The Washington Center for Equitable Growth President and CEO Heather Boushey earlier this month answered questions from across the world on economic inequality via the social networking platform Reddit as part of the “Ask Me Anything” series.

In her new book, Unbound: How Inequality Constricts Our Economy and What We Can Do About It, Boushey presents cutting-edge knowledge with journalistic verve, showing how inequality in the United States has become a drag on growth and an impediment to free market efficiency. She argues that policymakers can preserve the best of our economic and political traditions, and improve on them, by pursuing policies that reduce inequality and boost growth.

Boushey took questions for two hours on all things related to inequality, including the prospect of a wealth tax, the role of the Federal Reserve in warding off the next recession, addressing racial disparities in income and wealth, and more. Read more highlights of that discussion below.

This is a post we publish each Friday with links to articles that touch on economic inequality and growth. The first section is a round-up of what Equitable Growth published this week and the second is relevant and interesting articles we’re highlighting from elsewhere. We won’t be the first to share these articles, but we hope by taking a look back at the whole week, we can put them in context.

Equitable Growth round-up

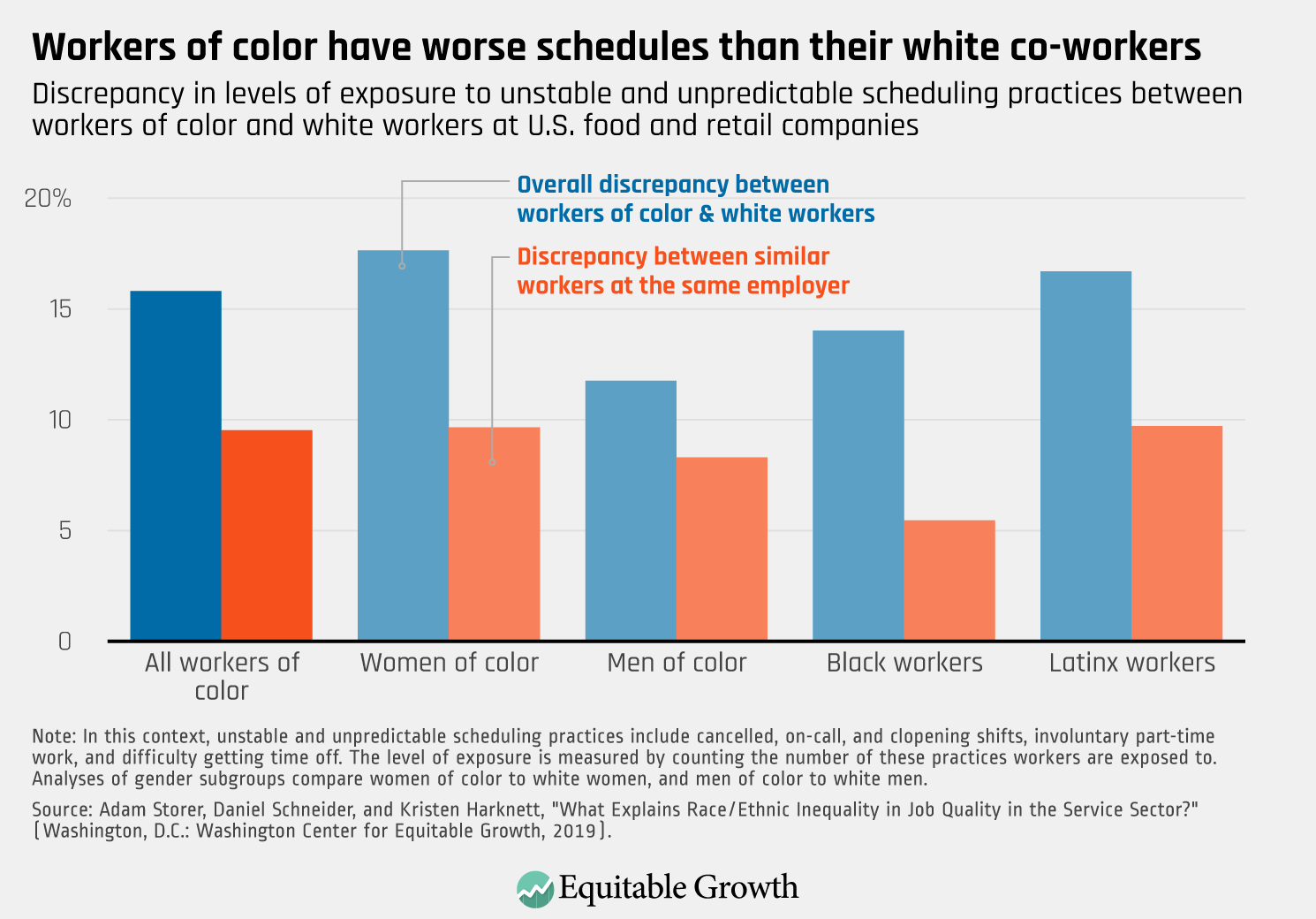

How do scheduling practices affect working families, particularly families of color, in the United States? A series of working papers released this week shows that not only are low-quality and unpredictable schedules pervasive among low-wage workers, but also that these schedules perpetuate racial and ethnic inequality across the country. The researchers surveyed 30,000 workers at 120 of the largest retail and food-service companies in the United States to find out who suffers the most from these schedules, and discovered that black and Hispanic women tend to have the worst schedules, while white men have the best ones. They also discovered that the children of those with the worst schedules behave worse and have less consistent childcare than those with parents who have better schedules. Cesar Perez and Alix Gould-Werth put together 10 charts highlighting the main findings of the research, which was also covered in The New York TimesThe Upshot blog.

Despite the evidence that desegregation boosts outcomes for low-income and minority students without negatively affecting their better-off and white peers’ outcomes, school segregation remains a problem across the nation. In fact, though the United States saw a large decline in black-white school segregation from the 1960s through the 1980s, in the years since then, desegregation has stalled and resegregation has actually increased, according to a report by former Research Assistant Will McGrew. In a blog post covering the report, Liz Hipple describes how McGrew makes it clear that school segregation is not an inevitable outcome of individual choices or preferences for “good” school districts, but rather that policy and legal decisions shape these preferences by continuing to tie school funding to local property taxes. Not only does this limit opportunities for individual students to achieve their own full potential, it also obstructs future dynamism and growth in the U.S. economy. McGrew recommends various policy options to reverse the trend of resegregation and put us back on the path to progress.

Equitable Growth President and CEO Heather Boushey testified before the Joint Economic Committee this week in a hearing on “Measuring Economic Inequality in the United States.” In her testimony, Boushey argued that one of the most important ways to fight inequality in the United States today is to properly track and measure it—namely, by adding measures of growth within income quantiles to the Bureau of Economy Analysis’ National Income and Product Accounts to better reflect the realities of the modern economy.

Equitable Growth Steering Committee member Jason Furman testified today before the House Judiciary Subcommittee on Antitrust, Commercial and Administrative Law. He discussed concentration in digital platforms, and how competition would benefit consumers, touching on ways to protect this competition such as more robust merger enforcement and regulations.

Be sure to head over to Brad DeLong’s latest worthy reads for his takes on must-see content from Equitable Growth and around the web.

Links from around the web

More than 9 million people work in food service, and 16 million more work in the retail sector, and according to estimates one-third of these workers receive less than one week’s notice for their schedules. As a result, these workers tend to have higher stress levels, more volatile income, less stable childcare options, and often have to get second jobs in order to make ends meet. Stephanie Wykstra explains on Vox the fight for fair workweek policies, who would be most affected, how these policies would help workers, and the challenges facing supporters in getting companies to comply.

The United States has never been richer, writes Eric Levitz in New York Magazine’s The Intelligencer. In fact, if wealth were evenly distributed across the United States today, each individual would have close to $300,000 and every family of four would be millionaires. So, why is it that middle- and working-class households are working way more and earning way less than they were a few decades ago? Levitz argues that three policy failures that have led us here: the dramatic decline in wages and worker bargaining power; the ever-increasing and unaffordable costs of housing, healthcare, and education; and the failure to modernize the social safety net.

At least half of the Democratic candidates for president in the 2020 race have put forward robust labor platforms touching on ideas from broadening union membership to banning noncompete agreements to treating independent contractors as employees, reports Noam Scheiber for The New York Times. One of the more striking of these proposals is the idea known as sectoral bargaining, which would allow workers to bargain with employers on an industrywise basis rather than with individual employers, potentially increasing wages for millions of workers at a time—even those who aren’t unionized. Scheiber hypothesizes that the large number of candidates supporting sectoral bargaining and other labor platforms likely reflects stagnant wage growth, increasing economic insecurity, and deepening inequality in the United States.

Rather than hitting the glass ceiling at the very top of the management ladder, new research suggests that women may face obstacles to advancing higher up much earlier in their careers—namely, at the very first rung of the management ladder. In fact, writes Vanessa Fuhrmans for The Wall Street Journal, “men outnumber women nearly 2 to 1 when they reach that first step up—the manager jobs that are the bridge to more senior leadership roles.” And, according to the study, it’s not because women are pausing there to raise children or that they have less ambition than men.

Antitrust and competition issues are receiving renewed interest, and for good reason. So far, the discussion has occurred at a high level of generality. To address important specific antitrust enforcement and competition issues, the Washington Center for Equitable Growth has launched this blog, which we call “Competitive Edge.” This series features leading experts in antitrust enforcement on a broad range of topics: potential areas for antitrust enforcement, concerns about existing doctrine, practical realities enforcers face, proposals for reform, and broader policies to promote competition. Jason Furman has authored this contribution.

The octopus image, above, updates an iconic editorial cartoon first published in 1904 in the magazine Puck to portray the Standard Oil monopoly. Please note the harpoon. Our goal for Competitive Edge is to promote the development of sharp and effective tools to increase competition in the United States economy.

Washington Center for Equitable Growth Steering Committee member Jason Furman, a professor of the practice of economic policy at the Harvard Kennedy School and a nonresident senior fellow at the Peterson Institute for International Economics, testifies today about “Online Platforms and Market Power: The Role of Data and Privacy in Competition” before the House Judiciary Subcommittee on Antitrust, Commercial and Administrative Law. Furman, who previously served as a top economic adviser to President Barack Obama, including as chair of the Council of Economic Advisers, was deeply involved in competition policy, issuing reports on concentration and promoting inclusive growth and employment monopsony in the U.S. labor market, during his time in the White House.

In his testimony today, Furman makes four points to congressional members of the subcommittee:

Digital platforms are highly concentrated.

Competition will benefit consumers.

More robust merger enforcement is needed to protect competition.

—Michael Kades, director of Markets and Competition Policy at Equitable Growth

Prepared Testimony for the Hearing “Online Platforms and Market Power, Part 3: The Role of Data and Privacy in Competition”

Jason Furman

Professor of the Practice of Economic Policy, Harvard Kennedy School

U.S. House of Representatives

Committee on the Judiciary, Subcommittee on Antitrust, Commercial and Administrative Law

October 18, 2019

Chairman Cicilline, Ranking Member Sensenbrenner, and Members of the Committee:

Thank you for the opportunity to testify on the important topic of online platforms and market power. I am a professor of the practice of economic policy at the Harvard Kennedy School, where I focus on a wide range of economic policy issues. I recently chaired the Digital Competition Expert Panel for the U.K. government that produced a report titled “Unlocking Digital Competition.”1 I am currently advising the U.K. as they move forward with a key set of recommendations from this report, including the establishment of a Digital Markets Unit to act as a procompetition regulator. Many of the recommendations in our report are applicable to the United States and I appreciate the opportunity to share some of those ideas with you today.

In my testimony today, I will make four points:

The major digital platforms are highly concentrated and, absent policy changes, this concentration will likely persist with detrimental consequences for consumers.

More robust competition policy can benefit consumers by helping to lower prices, improve quality, expand choices, and accelerate innovation. These improvements would likely include greater privacy protections given that these are valued by consumers. However, it is not clear that competition will be sufficient to adequately address privacy and several other digital issues.

More robust merger enforcement should be part of the solution to expanding competition, including better technical capacity on the part of regulators, more forward-looking merger enforcement that is focused on potential competition and innovation, and legal changes to clarify these processes for the courts.

A regulatory approach that is oriented toward increasing competition by establishing and enforcing a code of conduct, promoting systems with open standards and data mobility, and supporting data openness is essential. This is because more robust merger enforcement is too late to prevent the harms from previous mergers, and antitrust enforcement can take too long in a fast-moving market.

I also want to recommend to the Committee the recommendations in the recent report by the University of Chicago’s Stigler Center Committee on Digital Platforms on the economy and market structure, many of which dovetail with the suggestions in the report I chaired and with the recommendations in my testimony today.2

I will now elaborate on each of my four points.

Point #1: The major digital platforms are highly concentrated and, absent policy changes, there is a high likelihood that this concentration will persist with detrimental consequences for consumers.

The major online platforms, including online search, mobile operating systems, digital advertising, and social media, are each dominated by two players. Moreover, the two players in each of these markets are generally drawn from the same five major companies. A number of economic features of digital markets have helped to greatly reduce what economists call “competition in the market” by leading to tipping that results in a winner-take-most situation. These economic features include the combination of economies of scale and scope, the network externalities associated with having many users on the same platform, behavioral biases on the part of consumers, the data advantages of incumbents, the importance of raising capital, and brands. While many of these individual features are found in a wide range of markets, their combination in digital markets is unique.

It is more difficult to provide a definitive answer to the question of whether there is “competition for the market” in the digital sector. This is the idea that even if at any given moment only one or two major platforms are viable, over time these incumbents can be toppled and replaced by newer and more innovative competitors. Many of the dominant technology companies of the past seemed unassailable but then faced unexpected competition due to technological changes that created new markets and new companies. For example, IBM’s dominance of hardware in the 1960s and early 1970s was rendered less important by the emergence of the PC and software. Microsoft’s dominance of operating systems and browsers gave way to a shift to the internet and an expansion of choice. But these changes were facilitated, in part, by government policy, in particular, antitrust cases against these companies, without which the changes may never have happened.

Similar changes have been seen in the platform space, including Google replacing Yahoo and Facebook replacing MySpace. However, these and other similar examples all took place in the early days of the World Wide Web. Moreover, to the degree that the next technological revolution centers around artificial intelligence and machine learning, then the companies most able to take advantage of it may well be the existing large companies because of the importance of data for the successful use of these tools. New entry may still be possible in some markets, but to the degree that entrants are acquired by the largest companies with little or no scrutiny, anticompetitive behavior is tolerated, and open standards are limited, the channel of competition for the market is not fully operative.

