There is considerable research showing that recessions hit young college graduates harder than older graduates. Based on the evidence from research I’ve done for a new working paper, the damage (or “scarring”) is even worse and lasts far longer than anticipated. Indeed, the long-term consequences are comparable in magnitude to the short-run effects, roughly doubling the initial cost. The results suggest that policymakers need to do more to prepare for recessions and ameliorate their severity.

Economists have known for some time that in a recession, young workers, including new college graduates, are more likely to become or remain unemployed, lose access to training and work experience at a time in their careers when they need them most, and suffer from lost income both during unemployment and in the early years following a period of joblessness.

My research for a new working paper, which focuses on young college graduates in the Great Recession of 2007–2009 and its aftermath, suggests that the damage suffered by young workers in recessions lasts throughout their careers. Those who enter the labor market during recessions have permanently lower employment and earnings, even after the economy has recovered.

This long-term scarring argues not only for quicker and stronger action to counter recessions when they occur but also for putting in place policies that can be automatically triggered at the first signs of a recession to limit its depth and duration.

The Great Recession was the worst downturn since the Great Depression and wreaked havoc on U.S. workers and businesses. Unemployment rose by 6.5 percentage points and took nearly 10 years to get back to its prerecession level. Job losses amounted to 8.7 million. Perhaps more importantly, the prime-age employment rate, which measures the percentage of people aged 25–54 who are employed, fell by more than 5 percentage points to its lowest level in 25 years and, despite continuing tightening in the labor market, has not quite fully recovered after 10 years.

And yet, the long-term damage, while less visible, will cause more financial and career losses to cohorts of workers who entered the labor market during this period.

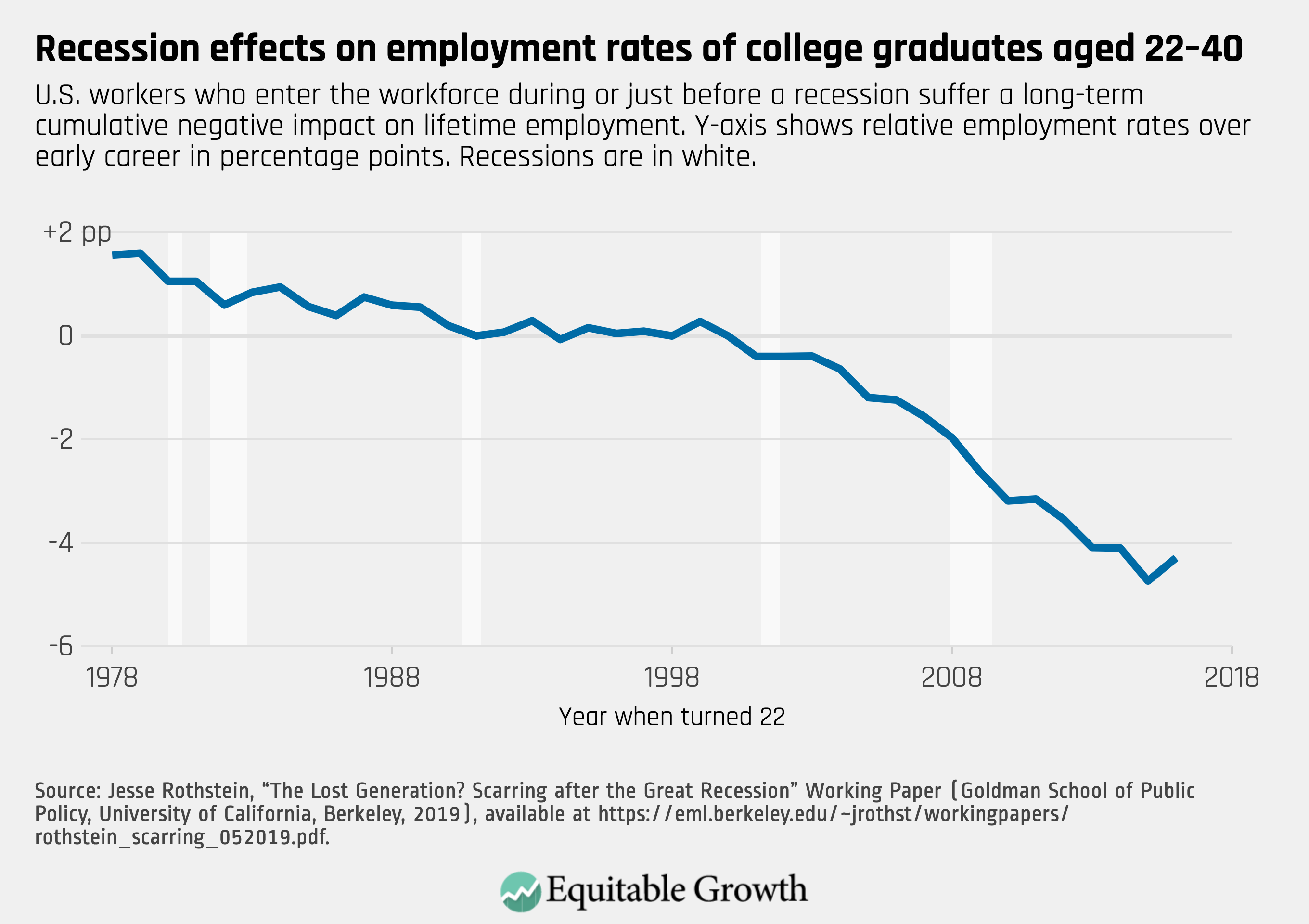

To obtain my results, I used the U.S. Census Bureau’s monthly Current Population Survey. I used the data to determine the degree to which poor employment rates of young graduates following recessions can be attributed to transitory shocks (the reduced demand for workers in the immediate wake of the recession) versus permanent differences that last long after the recession is over. In other words, once the overall labor market recovered, would there continue to be significant differences in employment outcomes (after adjusting for normal age differences) between those who entered during the recession and those who entered prior? (See Figure 1.)

Figure 1

Figure 1 shows the drop in employment rates around recessions (white areas) for different cohorts of college graduates ages 22 to 40, with the years on the x-axis indicating the year a cohort entered the workforce. These estimates net out effects that are common to workers of all ages during the recession and disappear after the recession is past; they show only differences in outcomes for new graduates relative to older workers. The sharp downward slope for younger cohorts (those entering the workforce more recently) shows how much harder hit they were by the Great Recession than other workers. Workers from these cohorts saw their annual employment rates drop by 2 percentage points to 4 percentage points per year, relative to older workers in the same labor market. Those who were established in the workforce by the beginning of the recession—those who graduated college in 2005 and earlier—essentially returned to prerecession levels of employment by 2014. But those who entered after 2005 have not; their employment rates remain depressed even as the overall market has recovered.

These findings raise an important question. Is the damage permanent, or will the affected cohorts recover as they age, thus making the damage only temporary? Evidence from past recessions is informative here. In each of the recessions of the past several decades, graduates who entered the market during the period of economic weakness were scarred, just as seen in Figure 1. They recovered part of the damage in the years following the recession, but only part—half of the damage to recession cohorts has been permanent, manifesting as lower employment rates throughout their careers than for cohorts that graduated in better times.

For the Great Recession graduates, I estimate based on past recessions that this permanent scarring will reduce the average individual’s post-recession employment throughout his or her career by a total of approximately one week. Moreover, my research also shows that those scarred by recessions will earn lower wages when they are employed—about 2 percent less through the early years of their careers.

On an individual level, these losses might seem relatively small. Taken together, as an entire cohort of workers, they represent a very substantial loss of potential earnings.

How policymakers can ameliorate the consequences of the next economic downturn

Recessions are inevitable, even if economists can’t predict their timing or severity. One of the many mysteries of economic policymaking is why Congress and successive administrations have not done more to prepare in advance for upcoming recessions.

To be sure, there are already federal programs, known as automatic stabilizers, that act as counter-cyclical measures. Unemployment Insurance is a good example. When the economy slows and joblessness rises, more people receive these benefits, propping up their ability to spend and thus pumping additional money into the economy. The tax system acts in a similar way—removing less money from the economy as workers earn less.

Yet these existing automatic stabilizers are rarely sufficient. By the time policymakers act in the middle of a downturn, the system has already failed millions of workers (along with their families) who may have lost their jobs unnecessarily and/or suffered avoidably long periods of unemployment. There is no need to wait for emergency legislation. To reduce the damage to workers and families, we need to have plans in place before recessions arrive to speed recoveries and cushion those affected until the recovery comes. Such measures are especially effective when targeted to those with the greatest marginal propensity to consume—those who live from pay/benefit check to pay/benefit check.

Equitable Growth and The Brookings Institution’s Hamilton Project released a book recently, titled Recession Ready: Fiscal Policies to Stabilize the American Economy, that makes the case for six policies that either strengthen existing stabilizers or add new measures to be triggered when unemployment begins rising with a consistency that has always proven to signal a coming recession. We ought to consider these and other ideas now, before the next recession hits.

While it will be some time before conclusive data are available, my research clearly suggests that as a group, the young people who graduated just before, during, or immediately following the Great Recession will find it harder to be employed and will receive measurably lower wages and annual earnings throughout their careers. This has also been true of past recessions. This adds up to massive damage to the affected individuals, their families, and our economy, and argues strongly for measures to ameliorate the impact and length of future downturns.

—Jesse Rothstein is an associate professor of public policy and economics at the University of California, Berkeley and a member of the Washington Center for Equitable Growth’s Research Advisory Board.

Tara Dawson McGuinness, a senior fellow at the public policy think tank New America and a senior adviser to its National Network and Public Interest Technology programs, has joined the Washington Center for Equitable Growth Board of Directors.

McGuinness, who also teaches public policy at Georgetown University, has a long history of leadership in building both governmental and nongovernmental organizations that serve the public and local communities. She is a champion of evidence-backed policy and program implementation that creates a feedback loop for citizens in the policy process. She recently completed, for example, an effort focused on landscaping public policies and programs that would decrease inequality and increase mobility for Americans.

Prior to joining New America in 2017, McGuinness served as a senior advisor in the Obama White House in several capacities. She ran the organizing and communications effort to sign up Americans for Obamacare after President Barack Obama signed the Affordable Care Act into law, helping 15 million people gain access to health insurance. She later oversaw the federal government’s initiatives to support cities and towns at the White House Office of Management and Budget.

McGuinness also directed the White House Task Force on Community Solutions, which facilitated interagency efforts to use data in new ways to tackle entrenched poverty at the community level. She oversaw federal teams working with local leaders in Detroit, Baltimore, Flint, Michigan, and elsewhere.

McGuinness writes frequently about the potential impact of data in helping cities and communities address problems. “A hallmark of successful public problem solvers today,” she wrote in the Stanford Social Innovation Review with co-author Anne-Marie Slaughter, “is their ability to use data (big and small) to measure problems, to learn what works and what doesn’t, and to make improvements as soon as they are necessary.” McGuiness and Slaughter added:

The opportunity for data use in public problem solving … can take the form of analytics … or performance management dashboards … or low-cost evaluation methods. Those making the most transformational change across the United States have a culture of measurement and reassessment, with data as the central ingredient. It is not the data, per se, that add value, but their ability to tighten the feedback loop between people receiving services and those … steering them.

McGuiness is currently writing a book on the intersection of data, human-centered design, and the importance of delivery in public policy to be published in 2021.

Prior to her work in the Obama Administration, McGuinness was the executive director of the Center for American Progress Action Fund. She has also worked at the National Democratic Institute and on Capitol Hill. McGuinness is a graduate of the University of Pennsylvania in urban studies.

Equitable Growth is excited about the leadership and expertise McGuiness brings to our organization. Her expertise examining and implementing data-driven, evidence-backed ideas and policies are central to our mission to promote strong, stable, and broad-based economic growth.

Rising economic inequality over the past 40 years has redrawn the U.S. wealth and income landscape, shifting many of the gains of prosperity into the hands of a smaller and smaller group of people and marginalizing members of vulnerable communities. This transformation is in turn reducing income mobility and opening gulfs in educational achievement and health outcomes between different levels of income. The eight graphs in the three sections below visually illustrate these findings.

