Until the public health crisis is addressed, economic activity will not return to anything close to normal.

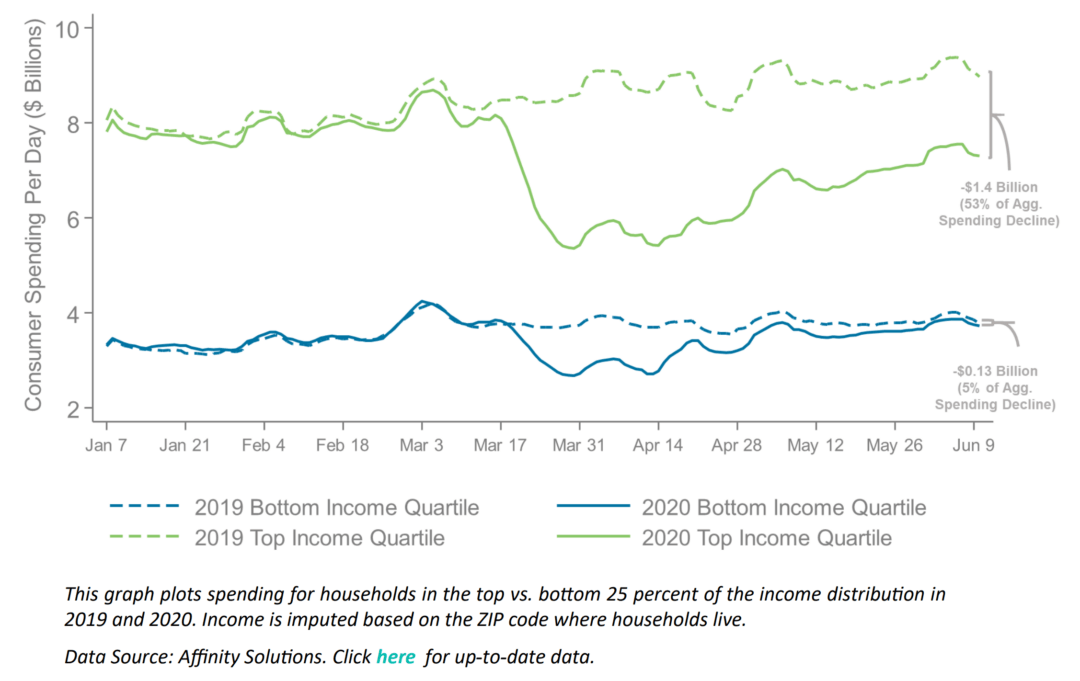

A new working paper released by Harvard University economist and former Equitable Growth Steering Committee member Raj Chetty and his Opportunity Insights colleagues finds that U.S. consumer spending fell dramatically over the past few months, driven by public health and safety concerns due to the novel coronavirus and COVID-19, the disease caused by the virus. These concerns are keeping people, especially those in high-income households, away from purchasing in-person services, indicating that until people feel safe engaging again in in-person services such as dining out or getting haircuts, consumer spending on services—which accounts for 66 percent of all consumer spending—will not meaningfully rebound.

In short, if policymakers want to fix the U.S. economy, then they must first fix the U.S. public health crisis. Merely announcing that the economy is “reopened” will not make it so. In the meantime, Chetty and his co-authors find that investing in social insurance programs—such as the expanded unemployment benefits enacted by Congress in the Coronavirus Aid, Relief, and Economic Security, or CARES, Act—is the best way to mitigate economic suffering during the recession, rather than stimulus measures targeted toward businesses or the rich.

One of the key findings underlying the conclusions in this latest research is that the fall-off in consumer spending is being driven by high-income households, particularly in areas with high rates of COVID-19. The authors find that as of May 31, two-thirds of the total reduction in credit card spending since January was from households in the top 25 percent of the income distribution, whereas spending by households in the bottom quartile had returned to normal levels. (See Figure 1.)