Point #2: More robust competition policy can benefit consumers by helping to lower prices, improve quality, expand choices, and accelerate innovation.

This lack of competition is costly. Consumers may think they are receiving “free” products, but they are paying a price for these products in a number of ways. First, the competitive price for some of these products might have been negative, so the fact that consumers are not being paid for the use of their data may reflect a failure of competition. Second, to the degree that the highly concentrated advertising market results in higher ad prices than would otherwise be the case, these higher costs are passed along by sellers in the form of higher prices for consumers. Third, consumers pay in the form of quality reductions. Finally, consumers pay in the form of reduced innovation in a world in which the major platforms have reduced incentives to innovate and incumbents have distorted incentives to make more incremental improvements that can be incorporated into the dominant platforms rather than more paradigmatic changes that could challenge these platforms.

Competition policy is very good at helping consumers get more of what they want. To the degree that public policy interests are aligned with those of consumers, that means that competition policy can be an effective tool in increasing social welfare. That is generally the case in the economy, and the digital sector is no exception. Many consumers want more privacy. Right now, with so few platform choices, they have limited options in this regard—a consumer can delete Facebook, for example, but will not have another place to go to connect with her friends. More choice would create more incentives for privacy protections.

There is an alternative perspective on privacy that is the basis for the European Union’s General Data Protection Regulation, or GDPR, which is that privacy is grounded in human rights and is generally applicable—it is not just something that should be provided to the degree that consumers want it in a competitive marketplace. This perspective would say that in addition to ensuring robust choices for consumers, regulators should also explicitly set minimal standards and rules for privacy, based on these human rights concerns or the worry that consumers will not be sufficiently attentive for competition to serve their needs. The United States already has such rules in areas like healthcare and banking, and understanding whether a generalized set of privacy rules is necessary—as a complement to competition policy and taking into account their impact on competition—is an important issue to resolve.

Beyond privacy, there are some issues that cannot be solved by competition. Some consumers value harmful content, like child pornography or instructions on assembling weapons of mass destruction. Competition, by itself, would deliver more of this content. While competition is an essential component of policy toward digital platforms, these other issues make clear that competition cannot be the only element of such a strategy.

Point #3: More robust merger enforcement should be part of the solution to expanding competition, including better technical capacity on the part of regulators, more forward-looking merger enforcement that is focused on potential competition and innovation, and legal changes to clarify these processes for the courts.

Competition policy generally recognizes a distinction between companies that grow organically, presumably reflecting efficiencies, and companies that grow through mergers, where regulators need to weigh the efficiencies against the harms from lessened competition.

In the past decade, Amazon, Apple, Facebook, Google, and Microsoft combined have made mor than 400 acquisitions globally. Many, if not most, of the major features of these companies have not been developed internally but acquired. Many of these acquisitions are small and almost certainly efficiency enhancing, but several have been quite big—the largest being Microsoft paying $26.2 billion for LinkedIn.

Merger control is subject to two types of errors: false positives, when a merger that should have been allowed to go through is blocked, and false negatives, when a merger that should have been blocked is allowed to go through. No enforcement can be perfect given all of the uncertainties inherent with forward-looking merger assessments, so some balancing of these types of errors is necessary.

To date, there have been no false positives in mergers involving the major digital platforms for the simple reason that all of them have been permitted. Meanwhile, it is likely that some false negatives will have occurred during this time. This suggests that there has been underenforcement of digital mergers, both in the United States and globally. Remedying this underenforcement is not just a matter of greater focus by the enforcer, as it will also need to be assisted by legislative change. Had such a change been in effect, it is likely that the vast majority of these mergers would still have gone through based on their minimal impact on competition and their potentially large benefits for consumers. But some would likely have been blocked, resulting in more competition today.

A better approach involves three elements. First, the Federal Trade Commission, or FTC, and the Department of Justice’s Antitrust Division need expanded resources to develop greater technical expertise in the digital space. Economics and law are essential, but so is computer science. Doing this will require more staff and an increased focus on digital expertise.

Second, merger analysis cannot simply be focused on short-run, static price effects, but must also consider the effects on innovation in the future. This can involve consideration of the role of data as a potential barrier to entry and the role of potential competition in the market. This is further complicated by the fluid definitions of digital markets, which continue to evolve over time. Economists have tools to assess some of these issues, but in many cases this can be very difficult and can lead to some ambiguity and uncertainty in any given case.

Third, in recent decades, courts have established an increasingly high bar for blocking mergers. This is likely inappropriate in the economy as a whole, but it is especially problematic in the digital sector, where a strong presumption in favor of mergers runs up against the necessity of considering what are inherently more speculative—but still very real and important—issues, like potential competition and innovation. As a result, the legal standards for merger review need to be clarified, either more generally or specifically for the digital space, including shifting some of the burdens of proof.

Point #4: A regulatory approach that is oriented toward increasing competition by establishing and enforcing a code of conduct, promoting systems with open standards and data mobility, and supporting data openness is essential.

Expanded merger enforcement would be helpful, but it is not sufficient since many of the horses have already left the barn. Antitrust scrutiny of the major platforms, like the valuable work being undertaken by this committee and the efforts by the FTC and Department of Justice, are important as well. But in a fast-moving technological landscape, none of these efforts are sufficient to ensure adequate competition—by the time enforcement happens, the competition may have been wiped out and the major platforms have moved on. Moreover, the fines associated with enforcement may not be a sufficient deterrent, especially when they are levied for very specific conduct and do not set a clear precedent for other companies operating in the future.

That is why my panel recommended the establishment of a “Digital Markets Unit,” a step the U.K. government announced it is taking and that I am currently helping them to implement. I believe this recommendation is fully applicable in the United States. I will describe the three main functions that regulation should undertake, recognizing that this could be housed in an existing regulator like the FTC or in a new body like the “Digital Authority” floated by the Stigler Center commission.

The first function is a code of conduct that would apply to companies that were deemed to have “strategic market status,” a designation that would be applied based on transparent criteria that would be re-evaluated every 3 to 5 years and would be focused not just on traditional criteria like market shares but also on the degree to which a platform acted as a “gateway” or a “bottleneck.” Companies with strategic market status should be subject to a code of conduct that would be developed through a multistakeholder process and should be enforceable. The elements of the code of conduct would be similar to existing antitrust law, including ensuring that business users are provided with access to designated platforms on a fair, consistent, and transparent basis; provided with prominence, rankings, and reviews on designated platforms on a fair, consistent, and transparent basis; and not unfairly restricted from, or penalized for, utilizing alternative platforms or routes to market. Importantly, smaller businesses and new entrants would not be subject to these rules—the goal of these rules is the establishment of a level playing field but not inhibiting innovation and choice by emerging competitors.

The second function is promoting systems with open standards and data mobility. These steps would benefit consumers by allowing them to access and engage with a wider range of people in a simpler manner, fostering more competition and entry—including enabling consumers to multihome by using multiple systems simultaneously or to switch more easily to alternative platforms. This step is not self-executing; you cannot just order it and expect it to happen. It will require hard work to identify relevant areas, like messaging or social networks, collaboration with companies on necessary technical standards, and careful consideration to ensure that it is done in a manner that is compatible with other objectives like protecting privacy. Much of this is happening already, including through initiatives like the Digital Transfer Project organized by many of the major tech companies. Companies do not, however, have a fully aligned incentive to facilitate competition through open standards, so further pressure can help by providing further incentive for private efforts to continue to become even more robust and/or by creating a more formal regulatory requirement.

The third function is data. Companies active in the digital economy generate and hold significant volumes of customers’ personal data. This data represents an asset which enables companies to engage in data-driven innovation, helping them improve their understanding of customers’ demands, habits, and needs. Enabling personal data mobility may provide a consumer-led tool that will increase use of new digital services, providing companies with an easier way to compete and grow in data-driven markets. However, in some markets, the key to effective competition may be to grant potential competitors access to privately held data. Such efforts, however, need to be very carefully balanced against both commercial rights and concerns about privacy. Digital platforms are already making an increasing amount of data open. Continuing to encourage this is important, but so is understanding additional steps that could foster more open data.

Thank you very much for your work on these important issues and I look forward to your questions.

Heather Boushey “On Reddit”: “I’m Heather Boushey, president and CEO of the Washington Center for Equitable Growth, and author of the forthcoming book, Unbound: How Inequality Constricts Our Economy and What We Can Do About It. The latest economic research from across academic disciplines shows the many ways that high economic inequality—in incomes, wealth, and across firms—serves to obstruct, subvert, and distort the processes that lead to widespread improved economic well-being.”

Unpredictable and chaotic work schedules are turning out to be an extra source of inequity that is, at least to me, surprisingly large. About the only half-silver lining is that Great Britain appears to be even worse. Read Cesar Perez and Alix Gould-Werth, “How U.S. workers’ just-in-time schedules perpetuate racial and ethnic inequality,” in which they write: “In an attempt to minimize labor costs, employers in today’s U.S. economy saddle workers with last-minute and low-quality schedules. These schedules, sometimes referred to as ‘just-in-time schedules,’ are unpredictable, unstable, and often provide workers with an insufficient number of hours. Today, sociologists Kristen Harknett at the University of California, San Francisco and Daniel Schneider at the University of California, Berkeley released new analyses drawing from surveys with 30,000 retail and food workers at 120 of the largest retail and food service companies in the United States to show who suffers from these schedules.”

An excellent piece from Fiona Scott Morton on the current state-of-play in antitrust is well worth re-elevating amid rising concern about market power among U.S. policymakers. Read her “Modern U.S. antitrust theory and evidence amid rising concerns of market power and its effects: An overview of recent academic literature,” in which she writes: “The experiment of enforcing the antitrust laws a little bit less each year has run for 40 years, and scholars are now in a position to assess the evidence. The accompanying interactive database of research papers for the first time assembles in one place the most recent economic literature bearing on antitrust enforcement … Horizontal mergers … Vertical mergers … Exclusionary conduct … Loyalty rebates … Most Favored Nation clause … Predation … Common ownership … Monopsony power … Macroeconomics and market power.”

Worthy reads not from Equitable Growth:

Let me highlight this once again: The very sharp Martin Wolf reacts to the Business Roundtable’s recognition that it and the corporations of which it consists need to take on a much broader system-stabilization role. In my view, the first thing the Business Roundtable and its fellow travelers need to do is to recover control of the political right from the armies of political and media grifters. They need to weigh in on what right-wing politicians ought to stand for. So far they have not. Read Martin Wolf, “Why rigged capitalism is damaging liberal democracy,” in which he writes: “Economies are not delivering for most citizens because of weak competition, feeble productivity growth, and tax loopholes … The U.S. Business Roundtable, which represents the chief executives of 181 of the world’s largest companies, abandoned their longstanding view that ‘corporations exist principally to serve their shareholders’ … What does—and should—[this] moment mean? The answer needs to start with acknowledgment of the fact that something has gone very wrong. Over the past four decades, and especially in the United States, the most important country of all, we have observed an unholy trinity of slowing productivity growth, soaring inequality, and huge financial shocks … The economy [is] not delivering … in large part … [because of] the rise of rentier capitalism … Market and political power allows privileged individuals and businesses to extract a great deal of such rent from everybody else … If one listens to the political debates in many countries, notably the United States and the United Kingdom, one would conclude that the disappointment is mainly the fault of imports from China or low-wage immigrants, or both. Foreigners are ideal scapegoats. But the notion that rising inequality and slow productivity growth are due to foreigners is simply false … Members of the Business Roundtable and their peers have tough questions to ask themselves. They are right: Seeking to maximize shareholder value has proved a doubtful guide to managing corporations. But that realization is the beginning, not the end … We need a dynamic capitalist economy that gives everybody a justified belief that they can share in the benefits. What we increasingly seem to have instead is an unstable rentier capitalism, weakened competition, feeble productivity growth, high inequality, and, not coincidentally, an increasingly degraded democracy. Fixing this is a challenge for us all, but especially for those who run the world’s most important businesses.”

There is no single effect of “automation” on the workforce and the labor market. It is long past time for us to dig deeper, and here is a good piece of spadework. Read Sotiris Blanas, Gino Gancia, and Tim Lee, “How different technologies affect different workers,” in which they write: “Since the early 1980s, technology has reduced the demand for low- and medium-skill workers, the young, and women, especially in manufacturing industries. The column investigates which technologies have had the largest effect, and on which types of worker. It finds that robots and software raised the demand for high-skill workers, older workers, and men, especially in service industries … From 1982 to 2005, using data from 30 industries spanning roughly the entire economies of 10 high-income countries … We used the Dictionary of Occupational Titles and the Occupational Information Network to evaluate which jobs are more prone to automation based on the type of tasks they require … Industrial robots decrease low-skill employment, while they increase the income shares of high- and medium-skill workers, old workers, and men … In manufacturing, robots lower low-skill, young, and female employment, while in services, they increase medium-skill and male employment. In both sectors, robots increase the income shares of high-skill, old, and male workers. Our results are consistent with the view that robots replace workers who perform routine tasks, especially in sectors where automation is more widespread, such as manufacturing. By contrast, they increase employment and incomes in sectors where automation has started more recently, such as in services, a sector in which new occupations are appearing. Given the industrial and occupational composition of these sectors, that robots are likely to complement engineers, product designers, and managers—that is, occupations that are dominated by high-skill, more senior, and male workers. Software has a similar effect to robots, whereas Information and Communications Technology, or ITC, capital is associated with employment gains mostly for medium- and low-skill workers.”

Moving to carbon-free electricity by 2050 is remarkably cheap, argues Geoffrey Heal. Read his “The Cost of a Carbon-Free Electricity System in the U.S.,” in which he writes: “I calculate the cost of replacing all power stations in the United States using coal and gas by wind and solar power stations by 2050, leaving electric power generation in the country carbon free. Allowing for the savings in the cost of fossil fuel arising from the replacement of fossil fuel plants, this is roughly $55 billion annually. Allowing, in addition, for the fact that most fossil plants in the United States are already old and would have to be replaced before 2050 even if we were not to go fossil free, this annual cost is reduced to $23 billion.”

