water systems, in preparing for and alleviating the baleful consequences of climate change, and, at long last, building rural broadband—the lack of which is freezing millions of rural Americans out of the modern economy.

And policymakers need to invest in fundamental scientific research, the lifeblood of our innovation economy and health advances. We need to invest in the National Institutes of Health, the National Science Foundation, and the other agencies supporting the basic research that has made possible everything from our smartphones to MRIs, from global positioning systems to the vaccine research we rely on today to fight the new coronavirus and COVID-19.

Tax cuts are decidedly not the answer. They double down on inequality. Most of the time, they favor the wealthy over everybody else. And the payroll tax cut now under discussion within the Trump administration and among conservative policymakers and pundits would likely just undermine Social Security finances without providing the direct infusion of funds workers and businesses need to survive the sharp economic downturn and then recover.

Although better U.S. fiscal policy is the key to better monetary policy, there are some monetary policy principles the Fed can and should embrace as it battles the coronavirus recession. Economic shocks generally involve both financial effects and real effects in the economy, with the wealthy experiencing declines in their net worth but the less wealthy experiencing job losses. In the past, the Fed has focused on propping up the financial system—for example, bailing out mortgage lenders but not mortgage borrowers during the Great Recession.

The Fed needs to expand its policy purview if the fiscal authorities won’t act in the interests of all the people. The U.S. central bank needs to make sure the next round of quantitative easing—Fed speak for the central bank’s purchase of financial securities in the marketplace to boost liquidity in the economy—or other extraordinary monetary policy action do not simply rescue the corporations whose past decisions created financial vulnerabilities.

U.S. policymakers need to enact and implement the fiscal and monetary policies tools needed to fight the coronavirus recession and prepare for a more equitable and thus more sustained economic recovery. They can and must build an economy that, unlike the one we just left behind, is built on strong, stable, and broad-based economic growth.

The U.S. economy is infected by the coronavirus pandemic, and a deep recession is practically inevitable. Congress and the Federal Reserve will lead the effort to fix the economy with fiscal and monetary stimulus, but state and local governments, too, have an important role to play.

Even the massive $2.2 trillion stimulus package passed by Congress last week is unlikely to offset the imminent collapse in spending across the country by consumers and businesses alike. Although states and localities cannot run deficits due to balanced budget requirements, they still control many policy levers that influence spending. To supplement whatever boost the national government can provide, states and localities can stimulate their own economies significantly by adjusting laws and regulations to promote spending, which, in turn, will help the U.S. economy overall recover more quickly.

Here are two detailed examples of how state and local governments can stimulate spending by promptly changing how utilities are regulated and how building construction is restricted, followed by three more short examples. (For more suggestions, see my book on legal remedies to recessions and my essay in the book the Washington Center for Equitable Growth published earlier this year, Vision 2020: Evidence for a stronger economy, for a range of federal, state, and municipal policy ideas.)

