This post reflects our organization’s overall guiding policy principles for confronting the coronavirus recession and its relationship to U.S. economic inequality as detailed on April 16. These principles still hold as there remains much to be done across communities and workplaces throughout the United States now and in the weeks and months ahead. Our coronavirus recession page provides updated analysis and policy resources from Equitable Growth.

Overview

The coronavirus pandemic presents a new and unprecedented challenge to the United States. First and foremost, it is a public health crisis that makes it impossible for our society and our economy to function as usual due to the necessary social distancing required for the health of us all. Because the federal government neither acted early enough to contain the deadly coronavirus nor swiftly enough to forestall mass layoffs, our nation is now facing a health crisis and economic recession simultaneously.

What’s more, the underlying problems of U.S. economic inequality today will only prolong and deepen this coronavirus recession. Historically high economic inequality has concentrated economic resources among those at the very top of the U.S. income and wealth ladders while leading to fewer and fewer protections for the economic security of workers and their families. This has left the United States particularly vulnerable to shocks such as health, climate, and economic crises.

Only a decade has passed since the end of the previous global financial crisis, from which U.S. working- and middle-class families had barely recovered despite a record run of economic growth. Indeed, younger generations and many families, especially families of color, never recovered. To avoid that same outcome on the other side of the coronavirus recession, policymakers’ response today will be most effective if directed at the roots of these underlying problems of economic inequality.

Decades of failed economic policies, based on ideology instead of evidence, and a blind adherence to the idea that markets can solve every problem, have made our economy and our society more vulnerable. Our nation now faces a grave economic challenge and concentrated efforts to weaken public institutions and leave decisions up to the market over the past 40 years mean our policymakers and society are ill-equipped to handle it. Disparities by income, race, ethnicity, and gender are inevitably exacerbated by this shift of social and economic risk from collective institutions to individuals—rendering any response to a deep recession and eventual recovery all the more difficult.

An economy only functions when there are people who are able to act as producers and consumers. The first principle of a strong and stable U.S. economy is to ensure the ability of people to secure a good, steady job that provides enough income for people to support their family and buy goods and services. The new coronavirus has uncovered how even as one of the richest economies in the world, the United States remains incredibly fragile.

This issue brief diagnoses why high and rising economic inequality left our economy and our society particularly unprepared to cope with the coronavirus pandemic and ensuing recession. Six key points of vulnerability are then detailed—ranging across inequalities in health, wages, purchasing power, worker power, and government investments—followed by a roadmap of broad policy principles to help guide policymakers as they consider long-term structural changes for the U.S. economy. These principles are detailed toward the end of this issue brief. But briefly, they are:

- Recognize that markets cannot perform the work of government

- Address fragilities in our markets themselves

- Keep income flowing to all the unemployed workers and small businesses now and in future crises

- Ensure those who are still employed can stay employed

- Produce headline economic statistics that represent the well-being of all Americans

The coronavirus recession is exacting a large human toll across our nation. This toll is all the more insidious due to the economic inequalities that cause the health and economic damages to fall unequally and inequitably among us. To have any chance of emerging on a stronger footing as a nation with less economic inequality and more sustainable economic growth, policymakers need to enact a robust set of protections that will ensure high-end inequality is contained, build counterweights to concentrated power, and provide economic security for all now and going forward.

Download File

The coronavirus recession and economic inequality: A roadmap to recovery and long-term structural change

Diagnosing U.S. economic inequality and the coronavirus recession

For decades, policymakers and economists alike have put their faith in the idea that markets are the best and only way for our economy to deliver what’s needed for sustained economic growth and well-being. This promise has not delivered. Over the past five decades, the U.S. economy has been characterized by high economic inequality and a lack of strong, stable, and broadly shared economic gains and well-being. Economic power at the top has translated into social and political power coalesced among an elite few. Those who start with economic advantages are able to design a system of economic inequality that preserves and amplifies their position at the top, to the detriment of the rest of us and the public good.

Allowing markets to determine outcomes, while pretending that the rules that govern markets are always neutral and fair, shifts economic risk toward people and families and away from institutions that could better bear them. At no time has this been more apparent than right now. Amid the coronavirus pandemic, many of the workers most likely to be in jobs with a high degree of face-to-face contact with the public—and thus at greater risk of exposure—are those least likely to have access to paid sick time or employer-provided health insurance. Those in jobs that allow them to telecommute are also the workers most likely to have the best insurance coverage and most generous workplace benefits.