Yes, rural Kansas is now, in some ways, reminiscent of 17th century England. Read Cory Doctorow, “In Kansas’s poor, sick places, hospitals and debt collectors send the ailing to debtor’s prison,” in which he writes: “Kansas is a living laboratory for far-right experimentation with extreme economic cruelty: a state where Medicare expansions were thwarted, where xenophobia has penetrated the state bureaucracy, where a grifty, incompetent lawyer has apologized for slavery and driven women out of his own party, even as neighboring states thrive by tending to the needs of working people, rather than the super-rich. As Kansas sinks into poverty and ruin, its people are growing ever-sicker: Poverty is strongly correlated with poor health outcomes, especially in America, where being poor means you can’t afford preventative care, and even more especially in Kansas, where limits on Medicare expansion exclude even very poor people from access to subsidized care. Enter hospital debt collectors. Propublica’s Lizzie Presser reports from Coffeyville, Kansas, home to Coffeyville Regional Medical Center, the only hospital for 40 miles, now that its rivals have all shut down. In Coffeyville, magistrate judges are appointed, and need no special training to hold the office. Judge David Casement—a cattle rancher who never studied law—presides over medical debt cases, which he hears quarterly at ‘debtor’s exam’ days. At these proceedings, debt collectors—who do have law degrees, and whom the judge relies heavily on for legal advice—are allowed to quiz sick people, or the parents or spouses of critically ill or dying people, about their assets and income and to ask the judge to order them to divert what little they have to Coffeyville Regional Medical Center, minus the debt collector’s healthy cut. But sick, poor people can’t always afford to travel to the courthouse: Sometimes, it’s because they have to go see a specialist (or take their kid or spouse to see one); sometimes it’s because they had to sell their car to make a previous debt payment. When this happens, debt collectors like Michael Hassenplug from Account Recovery Specialists Inc. can ask the judge to issue a warrant for the debtor, who is taken to the local jail and hit with $500 in bail. Many can’t pay it, and stay in jail (Hassenplug insists that they’re not in jail for their debts, but rather for their failure to appear), while others who manage to borrow the $500 often find that it is then surrendered to the hospital and its arm-breakers. Meanwhile, the debts mount: In addition to punitive, usurious interest, the hospital and its debt-collectors reserve the right to lard on fees, fines, and penalties.”

Heather Boushey

Washington Center for Equitable Growth

Testimony before the Joint Economic Committee,

Hearing on “Measuring Economic Inequality in the United States”

October 16, 2019

Thank you, Chairman Lee and Vice Chair Maloney, for inviting me to speak today. It’s an honor to be here.

My name is Heather Boushey and I am President and CEO of the Washington Center for Equitable Growth. We seek to advance evidence-backed ideas and policies that promote strong, stable, and broad-based economic growth.

By any measure, income inequality in the United States has increased significantly over the past 40 years. This increase in inequality has constricted the growth of our economy and had an insidious effect on our political institutions. The topic of today’s hearing speaks to a small but significant step we can take toward more equitable growth.

One of the most important things we can do to fight inequality in the United States right now is to start keeping track of it. Government statistics—Gross Domestic Product growth, inflation, jobs added, wage increases—drive economic policymaking in Congress, the Federal Reserve, and executive agencies. Better measurements of inequality are overdue additions to this list.

To properly contextualize economic growth, policymakers should ask the U.S. Bureau of Economic Analysis, or BEA, to add measures of growth within income quantiles to the National Income and Product Accounts. This is what we at Equitable Growth call “GDP 2.0”—an extension to our existing National Income accounts that updates them to better reflect the realities of our 21st century economy.

I want to thank Vice Chair Maloney and Sen. Heinrich, as well as Senator Schumer, for introducing a bill in 2018 that would do just that and for continuing their efforts in this Congress. The Measuring Real Income Growth Act of 2018 would tell us what growth looks like for low-, middle-, and high-income Americans.

This bill would task the Bureau of Economic Analysis with adding distributional measures of growth to its quarterly National Income and Product Account releases so we could see not just that the economy grew by 2 percent or 3 percent, but also how much it grew for Americans of different incomes.

Publishing this information would have four important effects.

First, it will connect the idea of aggregate economic data to the real-life circumstances of families in the economy. When members of the working class see politicians touting strong growth but look around and see no evidence of it in their communities, they are right to feel that their economic needs are not being paid attention to.

Second, by highlighting differences in how the economy is working for different groups of workers, it will focus our attention on the economic well-being of most families.

Third, distributional measures of growth will guide policymakers in designing policies that both raise output and do it in a way in which everyone gains.

Finally, these metrics will allow citizens to hold their elected representatives accountable to delivering an economy that works for all.

It is critical to start capturing this data so we can ensure strong, stable, and broad-based economic growth. There is a large—and growing—body of empirical research that shows we cannot create strong or broadly shared economic gains through a policy agenda that presumes growth follows from allowing those at the top to reap the bulk of the gains. The policy agenda we have pursued for decades, driven largely by the desire to maximize GDP growth at any cost, is not delivering for American families and is creating inequities in the economy that actually constrict growth.

In the sections that follow, I will explain why GDP growth became such an important indicator of economic success, how it became a poor proxy for the success of the average American family, and why we need a GDP 2.0 to better capture the full range of economic progress that is experienced by Americans up and down the income ladder. In the final section, I explain how inequality is constricting growth in the economy.

One number for an entire economy

The National Income and Product Accounts were pioneered in the 1930s by the economist Simon Kuznets. At the time, it was a radical new development in economic measurement. It let policymakers see for the first time just how much had been lost in the Great Depression and later helped them understand how the U.S. economy could be harnessed to go to war. For this groundbreaking work, Kuznets won the Nobel Memorial Prize in economics.

The member nations of the Organisation for Economic Co-operation and Development, or OECD, at the time adopted Kuznets’ principals as a general framework and National Accounts became a global phenomenon. GDP, the most prominent measure of aggregate output in the National Accounts, has attained a unique level of authority to the exclusion of other markers of a nation’s development. Because it is standardized across nations and available as a relatively long time series, economists and policymakers alike have latched onto GDP as a way to adjudicate which national economies are best and to conduct inquiries into what makes some economies grow faster than others.

But this was never the intent of Kuznets himself. In a section of his 1934 report to Congress titled “Uses and Abuses of National Income Measurements,” Kuznets noted that, “The welfare of a nation can, therefore, scarcely be inferred from a measurement of national income.”3 This is true for many reasons, but Kuznets was especially concerned with the distribution of resources in society. He understood that high aggregate output was not necessarily indicative of well-being if the underlying distribution of income was highly unequal. To address this concern, he helped compile some of the very first breakdowns of inequality by income quintile. For a short time in the 1950s, BEA regularly produced these statistics, but they were abandoned due to a lack of funding.4

Kuznets’ warnings have been repeated many times in the 85 years since he authored his report to Congress. Robert Kennedy famously echoed Kuznets’ warning when he said that GDP “measures everything … except that which makes life worthwhile.”5

GDP growth has been treated for decades by pundits and policymakers alike as synonymous with prosperity, but this is no longer a useful indicator of well-being. President John F. Kennedy famously alluded to it when he said that “a rising tide lifts all boats.” In the decades since, economists and commentators have used the metaphor of “growing the pie” to indicate that we should first and foremost be concerned with growing the economy rather than concerning ourselves with who gets a slice. But the pie is no longer growing for many Americans because much of the growth of the past four decades has been captured largely by Americans at the top of the income distribution.

Rising inequality means less informative aggregate statistics

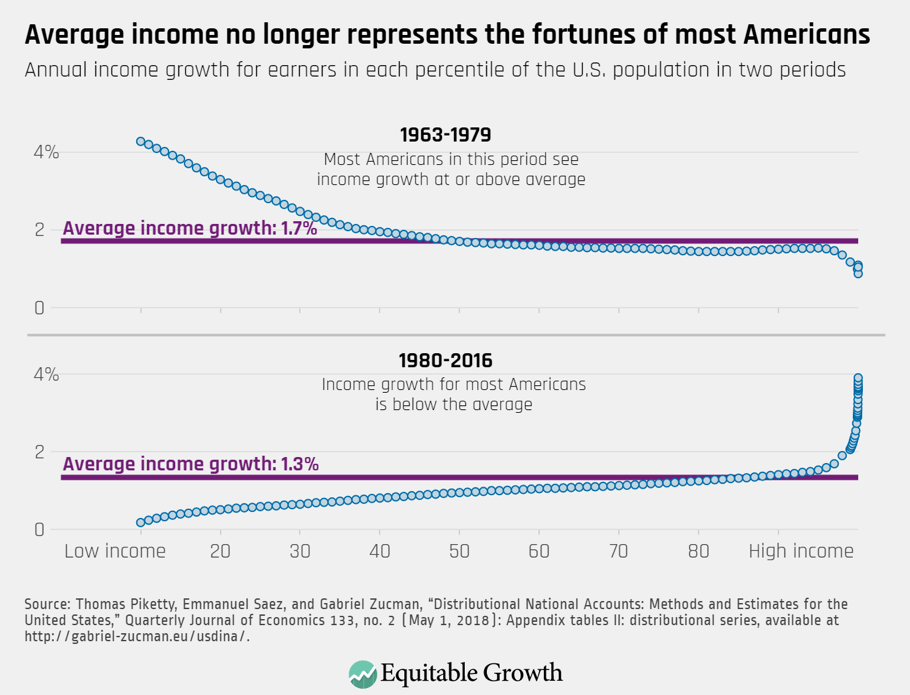

Over the period from 1980 to 2016, average growth was about 1.4 percent annually. Yet the bottom 85 percent of all adults saw income growth lower than this. Only those in the top 15 percent experienced better-than-average growth.6 (See Figure 2.)

Figure 2

This is a new phenomenon. Prior to this period, there was little need to disaggregate national growth because the headline GDP growth statistic was broadly representative of the economy as experienced by most Americans. Average growth was around 1.7 percent between 1963 and 1979—higher than in the years since. And that growth was broadly shared, as the scatter plots of pretax and post-tax income growth for each percentile of income show in Figure 2. Most Americans saw income growth at or above that average.

Today, GDP growth is decoupled from the fortunes of most Americans. What was once a useful indicator of how most families were faring is now unmoored from the experience of most families. Today’s economy is growing slower than in the past, and much of this growth benefits only those at the very top of the economic ladder. Incomes for the working class and the middle class have grown slowly for decades while incomes at the very top have exploded.

Between 1980 and 2016, the bottom half of Americans by income saw average annual income growth of just 0.6 percent. The richest 10 percent of Americans, by contrast, enjoyed annual income growth of 2 percent, resulting in this group doubling their income over the 35-year period. But even they were left behind by the top 1 percent, who saw their income increase by 162 percent over the same period.7

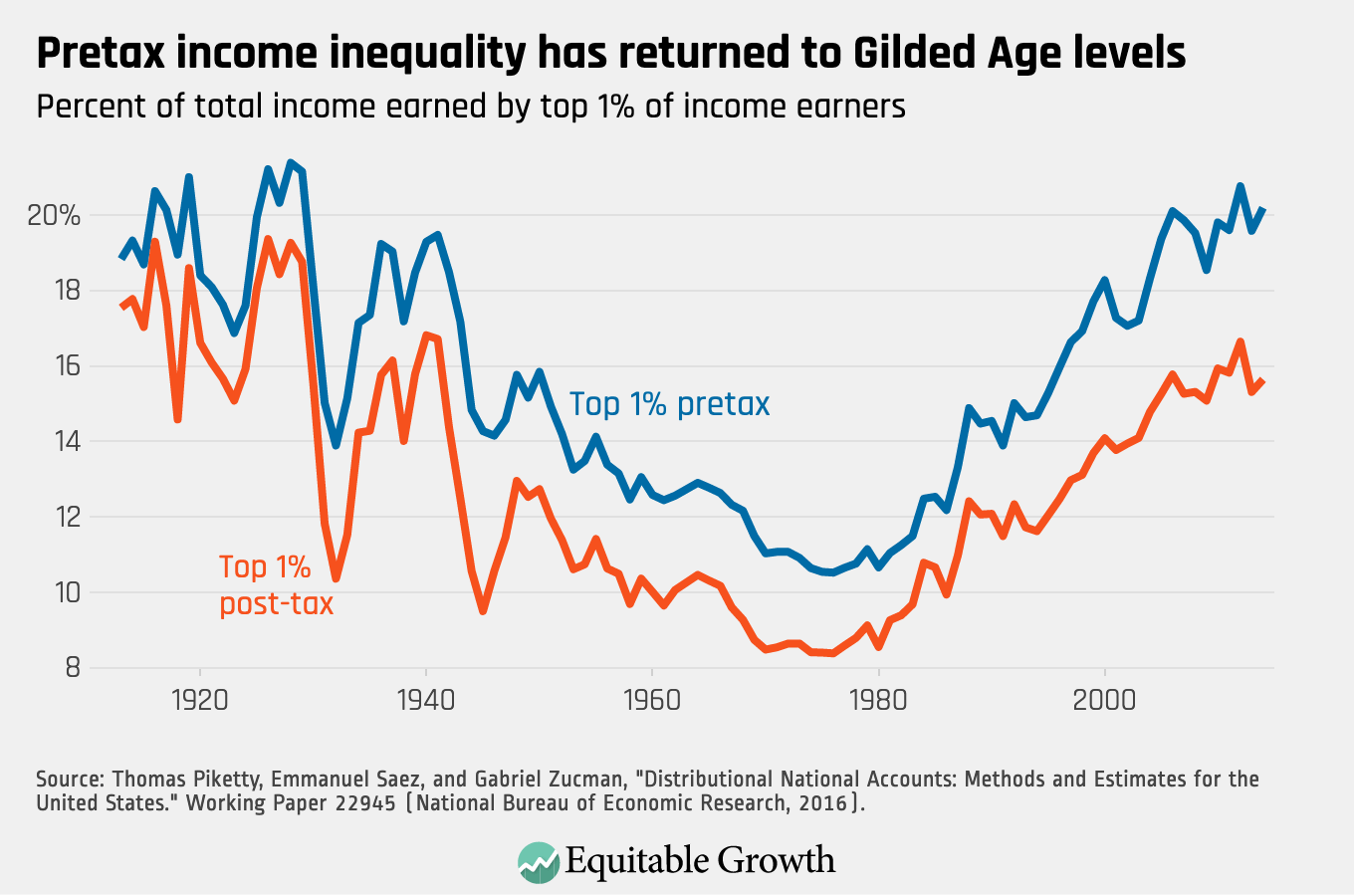

The result is that the pretax distribution of income has returned to the Gilded Age levels of the 1920s. The story is not quite so dramatic after government taxes and transfers, but by either measure, the share of total national income held by the top 1 percent has nearly doubled since hitting lows in the 1970s. (See Figure 3.)

