Downtown Prattville, Ala. during a period of shelter-in-place orders, mid-April 2020.

Overview

Prior to the current coronavirus recession, most U.S. economic metrics pointed to a slow but steady nationwide recovery amid an 11-year post-Great Recession run of economic growth. But prosperity was not spread equally across the breadth of the nation. In addition to widening income and wealth gaps, new data show that rural communities did not reap widespread benefits compared to urban regions of the country. The reasons for this gap between urban and rural economic growth bear serious policy consideration as the coronavirus pandemic sweeps across the nation.

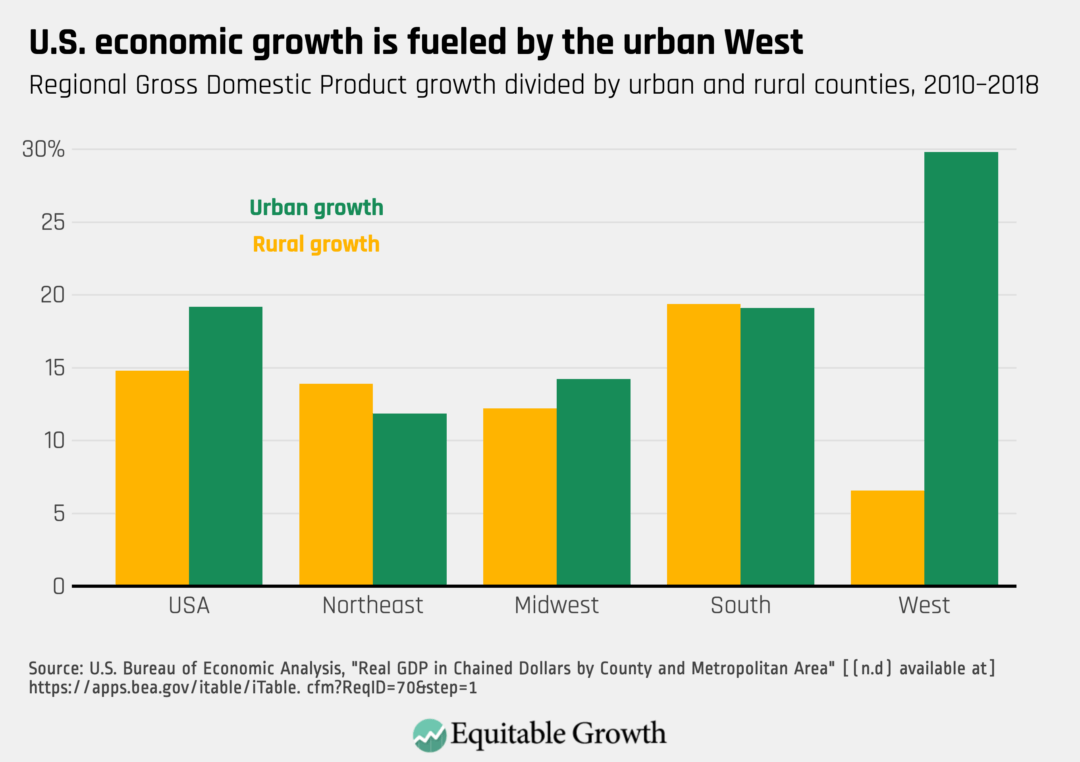

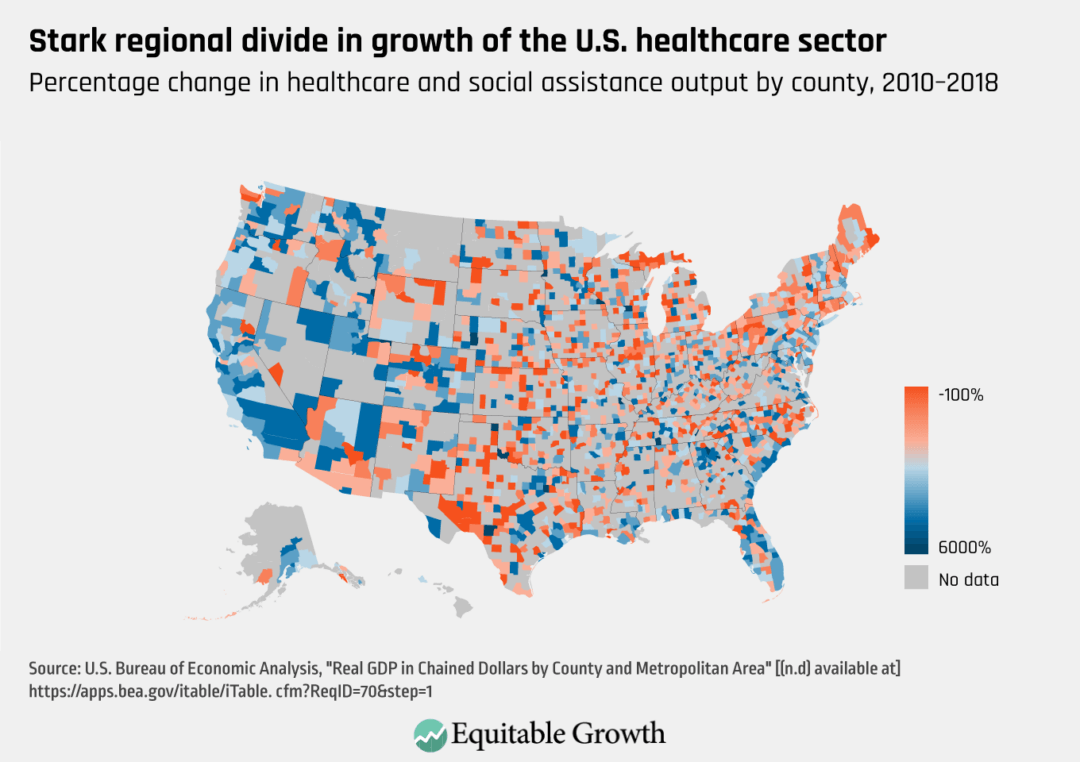

During the 11-year recovery following the Great Recession of 2007–2009, Gross Domestic Product growth in rural America lagged behind urban GDP growth, according to the recently released Local Area GDP measure, which provides annual GDP growth data by county and industry. Rural areas in the aggregate experienced post-recession growth of 14.8 percent while urban areas registered 19.2 percent growth. When the data are broken down regionally, we see that the largest urban-rural divide is in the West, which consists of California, Oregon, Washington state, Alaska, and Hawaii. (See Figure 1.)

Figure 1

Demographic and industry breakdowns

This divide in urban and rural outcomes was driven by changes in demographic and industry composition. Rural and nonmetropolitan areas have a higher share of older people over 65 years of age, 17.5 percent, meaning labor force participation rates will drop as rural communities age. In addition to age, educational attainment contributes to declining labor participation and outcomes because half of prime-age adults (ages 25 to 54) held no more than a high school diploma in rural communities. Decreasing educational attainment brought about an ever-widening labor force participation gap between rural and urban areas.

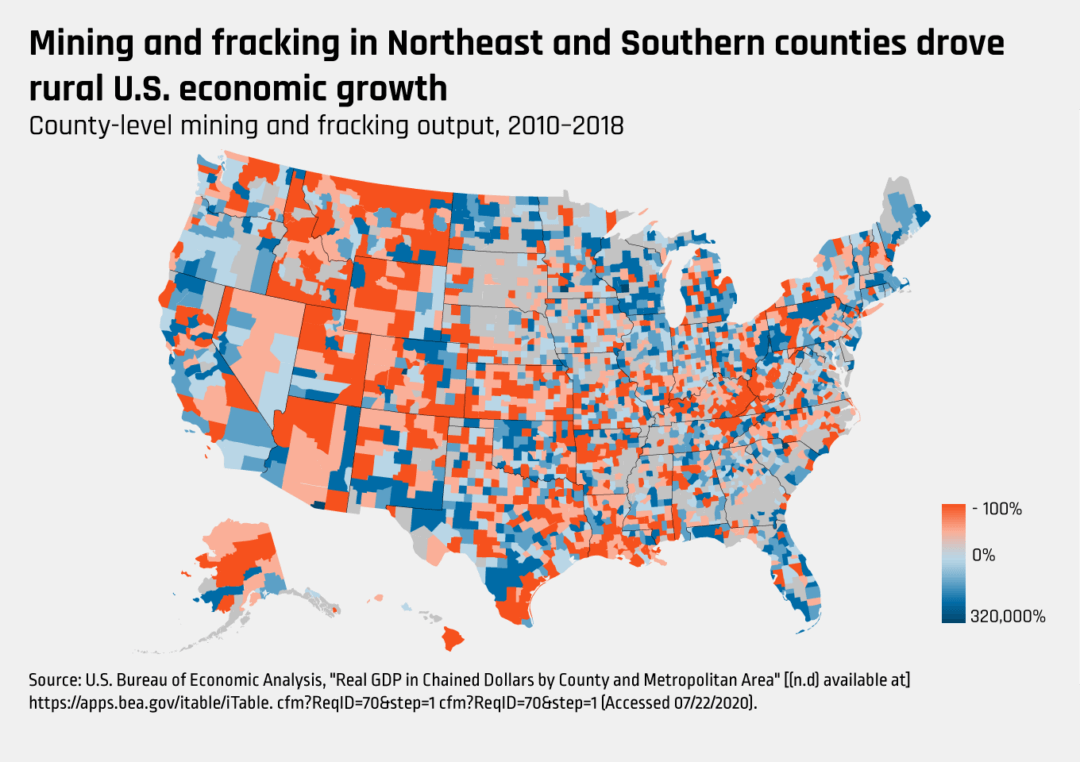

Looking at the regional breakdown of urban and rural growth, it is evident that rural communities rely on specific industries for economic growth and sustainability. Rural counties in some states such as Texas and Oklahoma depended on the mining and fracking industries for long-term growth after the Great Recession. (See Figure 2.)