At the same time, we’ve reduced the risks for those at the top, including big corporations. Whereas power once rested in freely chosen democratic institutions that collectively shouldered risk, that risk is now borne by individuals while the governance of commercial activity is determined by those with the money and power to subvert those same institutions. The failed ideology that claims the benefits of unconstrained private activity accrue to everyone with greater efficiency and fairness than collective governance is exposed today as not just failing but also false. As we see in this moment, a healthy economy and society require a competent, well-resourced federal government.

The coronavirus pandemic reveals how this shift in risks plays out across communities. Death rates are higher in communities of color, in no small part due to structural racism, segregation, and industrial policy, all of which have exposed them to greater levels of air pollution alongside underlying health inequalities due to overrepresentation in vulnerable jobs and a failure to invest in ensuring all communities have access to high-quality and affordable healthcare. At the same time, it’s now abundantly clear that the jobs that make it possible for those with families to go to work every day—childcare centers, schools, nursing homes—also are heavily staffed by women, especially women of color and, in particular, immigrants to our country, and are among the least paid. These jobs are a key building block of a functional economy.

Before the coronavirus crisis hit, the U.S. economy was experiencing the longest economic expansion in our history. But the headline numbers belied serious structural weaknesses, as the benefits of growth accumulated disproportionately to the already wealthy. New data show that in 2016—the latest year available—those in the top 10 percent of incomes accounted for 38 percent of the nation’s total personal income, while those in the lowest 10 percent accrued only 2 percent. Children in the United States used to have a 90 percent chance of earning more than their parents, but those chances had dropped to just 50 percent by 1980.

When the new coronavirus hit our shores, policymakers were ill-prepared. The fragilities created by economic inequality undermined our capacity to remain economically and politically stable. On the one hand, too many workers and their families were obstructed from accessing basic protections and the kind of jobs and income security that could help our nation weather this storm. On the other hand, those at the top who subverted our markets and our democracy to protect themselves, not our nation as a whole, are better prepared to ride out the coronavirus recession and further entrench the economic inequalities that left our nation unprepared for these twin public health and economic crises in the first place. These economic inequalities are identifiable and actionable.

The six key vulnerabilities facing our nation due to high economic inequality

There are six key factors that made the United States and the U.S. economy particularly susceptible to the coronavirus pandemic and COVID-19, the disease delivered by the new coronavirus. Each of them, when examined together, are not only a problem today but also threaten to become even more enduring as our economy goes through a wrenching recession and continues to confront the very real consequences of climate change. If these are not corrected, the United States is likely to experience a slow and inequitable economic recovery. These six factors are:

- Too many people lack the basic protections that would have slowed the spread of the virus.

- Workers lack the power to share in the gains of the economic expansion that would have given them protections and security.

- Decades of stagnant wages and meager workplace benefits leave many families without enough savings to weather the coronavirus recession.

- Policymakers starve public goods of investments that would have enabled better protections from the coronavirus pandemic and ensuing recession.

- States and localities don’t have the resources to deal with a pandemic or a recession.

- Business concentration across markets increases consumer and small business vulnerabilities just when those threats are most dire.

Let’s now look at each of them in turn.

Too many people lack the basic protections that would have slowed the spread of the virus

The gaps in our social insurance systems and labor market regulations to protect workers and families, including the lack of paid leave, unstable schedules, and limited access to childcare, both exacerbated the spread of the virus and left millions of workers highly at risk of not only contracting COVID-19 themselves but also spreading it further to their own families and wider communities. Compounding the problem is the lack of health insurance or fear of high medical bills, both of which kept—and are still keeping—those who feel sick from seeing a doctor, placing a serious burden on these individuals, as well as raising rates of transmission.

Research is already showing the significant economic and psychological toll this pandemic is taking on these workers. These stresses are heightened for people at the intersection of these eroded protections and institutional discrimination. People of color and immigrants, for example, are often foreclosed from accessing the limited protections that do exist, or are forced by their already precarious economic straits to succumb to workplace abuses at the hands of their employers.