Figure 3

We see these same divergent trends across multiple measures of economic well-being: wages, income, and wealth. The implication for how we evaluate the economy is that mean economic progress is pulling away from median economic progress. Almost all of our national economic statistics are becoming less representative of the experience of most Americans. Reforming our national statistical infrastructure to account for this reality is long overdue.

GDP 2.0: Measuring what matters

GDP 2.0 refers to adding subpopulation estimates of income growth to our existing National Income and Product Accounts reports. Currently, the Bureau of Economic Analysis releases a new estimate of quarterly or annual GDP growth every month. Distributional national accounts would add to some of these releases an estimate that disaggregates the topline number and tells us what growth was experienced by low-, middle-, and high-income Americans.

Academics have already constructed such a measure. The Distributional National Accounts (or DINA) dataset constructed by economists Thomas Piketty, Emmanuel Saez, and Gabriel Zucman disaggregates National Income growth from 1962 to 2016.8 This dataset gives us a complete picture of how inequality has changed in the United States over time and how recent growth in national output is being shared by Americans. In 2014, for example, total National Income growth was 2.1 percent. According to the DINA dataset, income growth for the lowest-earning 50 percent of all Americans was just 0.4 percent, while growth for the richest 1 percent of Americans was 5.3 percent.

The Bureau of Economic Analysis has begun studying how it could create its own similar dataset and has published preliminary findings for a small number of years in its Survey of Current Business.9

Members of Congress have also realized the importance of constructing these new indicators. In 2018, Sens. Charles Schumer (D-NY) and Martin Heinrich (D-NM) and Rep. Carolyn Maloney (D-NY) introduced the Measuring Real Income Growth Act of 2018 in both chambers. The Senate bill garnered 24 co-sponsors.

This initial legislative action has been followed by a flurry of further congressional interest. In March 2019, the conference report accompanying the Consolidated Appropriations Act of 2019 included a clause instructing Bureau of Economic Analysis to report income growth within deciles of income starting in 2020.10 In their appropriations bill for the Department of Commerce for FY2020, House appropriators instructed the agency to report on its progress toward the FY2019 appropriations language.11 Most recently, Senate appropriators allocated $1 million to the effort.12

It is expected that Bureau of Economic Analysis will publish a prototype set of distributional growth figures in 2020 in accordance with these instructions from Congress.

GDP 2.0 will inform policy

Distributional national accounts will be an important tool for crafting policy in today’s unequal economy. To give one powerful example, distributional national accounts might have allowed policymakers to spot and correct the significant decline in absolute intergenerational income mobility in the United States that occurred over the past 60 years.

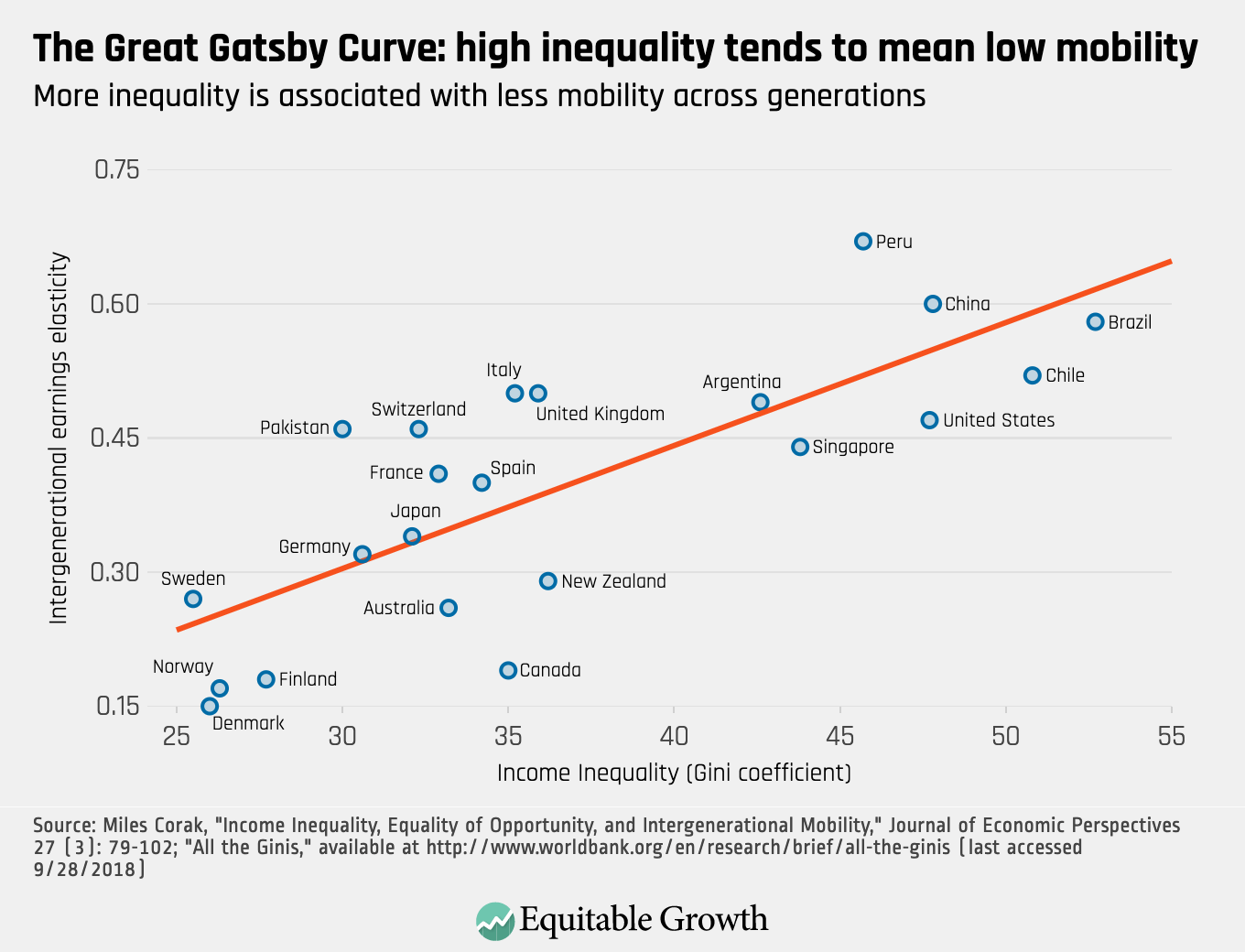

It is intuitively unsurprising that societies with higher inequality are also societies with low economic mobility. Economist Miles Corak created what former Chair of the Council of Economic Advisers Alan Krueger called “The Great Gatsby Curve,” which plots the relationship between inequality and intergenerational mobility across countries. Countries with higher inequality tend to have lower economic mobility. Figure 4 shows one version of this curve.

Figure 4

While critics often suggest that the relationship is not causal, more recent research shows that increasing inequality in the United States has significantly reduced absolute intergenerational mobility. Economist Raj Chetty has shown that children born in 1940—just before the baby boom, when inequality was low and growth was high—had a 90 percent chance of earning more than their parents. In contrast, Generation Xers born in 1980, when income inequality was high and growth was low, have just a 50 percent chance of surpassing their parents’ income.13

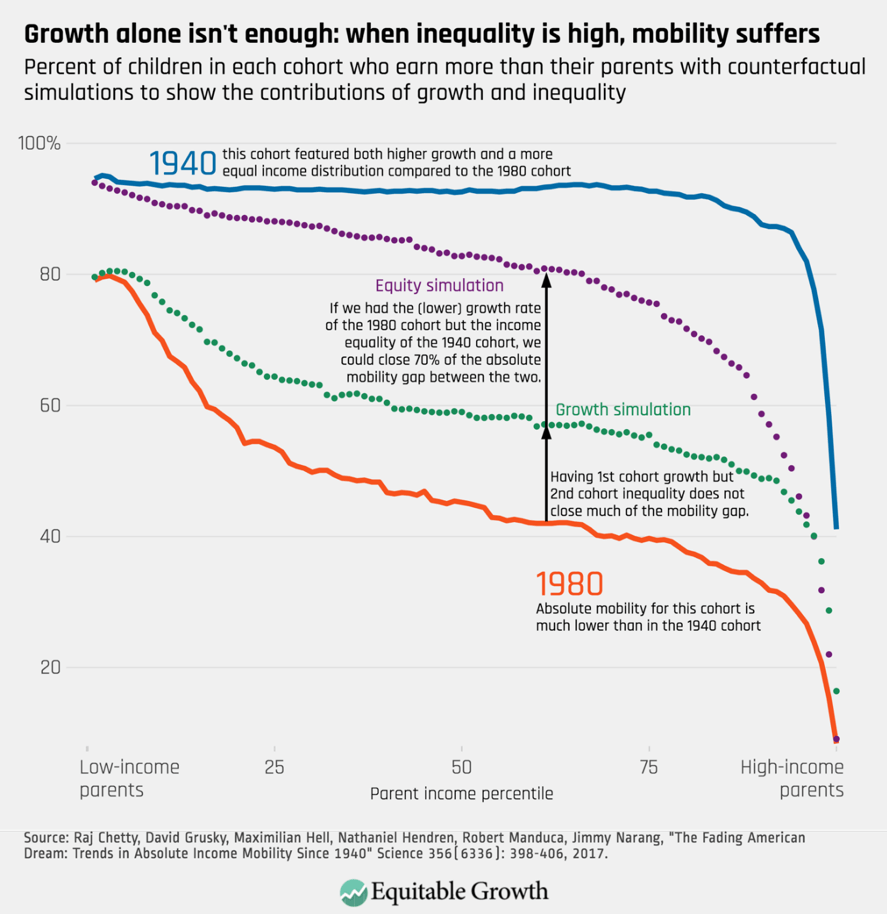

More importantly, the evidence shows that even if children born in 1980 had experienced the same higher growth experienced by children born in 1940, this would have closed only about one-third of the mobility gap. But if children born in 1980 had instead faced the same levels of inequality as children in 1940 (even with the lower growth), this would have closed two-thirds of the mobility gap. Figure 5 illustrates rates of absolute mobility by parent income percentile and shows these counterfactuals.

Figure 5

The implication is clear: Growth alone is not enough to produce strong absolute mobility. Distributional national accounts would allow us to track how growth is distributed annually and manage the economy accordingly to increase economic mobility. Notably, to diagnose this problem, it is not enough to know that median household income is stagnant. Understanding how mobility might be changing requires a complete picture of how growth is accruing to families all along the income curve, including at the very top.

GDP 2.0 will help families understand the economy

In addition to helping policymakers craft responses to changes in our economy, GDP 2.0 will also help families across the country understand how economic growth is related to their own personal circumstances. The separation of average growth from the experience of most Americans, as demonstrated above, leaves many feeling alienated when media trumpets high growth that does not reflect their own situation or the situation of those in their communities. GDP 2.0 will help people understand how the economy is working for them.

Equally importantly, when the economy is not working for families up and down the income curve, that information will be widely known and voters will be empowered to hold policymakers accountable if the economy is not performing for all Americans. This link is important, because inequality isn’t simply bad for some families at the bottom of the income distribution. Inequality is bad for the economy itself.

Economic inequality is bad for the economy

The most critical reason we need to measure who is prospering from growth is because the levels of inequality we see now are harming our economy. Inequality constricts growth by:

Obstructing the supply of people and ideas into our economy and limiting opportunity for those not already at the top, which slows productivity growth over time

Subverting the institutions that manage the market, making our political system ineffective and our labor markets dysfunctional

Distorting demand through its effects on consumption and investment, which both drags down and destabilizes short- and long-term growth in economic output

Inequality obstructs the supply of talent, ideas, and capital

The economic circumstances into which children are born affect children’s development in everything from their health to their ability to focus at school to their educational opportunities, and these, in turn, affect their economic outcomes as adults. Research by economists shows the links between factors such as children’s varying birth weights and their different levels of school performance, job-holding, and earnings as adults, relative to others with similar skillsets.

Even when children have access to skills, inequality obstructs their contributing to the economy to the best of their abilities, and these obstructions hinder productivity and growth. Research led by Harvard’s Chetty measured what is more important to earning a patent later in life: scoring high on childhood aptitude tests or parental income. Disturbingly, the richer the family, the more likely the child will be to earn a patent—far outweighing demonstrated intelligence. If a child who shows aptitude early on cannot climb the income and wealth ladder, then there’s something broken in the way our economy works. Inequality has blocked the process and, as result, drags down national productivity by making our workforce less capable than it could be and our economy less innovative.

Inequality subverts the institutions that manage the market

Growing inequality is subverting the public institutions and the policymaking processes we need to support our economy. It discourages a focus on the public interest and promotes the efforts of firms to accrue larger profits than truly competitive markets would allow.