Implement countercyclical utility regulation

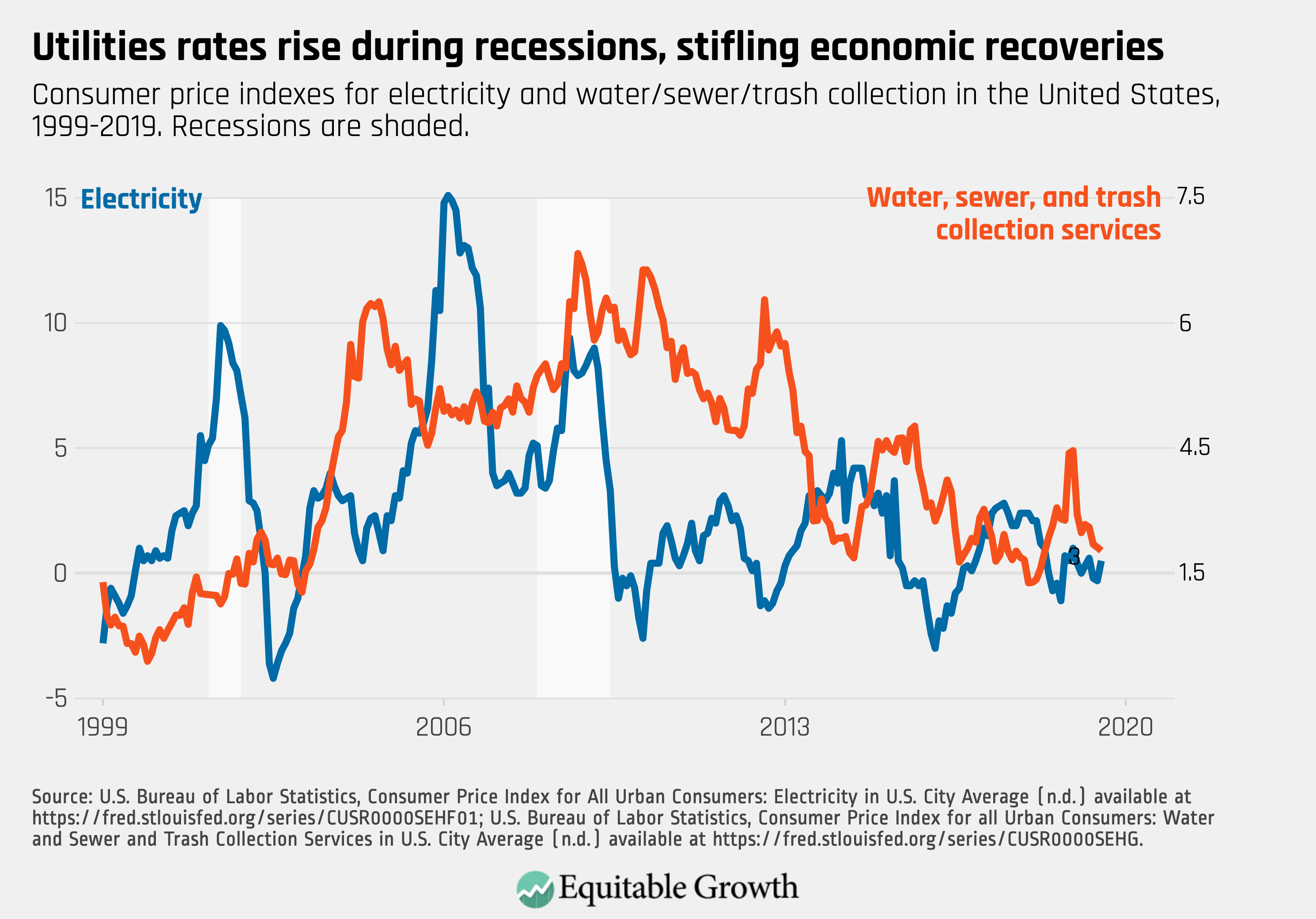

States can lower the financial burden that utilities—gas, electricity, and water companies—impose on consumers during the recession. States guarantee utility companies a nearly fixed profit, no matter how gloomy the economic situation. This legislative guarantee insulates utility profits from economic downturns, worsening recessions. That effect occurs because, at present, utility regulation aims to give utilities a median rate of return of approximately 10 percent a year every year. In good economic times, demand for utilities is high. This means that the utility can earn 10 percent without charging a particularly high price. In recessions, however, demand for utilities falls. For a utility to earn 10 percent in a recession, it needs to raise prices.

A utility regulator aiming to keep annual utility returns constant, as most regulators do, will consent to a rate increase. This pattern of regulation explains why utility prices have increased markedly during the previous two recessions. (See Figure 1.)

Figure 1

This regulatory practice reflects disastrous economic policy. Utility investors, who are insulated from recessions by regulation, are relatively affluent and have access to capital markets. They can easily borrow or sell assets in order to keep up spending in response to a downturn in income. Many or even most utility customers, by contrast, live paycheck to paycheck. Utility costs swallow 10 percent or more of many U.S. workers’ income, and when those costs rise during recessions, low- and medium-wage workers cut spending on everything else, exacerbating the recession.

In recessions—in other words, right now—regulators should lower the guaranteed profit that utilities make. Doing so would increase consumer discretionary income, just like a tax cut. In good times, regulators should permit utility prices to increase, so that utilities earn a fair, risk-adjusted return over the course of the business cycle. This approach, which is already implemented by Chinese utility regulators, would leave consumers with more money during lean times and would increase rates modestly when consumers can actually bear the increase.