Workers lack the power to share in the gains of the economic expansion that would have given them protections and security

Civic institutions—especially labor unions, which once served as voices for many wage-earning workers (though never representing all workers)—have suffered a long decline. Now, only 1 out of every 15 private-sector workers belongs to a union. On top of this, labor laws and policies have failed to reflect the growing role of the fissured workplace in our modern-day economy, where firms subcontract pieces of their work so they can avoid responsibility for workers and working conditions.

These two debilitating trends in our labor market mean that corporations that are ultimately in charge of labor practices and that make the largest profits are not liable for maintaining 21st century workplace standards. The coronavirus pandemic exposed the failure of these labor market inequalities and the need for them to manage health crises and family care, as well as protect workers against layoffs and the loss of these key health and family benefits.

Decades of stagnant wages and meager workplace benefits leave many families without enough savings to weather the coronavirus recession

At the onset of the coronavirus pandemic in the United States at the beginning of the year, millions of people across the country were one paycheck away from financial catastrophe, even after a decade of economic expansion and historically low unemployment. Case in point: Four in 10 adults in the United States said that if they had a $400 emergency expense, they would have to borrow, sell something, or would not be able to pay it.

As the coronavirus recession continues, more and more workers and their families who are most likely to spend money are robbed of buying power, which will undermine one of the key drivers of economic growth—the stable incomes that drive consumer spending. Today, less-well-off workers in sectors of the economy most immediately exposed to the consequences of necessary self-distancing, such as food services, hotels and accommodations, and general services, are now joining Unemployment Insurance telephone queues alongside millions of other workers who have been let go or furloughed by a broader array of firms, which will further crimp consumer spending.

Policymakers starve public goods of investments that would have enabled better protections from the coronavirus pandemic and ensuing recession

