Promote economic and racial justice: Eliminate student loan debt and establish a right to higher education across the United States

This essay is part of Vision 2020: Evidence for a stronger economy, a compilation of 21 essays presenting innovative, evidence-based, and concrete ideas to shape the 2020 policy debate. The authors in the new book include preeminent economists, political scientists, and sociologists who use cutting-edge research methods to answer some of the thorniest economic questions facing policymakers today.

To read more about the Vision 2020 book and download the full collection of essays, click here.

Overview

The amount of student loan debt in the United States has ballooned over the past decade—more than tripling from less than $500 billion to more than $1.5 trillion since 2006. What’s more, the repayment burden is substantial—approximately $400 per month on average.1 Yet students have little choice but to pursue a college education. Where college was once seen as a ladder to upward social mobility, students increasingly need a college education simply to remain where they are socioeconomically.

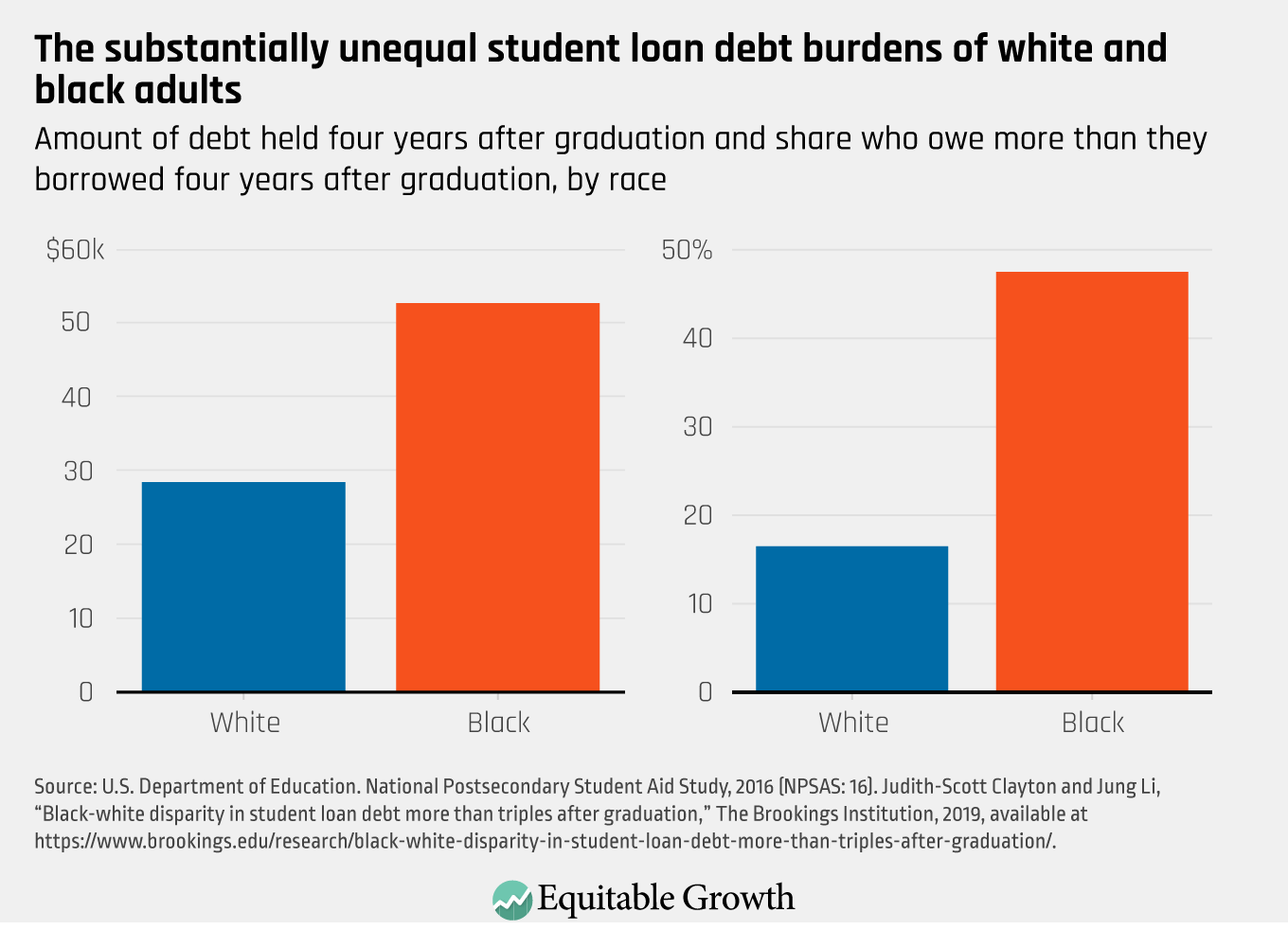

Higher education is, for many, a necessary step to earning a living wage, but black students face a particularly cumbersome burden to finance a degree. This essay explicates the disproportionately high burden of student debt carried by blacks in the United States, though all racially marginalized groups in the United States face particular financial burdens when pursuing higher education and repaying the necessary debts. (See “Snapshot” below.) Due in part to their families’ financial position, black students generally take on more debt than white students and, even at higher levels of socioeconomic status, are less protected by parental wealth.2 Then, after entering the labor market, young black adults face a harder time paying off their student loans in a labor market characterized by racial discrimination, as demonstrated by the experiences of prior cohorts of graduates.3 (See Figure 1.)

Figure 1

Upon exiting college, young adults are shaped by their indebtedness, including the need to secure paid employment with urgency in an endeavor not necessarily aligned with their career aspirations. New graduates with debt burdens enter the labor market more quickly and are more likely to work in unrelated fields after graduation.4 These borrowers have lower job satisfaction and overall life satisfaction, and lower psychological well-being well into adulthood.5 Student loan borrowers are less likely to get married, purchase a home, or start a business.6

While these negative economic and psychological consequences of student debt are distorting employment choices and depressing opportunities to pursue creativity across all borrowers, black students are hit the hardest. Evidence suggests that student debt impedes family formation specifically among the most vulnerable borrowers: black borrowers and those who have not completed their degree.7 Student loan debt is associated with poorer mental health and is even significantly associated with poorer sleep patterns among black borrowers, in particular compared to white borrowers.8