Extra consumer spending is unnecessary when the economy is healthy. But that spending is critical when times are lean. Letting utilities profit more during boom times and profit less during lean times—just like nearly any other business—could mitigate the coronavirus recession without harming utility investment. Reducing utility rates by 10 percent over the next 2 years would leave more than $400 in the pockets of consumers. A target profit-rate that exceeds 10 percent could be guaranteed for 3 years or 4 years out, which would guarantee utilities a fair rate of profit over the course of the business cycle rather than year by year—and would pump some adrenaline into the national economy.

Support construction by easing zoning rules

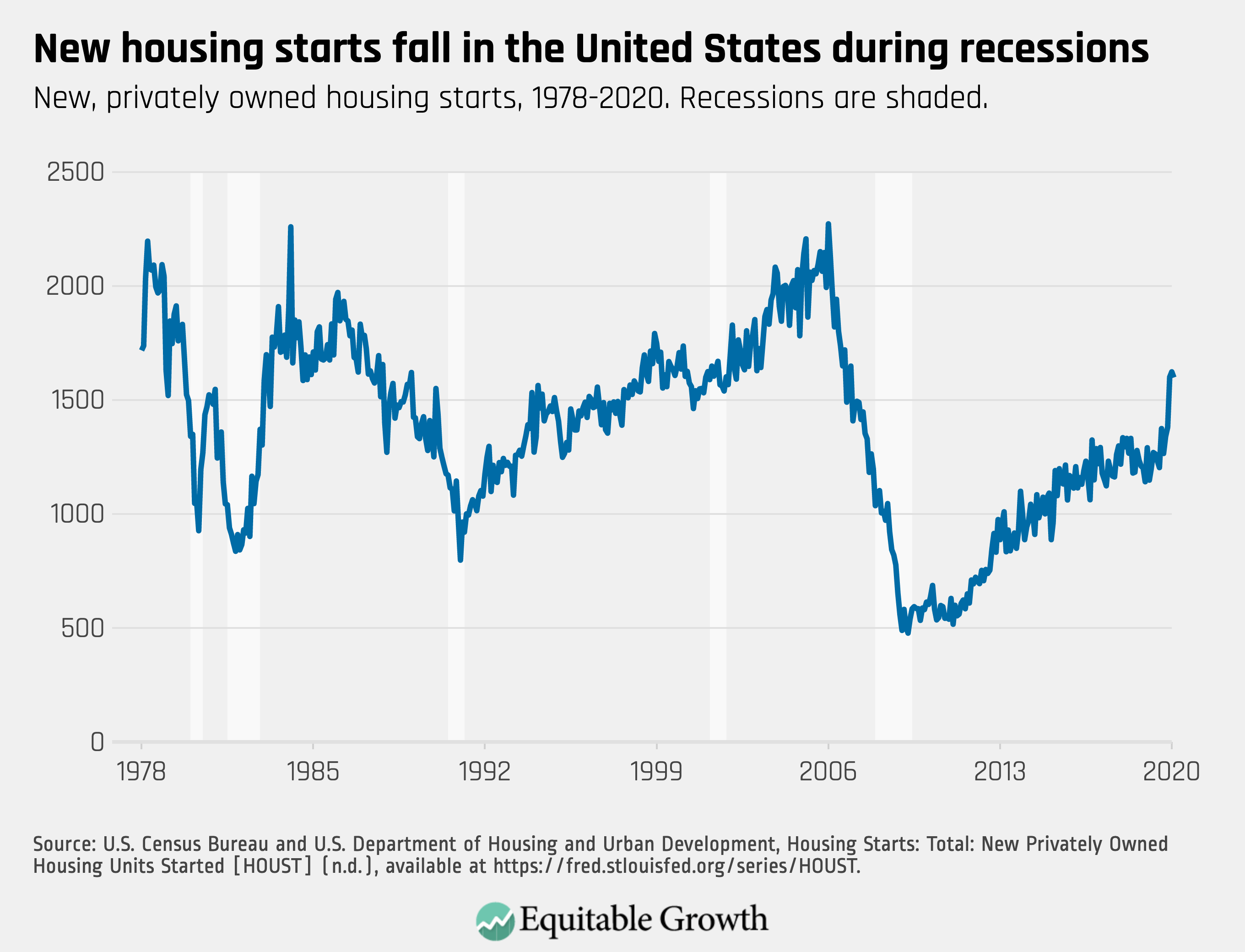

States and local governments—not the national government—dominate zoning rules, and sensible, temporary changes to those regulations could improve state and local economies and, in turn, the overall U.S. economy. Housing construction is a macroeconomically important industry. In many states, however, construction is limited by tight zoning regulations. By loosening these restrictions for a short period, such as for 2 years, states and municipalities could induce skittish investors to pull cash from underneath their mattresses in order to invest in housing “starts.” Doing so would cushion the painful downturn in housing output that will likely occur in response to coronavirus.

Housing is an expensive, long-lived asset. When economic times grow uncertain, housing developers and financiers know that a house will be expensive to build but are unsure that housing demand is sufficient to repay the investment and make a profit. When the Federal Reserve lowers interest rates, it tries to stimulate construction because lowering interest rates lowers a project’s total construction costs, which increases the expected profit from building a new home—and that spurs investors to open their checkbooks—in theory. In reality, however, past experience suggests that when interest rates are already low, additional dips in the rate don’t provide much of a stimulus to investment. (See Figure 2.)

Figure 2

So, housing developers and financiers need a reason to invest. A temporary loosening of zoning regulations would do the trick. Suppose that California—notorious for its restrictive zoning rules—passed a law enabling any housing project that puts shovels in the ground within 1 year to build larger houses or more units per lot. Developers would suddenly have a unique, fleeting opportunity. If they build immediately, then they could earn profits that would be unattainable if they wait. This type of incentive, passed at the state or even local level, could be enough to stimulate construction spending, mitigating what might otherwise be a terrible downturn in the sector.