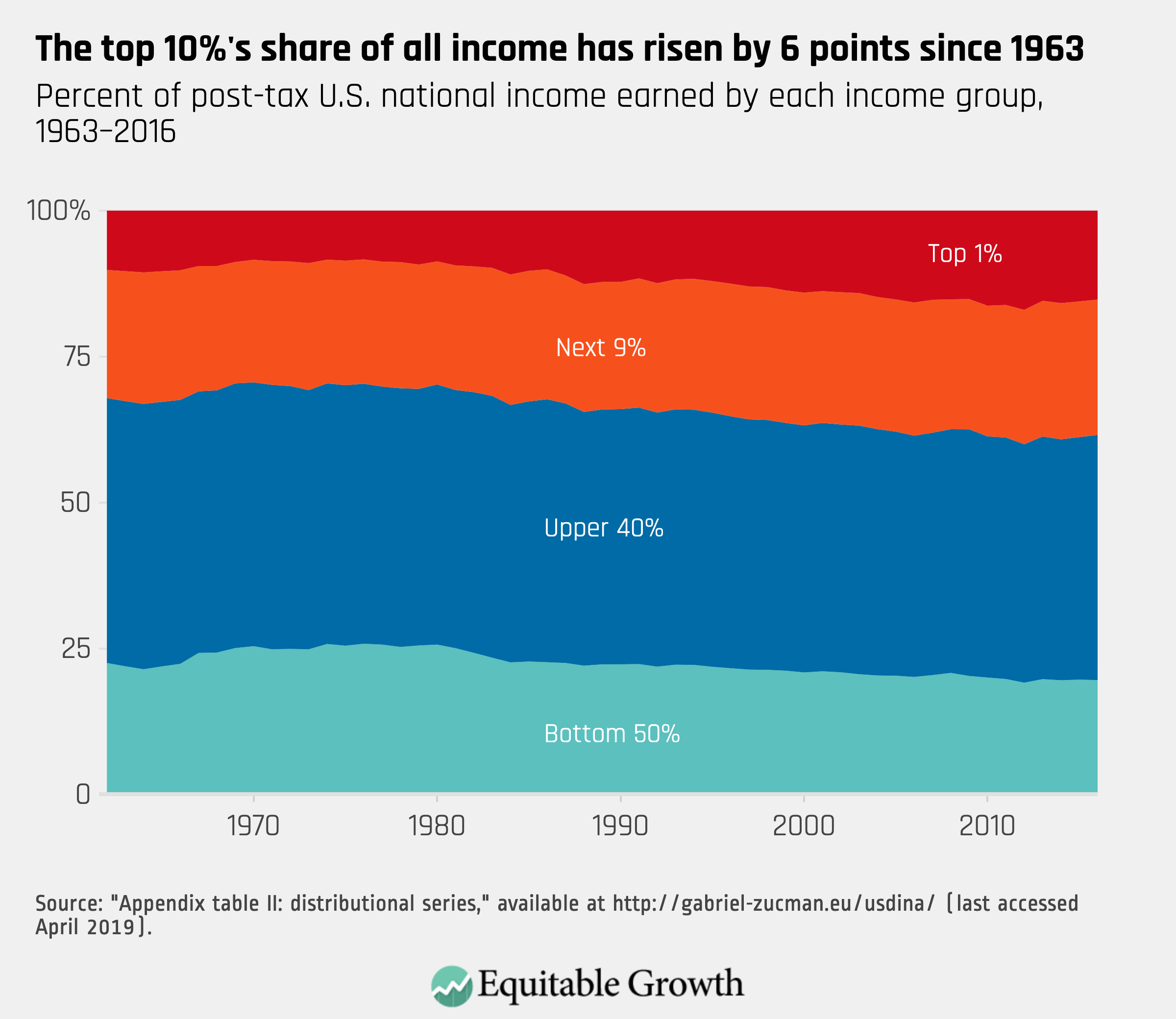

The first graphic tracks the share of all earned income accrued by the top 1 percent of earners, along with the next 9 percent, the upper 40 percent (from the 50th percentile to the 90th) and the bottom 50 percent. The share of income controlled by the top 10 percent bottomed out in the 1970s but has reached new highs—the top 10 percent of all income earners now control around 38 percent of national income. (See Figure 1.)

Figure 1

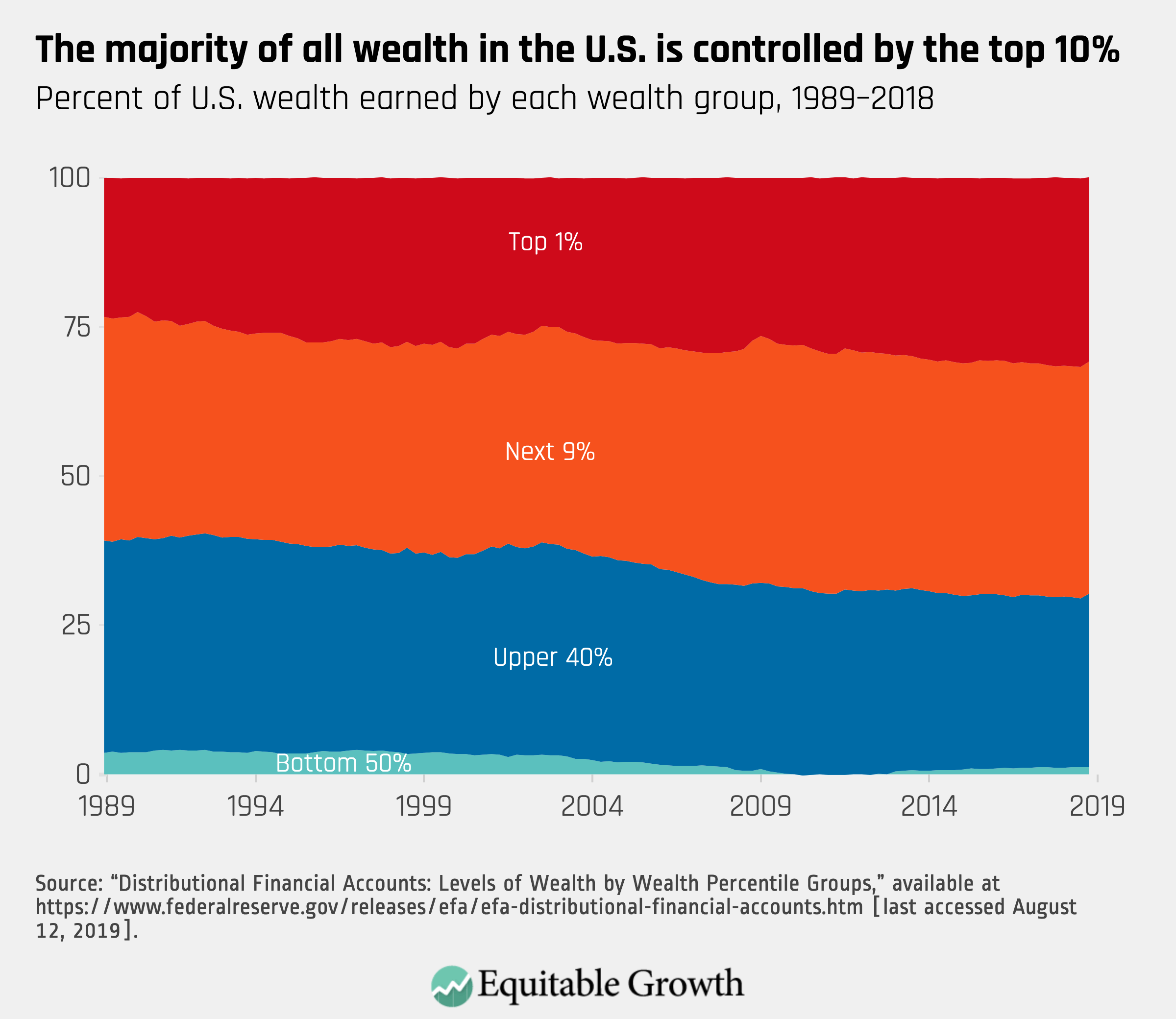

Wealth concentration has risen even faster. The wealthiest 10 percent of households have long controlled more than 50 percent of all wealth, but that proportion has grown steadily over the past two decades, according to new research from economists at the Federal Reserve. Just 1 in 100 Americans now own 31 percent of all wealth in the country, and the top 10 percent owns 70 percent of all wealth. Meanwhile, one half of Americans with the lowest wealth have paltry assets: just 1.2 percent of the total. (See Figure 2.)

Figure 2

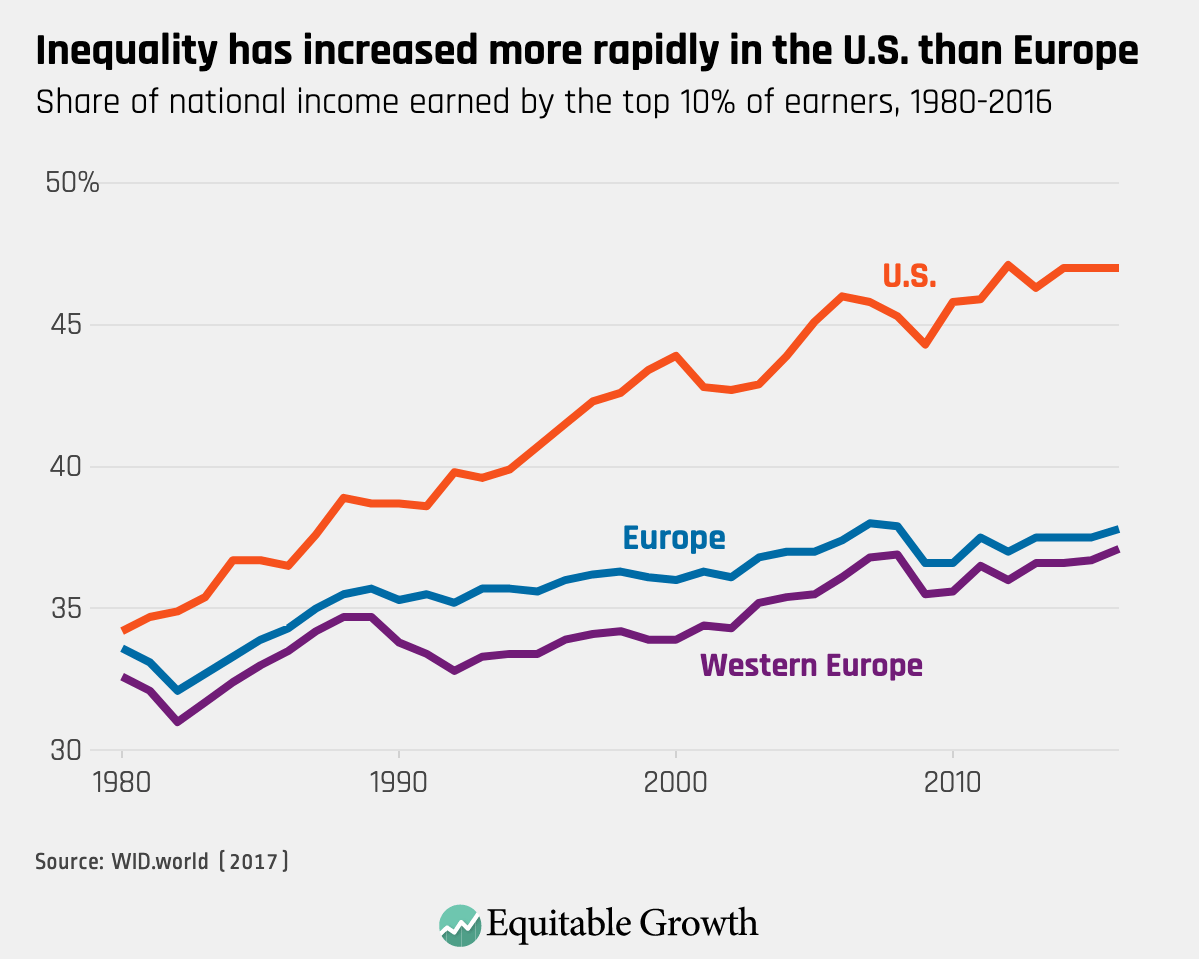

To some extent, these patterns are evident in other countries, suggesting that there may be global effects that explain some portion of the rise in inequality. But the rise in the United States has been much steeper than in Europe. (See Figure 3.)