In this essay, we briefly present a range of proposals for relieving the burden of student loan debt and use our analysis to urge the full cancellation of all undergraduate and graduate, federal and private, student loan balances. We come to this policy recommendation after examining how less ambitious proposals fail to fully fix the unsustainable status quo of increasing indebtedness as a strategy for financing rising costs of higher education in the United States. Only the full cancellation of all student debt fully protects black students, their families, and those of other racially marginalized and vulnerable groups from the burden of student loans while establishing higher education as a universal right and offering restitution to all those who have had to rely on debt finance to pursue upward mobility through the education system.

A history of student loan cancellation in the United States

The concept of loan cancellation is not new. The George W. Bush administration brought us the public service loan forgiveness program in 2007.13 This program was intended to erase student debt for teachers, other public servants, and anyone working in a not-for-profit organization after working in their chosen field for 10 years while paying down their debt. Additionally, these borrowers must consolidate their loans and enroll in a particular type of repayment plan.

These stipulations were complicated enough that the program failed to provide relief to the vast majority of these select borrowers, even those verifiably working for nonprofit organizations or the government. Over the program’s cumulative history, more than 132,000 borrowers submitted employer-verified applications but only 641 have gotten relief, or approximately 0.5 percent.14 The other 99.5 percent were rejected primarily on technical grounds.

President Barack Obama introduced a similar program, but expanded it beyond employees of public and nonprofit institutions. Under the Obama administration’s program, borrowers pay between 10 percent and 20 percent of discretionary income, as defined by the U.S. Department of Education, for 20–25 years, and then have the remaining balance canceled. Upon program completion, any canceled debts are taxed as income (though surely none of it has “come in,” from the perspective of struggling borrowers).

Because the program has not yet been in place long enough for borrowers to complete 20 years of payments, the rate of award is uncertain. Yet, as of 2018, approximately one-quarter of borrowers are enrolled, with many disenrolled by the annual re-certification requirements.15 And policymakers are paying attention: Following efforts to gut the program by the Trump administration beginning in 2017, 23 senators in October 2019 called upon the federal Consumer Finance Protection Bureau to investigate the loan service company employed by the federal government due to its exceedingly high rates of refusals to forgive loans.16 Clearly these types of programs can be administrative minefields for borrowers, and it is unclear if they will or can provide any real relief to borrowers.