Figure 1

High-income U.S. households have cut back sharply on spending Consumer spending changes during the coronavirus recession, by income group, January 2020–June 2020

This fall-off in spending by the highest-income households is not driven by a decrease in their incomes, but rather because of the decline in in-person services they’re buying, such as dining out, traveling, or haircuts. The authors find that spending on other services and luxury goods that do not require in-person contact—such as the installation of home swimming pools or landscaping services—actually increased slightly since the onset of coronavirus pandemic. This strongly suggests that public health concerns about contracting the novel coronavirus are driving the changes in spending patterns among the highest-income households, which also are more likely to have the luxury of working from home and maintaining self-isolation.

The findings by Chetty and his co-authors should come as no surprise because of what we already know about the differences in spending and savings patterns among low- and high-income households. Research by Harvard University economist and Equitable Growth Steering Committee member Karen Dynan and her co-authors finds that while Americans, on average, save about 20 cents of every dollar they earn and spend the rest, those in the top 5 percent save 37 cents, and those in the top 1 percent save 51 cents. Meanwhile, those in the bottom 20 percent save only one cent of every dollar. That’s because higher-income households earn enough money to actually be able to put some of it aside in savings.

In contrast, because of rising inequality, stagnant wages, and deteriorating public institutions, low-income households have to spend all their income just meeting their basic needs—paying rent, putting food on the table, and securing childcare. Additionally, we know that lower-wage workers’ accumulated savings don’t amount to much of a cushion. Research from the Federal Reserve shows that 40 percent of U.S. adults would have a hard time handling an unexpected bill of $400. The Opportunity Insights research builds on this scholarship by demonstrating that there was less of a coronavirus-related fall-off in low-income households’ spending because there were no fancy restaurant dinners out or Broadway theater tickets to eliminate from their budgets in the first place.

The trend in low-income households’ spending, falling during the second half of March and then gradually returning to close to its original level, is also evidence of the success in government efforts to help replace low-income households’ lost income from coronavirus-related job layoffs. Chetty and his co-authors find that in the week after April 15, when the $1,200 checks enacted by Congress in the CARES Act hit most Americans’ bank accounts, spending by the bottom quartile of households increased by nearly 20 percentage points. Spending by the top quartile increased too, but by not even half as much, consistent with the different spending needs of high- and low-income households, as well as the much higher levels of savings among high-income families discussed above.

Chetty and his co-authors also examine two other recent government policies to prop up consumer spending and employment: state governments’ declarations that they were reopening their economies and the Paycheck Protection Program, a $670 billion effort to provide loans to small businesses that convert to grants if employees are rehired. The researchers find that both of these efforts have had limited effects because they do not address the underlying cause of the fall-off in consumer spending—the public health concerns that are keeping people home, notwithstanding announcements about reopenings.