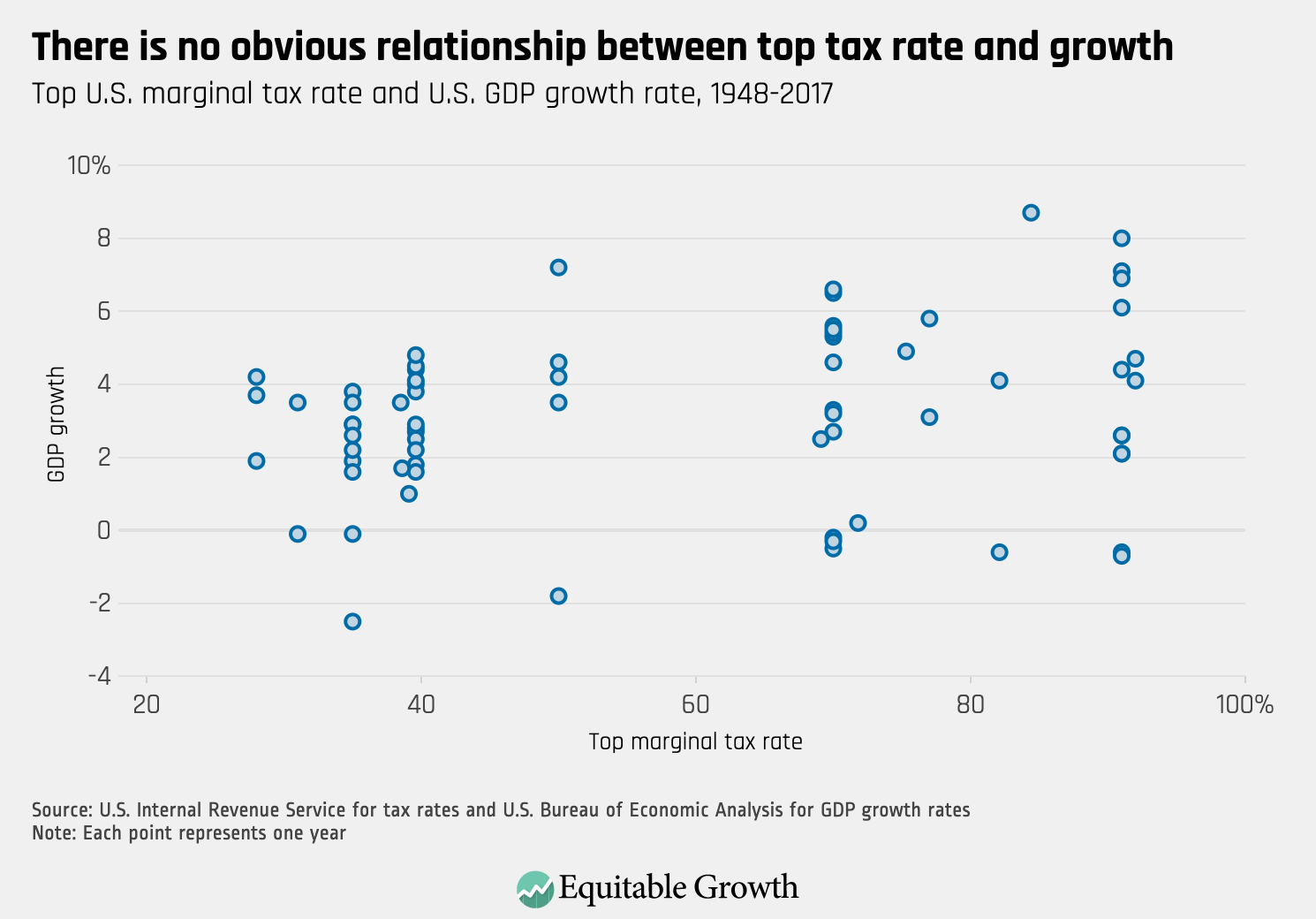

Today, firms are able to manipulate the functioning of the marketplace because economic inequality gives their owners the financial wherewithal to wield political influence. By exerting pressure on political processes, they can minimize the taxes on firms, owners of capital, and top-salaried workers. And they can rewrite laws and regulations in their favor. Research shows that lower taxes on those at the top of the income ladder do not lead to the kinds of beneficial outcomes some economists and policymakers suggest. The evidence is that when the rich pay less in taxes, it encourages them to act in unproductive ways. (See Figure 6.)

Figure 6

When a firm has too much power in its product or services market, it has monopoly power, which means it can raise prices with impunity and stymie competition. Indeed, our economy is increasingly dominated by a few firms in many industries. In healthcare markets, the biggest healthcare companies are increasing their stronghold by merging and then charging higher prices, which, in turn, leads to higher profits for managers and shareholders alongside less affordable—and sometimes lower quality—healthcare for everyone else. It also means lower wages for those working increasingly in what economists call “monopsony labor markets,” where there’s only one or a handful of employers in a given market, giving these firms outsized wage-setting power. What’s happening in healthcare is emblematic of changes across our economy.

By subverting our economy in various ways, inequality undermines confidence that institutions of governance can deliver for the majority. But for the economy to function, the public sector needs to function, and function well. In the 19th and 20th centuries, the U.S. government implemented policies that launched many families into prosperity with a solid financial foundation, including the Homestead Act, the estate tax, universal primary and secondary schools and land grant colleges across the nation, and the GI Bill. These policies weren’t perfect and were discriminatory in multiple ways, but they showed that the federal government could embark on big agendas to reduce inequality. Today, however, inequality in wealth and power is thwarting the government from taking on collective endeavors that provide the foundation for broad-based economic growth while promoting the interests of monopolists and oligopolists over others.

Inequality distorts both consumption and investment

Inequality distorts everyday decision-making by consumers and businesses. These outcomes are evident at the macroeconomic level. People’s spending drives business investment, as consumers account for nearly 70 cents of every dollar spent in the United States. But for the past several decades, U.S. families in the bottom half of the income distribution have seen no income gains, and the gains for those families not among the top 10 percent of income earners have been meager. This means that if firms were to invest more, they may not be able to sell additional goods and services because consumers might not be in positions to buy them.

Many businesses, eyeing demand, have understandably not invested much over this period. U.S. firms are sitting on record-high piles of cash, which have been steadily accumulating since the 1980s.14 Others have found customers willing to purchase their wares, but only because of the financially unstable expansion of household debt—as seen especially in the run-up to the Great Recession in the middle of the past decade, and as is occurring again today.15 Growing economic inequality thus destabilizes spending because everyday consumers either don’t have enough money to spend or are borrowing beyond their means to buy what they need.

Inequality is even driving changes in what firms are producing, with a number of economic implications for innovation and even inflation. Xavier Jaravel at the London School of Economics finds that businesses are investing in new products targeted at high-end consumers while developing fewer products for those in the lower end of the market. For those at the low end, there’s less competition for their business, which means lower productivity, lower innovation, and higher prices and inflation. This shows up in the data: Jaravel found that between 2004 and 2013, families with incomes greater than $100,000 per year saw yearly prices rise by 0.65 percent less than for families earning below $30,000 in the respective bundles of goods that those families bought.

With consumption dragged down by flagging middle-class incomes, too much money in the hands of those at the top, and investors sitting on the sidelines, conditions are ripe for an increase in the supply of credit. The deregulation of the financial sector over the past 40 years has made it easier to lend to U.S. households—in no small part due to the influence of the financial services industry. Empirical research and the U.S. experience over the past several decades show the consequences of these distortions and how credit-driven economic growth both increases economic instability and leads to lost economic opportunity.

Conclusion: Measure who prospers when the economy grows

Simon Kuznets knew that tracking GDP growth was not the endpoint for his National Income and Product Accounts. Much more needed to be done to ensure that the National Accounts were not just accounting tables but also could, in fact, say something meaningful about the well-being of American families. But despite some early progress toward adding a distributional component to the accounts in the 1950s, little changed over the next seven decades. It is time to fulfill this promise. Implementing GDP 2.0 will change our economic narrative and focus us on achieving broad-based growth. A new commitment to fighting inequality will, in turn, yield dividends for our economy.

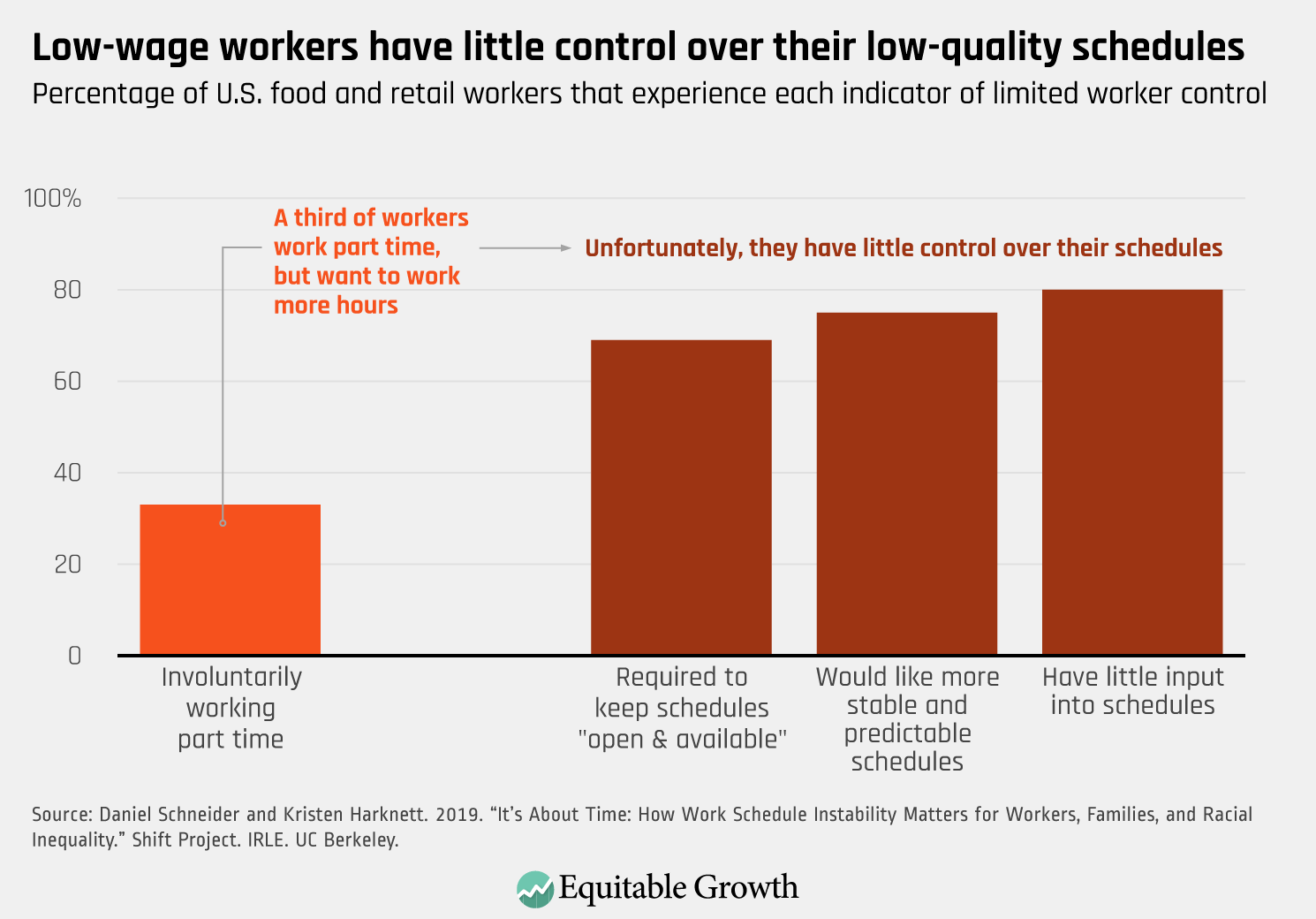

In an attempt to minimize labor costs, employers in today’s U.S. economy saddle workers with last-minute and low-quality schedules. These schedules, sometimes referred to as “just-in-time schedules,” are unpredictable, unstable, and often provide workers with an insufficient number of hours. Today, sociologists Kristen Harknett at the University of California, San Francisco and Daniel Schneider at the University of California, Berkeley released new analyses drawing from surveys with 30,000 retail and food workers at 120 of the largest retail and food service companies in the United States to show who suffers from these schedules, and how.

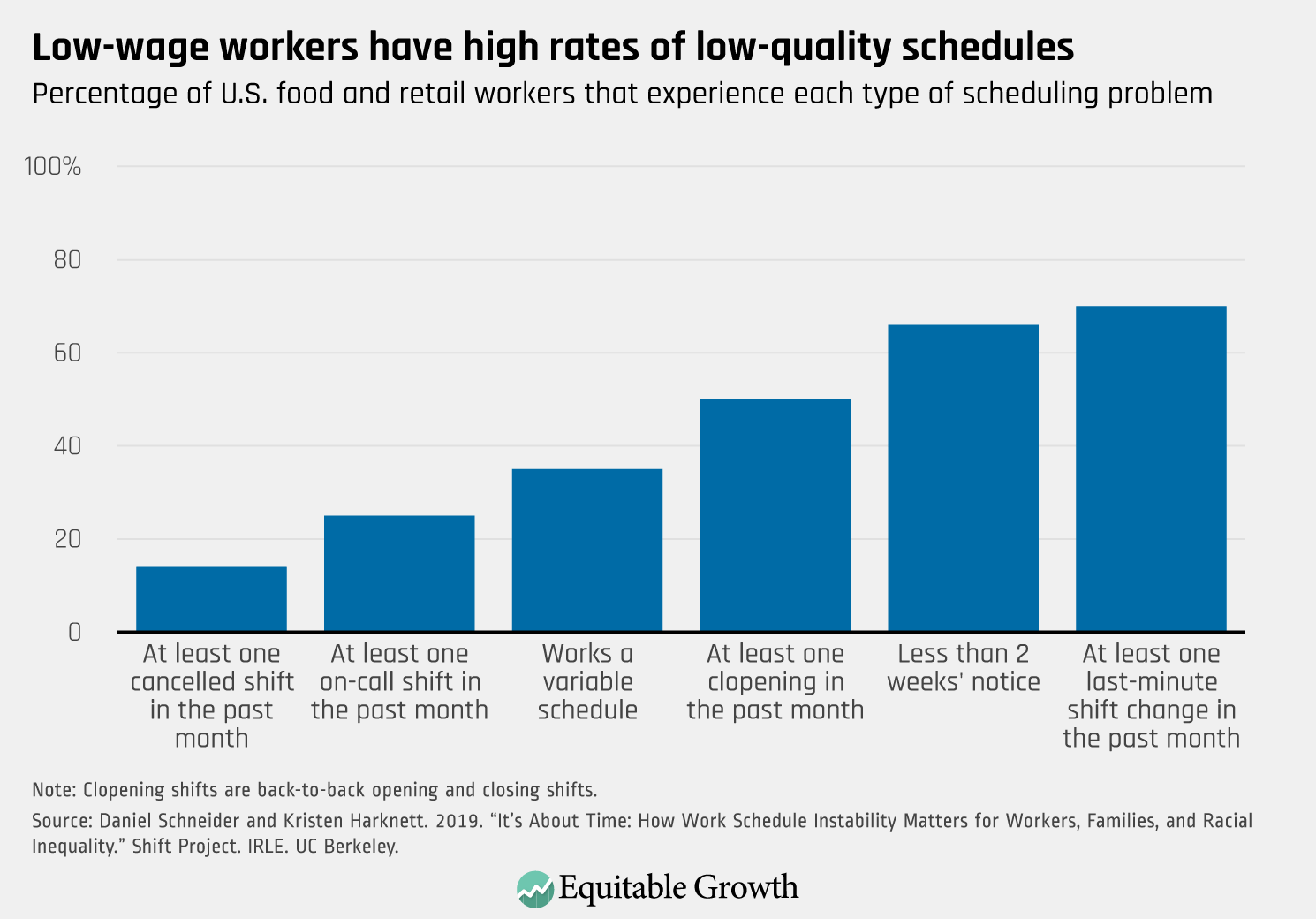

Bad schedules, sometimes referred to as “just-in-time schedules,” are common for low-wage workers: Nearly 3 in 4 workers experience last-minute shift changes, two-thirds have less than 2 weeks’ notice of their schedules, and many face back-to-back closing and opening shifts, or “clopening” shifts, and on-call shifts.