Housing starts produce jobs, spark the purchase of building materials, and by increasing supply ease financial pressures on residents by lowering housing costs. Passing these temporary laws at the state level would prevent local homeowners in municipalities from blocking changes. The “burden” of liberalizing zoning rules could be proportionate. A state law, for instance, could provide that any local zoning limits that specify the number of square feet of a project must increase by 25 percent. Multifamily developments could have 25 percent more units. That approach would loosen all local zoning laws to the same degree.

Three other steps that states and localities can take

Although many states and cities cannot use deficit spending to stimulate their economies, they can adopt creative “law and macroeconomic” policies to mitigate what is sure to be a painful economic downturn. State and local governments that enact these measures will suffer less than those that passively wait for the economy to heal itself or for Congress and the Fed to ride to the rescue with additional funding. Countercyclical utilities and zoning regulations are just two examples of the many regulatory stimulus options that are available to state and city governments alone or in league with the federal government, among them home foreclosure and tenant-eviction restrictions and rent adjustments, energy efficiency mandates, and easing unemployment insurance eligibility requirements.

—Yair Listokin is the Shibley Professor of Law at Yale Law School and the author of Law and Macroeconomics: Legal Remedies to Recessions (Harvard University Press 2019).

Every February for the past 45 years the United States commemorates African American history—a month dedicated to learning about and celebrating the accomplishments and stories of black Americans throughout our nation’s history. Typically, Black History Month is observed through various activities and lessons in school. In our public school systems in particular, teachers add elements to their curriculum about famous African American authors, scientists, politicians, and innovators. In history classes, many teachers explore the clash over slavery leading up to the Civil War, the passage of the 13th and 14th Amendments to the Constitution, and the civil rights movement of the 1960s, perhaps discussing the passage of the Voting Rights Act of 1965 and almost always distributing passages written by the Rev. Martin Luther King, Jr. and perhaps Maya Angelou, too.

It’s great that all of these topics are being discussed in public schools. But there is a lot more to black history than what our schools showcase during the shortest month of the year. Many Americans don’t ever truly discover the depths of the African American experience in ways that fully convey the harm inflicted upon those enslaved before the Civil War and the generations of blacks who continued to suffer from blatant and pervasive racial discrimination over the next 150-odd years.