Weighing the merits of full or partial student debt cancellation

The merits of full or partial student debt cancellation at first glance largely rest on the degree to which the cancellation helps borrowers in need of debt relief. Those plans that call for partial student debt cancellation focus to different degrees on whether some higher-income borrowers or those who have borrowed to attend graduate school would benefit inordinantly from having their debt cancelled, compared to those who borrowed in pursuit of an undergraduate or technical degree or those who are otherwise clearly burdened by their student loan repayments. Cost estimates based on the plans’ assessment of these borrowers’ needs run the gamut, from an estimated $1.5 trillion for a full cancellation to between approximately $2 billion and $200 billion for a partial cancellation, between $5,000 and $60,000 per borrower.17

In our estimation, however, the merits of full cancellation far outweigh those presented in plans for partial cancellation. Full cancellation not only would address the array of financial inequities in current student borrowing programs—inequities that are particularly egregious for black borrowers—but also eliminate the many and complex rules and regulations borrowers are now required to meet for debt cancellation. Full cancellation would require a larger budgetary allocation, but doing so would directly address the rise of economic inequality in the United States, particularly for black Americans, while laying the groundwork for more sustainable and broad-based economic growth.

Partial student loan cancellation

When considering partial debt cancellation proposals, it is noteworthy that, on average, black college graduates still owe $53,000 in student debt 4 years after graduation.18 (See Figure 1 above.) Plans that propose to cancel less than this amount would ensure that the average black family would owe a lot less, yet many would still be left holding substantial sums of student debt. According to our calculation using the 2016 Survey of Consumer Finances, a plan that cancelled $50,000 of student loans for every borrower would still leave 1 million black-headed households holding $18,000 or more in student debt.

In contrast, the average white graduate carries about $28,000 in debt 4 years after graduation. This suggests that a capped debt forgiveness plan would completely wipe out many more white graduates’ debts, as a proportion of the population, than black graduates.19

Moreover, cancellation plans that provide debt cancellation after a set number of years are insufficient. Most of these plans still require certification of one’s household income level, profession, or other characteristics, and thus leave in place the same institutional and administrative barriers currently preventing graduates from realizing the cancellation promised in the Public Service Loan Forgiveness Act. As we can see in that law’s failures to provide meaningful debt relief, even well-intentioned attempts to target forgiveness to the “most” needy populations can cause nearly insurmountable hurdles for those needy groups when a program is not administered generously and fairly.

Full student loan cancellation

Full cancellation of student debt would entirely eradicate all current student loan balances immediately. Everyone would be eligible and all debts would be relieved, with no rules for borrowers to decipher and then prove their eligibility under, thus removing the potential for similar bureaucratic barriers to those that so thoroughly hinder our current policy today.

Full cancellation would unquestionably include the debt balances carried by parents through the Parent Loans for Undergraduate Students program, which also exhibits a racially disparate distribution.20 The full cancellation would serve to even further advance the lives of millions of black debtors and graduates and, yes, would include a fraction of wealthy whites.

Full student loan cancellation is the best policy

Many student debt advocates express skepticism about full cancellation, arguing it would be racially regressive because it would not benefit people of color so much as help white borrowers. The argument rests on three misguided assumptions. The first assumption is that a higher level of debt probably indicates a graduate or professional degree. Secondly, white students are more privileged, the thinking goes, and are presumably more likely to go to graduate school after graduation, leading to their higher debt values. Finally, the argument concludes, it must mean that a full cancellation of debt would really just help white borrowers and their families, thus widening the racial wealth gap.