Figure 2

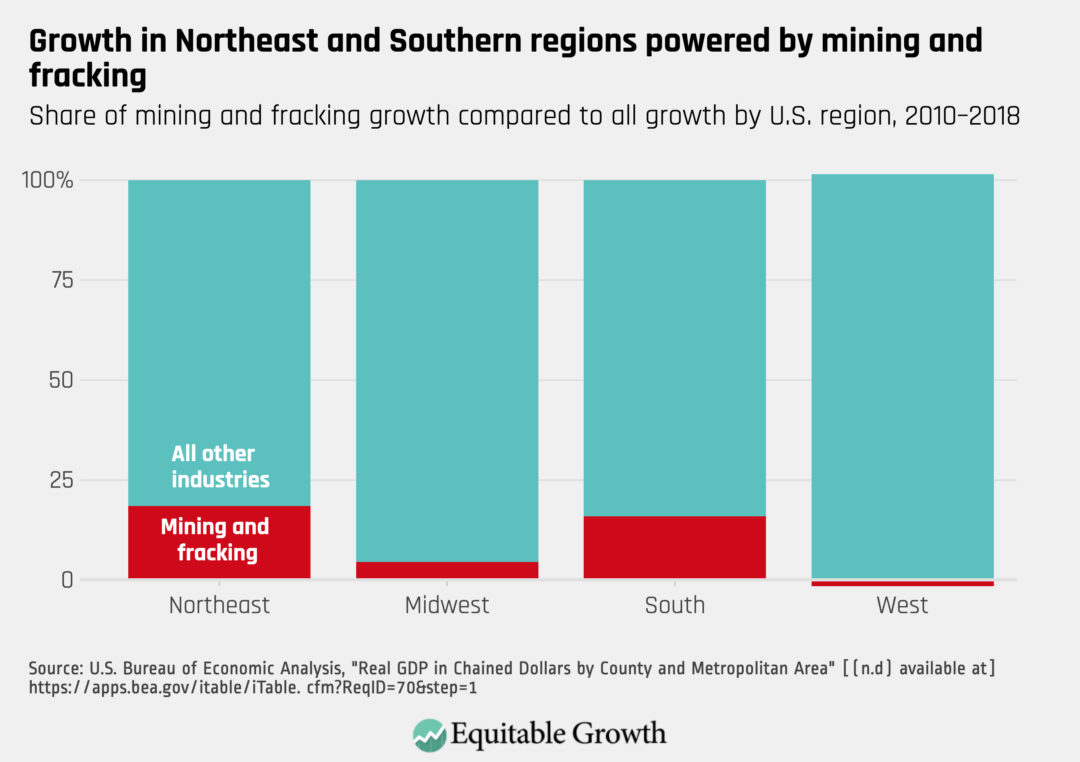

Indeed, Louisiana’s rural counties witnessed a 30 percent decline in post-recession output, yet the entire Southern region’s rural growth was able to counteract this decline partially through mining and fracking output in Texas. As a result, the South, as well as the Northeast, experienced large shares of growth coming out of the mining and fracking sector. (See Figure 3.)

Figure 3

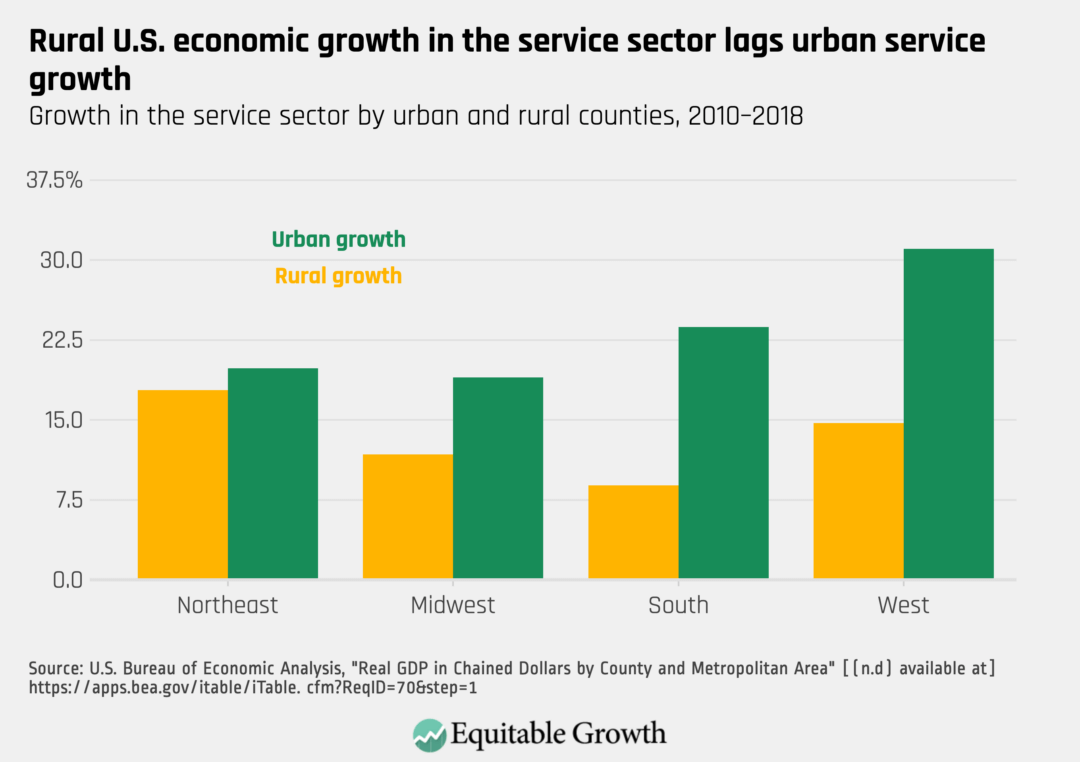

Beyond farming, mining, and fracking, the rural economy relied heavily on the service industry as a form of sustainable employment. In 2016, data from the U.S. Census Bureau’s American Community Survey showed that 22 percent of people living in completely rural counties (counties in which 100 percent of the population live in a rural area) were employed by the educational, healthcare, and social assistance service sector. Another 7.3 percent worked in the arts, food, and accommodations service sector. Yet even though many rural workers depended on services over fracking, mining, and agriculture, the service industry output fell short for these communities during the post-Great Recession run of economic growth.

What’s more, growth in the rural service sector lagged behind similar industries in urban communities. In the South and the West, there was a 14 percentage point and 16 percentage point gap, respectively, in the growth of service output between urban and rural communities. The gaps were smaller in the Midwest and especially in the Northeast. (See Figure 4.)

Figure 4

Rural and urban and regional economic growth gaps in healthcare

Then, there’s the healthcare sector. There are widespread regional and rural-urban divides in economic output in healthcare since the Great Recession. Rural counties in the West and Rocky Mountain states experienced growth in healthcare while rural counties in the South, Midwest, and Northeast registered more contraction in this industry since the previous recession. (See Figure 5.)

Figure 5

One explanation for such geographic divides is the growing trend of healthcare professionals moving away from rural counties toward urban counties, where hospitals are growing rather than closing or consolidating. Since 2010, 130 hospitals in rural communities have closed their doors, predominantly in the South. A study from the Chartis Center for Rural Health estimates that another 453 hospitals out of the remaining 1,800 are vulnerable to closure based on their performance and funding support between 2019 and 2020.

In addition to funding struggles and closures, rural hospitals are often vulnerable to mergers and acquisitions. Between 2007 and 2012, approximately 8 percent of rural hospitals, or 121, were involved in a merger. These hospitals had fewer profit margins, a lower percent of outpatient revenue coming from Medicare, a smaller ratio of full-time-equivalent, or FTE, employees to hospital beds, and higher amounts of debt compared to hospitals not involved in a merger. Researchers found that after the mergers, salaries went down by more than $1,220 per FTE employee, or almost $645,000. Other studies show that rural hospitals that merged with larger hospital systems experienced a decline in services provided, such as diagnostic imaging and outpatient care.

Despite the reduction in services, these rural hospitals showed significantly increased operating margins, which indicates that they aren’t performing at any greater efficiency than before the mergers took place.

The preservation and improvement of rural hospitals is crucial to the growth of the rural economy, particularly amid the current pandemic. Without accessible and good-quality healthcare, rural workers won’t be able to effectively work and promote growth within their local economies. Lack of accessible healthcare in rural counties means people risk losing their jobs in order to travel further distances to seek medical care that they can’t afford, thus exacerbating the social disparities in rural and urban public health outcomes.

Protecting healthcare accessibility doesn’t mean preserving poorly operating hospitals. In order to close the growth gap between rural and urban communities, policymakers should look at ways to strengthen healthcare accessibilities, such as providing public funding for nonprofit rural healthcare or expanding Medicaid in states with higher rural populations.

Reasons for the growth gap between rural and urban economies

Research by Charles S. Gascon and Brian Reinbold of the St. Louis Federal Reserve credits the urban-rural growth gap to agglomeration effects, which are seen when urban cities experience stronger growth because of firms’ access to resources that increase productivity, such as airports, efficient public transportation, and large pools of consumers. Some urban firms do provide services that spill over into rural communities, such as an urban hospital providing telemedicine to rural patients. But this is still output generated by and for urban areas, and so improvements in rural accessibility to resources primarily boosts urban output and growth. Nonetheless, these spillover effects and increased accessibility to cities’ resources improve rural prime-age adults’ employment prospects and optimism.

On the urban side, much of the gap is attributed to a technology boom concentrated in major metropolitan areas such as San Francisco, Boston, Austin, and New York. The rise of the tech industry worked in tandem with the phenomenon known as the rural brain drain. Young and talented individuals raised in rural communities are migrating to metropolitan areas in waves, searching for jobs in new industries and a higher quality of life.

In a study conducted by demographers Ken Johnson at the University of New Hampshire and Richelle Winkler at Michigan Technological University, the data show that large metropolitan areas experienced net population gains while nonmetropolitan areas experienced net population losses of people ages 20 to 34 years old. As a result of the decreased supply of workers, tech industries are failing to establish themselves in rural areas, despite the relatively low cost of living in such areas.

Policy implications

It is imperative that policymakers consider rural communities when discussing economic policy initiatives. Programs that promote urban growth, for example, may have negative effects on the rural economic expansion. Through the use of data, such as the U.S. Bureau of Economic Analysis’s Local Area GDP measure, academics and policymakers alike can track rural industry trends and create policies that promote a stable and resilient rural economy.

Policymakers learned late last week that the U.S. economy registered a stunning 9.4 percent contraction in the second quarter of this year, a drop not experienced since the Great Depression more than eight decades ago. And that extraordinarily bad news came in late July—following weeks of the novel coronavirus becoming “extraordinarily widespread” across most of the country, leading a number of states and municipalities to restrict or re-restrict economic activity to stem the pandemic and rising number of deaths due to COVID-19, the disease caused by the coronavirus. U.S. economists are mildly to extraordinarily concerned that our economy is moving toward further contraction and a possible return to the record unemployment numbers posted this past spring.