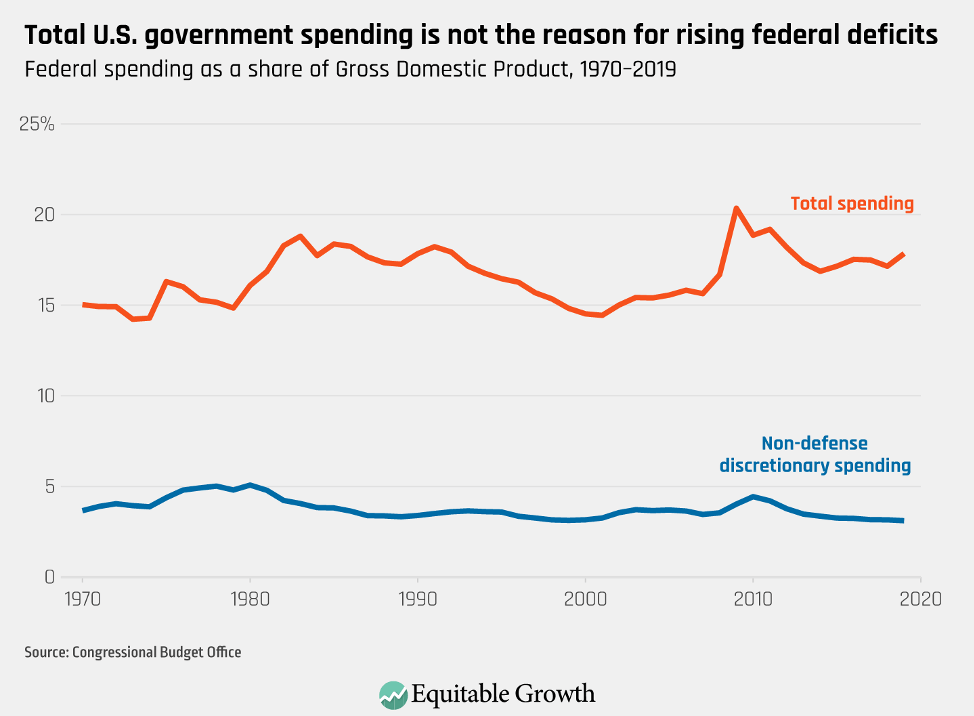

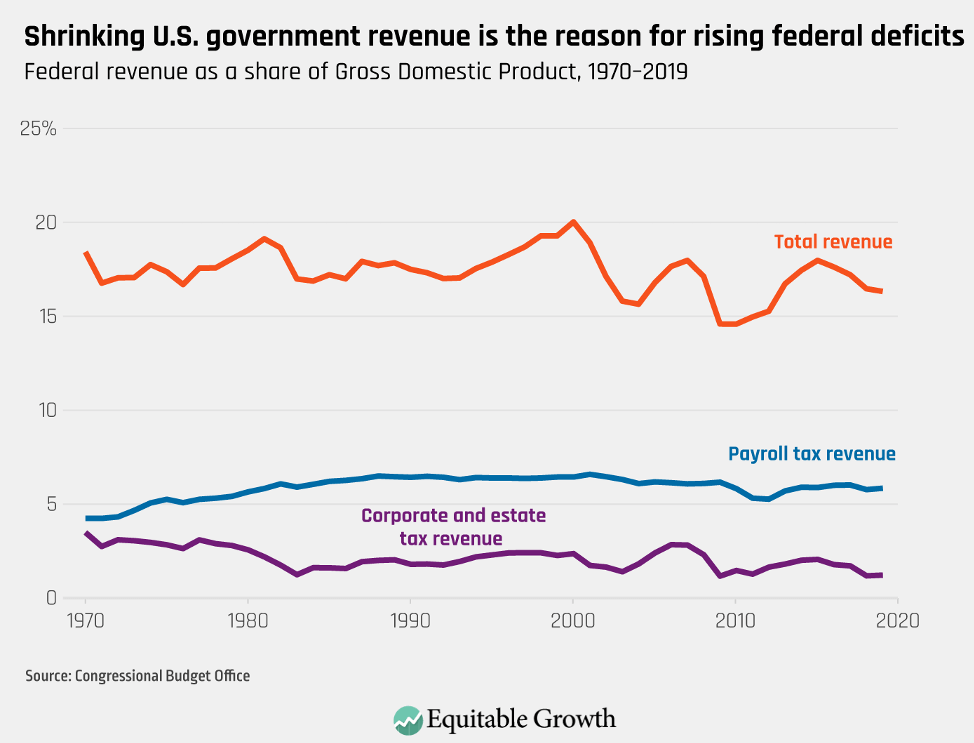

Decades of tax cuts, culminating in the sharply regressive Tax Cuts and Jobs Act of 2017, have fueled a long-term decline in federal revenue that has starved resources that can be used to fund critical public investments and basic governmental functions, including in public health. High concentrations of income and wealth hamstring our political system because the wealthy dictate the legislative agenda and shape news headlines.

Yet these same wealthy elites don’t prioritize investments in public health infrastructure or other public goods, such as an effective Internal Revenue Service or the provision of paid leave or wage replacements during emergencies—even though the lack of these policies have accelerated the spread of the new coronavirus, endangering us all. Case in point: even as people at the top end of the wealth distribution can retreat to their private enclaves with concierge medicine, too many others cannot access high quality care amid this crisis. The government is the only entity with the power and scope to dismantle the control that the economic elite have over our political system.

States and localities don’t have the resources to deal with a pandemic or a recession

During and after the Great Recession of 2007–2009, hard-hit state and local governments saw large drops in capacity as Medicaid rolls rose and tax revenues fell. The decline in resources and staffing continued in the 2010s even as the economy recovered. Yet the critical role that states and localities play in addressing the coronavirus pandemic are clearly emerging in community after community. From ensuring hospitals are prepared to putting in place and enforcing stay-at-home orders, the importance of effective local policymakers is abundantly clear.

Now, state and local governments are likely to experience sharper drops in their capacity to provide the services needed to cope with the coronavirus recession, which will surely induce further cuts to health and education and exacerbate the ongoing weaknesses. If this happens, it will not only starve communities of the investments they need to thrive but also leave the nation even less prepared for the next crisis. Austerity in state governments likewise disproportionately harms people of color, as public-sector jobs form the basis of a strong middle class for black and Latino workers.

Business concentration across markets increases consumer and small business vulnerabilities just when those threats are most dire

Wealthy and powerful corporations use their status to maintain dominance in the marketplace. Large businesses and monopolies muscle competitors out of business, suppress wages, and hobble innovation. These companies are also precisely the ones that will thrive after the coronavirus pandemic passes. Strong cash reserves combined with political influence allow entrenched businesses to swoop in when asset prices are low and reshape rules of entire markets in the aftermath. The collapse of small businesses will disproportionately hurt people of color for whom business ownership is an especially important route to wealth creation and to closing the racial wealth gap.