A similar critique could apply to partial student debt relief, under an assumption that black students are generally less burdened by student loans than their white counterparts seeking higher levels of education. Together, these critiques exaggerate the consequences of full debt cancellation. The first problem with the argument is that carrying large amounts of student debt does not necessarily indicate a graduate degree, especially considering that the average black student who graduates from college has $53,000 in debt 4 years after graduation. Many have simply attended universities with inadequate public funding, including those in the Historically Black College and University system, which awards a disproportionate share of black college degrees and is more tuition-dependent than its counterparts.21

Next, black students, in fact, enroll in graduate degree programs at high rates. While this might run counter to conventional expectations, black college graduates are overrepresented in graduate education relative to their share of the population overall, according to the National Center for Education Statistics.22 Furthermore, as of 2012, 47 percent of black college graduates were enrolled in a graduate school degree program within 4 years of completing their bachelor’s degrees, which is higher than that of white recent graduates (38 percent).23

Indeed, this and the common finding in the social science literature that blacks from similar socioeconomic backgrounds as whites actually acquire more years of schooling runs counter the bootstrap narrative that situates inadequate investment in education on the part of blacks as the primary explanation for racial disparity.24

Finally, there’s the concern that full cancellation might favor white debtors in a way that increases the racial wealth gap. The evidence here is, at best, mixed. But a compelling recent study finds the opposite—that a full cancellation of student debt would reduce racial wealth disparities between black students and their white counterparts.25 Black students tend to take on more debt at every level of higher education, and are more likely than white students to drop out of university because of financial concerns in large part because of comparatively lower household-finance levels for black families in the first place. So, at each level of higher education, undergraduate and graduate, removing student debt proportionately benefits historically disadvantaged black students more.

The real problem, however, with making the argument that full cancellation of student debt widens the racial wealth gap is that it confuses the urgent problem of rising and unjust student debt burdens with the urgent problem of racially unequal access to capital. Relieving student debt is not the policy tool for eliminating the racial wealth gap, which has a great deal more to do with a lack of assets among black families than an abundance of debt on their part. Black families headed by a college graduate have less wealth than white families headed by a high school dropout.26 This wealth gap is not driven by student debt. That inequity stems from the insufficient assets within communities of color, regardless of education.

Hence, independent of student debt, young students of color start out in a less favorable economic position than their white peers. White families have had generations to amass and pass down wealth in a way that families of color have not. Neither a full nor a limited cancellation changes those roots of the racial disparity in assets.

This is not to say there is no connection between student debt and the racial wealth gap. Families with outsized financial advantages can “buy” crucial additional advantages for their children, such as the ability to obtain a college degree without accruing costly educational debts. Lack of wealth (primarily inherited wealth) prevents many black families from ever exercising this advantage.

Nonetheless, the alarming rise of student indebtedness, which, in the context of stagnating real wages (after accounting for inflation) and growing income and wealth inequality, point to alarming economic vulnerabilities that need to be addressed. The bad news is that this immediate yet also intergenerational problem may be getting worse. A recent report illustrates that lost income gains among millennials in the aftermath of the Great Recession of 2007–2009, alongside record levels of student debt accumulations, has left the homeownership rate for young adult millennials lower than every other generation at a similar age dating back about 100 years—to the Greatest Generation, who entered young adulthood right after the Great Depression and World War II.27 What’s more, the racial disparity in homeownership for young millennials is as large as it has ever been.28

Download FilePromote economic and racial justice: Eliminate student loan debt and establish a right to higher education across the United States

Conclusion

Black Americans are highly motivated to pursue higher education, but the reality is that as a group, they are financially stymied. Fewer black students begin college, even fewer graduate, and those who do graduate carry much more debt than their white counterparts. While student debt is conventionally thought of as “good debt,” the returns on investment that it generates are widely disparate by race within the prevailing socioeconomic framework that still subjects blacks and other subaltern groups to inferior housing and education, targets them disproportionally with predatory financial products, and continues discriminatory labor market practices.

These enduring levels of historical and ongoing discrimination patterns in the U.S. economy and society are why we enthusiastically applaud proposals that remove the economic burden of student loan debt for all students and their families. Additionally, providing tuition-free education at public colleges and universities to all Americans would eliminate the social and psychological stigma associated with the system of financial aid and eliminate the need for future generations to carry burdensome debts. We urge lawmakers to support proposals that implement restorative economic justice by cancelling the burden of all existing student debt. In essence, we can do the right thing and establish higher education as a universal economic right.