Public schools tend to gloss over the details of enslavement. And most teachers are not properly equipped to handle discussions of this sordid past in their classrooms or to teach their students about the violent resubjugation of blacks in the South after the Civil War via race riots, lynchings, mass incarceration, voter disenfranchisement, and segregation—actions that spread across the nation as African Americans embarked on the Great Migration out of the South beginning in the late 19th century and continuing well into the post-WWII era.

Because these particular lessons of American history go largely untaught in our public schools, the cascading ill-effects of these discriminatory, state-sanctioned actions on African Americans’ opportunities to succeed and thrive amid the growth of the wealthiest and most powerful nation on earth also goes untaught. The missing chapters in our nation’s history of racial discrimination and the ensuing economic consequences over generations mask the social costs of inequality and the ways in which it obstructs, subverts, and distorts our economy, and society’s ability to stimulate unbiased economic growth as the Washington Center for Equitable Growth’s Heather Boushey explains in her book Unbound: How Inequality Constricts Our Economy and What We Can Do About It.

Indeed, evidence-based research demonstrates that racial economic inequality, driven by opportunity-hoarding and discrimination, obstructs the supply of talent, ideas, and capital in our economy, slowing productivity growth. Our racialized criminal justice system and unresponsive political institutions subvert the ability of the vast majority of African American individuals, families, and communities to thrive. And discrimination in our credit, housing, and labor markets across generations slows wealth creation among African Americans and distorts the macroeconomy by undermining consumer spending.

What’s more, white supremacy and related violence and vitriol are rising at an alarming pace such that the U.S. Department of Homeland Security, in 2019, acknowledged its serious threat to society. Even the Black Lives Matter movement—which merely asks society to acknowledge the disparities faced by African Americans and the fact that their lives are valued less than other demographic groups (not that black lives should be valued more than others)—sparked an outcry from people who likely don’t understand the depths of injustice that black Americans have endured for centuries.

We have both advocated extensively for improving the public education system’s ability to teach our students about the baleful historical consequences for African Americans of enslavement, Jim Crow, and ongoing racial discrimination, as well as the ramifications that continue to this day. Most recently, in Equitable Growth’s newly released book, Vision 2020: Evidence for a stronger economy, we each urge in our separate essays—“Overcoming social exclusion: Addressing race and criminal justice policy in the United States” and “The logistics of a reparations program in the United States”—that the next presidential administration consider new ways to elevate this largely untaught aspect of American history and the African American experience in public schools. Our ideas include:

Allocating funding to local and state-level governments to establish programs and initiatives across subjects within the public Kindergarten through 12th-grade school system that would educate the public about the history of race in the United States and how this history affects social outcomes and our society’s beliefs about race

Beginning the necessary work to implement a reparations program that would elevate the full history of the African American experience and improve public education around these topics as a means to acknowledge this complete history and attempt to repair the damage done

Educating people about racial biases and implicit biases, as well as systemic racism, and how these structures and perceptions shape society and the African American experience within it

Perhaps if our public school systems were given the tools and the encouragement to really teach the atrocities and outcomes of slavery, Jim Crow, and ongoing racial discrimination, the African American experience would be better understood by everyone. Improving education around these topics would provide much-needed context to the lived experiences of black Americans and their ancestors, opening up the possibility for understanding around the past and how its legacy continues to affect the present. Maybe then, our society could garner the mainstream support needed to create the targeted policies needed to close the gaps in educational attainment, innovation, economic standing, and the criminal justice system between African Americans and their white counterparts. Maybe then, all Americans could observe Black History Month fully conscious of the plight of black Americans throughout our history, how much they have achieved despite being held back at every turn—and how much more they could do if they weren’t.

—Robynn Cox is an assistant professor at the University of Southern California Suzanne Dworak-Peck School of Social Work. Dania V. Francis is an assistant professor of economics at the University of Massachusetts Boston.

The need for systemic change, the power of government to improve the U.S. economy and society, and the importance of connecting research, evidence, and data to the U.S. policymaking process dominated the conversation among a panel of scholars at the February 18 introduction of the Washington Center for Equitable Growth’s new policy book, Vision 2020: Evidence for a Stronger Economy.