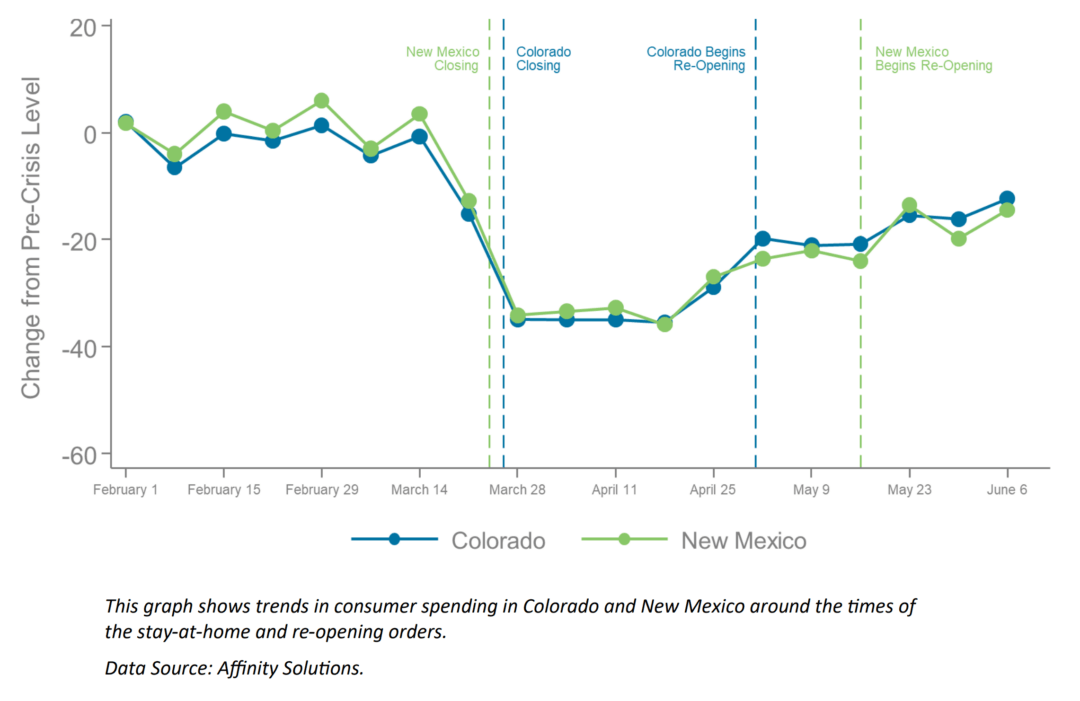

The authors offer a case study of Colorado and New Mexico. These two states issued stay-at-home orders within days of one another in late March, and then Colorado partially reopened its economy May 1 while New Mexico didn’t do so until May 16. Despite this difference in reopening dates, there’s no discernible difference in spending between the two during early May. (See Figure 2.)

Figure 2

Different economic reopening dates did not make a difference in consumer spending Effects of reopening on consumer spending in Colorado and New Mexico, February 2020–June 2020

Source: “How Did COVID-19 and Stabilization Polices Affect Spending and Employment?,” Opportunity Insights

Similarly, the authors’ analysis of the Paycheck Protection Program find it had negligible effects on employment—total payroll at businesses fell by about 40 percent for both small firms eligible under the program and larger firms that weren’t eligible. Instead, the researchers’ analysis found that PPP loans were most likely to go to industries and the areas that were the least likely to experience job losses during the pandemic.

Professional, scientific, and technical services, for example, received a greater share of loans than did accommodation and food-service businesses. This is consistent with research recently highlighted by Equitable Growth from University of North Carolina, Chapel Hill economist T. William Lester, which showed that small, independent restaurants are suffering particularly acutely during the coronavirus recession, with current programs ill-suited to their needs.

The coronavirus and the economic recession it triggered have caused widespread physical and economic suffering. This latest research clearly illustrates that until the public health crisis is addressed, economic activity will not return to anything close to “normal,” regardless of whether state officials declare their economies reopened. Therefore, government efforts to address the public health crisis must be improved.

In the meantime, policymakers should concentrate their efforts not on stimulus measures for the rich or for businesses, but on supporting the incomes of the tens of millions of workers who have lost their jobs, who are far more likely to have been low-income to begin with and have little savings to draw on. Most importantly, this includes extending the additional $600 in Unemployment Insurance benefits contained in the CARES Act, which are set to expire at the end of July.

This extra $600 is the easiest way to ensure that most workers and their families are able to get close to full wage replacement and continue to support themselves during what is increasingly looking like a prolonged economic recession. Other policies, such as providing stimulus for the rich, re-employment bonuses, or credit to businesses, will do little to reduce economic hardship when it is increasingly clear that economic activity simply will not come back while the threat of contagion continues.

Coronavirus recession relief packages now under discussion on Capitol Hill present an opportunity to power an economic rebound and address climate change at the same time. This approach would save American lives. Air pollution from dirty energy infrastructure makes people much more likely to die from COVID-19, the disease caused by the novel coronavirus. And those dying in the United States are more likely to be people of color, in part because dirty fossil fuel infrastructure is overwhelmingly placed in communities of color.