Figure 2

Employers often talk about these practices as being “flexible,” which implies that schedules bend to the needs of workers. In reality, workers have little control over their schedules.

Figure 3

Bad schedules are prevalent, but they’re not distributed equally across the population. Workers of color experience more schedule instability than white workers, and the disparity is largest for women of color and Latinx workers. The disparity remains even when looking at similar workers employed by the same companies.

Figure 4

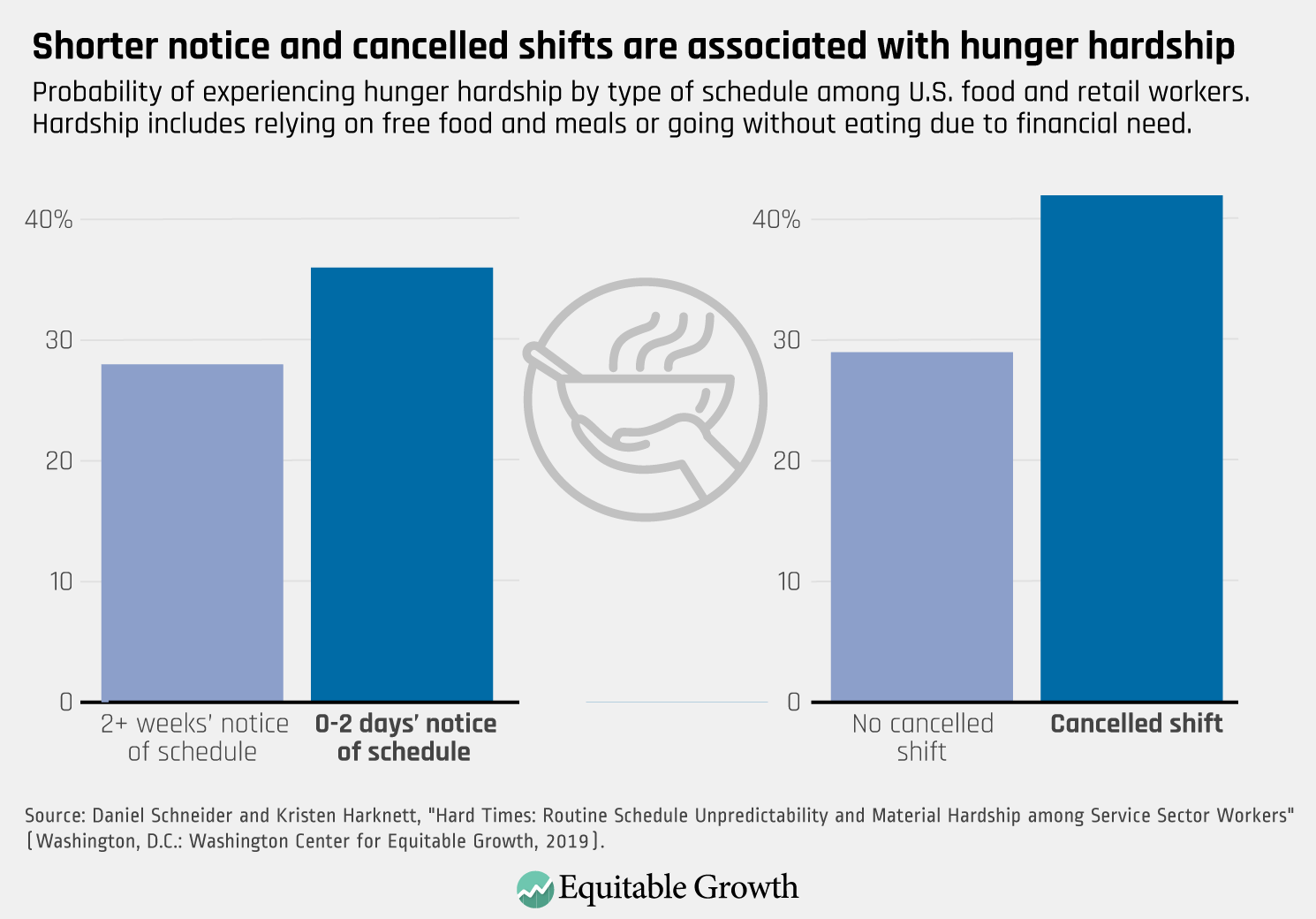

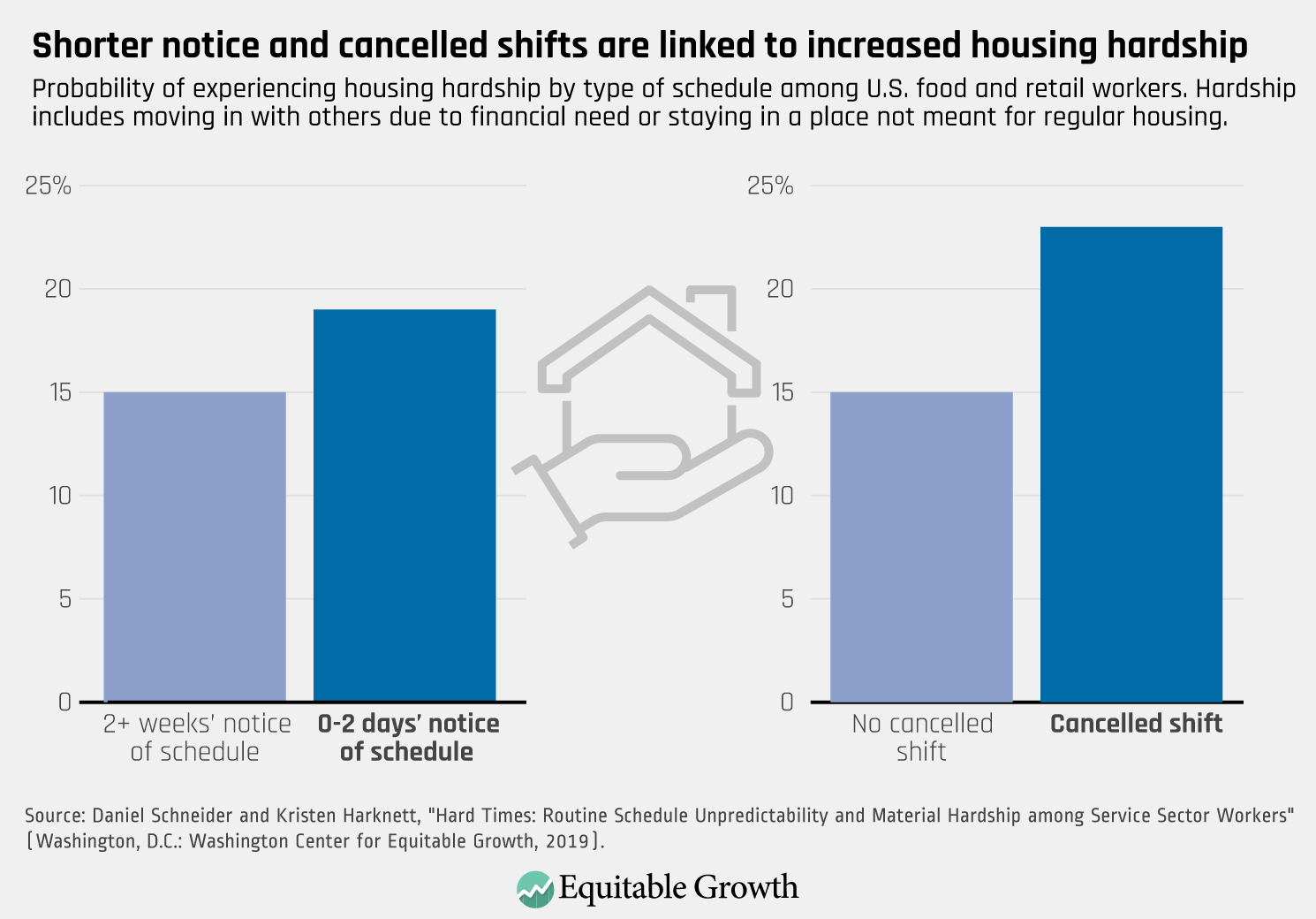

When hours fluctuate unpredictably, it is hard for workers to budget for necessities. Workers with just-in-time schedules are more likely to skip meals or rely on food pantries.

Figure 5

They are also more likely to find themselves moving in with other people to save money, or staying in shelters, cars, or abandoned buildings.

Figure 6

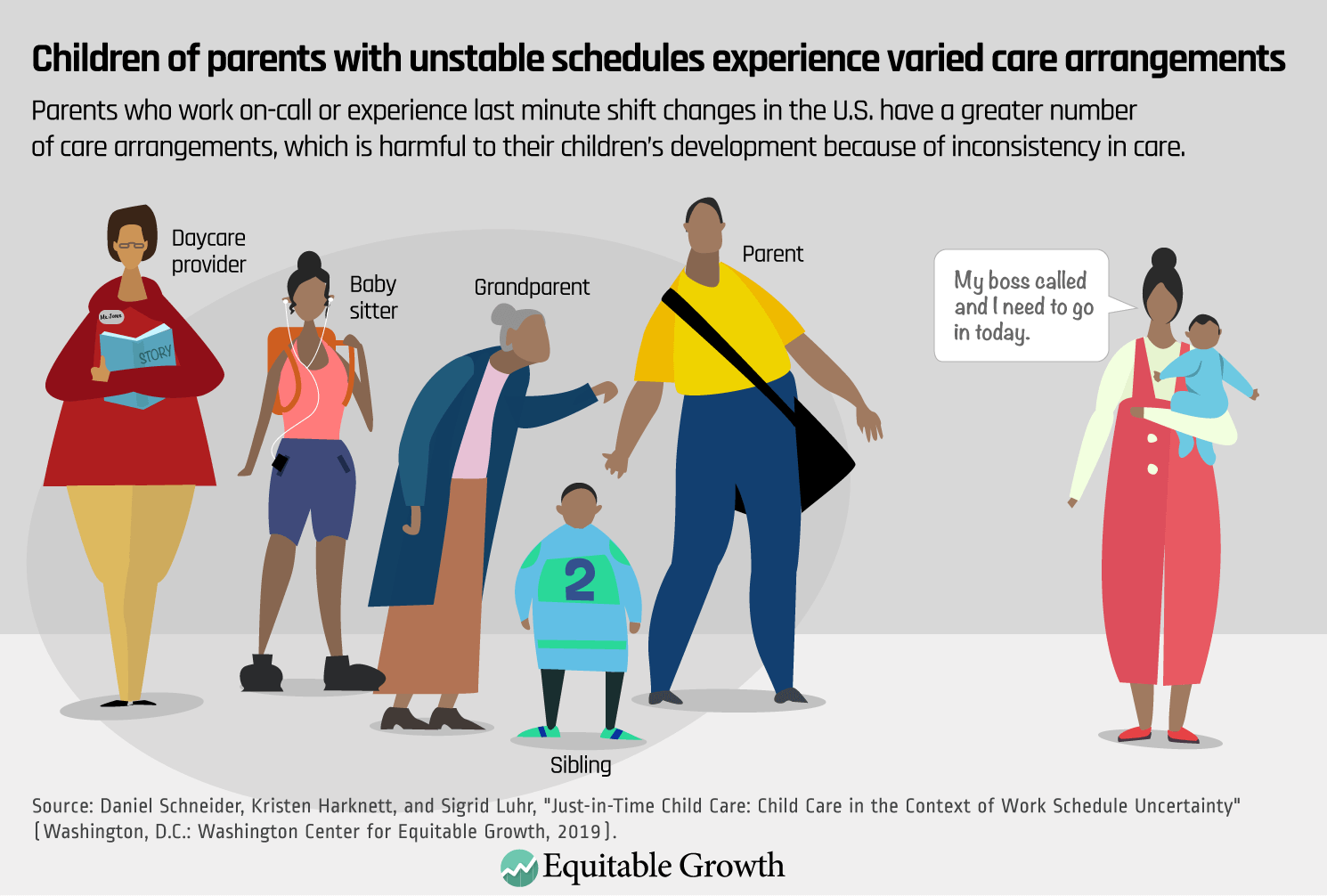

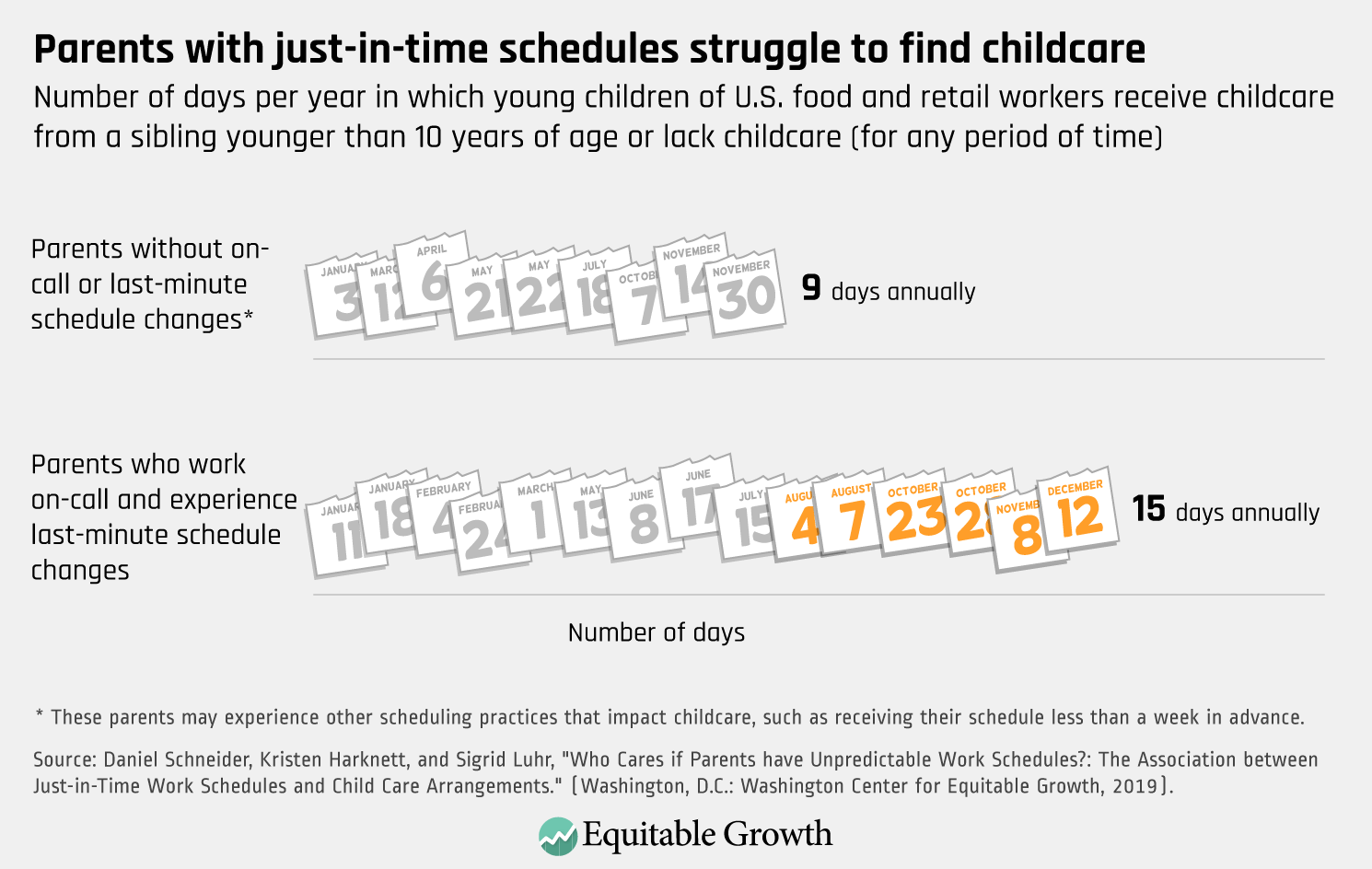

The problems posed by unstable and unpredictable work schedules ripple to the next generation. Parents with just-in-time schedules are more likely to rely on a patchwork of childcare providers, which can undermine childrens’ relationships to caregivers and increase stress, especially for very young children.