Figure 3

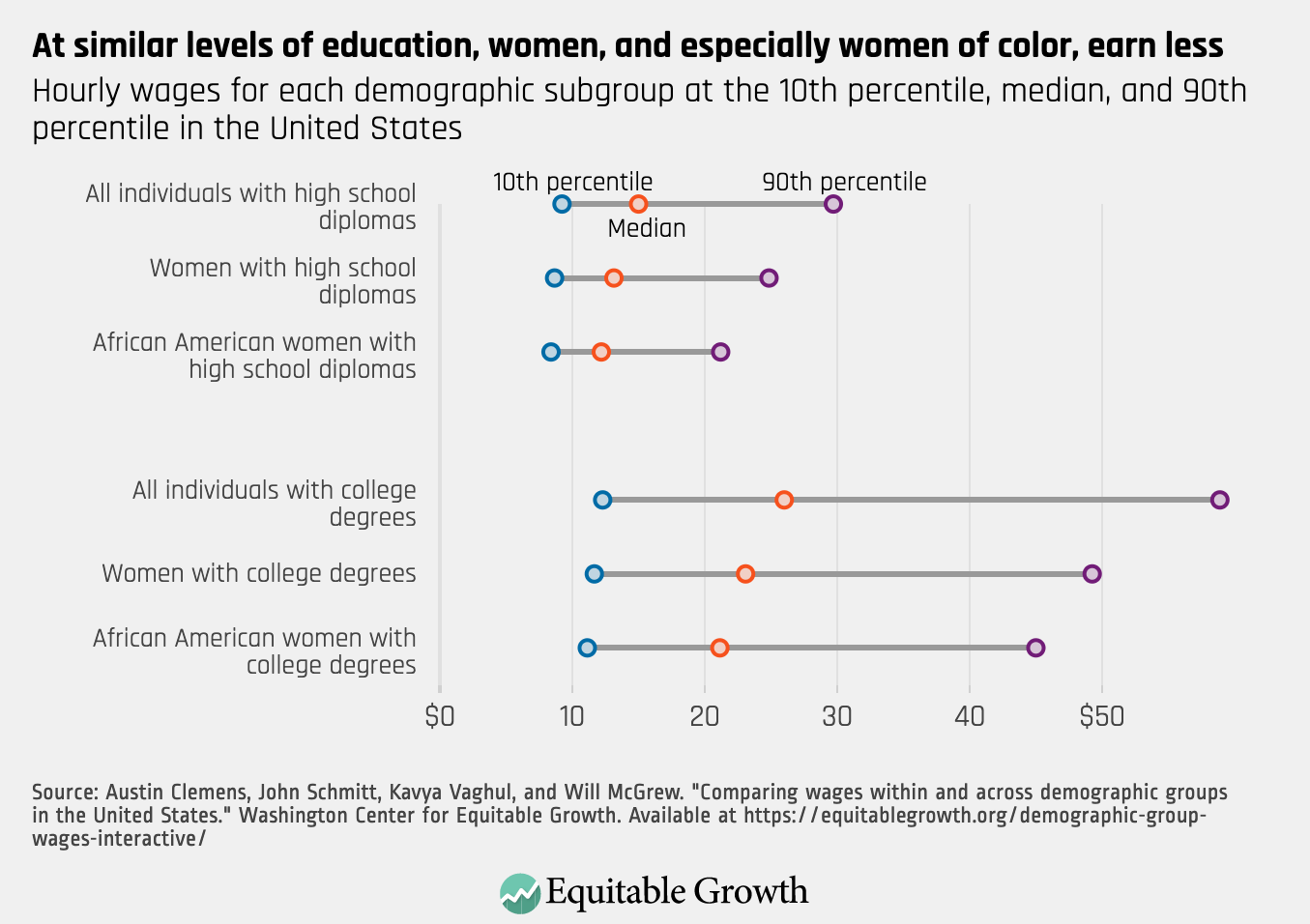

Underlying these broad income inequities in the United States is long-standing and ongoing racial inequity that results in people of color, and especially women of color, having lower salaries than white and male workers at similar levels of education. Not all of this gap is due to discrimination, but significant portions of it remain unexplained and are generally attributed to discrimination. (See Figure 4.)

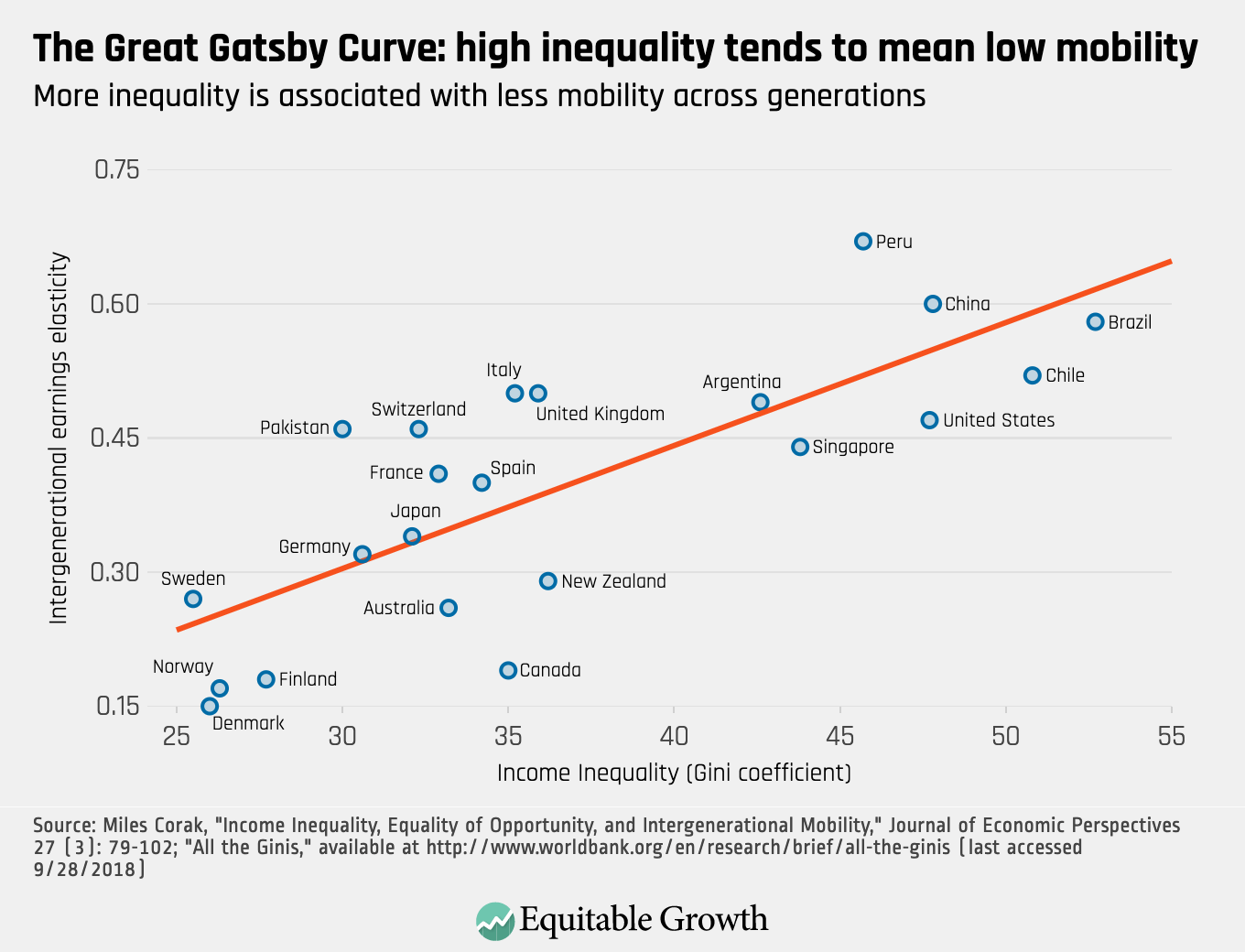

In fact, economic inequality and low economic mobility appear to occur together frequently. The next graph was first produced by City University of New York economist Miles Corak and has since been dubbed “The Great Gatsby Curve.” It demonstrates that there is a correlation between inequality and weak mobility across countries. (See Figure 6.)

Figure 6

Gulfs in outcomes between the rich and poor

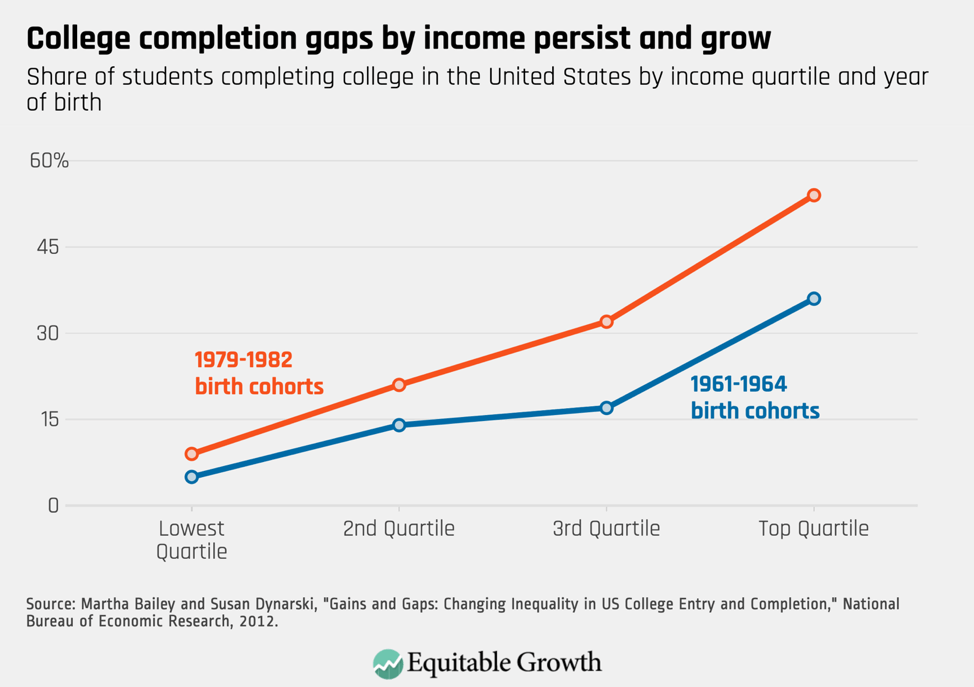

As economic inequality increases, the lives of the rich and poor are diverging. This is true across many metrics, but two examples are telling. First, the rich in the United States are significantly more likely to complete college, and this gap has risen with inequality. The child of a top quartile family is now 45 percentage points more likely to complete college than the child of a bottom quartile family, reinforcing the income mobility problems discussed above. (See Figure 7.)

Figure 7

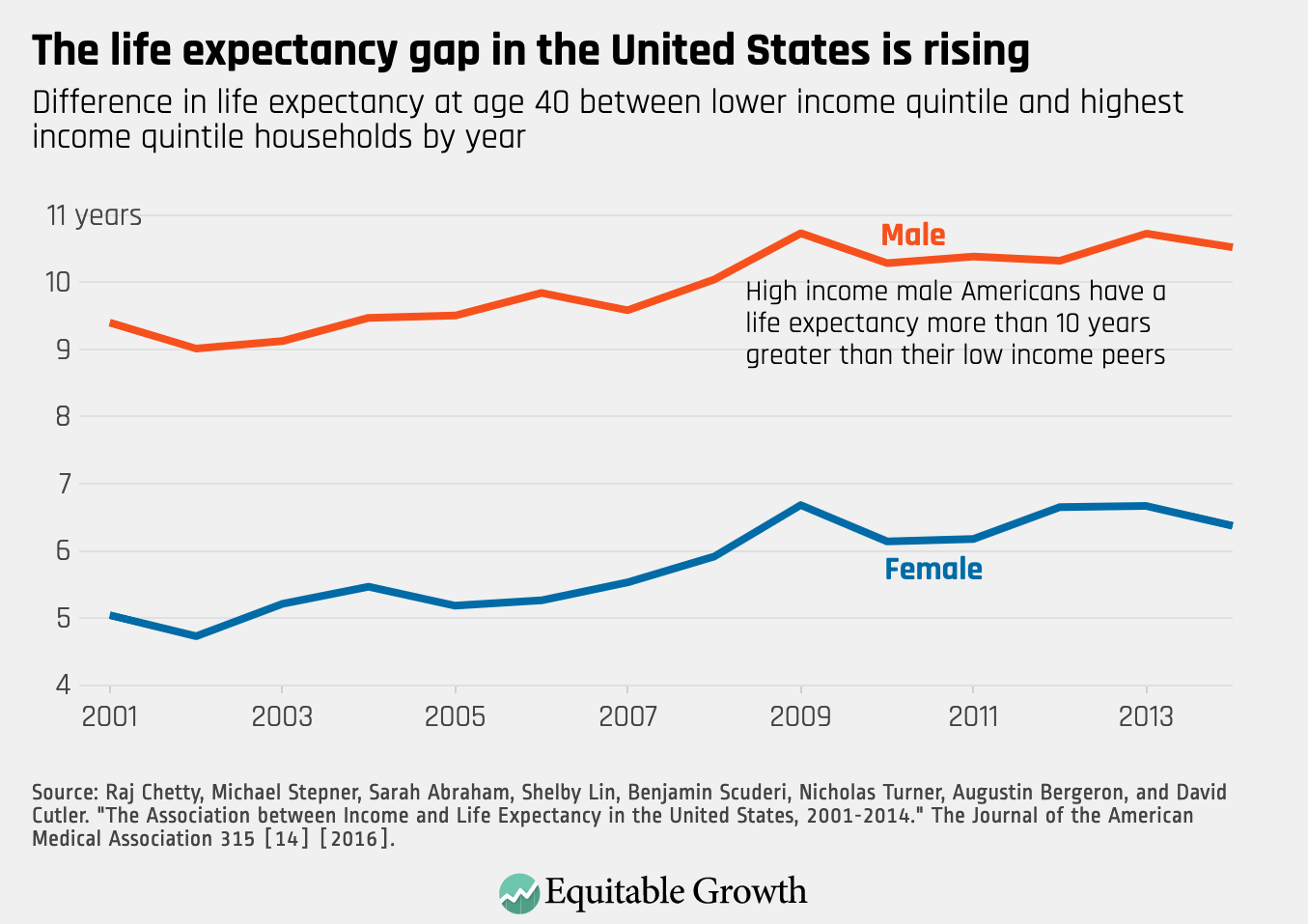

Wealth also buys a longer lifespan. Research by Raj Chetty and others shows that the gap in life expectancy between the very poorest and richest Americans is 15 years for males and 10 years for females. Notably, the gap has grown slightly for both males and females over just a 13-year period. (See Figure 8.)

Figure 8

Questions about whether and how this rise in inequality affects economic growth and stability are fundamental to Equitable Growth’s work. This is why we explore how economic inequality impacts individuals and families across a wide range of issues, and what policies might address these challenges.

This is a post we publish each Friday with links to articles that touch on economic inequality and growth. The first section is a round-up of what Equitable Growth published this week and the second is relevant and interesting articles we’re highlighting from elsewhere. We won’t be the first to share these articles, but we hope by taking a look back at the whole week, we can put them in context.

Equitable Growth round-up

In the lead-up to the 2020 presidential election, Equitable Growth is engaging in a number of activities to help focus the national debate on how to achieve strong, stable, and broad-based economic growth. Last month, we hosted a day-long policy conference in Washington, D.C., entitled “Vision 2020” that featured leading thinkers and activists addressing a broad range of important issues. We posted a column describing the themes that weaved through the various conversations and containing links to video excerpts. Equitable Growth also announced the forthcoming publication of a book containing 21 essays by an impressive list of authors, including some of the conference participants, exploring recent transformative shifts in economic thinking that demonstrate how inequality obstructs, subverts, and distorts broadly shared economic growth, as well as what can be done to fix it.

Raksha Kopparam reminds policymakers that there is a direct relationship between economic inequality and a significant decline in the intergenerational economic mobility that was once a hallmark of U.S. society. Restoring mobility should be a priority for policymakers, and measuring economic inequality can tell us where policies need to be focused. For too long, government has focused on Gross Domestic Product growth as the primary measure of economic success, without examining whether that growth is broadly shared. Kopparam points to Equitable Growth’s GDP 2.0 initiative, which has helped convince the federal government not to track the growth of GDP only, but to track who benefits from that growth.

The U.S. Bureau of Labor Statistics today issued its monthly report on the U.S. labor market for November. The employment rate for prime-age workers held steady and the unemployment and underemployment rates continued their downward trend, but year-over-year wage growth, while slowly rising, remains tepid, given near-historic low levels of unemployment and a significant number of jobs added in November. Raksha Kopparam and Kate Bahn compiled five graphs on the report that show both rosy and not-so-rosy developments in the U.S. economy.

Equitable Growth posted a working paper by Will Dobbie of Harvard University and Jae Song of the Social Security Administration describing a field experiment designed to deepen understanding of how debt contributes to financial distress. Their findings about the impact of long-term debt “run counter to the widespread view that financial distress is largely the result of short-run constraints.”

And be sure to check out Brad DeLong’s worthy reads, which provide Brad’s takes on content from Equitable Growth and elsewhere.

Links from around the web

Tim Wu in The New York Times writes about the struggles of local hardware stores competing with Amazon.com Inc., and asks the question: “Why is a less efficient, less personalized and more wasteful way of buying screws and plungers—ordering online—displacing the local hardware store?” Telling the story of the hardware store in his own New York City neighborhood, Wu says that both the illusion of greater convenience in online shopping and a significant rent increase “reflect the transformative consolidation and centralization of the American economy since the 1990s, which have made the economy less open to individual entrepreneurship.”

While we’re on the subject of paid leave, The New York Times’s Claire Cain Millerasks why men say they want paid leave but then don’t use all of it. She cites reports by New America and the Boston College Center for Work and Family. The reasons seem to be a combination of financial considerations and the persistence of societal gender role expectations.

Matthew Boesler of Bloomberg reports that Neel Kashkari, the president of the Federal Reserve Bank of Minneapolis, who believes the Fed can do more to combat inequality, has recruited an ally to help advance his agenda of reducing inequality in the U.S. economy. He has hired Abigail Wozniak, former senior economist to the White House Council of Economic Advisers and also an Equitable Growth grantee, to serve as first head of the Minneapolis Fed’s Opportunity and Inclusive Growth Institute.

Finally, policymakers and workers alike are well aware of how technological changes have been a key factor in diminishing job opportunities for factory workers, but there’s another significant group of workers deeply affected by technological progress: administrative assistants. Heather Long of The Washington Postwrites, “The United States has shed over 2.1 million administrative and office support jobs since 2000, Labor Department data show, eroding what for decades had been a reliable path to the middle class for women without college degrees.”

If you haven’t read Heather Boushey’s new book, Unbound: How Inequality Constricts Our Economy and What We Can Do About It, then you should. She writes: “Do Americans really have to choose between equality and prosperity? … [Would] reducing economic inequality … require such heavy-handed interference with market forces that it would stifle economic growth[?] … Nothing could be further from the truth … Cutting-edge economics … shows how today’s inequality has become a drag on growth and an impediment to free market efficiency … [There are] deep problems in the U.S. economy, but … policymakers can preserve the best of our economic and political traditions, and improve on them.”

Solvency crises, not liquidity crises, underpin the substantial bulk of Americans’ financial distress experiences. Read Will Dobbie and Jae Song, “Targeted Debt Relief and the Origins of Financial Distress: Experimental Evidence from Distressed Credit Card Borrowers,” in which they write: “We study the drivers of financial distress using a large-scale field experiment that offered randomly selected borrowers a combination of (i) immediate payment reductions to target short-run liquidity constraints and (ii) delayed interest write-downs to target long-run debt constraints. We identify the separate effects of the payment reductions and interest write-downs using both the experiment and cross-sectional variation in treatment intensity. We find that the interest write-downs significantly improved both financial and labor market outcomes, despite not taking effect for three to five years. In sharp contrast, there were no positive effects of the more immediate payment reductions. These results run counter to the widespread view that financial distress is largely the result of short-run constraints.”

In a world riddled by frequent and deep business-cycle recessions, work requirements for safety-net programs are a really bad idea. Read Hilary Hoynes and Diane Whitmore Schanzenbach, “Strengthening SNAP as an Automatic Stabilizer,” in which they write: “The Supplemental Nutrition Assistance Program (SNAP) is a universal program with eligibility criteria based on household income, allowing it to expand automatically when the economy contracts and vice versa. Unfortunately, this stabilization feature is often limited by work requirements for SNAP eligibility, which restrict benefits for some workers who lose their jobs or otherwise experience labor market volatility during recessions … Two reforms [would] strengthen SNAP as an automatic stabilizer. First … either limiting SNAP work requirements—by automatically removing work requirements during downturns—or eliminating work requirements altogether. Second … an automatic 15 percent increase in SNAP benefits during recessions.”

It is a great pity that Steve Greenhouse’s generation of labor reporters at major media institutions was the last. When they retired, the slots were cut. Read Zephyr Teachout, “Review of Steven Greenhouse: The Upheaval in the American Workplaces,” in which she writes: “There’s an enormous upheaval in the American workplace right now … Beaten Down, Worked Up [is] the engrossing, character-driven, panoramic new book on the past and present of worker organizing by the former New York Times labor reporter Steven Greenhouse. At the beginning of this decade, less than 7 percent of private-sector workers belonged to a union, and support for organized labor unions was at an all-time low. Corporations were using illegal tactics to stop unionization, tactics unheard-of in other countries, and new hires at the biggest companies were often required to watch anti-labor propaganda depicting unions as greedy and self-interested … The “Fight for $15” was born, leading to huge rallies and predawn fast-food walkouts across the country. The workers lacked union protection, and big corporations shelled out cash telling lawmakers that raising the wage would cause small businesses to collapse and result in economic disaster. Nonetheless, the workers won. A wave of minimum wage raises passed. In New York, the rate hit the magic number of $15 an hour. Those 2012 meetings and the Fight for $15 almost didn’t happen; this was not the kind of organizing work that labor unions like S.E.I.U. had been doing for decades. This required unions to spend money on organizing people who would most likely never pay dues. You’ll have to read Greenhouse’s book to learn why the union did it, and how a $50 million failure by one of the country’s biggest unions led to one of its greatest recent successes.”

I was surprised to find, in some circles, a strange lack of enthusiasm for the Banerjee-Duflo-Kremer Economics Nobel Prize. Here is some necessary and important pushback against this lack of enthusiasm. Read Oriana Bandiera, “Alleviating Poverty with Experimental Research: The 2019 Nobel Laureates,” in which she writes: “The 2019 Nobel Prize in Economic Sciences has been jointly awarded to Abhijit Banerjee, Esther Duflo, and Michael Kremer “for their experimental approach to alleviating global poverty.” This column discusses the new laureates’ vision and their common interest in both understanding and addressing the persistence of poverty and the huge differences in living standards across countries … Development economics had no Ph.D. courses, no group at the NBER or CEPR, and hardly any publications in top journals until the early 2000s. What this year’s Nobel laureates did was to build the infrastructure to make fieldwork widely accessible and the methods to make the analysis credible. What they did, and what they were awarded for, is to put development economics back on center stage. The prize to Abhijit Banerjee, Esther Duflo, and Michael Kremer is unusual in many ways. Passionate about statistical trivia, the economist on the street will quickly point out that the three are very young, that Esther Duflo is only the second woman to win it, and that she is the youngest ever economics laureate. This is indeed unusual—but it is largely irrelevant. What is unusual and relevant is that the nomination explicitly mentions that the winners lead a group effort.”

What the researchers call, I think somewhat unfortunately, “non-cognitive routine” work is a puzzle for us as we try to look into the future. We used to know what this very large and very important category of jobs was: staple crop farming, or simple craftwork, and later factory work on an assembly line or moving items or boxes in a distribution channel. There still is a lot of this work in distribution channels and in construction, but we can foresee this category of employment shrinking rapidly in the next generation, and we are having a hard time imagining what other jobs in this category will rise. Read Beth Gutelius and Nik Theodore, “The Future of Warehouse Work: Technological Change in the U.S. Logistics Industry,” in which they write: “Are “dark” warehouses, humming along without humans, just around the corner? Predictions of dramatic job loss due to technology adoption and automation often highlight warehousing as an industry on the brink of transformation … We project that the industry likely won’t experience dramatic job loss over the next decade, though many workers may see the content and quality of their jobs shift as technologies are adopted for particular tasks. Employers may use technology in ways that decrease the skill requirements of jobs in order to reduce training times and turnover costs. This could create adverse effects on workers, such as wage stagnation and job insecurity. New technologies potentially can curtail monotonous or physically strenuous activities, but depending on how they are implemented, may present new challenges for worker health and safety, employee morale, and turnover. Additionally, electronically mediated forms of monitoring and micro-management threaten to constrain workers’ autonomy and introduce new rigidities into the workplace.”

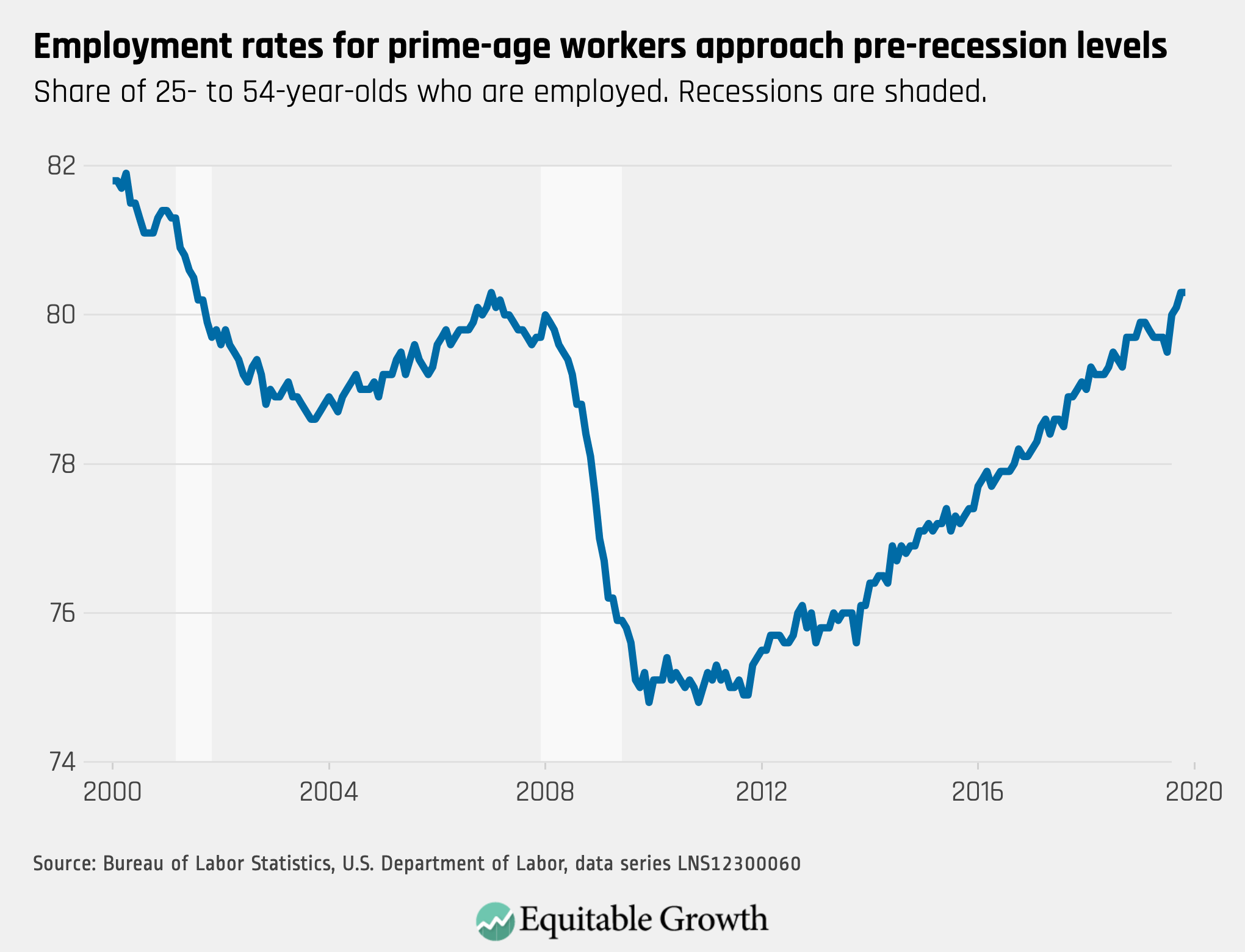

On December 6th, the U.S. Bureau of Labor Statistics released new data on the U.S. labor market during the month of November. Below are five graphs compiled by Equitable Growth staff highlighting important trends in the data.

1.

The employment rate for prime-age workers stayed at 80.3%, holding at it’s pre-recession level for the second month.

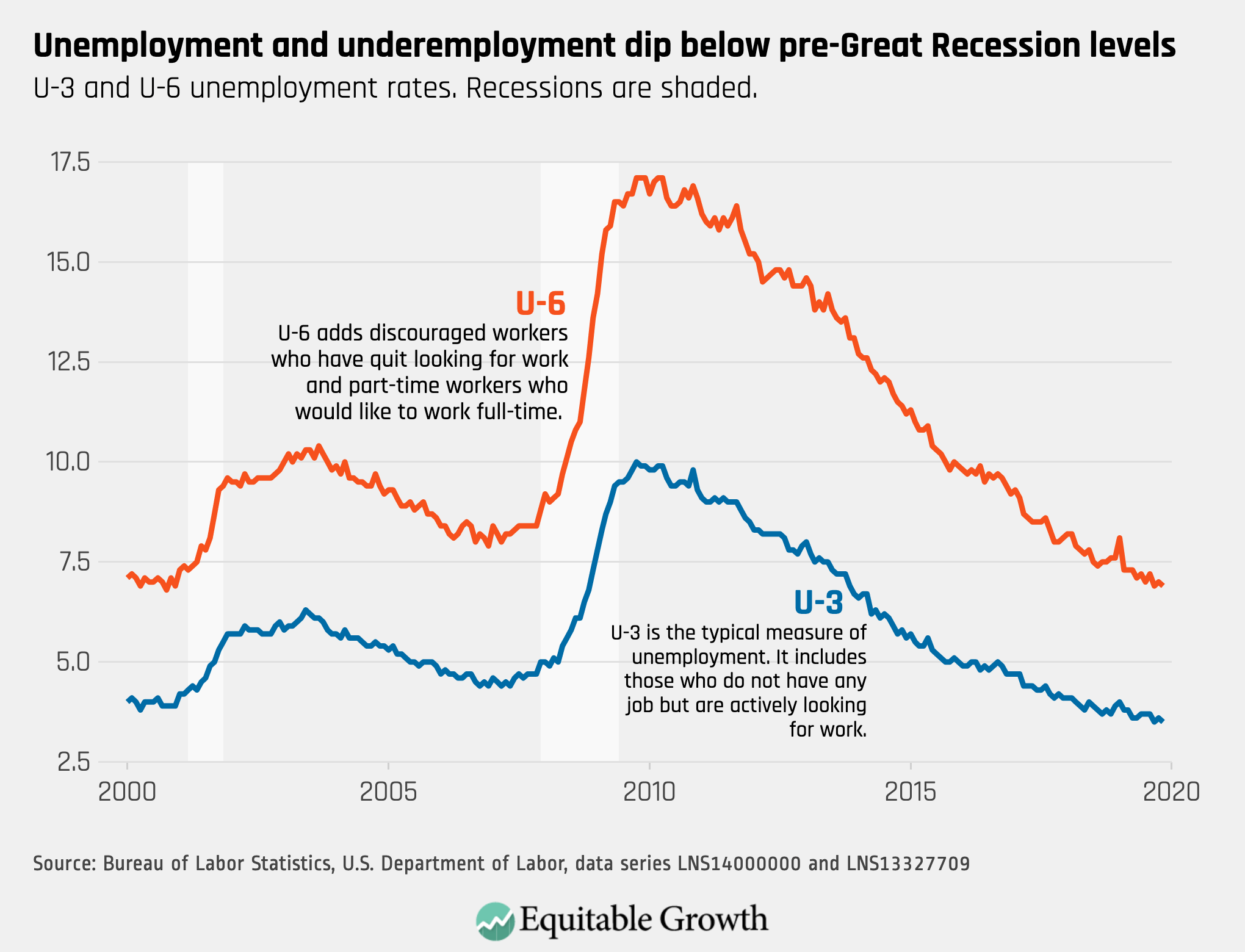

2.

Both the unemployment rate and the underemployment rate trended downward in parallel, reaching 3.5% and 6.9% respectively in November.

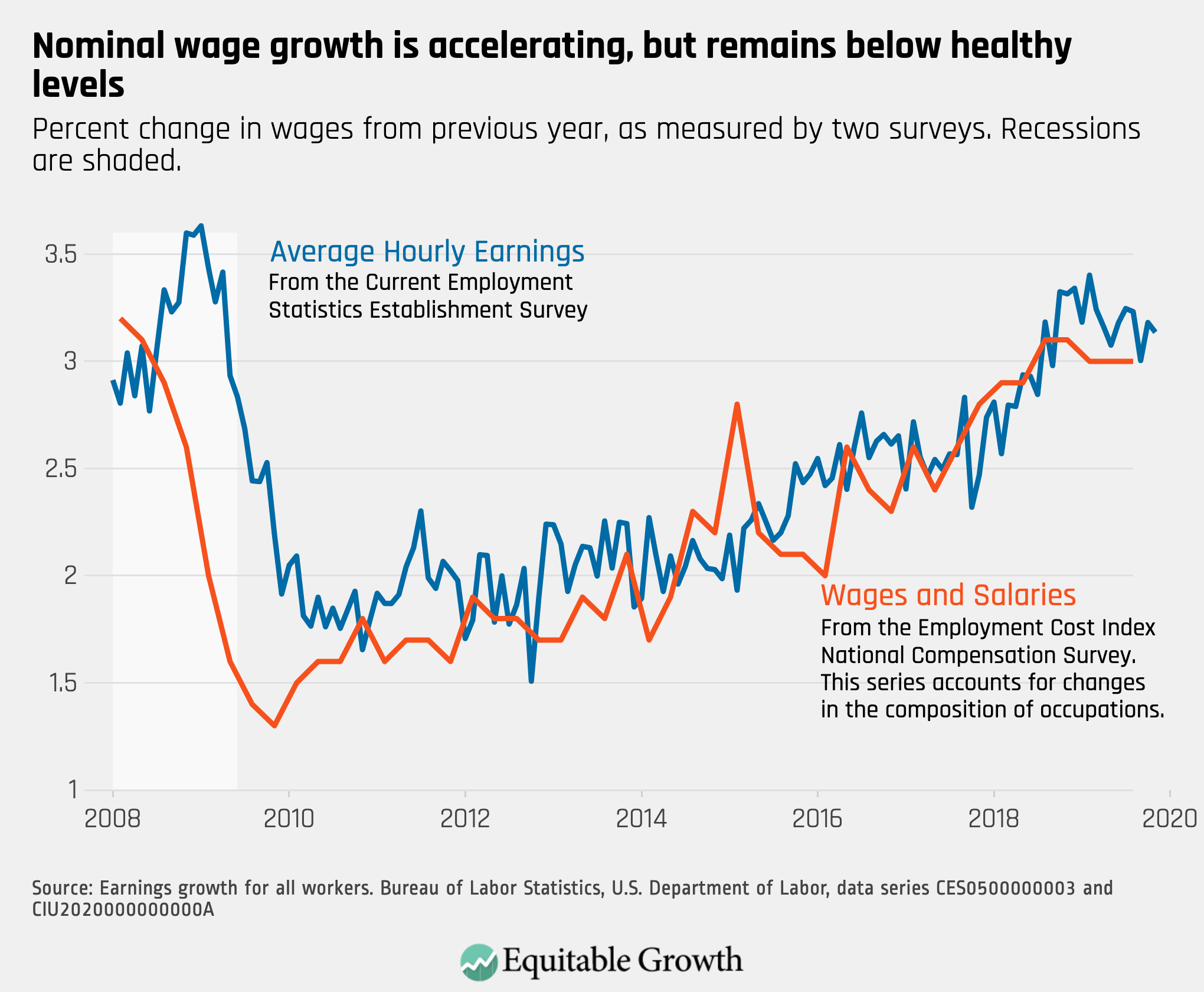

3.

Year-over-year wage growth picked up to 3.1%, but it still remains tepid given near-historic low levels of unemployment and a significant number of jobs added in November.

4.

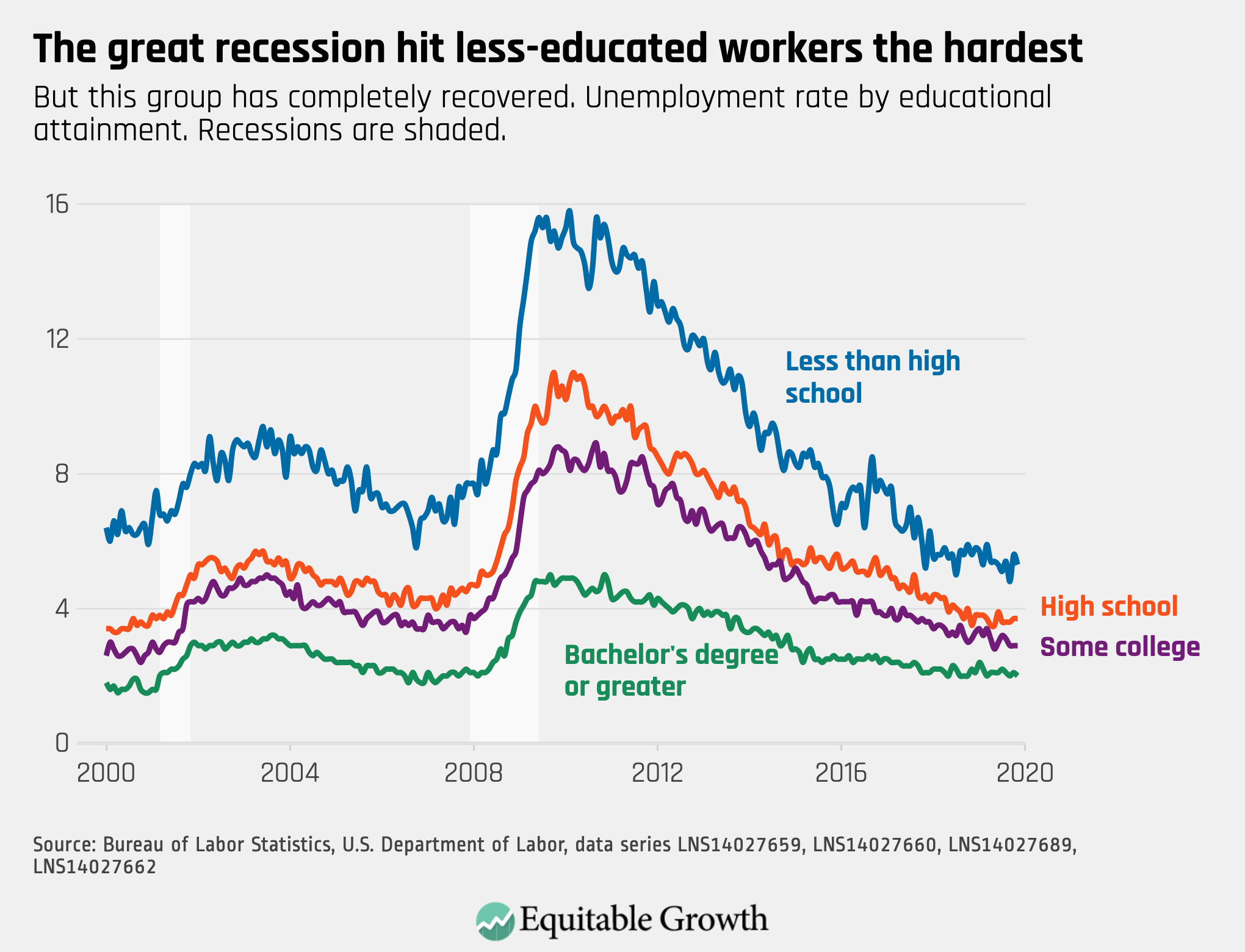

Unemployment remains significantly higher for workers with lower levels of education, but those with less than a high school diploma saw a decline from 5.6% in October to 5.3% in November, after a steep increase from 4.8% in September (amid noisy data in the previous year).

5.

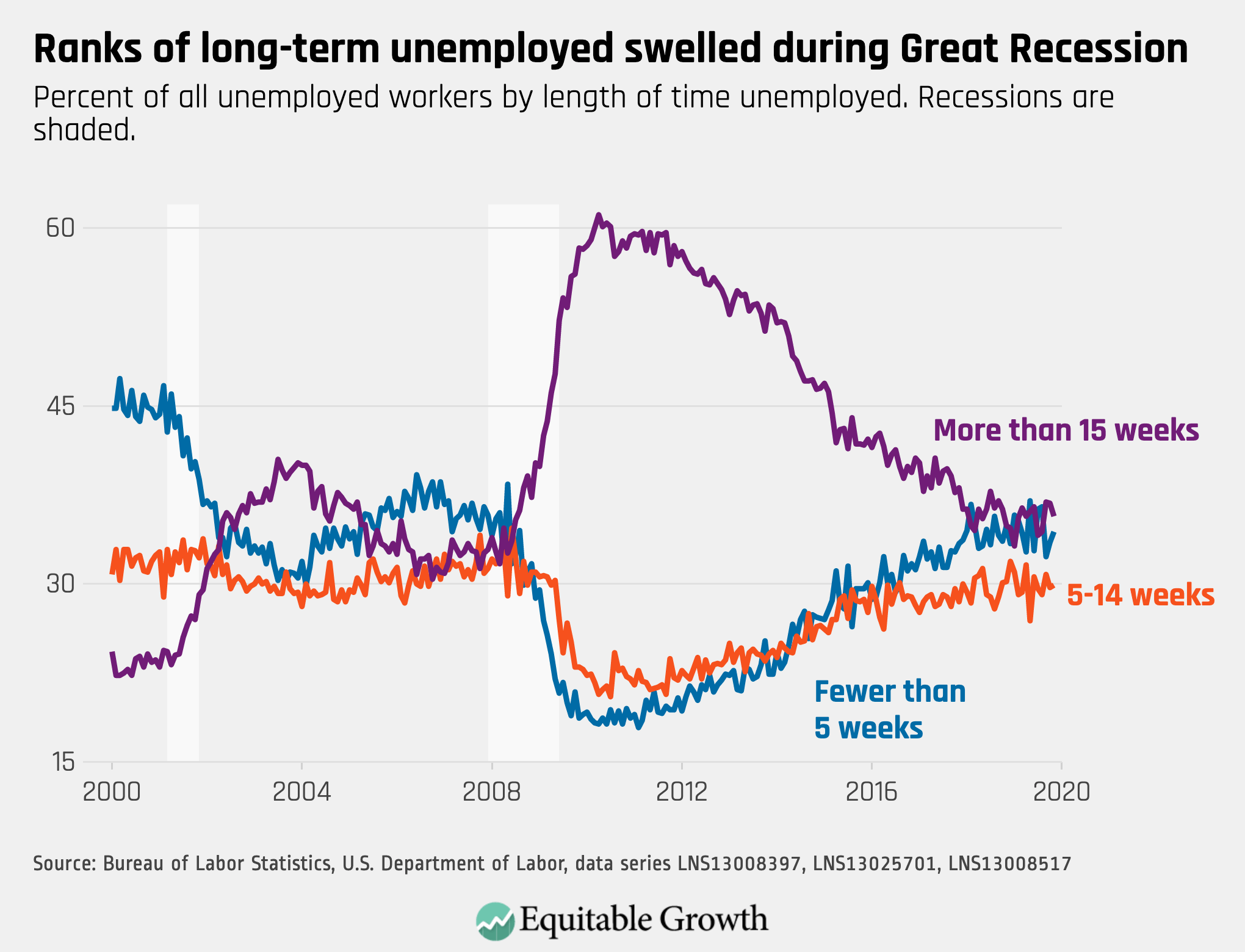

Despite low unemployment and strong job growth, the share of unemployed workers who have been searching for work for more than 15 weeks has not budged, as these workers face significant barriers in finding a new job.

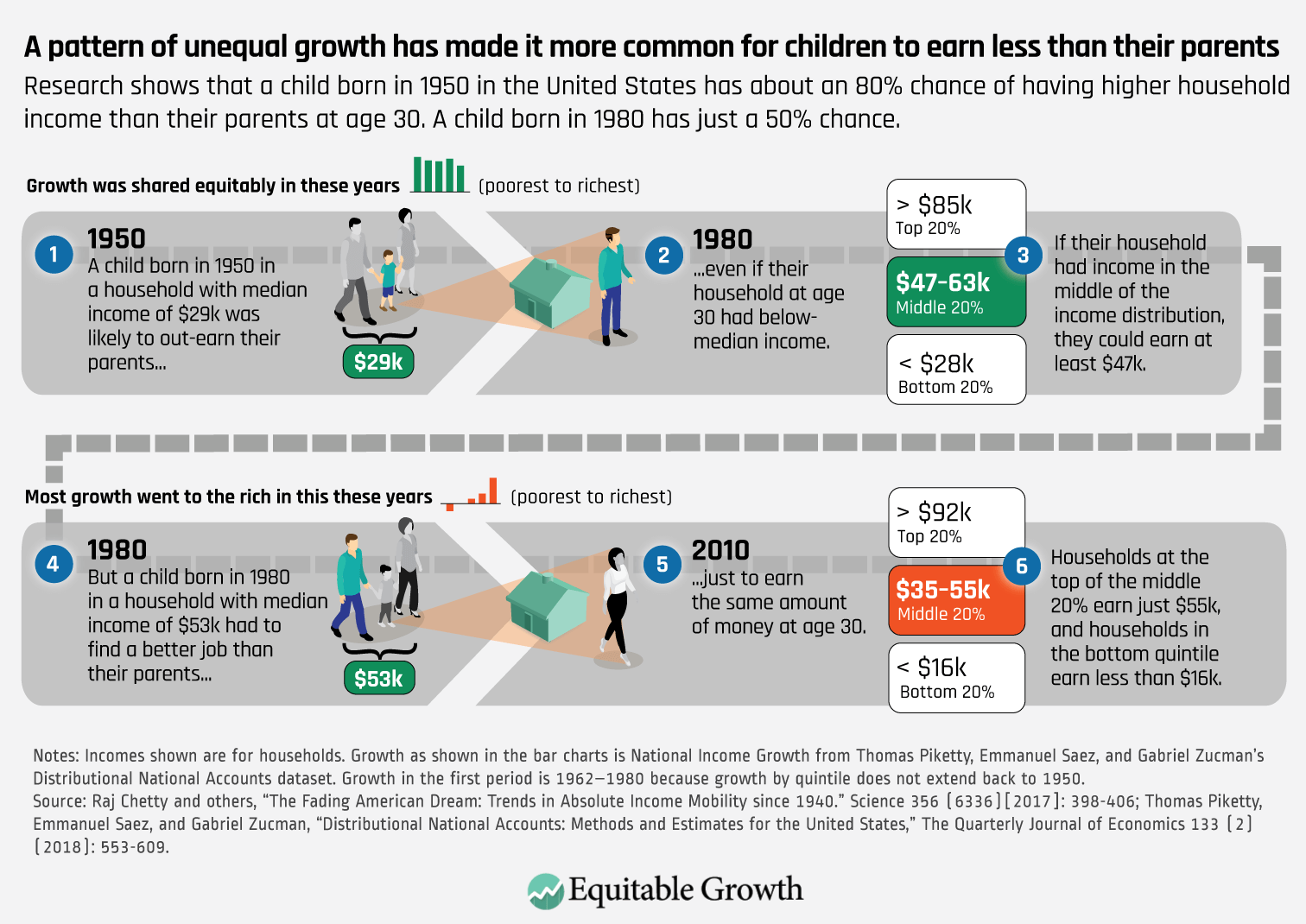

Economic inequality—on the rise since the 1980s—is occurring at the same time that intergenerational mobility is on the decline. Intergenerational mobility measures the relationship between children and their parents’ incomes. Raj Chetty of Harvard University and his co-authors investigated the relationship between intergenerational mobility and economic inequality in the United States in their 2016 article in Science, “The Fading American Dream: Trends in Absolute Income Mobility since 1940.” The authors tracked the economic progress of cohorts of children born between 1940 to 1980 and found that absolute mobility decreased for each successive cohort. In the 1940 cohort, 92 percent of children earned more than their parents. However, by the time the 1980 cohort turned 30 years old, only 50 percent of them were able to do the same.

We visualize this declining mobility in the infographic below using the economic paths of two children, one born in 1950 and the other born in 1980. If the child born in 1950 grew up in a household with a median income of $29,000 annually, as an adult, that child would be able to out-earn their parents even if they were earning below-median incomes. But the child born in 1980 who grew up in a household earning a median income of $53,000 annually would have to have a better job than their parents in order to out-earn them. That 1980 child could be at the 60th percentile of the income distribution—a full 10 percentage points above their parents’ place in the distribution—and still barely out-earn them with an income of $55,000. The cost of downward mobility has also grown even steeper over time, with children in the 1980 cohort unlucky enough to slip into the bottom fifth of the income distribution, earning less than $16,000 per year versus $28,000 in the earlier cohort. (See Figure 1.)

Figure 1

The bar graphs above each child’s path in Figure 1 above show patterns of growth during the child’s lifetime. The green bars show us that total growth was distributed more or less equally across all five income quintiles for the earlier time period. This era of equitable growth corresponded to the era of upward mobility. Then, the pattern changed over the next three decades. The orange bars, which represent how total growth in the later time period was distributed across those same income quintiles, show how growth was concentrated among the top income earners and was even negative for those at the very bottom. This period of unequally distributed growth is also when we see the lower rates of mobility for the 1980 cohort.

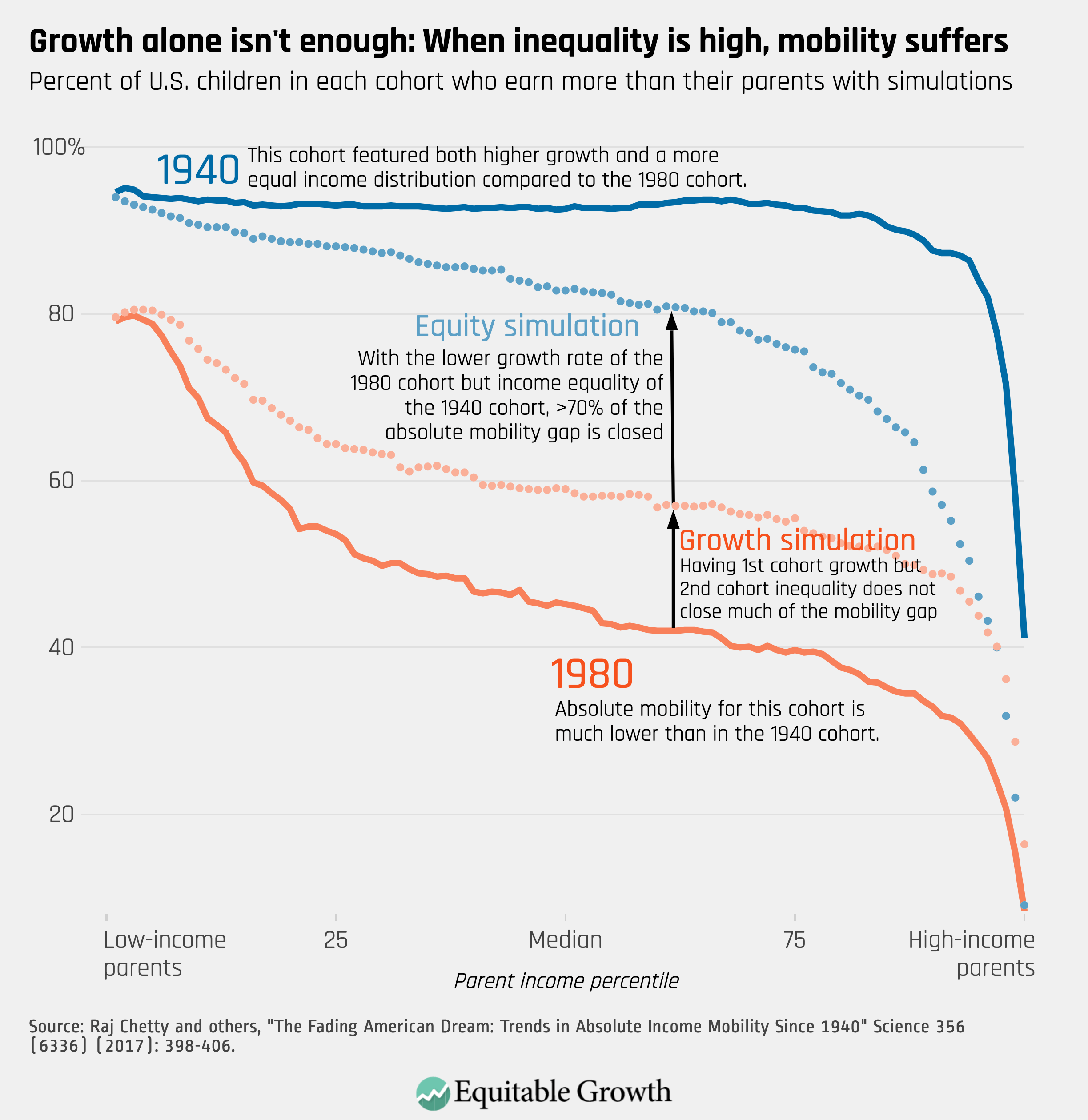

How much did rising inequality versus lower economic growth over the latter time period affect mobility outcomes? Figure 2 below shows the mobility trajectory of kids born in 1940 and 1980. Chetty and his co-authors conducted two counterfactual simulations:

A cohort experiencing the 1940 growth rate and 1980 levels of income inequality, represented by the green line

A cohort experiencing 1940 levels of income inequality and 1980 growth, represented by the purple line

When counterfactual one is applied, the gap between the 1940 cohort and the 1980 cohort closes by only 29 percent, while counterfactual two closes about 70 percent of the gap. (See Figure 2.)