Congress has similarly lagged in promoting green stimulus. For the next round of coronavirus recession relief, some groups propose investing in clean energy programs—such as home retrofits, rooftop solar, and electric buses, all of which could boost the U.S. economy and reduce the pollution that drives climate change and heightens vulnerability to the coronavirus and COVID-19. As our research shows, this policy approach increases popular support for stimulus spending.

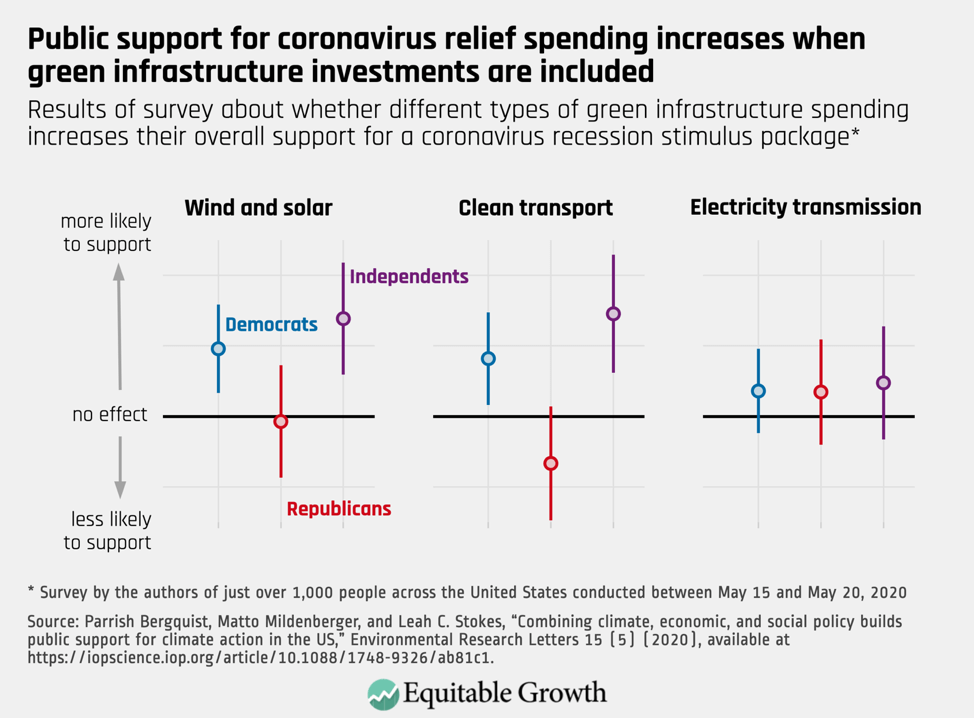

Estimating public support for green stimulus

Whether Congress incorporates green programs into coronavirus relief spending depends, in part, on public support. To investigate public opinion on green stimulus as part of any new relief packages, we launched a nationally representative survey of slightly more than 1,000 people between May 15, 2020 and May 20, 2020. Our survey was fielded online by Qualtrics, a platform that hosts surveys and recruits respondents for researchers. We use quota samples for age, gender, and race to ensure a nationally representative sample. Respondents were weighted to account for remaining demographic imbalances using iterative proportional fitting, also known as raking.

In our survey, some people read about coronavirus relief packages that included climate spending or climate-related standards and regulations. Others saw packages that did not include these policies. Social scientists call this type of experiment a conjoint design—it’s a way to measure people’s preferences when facing complex policy choices. When we analyze our conjoint experiment, we can measure whether each individual component of a policy bundle increases or decreases public support for the overall package.

The public supports green stimulus but not at the expense of broad economic relief

Our experimental results show that including green infrastructure spending increases support for a coronavirus relief package. Support for wind and solar investments and for clean transportation investments is particularly strong. Including these measures increases support by 8.5 percentage points and 6.1 percentage points, respectively. Notably, including electricity transmission investments does not cause a change in support for the package. We visualize these shifts, broken down by Democrats (blue), Republicans (red), and Independents (purple) in Figure 1.