In the early days of the coronavirus pandemic in the United States, the Washington Center for Equitable Growth launched a new web page dedicated to policy resources for the coronavirus recession. Nearly every day since, we’ve posted new analysis and policy recommendations backed by evidence-based research on the ways the federal government can help our economy recover and ensure that recovery is broad-based and equitable. Much of this policy work is based on our Vision 2020 project, a resource designed to provide policymakers in Congress and the federal government with detailed policy recommendations on a wide array of issues.

Together, these two resource pages on our website point to workable solutions to the multitude of interconnected economic travails besetting the country. Some of these ideas are immediately relevant to economic growth for the remainder of the year, particularly the need to deal with the spread of the coronavirus itself as the first order of business. Other ideas on these resource pages point to ways policymakers can ensure the recovery from this recession is different from past ones. Here is a list of some of these most relevant posts.

Heather Boushey Washington Center for Equitable Growth Testimony before the Joint Economic Committee, Hearing on “Reducing Uncertainty and Restoring Confidence During the Coronavirus Recession”

July 30, 2020

Thank you, Vice Chair Beyer and Chairman Lee, for inviting me to speak today. It’s an honor to be here.

My name is Heather Boushey, and I am president and CEO of the Washington Center for Equitable Growth. We launched in November 2013 with the goal of advancing evidence-backed ideas and policies in pursuit of strong, stable, and broad-based economic growth. We do this through a unique institutional strategy: We fund academics to investigate whether and how economic inequality—in all its forms—affects economic growth and stability. We have an open and competitive academic grants program that now, in our seventh cycle, has given away about $6.5 million to more than 250 scholars nationwide.

What the research now shows is that there are many ways that inequality hurts both families and the long-term trajectory of our economy. These long-term trends are inimically tied up in the current coronavirus pandemic and resulting recession.

The most important economic uncertainty facing your constituents and our nation is: When will the administration and Congress address the public health crisis caused by the coronavirus pandemic?

Addressing the administration’s failure to contain the coronavirus and COVID-19, the disease caused by the virus, is the only way to fully restore confidence and put us on the path to economic recovery. The United States is experiencing the most uncontrolled and deadly outbreak of any high-income country in the world. Compared to the European Union, we now record 10 times as many daily coronavirus cases and COVID-19 deaths.

Until the virus is contained, however, there are key actions that can bolster economic confidence and rein in uncertainty. Specifically:

Immediately renew the $600 Pandemic Unemployment Compensation payments

Set economic assistance programs, such as Unemployment Insurance, to continue automatically until objective economic conditions improve

Pass generous aid for states and localities, which have already shed 1.5 million jobs and are bearing the brunt of responding to the pandemic, on the order of the $900 billion in the HEROES Act

Resist enacting corporate liability immunity and instead release workplace health standards that protect workers’ lives and give employers evidence-based guidance

Enact other policies to stabilize demand and help those most affected by the crisis, including:

Food assistance

Rental assistance and the extension of the eviction moratorium

Direct payments to a broad swathe of low- and moderate-income Americans

Investments in communities of color hit so hard by the coronavirus

Funding to ensure safe and secure elections in November

Help for small businesses

Premium pay to our essential workers

Fixes to the long-term fragilities detailed below that have made us so susceptible to this shock

Build the data tools to know how this crisis and recovery are affecting families up and down the income ladder by enacting GDP 2.0 measures

The HEROES Act, which was passed by the House more than 2 months ago, contains many of these priorities. The Senate should immediately consider passing this bill or a similar bill that includes a recently introduced bill from Sens. Schumer and Wyden to peg expanded unemployment benefits to the economic conditions in each state. This would allow aid to automatically adjust based on objective criteria. Vice Chair Beyer has authored a similar proposal.

The coronavirus pandemic abruptly ended of the longest economic recovery in U.S. history. But before we get to the current situation, we need to acknowledge that even in those good years, the gains from that economic growth weren’t shared. This created systemic fragilities that left us less economically resilient and set us up for the multiple failures we are now experiencing.

The Roots of this Failure

This immediate failure is the result of a series of decisions made by this administration. But it also is the result of decisions made over the past 50 years that have created underlying fragilities in our economy and society. These decisions have made our economy less effective in good times and less resilient to shocks.

Even as the topline economic markers signaled to policymakers that our economy was growing last year—indicators such as a historically low unemployment rate and annual Gross Domestic Product growth of around 2 percent—wages were not growing commensurate with a tight labor market or at a pace to close our country’s unconscionable longstanding racial income and wealth divides.

The fruits of our economic growth, in terms of both income and wealth, were diverging sharply.

The Federal Reserve Board’s new Distributional Financial Accounts and the latest research by University of California, Berkeley economists Emmanuel Saez and Gabriel Zucman document that income inequality remained historically high, and wealth inequality was outpacing it.

Inequality hurts economic growth and mobility. Growth has slowed since 1980, and average people no longer share in the growth we do have. The bottom 50 percent of the population has the same inflation-adjusted pretax income that they did in 1980, and lower absolute mobility means that people born in 1980 now have only a 50 percent chance of surpassing their parents’ income.

Obstructing the supply of people and ideas into our economy and limiting opportunity for those not already at the top, which slows productivity growth over time

Subverting the institutions that manage the market, making our political system ineffective and our labor markets dysfunctional

Distorting demand through its effects on consumption and investment, which both drags down and destabilizes short- and long-term growth in economic output

As a country, we have put ideology over evidence. We have chosen tax cuts and deregulation over investments such as paid family leave, robust social insurance programs, and public institutions. We have put our faith in the idea that markets can do the work of governing.

Instead, we should put our economy—and society—on a path where growth is strong, stable, and broadly shared. To do that, we need to enact policies that constrain inequality at the top, not allowing it to spiral out of control, and giving the beneficiaries of that inequality the power to subvert our markets, politics, or economy. And we need to provide counterweights to concentrated economic power. As we consider the economy we had at the onset of the pandemic, we can see clearly how failures to ensure workers and families, especially Black, Latinx, and Native American workers and families, have access to the tools to be healthy and safe—policies such as paid sick time, access to affordable healthcare, and well-enforced workplace safety standards—made our nation less resilient to this shock.

There are six key factors that made the United States and the U.S. economy particularly susceptible to the coronavirus pandemic and COVID-19. Each of them have contributed to the current crisis. And if they are not corrected, the United States is likely to experience a slow and inequitable economic recovery.

Too many people lack the basic protections that would have slowed the spread of the coronavirus

The gaps in our social insurance systems exacerbated the spread of the coronavirus. The United States is behind its peer nations in labor market regulations to protect workers and families, including on paid leave, stable schedules, and access to child care. Compounding the problem is the lack of health insurance and fear of high medical bills, both of which kept—and are still keeping—those who feel sick from seeing a doctor, placing a serious burden on these individuals as well as raising rates of transmission.

Research is already showing the significant economic and psychological toll this pandemic is taking on workers. These stresses are heightened for people of color and immigrants, who face institutional discrimination and are often forced by their already precarious economic straits to succumb to workplace abuses at the hands of their employers.

Workers lack the power to share in the gains of the economic expansion that would have given them protections and security

Civic institutions—especially labor unions, which once served as voices for many wage-earning workers (though never representing all workers)—have suffered a long decline. Now, only 1 out of every 16 private-sector workers belongs to a union. On top of this, labor laws and policies have failed to reflect the growing role of the fissured workplace in our modern-day economy, where firms subcontract pieces of their work so they can avoid responsibility for workers and working conditions.

These two debilitating trends in our labor market mean that corporations that are ultimately in charge of labor practices and that make the largest profits are not liable for maintaining 21st century workplace standards. The coronavirus pandemic exposed the failure of these labor market inequalities and the need for workers to manage health crises and family care, as well as protect workers against layoffs and the loss of these key health and family benefits.

Decades of stagnant wages and meager workplace benefits leave many families without enough savings to weather the coronavirus recession

At the onset of the coronavirus pandemic in the United States, millions of people across the country were one paycheck away from financial catastrophe, even after a decade of economic expansion and historically low unemployment. Case in point: Four in 10 adults in the United States said that if they had a $400 emergency expense, they would have to borrow, sell something, or would not be able to pay it.

As the coronavirus recession continues, more and more workers and their families are robbed of buying power, which will undermine one of the key drivers of economic growth—the stable incomes that drive consumer spending.

Policymakers starve public goods of investments that would have enabled better protections from the coronavirus pandemic and ensuing recession

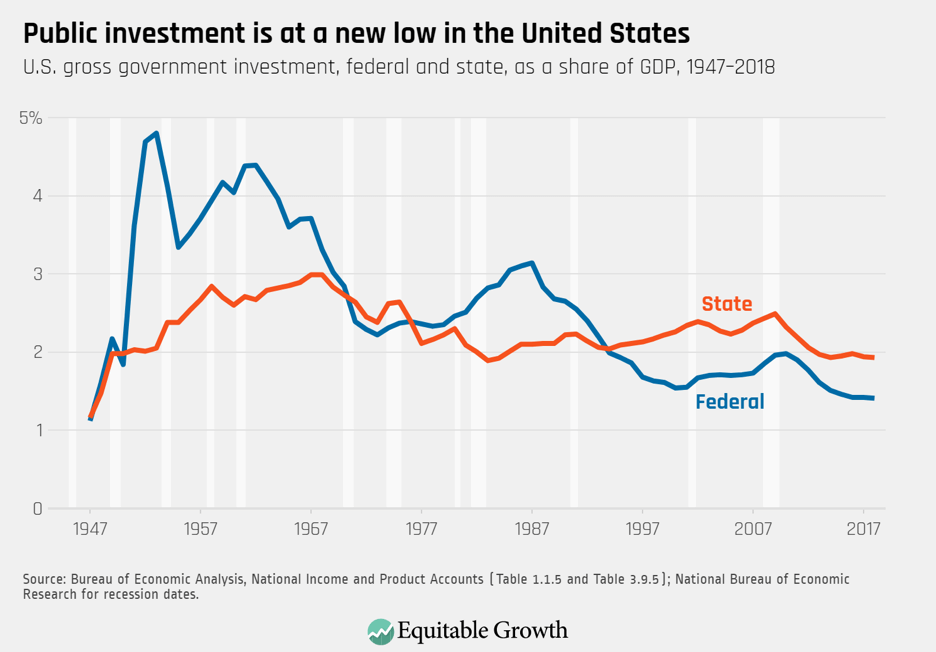

Decades of tax cuts, culminating in the sharply regressive Tax Cuts and Jobs Act of 2017, have fueled a long-term decline in federal revenue that has starved resources that can be used to fund critical public investments and basic governmental functions, including in public health. High concentrations of income and wealth hamstring our political system because the wealthy dictate the legislative agenda and shape news headlines.