Figure 7

They also struggle to find satisfactory childcare at all: Their children experience moments in which they are cared for by a young sibling or have no childcare six more times per year than workers with better schedules.

Figure 8

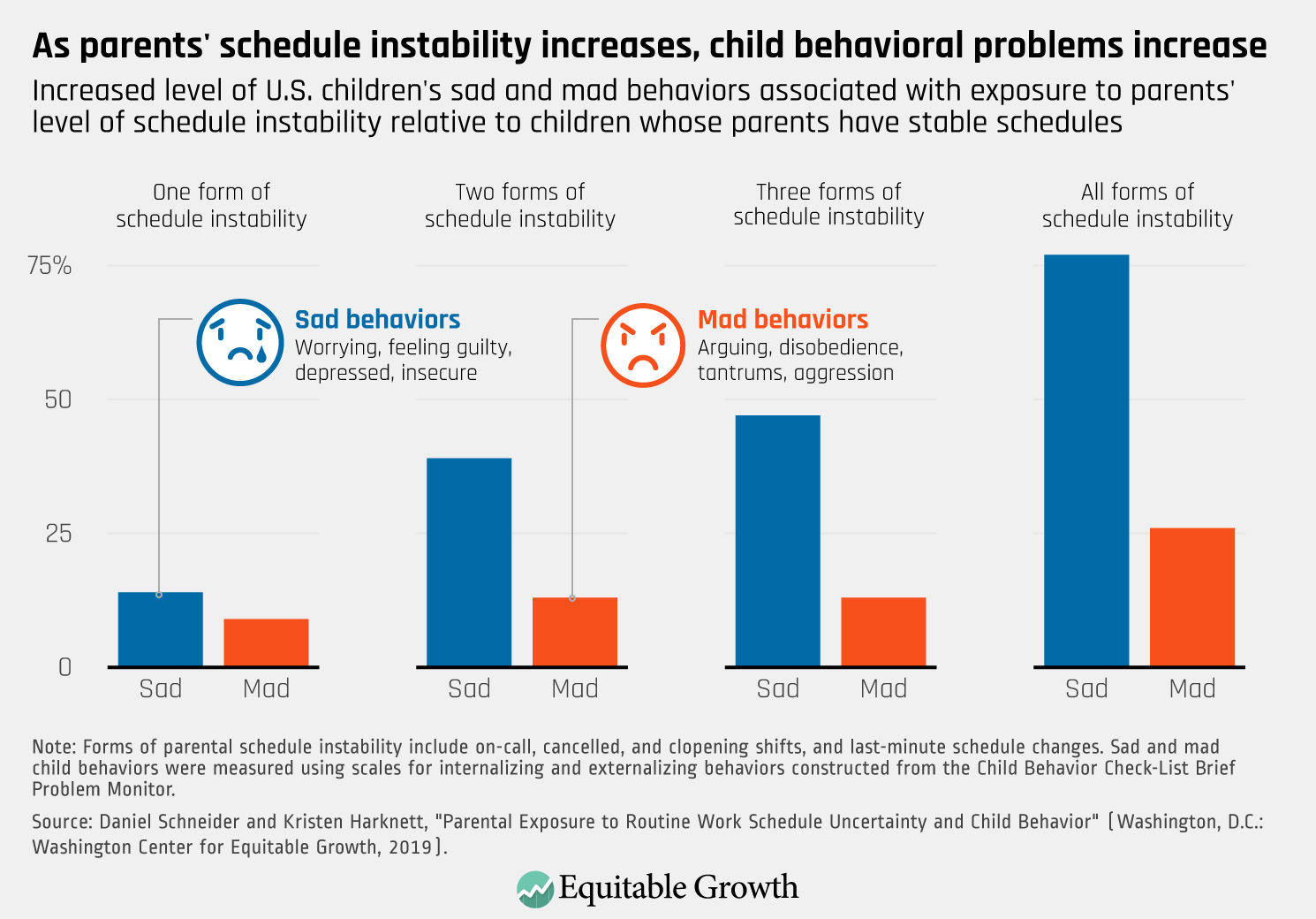

Children suffer in ways that extend beyond childcare. Parental instability is linked to child behavioral problems such as worrying and arguing. The more schedule instability the parent experiences, the more common behavioral problems are.

Figure 9

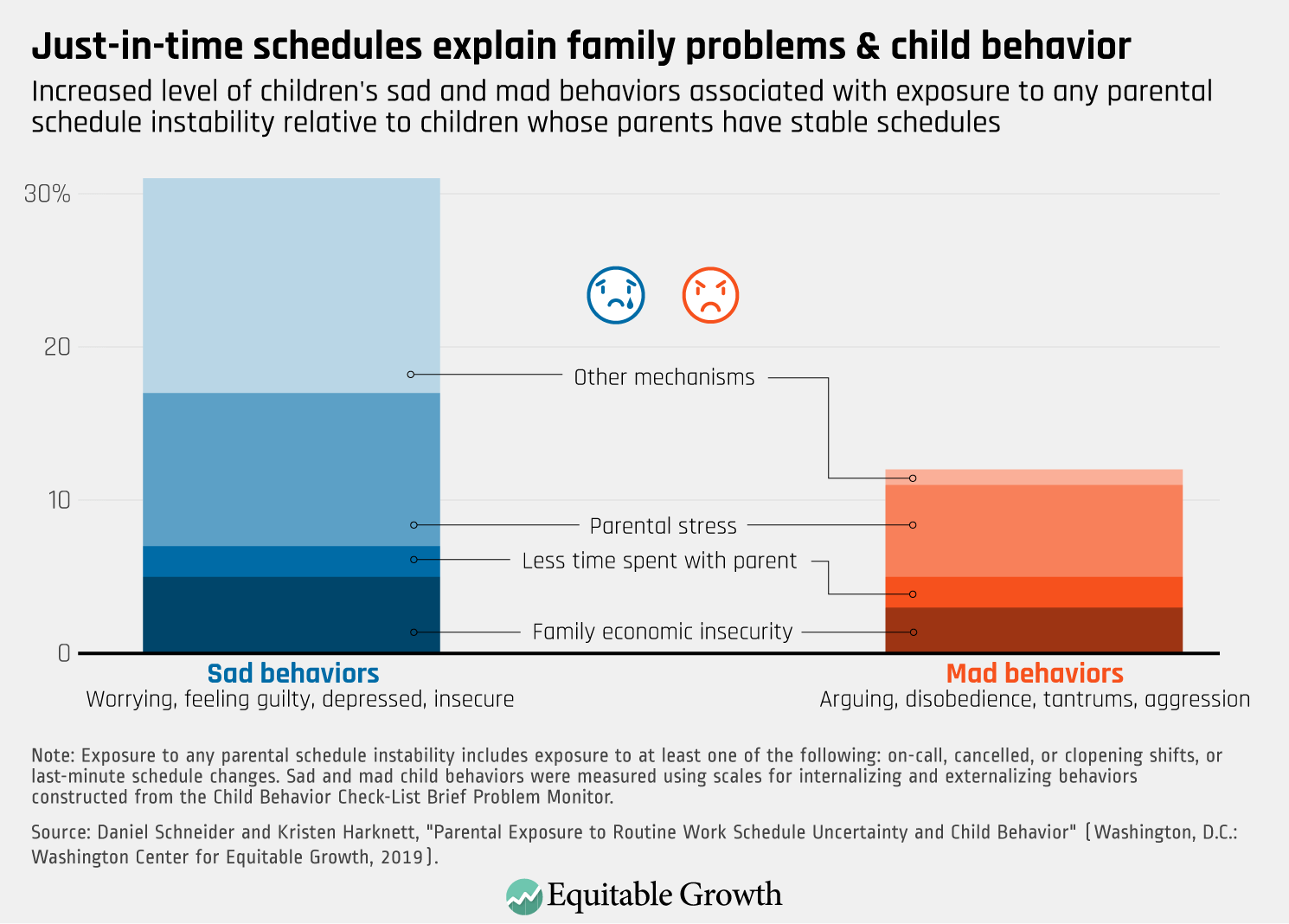

When you think about it, the connection between parents’ schedule instability and their children’s behavioral problems makes sense. Just-in-time schedules are linked to economic insecurity for the entire household, lack of quality time with parents, and high parental stress. All of these factors affect child behavior.

Note: Chart 9 decomposes association between child behavior problems and a dichotomous variable indicating any scheduling problems. This association is not depicted in Chart 8.

Figure 10

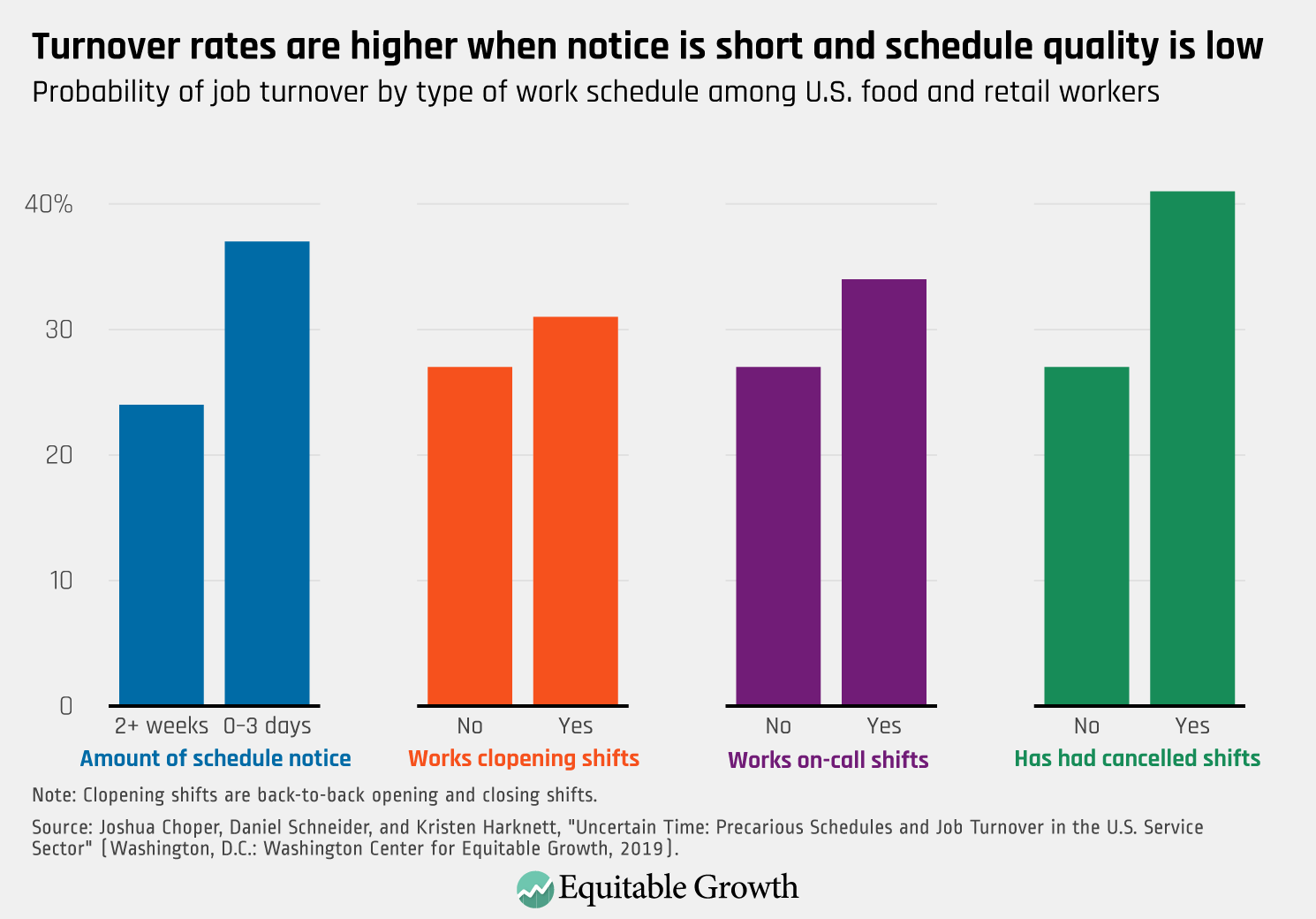

With all these problems, it’s probably not a surprise that workers with low-quality schedules are more likely to leave their jobs.

Yet it’s also important to remember that leaving their jobs doesn’t enable workers to escape the problem—other research shows that turnover is associated with lower wages going forward in a worker’s career.

Back to Figure 3

Again, the negative impacts of just-in-time scheduling are more likely to be felt by workers of color, who have worse schedules than similar white workers employed at their same companies.

That means that workers of color and their families, also disproportionately experience the consequences of just-in-time schedules: hunger and housing hardship, difficulty arranging childcare, child behavioral problems, and job turnover. Just-in-time schedules thus amplify and perpetuate inequality along lines of race and ethnicity.