The book presents 21 essays by leading academic economists and other social scientists containing innovative, evidence-based, and concrete policy ideas that are aimed at shaping the 2020 policy debate. They cover a wide range of issue areas, from tax and macroeconomics to racial and environmental justice, and from labor market reform to antitrust policies.

At the February 18 event, authors of four of the essays discussed their policy proposals: Robynn Cox, assistant professor of social work at the University of Southern California; Susan Lambert, professor of social service and administration at the University of Chicago; Fiona Scott Morton, professor of economics at Yale University, and Equitable Growth president and CEO Heather Boushey, who moderated the discussion.

An audit of current federal crime-control policies and funding to determine what needs to be done to end mass incarceration and repair the criminal justice system

The collection by state and local governments of unbiased data to understand the reasons for persistent racial disparities in criminal justice

Incentives for states to repeal felon disenfranchisement laws

A process of re-educating the American public about the history of race in the United States to “break flawed perceptions in the association between race and crime”

The first step in this process, she writes, should be reconciliation and atonement, which could address reparations for past and current oppressive policies. (Dania V. Francis writes separately about reparations in Vision 2020.)

At the book launch event, Cox noted that we “live in a society that has a dual criminal justice system in which individuals from different social groups are treated differently … We choose to punish differently based on who is committing the crime.” She added, “That seems to be based on age-old perceptions … about race and crime. One can view crime as a symptom of poverty, or you can say individuals have innate criminality and they’re committing crimes because of this innate criminality.”

Cox also explained that “colorblind” policies, whether relating to criminal justice or other policy areas, are not the same as “race-neutral” policies. “We’ve created policies that have been seemingly colorblind, but they have not been implemented in a race-neutral way,” she said, “either because they disproportionately seem to impact certain groups, which then continues to drive disparities and inequality, or because their actual implementation has been biased.”

She concluded, “When we’re making policies, we really have to consider not only this colorblind notion, that this policy is going to help the poor, but is it going to help the most marginalized groups in society? How does it impact racial disparities?”

To learn moreabout Cox’s Vision 2020 essay, see this Equitable Growth video:

Lambert’s contribution, “Fair work schedules for the U.S. economy and society: What’s reasonable, feasible, and effective,” addresses the problems of work schedule instability and unpredictability. Too many workers, especially low-income workers, are subject to employers setting and changing work schedules with insufficient notice, making it difficult to arrange childcare and healthcare, hold second jobs, and predict household earnings from week to week and month to month. Oregon and several U.S. cities have passed comprehensive scheduling laws that, generally, provide workers with two weeks’ notice of their schedules and a good-faith estimate of their hours, as well as greater say over their shifts and protection from arbitrary last-minute schedule changes. Lambert urges the federal government to consider national legislation based on the evidence of how well these and future local and state rules work.

At the February 18 session, Lambert noted the disproportionate impact of scheduling problems. “The most disadvantaged workers,” she said, “experience a constellation of problematic scheduling practices. For example, lower-paid workers, and African American workers compared to white workers, are at significantly higher risk of experiencing what we call the ‘triple whammy’ of having work-hour volatility plus short advance notice plus no say in when you work.”

She also addressed new technologies that enable employers to use algorithms to set schedules for efficiency. She said the new software “is a tool and not the cause of this instability and unpredictability.” But she added that the algorithms “can be used to provide stable and predictable schedules” and that some companies are, in fact, using the software that way.

For more on Lambert’s essay, see this video:

Scott Morton’s essay, “Reforming U.S. antitrust enforcement and competition policy,” lays out the data showing increasing corporate mergers and anticompetitive activity that have led to rising concentration in the U.S. economy and points out why and how antitrust laws are being underenforced. She proposes a number of changes to begin to correct the problem:

She calls on Congress to approximately double the budgets of the Antitrust Division of the Justice Department and the Federal Trade Commission to allow for greater enforcement activities, noting that resources for enforcement have declined significantly since 2000, that the number of enforcement actions has declined, and that firms have been able to raise prices above marginal costs with greater frequency, signaling noncompetitive markets.

She urges the appointment of leaders of the two enforcement agencies who are prepared to use existing authority to toughen enforcement of the antitrust laws and bring challenging cases to the courts.