We can see how these fragilities created by inequality are playing out right now by looking at the healthcare industry having to cope with the coronavirus pandemic. Hospital consolidation resulted in higher costs, decreased quality of care, and fewer worker protections, leaving staff less able to deal most effectively with the surge of incoming COVID-19 patients alongside the collapse in other hospital procedures that provide key sources of revenue. Similarly, private-equity backed clinics and doctors—alongside profit and nonprofit hospitals more generally—fought against surprise billing legislation, which would limit patients from being hit by huge out-of-network fees for care, a problem whose impact will increase as more people need care.

Huge pharmaceutical companies have likewise used their market power to suppress low-cost competition from generic alternatives by preventing the development of generic medicines, paying generics companies to delay launching their products, and excluding competition by other anticompetitive conduct. And they have offshored the production of these drugs and their key ingredients, leaving our healthcare system very vulnerable to a pandemic. Developing a coronavirus vaccine or treatment is paramount, but it is also critical that we ensure such solutions are affordable and readily accessible to prevent unequal access to life-saving medicine.

The failure to prevent coronavirus infections and deaths and the ensuing recession

President Donald Trump’s focus is and always has been on the stock market rather than conceiving of and effectively implementing a comprehensive and fully thought out federal plan to address the coronavirus pandemic and its economic effects. Case in point: Though the administration knew about the threat of the virus in early January and took an early effort to limit the transmission into the United States by halting travel from China, where the virus first emerged, it did not use that time to prepare sufficient stockpiles of medical and protective supplies.

Nor did the Trump administration put in place an economic plan to limit the transmission, such as immediately requiring all firms to provide paid sick time or ensure access to free test kits, let alone free healthcare. These failures are now distorting our economy and seriously undermining our economic stability—failures that are further fueled by the key vulnerabilities detailed above that are intertwined and ensconced across the breadth of our society and economy.

The incidences of the coronavirus in the United States have surpassed every other nation, and the underlying fragilities may make our economic crisis equally uniquely bad. Some economists and policymakers argue that these fragilities were the inevitable result of globalization, technological innovation, or economies of scale, and that the result in the end will be better for both workers and consumers. But the role of policy choices in arranging our market structure—from the choice to bailout Wall Street rather than save homeowners a decade ago, to a long history of declining antitrust enforcement, to policy choices and court decisions that make it harder to join a union—are unmistakable and remain enduring.

Solutions to come out of the coronavirus recession more quickly and sustainably

Congress, the Trump administration, and states and localities have each taken steps to address the twin health and economic crises facing all of us today. As policymakers consider the next federal aid package, they also need to address long-term structural challenges in our economy. They should focus on the following priorities:

- Recognize that markets cannot perform the work of government

- Address fragilities in our markets themselves

- Keep income flowing to all the unemployed workers and small businesses now and in future crises

- Ensure those who are still employed can stay employed

- Produce headline economic statistics that represent the well-being of all Americans

A detailed examination of each of these priorities closes out this issue brief.

Recognize that markets cannot perform the work of government

The federal government must step up and provide the effective leadership required to fully contain the new coronavirus. This includes ensuring that all across the United States, people have access to testing and protective gear, that our national health infrastructure is prepared for patient loads—without putting the lives of healthcare workers unnecessarily at risk—and that proper and effective steps are taken to protect all workers and contain the spread of this new, deadly virus. The only entity with the capacity to manage this health and economic crisis is the federal government.

Policymakers must reject the false premise that tax cuts and deregulation form the basis of effective macroeconomic stimulus. Research finds that even in the best of times, tax cuts favor the wealthy and are not stimulative because rich households just preserve their wealth and income rather than deploying it in an economy that is 70-percent powered by consumer spending. Similarly, researchers have found payroll tax cuts to be among the least effective stimulus programs during recessions.

This is especially true in a pandemic, when discretionary spending is limited by social isolation. Instead of cutting taxes and cutting regulation, the federal government must save the economy through the expansive fiscal stimulus that this extraordinary crisis warrants.