Figure 1

As Figure 1 makes clear, green investments increase support among a broad range of constituencies. This suggests that climate action can and should be included in the next coronavirus recession relief package.

In addition to the experiment, we asked Americans directly whether they think Congress should address coronavirus recession relief funding and climate change together. Despite their revealed support for incorporating green stimulus into any response—as indicated in our experimental results—58 percent of respondents said they think Congress should focus on coronavirus relief spending alone.

This suggests that Americans may view linked solutions as a trade-off that requires sacrifices on one dimension in order to achieve gains on the other. Given the high unemployment rate, which is compounding existing economic inequality, Americans do not support climate programs at the expense of sweeping aid for all Americans.

That said, there need not be a trade-off. As a recent economic analysis from the Sierra Club suggests, a sustained investment in climate action could yield 90 million new jobs over the course of the current decade. There is so much work to do to address the climate crisis. If the federal government focuses on tackling this challenge, it can power economic recovery at the same time.

Americans support this approach. They want Congress to lead the way with green stimulus that will promote broader adoption of clean energy and create good jobs. Congress should seize a politically opportune and popular win-win solution—promoting more equitable economic recovery and addressing climate change simultaneously.

—Parrish Bergquist is a postdoctoral researcher at the Yale Program on Climate Change Communication and an incoming assistant professor of public policy at Georgetown University. Matto Mildenberger is an assistant professor of political science at the University of California, Santa Barbara and the author of Carbon Captured (The MIT Press, 2020). Leah C. Stokes is an assistant professor of political science at the University of California, Santa Barbara and the author of Short Circuiting Policy (Oxford University Press, 2020).

With the United States having just completed a long July 4 weekend while registering more than 2.4 million cases of the novel coronavirus prior to the holiday celebrations, health experts are making it clear that alongside social distancing, wearing protective masks, and ramping up testing, our nation needs more tracking and tracing of cases so that people can be notified and help limit the contagion of others. Unfortunately, the implementation of contact tracing programs has been uneven across the country even though the federal government has provided some funding for contact tracing since late April.

At the same time, more than 44 million Americans have filed for unemployment benefits in less than 4 months. These two dire and worrisome trends—one related to public health and the other economic—also create a singular opportunity. Policymakers could place millions of people searching for work into contact tracing jobs through a modern-day Works Progress Administration, a jobs program first implemented during the Great Depression—the previous time U.S. unemployment was so high.

The public health need is clear. Hospitalizations are up in more than a dozen states since Memorial Day, as governors across the country lifted stay-at-home orders, now forcing states to roll back or pause phases of reopening. Having a new corps of federal workers for contact tracing to prevent states from having to shut down their economies for a second time could help curb businesses having to close their doors for a second time.

South Korea has become a model country in implementing strong policies around contact tracing, and has been able to successfully lift stay-at-home orders as most business have reopened. The country has relied heavily on high-tech solutions that include contact tracers who monitor all new arrivals to the country and using CCTV footage and credit card transaction data to monitor location data of patients.

Or consider a state-level track-and-trace program already underway here in the United States. In Massachusetts, the nonprofit global health organization Partners in Health has been tapped to spearhead the state’s new contact-tracing program. Already, it has hired and trained close to 1,000 contact tracers. They are paying workers $27 an hour for their time and providing all contact tracers with health insurance.

Massachusetts is taking a step in the right direction, but there are estimates that the United States will need to hire as many as 300,000 contact tracers to track and prevent the spread of COVID-19, the disease caused by the new coronavirus. Reports show that building on similar successes by integrating them into a federally funded Works Progress Administration would cost Congress just $3.6 billion.