She calls on Congress to reform antitrust statutes to guide the courts more closely and thus deter and prevent anticompetitive conduct more effectively, pointing to increasingly pro-business court decisions based on loose interpretations of existing law. Such changes would:

Overturn Supreme Court precedent that has permitted anticompetitive behavior on a large scale

Prohibit courts from avoiding examination of the evidence in a case and just assuming that a market is or will become competitive

Create simple rules (presumptions) that deter practices that, based on existing evidence, are likely to be anticompetitive

Clarify that antitrust violations can result in not only higher prices but also reduced quality, harm to innovation, lower wages, and elimination of potential competition

She urges creation of a new federal agency to regulate digital businesses that could take such actions as establishing standards for a competitive digital marketplace and considering whether consumers should be able to coordinate their use of social media applications or commerce websites (known as interoperability).

At the Equitable Growth event, Scott Morton decried the inability or unwillingness of federal judges to consider empirical economic evidence in their antitrust decision-making rather than relying solely on what she considers to be outdated antitrust theory and legal interpretations.

“We know a lot more about how markets work,” she said. “That progress has not translated into the courts, so not only are we enforcing less because of the push to make the judiciary believe that antitrust enforcement is not a good idea, but also we’re not giving courts the tools to enforce well, or when we give the courts those tools, they’re rejecting them and saying they’re too hard, we can’t do economics … Then, you’re throwing darts rather than using scientific tools to figure out whether consumers will be harmed.”

She said one possible reason for judges finding it too difficult to use economic analysis is that most do not get a lot of antitrust cases because of the randomness of how judges are selected for cases. She suggested the creation of a specialized trial court, made up of judges with some economic expertise, to hear cases brought under the federal antitrust laws.

To learn more about Scott Morton’s research, see the following video:

Heather Boushey noted on several occasions the reliance of policy proposals on newly available data, as well as the need for more going forward. In her Vision 2020 essay, “New measurement for a new economy,” she argues for the importance of new metrics in an age of inequality to show whether the U.S. economy is delivering benefits for all Americans. She points to GDP 2.0, an Equitable Growth initiative that urges policymakers to use data to show how the benefits of economic growth are distributed up and down the income ladder.

At the book release event, she also made a connection between data and the other issues discussed by panelists. “You can only analyze things for which you have data and that you know,” she said, “so if you have a set of policies, you know whether or not they were effective. But you don’t know anything about the policies that don’t exist or trends that you aren’t tracking. And so these questions about what kinds of data government should be creating, what kinds of data we could be using from the private sector, are imperative not just for evaluating failures of current policies but for knowing more, which is something that we really want to focus on a lot at Equitable Growth.”

Equitable Growth plans to distribute Vision 2020 to policymakers and others in the hope that its 21 essays can both contribute to the current policy debate and spur action on these critical issues in the coming months and years.

The Washington Center for Equitable Growth today is publishing a collection of 21 essays, with innovative, evidence-based, and concrete policy ideas to shape the 2020 policy debate. The essays, which will be introduced at an event in Washington, DC, cover a wide range of economic issues, including taxes, macroeconomics, racial and environmental justice, labor market reform, and antitrust policies.

The new book, Vision 2020: Evidence for a Stronger Economy, builds on last fall’s Equitable Growth conference of the same name and features leading voices from academia tackling the most pressing economic issues facing Americans today.

Recent transformative shifts in economic thinking illustrate how inequality obstructs, subverts, and distorts broadly shared economic growth. Undoing the economic damage caused by inequality and building the structures and institutions necessary to chart a new path will require systemic reforms in how markets and government work. Vision 2020: Evidence for a Stronger Economy offers some of the most promising, evidence-backed ideas for how to do just that.

At the release event, three book contributors—Robynn Cox of the University of Southern California, Susan Lambert of the University of Chicago, and Fiona Scott Morton of Yale University—will speak with Equitable Growth President and CEO Heather Boushey about their proposals.

Cox’s essay, “Overcoming social exclusion: Addressing race and criminal justice policy in the United States,” questions the idea of dealing with economic inequality through criminal justice reform, arguing instead for a widespread audit of current federal crime-control policies and funding to determine what needs to be done to end mass incarceration and repair the justice system.