—Darrick Hamilton is the executive director of the Kirwan Institute for the Study of Race and Ethnicity at The Ohio State University. He also holds a primary faculty appointment in the university’s John Glenn College of Public Affairs, with courtesy appointments in the Departments of Economics and Sociology in the College of Arts and Sciences. Naomi Zewde is an assistant professor in the Graduate School of Public Health and Health Policy at The City University of New York. Both Hamilton and Zewde are fellows with the Roosevelt Institute. Hamilton would like to thank the Omidyar Network and the Hewlett Foundation for providing the Kirwan Institute with financial support while he conducted this research.

End Notes

1. Federal Reserve Board of Governors, “Report on the Economic Well-Being of U.S. Households in 2016 – May 2017” (n.d.), available at https://www.federalreserve.gov/publications/2017-economic-well-being-of-us-households-in-2016-education-debt-loans.htm.

2. Center for Responsible Lending and others, “Borrowers of Color & the Student Debt Crisis” (2019), available at https://www.responsiblelending.org/sites/default/files/nodes/files/research-publication/crl-quicksand-student-debt-crisis-jul2019.pdf.

3. Fenaba R. Addo, Jason N. Houl, and Daniel Simon, “Young, Black, and (Still) in the Red: Parental Wealth, Race, and Student Loan Debt,” Race and Social Problems 8 (1) (2016): 64–76, available at https://www.ncbi.nlm.nih.gov/pmc/articles/PMC6049093/pdf/nihms980016.pdf.

4. Justin Weidner, “Does Student Debt Reduce Earnings?” (Princeton University, 2016), available at https://scholar.princeton.edu/sites/default/files/jweidner/files/Weidner_JMP.pdf.

5. Mi Luo and Simon Mongey, “Assets and Job Choice: Student Debt, Wages and Amenities.” Working Paper No. 25801 (National Bureau of Economic Research, 2019), available at http://www.nber.org/papers/w25801; Jinhee Kim and Swarm Chatterjee, “Student Loans, Health, and Life Satisfaction of US Households: Evidence from a Panel Study,” Journal of Family and Economic Issues 40 (1) (2019): 36–50, available at https://ideas.repec.org/a/kap/jfamec/v40y2019i1d10.1007_s10834-018-9594-3.html.

6. Alvaro A. Mezza and others, “On the Effect of Student Loans on Access to Homeownership” (Washington: Board of Governors of the Federal Reserve System, 2016), p. 50, available at http://dx.doi.org/10.17016/FEDS.2016.010; Brent W. Ambrose, Larry Cordell, and Shuwei Ma, “The Impact of Student Loan Debt on Small Business Formation” Working Paper (Federal Reserve Board of Philadelphia, 2015), available at https://papers.ssrn.com/abstract=2633951; Dora Gicheva, “Student loans or marriage? A look at the highly educated,” Economics of Education Review 53 (2016): 207–16, available at https://ideas.repec.org/a/eee/ecoedu/v53y2016icp207-216.html.

7. Jason N. Houle and Cody Warner, “Into the Red and Back to the Nest? Student Debt, College Completion, and Returning to the Parental Home among Young Adults,” Sociology of Education 90 (1) (2017): 89–108, available at https://journals.sagepub.com/doi/abs/10.1177/0038040716685873.

8. Katrina M. Walsemann, Jennifer A. Ailshire, and Gilbert C. Gee, “Student loans and racial disparities in self-reported sleep duration: evidence from a nationally representative sample of US young adults,” Journal of Epidemiology and Community Health 70 (1) (2016):42–8, available at https://www.researchgate.net/publication/280777111_Student_loans_and_racial_disparities_in_self-reported_sleep_duration_Evidence_from_a_nationally_representative_sample_of_US_young_adults.

9. Julia Barnard and others, “It Made the Sacrifices Worth It: The Latino Experience in Higher Education” (Washington: UnidosUS, 2018), available at http://publications.unidosus.org/handle/123456789/1850.

10. Ibid.

11. Molly Hensley-Clancy, “Native American Colleges Have Abandoned The Student Loan System,” BuzzFeed News, October 10, 2016, available at https://www.buzzfeednews.com/article/mollyhensleyclancy/tribal-colleges-exit-the-student-loan-system; Deborah His Horse is Thunder, “Breaking Through Tribal Colleges and Universities” (American Indian Higher Education Consortium, 2012), available from: http://www.aihec.org/our-stories/docs/reports/BreakingThrough.pdf.