Figure 2

This disparity indicates that addressing economic inequality would have a greater positive effect on intergenerational mobility than would boosting economic growth. As our GDP 2.0 project illustrates, the unequal distribution of growth has made GDP a misleading metric that does not paint a representative picture of how Americans experience and benefit from growth, especially among the bottom half of income earners.

By measuring how growth is distributed, we will be better able to assess how economic growth is impacting households across income levels and who is benefiting from current economic trends. GDP 2.0 statistics would help facilitate the diagnosis of concerning phenomena in the economy, such as indicating falling intergenerational mobility, increases in inequality that could presage weakness in future consumer spending, and that the U.S. economy is not working for every American. These results suggest that policymakers need to prioritize GDP growth that promotes low- and middle-class households, rather than just growth concentrated at the top. Increasing the GDP growth rate alone will not be sufficient enough to restore mobility to the levels witnessed in the 1940s, especially with the current distribution of income.

At our “Vision 2020 conference” last month, the Washington Center for Equitable Growth announced the forthcoming release of a compilation of 21 innovative, evidence-based, and concrete ideas to shape the 2020 policy debate. This compilation of essays into a book, Vision 2020: Evidence for a Stronger Economy, will be released mid-to-late January.

Several of the contributors to this book of essays spoke at the Vision 2020 conference—which brought together leading voices from the policymaking, academic, and advocacy communities to highlight the most pressing economic issues facing Americans today.

Chief among the themes of Vision 2020 are the exploration of recent transformative shifts in economic thinking that demonstrate how inequality obstructs, subverts, and distorts broadly shared economic growth, as well as what can be done to fix it. “Through these essays, the Washington Center for Equitable Growth aims to infuse cutting-edge research findings and prominent academics into the current policy debate,” said David Mitchell, director of external and government relations at Equitable Growth. “Our goal is for future decisions about the U.S. economy to be informed by the best available evidence.”

Essay authors who spoke at the Vision 2020 conference include:

Heather Boushey, president and CEO of the Washington Center for Equitable Growth, who will write about new ways to measure the economy

Arindrajit Dube, professor of economics at the University of Massachusetts Amherst, who will write about minimum wage and sectoral wage boards

Dania Francis, assistant professor of economics at the University of Massachusetts Boston, who will write about reparations

Bradley Hardy, associate professor of public administration and policy at American University, who will write about race and economic mobility

Alexander Hertel-Fernandez, assistant professor of international and public affairs at Columbia University, who will write about labor unions

Additional contributors to the essay compilation and their topics include:

Kimberly Clausing, professor of economics at Reed College, on trade policy

Robynn Cox, assistant professor of social work at the University of Southern California, on criminal justice policy

Blythe George, post-doctoral sociologist at the University of California, Berkeley, on Native American resilience in the face of incarceration and drug use

Darrick Hamilton, professor of public affairs at The Ohio State University, and Naomi Zewde, assistant professor of public health and health policy at The City University of New York, on student debt

Aaron Kesselheim, professor of medicine at Harvard University, on prescription drug costs

Susan Lambert, professor of social service and administration at University of Chicago, on stable scheduling in the workplace

Yair Listokin, professor of law at Yale University, on macroeconomics and the law

Trevon Logan, professor of economics at The Ohio State University, and American University’s Hardy, on race and economic mobility

Taryn Morrissey, associate professor of public policy at American University, on childcare

Suresh Naidu, professor of economics and international and public affairs at Columbia University, and Sydnee Caldwell, incoming assistant professor of business administration and economics at University of California Berkeley, on U.S. labor market monopsony

Maya Rossin-Slater, assistant professor of health policy at Stanford University, and Jenna Stearns, assistant professor of economics at University of California, Davis, on paid leave

John Sabelhaus, visiting scholar at the Washington Center for Equitable Growth, on fiscal and monetary policy

Diane Schanzenbach, professor of human development and social policy at Northwestern University, and Hilary Hoynes, professor of public policy and economics at the University of California, Berkeley, on the Supplemental Assistance Nutrition Program, on supplemental nutrition assistance

Fiona Scott Morton, professor of economics at Yale University, on antitrust policy

Leah Stokes and Matto Mildenberger, assistant professors in the Department of Political Science and affiliated with the Bren School of Environmental Science & Management at the University of California, Santa Barbara, on climate policy and economic inequality

Emily Wiemers, associate professor of public administration and international affairs at Syracuse University, and Michael Carr, associate professor of economics at University of Massachusetts Boston, on U.S. workers’ earnings instability and mobility

Owen Zidar, associate professor of economics and public affairs at Princeton University, and Eric Zwick, associate professor of finance at the University of Chicago, on income tax reform

For more information on the Vision 2020 conference and to view the recorded panels, click here. To sign up for notifications on upcoming content, including the Vision 2020 essay compilation, and events, click here.

A spirit of optimism about the ability of government to address fundamental issues underlying U.S. economic inequality and a determination to advance evidence-based policies for broad-based economic growth infused an all-day policy event hosted by the Washington Center for Equitable Growth on November 1.

At “Vision 2020: Evidence for a Stronger Economy,” which was designed to help inform economic policy ideas in advance of the 2020 elections, speakers and participants engaged in thoughtful discussion on a number of key topics. Those topics included the effects of the decline of union power, structural racism in the economy, the rise of monopsony power in the labor market, and more.

The speakers at the conference made clear that the depth of structural problems, such as racial and gender income and wealth gaps, the decline of worker power, and economic concentration, make dramatic changes in policy essential, yet they also acknowledged the difficult political, economic, and societal barriers to achieving real change. There are no simple solutions, and inequality has caused the economic and political decks to be stacked against systemic reform.

Attendees heard several major threads woven through the day of panels, speeches, and conversations (to watch video from the day’s session, click here, and for photos, click here).

The first major theme was that the change needed to achieve broad-based economic growth and significantly diminished inequality is not possible without the legislative and regulatory tools of the federal government. This point was made by several speakers. Carmen Rojas, formerly of The Workers Lab, related that her former organization’s efforts to empower workers were initially aimed at getting the private sector to act, but the organization found that “government is actually key to scaling anything that would benefit working people.” She noted that this “should have been obvious, given the history of the labor movement in this country, and unfortunately, it wasn’t.”

Economy in Focus: Building Worker Power

Federal Trade Commissioner Rohit Chopra emphasized the power of the federal government needed to be brought to bear on corporate concentration. The FTC, he said, “should be about confronting massive concentrations of power in our economy, ending conflicts of interest in some of the biggest businesses in our society, going after the practices that diminish workers’ wages and independence, and fundamentally, making sure that the economy is competitive and delivers benefits for everyone who wants to work hard.”

And Harvard University’s Lizabeth Cohen, discussing the political challenges facing supporters of the Green New Deal, pointed to the New Deal implemented by President Franklin Delano Roosevelt in response to the Great Depression, as the “gold standard” for the federal government taking responsibility in a national emergency.

The second major theme of the day was that inequality in the United States has led to the concentration of economic power at the top of the income distribution, which has led to a comparable aggregation of political power. That confluence of power has turned policy in favor of elites and stands in the way of change.

Equitable Growth President and CEO Heather Boushey said that inequality gave those at the top not only economic power but also political power. As inequality has risen, she said, “it’s not just the buying of a particular piece of legislation, but how that concentration of economic resources gives people that political and social power to set the agenda, to decide what it is that we’re going to talk about, what it is that’s important to us.” She added, “How can you have democratically accountable institutions when you have so much concentration of wealth in the hands of individuals and across markets?”

Panel: Toward a New Economy

On this topic, Alexander Hertel-Fernandez of Columbia University also invoked FDR, who, he said, “understood that public policy is a tool for building both economic and political power.” Explaining one of the reasons wages have lagged and unions have declined, Hertel-Fernandez pointed to the post-World War II era when he said, “employers realized that they could use public policy to entrench their economic positions and … since the New Deal … the story of declining worker power is not just one of automatic changes in the economy. Employers have worked in new domains and invested in old domains to change policies in ways that disadvantage workers.”

As Tom Perriello of the Open Society Foundations put it:

I think we need to understand the interrelationships of economic [and] corporate power with democratic power and with racial power. And we see right now an unbelievable concentration of wealth, but that concentration of wealth is able to translate itself into political power that affects the ability to produce results for the very parties or organizations that want to build power by standing up for working-class people, middle-class folks of all races.

He added that there “are very few examples through human history, including American history, of multiracial democracy existing with genuine equality of voice.” He argued that “to sustain that kind of multi-identity democracy is difficult in part because of how those with power can divide in order to prevent the building of power.”

Citing a specific example, Karen Dynan of Harvard University discussed the student debt burden facing millennials, especially people of color, and noted that the problem is not with the federal student loan program in general. College is a worthwhile investment for most students, she said, particularly those from low-income families. But weak regulation, she noted, fails to hold colleges—in particular, private for-profit colleges—accountable for luring students into taking on significant debt and then too often failing to deliver value in the form of college degrees. In the same session, Claudia Sahm, formerly with the Federal Reserve and now the director of macroeconomic policy at Equitable Growth, noted that the victims of for-profit colleges were disproportionately the first in their families to attend college. Both Dynan and Sahm made clear that the for-profit college industry has used its political power to weaken regulation.

Panel: Macroeconomic Implications of Inequality

The third theme, a loss of trust, probed the diminution of Americans’ confidence in institutions—in politics and government, in business, and in the media—resulting from economic anxieties and the concentration of power.

In describing the different political landscapes faced by President Franklin D. Roosevelt and today’s supporters of the Green New Deal, Harvard’s Cohen pointed to the difference in the level of trust among the American people. “The New Deal of the 1930s was most remarkable for how it inspired a generation of Americans to trust the federal government as capable of solving many of the nation’s and their personal problems,” she said. “That confidence would persist during at least three more post-war decades. Today, however, we are in a very different place. Trust in the federal government has eroded.”

Boushey said that inequality subverts trust in institutions, and the people most in need of political and economic change mistrust the ability of government, political parties, and other organizations to support them and their families. It makes the public less willing to pay taxes, she said, because there is less confidence that resources will be spent in ways that make their lives better.

Duke University’s Sarah Bloom Raskin, describing how an increasing number of Americans have lost their economic resilience, or the financial ability to withstand economic shocks, noted that people become alienated from the political system as they lose confidence that it can produce change for them. “As income levels get a match on the political side, we lose a political and a regulatory responsiveness that actually could be doing something to address these questions of resilience,” she said. “People then lose confidence in [actual] solutions to do anything for them.”

Finally, the President of the Services Employees International Union Mary Kay Henry said that this weakening of trust in institutions was affecting the efforts of unions to gain the support of workers.

The fourth theme was that economic anxieties felt by much of the U.S. population are due, in considerable part, to the decline of worker power—the ability, mainly through labor unions, to stand up for higher wages from employers.