Boushey’s essay, “New measurement for a new economy,” examines why it’s important in an age of inequality for policymakers to craft and make use of new metrics that show them and the public how the U.S. economy delivers for all Americans. What’s needed, she says, is GDP2.0 as an absolutely essential component of a policy agenda.

Reimagining an economy that works for all—providing good jobs and opportunities and rebuilding economic and political power for people and communities across the nation—is the defining challenge of our time. Equitable Growth has published Vision 2020 in the hope that the bold ideas advanced by its authors can inspire the country’s leaders to rise to that challenge.

This essay is part ofVision 2020: Evidence for a stronger economy, a compilation of 21 essays presenting innovative, evidence-based, and concrete ideas to shape the 2020 policy debate. The authors in the new book include preeminent economists, political scientists, and sociologists who use cutting-edge research methods to answer some of the thorniest economic questions facing policymakers today.

To read more about the Vision 2020 book and download the full collection of essays, click here.

Overview

Competitive markets deliver to consumers a variety of benefits: higher productivity, lower prices, better quality products, and more innovation. Yet firms have a financial incentive to restrain competition in order to obtain monopoly profits. There are three main harmful methods of limiting competition: colluding with rivals in a market, merging with rivals or potential rivals, and using anticompetitive techniques to exclude existing or potential entrants.

U.S. antitrust laws are designed to prevent these behaviors by making price-fixing, bid-rigging, and similar behavior illegal, requiring government review of mergers to prevent those that lessen competition, and prohibiting anticompetitive conduct by an incumbent with market power that tends to exclude entrants and rivals. Unfortunately, over the past few decades, these laws have not been operating in a way that generates and preserves vigorous competition in U.S. markets.

It is well understood that market power decreases innovation, productivity, and the efficient use of resources. Market power, however, also contributes to growing inequality. Shareholders and senior executives who benefit from increased market power through higher salaries and increased stock prices are disproportionately wealthier than consumers, on average. Furthermore, consumers, suppliers, and workers may beharmed by paying higher prices for monopoly products or services and receiving lower compensation for the products and services (inputs or wages) they supply to monopsonists (buyers with market power).1

Consumption, by contrast, is not nearly so concentrated. Joshua Gans at the University of Toronto’s Rotman School of Management and his co-authors report that the consumption of the top 20 percent of the wealth distribution in the United States is approximately equal to that of the bottom 60 percent, but their equity holdings are 13 times larger. Thus, if a dollar of monopoly profit is transferred to lower prices, most of that dollar moves from benefitting the top 10 percent through the value of their stock or dividends to instead benefitting the bottom 90 percent through lower costs of purchases.

Therefore, antitrust enforcement redistributes wealth without incurring the traditional shadow costs arising from taxation and, indeed, is an actively beneficial form of redistribution for the economy.2 Because antitrust enforcement both redistributes income and wealth to the bottom 90 percent of the population, as well as increases efficiency, it should be the first choice of policymakers concerned with equity. The standard for anticompetitive harm that courts use today is the protection of consumer welfare—meaning price, quality, and innovation, now and in the future. Antitrust enforcement using the best available economic tools—developed, in some cases, decades ago—generates the evidence needed to show where such anticompetitive conduct is present.

The underenforcement described below is the fault neither of this standard nor of the economic tools themselves—though they could, of course, be better. The antitrust underenforcement we see today is primarily the result of decisions made over the past 40 years in the courts.

The four policies I recommend to reverse this harmful trend are:

Dramatically increase the budgets of two federal antitrust agencies, the Federal Trade Commission and the Antitrust Division of the U.S. Department of Justice, which would be less expensive than it might appear because the two agencies collect disgorgement and restitution awards that flow back to consumers.

Appoint leaders of these two agencies who are committed to using the best tools available to reverse the decline in competition. Aggressive but appropriate enforcement will either lead to good results or will identify failures in the law or by the judiciary to protect competition and consumers.

Support and pass new legislation so that Congress can make it clear to the courts how it would like federal antitrust laws to be enforced and require courts to adopt up-to-date economic learning.