Policymakers also need to rebalance their priorities going forward to provide a stronger foundation for our economy and our society. Across all levels of government, revenue is too low. Policymakers need to find ways to tax the enormous wealth concentrated in one part of our economy, so that we can deploy it for the common good. Over the decade since the end of the financial crisis, investment has been low relative to the resources firms have on hand, even as our nation is facing grave challenges—from the lack of a health system sufficiently resourced to address a pandemic, even though Americans spend twice as much on healthcare per capita than our economic competitors, to the need to ensure all children have access to world-class educational opportunities, and from the lack of basic family economic stability for most Americans in the wealthiest nation in the world, to the urgent and pressing need to address climate change.

Much of this work is done by state and local governments. Without federal assistance, many will have to pivot to austerity in the months and years ahead due to strict limits on deficit spending, thereby undermining any federal efforts to provide macroeconomic stimulus in the short run and address the underlying fragilities in the medium to long run. Supporting states and localities through the crisis and beyond is an urgent national economic priority.

Nor can markets fix the structural racism and gender inequities that permeate the foundations of our economic system. Coronavirus policy interventions must affirmatively seek to break the feedback loop of disadvantage and exclusion. This means directing healthcare investment for testing and treatment in communities of color, pursuing policies that expressly and progressively support low-wage workers and care workers, and requiring proactive engagement with minority-owned small businesses, rather than relying on them to navigate complex bureaucracies and overcome entrenched discrimination. Otherwise, these pervasive inequities will become further entrenched.

Address fragilities in our markets themselves

For too long, the U.S. economy has been on a path toward greater corporate concentration across industries. Policymakers cannot allow the coronavirus recession to amplify this trend. This is why they must ensure the stability of U.S. small and medium-sized businesses and provide them the support they need so that they are still standing once we’ve solved the health crisis.

Policymakers need to increase the size of assistance, especially as each day of mandatory public health lockdown increases the likelihood of small business failures. They need to ease hurdles to access to financing by reducing barriers to small business aid. They must level the playing field by ensuring equal access for both small lenders and small businesses owned by people of color and women. And they must take aggressive steps to reduce the likelihood of unlawful discrimination by collecting better lending data, affirming a commitment to fair lending, and requiring that the Small Business Administration affirmatively further the issue of credit access.

All of these policy actions must also include lasting structural reform to ensure that the next time this happens, small businesses can access the financial plumbing easily and quickly so that they can cope effectively and efficiently. At the same time, we cannot allow the largest businesses to receive blank checks. We must use the oversight tools provided in the Coronavirus Aid, Relief, and Economic Security, or CARES, Act to hold the U.S. Treasury Department and Federal Reserve accountable in establishing aid programs that deliver for workers.

All rescue programs for businesses should ensure that funds are directed to productive uses that support workers and customers, and not financial speculation. This should include banning dividends and stock buybacks for the duration of assistance, including a prohibition that banks suspend capital distributions during the crisis in order to support lending to the real economy. Congress should also make maximal use of its oversight powers to ensure that the $500 billion directed to large corporations is free from fraud and does not merely enrich the well-off.

If there are future bailouts or use of the Federal Reserve’s emergency lending authority, policymakers should use both fiscal and central bank policies to improve corporate governance, empower workers to influence how businesses operate, and protect taxpayers from the risks posed by thin capitalization and profiteering by corporations.

And policymakers need to recognize that for too long, they’ve acted as though the Fed holds all the cards in a recession, as if an economic downturn can only be solved by monetary policy. Not only is monetary policy unable to tackle this crisis alone, the Fed has also already used its most powerful tool: cutting interest rates. Monetary policy needs to work together with effective fiscal policy. Still, it is essential to keep in mind that monetary policy actions that are taken have important distributional implications. Policymakers must ensure that the policies being implemented at the Fed do not simply rescue those at the top who started at a much better place and have the resources to weather the storm.

Keep income flowing to all the unemployed workers and small businesses now and in future crises

So long as the new coronavirus continues to spread without a vaccine or effective treatments available, there will be swaths of the U.S. economy that will remain shut down or intermittently turned on and off. As the health and economic crisis continues, more layoffs are likely to occur, so the more resilient that policymakers can make businesses and families, the more long-term damage can be mitigated.

Policymakers should start by extending direct payments, Unemployment Insurance, small business grants and loans, aid to states, and emergency paid leave until the coronavirus recession passes. The most effective way to do this is to use unemployment rate-based “triggers” that only turn off when the recession is ending and the recovery is underway. This allows programs aimed at maintaining incomes to ramp up and wind down automatically. Policymakers also should make it easier for employers to cut employees’ hours and have them access partial unemployment benefits in order to foster a faster economic recovery.

Macroeconomic stability also requires that all people who are unemployed and their families can access healthcare. If the Trump administration continues to leave unemployed workers, including immigrants and their families, without access to healthcare, Congress must step in with a special enrollment period for Obamacare, subsidized COBRA health insurance plans for employees who are laid off but want to keep their employer-based health plans, a Medicare buy-in, expanded Medicaid, or some combination thereof.

The challenge of supporting those out of work is magnified by the reality that the sectors of our economy that are the first economic casualties of the coronavirus pandemic and ensuing recession tend to be small businesses with little cash reserves and with employees who are mostly paid at the low end of the wage scale and provided with few benefits. As of mid-March, more than 90 percent of jobs lost were in low-wage industries, particularly in the accommodations and food services industries, heightening the likelihood that this causes real hardship for those affected.

Both these business owners and their employees are precisely the people who are likely to have little in savings. As we support those out of business or out of work, policymakers must ensure that these policies are inclusive and reach these hard-hit businesses and workers. As we look to the long term, what our economy needs is more families with economic security, gained through policies that ensure fair pay—such as encouraging more union coverage—and helping families afford the big-ticket items, such as a home, a college education, and retirement, without having to take on unmanageable debt.

Ensure those who are still employed can stay employed

Policymakers need to ensure that businesses do not become hotspots for transmitting the coronavirus. To that end, all workers must have what they need to do their job safely for themselves and the public. This means, first and foremost, ensuring that we adopt widespread testing and provide protective gear, starting with essential industries—healthcare, food production and distribution, utilities, and childcare, among others—but extending to all as necessary as more parts of the economy are opened back up.