Yet these same wealthy elites don’t prioritize investments in public health infrastructure or other public goods. Early in this crisis, our neglected Unemployment Insurance system was unable to handle millions of Americans losing their jobs. Millions have waited weeks or months as decades-old computer systems struggled to process their claims. This dearth of investment is a systemic problem in the United States. (See Figure 1.)

Figure 1

States and localities don’t have the resources to deal with a pandemic or a recession

State and local governments are experiencing sharp drops in their capacity to provide the services needed to cope with the coronavirus recession. Already, state and local governments have shed 1.5 million jobs. A continuing recession will induce further cuts to health and education and exacerbate the ongoing weaknesses. Austerity in state governments likewise disproportionately harms people of color, as public-sector jobs form the basis of a strong middle class for Black and Latinx workers.

Business concentration across markets increases consumer and small business vulnerabilities just when those threats are most dire

Wealthy and powerful corporations use their status to maintain dominance in the marketplace. Large businesses and monopolies muscle competitors out of business, suppress wages, and hobble innovation. These companies are also precisely the ones that will thrive after the coronavirus pandemic passes. Strong cash reserves combined with political influence allow entrenched businesses to swoop in when asset prices are low and reshape rules of entire markets in the aftermath. The collapse of small businesses will disproportionately hurt people of color for whom business ownership is an especially important route to wealth creation and to closing the racial wealth gap.

The failure to prevent coronavirus infections and deaths and the ensuing recession

President Donald Trump’s focus is and always has been on the stock market rather than conceiving of and effectively implementing a comprehensive and fully thought-out federal plan to address the coronavirus pandemic and its economic effects. Case in point: Though the administration knew about the threat of the coronavirus in early January and took an early effort to limit the transmission into the United States by halting travel from China, where the coronavirus first emerged, it did not use that time to prepare sufficient stockpiles of medical and protective supplies.

Despite the months that have passed, the administration also has not set up a nationwide system to contact trace confirmed COVID-19 cases or given states the resources to do it themselves. And tests for the general population still can take a week or more to process and access too often varies by race.

Addressing the Immediate Economic Uncertainty

Unemployment Insurance

The largest economic uncertainty facing the United States is whether the Senate will renew the $600 increase in weekly unemployment benefits, known as Pandemic Unemployment Compensation, or PUC. The Senate majority has refused for months to act to renew this critical lifeline despite dire circumstances in the labor market.

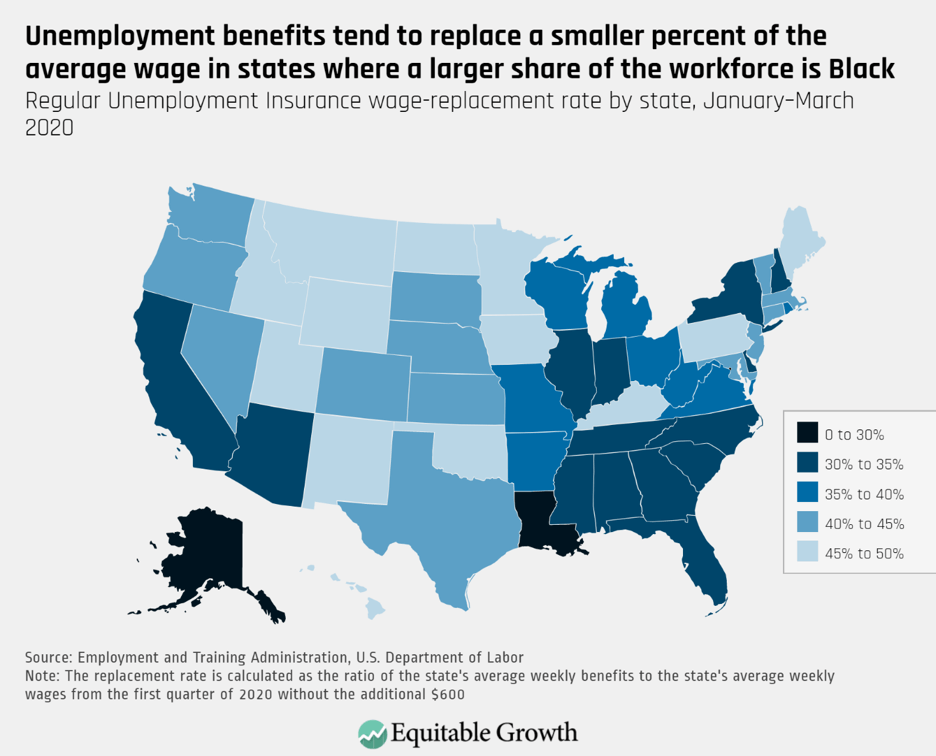

There is a racial component to the Senate’s refusal to renew the $600 PUC benefit. States with a higher share of Black workers tend to have less generous jobless benefits. For Black workers, an estimate shows, the average maximum weekly benefit is $40 short of that received by White workers. (See Figure 2.)

Figure 2

We risk a cascade of economic damage that could be uncontainable if Congress does not act immediately to extend the $600 unemployment benefit boost. Families need this benefit to sustain them. Their landlords need them to pay their rent, and their local small business owners desperately need them to keep ordering take-out and popping by for socially distanced shopping.

Like a virus out of control, high unemployment spreads economic pain throughout the entire community.

Unemployment benefits accounted for 14.6 percent of all wage and salary income in May. Failure to extend the $600 boost alone would contract GDP by a rate of 2.5 percent in the second half of this year, per an analysis by Harvard University’s Jason Furman. As a percentage, that is more than the economy grew in 2019.

Allowing the $600 boost to remain expired would devastate local economies.

Our communities rely on the temporarily unemployed being able to continue spending. States where unemployment benefits replace a greater percent of workers’ wages experienced the smallest drop in work hours in March—and, as of early June, had the strongest recovery.

There have been unfounded concerns that the $600 boost might be a meaningful disincentive to work during this crisis, perversely causing the very economic ailment is it meant to alleviate. This is not the case. The ongoing failure to be able to get back to business-as-usual due to the out-of-control pandemic, the absence of safe working conditions, a sharp drop in consumer spending, and lack of support for parents and caregivers are preventing millions from working, not Unemployment Insurance payments.

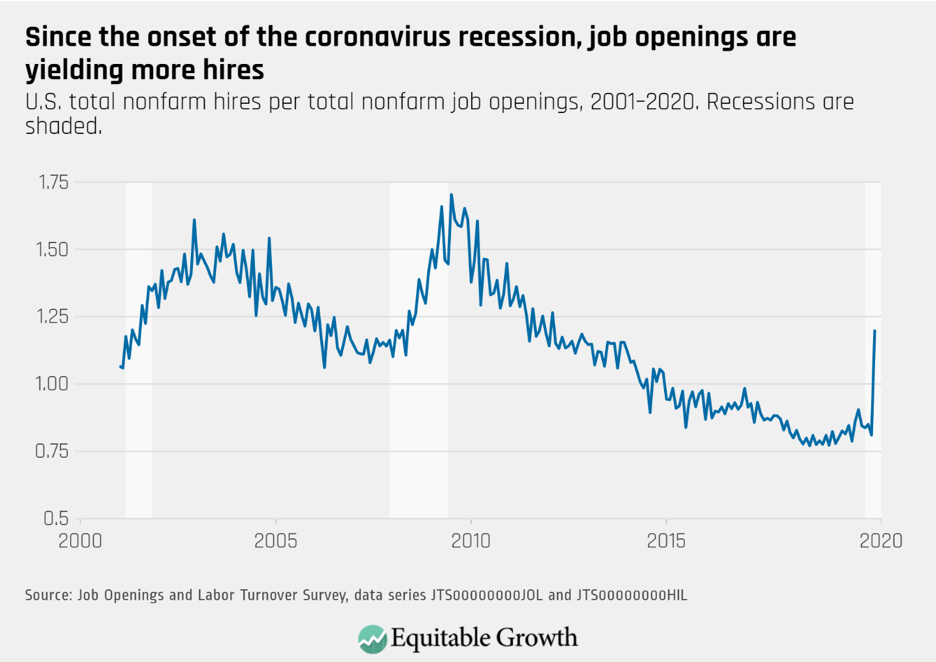

People are eager to get back to work when they have the opportunity, but there are not enough jobs in our labor market. The Job Openings and Labor Turnover survey shows that there were four unemployed people for every job opening in May. Lack of opportunities to work, not a lack of eagerness to work, are keeping unemployment elevated.

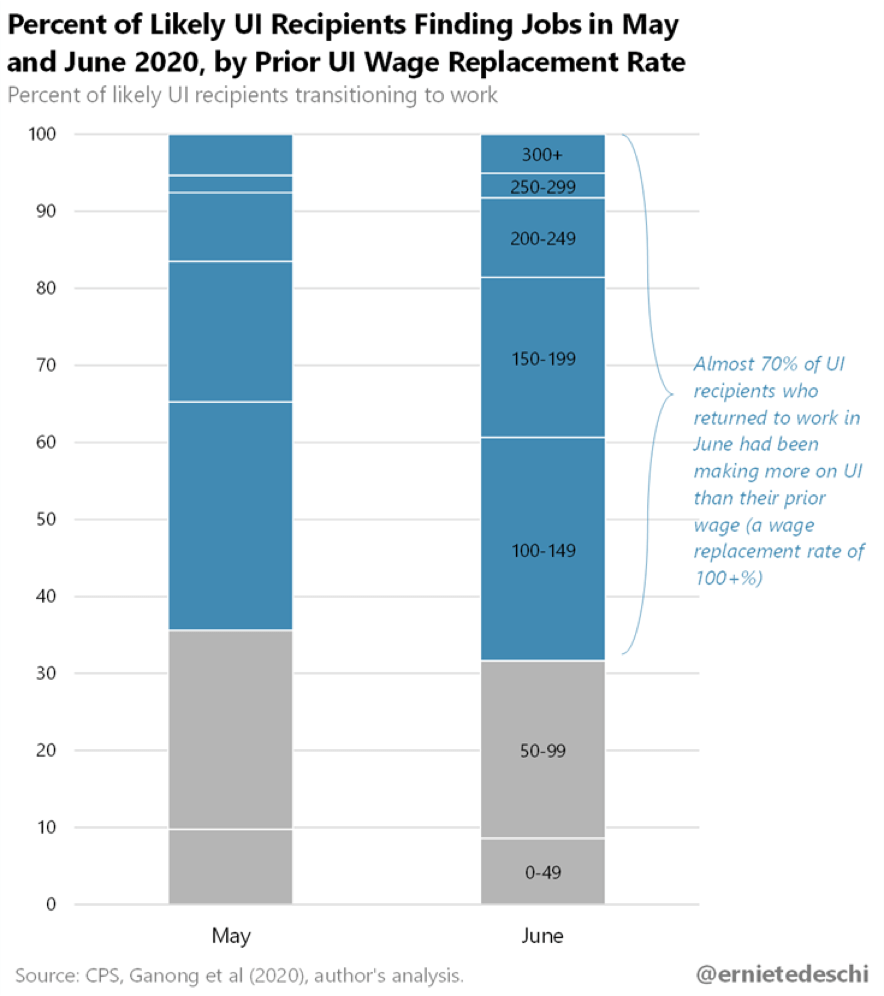

We can also see this in the population of people who returned to work in May and June after being laid off in April. Nearly 70 percent of those who returned to work in May and June did so despite the fact that they were making more from Unemployment Insurance than at their job, according to analysis by Ernie Tedeschi, an economist at Evercore ISI and former Treasury economist. (See Figure 3.)