School segregation—far from being a topic relegated to debates about school busing in the past or something that is only relevant in the South—is an issue very much present and alive today. Just in the past week, a decision about whether the state would take over some of the schools in Little Rock, Arkansas, raised concerns that the home of the Little Rock Nine would be resegregated, and a story came out about the racist reactions to a plan to desegregate schools in Howard County, Maryland.

Adding to the chorus of voices calling for renewed attention to the issue of school segregation is a new report, “U.S. school segregation in the 21st century: Causes, consequences, and solutions,” by former Equitable Growth Research Assistant Will McGrew. He draws upon the latest social science research into the persistence and resurgence of school segregation, examining trends in racial and socioeconomic school segregation since 1954 and the key legal and economic drivers of these trends in school segregation through to the present day. McGrew then breaks down the empirical effects of school segregation on economic inequality, mobility, and growth, concluding with a set of policy recommendations.

Throughout, he uses the research to make the case that school segregation is not an inevitable outcome of individual preferences or choices, but rather is highly responsive to legal and policy decisions. The consequences of school segregation on economic mobility are of particular concern because they lock in and perpetuate inequalities in economic outcomes between white Americans and Americans of color, particularly black and Latinx Americans.

Furthermore, by limiting children’s ability to reach their full potential, school segregation obstructs the future dynamism of the U.S. economy. As the U.S Supreme Court decision in Brown v. Board of Education—the 1954 ruling that school segregation is unconstitutional—clearly stated, separate is inherently unequal. And by trapping low-income and black and Latinx students in poorly resourced schools, segregation obstructs their human capital development and limits their exposure to examples and options for their future, thereby hurting their individual economic outcomes, as well as future U.S. economic dynamism and growth.

In his report, McGrew highlights the research of economists Stephen B. Billings of the University of Colorado, David J. Deming at the Harvard Kennedy School of Public Policy, and Jonah Rockoff at Columbia University to present the consequences of renewed school segregation. They found that when busing, and therefore desegregation, ended in the Charlotte-Mecklenburg, North Carolina, school district in the early 2000s, test scores and high school graduation rates fell for both white and black students in the newly segregated, high-poverty schools. Conversely, McGrew cites research by University of California, Berkeley economist Rucker Johnson, who found that among black students, the average effects of 5 years of exposure in desegregated schools led to about a 15 percent increase in wages and a 11 percentage point decline in the annual incidence of poverty in adulthood.

Other research by Harvard University doctoral student and Equitable Growth grantee Alex Bell, Harvard economist and former Equitable Growth Steering Committee Member Raj Chetty, and their co-authors examines who becomes an inventor. They found that exposure to innovation during childhood is a key determinant of who grows up to become an inventor. McGrew, in his report, weaves these findings together with research by Michigan State University economist and Equitable Growth Research Advisory Board member Lisa Cook, who details the obstacles that women and black and Latinx people face in becoming inventors, including the discrimination they encounter. The consequences of these obstacles are too many individuals being held back from reaching their full potential because of segregation, and the U.S. economy missing “lost Einsteins” and “lost Katherine Johnsons,” whose innovations could boost output and dynamism in the economy as a whole.

School segregation is not an inevitable outcome of individual choices or preferences. In fact, the “preferences” that lead high-income, white families to choose to buy homes in “good” school districts are, in fact, themselves shaped by policy decisions that continue to tie primary and secondary school financing to local property taxes. Policymakers who use the excuse of “personal preferences” ignore the evidence that desegregation efforts did work and had positive impacts on students’ outcomes both as students and as workers. Allowing what little progress was made during the brief period of court-ordered school desegregation to erode and reverse risks not only the individual opportunities of millions of kids to reach their full potential but also the strength of the broader U.S. economy.

This is a post we publish each Friday with links to articles that touch on economic inequality and growth. The first section is a round-up of what Equitable Growth published this week and the second is relevant and interesting articles we’re highlighting from elsewhere. We won’t be the first to share these articles, but we hope by taking a look back at the whole week, we can put them in context.

Equitable Growth round-up

Amid the ongoing and growing debate about ways to reduce inequality, a new working paper shows that a wealth tax, rather than capital income taxes, would better boost efficiency, productivity, and investments in the economy. Summarizing the working paper, Somin Park explains the authors’ findings that switching to a wealth tax rewards productive investments and broadens the tax base, improving the allocation of capital and increasing output, compared to a system of capital income taxation. In effect, a wealth tax would increase economic growth while reducing consumption inequality.

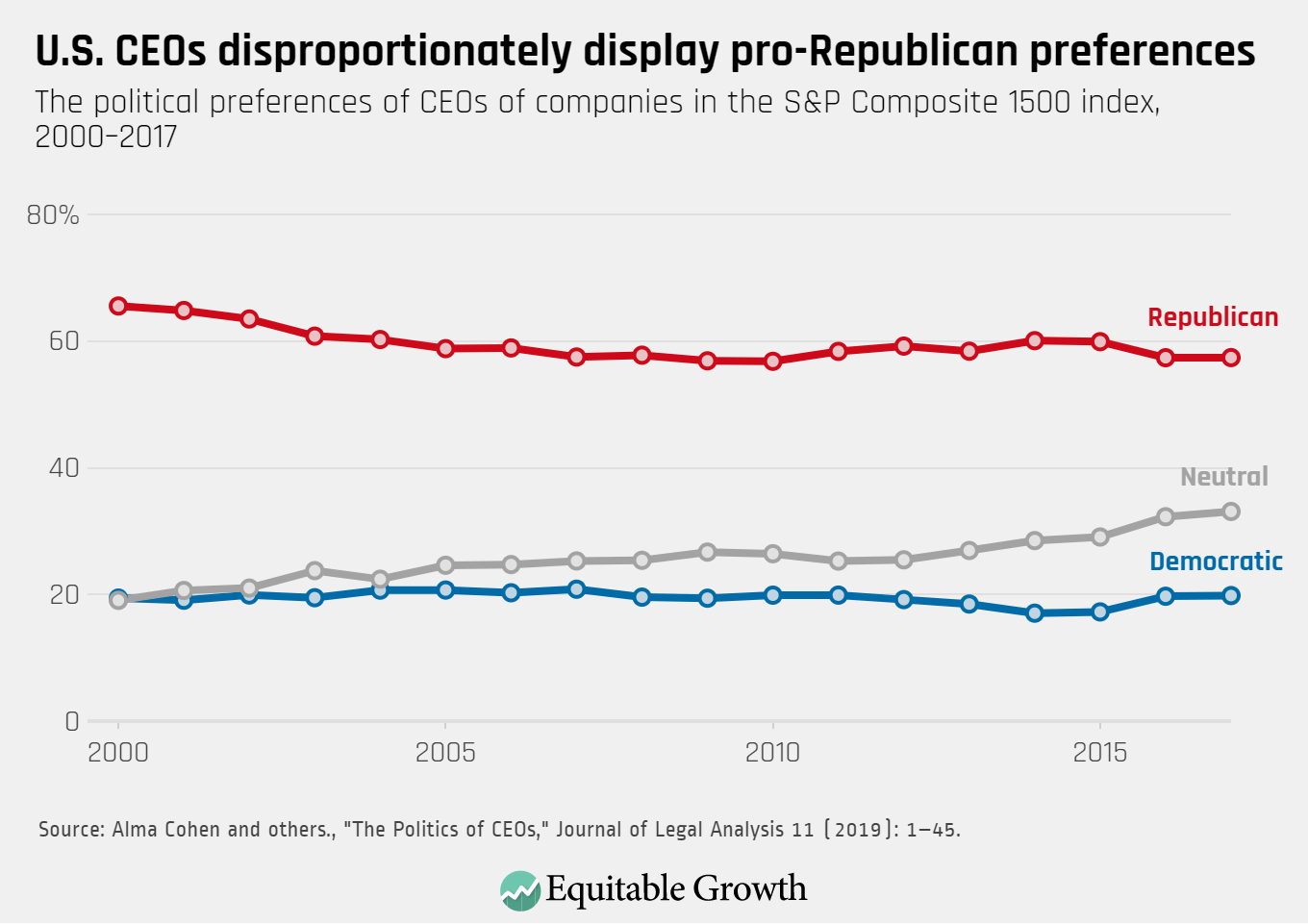

As inequality concentrates more and more economic power at the very top of the income and wealth ladders, the political preferences of the economic elite are ever more relevant. A new working paper studying the partisan leanings of top CEOs shows that a majority of these executives vote for and support Republicans, Somin Park writes in a post covering the new research. The authors of the paper studied Federal Election Commission records for more than 3,800 individuals who served as chief executive officers of companies in the S&P Composite 1500 index between 2000 and 2017, and found that 57 percent were Republican, while only 19 percent were Democrats and the remainder were neutral. As Park notes, these findings are significant because the preferences of CEOs are a window into corporate political spending, which, since the Supreme Court ruling in Citizens United v. Federal Election Commission, is unlimited and is not necessarily disclosed to investors. CEOs also express their views and provide advice on policy to lawmakers, occupying an influential position in the policymaking process.

The U.S. Bureau of Labor Statistics this week released the August data from the Job Openings and Labor Turnover Survey, or JOLTS. Raksha Kopparam and Austin Clemens produced four graphs using the data, which demonstrate that job openings declined slightly in August, as did the quits rate and the rate of hires per opening.

And finally, check out Brad DeLong’s latest worthy reads for his takes on must-see content from Equitable Growth and around the web.

Links from around the web

In 2018, for the first time in the history of the United States, the richest of the rich Americans paid a lower effective tax rate than the working class, writes Christopher Ingraham in a Washington Postarticle covering a new study by Emmanuel Saez and Gabriel Zucman of the University of California, Berkeley. More specifically, the study finds that the richest 400 families in the United States paid an average effective tax rate of 23 percent, while the bottom 50 percent of American households paid an average rate of 24.2 percent. Saez and Zucman attribute the shocking results of their study to decades of top income-tax rate cuts, slashed capital gains and estate tax rates, and an inadequate IRS enforcement budget, as well as the Tax Cuts and Jobs Act of 2017, which lowered the top income tax bracket and slashed the corporate tax rate.

In light of this, maybe we should take Annie Lowrey of The Atlantic’s suggestion—to “cancel billionaires”—more seriously. It isn’t just that the increase in inequality has left too many with too little, she writes, while noting that this is certainly a troubling trend. But inequality is also changing the very nature of our society, our economy, and our country. Lowrey describes exactly how inequality constricts mobility, damages human capital, stifles innovation, drags down growth, and endangers our political system. She concludes that a wealth tax could be a way to both pay for programs for the poor and “[reduce] the incentive for the rich to soak up all that money in the first place … pushing the steps of the income ladder closer together to make them easier to climb.”

As the rich become richer and the middle class stagnates, families face many more hurdles than they used to in their quest to achieve the American Dream. With rising costs of housing, healthcare and childcare, and education, and increasingly demanding jobs that pay less for the same or more work, “middle-class families are working longer, managing new kinds of stress, and shouldering greater financial risks than previous generations did,” write Tara Siegel Bernard and Karl Russell in The New York Times. They go on to examine in detail four families from different corners of the United States, as well as their monthly budgets, to illustrate the challenges these households—and millions more like them across the country—face as they work to enter or stay in the middle class.

And considering the increased cost of childcare in recent years, should we start paying stay-at-home parents for their hard work? The idea has bipartisan support, writes Claire Cain Miller in The New York TimesUpshot blog, with social conservatives endorsing its support of traditional families and progressives rallying behind the recognition of the economic value of unpaid domestic labor. While both sides certainly also take issue with the idea for different reasons, and there are various takes on how to go about doing it, people can agree on one thing: Children need care, and families usually take some kind of financial hit to provide it, whether it’s leaving a job to provide it yourself or paying someone else to do so.

This is very, very, very much worth watching: “Research on Tap: Unbound,” in which “Equitable Growth celebrated the release of Heather Boushey’s book, Unbound: How Inequality Constricts Our Economy and What We Can Do About It. She was joined by Sandra Black, Atif Mian, and Angela Hanks for a conversation moderated by Binyamin Appelbaum.”

And this upcoming event will be well worth attending, “Vision 2020: Evidence for a Stronger Economy”: “Vision 2020 will bring together leading voices from the policymaking, academic, and advocacy communities to highlight the most pressing economic issues facing Americans today. This daylong conference will explore recent transformative shifts in economic thinking that demonstrate how inequality obstructs, subverts, and distorts broadly shared economic growth and what we can do to fix it.”

I would have thought wealth taxation would be the default conventional neoliberal public finance position. You want to broaden the base and lower the rates. And what base is broader than wealth? Administrative, behavioral-response, and information-revelation considerations can move you away from a wealth tax to narrower bases. But it has always seemed to me that a wealth tax is where you start. That does not seem to be how the public finance intellectual community is reacting. We, however, are providing pushback. Read Fatih Guvenen, Gueorgui Kambourov, Burhan Kuruscu, Sergio Ocampo, and Daphne Chen, “Use It or Lose It: Efficiency Gains from Wealth Taxation,” in which they write: “How does wealth taxation differ from capital income taxation? When the return on investment is equal across individuals, a well-known result is that the two tax systems are equivalent. Motivated by recent empirical evidence documenting persistent heterogeneity in rates of return across individuals, we revisit this question. With such heterogeneity, the two tax systems have opposite implications for both efficiency and inequality. Under capital income taxation, entrepreneurs who are more productive, and therefore generate more income, pay higher taxes. Under wealth taxation, entrepreneurs who have similar wealth levels pay similar taxes regardless of their productivity, which expands the tax base, shifts the tax burden toward unproductive entrepreneurs, and raises the savings rate of productive ones. This reallocation increases aggregate productivity and output.”

“My Job as the Economist Here Is to Do the Numbers,” in which I write: “People believe that they have rights to a good life. People believe they have rights to stable communities that support them and that don’t disrupt and overturn their lives … Look at my neighbors … horrified at the idea that they might want to tear down a single-family house and build an apartment building for students. People think that they have the right to the income that corresponds to the profession or the occupation that they have worked hard to become part of … People believe that … their job shouldn’t suddenly vanish because some financier 3,000 miles away decided it doesn’t make a cost-benefit test. Yet the only rights the market respects are property rights, and the only property rights that are worth anything are those that help you make things for which rich people have a serious and unsatiated jones. The fact that the U.S. economy over the past 40 years has not been delivering substantially rising living standards for everybody means that the market’s failure to deliver these other forms of nonproperty rights becomes the source of—call it economic anxiety—a big potential problem.”

Worthy reads not from Equitable Growth: