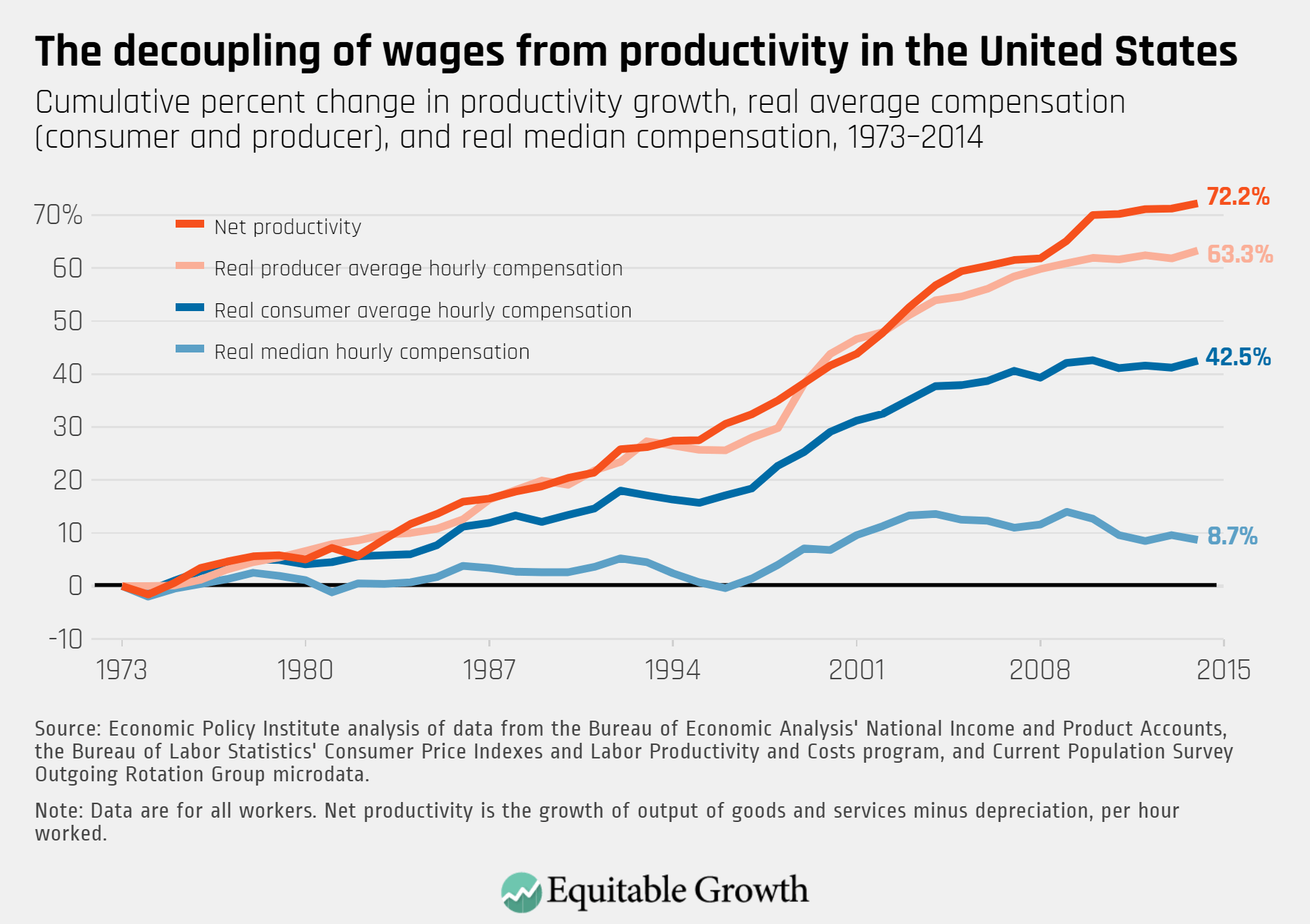

The U.S. labor market is shackled by decades of wage stagnation for the majority of workers, persistent wage disparities by race, ethnicity, and gender, and sluggish economic growth. The steady increase of income inequality since the 1970s leaves generations of U.S. workers and their families unable to cope with the daily costs of living, let alone save for emergencies or invest in their futures—conditions that have left many families ill-prepared for the “stress test” of the coronavirus recession.

These labor market ills particularly affect women and workers of color due to decades of gender inequality and structural racism erecting barriers to opportunities. There is increasing evidence that broad structural inequality leads to a misallocation of talent and the undervaluation of different types of work, which contributes to anemic economic growth and slower productivity gains.

Creating an economy that works for everyone and serves those who are historically marginalized requires addressing underlying economic structures that form the foundation for U.S. labor market policies. These unequal structures entrench barriers to opportunity based on race, ethnicity, and gender, and exacerbate the power imbalances that allow employers to undercut wages and allow gains of growth to accrue to the few while stifling a robust, dynamic U.S. economy.

Existing efforts to address wage stagnation and persistent disparities tend to be limited to two narrow approaches: minimum wages and educational investments. Both are critically important, but neither are sufficient to overcome the unequal structures in the U.S. labor market. Minimum wages reach only the bottom of the wage distribution, while increasing education as a response to stagnating or falling wages at each education level amounts to asking workers to run faster on a treadmill, making little progress against the overall deterioration of worker compensation.

This book, a joint effort of the Washington Center for Equitable Growth and the Institute for Research on Labor and Employment at the University of California, Berkeley, presents a series of essays from leading economic thinkers, who explore alternative policies for boosting wages and living standards, rooted in different structures that contribute to stagnant and unequal wages. The essays cover a variety of strategies, from far-reaching topics such as the U.S. social safety net and tax policies to more targeted efforts emphasizing laws governing American Indian tribal communities and the barriers facing women and workers of color in the science, technology, engineering, and mathematics fields.

These essays demonstrate that efforts to improve workers’ access to good jobs do not need to be limited to traditional labor policy. Labor income is still how most Americans achieve security and stability, but the determination of those earnings does not take place in a vacuum. Policies relating to macroeconomics, to social services, and to market concentration also have direct relevance to wage levels and inequality, and can be useful tools for addressing them.

We divide the essays presented in this book into three broad themes:

Worker power

Worker well-being

Equitable wages

Here are brief synopses of each of these themes.

Worker power

In recent decades, worker compensation has failed to keep up with economic growth and productivity. This is, in large part, a reflection of eroding worker bargaining power, which has not been strong enough to ensure that workers receive their fair share of the gains. Decades of declining unionization, poorly enforced labor market protections, and competition policy biased toward corporations have eroded worker bargaining power in the United States. A critical part of boosting workers’ earnings is to reverse this erosion and ensure that workers have the bargaining power to claim their share of employer profits.

A first step to boosting wages is making sure that legal protections and statutory minimum wages already on the books are enforced. In their essay titled“Strategic enforcement and co-enforcement of U.S. labor standards are needed to protect workers through the coronavirus recession,” Janice Fine, Daniel Galvin, Jenn Round, and Hana Shepherd at Rutgers University’s School of Management and Labor Relations highlight novel evidence on the prevalence of wage theft. This occurs when employers violate minimum wage or overtime pay statutes, essentially stealing the wages to which workers are legally entitled.

Unfortunately, workers have little recourse against this wage theft. The enforcement of these laws requires workers to file claims of their own accord, an expensive and risky proposition that is generally out of reach for exactly the groups of workers most at risk of wage theft. Fine and her co-authors propose strategic enforcement for likely violators, such as targeting wage theft investigations for employers in industries with higher rates of wage theft, and co-enforcement with organizations that are more effective at identifying violations, such as worker centers embedded within economically marginalized communities.

But the enforcement of labor standards takes place in an increasingly fissured and global economy. Work is increasingly outsourced from large companies to small contractors, where the large employer may control the work process but can disclaim responsibility for the treatment of workers. This depresses wages and reduces workers’ ability to claim the benefits of their productivity.

Economist Susan Helper at Case Western Reserve University discusses what she calls “supply chain dysfunction,” or when the outsourced company has little power against the outsourcing company so they must manage supply chain inefficiencies by cutting their own costs, which exerts a further downward pressure on wages. In her essay, “Transforming U.S. supply chains to create good jobs,” Helper examines how production is connected across companies and space. She proposes a new industrial policy that addresses the power imbalances of production in the United States. Small companies need to be able to share in the value created by supply chains so they can provide quality jobs, and collaboration and partnership must be promoted, so that supply chain ecosystems across manufacturing and service industries create dynamic and healthy labor markets.

Another, related factor influencing worker bargaining power is the increasing concentration of the economy into a small number of large, dominant employers that are able to exert substantial wage-setting power. In neoclassical models, the fact that many employers are competing for each worker’s labor ensures that workers will be compensated in proportion to their contributions, but when employment is concentrated (known as “monopsony”), this assurance falls apart. In “Boosting wages when U.S. labor markets are not competitive,” Ioana Marinescu at the University of Pennsylvania’s School of Social Policy and Practice reviews the evidence relating labor market concentration to wages, and proposes antitrust enforcement and increasing worker power as two tools to offset the wage-setting power that comes from further concentration.

It is not only microeconomists who are grappling with the growing disconnect between productivity and wages. This is also an important challenge to standard macroeconomic models. In “Collective bargaining as a path to more equitable wage growth in the United,” economist Benjamin Schoefer at the University of California, Berkeley reviews the macroeconomic literature on the presumptions and evidence for how the macroeconomy works, and finds various policies that promote worker bargaining power, such as sectoral wage determination, may help workers share in the fruits of their own productivity growth.

The policies in any of these essays work in tandem with fostering worker voice. Growing attention on fostering worker power is evident in initiatives such as the clean slate for worker power agenda from Harvard Law School’s Labor and Worklife Program. The proposals in the clean slate agenda would boost the effectiveness of each of the topics in this series, including a pathway toward sectoral bargaining and more protections for workers on-the-job.

Worker well-being

The second group of essays considers ways to improve worker well-being, given existing bargaining relationships. In “U.S. labor markets require a new approach to higher education,” economist Andria Smythe at Howard University points to universities—anchors of local economic activity and innovation—as key institutions that can contribute to worker well-being. She demonstrates that broad policies that increase access to education also support the higher education industry, which, in turn, fosters an innovative U.S. economy, creating a virtuous cycle that links individual skill-building to local economic activity to a more equitable U.S. economy across cities and regions of the nation.

Furthermore, Smythe details how accessible higher education tightens labor markets by eliminating the need for students to work while in school, which often both limits their engagement with school and takes jobs that might otherwise go to nonstudents. More accessible higher education would increase demand for workers and increase worker bargaining power.

Another policy approach is to adopt labor market policies that enable workers’ compensation to go further. An essay by one of the authors of this introduction, Jesse Rothstein at the University of California, Berkeley, and Columbia University’s Sandra Black, titled “Public investments in social insurance, education, and child care can overcome market failures to promote family and economic well-being,” demonstrates how rising costs of key necessities, such as higher education and medical and child care, as well as increasing risk faced by workers, erodes worker well-being and thus their effective wages.

Rothstein and Black argue that the public provision of early childhood education, the alleviation of student debt, and the provision of comprehensive social insurance such as Unemployment Insurance, retirement security, health insurance, and long-term care insurance would all help build the foundation for workers to have a lower cost of living and security to invest in their economic futures. This kind of social safety net would mitigate downside risks while also fostering a more resilient economy, in which economic shocks and business cycles will be less likely to lead to permanent negative consequences for workers and families.

Another aspect of promoting wage growth for workers are tax policies that influence corporate investment and sharing the gains of productivity growth. In an essay titled “Targeting business tax incentives to realize U.S. wage growth,” economist Juan Carlos Suárez Serrato of Duke University describes the different ways that corporations respond to tax cuts. Do they take them as windfalls to distribute to shareholders, with no benefit for workers, or do they use them to invest in productivity enhancements that would lead to increased worker compensation? He suggests that the design of the tax cuts influences their allocation, and proposes that tax cuts need to be linked to wage gains for workers to ensure that companies share gains with workers to improve the well-being of their employees and their families.

Equitable wages

The third group of essays considers strategies for reducing wage disparities to create more equitable wage structures across the U.S. labor market for all U.S. workers. A labor market in which workers from historically marginalized backgrounds are able to access equitable opportunities is a labor market that works for everyone.

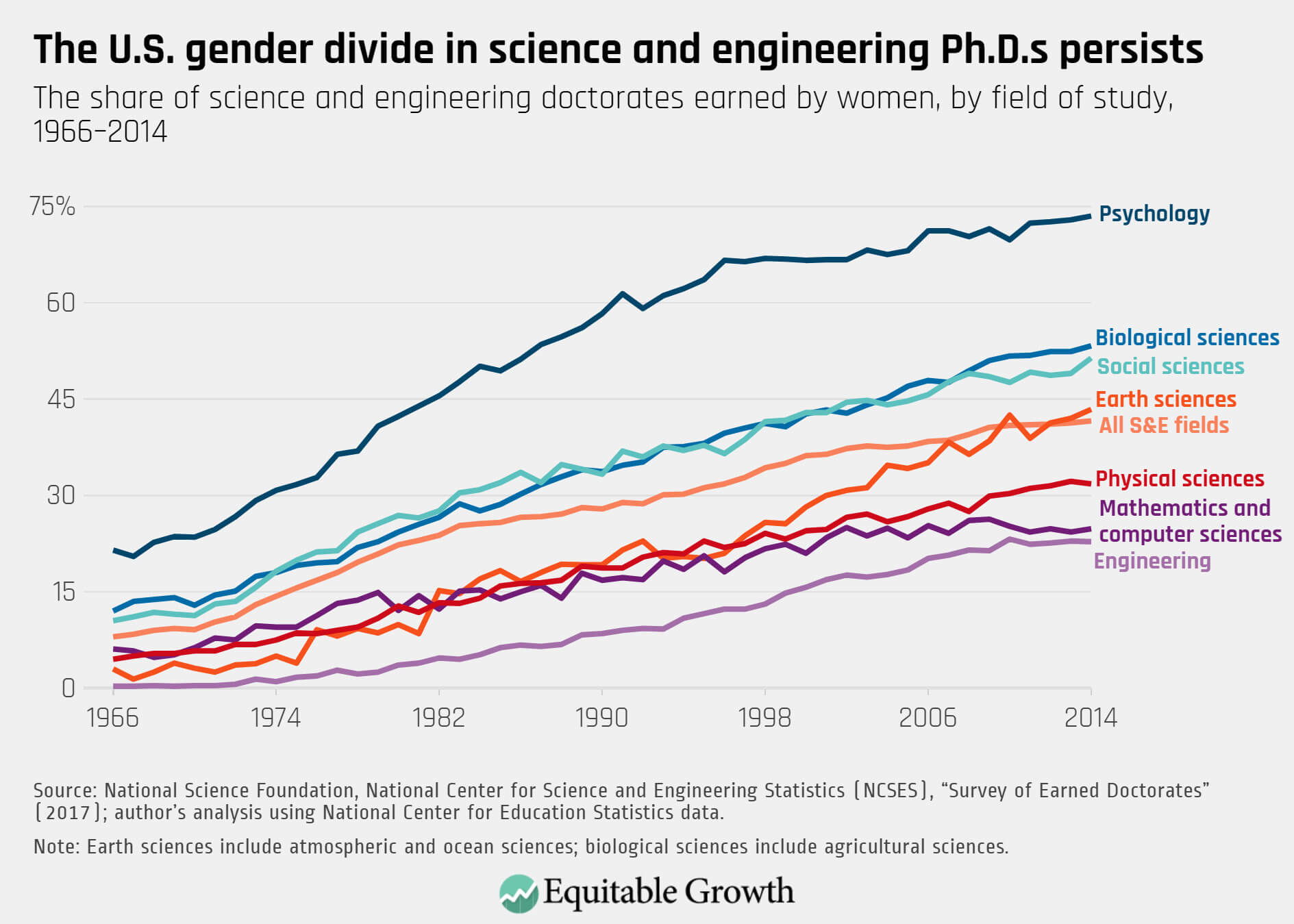

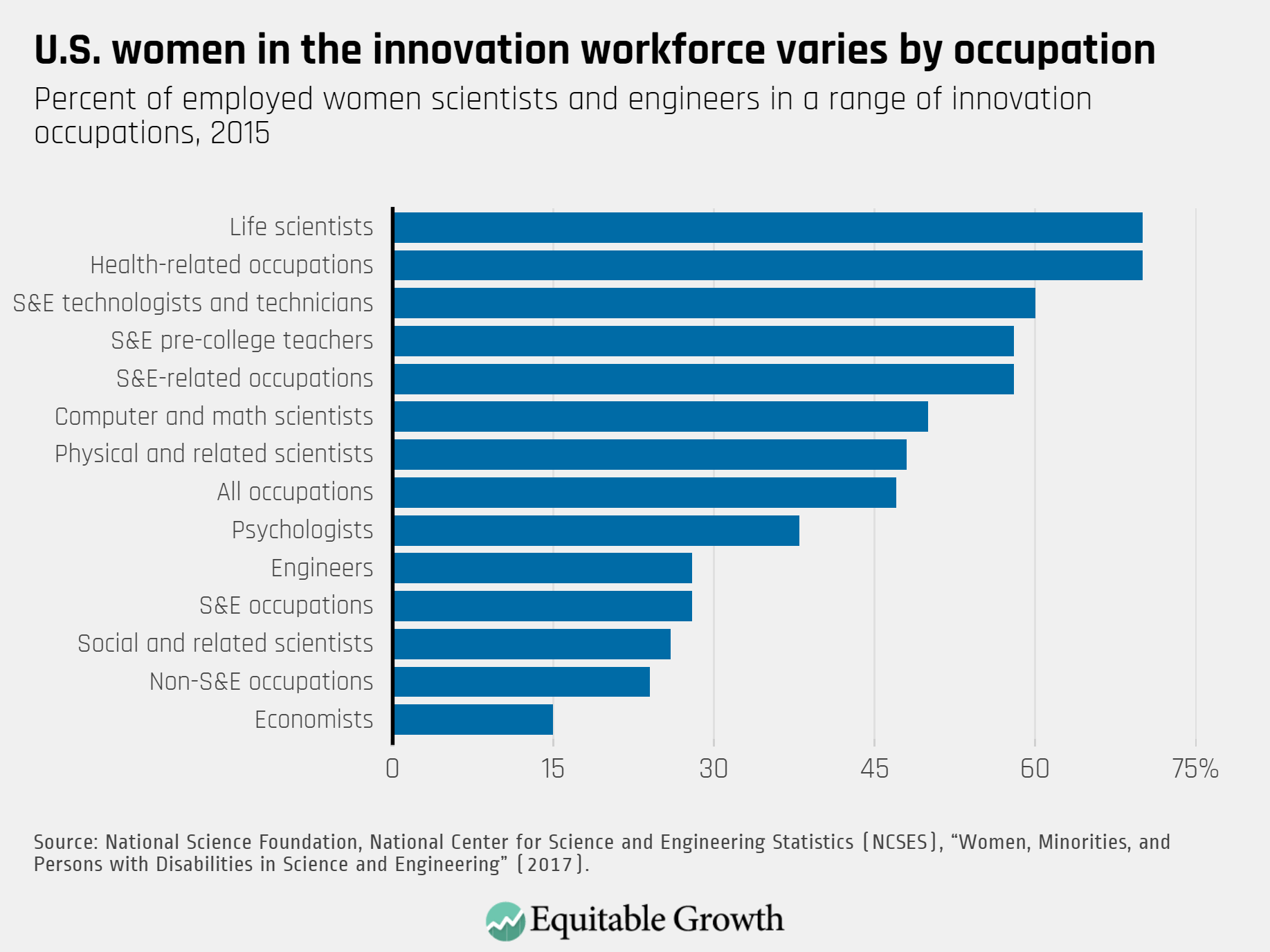

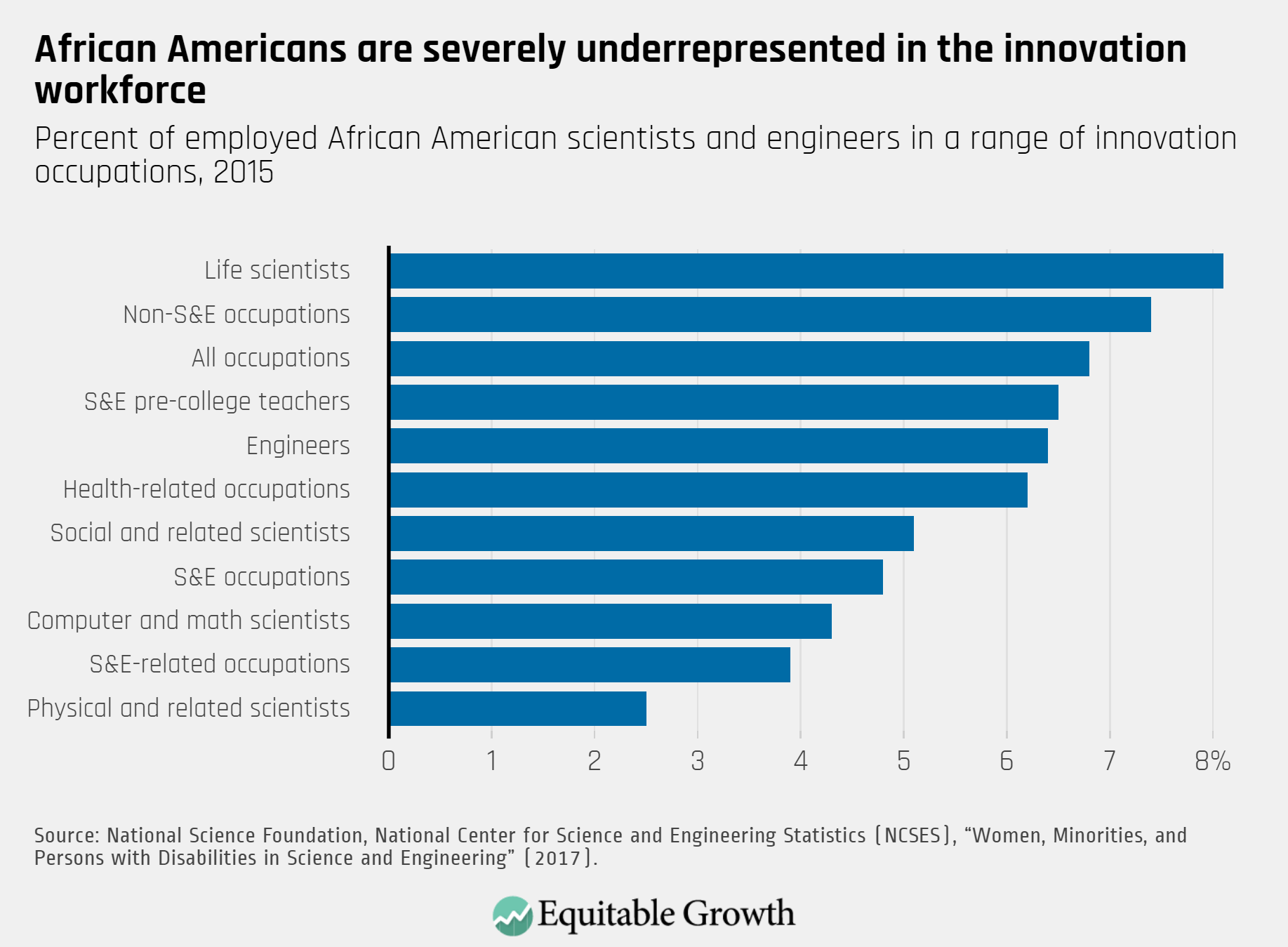

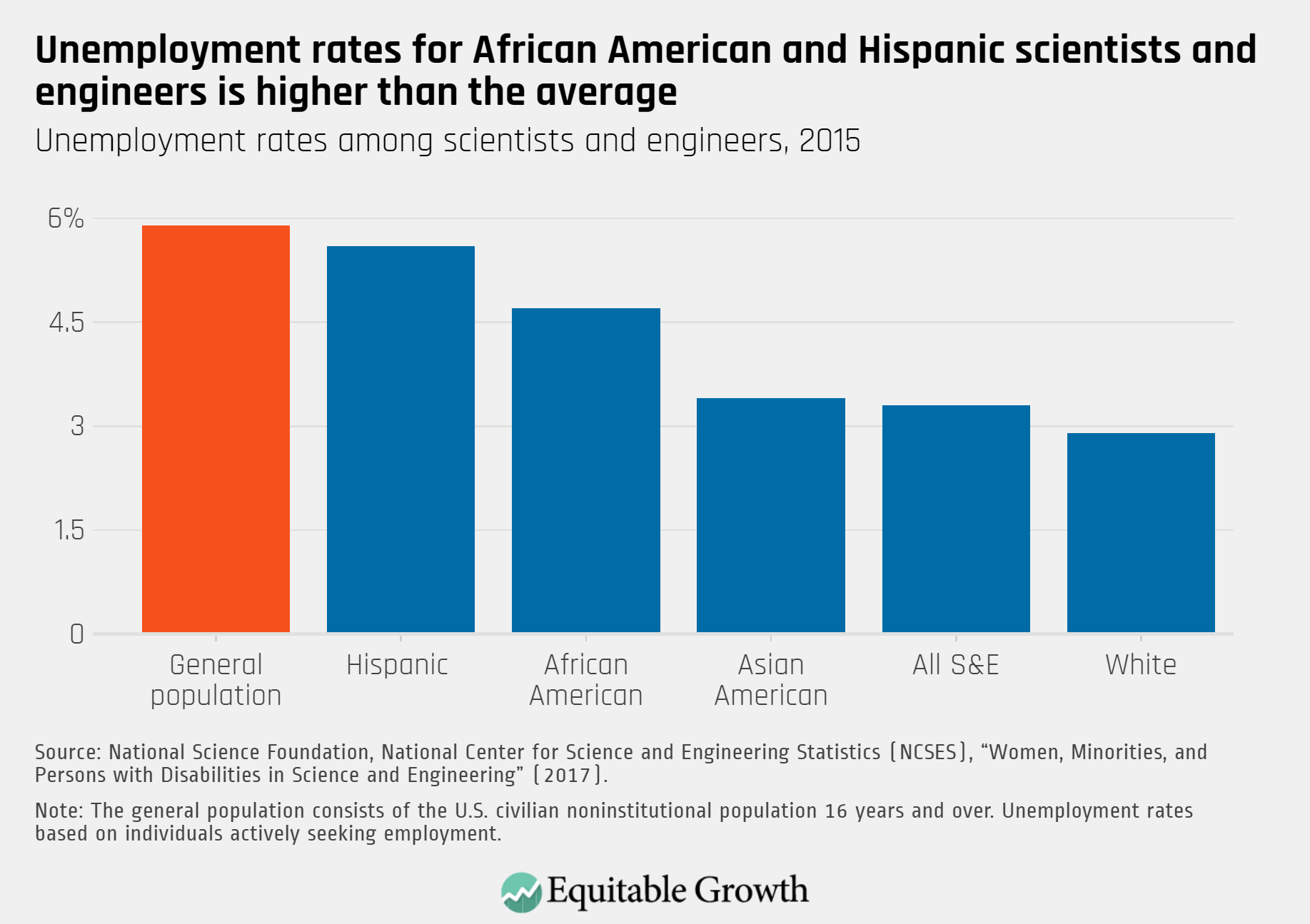

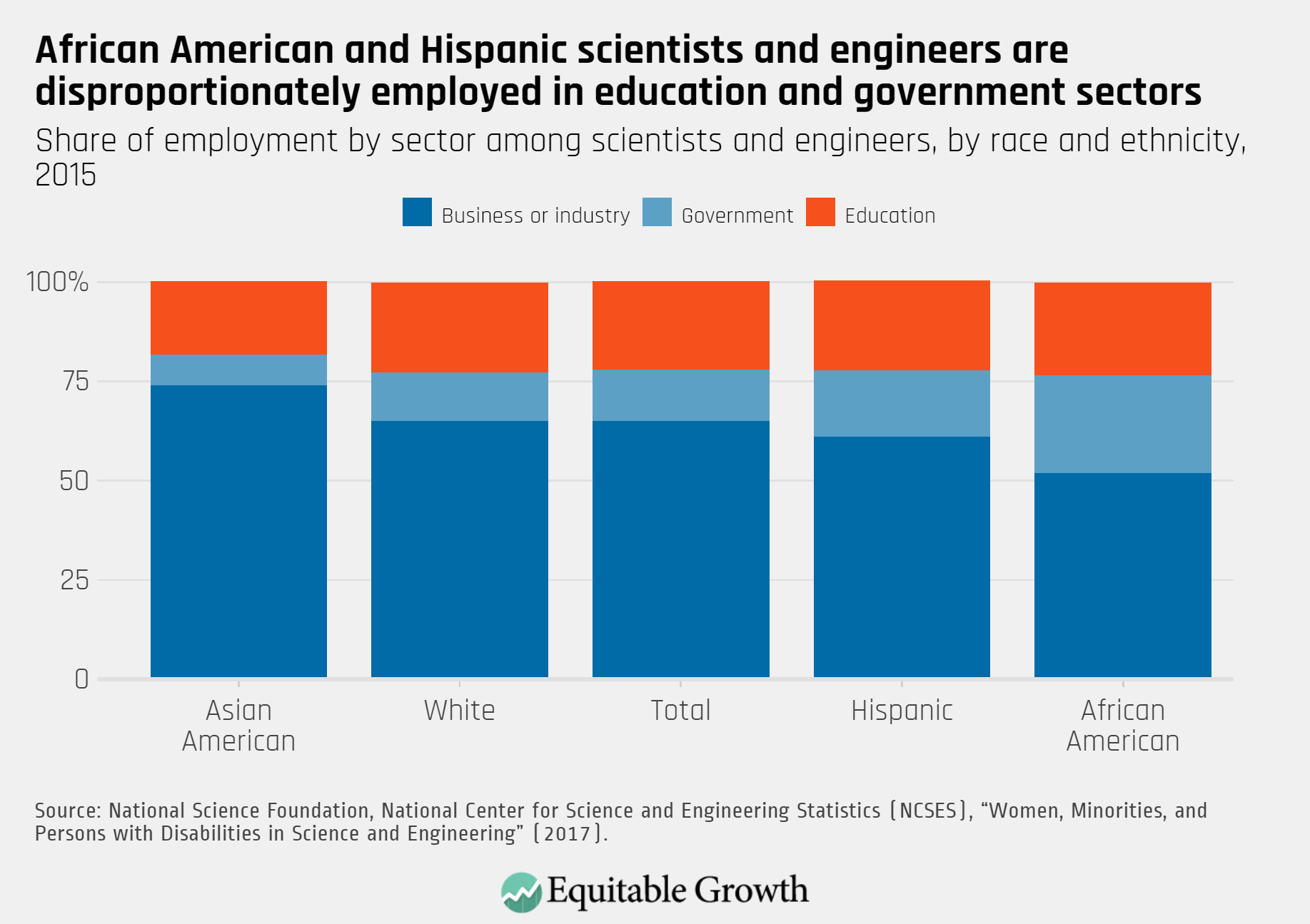

In her essay on racial and gender inclusion in the so-called STEM fields of science, technology, engineering, and mathematics, titled “Addressing gender and racial disparities in the U.S. labor market to boost wages and power innovation,” economist Lisa Cook at Michigan State University demonstrates how marginalized groups, particularly women and Black workers, face barriers at each stage of the innovation pipeline, limiting economic growth and prosperity for all. Cook argues for investments, mentoring support, and other practices to not only open the doors to STEM education and research for underrepresented groups, but also to allow Black and women innovators to share in the gains from their work.

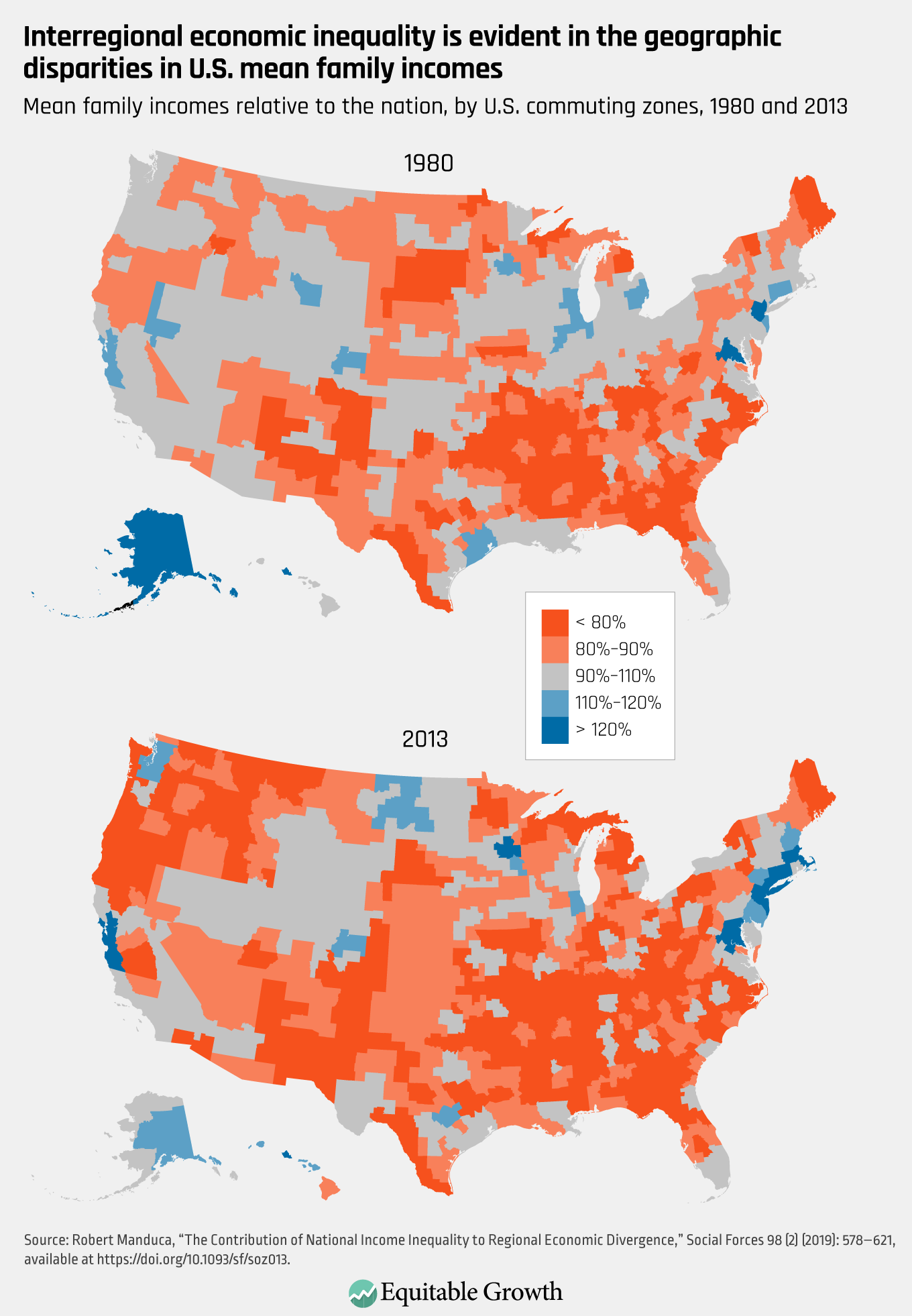

Sociologist Robert Manduca at the University of Michigan demonstrates that a great deal of wage inequality ranges across geographic regions. In his essay, “Place-conscious federal policies to reduce regional economic disparities in the United States,” he proposes place-conscious universal policies to address geographic wage inequality. Increasing geographic inequality is exacerbated by deregulation in the transportation and communications industries and by weak antitrust enforcement, which favors increasingly powerful companies and well-connected urban areas. Manduca points out that the enforcement of national antitrust policy is especially important in those locations where there are dominant employers, such as those described in Marinescu’s essay. Universal programs, such as a broader social safety net and creating jobs through direct public investment and employment, can help boost wages in communities that have been left behind, increasing economic security for workers and families located in these economically depressed regions of the nation.

This book closes with an essay examining one of the most marginalized groups in the U.S. labor market, Native Americans, who face extremely high rates of poverty and unemployment due to myriad economic, social, and political injustices inflicted over centuries of oppression. In his essay, “Sovereignty and improved economic outcomes for American Indians: Building on the gains made since 1990,” Randall Akee at the University of California, Los Angeles reviews the current status of tribal communities across the United States. He considers what is needed to create structures, including improving infrastructure and education, that allow for economic growth and prosperity after centuries of marginalization, oppression, and genocide.

Policies that address structural economic issues in tribal reservations can also impact economic inequality in the surrounding regions, particularly in states in the West and Southwest, where American Indians make up larger shares of the population. Akee writes that the specific historical and cultural context of tribal sovereignty is a critical aspect of boosting wages for workers from these communities. He also calls for improving outcomes in tribal communities by improving data collection and researching the barriers to economic development.

Worker empowerment matters for all policies

A theme that runs across all of these essays is that worker empowerment is crucial to ensuring wage equality and financial security across the U.S. labor market. The essays provide a set of roadmaps for encouraging wage growth and reducing wage inequality by the creation of underlying economic structures that allow workers, particularly those who face the greatest barriers, to advance in their careers, contribute to productivity growth, and share in the gains of a robust and resilient economy.

As the U.S. economy eventually recovers from the coronavirus recession and progresses into another period of economic growth, the policies developed by top academics in this series of essays provide a pathway for more equitable growth. Dealing with the baleful economic consequences of economic inequality now, which the current pandemic has laid bare, would result in stronger and more sustainable economic growth in the years and decades ahead.

This essay is part ofBoosting Wages for U.S. Workers in the New Economy, a compilation of 10 essays from leading economic thinkers who explore alternative policies for boosting wages and living standards, rooted in different structures that contribute to stagnant and unequal wages. The authors in the new book demonstrate that efforts to improve workers’ access to good jobs do not need to be limited to traditional labor policy. Policies relating to macroeconomics, to social services, and to market concentration also have direct relevance to wage levels and inequality, and can be useful tools for addressing them.

To read more about Boosting Wages for U.S. Workers in the New Economy 20 and download the full collection of essays, click here.

Overview

The coronavirus pandemic and resulting recession combine to create a uniquely dangerous time for low-wage workers. U.S. unemployment hit record highs in April 2020 and remains persistently elevated. And employers are more likely to break labor laws and take advantage of low-wage workers, both in sectors where labor law violations are traditionally high and in sectors that normally have higher rates of compliance. These dangers confront workers because in a pandemic-induced recession they are in even weaker positions to speak up for themselves, report violations, or find new jobs.

Evidence from the Great Recession of 2007–2009 indicates that high levels of unemployment weakened the labor market power of those low-wage workers who remained employed. Our recent research on minimum wage violations during the Great Recession found dramatic increases in these violations that disproportionately harmed noncitizens, Latinx, Black, and women workers.1 It is therefore critically important that federal, state, and local labor standards are vigorously and strategically enforced during times of economic stress.

Webinar: How to strengthen U.S. labor standards enforcement to protect workers’ rights

Yet state and local governments are facing extraordinary budget deficits. This fiscal crisis makes it even more difficult for state and local labor enforcement agencies to respond to violations, just when this work is needed most. This essay summarizes our findings and proposes two complementary frameworks for greatly strengthening enforcement:

Strategic enforcement, in which labor standards enforcement agencies target high-violation industries and maximize the use of enforcement powers to increase the cost of noncompliance

Co-enforcement, in which labor standards enforcement agencies engage in sustained partnerships with worker centers, unions, legal advocacy organizations, and other community-based organizations embedded in low-wage worker communities and high-violation sectors

We then put forward some federal policy recommendations to enact these two robust enforcement standards.

The problem: High unemployment will likely lead to dramatically increased violations while state and local governments face massive budget deficits

The coronavirus pandemic and the resulting disruption to the global economy is unprecedented in modern times. In February 2020, unemployment in the United States was at 3.5 percent, a 50-year low.2 By April 2020, unemployment rose to a staggering 14.7 percent, the largest increase in the history of the series.3 In just 2 months, job losses due to the pandemic surpassed the total number of jobs lost from December 2007 to June 2009 during the Great Recession.4 These job losses disproportionately affected Latinx, Black, and female workers.5 By the end of 2020’s third quarter, the unemployment rate remained at 7.9 percecnt, with 12.6 million people without a job.6

Like the current recession, Black and Hispanic communities also faced disproportionate rates of unemployment during the Great Recession. Black unemployment peaked at 16.8 percent, while the Hispanic unemployment rate reached 13 percent, both of which were markedly higher than the 9.2 percent high for White workers.7 Though shocking, these outcomes are unsurprising, as workers of color are disproportionately employed in industries and occupations that are more vulnerable to cyclical downturns.8

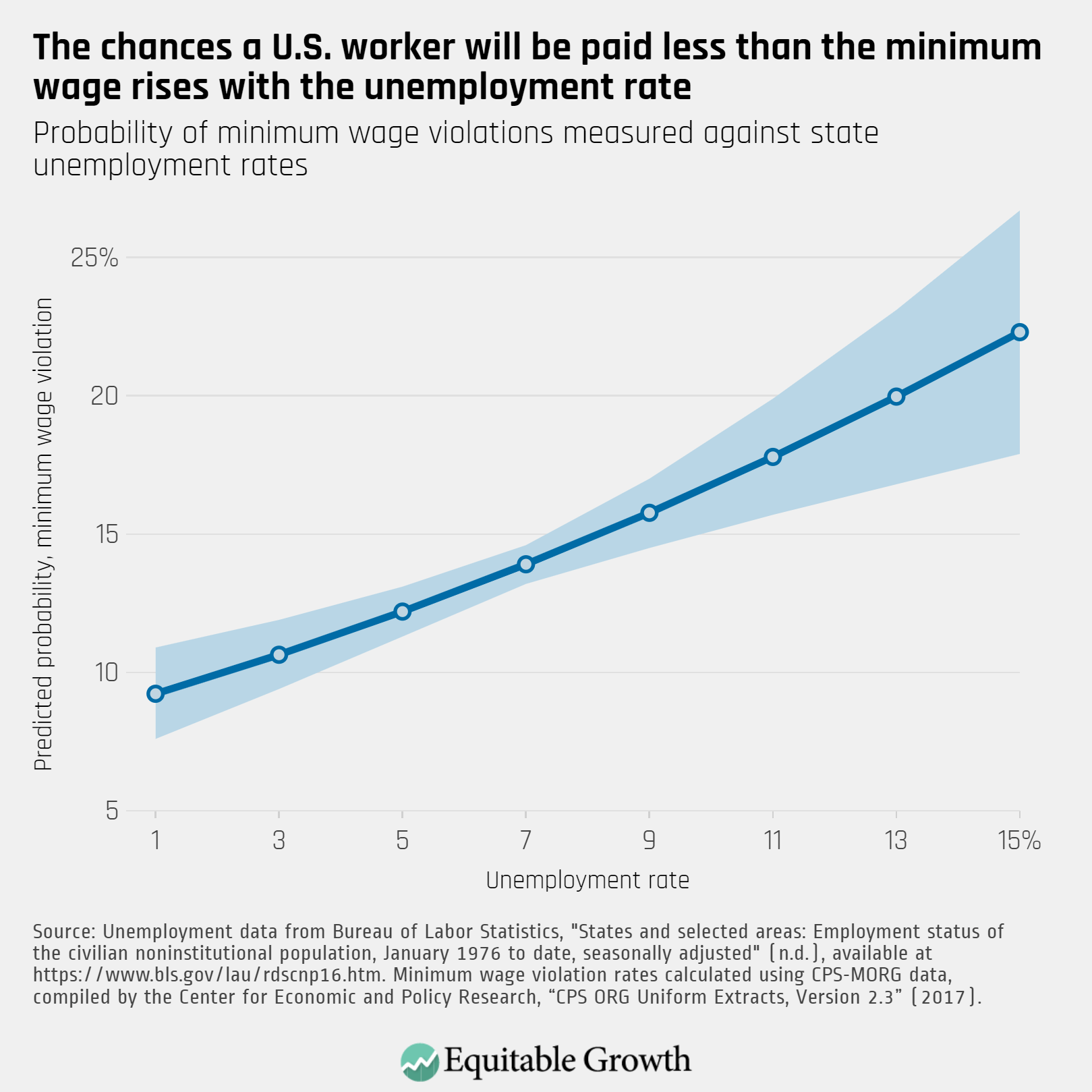

While the circumstances surrounding the Great Recession are markedly different, data from that period provide insight into what we can anticipate for workers amid the current coronavirus recession. Using Current Population Survey data, we estimate that the probability that any given low-wage worker would be paid below their applicable minimum wage ranged from about 10 percent to about 22 percent between 2007 and 2013, with each percentage point increase in their state’s unemployment rate predicting, on average, almost a full percentage point increase in the probability they would experience a violation. The average amount of money these workers lost to minimum wage violations was 20 percent of their hourly wage, or $1.46 per hour on average. (See Figure 1.)

Figure 1

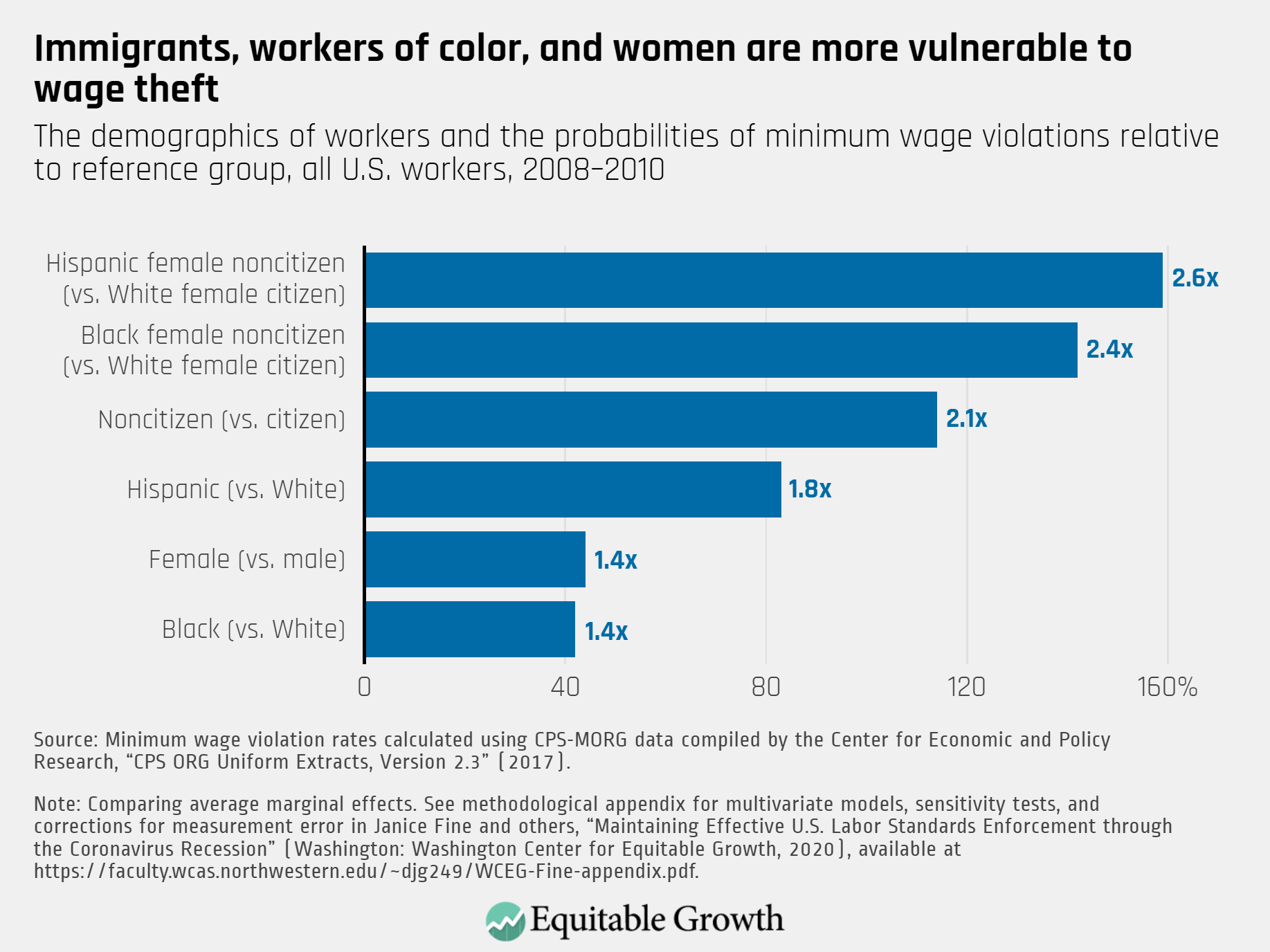

Notably, the negative consequences of the Great Recession were shouldered by some groups of workers more than others. To assess the relative likelihood that workers in key demographic groups would experience minimum wage violations (relative to the reference group), we examine all workers during the height of the recession and its immediate aftermath in 2008–2010. We find that the probability of experiencing minimum wage violations was much greater for women, noncitizens, Hispanic, and Black workers. When the interaction of gender, race, and citizenship are taken into account, the effects of discrimination are compounded. Hispanic women who were not U.S. citizens, for example, were 2.6 times more likely to experience a minimum wage violation than White female citizens, while noncitizen Black women were 2.4 times more likely. (See Figure 2.)

Figure 2

New research suggests that minimum wage laws can reduce the racial earnings divide, which is now larger than it was in 1979,9 as well as income divides.10 But when the right to be paid the minimum wage is not realized, policymakers can expect the efficacy of such efforts to be curtailed, with dire consequences of minimum wage violations for workers and their families. A 2017 Economic Policy Institute report found that failure to pay workers the applicable minimum wage for all reported hours increased the percentage of workers living in poverty from 14.8 percent to 21.4 percent in the 10 most populous states.11

In addition to the extraordinary job losses in the private sector caused by the coronavirus recession, the shuttering of the U.S. economy also sharply reduced public-sector revenues, which, combined with unanticipated expenditures related to the coronavirus recession, leaves state and local governments at all levels with substantial deficits, leading inexorably to more and more mass layoffs of public-sector workers.

As a result of state and local budget cuts, funding for labor standards enforcement is almost certain to decrease. Troublingly, even in times of economic prosperity, there is little funding for labor standards enforcement. A survey by two of the authors of this essay, alongside Greg Lyon at Rutgers University, conducted in 45 states and cities that enacted labor standards laws between 2012–2016, found that 27 percent of the states received no additional funding at all for enforcement, and another 13 percent received $50,000 or less. At the city level, more than 50 percent have no funding whatsoever to carry out the new policies, and another 22 percent have $50,000 or less.12

This lack of funding at the state and local levels means that even in some jurisdictions that have passed higher state and local minimum wage policies, the U.S. Department of Labor’s Wage and Hour Division is effectively the sole enforcement agency working to ensure compliance. The division, though, has its own resources deficit. As of May 1, 2020, for example, it employed 779 investigators to protect more than 143 million workers, which is significantly fewer than the 1,000 investigators employed in 1948 when the division was responsible for safeguarding the rights of only 22.6 million workers.13

Research by labor economists demonstrates that U.S. employers weigh the costs and benefits of minimum wage compliance and are more likely to violate the law if there is a low probability of being investigated or face minimal fines even if they are caught.14 Without resources for effective enforcement, hard-won state and local minimum increases are at great risk. More broadly, unaddressed wage theft facilitates unfair competition where weaker firms in an industry are able to undercut compliant firms. Widespread wage theft can undermine the whole structure of wages in an industry.

The challenge: Complaint-based enforcement overlooks violations against vulnerable workers

Labor enforcement agencies across the United States overwhelmingly engage in a reactive complaint-based approach to enforcement, in which agencies assume that when workers experience a violation, they will complain to the appropriate public agency that will then investigate it. Complaint-based enforcement became the default mode of enforcement in the early years of the Fair Labor Standards Act of 1938 and largely remained so until the Obama administration.15 Likewise, in our survey previously cited above, 70 percent of cities surveyed indicated their enforcement is complaint-driven while 54 percent of states interviewed said the same.16

Despite the prevalence of complaint-based enforcement, the model is inadequate. First, complaint-based enforcement has failed to keep up with the growth of subcontracting and attenuated labor and product supply chains—new firm and industry structures and strategies and employment arrangements that continue to evolve.17 Low-wage industries in particular are experiencing an explosion of what David Weil, the former head of the federal Wage and Hour Division, calls the “fissuring” of the employment relationship.18

Fissuring occurs when companies shift the direct employment of workers to other business entities through increased reliance on strategies such as subcontracting, use of temporary employees, and independent contracting arrangements.19 Often, firms are embedded in subcontracting networks, in which one large firm or a few firms are setting the terms of exchange but are not the employers of record for the purposes of labor standards enforcement.

Second, complaint-based enforcement tends to embrace an individualized regulatory approach that conceives of each individual case—or worker complaint—as an isolated and idiosyncratic incident. This means that even a high number of individual cases or complaints are unlikely to lead to structural reforms across an industry. Agencies handle each worker complaint as a separate transaction that yields no other regulatory actions beyond opening and closing the particular case at hand; the case itself is considered apart from the broader structural context from which it emerged and without an eye toward systemic reform.20

Third, research on minimum wage enforcement suggests that workers in some of the industries with the worst conditions are much less likely to complain about wage theft.21 Comparing complaint rates to estimates of underlying minimum wage violations in various state and local jurisdictions across the United States, we find an insufficient overlap to justify enforcement based solely on complaints.

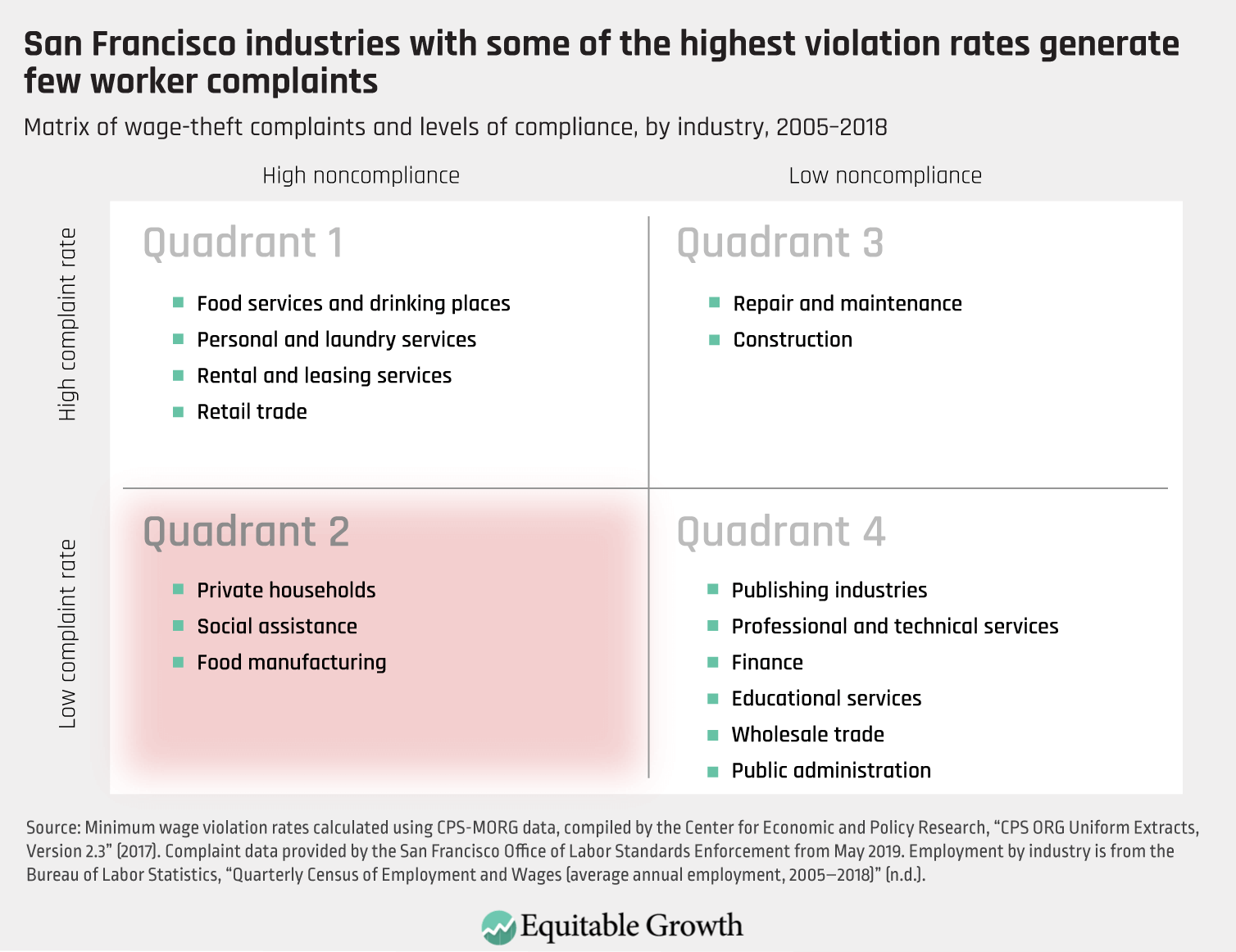

Even in some of the most progressive cities with well-funded local enforcement agencies, there are stunning gaps between the industries with the highest rates of complaints and those with the highest violation rates. Our study of San Francisco, for example, demonstrates that in many industries, the number of minimum wage complaints reported to the San Francisco Office of Labor Standards Enforcement was significantly lower than estimated violation rates in those industries. We compare the actual number of complaints submitted to the agency to estimates of minimum wage violations by industry in 2005–2018, again using CPS data. We find that violations in the private households, social assistance, and food manufacturing industry sectors were among the highest of any industry, but workers in these three industries made very few complaints to the city’s labor standards enforcement agency.22 (See Table 1.)

Table 1

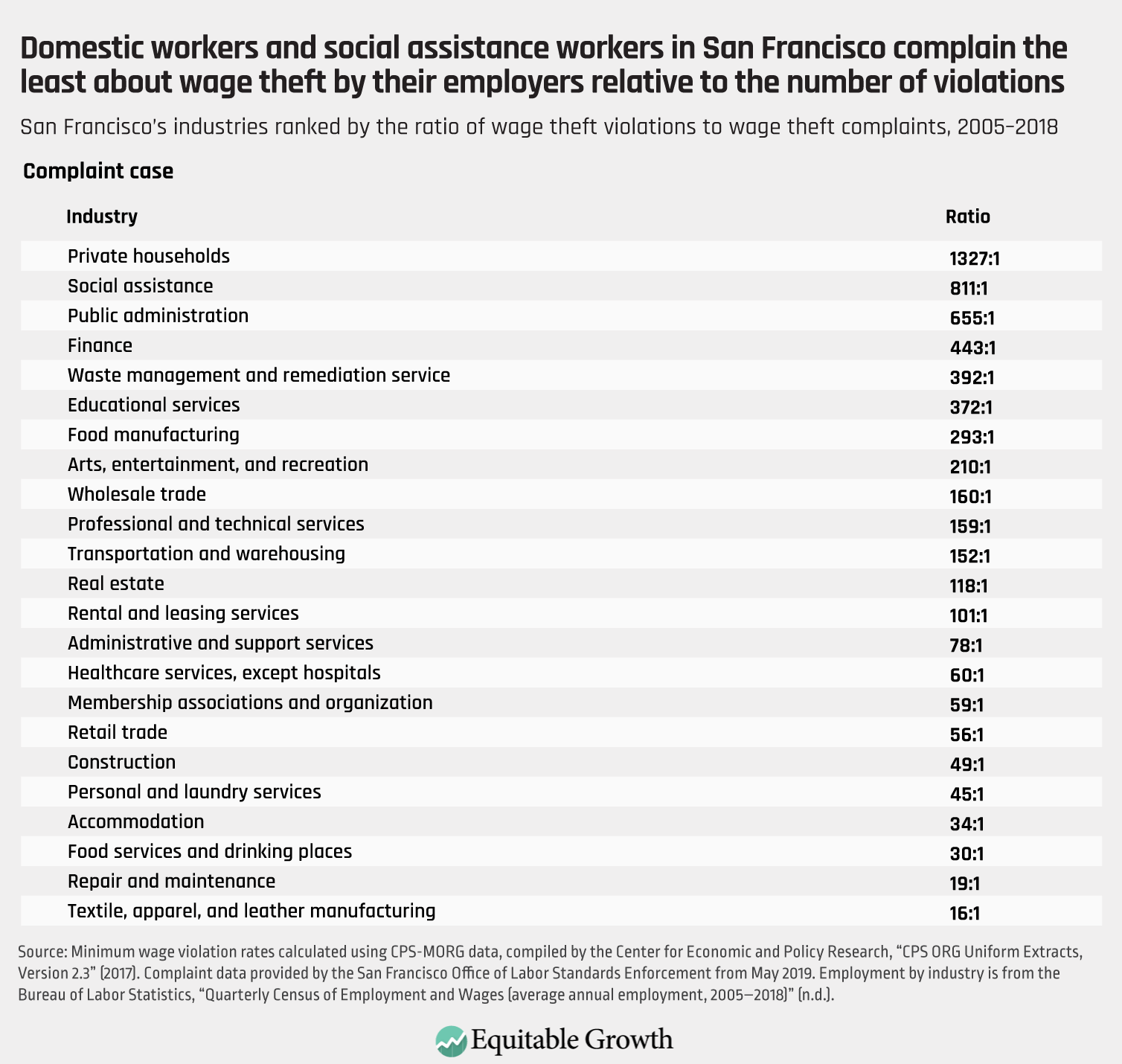

Another way to think about the extent of the discrepancy between individually driven complaints and minimum wage violations is to calculate a ratio for each industry.23 In San Francisco, more than 1,300 violations are estimated to occur for every one worker complaint in the private households industry, which largely employs child care workers, personal and homecare aides, and housecleaners. In social assistance, an industry in which a significant number of child care workers, cooks, and homecare and home health aides work, more than 800 violations are estimated to occur for every one complaint. (See Table 2.)

Table 2

Such results demolish the premise of the complaint-based enforcement model—that workers whose rights are violated will speak up. On the contrary, we find that some of the most regularly exploited workers are among the leastlikely to complain. In the complaint-based enforcement model, quiet industries are presumed to be compliant industries, not industries where workers are suffering silently.

The consequences of this faulty assumption are grave. Where enforcement is most needed, few investigations are triggered. Meanwhile, labor standards enforcement agencies inefficiently devote resources to pursuing complaints in far more compliant industries. These inequalities are only likely to be exacerbated in the context of a recession, and particularly amid the current pandemic-induced recession.24

The discrepancy between individual complaints and business violations is caused by asymmetries of power between low-wage workers and the firms for which they work. Workers with the least power and few alternative employment options face barriers that keep them from stepping forward to complain much of the time.25 In a recession, high unemployment increases workers’ desperation to maintain any job, thus tipping the power imbalance even further toward firms. Again, looking back at violations during the Great Recession is instructive. We find that workers who belonged to a union were more than three times less likely to experience a minimum wage violation than workers who did not belong to a union.

Just as noncitizen workers and workers of color became more vulnerable during the Great Recession, we expect, given the current coronavirus recession, that they will once again become highly vulnerable but unlikely to file a complaint out of fear of losing their jobs.

Frameworks for changing U.S. labor enforcement standards

Given the likelihood of the persistence of the coronavirus pandemic and recession, what is the most effective framework to enforce labor standards laws when violations increase and enforcement resources are further diminished? There are two primary, interrelated frameworks that answer this question: strategic enforcement and co-enforcement.

Strategic enforcement of labor standards

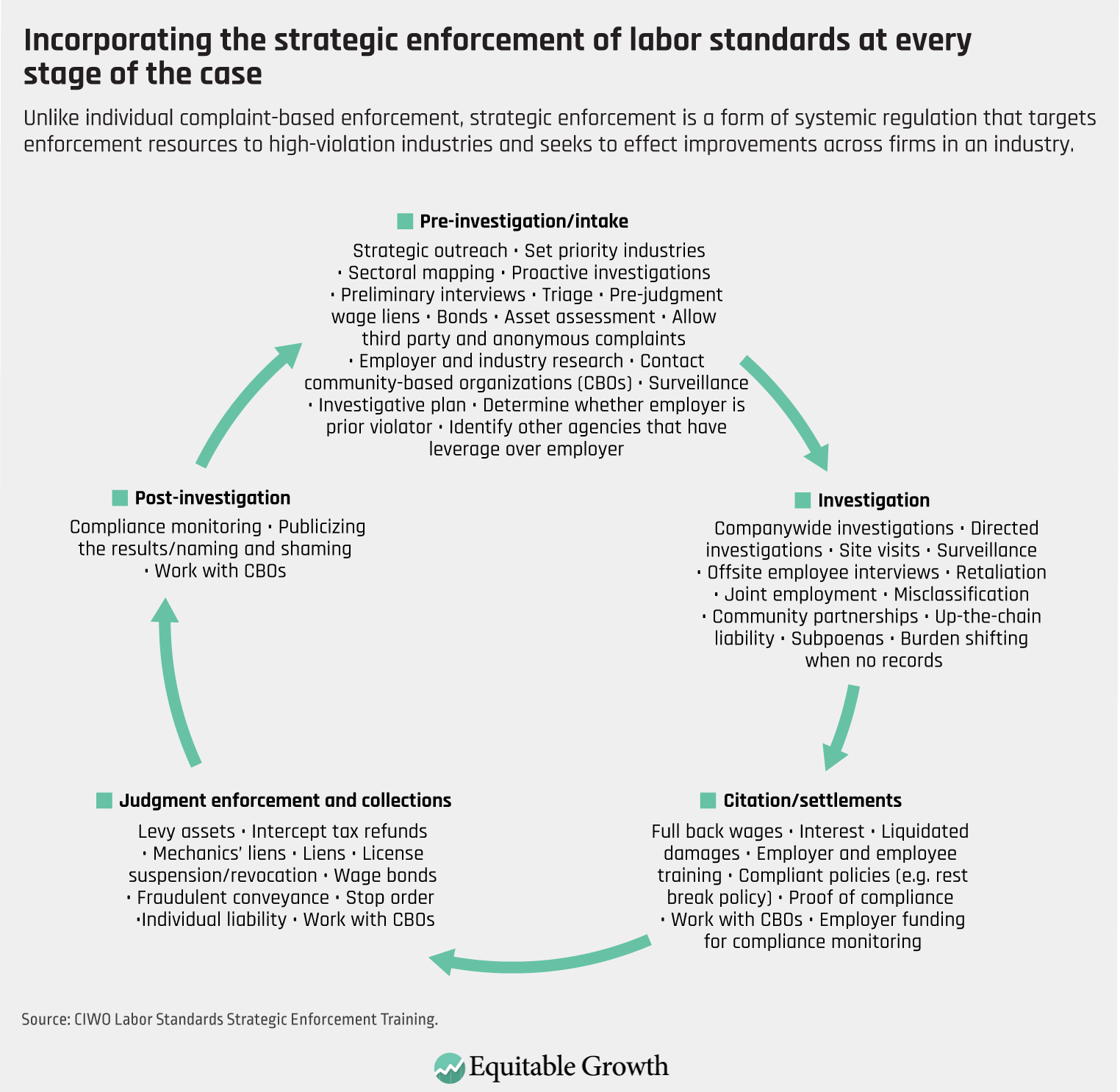

Strategic enforcement is a form of systemicregulation that conceives of each violation as a potential signal of a broader pattern of labor market violations.26 Unlike complaint-based enforcement, in which each case is typically processed as an isolated or idiosyncratic incident, a strategic enforcement model analyzes complaints for underlying causes and targets enforcement resources to high-violation industries.

As articulated by David Weil, the overarching goal of strategic enforcement is “to use the limited enforcement resources available to a regulatory agency to protect workers as prescribed by laws by changing employer behavior in a sustainable way.”27 At the federal level, the main components of strategic enforcement include a proactive, rather than reactive, approach to investigations, targeting industries high in violations but low in complaints, maximizing the extent of legal penalties imposed on violators, informational campaigns to businesses and workers, strategic communications and signaling to employers, robust compliance agreements with violators, and using data to measure effectiveness.28

Of course, federal, state, and local enforcement agencies operate in vastly different political climates and with a wide variety of statutory powers and bureaucratic limitations. Accordingly, strategic enforcement cannot be cast in “one size fits all” or “all or nothing” terms. Instead, there is a full complement of tools and techniques that agencies can use at each stage of the process to achieve broad, long-term compliance. Agencies can adopt and incorporate some of these strategic practices and work toward adopting others by taking on administrative and statutory limitations over time. (See Figure 3.)

Figure 3

Strategic enforcement addresses gaps created by traditional complaint-based enforcement in several ways. First, the use of proactive investigations in targeted industries means enforcement resources are more likely to identify and reach vulnerable workers who are unlikely to complain. Agencies looking to target high-risk sectors in this pandemic-triggered recession should look to those low-wage sectors in which unemployment rates are the highest. These include food service and drinking places; accommodation; arts, entertainment, and recreation; transportation and warehousing; personal and laundry services; private households; retail trade; administrative and support services; and social assistance.29 Likewise, industry research to identify industry structure, influential employers, and widespread noncompliant industry practices help agencies target employers that are likely to get the attention of others in the industry.

In addition to proactive investigations, strategic enforcement includes implementing a triage system to sort complaints, so that high-violation industries with high- and low-complaint rates are prioritized,30 maximizing the use of statutory tools that are designed to address common enforcement impediments and disincentivize bad-faith employers from acting to obscure noncompliance,31 and assessing high damages and penalties in addition to back wages owed to deter future violations.32

Addressing the fissuring of employment relationships is also key. Holding those with the most power and reputational risk in the contracting relationship liable for downstream violations through joint employment analyses, combined with a press strategy to publicize investigations, is crucial for maximizing the ripple effects of strategic enforcement.33 Finally, robust collections efforts and tools that ensure workers in fact receive money they are owed and innovative settlement terms that address the root of violations while promoting ongoing compliance are also central components of strategic enforcement.34

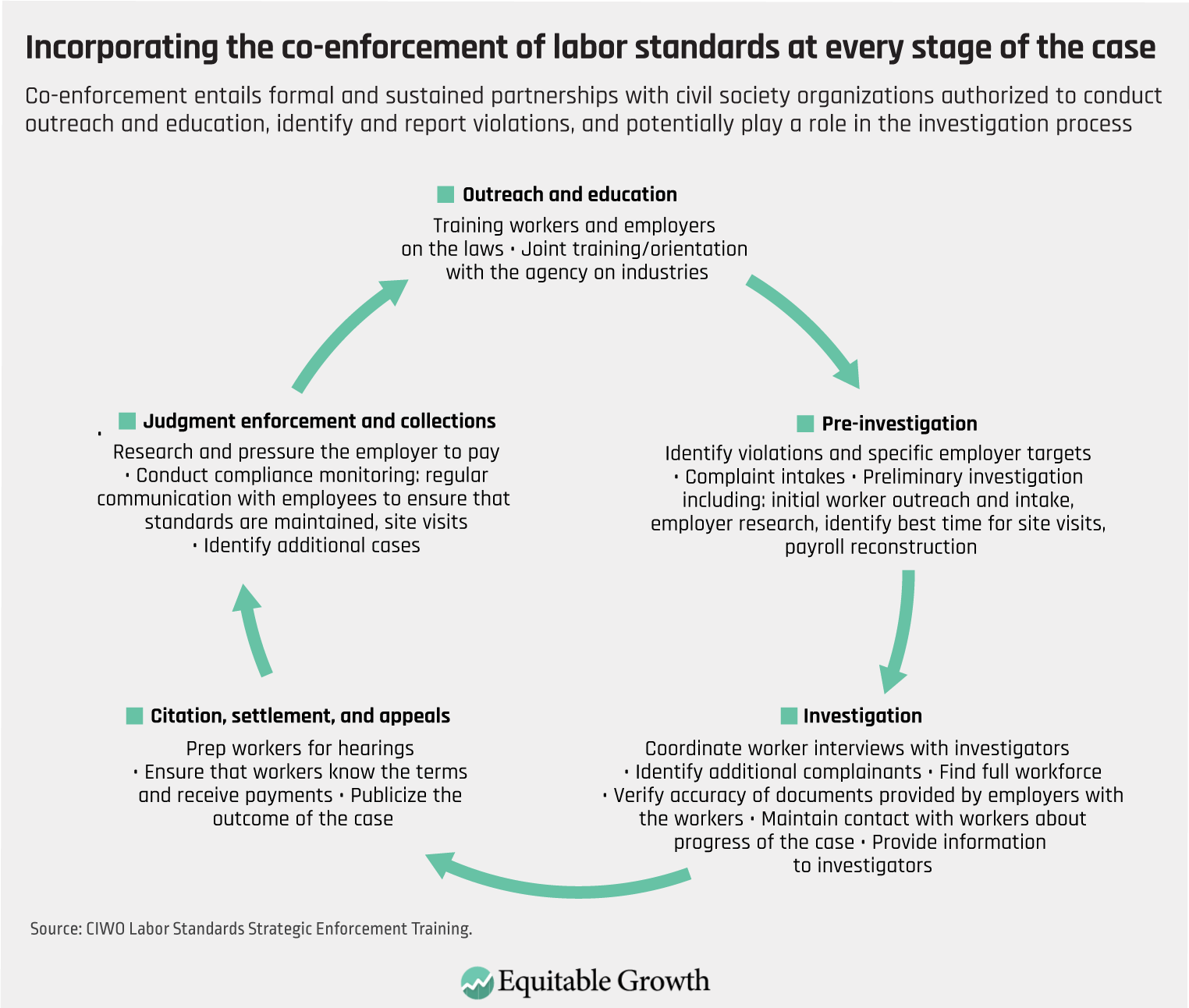

Co-enforcement of labor standards

Strategic enforcement is a logical response to the coronavirus recession, but it will not succeed unless it is accompanied by a significant enhancement of workers’ voices.35 Simply put, problems will remain hidden unless workers speak up, yet vulnerable workers will not speak up in isolation. Likewise, as strategic enforcement includes moving to a more proactive investigative approach, it renders co-enforcement—sustained partnerships with worker centers, unions, legal advocacy organizations, and other community-based organizations that are embedded in low-wage worker communities and high-violation sectors—essential to addressing the enforcement challenges created by the 21st century labor market.36

To illustrate this, we must consider why the vast majority of agencies continue to utilize the complaint-based enforcement model. One reason is that complaints often provide a foundation from which to build a strong case. In reacting to a complaint, before an investigation even begins, the agency has a cooperating witness and an array of information that may include the nature of the violations, how the employer may attempt to hide violations, names of management and ownership personnel, and other facts relevant to the case. Worker participation and evidence is particularly important in establishing violations and back wages owed in more difficult investigations, in which employers have no records or have falsified timesheets and payroll records to appear compliant. Without a connection to the workforce on which the agency can build an investigation, proactive investigations can be daunting and the agency may be unable to establish violations are occurring.

Worker organizations have access to information on compliance with labor standards that would be difficult, if not impossible, for state officials to gather on their own.37 It is often only when the organization that has relationships with vulnerable workers has vouched for a government agency that they have been willing to come forward. By building on existing trust between workers and organizations, investigators can gain access to the knowledge and information workers possess about violations.38

Additionally, through their relationships and local credibility, community organizations can educate workers, encourage them to file complaints, and help to gather testimony and documentation. Drawing on workers’ networks, community organizations can also recruit workers from problematic firms and industries by providing a safe space and interpretation and facilitation services, as well as helping state inspectors meet with workers who may be too intimidated to go to a government office. They also exercise a kind of moral power and broaden public support for robust enforcement when they document and publicize egregious examples and patterns of abuse.39

Enforcement agencies face a wide range of political pressures not to engage in vigorous enforcement. Worker organizations can act as countervailing points of pressure and when an investigation is undertaken by an agency, through their relationships with workers, can continue to monitor the employer over time, after inspectors have moved on to new cases.40 (See Figure 4.)

Figure 4

The effectiveness of combining strategic enforcement with co-enforcement is not merely theoretical. One of the greatest success stories comes from California, wherein Julie Su’s appointment as labor commissioner in 2011 placed a longtime advocate from a legal advocacy organization who had seen firsthand the inadequacies of the existing system into a top leadership position. Su revolutionized the enforcement model and internal culture of the agency such that the California Labor Commissioner’s Office marshalled its full powers, sought additional powers from the legislature over time (with the support of labor and community allies), systematically changed management and personnel practices, and brought community partners into the very center of its strategic enforcement efforts.

These changes achieved powerful results. Through its partnerships, the state’s Labor Commissioner’s Office is able to focus its resources on cases of a greater magnitude, resulting in the agency finding more violations per investigation and more wages owed to workers in its history. Under Su, the agency was able to identify many more violations, increasing the ratio of violations to investigations from 49 percent in 2010 to 150 percent in fiscal year 2017–2018, and wages assessed per inspection rose from $1,402 to $28,296 over the same time period. As the Labor Commissioner’s Office noted, “better targeting leads [to] fewer law-abiding employers to be inspected, more unpaid wages to be found, and more citations to be issued per employer.”41

Federal policy recommendations to strengthen strategic enforcement and co-enforcement of labor standards

Given what we know about the impact of the recession on violation rates, the transition to strategic enforcement and co-enforcement is imperative at all levels of government. Maintaining agency budgets to fund strategic enforcement and co-enforcement at all levels of government is a good investment of scarce resources that will better protect the rights of workers and maintain a level playing field for compliant employers.

There are a number of legislative changes, which are more fully outlined here, that should be adopted at the federal level to empower the U.S. Department of Labor’s Wage and Hour Division to implement a robust strategic enforcement and co-enforcement program.42 These include key amendments to the Fair Labor Standards Act to create a number of important strategic enforcement tools, many of which have already been passed at the state and local levels. And they include the creation of a grant program to fund partnerships with organizations that have deep connections to vulnerable, low-wage workers and/or expertise in high-violation industries to facilitate co-enforcement.43

Finally, funding for the federal Wage and Hour Division must be appropriated such that the agency has sufficient staff to protect U.S. workers and compliant employers. As of May 2020, the division employed approximately one investigator per 183,568 workers, a critically insufficient investigator-to-worker ratio. The International Labour Organization has estimated a reasonable benchmark is one investigator for every 10,000 workers, a standard that calls for approximately 14,300 investigators in the United States.44

That’s why, at the very least, funding should be appropriated at a level equal to that requested for FY 2016, wherein the division proposed funding for 2,044 full-time staff.45 These additional enforcement resources should be focused on industries hardest hit by the pandemic and where data indicate violations are high and workers are especially vulnerable, with the goal of achieving ongoing, industrywide compliance.46

Conclusion

The U.S. labor market today is characterized by growing income inequality, pay stagnation, declines in union participation, and deregulation such that the balance of power largely favors employers at the expense of workers. The coronavirus pandemic in particular threatens to exacerbate this power imbalance and undo the progress made in cities, counties, and states that have raised the minimum wage and passed other innovative worker protection laws.

Policymakers should work to maintain hard-fought state and local gains and consider passing additional federal worker protections. In these efforts, they must prioritize legislation that empowers agencies to engage in enforcement strategies as sophisticated as the industries and companies they are meant to monitor, proactively target those sectors where vulnerable workers are experiencing high rates of violations, implement robust retaliation protections, partner with organizations these workers trust, and impose damages and penalties high enough to compel compliance.

—Janice Fine is a professor of labor studies and employment relations at the Rutgers School of Management and Labor Relations and director of research and strategy at the university’s Center for Innovation in Worker Organization, or CIWO. Daniel J. Galvin is an associate professor of political science and faculty fellow at the Institute for Policy Research at Northwestern University and a CIWO fellow. Jenn Round is a senior fellow with CIWO’s labor standards enforcement program. Hana Shepherd is an assistant professor of sociology at Rutgers University-New Brunswick.

This essay is part ofBoosting Wages for U.S. Workers in the New Economy, a compilation of 10 essays from leading economic thinkers who explore alternative policies for boosting wages and living standards, rooted in different structures that contribute to stagnant and unequal wages. The authors in the new book demonstrate that efforts to improve workers’ access to good jobs do not need to be limited to traditional labor policy. Policies relating to macroeconomics, to social services, and to market concentration also have direct relevance to wage levels and inequality, and can be useful tools for addressing them.

To read more about Boosting Wages for U.S. Workers in the New Economy 20 and download the full collection of essays, click here.

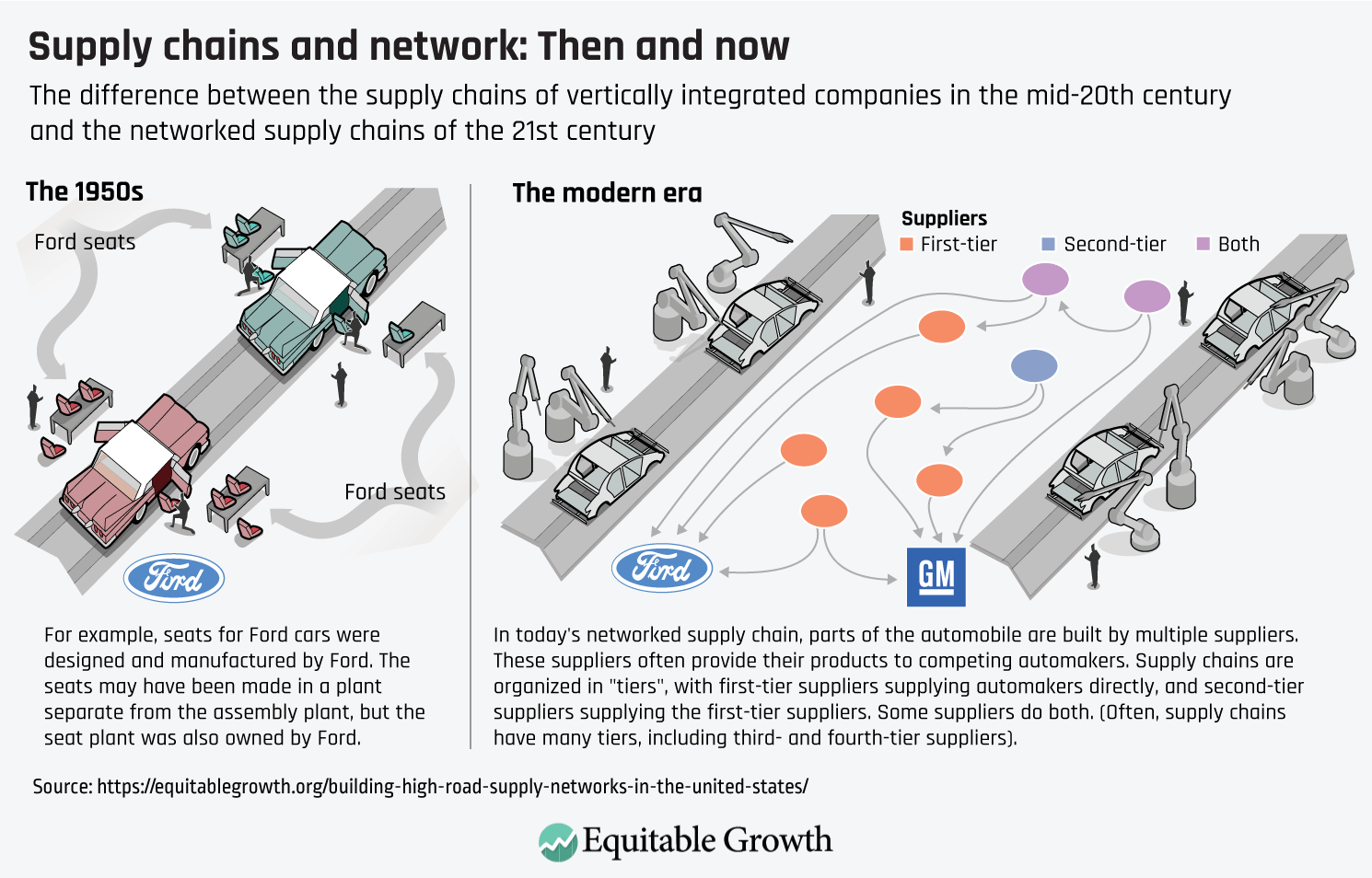

The two vignettes that open my essay illustrate the serious job-quality issues faced by U.S. workers and small businesses due to supply chain challenges. These challenges are due to the current structure of supply chains that reduce the bargaining power of workers and small businesses alike.

“After paying about $1,500 for home office equipment: a computer, two headsets, and a phone line dedicated to Arise; after paying Arise to run a check on her background; after passing Arise’s voice-assessment test and signing Arise’s nondisclosure form; after paying for and passing Arise’s introductory training, to which she devoted 3 days, unpaid; after paying for and passing a certification course to provide customer service for Arise client AT&T, to which she devoted 44 unpaid days; after then being informed she had to get more training yet—an additional 10 days, for which she was told she would be paid but wasn’t; and then, after finally getting a chance to sign up for hours and do work for which she would be paid (except for her time spent waiting for technical support, or researching customer issues, or huddling with supervisors), Tami Pendergraft spent 3 weeks fielding telephone calls from AT&T customers, after which she received a single paycheck. For $96.12.”47

The owner of a small rubber manufacturing plant in Cleveland explained to me (prior to the coronavirus recession) the consequences of his current low-wage policy. He paid his workers about $12 per hour, resulting in frequent absenteeism, the inability to fire inattentive workers because of lack of replacements, and late fees owed to his customers. Yet even with generous assumptions about the impact of higher wages on his workers’ efficiency, he makes a convincing case that raising wages by itself wouldn’t pay off. To fill his last 10 positions, he explained, he would need to raise wages for all 60 workers, including those who haven’t complained about pay so far. To fix his problems, he believed, he would need to invest in newer, more automated equipment, and pay enough (more than $20 per hour) to attract workers who could and would tend several machines. But such equipment costs millions of dollars, and if he takes out large loans to buy this equipment quickly, then it might lead to the loss of his house. He also would have to redesign many of his products to be compatible with the new equipment. He doubts that his customers would pay more, even if quality and delivery improve. And he’s locked in competition with other low-wage manufacturers, many of them abroad; his current operations are optimized for the purchasing environment he faces. He thinks he can probably survive until retirement by slowly shrinking as his equipment wears out.48

Overview

Decisions about how firms structure their supply chains matter greatly for working Americans, yet this topic rarely takes a front seat in discussions of policies to address income inequality. The customer service agent, the factory owner, and his workers in the vignettes above suffer significantly because of supply chain dysfunction.

Firms have restructured their supply chains significantly in recent decades. They have outsourced many activities previously done in-house by full-time employees to a complex web of outside firms. These outside suppliers manufacture components and provide services such as logistics, cleaning, and information technology.

Some of this restructuring contributes to innovation. As final products become more complex, it makes sense for large firms to purchase key components from firms that specialize in that technology or process.49 Supply networks based on product specialization do not necessarily reduce wages and could have the opposite effect.

But in other cases, firms outsource so as to offload production onto firms with weak bargaining power. These supplier firms have little ability to compete except by aggressively holding down wages. Aided by rampant worker misclassification, the erosion of workers’ bargaining power, and periods of weak regulatory enforcement, these forces further erode the quality of jobs for these downstream workers. This “fissured”50 or “low-road” model weakens innovation and suppresses wages, contributing to the erosion of U.S. workers’ standard of living.51

This essay explains how the structure of supply chains affects wages—in particular, why current models of outsourcing and offshoring manufacturing and services operations often lead to worse jobs. I propose policies to make supply chains fairer and argue that these better, “high-road” supply chains also serve other social goals, especially innovation. Specifically, I propose:

Improving bargaining power for all workers

Increasing the capability of small suppliers to innovate and provide good jobs

Redesigning supply chains to promote collaboration among firms, using both carrots and sticks

Creating a new federal institute to develop and diffuse management practices needed for high-road supply chains because the worker-power policies mentioned above may outlaw many techniques that firms have used to compete, such as low pay and union avoidance

Enabling the federal government to promote high-road supply chains through its purchasing power

Strengthening productive ecosystems

To the extent that workers are caught in supply chains with cutthroat competition, policies that attempt to upskill individual workers or contractors without changing the incentives of lead firms will not raise their wages. Thus, policies to reform supply chains will make other pro-worker policies more effective.

Supply chains defined

A supply chain is a network of firms involved in designing, producing inputs for, assembling, and distributing a good or service. (See Figure 1.)

Figure 1

Overall, 43 percent of U.S. workers are in supply chain industries, employed either at lead firms or their suppliers.52 Domestic U.S. firms purchase intermediate inputs equal to about 50 percent of their overall output, while intermediate inputs comprise 75 percent of the output of U.S.-based multinationals. Because of deregulation, market failures, and corporate policies, the providers of these intermediate goods are often small, weak firms that compete by cutting corners on existing products and processes, and thus innovate less and pay less.53

The customer service agent in the opening vignette is considered an independent contractor. Even though lead firms (such as AT&T Inc. or Walt Disney Co.) demand investments and methods of work that are specific to them, these firms bear no legal responsibility under current (inadequate) law to provide her with work hours or to pay for benefits. In a previous decade, she might have been a direct employee of one of these firms, with stable hours and pay that reflected the handsome profits earned by the lead firm. The factory owner in the opening vignette would like to provide defect-free products to his customers and a living wage to his employees, but can’t find a way to fund the transformation required, given the terms of competition imposed by his customers and allowed by current law.

Low-road outsourcing is found in services such as payroll, janitorial work, and security, and now includes “employment activities that could be regarded as core to the company: housekeeping in hotels; cooking in restaurants; loading and unloading in retail distribution centers; even basic legal research in law firms.”54 (See Figure 2.)

Figure 2

Some outsourcing contributes to innovation. As final products have become more complex, it makes sense for large firms to purchase key components from firms that specialize in that technology or process.55 Supply networks based on product specialization do not necessarily reduce wages and could have the opposite effect.

High-road supply chains are possible. Dana Corporation, for example, is a $9 billion supplier of propulsion systems for both conventional and electric vehicles. They have long supplied multiple automakers based on their innovative capabilities. The company provides a complete electric propulsion system, reducing barriers to entry into the electric vehicle market. Many Dana production workers are unionized, earning $16 to $25 per hour, plus benefits.56 These highly skilled workers were able to pivot quickly toward using 3-D printers to make face shields during the coronavirus pandemic.57

The impact of supply chains on U.S. employment

The outsourcing of work takes several forms, leading to a variety of types of workers in supply chains, sometimes working side by side. In many U.S. companies today, there are:

Regular employees of lead firms

Independent contractors working for other companies

Independent contractors who are self-employed

Subcontractors, including:

At lead firm’s site

At another site

These employees may be full time, part time, or temporary (except those in the first category).

These forms of outsourcing of employment, especially as carried out in the United States, typically create undesirable outcomes for most of these workers. Compared to regular employees in lead firms, workers in other forms of employment experience worse outcomes in areas such as wages, benefits, job security, and safety.58

Research by Nathan Wilmers at the Massachusetts Institute of Technology’s Sloan School of Management, for example, finds that firms that sell to a small number of buyers pay lower wages than do similar firms with more customers; this greater dependence on large buyers lowers suppliers’ wages and accounts for 10 percent of wage stagnation in nonfinancial firms since the 1970s.59 It is important to note that most of the workers in Wilmers’ study are full-time, regular workers with all the rights and privileges that comes with that employment. Yet because they work in firms with less market power, they earn less.

Why are outsourced jobs generally worse for most workers?60 Research suggests several reasons:

Rent-sharing. Outsourced workers don’t benefit from norms of fairness that limit wage differentials within firms and encourage rent-sharing.61 It is also easier to fire a supplier than an internal division, due to social ties, complex flows of information, and funds. Thus, wages may creep up at an internal division, leading to cost increases that would lead to an outside firm losing business.

Design for supplier interchangeability. Many lead firms structure their supply chains to make contractors easily replaceable. For instance, U.S. automakers in the past brought product design and complex subassemblies in-house, making it possible to have contractors compete on simple tasks like making a small, pre-designed component. This strategy lowered barriers to entry to being a supplier, meaning that suppliers did not capture many rents.62 This has led to many lead firms in the apparel industry employing long chains of anonymous subcontractors; Walmart Corp., for example, professed to be surprised when goods marked with its label were found in the aftermath of the horrific Rana Plaza fire in Bangladesh.63

Monitoring without accountability. Other lead firms minutely specify the actions to be taken by workers in their supply chains, even those who are not their employees. That is, lead firms can control workers without taking responsibility for paying them benefits. Tight monitoring from lead firms means one of the few profit-making strategies available to subcontractors is to keep wages low.64 In much gig work, contractors have no pricing power; they must accept the price given to them in the app. In addition, workers for Uber Technologies Inc. and Lyft Inc. are tracked continuously by the two firms using GPS, rating workers based on their speed, harshness of braking, and the efficiency of their routes.65

Low supplier capability. As a result of lead firms’ strategies that maximize their replaceability and control their work methods, subcontractors’ ability to create or capture value is low. Innovation is often not feasible, since it typically requires collaboration and organizational slack. Even though investments might yield productivity improvements, contractors often don’t make them because they lack the capability to do so or would not capture much of the benefit due to fierce competition. As a result, subcontractors often cannot increase pay without risking bankruptcy.66

Weak ecosystems. Not only do U.S. suppliers lack support from lead firms, they are “home alone” in other ways as well.67 The reason: There are few institutions to help with innovation, training, or finance. 68 In contrast, Germany’s Mittelstand (medium-sized firms) are the backbone of the German manufacturing sector due to the help they get from community banks, applied research institutes, training institutions, and unions.69

Policy recommendations for fair, innovative supply chains

A different kind of outsourcing is possible: high-road supply networks that benefit firms, workers, and consumers alike.70 Under this model, there is greater collaboration between management and workers, and along the length of the supply chain, there is sharing of skills and ideas, new and innovative processes, and, ultimately, better products that can deliver higher profits to firms and higher wages to workers.71

Getting to this better outcome, however, requires overcoming both market and network failures. Understanding the rationale for existing practice is key to designing good policies. Below, I propose policies that aim to directly address each of the reasons that outsourcing increases wage inequality. The first two sets of policy recommendations support workers and firms, respectively, more or less in isolation. The last three sets of recommendations improve job quality by redesigning the structure of supply relationships in which workers and firms are embedded.

Reduce bargaining power differences between lead firms and outsourced workers by improving bargaining power for all workers

The pro-labor policies discussed throughout this book would make it easier for workers to choose unions, raise the minimum wage, and provide universal access to healthcare and retirement savings. These policies would promote high-road supply chains, while discouraging low-road strategies.72

Increase the capability of small firms for quality and innovation

One consequence of the low-road supply chain practices prevalent among many lead firms is that it hinders the development of innovative capabilities among their suppliers. Government can help upgrade these suppliers’ capabilities. For example, it can:

Provide technical assistance, subsidize, and directly engage in efforts to upgrade firms. In manufacturing, for exampe, the Manufacturing Extension Partnership, a state-federal program, has provided technical assistance to small firms since 1989. The program, at its current size, is very effective, with surveys suggesting that $1 of federal investment in the program leads to a $12 increase in economic activity. The Manufacturing Extension Partnership should be expanded significantly and given tools to work with supply chains as a whole, rather than firms one by one.

Develop and diffuse high-road management practices. Management practices within firms are a key determinant of productivity differentials. 73 The management of suppliers by lead firms affects their productivity and innovation.74 Much researchdocuments the ways that firms can utilize high-road policies or good-jobs strategies to tap the knowledge of all their workers to create innovative products and processes.75

High-road firms remain in business while paying higher wages than their competitors because their highly skilled workers help these firms achieve high rates of innovation, quality, and fast response to unexpected situations. The resulting high productivity allows these firms to pay high wages while still making profits that are acceptable to the firms’ owners.

Diffusing new management practices is hard and risky, but these practices deliver social, as well as private, benefits.76 That’s why the government should fund the development and implementation of high-road management practice either through a consortium of universities or via a pilot project focused on manufacturing that could be established in the Manufacturing USA network.

Such an institute dedicated to managing a sustainable manufacturing ecosystem could collaborate with the Manufacturing Extension Partnership. The institute could develop and diffuse methods for managing high-road labor practices, establishing collaborative supplier relationships, and developing worker capabilities to participate in discussions of innovation. Such an institute or consortium would be particularly valuable in helping small firms adjust to the worker power policies mentioned above, which would make less effective (and possibly illegal) many of the low-road techniques that firms have used to compete, such as low pay and union avoidance.

Responding to these new rules would require not just changes in labor practices, but also changes in marketing, product development, and information technology to take advantage of the higher-skilled (but also higher-cost) labor entailed by the new policies.77

Redesign supply chains to promote collaboration and partnership among firms

Two problems with adopting solely the policies above is that firms embedded in low-road supply chains will have trouble finding capital to invest in innovation, and that these policies do little to promote information exchange among firms. Thus, it makes sense to redesign supply chains to allow for this greater investment and interchange.

Simply expanding the Manufacturing Extension Partnership alone is unlikely to lead to dramatic effects on job quality. The program already spends a great deal of time marketing its services, and its average project size is less than $15,000—not nearly enough to make the interlocking changes in product development, information technology, marketing, job design, and labor relations that are needed for a firm to move to the high road.

Making such a transition comes with significant risk. Firms need to invest in new equipment and training, and then live with expensive downtime as kinks are worked out of the new systems. The factory owner in the opening vignette could afford to hire the Manufacturing Extension Partnership to help with small projects, but can’t afford the high-road transformation described above. He’s locked in competition with other low-wage manufacturers (many of which are abroad), his current operations are optimized for the purchasing environment he faces, and he doesn’t think his customers would pay more for higher-quality products or reliable delivery.78

The federal government can promote supply-chain redesign in two main ways:

Encourage lead firms to build high-road supply chains. Low-road outsourcing strategies are costly to lead firms. These strategies slow innovation in auto manufacturing, for example.79 And they increase the frequency of infections in hospitals.80

In contrast, collaboration among firms along a supply chain can lead to greater productivity and innovation.81 By breaking down the usual silos within and between firms, lead firms can ensure that workers along the supply chain are exposed to ideas and training, to the ultimate benefit of all.

Collaborative relations could offset some of the stratification effects of outsourcing. Suppliers that collaborate with customers may be less interchangeable; workers at such suppliers may be more skilled and able to capture some of the supplier’s rents.82

One reason that firms don’t adopt high-road supply chain strategies is due to the slow diffusion of new management techniques. A new high-road supply chain initiative led by a new management institute or consortium should teach (and further develop) methods to help firms maximize the total value contribution of their suppliers rather than relying on price per-unit alone.83

That’s why the federal government should build on the work of the Obama administration in convening lead firms for a Supply Chain Innovation Initiative, which can drive innovative solutions while complementing a strong regulatory approach.84

Even with greater awareness, lead firms are unlikely to capture all the gains to high-road purchasing policies; the benefits of higher wages, for example, spill over to society as a whole.85 Thus, there remains a significant role for government in promoting high-road supply chains in its capacity both as a purchaser and as a regulator.

Act as a high-road purchaser.The federal government can buy preferentially from companies that use high-road practices. It can require its suppliers to pay prevailing wages, as is required in government-funded construction by the Davis-Bacon Act—a requirement that helps support the apprenticeships and training centers mentioned above. The Obama “Fair Pay and Safe Workplaces” executive order (which has since been overturned) blocked government purchases from companies if they or their suppliers had recent violations of labor laws.

Firms that receive government contracts should pay at least a living wage to their workers and subcontractors. In addition, government should allow prime contractors to count in their bids only 90 percent of the costs of small business subcontractors, as long as the forgiven costs went to investments in wages, training, or equipment. This would enable the government to invest more in contractors who invest more in their people.

The federal government also could offer technical assistance to its own and others’ suppliers by expanding the Manufacturing Extension Partnership and the U.S. Department of Energy’s Industrial Assessment Centers, which helps firms redesign their operation to conserve energy. Combining Buy America requirements with the Manufacturing Extension Partnership has proven effective. The Obama administration’s Department of Transportation enacted rules requiring that any time a federal contractor requested a waiver based on a claim that something can’t be made in America, it was published on a website for potential bidders and relevant stakeholders to see. The department contracted with the Manufacturing Extension Partnership’s supplier scouting service to identify firms that had the capability to fill these procurement needs.86

Government should use its purchasing power to incentivize lead firms to adopt high-road supply chains. Government purchasing policies should include carrots, such as the convening and funding of joint networking, roadmapping, and training efforts.87 But sticks are necessary, too, such as the enforcement of existing legal provisions that allow inspectors to confiscate “hot goods” at lead firms made by suppliers in violation of labor laws.88

The government should require firms that wish to exercise detailed control over workers to be accountable for those workers in order to end abuses such as those experienced by the customer service agent in the opening vignette. The new administration should put in place efforts to fight such misclassification of workers as independent contractors and to treat the lead firms that, in practice, direct the work as joint employers.

The new administration also should establish a commission to discover and end hidden incentives for firms to offshore their manufacturing and services operations. The new commission could recommend, for example, that the U.S. Food and Drug Administration should do unannounced inspections of offshore pharmaceutical manufacturing facilities as they already do for U.S.-based facilities.89

Finally, Congress should commission the National Academies of Sciences, Engineering, and Medicine to study the collection of data on supply chains. A potential model is the U.S. Chambers of Commerce’s work with the U.S. Census Bureau to create a standard for learning and employment records that employers can use to keep track of employee information.90 Once this is done, firms can easily opt in to having certain fields within this information automatically uploaded to secure servers at statistical agencies.

Participation in such an effort could be made a condition of receiving government contracts or other government funds greater than a certain threshold, since such data would be needed to determine compliance with proposed requirements for government prime contractors and their subcontractors to provide “good jobs.”

Strengthen productive ecosystems

For reasons of both equity and efficiency, workers and small business should not depend solely on lead firms for strategic support. In the United States, the unionized construction sector has developed structures that create good jobs and fast diffusion of new techniques even though the industry remains characterized by small firms and work that is often intermittent.

Training is a way that workers can build their skills and thus potentially increase their wages. Building-trades unions work with signatory employers to provide apprenticeships, continuing-education programs, and portable benefits.91 Other unions have begun similar efforts to create career ladders for workers in the hotel and hospital sectors.92 A century ago, the federal government created an innovative farming sector by funding land grant universities, which led not only to the creation of knowledge but also to the creation of durable networks of researchers and practitioners through which such knowledge could quickly spread.93

Sectoral partnerships that include employers, unions, and community colleges have shown promise in providing stable, family-supporting jobs.94

Conclusion

This essay applies a supply-chain lens to the problem of income inequality. Some of the solutions proposed are fairly standard, such as various methods of paving the high road while blocking the low road. Others are more novel, including creating an institute to develop and diffuse management practices needed for high-road supply chains, directing the federal government to become a high-road purchaser and convenor of lead firms, and helping firms to collect better data on supply chains.

In closing, I note two key features of these proposals. First, complementary policies are needed to promote high-road supply chains. It is ineffective to simply attempt to enforce minimum wage laws when firms can go bankrupt and easily re-enter the market under a different name. Instead, long-term progress requires working with both suppliers and their buyers, using carrots (technical assistance) and sticks (“hot goods” enforcement) to transform production and purchasing practices toward a more productive model.95

Another example is that network failures make Buy America alone impractical.96 Over the past 20 years, the answer in U.S. manufacturing has often been to turn to China because firms are frequently unaware of suppliers nearby who could meet their needs. The combination of supplier scouting and Buy America discussed above is more powerful than either policy alone in bringing good jobs back.

Second, policies aimed at creating high-road supply chains will make other policies more effective at reducing inequality. Training, for example, may well not lead to increased wages if workers are employed by low-road suppliers. Suppliers may be unable to reorganize to productively use the new skills, and gains from improved performance may instead accrue to a monopsonistic lead firm.

If policies such as those suggested above are enacted, then lead firms are likely to reduce outsourcing for the purpose of maximizing their bargaining power, and move both to bring work back in-house and to engage with high-road suppliers for their unique capabilities.

— Susan Helper is the Carlton professor of economics at the Weatherhead School of Management at Case Western Reserve University, and a visiting scholar at the Massachusetts Institute of Technology. She was formerly chief economist at the U.S. Department of Commerce.

This essay is part ofBoosting Wages for U.S. Workers in the New Economy, a compilation of 10 essays from leading economic thinkers who explore alternative policies for boosting wages and living standards, rooted in different structures that contribute to stagnant and unequal wages. The authors in the new book demonstrate that efforts to improve workers’ access to good jobs do not need to be limited to traditional labor policy. Policies relating to macroeconomics, to social services, and to market concentration also have direct relevance to wage levels and inequality, and can be useful tools for addressing them.

To read more about Boosting Wages for U.S. Workers in the New Economy 20 and download the full collection of essays, click here.

Overview

In many local labor markets across the United States, only a handful of employers compete for workers’ services. In these markets, employers can take advantage of their market power to underpay workers. Stronger antitrust enforcement can increase competition across all U.S. labor markets, thereby raising wages.

When labor markets are not competitive, two other well-known policy tools can also play a new role—unions and minimum wages. Increasing workers’ bargaining power by strengthening unions can counteract the effects of employers’ market power and increase wages. Similarly, a moderate increase in the federal minimum wage would lift workers’ pay without decreasing employment opportunities or existing jobs. An increase in the minimum wage can even create jobs in those parts of the country where there is little competition among employers.

In this essay, I will detail why so many workers are underpaid due to lack of competition for their labor among employers and how such labor market “monopsony” (the term for a monopoly in the labor market) suppresses wages. I will conclude with specific antitrust and labor market policy solutions to lift workers’ wages and incomes to create a more equitable U.S. labor market that contributes to stronger economic growth.

The problem: Workers are underpaid due to lack of competition among employers

Interest in policies that can boost wages is growing today because wage growth since 1980 has been very limited.97 Anemic wage growth is disconcerting because there have been steady productivity increases over the same period.98 To address this issue, a classic prescription from economics is to raise workers’ skills by increasing education. The thinking goes like this: If skills increase, then wages go up because workers are paid in proportion to their productivity. The fundamental assumption of standard economics is that wages exactly reflect workers’ productivity—their contribution to employers’ bottom lines.

This assumption is sensible if labor markets are perfectly competitive and there are no frictions in the way of workers finding good jobs that value their skills. If an employer underpays a worker, then that worker can credibly threaten to immediately quit for another job. Therefore, in such a perfectly competitive, frictionless labor market, employers cannot afford to underpay workers if they want to keep them around.

But if labor markets are not perfectly competitive, then education may not be the best tool to raise wages. And in the U.S. labor market, perfect competition is stymied for a number of reasons. One is the lack of competition among employers in many U.S. local labor markets, which makes it hard for workers to shop around for a better wage offer. Another reason is what economists call search frictions: It can be difficult for workers to efficiently search for jobs, for example, because they lack information on jobs far away from their homes. And a third is job differentiation: Jobs differ in many ways, beyond how much they pay. For example, some jobs may be close to a worker’s extended family, helping fulfill child care needs, and some jobs provide good health insurance, which is especially valuable to workers whose spouse has a chronic illness. When a job uniquely fulfills some of the worker’s personal needs, the employer has some leeway to pay the worker less than the value of their contributions.

For all of these reasons, raising workers’ skills may not be enough to significantly boost wages. In the extreme, if there is only one employer in the labor market, an increase in education does not increase workers’ wages at all. This is because workers cannot threaten to take their education elsewhere. Without competition, employers are the only ones to benefit from more education through higher productivity.

In the 1930s, economist Joan Robinson already thought about how employers could suppress wages. She coined the term “monopsony” by analogy to monopoly.99 While a monopoly is a situation where a single firm is supplying a product, monopsony is a situation where a single customer is buying a product. Applied to the labor market, monopsony is a situation where a single employer “buys” workers. This is obviously not perfect competition. While most labor markets have more than one employer, a handful of employers isn’t perfect competition either. More broadly, economists have been referring to labor markets with limited competition among employers as monopsonistic labor markets.

Monopoly in the product market has been widely studied by economists, and it is now well-known that product markets are often not perfectly competitive.100 If so, why should we expect labor markets to be perfectly competitive? Workers typically do not have that many options: Given the specificity of workers’ skills, as well as other relevant considerations such as commuting time, the number of good jobs for a given worker can often be counted on the fingers of one hand.

Monopsony is a real problem leading to less worker power, less labor market competition, and wage suppression. Policies that can address monopsony and its root causes will boost wages.

Monopsony in labor markets suppresses wages

If an employer can retain workers even when they underpay them, this opens the door to wage suppression. The concept of labor supply elasticity, which measures how sensitive, or “elastic,” workers are to wages, explains how much employers can afford to underpay their workers. If the labor supply elasticity is high, then workers are sensitive to wages, so an employer who underpays workers will run into serious recruitment and retention difficulties. Conversely, when the labor supply elasticity is low, workers are not very sensitive to wage changes, and employers can afford to underpay them without enduring high numbers of workers quitting to go to other jobs, alongside expensive and time-consuming efforts to recruit new workers.