Figure 3

In short, Americans want to work, and they know that a permanent job is more valuable than a temporary Unemployment Insurance check. This is one reason why employers are filling their scarce open positions faster than at any point since February 2012, as shown in the U.S. job vacancy yield.

Automatic Stabilizers

Nobody knows for sure how long the coronavirus recession will last or exactly how severe it will be. The uncertainty that would exist when confronting any recession is compounded by the uncertainty about the nature and consequences of the coronavirus itself, including the number of people who will die from COVID-19 now and in the future, the short- and long-term health impacts of the virus on those who recover, the pace at which treatments and vaccines will be developed, and the quality of the public health response.

Enhanced unemployment benefits should end when objective conditions show they are no longer needed. An unemployment-rate-based “trigger” that only turns off when a stable recovery is underway would allow this program to wind down automatically.

Sens. Schumer and Wyden have introduced a bill that would extend the $600 increase in weekly UI benefits beyond July 31, 2020 until a state’s 3-month average total unemployment rate falls below 11 percent. The benefit amount then reduces by $100 for every percentage point decrease in the state’s unemployment rate, until the rate falls below 6 percent. Vice Chair Beyer has sponsored a similar bill in the House. These bills follow the best evidence in research-driven policy design, inspired by research on automatic stabilizers from Equitable Growth and the Hamilton Project’s book Recession Ready.

State and Local Government Aid

The next priority, if Congress wants to create economic certainty, is to pass fiscal relief for states and localities with around $900 billion in aid in the HEROES Act.

States and localities are bearing the brunt of responding to this virus in light of federal inaction. They are losing tax revenue and, as a result, have shed 1.5 million jobs so far—even as their services are more necessary than ever. These job losses make up a significant portion of the overall 12 million jobs permanently lost since February.

With state and local general fund revenues in freefall due to needed increases in spending on healthcare and related spending amid plummeting tax revenue, these governments’ budgets are on the precipice. State budget shortfalls could total more than $550 billion over the next 3 years, nearly double what it was estimated states missed out on in the entire decade following the Great Recession more than a decade ago. Fiscal requirements that states balance their budgets are already forcing governors to propose cuts in spending that will harm already struggling communities. Local governments are, if anything, in an even more challenging economic situation.

During the previous recession, these budget cuts proved seriously harmful to the economy. Shrinking state and local government budgets during the Great Recession reduced Gross Domestic Product by more than three times the size of the cuts themselves, according to estimates.

Other Crucial Policies

Other policy priorities include food assistance, rental assistance and extension of the eviction moratorium, investments in communities of color hit hard by the virus, funding to ensure safe and secure elections in November, help for small businesses, and premium pay to our essential workers. And I urge you not to support enhanced liability protections for big corporations facing lawsuits if they put their workers at risk. Federal policymakers need to provide evidence-based guidance so firms open safely, not shift risks onto workers.

Finally, Congress should also implement new data tools to measure how the recession and recovery will affect people differently up and down the income and wealth ladders. The GDP 2.0 measure Equitable Growth has proposed, and which I have previously discussed before this Committee, will tell us whether families are recovering from the crisis and which need more help. We can lay the groundwork now to make sure we understand who benefits from a future recovery and what other action is needed.

We can see clearly that markets cannot perform the work of government. Americans need public institutions that can protect them from threats to their lives and livelihoods, and provide leadership in times of crisis. Our economy and society have a long way to go to get back to full health. We have even further to go to implement fixes for our long-running systemic fragilities. I thank you for the chance to submit this testimony on how you can do just that.

We now have 4.3 million confirmed cases of the novel coronavirus in the United States. The virus moves fast, and policymakers in Washington move slow. Families across the country face a wide array of individual income crises and need federal fiscal support, yet policies to address public health and economic hardship are backsliding. Families, unemployed workers, small business owners, and communities need more money, and only Congress has the means to help.

Congress must deliver a multitrillion-dollar package. One-fifth of families have lost a breadwinner and twice as many have lost income, according to surveys by the University of Michigan and Google. Black, Hispanic, and Asian families, as well as young adults and less educated workers, are being hit much harder than others. This is a clear income crisis, larger than any since the Great Depression.

Early on, when the pandemic first crashed the U.S. economy, policymakers had to act with limited information. Key indicators on public health and the economy were not keeping up with quickly changing conditions. Recessions normally build over months or even quarters. This crisis arrived in days and weeks. In addition, huge disagreements among professional forecasters, including me, and massive uncertainty about the path the coronavirus would take hindered the federal response.

None of those excuses prevail today. Official statistics, administrative data, and new research all have caught up. There is no rapid bounce back in our economy. And there will be no solid economic ground until the coronavirus is under control.

Congress, in those first few months, designed the first relief packages for a crisis they hoped would be over by the summer. They were wrong. It is not over, which means they must do more—even more than in March. Coronavirus cases spiked this month, and the U.S. economy worsened. Deaths from COVID-19, the disease caused by the virus, are consequently on the rise. Policymakers must face this harsh reality. They must go bigger and better. They must move faster.

Workplaces must make it safe enough for workers to return to their jobs. Congress must invest aggressively in public health, testing, contact tracing, and personal protective equipment. They must get money out to make up for lost paychecks and reverse cuts in hours and wages of the employed. Families must have paid health insurance, sick leave, and child care. Renters and homeowners behind on their monthly obligations must get help. As many small businesses as possible must avoid bankruptcy. And Congress must get grants to state and local governments to avoid laying off more teachers and essential workers. Congress must get more money out now.

Do what worked again, and keep it simple

Better jobless benefits are the big success story of the relief provided by Congress so far. In March, Congress made more workers eligible for unemployment benefits, including independent contractors and gig workers, and added an extra $600 per week to those benefits while extending the number of weeks someone could receive benefits. By April, the unemployment rate hit its highest level since the Great Depression, and those enhanced unemployment benefits prevented that joblessness from translating into mass human suffering and a macroeconomic collapse. Currently, around 30 million people are receiving jobless benefits, including those who suffered big cuts in hours or wages. Helping the unemployed is crucial to getting us through this income crisis.

New research by the JP Morgan Chase Institute shows that the better jobless benefits worked. Using bank account data, the researchers find these benefits allowed these families not to pull back on their spending. In fact, their spending in July was somewhat higher than before the start of the coronavirus recession. Keep in mind, lower-income families have been twice as likely as the national average to lose jobs in this crisis. Even before losing their jobs, many could not buy what they needed. One-quarter of families, for example, went without medical care because they could not afford it in 2019. Avoiding medical care now is disastrous.

The extra $600 per week in Pandemic Unemployment Compensation will expire on Friday. The last $600 extra went out last weekend. A lapse in this benefit will mean a delay in payments of weeks. Congress must renew the extra $600 per week now and taper it down only when it is safe to go out and the unemployment rate falls.

Another way to fight the income crisis is one-time payments to all families—referred to as recovery rebates. The first round worked well: Most U.S. families got $1,200 per adult and $500 per child. It came within weeks. Nearly all $300 billion arrived by the end of May. In my forthcoming research with University of Michigan economists Matthew Shapiro and Joel Slemrod, one-fifth of families told us they would mostly spend their rebates, mainly within weeks or a few months. We know from a prior study that families said they will mostly save or pay off debt and will spend some too—the cumulative result of which is for every dollar of rebates, 50 cents was spent quickly.

That’s $150 billion—or 4 percent of all consumer spending in the second quarter. These rebates softened the freefall some. And other researchers confirm the sharp upturn in spending when those rebates arrived. The rebates worked. Do it again.

Congress also must extend the enhanced jobless benefits. Again, my forthcoming research shows that half of the unemployed workers in our nation had not yet received any of these benefits by June. Relief packages are pointless if they do not get into the hands of those who need it.

One last piece of the income crisis is employee wage cuts—a hardship not seen since the Great Depression. This income loss comes on top of the layoffs, the lost overtime, and the fewer hours. Many of these workers are employed by small businesses. Congress must get money to small businesses to keep paying employees. Another round of rebates will help, but it cannot make up for less money in every paycheck.

Fix what did not work, and make it simple

Congress left state and local governments to fend for themselves. It is a disaster. States face rising public health costs from the pandemic at the same time that their revenues have plummeted. As a result, state and local governments had laid off or furloughed 1.5 million workers by June, disproportionately harming women and Black workers. Congress increased its share of Medicaid expenses, but not enough to make up for massive budget shortfalls. State governors are calling on Congress repeatedly to send help. We know from the Great Recession more than a decade ago that our communities need support, or the recovery will be slow and painful. Congress must generously support these fiscally embattled state and local governments.

In the private sector, some businesses have rehired some workers, but that uptick in re-employment is unsustainable amid an unabated public health crisis. Most importantly, Congress must find a better way to get money to small businesses—they are the bedrock of U.S. employment. The Paycheck Protection Program was well-intended but failed to get relief to the hardest hit of these firms. Banks gave loans to their most well-connected customers and those faring relatively well, such as construction businesses that continued operating in the shutdown. But the administration of the loans was confusing and too risky for many businesses. Business owners had to use the funding largely for payroll, but many businesses have other big expenses to overcome to stay afloat.