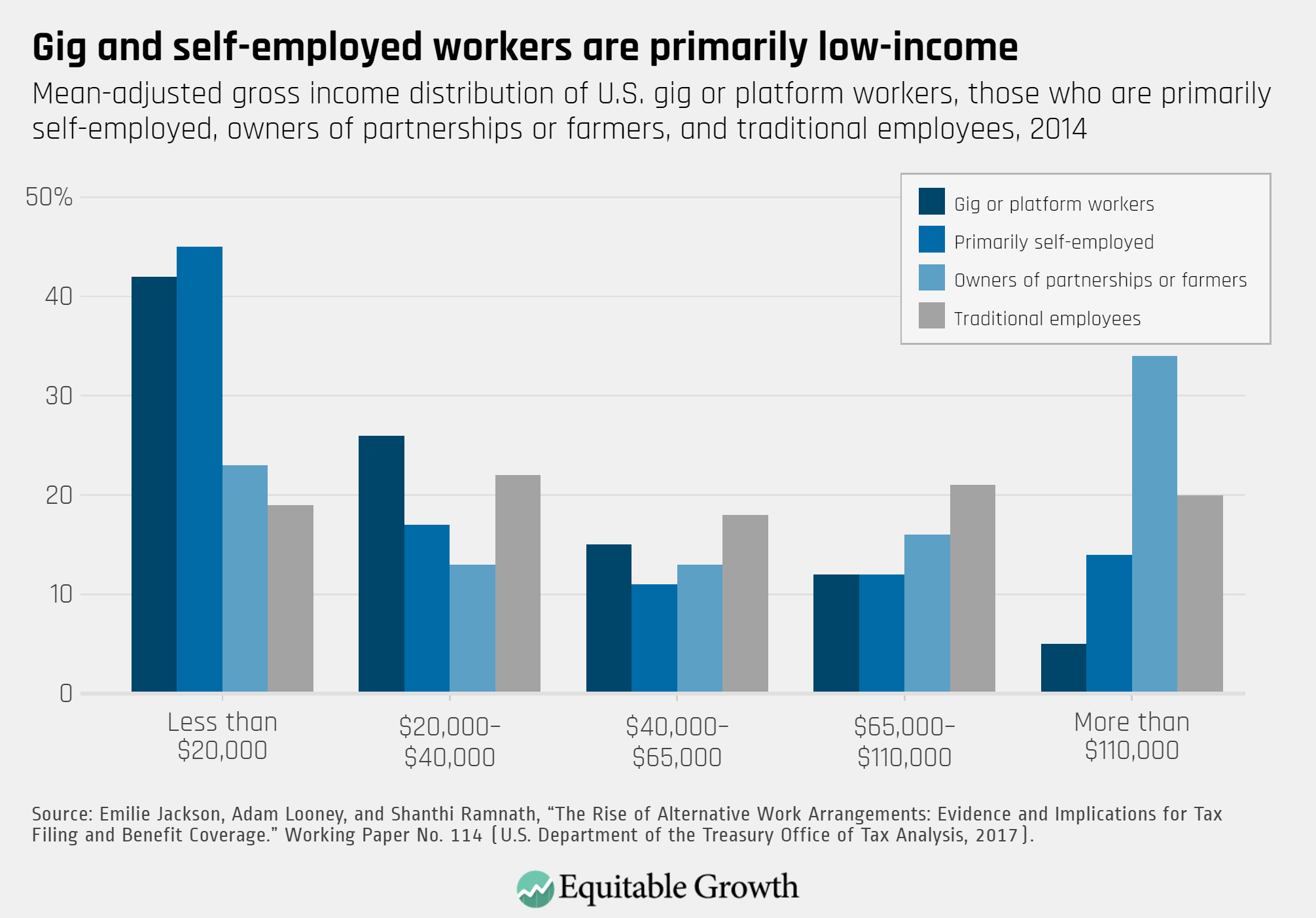

This moment of crisis has exposed deep underlying fragilities, too. To move forward, policymakers need to make our economy more resilient by establishing for all workers, including contractors and gig workers, guaranteed universal paid sick days and paid family and medical leave, universal access to health care—including free coverage for any coronavirus-related illnesses—and high-quality, affordable, safe care for children, both young children and those who may need care while schools are closed, while parents are working.

Produce headline economic statistics that represent the well-being of all Americans

Amid a pandemic and a steep and swift decent into recession, concerns about how policymakers calculate headline economic statistics may seem to be a misplaced priority. Yet the inability of policymakers to convey how this recession will affect people differently up and down the income and wealth ladders means that effective solutions to get to the economic recovery swiftly and sustainably will be equally elusive. A continuing inability to fully appreciate and identify structural weaknesses in the U.S. economy for all workers and their families during the recession will make it even more likely that existing economic inequalities become further entrenched, to the peril of a more equitable economy emerging on the other side of the recession.

Although Gross Domestic Product growth may once have been a reliable indicator of the fortune of most Americans, many have been left behind over the past several decades, making GDP a misleading metric. In an era where economic inequality has swelled to levels approaching those last seen nearly a century ago, policymakers need to know who is prospering from economic progress and who is suffering in a downturn. We can lay the groundwork now to make sure we understand who benefits from a future recovery and what other action is needed. The effectiveness of our policies to save the U.S. economy and ensure that growth is broadly shared depends on using the most precise measurements for today’s economy.

Conclusion

Unless policymakers actively address all of these structural issues detailed in this issue brief, the United States will experience continued increases in income and wealth inequality amid the coronavirus recession and coming out of it. This is exactly what happened after the Great Recession, when the U.S. economy lost 8.7 million jobs and $12 trillion in total household net worth. One group emerged as strong as ever: the wealthiest 1 percent, who regained what they had lost by 2012. That year, their inflation-adjusted average wealth (not including any funds hidden in overseas accounts) was $13.8 million—just 3.5 percent below the 2007 peak. Middle-class families, meanwhile, were still recovering in March of this year.

The United States was founded on a set of principles that a democratically elected government could act in the interest of the general welfare. That faith has proved tremendously powerful over the course of our history, when we have shown the ability to come together as a nation to address sweeping structural crises. Crises have a way of bringing us together. We must now act as one to make our nation stronger, more resilient, and more equitable today and for generations to come.

—Heather Boushey is the president and CEO of the Washington Center for Equitable Growth and the author of Unbound: How Inequality Constricts Our Economy and What We Can Do about It (2019, Harvard University Press) and Finding Time: The Economics of Work-Life Conflict (2016, Harvard University Press). Somin Park is a research assistant to the president and CEO of Equitable Growth.