Promisingly, Sens. Chris Van Hollen (D-MD) and Christopher Coons (D-DE) recently introduced the Pandemic Response and Opportunity Through National Service Act, a proposal that would pay for 750,000 national service positions over the next 3 years, including 300,000 contact tracers. The legislation proposes using AmeriCorps and other existing programs that have standing partnerships with government agencies to hire people left unemployed by the COVID-19 pandemic and recession to help lead the charge.

Their proposed bill would also provide funding for public health services directly related to recovery and response, workforce and re-employment services, education support, and services that combat nutrition insecurity. It also would seek funding to create an online tool to enable seniors to safely access care through a teleservice model.

This program would provide a needed boost for our economy. Analysis shows young and low-income workers have been particularly hit hard by layoffs. Workers earning less than $20 per hour were 115 percent more likely to be laid off than those earning $30 per hour or more. And workers under age 25 were 93 percent more likely to have been laid off than those who are 35 and older.

A WPA-like program in 2020 would create openings for safe job opportunities for the hardest-hit workers, particularly low-income and younger workers. Ideally, workers in these jobs would learn new skills and be able to transition into nursing and home healthcare jobs during the post-pandemic economic recovery should they choose to do so.

This is what the World Health Organization recommended in the context of the outbreak of Ebola in sub-Saharan Africa earlier this century. The international agency recommended that contact tracers be trained with necessary skills to assess relevant symptoms, investigate and follow up with contacts, and have basic analytical skills to be able to conduct tracing remotely. The WHO also suggested they be trained to use personal and protective equipment, be aware of local cultural sensitivities, and be able to navigate the public health and healthcare systems in the jurisdictions in which they are working.

History teaches us such a program could work in the United States. The Works Progress Administration was an employment and infrastructure program established during the Great Depression that provided jobs for roughly 8.5 million Americans. Part of President Franklin Roosevelt’s New Deal, the WPA employed people to carry out public works infrastructure projects. It resulted in more than 4,000 new schools, 130 hospitals, and 29,000 bridges being built, in addition to 280,000 miles of newly paved roads. The program was successful in targeting Black Americans and women, employing approximately 350,000 Black workers, including funding for projects that supported Black musicians and actors, and hired women in clerical jobs and as librarians and seamstresses.

A modern-day Works Progress Administration would be federally funded and organized by states and localities to place out-of-work Americans into jobs serving as contact tracers and supporting those in need. Contact tracers would help identify those who test positive for the novel coronavirus and sequester those who have been exposed to help prevent further spreading of the virus and avoid overwhelming our hospitals and healthcare system. As a potential resurgence of cases arises due to the lifting of stay-at-home orders, such a contact tracing program might be necessary to prevent infections and hospitalizations from again overwhelming our healthcare system before a possible second wave of infections begins in the fall.

States cannot inch toward reopening without a roadmap for how to halt the coronavirus pandemic now and over the course of the rest of the year and into 2021. Without a plan to provide appropriate personal protective equipment and track and contain any new cases of the novel coronavirus and COVID-19, our economy will continue to recover only in fits and spurts. Congress needs to take bold action to fund a new corps of contact tracers and other healthcare workers. Implementing a modern-day Works Progress Administration to curb high unemployment not experienced since the Great Depression while simultaneously keeping our communities healthy is a necessary step to bringing an end to the public health and economic devastation that now grips our nation.

The latest jobs numbers released by the federal government today indicate the brunt of the job losses due to the coronavirus recession continue to fall heaviest on Black and Latinx workers, even though the month-on-month changes between May 2020 and June 2020 were better overall. Over those 2 months, the U.S. economy gained 4.8 million nonfarm payroll jobs, the share of the employed prime-aged population increased from 71.4 percent to 73.5 percent, and the jobless rate fell from 13.3 percent to 11.1 percent.

This latest monthly Employment Situation Summary—also known as the Jobs Report—from the U.S. Bureau of Labor Statistics shows that the U.S. unemployment rate is now below its April peak but remains well above the Great Recession high of 10 percent. What’s more, the share of unemployed workers who report having permanently lost their jobs increased for the second month in a row, jumping from 14 percent in May to 20.9 percent in June.