Then, the rules kept changing. As a sign of the mess, even after Congress put more money into the program, businesses did not borrow. Amanda Fischer, my colleague at Washington Center for Equitable Growth, argues that Congress must do better at targeting smaller businesses. They must expand eligible uses for funding and improve incentives for short-term wage compensation, or work-sharing arrangements. Congress must get relief to business owners of color who are serving low-income neighborhoods and hire workers in those communities who need jobs to come back to and earn living wages.

Finally, Congress cannot rely on the Federal Reserve to prop up Main Street. The Fed stabilized Wall Street this spring, and bond and equity markets soared. But the indirect effects are not enough to help small businesses and Main Street communities. Loans from the Fed, to date, are not widespread enough to save enough businesses and keep municipalities from laying off more teachers and other frontline public servants. Congress must instruct the Federal Reserve to fully use its Main Street and Municipal Lending Facilities, even if it means making some loans that may not be repaid. The Fed has made only a handful of loans so far, even as tremendous need exists for more financial support.

Next relief package from Congress

Congress must do what works and commit to doing whatever it takes to support an economic recovery that is strong, stable, and broadly shared. Congress should spend $6 trillion in its next coronavirus relief package. Specifically:

$2 trillion to continue enhanced jobless benefits until people are safely back to work

$1 trillion for grants to state and local governments

$1 trillion in payments to the hardest-hit small businesses

$500 billion for public health efforts to contain the pandemic and keep essential workers safe

$500 billion for another direct payment to all families now and again at the end of the year

$1 trillion for other efforts to support families in need, such as paid child care and sick leave; and rent and mortgage forgiveness

The cost of doing too little now will be enormous in the coming years. No matter what Congress does next, so many families will never get their loved ones back and will never get the chance to say goodbye. But if Congress acts now and commits to stay the course, our workers will get the dignity of work back, our small business owners will succeed, our essential workers will be kept safe, and our children will have teachers. Congress must fight for our future.

Sudden economic contractions are dangerous. Individuals experience income shocks that leave them hungry, sick, and frightened. And if left unchecked, these shocks spread. When people lose income, they stop spending, businesses lose customers, layoffs begin, more people lose income, and more people stop spending. This cycle sends hardships rippling through the population.

Well-crafted economic delivery systems to absorb these shocks are crucial to stopping this cycle, but some policymakers in the United States construct them poorly on purpose. They design systems well that transfer cash to the powerful but use faulty delivery systems as a backdoor way to tamp down aid and assistance to everyday people.

To understand how economic delivery systems can stop the cycle of economic contraction, it’s instructive to look back over the past two decades. Economists drew a clear lesson from the Great Recession a decade ago—delivering money to the hardest-hit individuals and families is one of the best tools to break the cycle of economic contraction. When people have money to buy essential goods and services, businesses maintain their customer base and don’t need to lay off staff. And, as Harvard University economist and Equitable Growth Steering Committee member Karen Dynan and her co-authors’ research found, delivering money to working- and middle-class Americans is the best way to create a virtuous cycle to stabilize the U.S. economy amid an economic downturn.

In the early days of the coronavirus recession, Congress realized this and acted, appropriating more than $2.3 trillion to halt the sharp economic downturn. But earmarking money for individuals and families is not enough. Money needs to actually reach consumers for them to spend it and stabilize the economy.

What are the steps between policymakers acting and families having money to spend to meet their needs? A metaphor can be instructive here. Think of the appropriated resources as water, stored in an aquifer. When resources are delivered effectively, a consumer will turn on the tap at her bathroom sink, and the water will flow. To get from the aquifer to the tap, the water flows through a plumbing system. When there are problems with the plumbing, consumers find their taps empty.

Well-functioning delivery systems, like plumbing systems, are essential to stopping the cycle of economic contraction. At the onset of the coronavirus recession, Congress decided to deliver money to consumers using a variety of programs. Each program has its own set of plumbing systems, beset with its own challenges. As economist Esther Duflo at the Massachusetts Institute of Technology notes, economists have a responsibility to not just create theoretical models but also engage in the messy, complicated work of ensuring that our economic “plumbing” is effective.

It is tempting to look at our broken plumbing and feel resigned that it has to be this way. Fixing delivery systems is a relatively boring and decidedly challenging task. But that perspective misses an important fact: For some people and businesses, delivery systems do work well. In fact, they tend to be incredibly effective for the most powerful members of our society. It’s not that good plumbing is too hard to build or that it naturally breaks down over time. Rather, our policymakers intentionally underresource the systems that deliver aid to everyday people, while quietly maintaining systems that efficiently funnel resources to the powerful.

Using faulty plumbing is a discreet way to cut off aid from those with great need but little political power. It can also be a way to deliver aid through channels that provide profit-making opportunities to private plumbing systems that pop up to fill gaps left open by absent or rusty public plumbing. In good times, the burdens of this system are borne primarily by the very vulnerable. In bad times, economic shocks spread more widely, and the plumbing problems affect more people.

Below, we detail four delivery systems tasked with providing relief during the coronavirus recession— relief targeted to small and large businesses, Unemployment Insurance, direct payments to consumers, and paid leave programs—each of them emblematic of a different plumbing problem. Looking at business rescue programs, we see pipes well-designed to flow easily to people with power, while the taps of the less powerful remain dry. Looking at Unemployment Insurance, we see the failure to invest in pipes, preventing these benefits from flowing smoothly to people who need them the most. Looking at direct payments, we see who profits when the plumbing is routed through costly private systems that twist and turn, enabling the powerful to siphon off of the plumbing. And looking at paid leave, we see what happens when policymakers build no pipes at all and suddenly need to turn on a spigot when the economy hits a drought.

To summarize this research brief’s conclusions, policymakers must invest in our economic infrastructure if our economy is to emerge from the COVID crisis more resilient. This includes:

Re-engineering plumbing to deliver aid to those who need it most in a manner just as quick as our most sophisticated plumbing for the well-connected and well-resourced. This problem comes into stark relief with regard to business rescue programs.

Fixing broken plumbing that has been degraded by years of deliberate neglect. An example of this rusty plumbing is embodied with the degradation of our Unemployment Insurance systems.

Re-routing plumbing to deliver aid directly to the most vulnerable and eliminate costly detours that happen along the way. This brief discusses how a public payment system has been supplanted by private delivery channels that are both slower and costlier to our most vulnerable individuals and families.

Building new plumbing for new programs that invest in an equitable economy. The absence of a paid leave delivery infrastructure has hobbled our ability to quickly and efficiently set that up in the midst of the coronavirus pandemic.

Business rescue programs—unequal plumbing

Challenges in small business rescue systems

Previous writing from the Washington Center for Equitable Growth discusses how mechanisms to aid small businesses are ad hoc, unfamiliar, and difficult to scale up to reach all impacted firms, while mechanisms to aid medium- to large-sized businesses are efficient, well-practiced, and can be deployed at scale. In other words, the economic plumbing to help our small businesses is rusty and degraded, while the plumbing that serves medium- to large-sized businesses is sturdy and resilient.

How is this playing out during the coronavirus recession? News articles declare that “the small business die-off is here,” notwithstanding the $670 billion approved by Congress to save small businesses via the Paycheck Protection Program. Reporting shows that small business owners did not feel confident that they could meet PPP requirements in time for loans to convert to grants, and that even for those who did receive small business loans, the support may not be enough to cover expenses during periods of mandatory lockdown or partial business closures. A survey of research on the Paycheck Protection Program shows that the loans were not properly targeted to the geographic areas hit hardest by the pandemic or its economic effects, and were not designed in a way to prevent avoidable layoffs. Because the assistance provided by the PPP was relatively shallow in comparison to the shock faced by most small businesses, the program ended up serving as a liquidity backstop for small businesses that needed a temporary boost, rather than a lifeline for the most devastated businesses.

The funding also likely arrived too late for many businesses. Recent research from Opportunity Insights, led by former Equitable Growth Steering Committee member Raj Chetty, finds that small businesses providing services that require face-to-face contact in certain ZIP codes saw an 80 percent drop-off in revenue largely before government rescue money was even available. Moreover, early survey research is showing that small businesses owned by Black and Latinx entrepreneurs are suffering particularly acutely.

The story is different for medium- to large-sized businesses, whose aid came largely via lender-of-last resort interventions by the Federal Reserve rather than through appropriations by Congress. The Federal Reserve’s stated commitments to support the economy across a number of interventions had the effect of bolstering these businesses’ ability to raise capital, even before most policy actions were undertaken. So, it doesn’t even much matter when the Fed starts to lend to companies or buy their bonds because the mere reassurance that the Fed will step in is enough to soothe the markets that serve medium- to large-sized businesses. Investment-grade, or the most creditworthy, U.S. companies issued record-breaking amounts of debt during the first few months of the coronavirus recession and have continued to do so. Junk bonds, or those that are backed by less creditworthy but still medium- to large-sized companies, are strongly rebounding too.

The gap between the efficient business rescue programs for medium- to large-sized businesses and laggard small business rescue programs was known to policymakers well before the coronavirus pandemic caused the latest recession. After the global financial crisis of a decade ago, the stock market and bank profits rebounded quickly, while small businesses recovered much more slowly. While the Federal Reserve at that time was able to calm markets with monetary policy interventions and bail out large financial firms over the course of mere days, small business rescue programs never received a needed revamp.

Fast forward to today. Markets rightly believe Fed Chair Jerome Powell when he says that the Federal Reserve is “not going to run out of ammunition,” largely because the Fed took extraordinary actions a decade ago when faced with the previous crisis.

Small businesses do not hear the same reassurances and would have no reason to believe such statements even if they were declared. In fact, multiple government oversight reports and pieces of journalismdocument how small business aid was slow to arrive for eligible firms after natural disasters over the course of the past decade. This pattern was replicated on a larger scale during the current crisis, when the U.S. Small Business Administration was tasked with deploying funding provided via the Paycheck Protection Program to ailing small firms.

There certainly are success stories for small businesses due to the Paycheck Protection Program, yet the small business aid also was beset by administrative chaos at its inception. The Small Business Administration website crashed on its first day of launching and many times thereafter, and many small businesses remain in grave danger. One survey of small business owners shows that more than half of them expect to be out of business in the 6 months after the survey was taken in April 2020.