12. Deborah His Horse is Thunder, “Student Success at Tribal Colleges and Universities” (American Indian Higher Education Consortium, 2015), available at http://www.aihec.org/our-stories/docs/reports/StudentSuccess.pdf.

13. “Public Service Loan Forgiveness (PSLF),” available at https://www.nelnet.com/pslf (last accessed November 21, 2019).

14. Zach Friedman, “99% Of Borrowers Rejected Again For Student Loan Forgiveness,” Forbes, May 1, 2019, available at https://www.forbes.com/sites/zackfriedman/2019/05/01/99-of-borrowers-rejected-again-for-student-loan-forgiveness/#36dcc098b16b.

15. Katherine Lucas Mckay and Diane Kingsbury, “Student Loan Cancellation: Assessing Strategies to Boost Financial Security and Economic Growth” (Washington: Aspen Institute, 2019), p. 23, available at https://assets.aspeninstitute.org/content/uploads/2019/04/EPIC_Student_Loan_Cancellation.pdf.

16. National Public Radio, “23 Senators Demand Investigation Into Mismanagement Of Student Loan Program,” October 29, 2019, available at https://www.npr.org/2019/10/29/774395247/23-senators-demand-investigation-into-mismanagement-of-student-loan-program.

17. Ben Miller and others, “Addressing the $1.5 Trillion in Federal Student Loan Debt” (Washington: Center for American Progress, 2019), available at https://www.americanprogress.org/issues/education-postsecondary/reports/2019/06/12/470893/addressing-1-5-trillion-federal-student-loan-debt/.

18. Judith Scott Clayton and Jung Li, “Black-white disparity in student loan debt more than triples after graduation” (Washington: The Brookings Institution, 2019), available at https://www.brookings.edu/research/black-white-disparity-in-student-loan-debt-more-than-triples-after-graduation/.

19. Ibid.

20. Rachel Fishman, “The Wealth Gap PLUS Debt: How Federal Loans Exacerbate Inequality for Black Families” (Washington: New America, 2018), available at https://www.newamerica.org/education-policy/reports/wealth-gap-plus-debt/.

21. Krystal L. Williams and BreAnna L. Davis, “Public and Private Investments and Divestments in Historically Black Colleges and Universities” (Washington: American Council on Education, 2019), available at https://www.acenet.edu/Documents/Public-and-Private-Investments-and-Divestments-in-HBCUs.pdf.

22. “Total fall enrollment in degree-granting postsecondary institutions, by level of enrollment, sex, attendance status, and race/ethnicity or nonresident alien status of student: Selected years, 1976 through 2017,” available at https://nces.ed.gov/programs/digest/d18/tables/dt18_306.10.asp (last accessed November 21, 2019).

23. Clayton and Li, “Black-white disparity in student loan debt more than triples after graduation.”

24. Darrick Hamilton and others, “Umbrellas don’t make it rain: Why studying and working hard isn’t enough for Black Americans” (The New School, 2015), available at http://www.insightcced.org/wp-content/uploads/2015/08/Umbrellas_Dont_Make_It_Rain_Final.pdf.

25. Marshall Steinbaum, “Student Debt and Racial Wealth Inequality” (New York: Jain Family Institute, 2019), available at https://phenomenalworld.org/content/2-higher-education-finance/1-student-debt-racial-wealth-inequality/student_debt_and_racial_wealth_inequality_final_7-19-19.pdf.

26. Hamilton and others, “Umbrellas don’t make it rain: Why studying and working hard isn’t enough for Black Americans.”

27. Derrick Hamilton and Christopher Famighetti, “State of the Union: Housing” (Columbus, OH: Kirwin Institute, 2019), available at http://kirwaninstitute.osu.edu/wp-content/uploads/2019/06/Pathways_SOTU_2019_Housing-copy.pdf.

28. Derrick Hamilton and Christopher Famighetti, “The Great Recession, education, race, and homeownership” (Washington: Economic Policy Institute, 2019), available at https://www.epi.org/blog/the-great-recession-education-race-and-homeownership/.