June’s Jobs Report also suggests that the improvements in the labor market have been uneven, and that Black and Latinx workers, in addition to women workers and low-wage workers generally, continue to be disproportionately affected by the coronavirus recession.

Even though the unemployment rate has been greater for women than for men since April—a relatively novel phenomenon since experience from previous recessions shows that men tend to lose more jobs early on in downturns—the gap between the two rates narrowed last month. Whereas men’s unemployment rate dropped from 12.2 percent in May to 10.6 percent in June, women’s declined from 14.5 percent to 11.7 percent.

But the gap between Black and White unemployment widened. The jobless rate of White workers fell from 12.4 percent in May to 10.1 percent in June, but Black workers’ unemployment rate only fell from 16.8 percent to 15.4 percent. And despite experiencing the largest month-to-month drop, going from 17.6 percent to 14.5 percent, Latinx worker’s jobless rate is 4.4 percentage points above that of their White counterparts.

Some of these data points should be taken with caution, however, since the Jobs Report sampling size makes small changes in Black workers’ labor market indicators difficult to interpret. Indeed, the disparate impacts of the coronavirus recession by race and ethnicity highlight the need for oversampling of minorities in the workforce in surveys.

Yet analyses using alternative sources of data also provide insight into these racial and ethnic disparities. Industries with the lowest average wages saw the biggest increases in employment this month, but research using data from payroll-services provider Automated Data Processing, Inc., finds that losses have been much more severe for low-wage jobs—positions in which Black and Latinx workers are overrepresented. The ADP data show that only a relatively small share of that difference can be attributed to workers’ age, the size of the business in which they were employed, or the industry in which they worked.

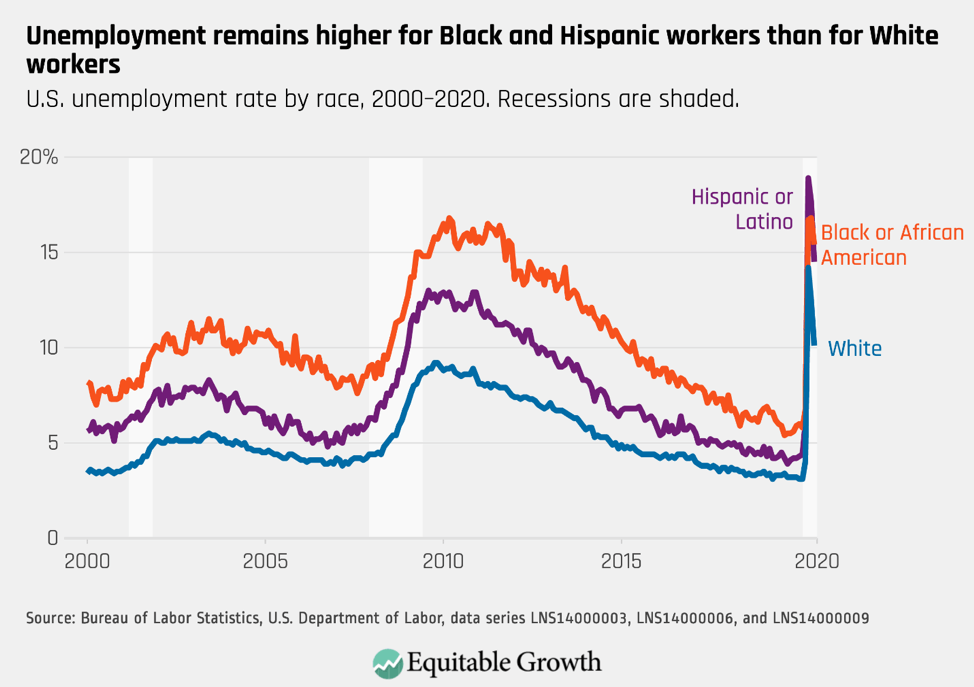

The disparities between races also reflect that, in other ways, the coronavirus recession is not unlike the previous ones. Researchers found that in Black workers were more likely to exit work in April and less likely than their White and Latinx counterparts to be rehired in May, as some businesses reopened. This trend is consistent with existing research, which shows that at least since the 1980s, Black workers have been more likely to be displaced from their jobs. This disparity, moreover, has become larger since the 1990s. (See Figure 1.)