Profit-seeking in private rescue systems

In the case of both programs—both the insufficient small business rescue efforts and the efficient medium- to large-sized business rescue efforts—it should be noted that the government lacked the infrastructure to administer programs directly. In fact, each was administered by agents in the financial sector, rather than through the direct public provision of assistance.

This means that certain private firms, usually the most advantaged and well-connected, profit from the taxpayer-directed deployment of rescue aid. That profit represents funds that reinforce existing political power and that could otherwise be channeled back into helping those suffering.

In the case of small business rescue programs, the Small Business Administration, lacking staff or technical capacity to loan hundreds of billions of dollars using in-house capacity, relied on financial institutions to intermediate the delivery of financial aid from taxpayers to eligible small firms. In exchange for these services, lenders received more than $18 billion in fee income from processing Paycheck Protection Program loans—money that was deducted from the pool of funding available for small businesses.

By intermediating aid through the banking sector, the program also reinforced existing inequities in small business credit, at least according to anecdotal reports. The New York Times reported that a large small business lender established a “concierge service” for VIP business clients, allowing them to bypass call center wait times and avoid online portal snafus. As stated earlier, other stories documented the troubles faced by Black- and Latinx-owned small businesses in accessing funds, repeating longstanding discrimination in small business funding from the banking sector.

Again, this policy choice is not inevitable. Congress could have found ways to directly compensate businesses using systems similar to best practices from abroad. Denmark’s business rescue program, for example, had businesses apply directly to the Danish Business Authority for rescue aid. Denmark is now on track for a much less dramatic collapse in GDP this year, compared to peer countries, due both to the success of public health measures and economic rescue programs in the country. An efficient and already well-developed U.S. Small Business Administration, with pre-existing relationships with the IRS or payroll processing companies, could have worked to release aid in a more efficient and equitable manner.

One natural experiment in the United States is the state of North Dakota, which led the nation in small business rescue funding received per small business worker in the state. Observers credit the Bank of North Dakota, a public bank, for the state leading in the deployment of small business funds. In the words of Robert Hockett, a Cornell University law professor and alumnus of the Federal Reserve Bank of New York, in a comment to The Washington Post, “there was no leakage—the sort of ridiculous fee-charging that tends to happen when you do it through larger banking entities.”

He added that the North Dakota model “isn’t really designed to maximize revenue lines by finding as many places to assess fees or brokerage charges as possible.” Though the bank offers few retail services or direct loans, it did serve as a clearinghouse to community banks, educating them about the new program, coordinating across the state, and buying slices of loans from local lenders where needed. The amount and type of help available in North Dakota was clearly well-practiced and scaled to the extent of the crisis in the state.

In the case of large business rescue programs, profit-seeking firms also sit at the center of aid programs. The Federal Reserve is being supported by asset management firms BlackRock, Inc. in the purchase of corporate bonds and Pimco Company in the purchase of commercial paper. Both are programs designed to boost large businesses’ financial health. All told, BlackRock and Pimco are under contract to purchase hundreds of billions of dollars’ worth of financial investments on behalf of the Fed, with BlackRock, for example, slated to earn around $40 million in profit from the services it’s providing.

This raises significant conflict of interest concerns, as each company is also a large shareholder or bondholder in many of the companies whose financial investments they may buy on behalf of taxpayers. In the case of BlackRock, the company was also tasked with purchasing exchange-traded funds, and early reports show that BlackRock ETFs were the primary beneficiaries of BlackRock purchases as an agent of the Federal Reserve. Other observers point to relatively lax conflict of interest standards in place within Federal Reserve financial agent contracts, allowing potentially unfair access to market-moving information. And while these contracts will come up for a bid by the summer, they were initially granted by the Fed on a no-bid, temporary basis in response to the coronavirus recession emergency.

The use of these firms to administer rescue programs on behalf of the Federal Reserve is not a new phenomenon. The same approach was used in response to the 2008 financial crisis, underscoring that the Fed and policymakers have had time to consider alternative approaches to responding to a financial emergency and chose not to build public plumbing, but instead to rely merely on private plumbing. This represents a missed opportunity, as the Federal Reserve System employs almost 23,000 individuals, including sophisticated lawyers, economists, and market experts, and its budget authority is unlimited and set outside the congressional appropriations process. Given that this is the second major rescue program in more than 12 years, it stands to reason that it may be in the public’s best interest to develop this expertise in-house.

Alternatively, scholars such as Saule Omarova and Robert Hockett, both from the Cornell School of Law, suggest that Congress create a National Investment Authority that could serve as an institutional bailout manager, with democratic governance, to manage taxpayer investments in private enterprises with a fiduciary duty to the public. Similar proposals have been floated in major news outlets, harkening back to the Great Depression’s Reconstruction Finance Corporation, and in a piece by Todd Tucker, the director of governance studies at the Roosevelt Institute.

The plumbing that serves our least well-resourced constituencies—small businesses—is rusty, compared to the plumbing that serves medium- to large-sized businesses. Compounding that imbalance is the fact that the very firms that benefit from the efficient plumbing also manage to profit from the laggard plumbing available to others, reinforcing inequities in a feedback loop that accelerates during times of crisis.

Unemployment Insurance—rusty plumbing

At a moment when nearly 1 in 4 U.S. workers is not receiving a paycheck due to a pandemic that is clearly beyond their control and taking place in a country with no paid leave social insurance program, Unemployment Insurance is an obvious choice for delivering income to those who lose work due to the pandemic and its economic fall-out. Indeed, Congress recognized this when they gave states the ability to modify rules affecting the receipt of Unemployment Insurance to suit the conditions of the pandemic, and again when they established three pandemic-specific Unemployment Insurance add-ons: one increasing the benefit amount, another lengthening the benefit duration, and a third expanding the group of people eligible for benefits to include independent contractors, those with low earnings, and independent contractors.

Yet when people went to access the benefits they were entitled to under the law, many were greeted by crashed websites, jammed phone lines, and even instructions to line up in person to receive paper applications. The $600 weekly increase took weeks to implement, and in some states, the program expanding benefits to new groups of claimants took months. While some policymakers try to pass off this state of affairs as an unexpected tragedy—a sad coincidence that the system was out of shape just when benefits were needed most—the difficulties with benefit delivery are the result of decades of conscious choice by policymakers to starve the system of the resources it needed most. With computing systems that are hard to navigate for claimants and challenging to update for administrators, and without adequate resources for staffing and system updates, the plumbing for delivering Unemployment Insurance benefits is broken from years of neglect.

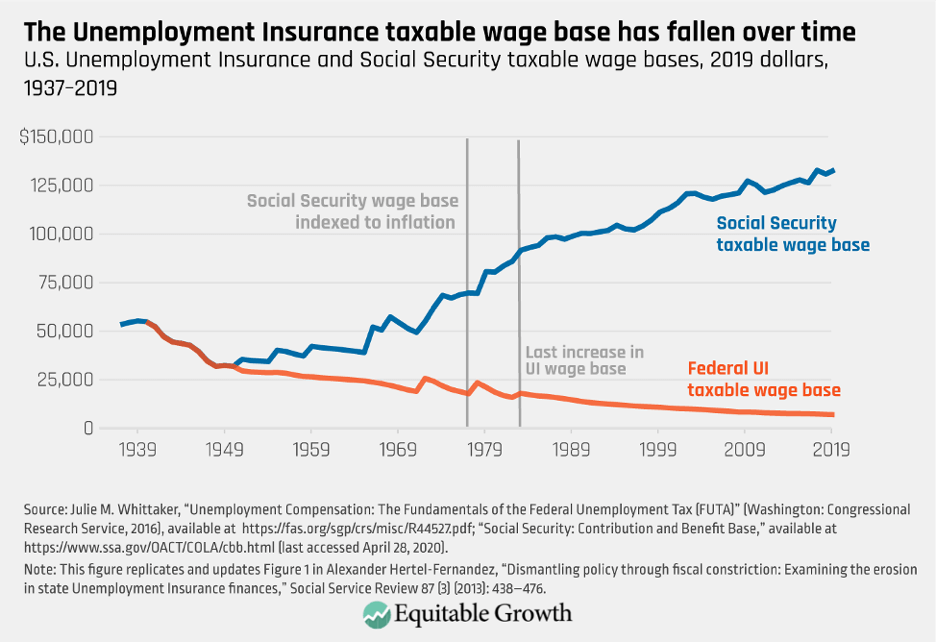

Unemployment Insurance program administration is funded through federal taxes based on employee payroll—referred to as FUTA taxes after the Federal Unemployment Tax Act. Taxes are collected at a rate of 0.6 percent (the FUTA tax rate is 6 percent, but a 5.4 percent credit is applied for state taxes paid) and are levied on the first $7,000 of earnings for each worker on an employer’s payroll. For a full-time, year-round employee, the FUTA tax is $42 per worker per year.

These taxes are technically charged to employers, but research finds that employers pass the cost on to workers by paying them less. This revenue is tasked with not only maintaining more than 50 administrative systems but also funding half the cost of the extended benefits that workers receive in times of economic contraction. In 1939, the taxable wage base was $3,000, equivalent to $55,000 in 2020 dollars. Because this amount can only be raised by law (and has only increased three times over the past 80 years), its value has eroded by nearly 800 percent. In contrast, the taxable wage base for Social Security benefits was indexed to inflation in 1977. The chart below shows their divergent histories. (See Figure 1.)

Figure 1

This trend has been labeled fiscal constriction by Columbia University scholar Alexander Hertel-Fernandez, and it means that by starving the Unemployment Insurance program of resources, policymakers effectively bind their own hands and purposefully prevent themselves from establishing a modern and efficient system for disbursing benefits. During the Great Recession, we saw the consequences of fiscal constriction clearly. Yet federal policymakers left the taxable wage base at the same level it has been stuck at since 1983, unmoved by the hardship of millions of members of the U.S. labor force and unwilling to risk even a small amount of political capital by modestly nudging tax levels upward.

Bringing the Unemployment Insurance taxable wage base back to the same level as the Social Security taxable wage base and then indexing it to inflation would provide states with the resources they need to deliver unemployment benefits efficiently and effectively.