In a conversation about the rise of monopsony—when firms, rather than labor markets, set wages—Arindrajit Dube of the University of Massachusetts Amherst said that the most significant trends limiting wages over the past several decades have been the loosening of certain constraints on employers, such as fairness norms, labor unions, and more meaningful minimum wages. Hertel-Fernandez emphasized the inadequacy of the law and of the judiciary to address the “malign neglect” of labor law by employers. He cited the potential revamping of labor laws as an opportunity to find out what workers want in labor organizations. Likewise, Cecilia Muñoz of New America focused on how the nature of work is changing and stressed the need to engage workers in the conversation about how best to empower them to affect work’s future direction. Rojas cited the need to build new models of worker power, using 21st century technology. And the FTC’s Chopra said that he hopes the FTC will bring an antitrust case that focuses on labor market competition, noting that the agency has been too weak with respect to enforcement in this area.

But perhaps the most powerful evocation of how workers are faring in today’s economy was a story told by the SEIU’s Henry, who made the case for workers to be able to organize in entire sectors to combat the increasing concentration in many industries. She told the audience about a hospital worker named Nyla Payton, an employee at the University of Pittsburgh Medical Center. Hospital mergers have given UPMC something close to monopsony power over the labor market for hospital workers in the Pittsburgh region, she said. Henry spoke in detail about how the institution has abused that power to impose egregious working conditions on its workers and prevent them from forming a union.

Fighting Power with Power: Unions for All

The fifth theme of the day was the experience of individuals and families in the U.S. economy as fundamentally different based upon race, ethnicity, and gender.

The economic and political disparities faced by people of color and by women (and especially by women of color) were a major theme throughout the day. Dania Francis of the University of Massachusetts Boston pointed to the impact of the gaping racial wealth gap on human capital investment. She noted that wealth, in addition to being a source to draw on for such investment, is protective (providing shelter from life’s unexpected setbacks), affords opportunities (to be an entrepreneur, to take risks), and perpetuates itself (is intergenerational). “Who are we losing?” she asked.

Similarly, Camille Busette of The Brookings Institution said that the asset creation process “is very racialized.” She pointed to government policies such as redlining, the exclusion of blacks from certain kinds of jobs, and other structural issues built upon existing disparities to contribute greatly to the racial wealth gap. Even for African Americans who owned homes before the 2007 financial crisis, a disproportionate amount of those were bought using subprime loans, so they were set up to fail, and those assets disappeared. “The reason that we have a racial wealth gap,” she said, “is that we have racism.”

In the same session, Opportunity at Work’s Byron Auguste discussed the skills gap, pointing out that if employers wanted more workers in a particular field, then they could raise compensation for those jobs. He also said that the conversation about the skills gap misses a key point. “We’re thinking about the skills gap backwards,” he argued. “The skills gap is the consequence of an opportunity gap … it’s not the cause.” He said that artificial credentials requirements for certain jobs, such as a bachelor’s degree for office administrative assistants, tended to exclude black workers.

Bucknell University’s Nina Banks told the story of Sadie Alexander, who, in 1921, became the first African American woman to receive a Ph.D. in economics in the United States (at the University of Pennsylvania). Since nobody would hire her, she went on to earn a law degree at UPenn as well and became one of the leading civil rights voices challenging the legacy of slavery. She did so from the point of view of an economist. Concerned about the status of African American workers—who were frequently the last hired and therefore first fired—she focused on the need for full employment policies and was possibly the first economist to advocate a federal jobs guarantee, a policy idea that is enjoying renewed attention in the current economic and political debate.

And finally, the last theme of the day was elicited by the session moderators, as well as through audience questions, which asked for evidence-based policy recommendations from the panelists and speakers. Among them were the following:

Bradley Hardy of American University pointed to the need to direct considerably greater public resources into education, safety net programs, skills training, and other programs critical to building human capital.

Monica Garcia-Perez of St. Cloud State University urged policymakers not to focus only on the job market. She said it was a symptom, not the fundamental problem. She called for wellness benefits such as health insurance and retirement to be separated from jobs, so that individuals and families could receive them regardless of whether they are employed.

Maya Rockeymoore Cummings of Global Policy Solutions said the policy changes that were most needed were programs that support families along the continuum of life, such as paid family leave, universal childcare, and long-term care, and while expressing strong support for Social Security, pointed to the need to strengthen other retirement benefits to provide greater income to seniors.

Francis called for a program of reparations that includes a direct transfer of resources in order to help African Americans reduce the wealth gap created by the legacy of slavery, Jim Crow laws, and other state-sanctioned discrimination.

Henry, in addition to supporting sectoral collective bargaining, which is the norm in many European countries, called for “a new American social wage” that includes benefits such as healthcare, childcare, parental leave, vacation, and pension support. Similarly, Dube called for sectoral wage standards and for wage boards to enforce them.

Auguste noted the need for greater income support for those learning new skills to improve their status in the job market, and for student loan forgiveness in unusual circumstances such as the financial crisis.

Busette called for the elimination of the juvenile justice system, which she said has a deeply negative, lifelong impact on countless African American boys.

Dynan and Sahm stressed the need for policies to inject money into the U.S. economy when a recession is beginning by providing benefits to low- and middle-income Americans, who are most likely to spend those resources. Sahm pointed to the proposals contained in Recession Ready, a book of ideas compiled by Equitable Growth and the Hamilton Project.

These and other policy ideas will be compiled into a collection of 20 innovative, evidence-based, and concrete ideas to shape the 2020 policy debate, which Equitable Growth’s Director of External and Government Relations David Mitchell announced will be published in January by Equitable Growth. Several of the speakers at “Vision 2020” are among the academics who are contributing essays.

This is a post we publish each Friday with links to articles that touch on economic inequality and growth. The first section is a round-up of what Equitable Growth published this week and the second is relevant and interesting articles we’re highlighting from elsewhere. We won’t be the first to share these articles, but we hope by taking a look back at the whole week, we can put them in context.

Equitable Growth round-up

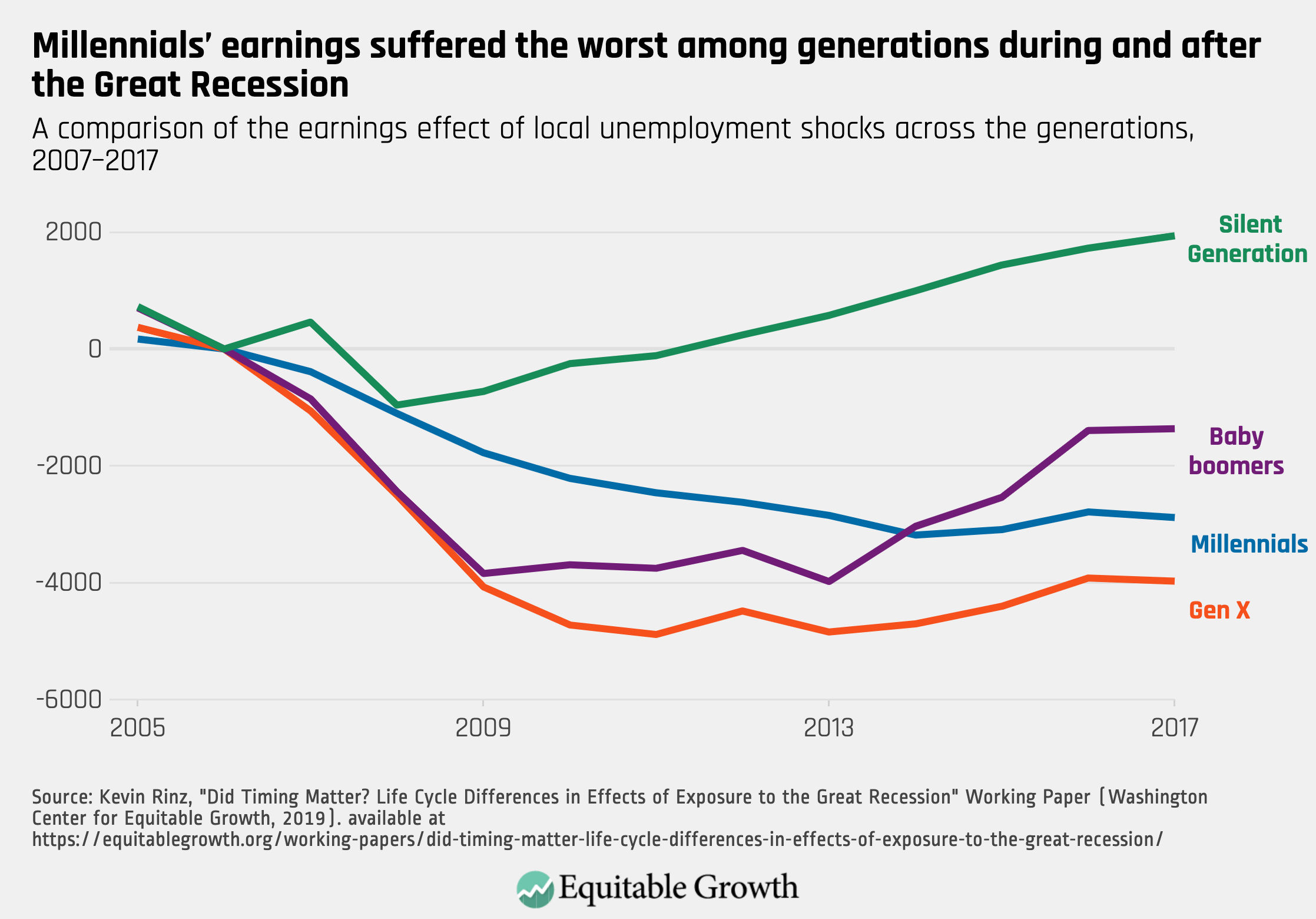

Apparently, the time for niceties between generations has come to a close with just two words: “OK, boomer.” The phrase is being thrown around like a new four-letter word on the internet, while new research from Equitable Growth shows that perhaps there’s an economic undertone to this latest intergenerational animosity: Millennial workers have not fared as well in the post-Great Recession period as other working-age groups. As Kate Bahn writes in a post about the research, local unemployment shocks during the Great Recession had a negative impact on the employment of all age cohorts, but millennials (defined as those born between 1980–1994) were the most negatively affected. Millennials’ earnings also suffered the worst during and after the Great Recession, compared to other generations, and they are less likely to be working for a high-paying employer today. These persistent negative outcomes for millennials demonstrate “how inequality reduces economic opportunity for those who have less to start with in terms of jobs and earnings” and how a tight labor market doesn’t necessarily translate into positive economic outcomes for all workers, writes Bahn.

Three recent reports—one from the Stigler Center, one commissioned by the United Kingdom, and one to the European Commission—examine antitrust and competition issues in the digital arena. Michael Kades discusses each report in detail, providing an overview of current digital market conditions, what that means for competition online, and potential remedies to some of the biggest issues facing digital market competition: the acquisition of nascent competitors and online platform discrimination. Kades writes that “a combination of antitrust enforcement and competition-enhancing regulations likely provides the best path forward to exploiting the benefits of these markets while limiting the dangers they pose for competition.” His column summarizes the paper about these three reports that he submitted to the American Bar Association’s Fall Forum.

Check out Brad DeLong’s latest worthy reads for his takes on recent Equitable Growth content and posts from around the web.

Links from around the web

A new study indicates that a higher minimum wage does not lead to higher unemployment, writes Dylan Matthews in an explainer on raising the wage floor for Vox.com. Matthews summarizes the recent research, which finds that “even if a few workers lose jobs, those costs are significantly outstripped by increased wages for workers who keep their jobs.” Matthews points out, however, that some economists remain skeptical, particularly regarding long-term effects on job growth and the level to which the minimum wage is raised. The disagreements and varying research results point to larger structural forces, Matthews concludes: “There are big monied interests opposed to minimum wage increases, and smaller but real monied interests (specifically unions) supportive of them.”

For all the talk of late about wealth taxes and fighting billionaires, writes Noah Smith for Bloomberg, you’d think the number of ultra-wealthy people had skyrocketed in the past few years alone. Wealth inequality has been high in the United States for decades, so Smith asks, where did all this class resentment come from? It probably has its roots in the bursting of the housing bubble, he argues, when the vast majority of the country lost everything they had been saving, but the wealthy largely made it through with barely a scratch. This immunity to financial setbacks highlights how rare it is these days for wealthy people to lose their fortunes just like the rest of us, Smith writes—and why policymakers looking to avoid class conflicts should support ideas that will help reduce financial risks for the middle class.

Republicans have now come up with a plan for paid family leave, which has long been a policy for which Democrats have fought. If both sides want it, then what’s the hold up? Claire Cain Miller of The New York Times’ The Upshot argues that the big divide between the two parties is over which workers would gain access to the paid leave, and where the money to pay for it would come from. Generally, she explains, Democrats want to create a new federal fund, financed by a payroll tax increase, that covers paid leave for new parents and workers needing time to care for their own serious illness or that of a family member. Republicans support using people’s existing Social Security benefits to cover leave for new parents and reducing the amount they’d then receive when they retire—essentially, treating Social Security like an individual account more than a larger social insurance fund. There have been a flurry of bills proposed in Congress, and the Trump administration has, so far, not taken sides on which one it will back. The administration, however, plans to host a summit on the issue at the White House next month.