Looking to 2017 as an example and conducting a simple back-of-the-envelope calculation that keeps the FUTA tax rate at 6 percent and applies a 5.4 percent state credit reduction to the $7 trillion of taxable earnings under the Social Security wage base indicates that using this tax base would generate $41 billion. This is a $33 billion increase over the $8 billion in FUTA taxes that were actually collected in 2017. Similar to other social insurance programs, Unemployment Insurance has an elegant design—small taxes in good times ensure smooth delivery of benefits in hard times. By allowing the pay-for to erode over time, policymakers shirk their fiscal responsibility, and workers and families pay the price. Following the Social Security model and indexing the wage base is a small investment that will yield large dividends.

In fact, this additional revenue would provide sufficient funds for Unemployment Insurance system modernization efforts (past grants to states have ranged from $50 million to $200 million), ongoing maintenance, and appropriate staffing. These funds also could be used to provide grants to states to partner with community-based organizations serving vulnerable workers to raise awareness of Unemployment Insurance benefits and provide assistance in the application process. Additional revenue would cover the increased use of the Extended Benefits program and could be used to provide grants to states as they standardize the amount and length of benefits, as detailed below. Any change to the taxable wage base could be scheduled—for example, occurring when unemployment rates return to pre-pandemic levels with revenue advanced prior to that time.

Without this type of policy change, policymakers won’t have the resources that are so badly needed to repair our broken plumbing and efficiently deliver benefits to people who are entitled to them under law. The case of Unemployment Insurance shows that it’s not enough to build a system to disburse benefits—that money needs to be spent over the long haul to maintain that system. This type of continued investment is necessary to deliver the benefits that provide relief to individuals and stabilize our economy when crisis hits.

Direct payments to households—plumbing that twists and turns to allow siphoning off along the way

Most Americans live on razor-thin budgets, even in good times. One study from the Federal Reserve has found that only 40 percent of Americans could cover a $400 emergency expense.

So, when Congress authorized emergency direct payments to households as part of the Coronavirus Aid, Relief, and Economic Security, or CARES, Act, the efficiency of the plumbing was nearly as important as the amount of water unleashed from the aquifer. The degradation of our public plumbing systems—namely, the IRS as an agency tasked with locating all U.S. taxpayers and building a channel to allow payments between individuals and the government—was laid bare.

While around 6 in 10 people who file taxes received a direct deposit refund from the IRS in 2018 or 2019—the filing years the IRS used to track bank account information for these payments—4 in 10 filers, representing almost 64 million filers, did not (the vast majority of those 64 million filers was eligible for CARES Act payments, which phase out for higher-income earners). These individuals and families had to wait weeks for paper checks to be mailed, with one estimate suggesting that certain filers may have to keep waiting until September, about 20 weeks after the direct payments were authorized by Congress. While the IRS rightly prioritized mailing checks out sooner for those with the lowest adjusted gross income, mailing paper checks still took weeks longer than for those with direct deposit numbers on file.

Those who don’t file tax returns with the IRS faced an even more complex situation. Social Security recipients who didn’t, in the recent past, file tax returns received unclear information about whether they had to file a supplementary tax form to get a direct payment check and had to meet a deadline if they wanted to claim dependents. While the IRS set up an online portal for nonfilers to report direct deposit information and avoid the check-mailing process, the deadline for such submissions was May 13, and many less-tech-savvy individuals probably didn’t know where to enter that information or were unable to do so.

While the IRS worked as quickly as possible to deploy money in a timely manner, there are consequences to this lack of preparedness. Those who receive paper checks may have needed, or may still need, to get expensive payday loans to tide them over until checks arrive. Others still may overdraft on their bank accounts, leading to fees. Others who don’t need an advance on their checks may need to go to expensive check cashers to convert checks into money once they arrive. And because policymakers allowed creditors to “eat first” once checks arrived, stories surfaced showing that banks garnished the checks deposited into peoples’ accounts, both to repay bank debts and on behalf of debt collectors.

All told, direct coronavirus-payment challenges replicate our existing understanding of the high cost of being poor, with low- to moderate-income households spending far more than other households on fees as a percentage of their income, averaging a whopping 10 percent of income, using data from before the coronavirus.

These expenses reflect a lack of public economic infrastructure. And while they represent burdensome budget items for some, they represent profit to others. Banks made an estimated $11.68 billion in overdraft fees in 2019, with an average fee of around $35 per overdraft. These fees fall particularly hard on the working class, with only 9 percent of account holders (typically those with low account balances) representing 84 percent of the total fees charged. Check cashers and payday lenders made a similar amount in fees, totaling around $11.4 billion in 2019.

Further, the tax preparation company TurboTax, owned by Intuit Inc., created a proprietary website where individuals could go to enter direct deposit information, calculate anticipated check amounts, and check on the status of their payments. While the website services are offered at no charge, TurboTax has, in the past, used the promise of free services to steer filers into more expensive proprietary and add-on products, even when they qualified for free filing. TurboTax made $1.6 billion in income in the most recent filing year.

Solutions for quicker direct payments

All of these frictions were avoidable had other public policy choices been made. Just as fiscal constriction has hobbled state Unemployment Insurance systems, federal policy has deliberately underinvested in technical capacity and potential delivery systems for the IRS. While the IRS staff had an unenviable task of accomplishing the massive technical and logistical challenge of deploying millions of direct payments in a matter of weeks during a global pandemic, the snafus experienced by the agency were undoubtably made worse by sustained budget cuts over the past decade. As the Center on Budget and Policy Priorities documents, the IRS has lost nearly 15 percent of its staff and 21 percent of its budget since 2009. A more well-resourced IRS would have been better prepared for this moment.

Policymakers also missed an opportunity to build out the IRS’s technology infrastructure by not considering legislation to direct and support the IRS in establishing a free file online portal system for annual tax returns. Though envisioned as a tool for routine annual filings before the pandemic, such a system run by a well-resourced IRS could have been quickly repurposed to meet direct payment needs and could have supplanted TurboTax.

Moreover, policymakers could have advanced other actions to strengthen payment delivery mechanisms to individuals and households. The United States has one of the slowest payment systems in the world, compared to peer countries. This means that it can take days after funds are deposited in private bank accounts for those funds to actually be available to spend. Again, in the case of the coronavirus recession, this adds yet more frictions to the delivery of aid. But this slow system is not inevitable.

In the United States, the Federal Reserve both regulates the private payment system and operates its own system. The private payment system, which is the dominant system, is operated by The Clearing House, a consortium of 24 large banks. The Fed has long had the goal of modernizing its own payment system, which hasn’t been updated in decades, releasing a proposal to bolster payment infrastructure in 2013 and then committing in 2019 to finalize an upgraded payment infrastructure by 2024.

Such moves to modernize our public payment infrastructure have been opposed by The Clearing House. The bank association argues that large banks have already invested substantial time in building their own system, that the Fed cannot act as both a regulator and a competitor, and that further investments would be needed to ensure interoperability with the new Fed system. Below the surface are the obvious concerns that this public system would undercut The Clearing House’s market dominance, would reduce profits on payment transactions, and would dampen the use of overdrafts, thereby further reducing bank fees.

In the case of the deployment of coronavirus rescue funds, a public, faster payment system would have clear benefits. One estimate from Aaron Klein, policy director for the Center on Regulation and Markets at The Brookings Institution, finds that implementing the Fed’s real-time payment system could save low-income families $7 billion a year simply by helping money to arrive faster and allowing families to thereby avoid intermediaries such as check-cashing services and payday lending companies to access their money.

Further, a public payment system also would help small businesses to manage incoming and outgoing payments, as these businesses are now operating on thinner margins during the recession. Lastly, a faster digital payment system is essential during a highly transmissible pandemic. While the use of cash to make payments has been declining for years, public health concerns and social distancing have increased the need to more quickly mediate money electronically.

In addition to building a quicker public payment system to deliver funds to private bank accounts, policymakers also could build accounts that are themselves public. Legislation based on the work of Washington Center for Equitable Growth Board member Mehrsa Baradaran has, for years, been introduced to allow the U.S. Postal Service to provide basic banking services to customers—bank accounts that could be available in every community across the country and could allow for a functioning economic system that equitably serves all individuals and families.

In this way, policymakers could eliminate or reduce costly fees and stop garnishments through this public system. And it wouldn’t be a new or untested approach. The U.S. Postal Service has done this in the past, providing banking services for 50 years starting in 1911. This would have the benefit of both expanding access, reducing costs to consumers, and shoring-up the finances of the postal system, which stands in a precarious position due to both the pandemic and congressional legislation that has required the service to pre-pay 75 years’ worth of healthcare and retirement benefits for workers. The Postal Service could offer these accounts either through a congressional authorization or via administrative action, with its Board of Governors authorizing the measure.

Paid leave—when plumbing does not exist

If ever there were a moment that called for paid leave, the coronavirus crisis is it. The term “paid family and medical leave” refers to social insurance programs in which a small payroll tax is collected while people work and then—when the need arises to care for a new child, seriously ill loved one, or one’s own serious medical need—workers can take weeks or months away from work with partial wage replacement. In some thoughtfully designed paid leave programs, workers are guaranteed to be able to return to their job when their leave is complete.

Most paid leave programs were not designed with a pandemic in mind, but they are built to deliver paid time away from work for health reasons while maintaining attachment to one’s employer. If you are scratching your head and wondering why policymakers chose not to deliver payments through a small modification to the eligibility criteria associated with our federal paid leave system, the answer is simple: We do not have a federal paid leave system. Legislation has been introduced for many years that proposes the adoption of a federal paid leave program. Yet political obstacles have prevented us from establishing a federal system, despite the research that suggests doing so would strengthen the economy and benefit the finances and health of paid leave claimants and those who receive care from them. A lack of a federal system leaves us scrambling to provide paid leave solutions when workers need them most.

Congress eventually passed legislation in response to the employment crisis caused by the COVID pandemic. But the “paid leave” program it enacted bears little resemblance to a strong social insurance system that provides adequate time away from work to care for oneself or a loved one. This is a temporary stop-gap, not an investment in permanent plumbing. This stop-gap system provides a fraction of the workforce with 80 hours of leave at full pay for those with symptoms or the need to quarantine due to one’s own COVID-19, the disease caused by the coronavirus, 80 hours at two-thirds pay for to care for someone subject to quarantine or a child subject to COVID-19-related school or childcare closure, and another 10 weeks of leave at two-thirds pay to provide childcare for one’s own children who are subject to COVID-19-related school or childcare closure. These benefits don’t provide the support that social insurance programs offer and that people whose families are affected by COVID-19 need: weeks, not days, of leave to attend to one’s illness or the illness of loved ones.