Figure 1

There are similar findings in the case of women workers, showing that women’s overrepresentation in industries such as leisure and hospitality—a sector that, even after recovering 2.1 million jobs this month, has seen a massive 29 percent decline in employment since February—cannot fully explain why women are continuing to lose their jobs at a higher rate than men, since they are also experiencing more severe unemployment within industries. That women and women of color in particular have been hardest hit by this recession is likely driven by their overrepresentation in lower-wage and insecure occupations within sectors.

This trend also reflects feminist economists’ insight that the current health crisis and the disruption to education caused by the coronavirus pandemic have fallen more heavily on women. They continue to do the lion’s share of the unpaid work of caring for their families.

The relatively rosy jobs report this month masks other disconcerting trends. With almost 15 million nonfarm payroll jobs lost since February, more than four unemployed workers for every job opening, and some states backtracking on the reopening of businesses due to a surge in new coronavirus infections, the prospect of a fast economic recovery is slim. Moreover, important government financial support that helped keep workers whole and the economy out of freefall since March is set to expire in the coming months.

At the end of July, the extra $600 a week in emergency Unemployment Insurance will expire, including for so-called gig workers, who, for the first time, were able to tap unemployment benefits. And companies that borrowed funds beginning in April under the federal Paycheck Protection Program to keep their employees on payrolls will no longer have to do so beginning 8 weeks later, which means many of those employees could be furloughed or let go over the next 2 months.

In the next coronavirus recession relief package now under debate on Capitol Hill, Congress should increase access to the additional $600 weekly Unemployment Insurance benefits beyond the end of July, and only scale back unemployment benefits as the jobless rate declines by enacting automatic stabilizers. Policymakers also should provide financial support for state and local governments so they can avoid layoffs of critical public-sector employees amid the pandemic, and increase federal support for social infrastructure such as paid leave and health insurance systems. Doing so would bring some security to workers and their families, and make an eventual recovery both quicker and more equitable.

The United States is experiencing a severe recession attributable to COVID-19.

Overview

In February 2020, the U.S. unemployment rate was 3.5 percent. In May 2020, it stood at 13.3 percent. The unemployment rate for Black workers was a still-higher 16.8 percent. Unemployment for women exceeded that for men overall, among Black workers and among White workers. Adjusting for classification errors associated with the coronavirus pandemic would increase the overall rate by about 3 percentage points.1 Job losses were concentrated among lower-income workers and in sectors that rely on close physical proximity. In March and April, employment in the leisure and hospitality sector fell by nearly one-half; that is, there were half as many people working in that sector in May as there were just a few months before.

The emergence of the novel coronavirus that causes the COVID-19 disease led to this collapse in economic activity. This recession is unique in that it was caused by a global pandemic, but it also shares many features with the typical recession. One thing specifically: We know certain policies will support the U.S. economy while we work toward recovery. Automatic stabilizers—programs that automatically scale up in recessions and draw down during booms to stabilize the economy—play a critical role in fighting every recession.

In May 2019, Equitable Growth and the Hamilton Project published Recession Ready, which contained six proposals on automatic stabilizers. This issue brief examines the critical role that automatic stabilizers can play amid the current recession and in future downturns. The brief first explains what a recession is, what role public policy plays in fighting recessions, and then a few important ways in which this recession differs from previous recessions. Finally, the issue brief explains why Congress should expand and reform the United States’ existing automatic stabilizers.

What is a recession?

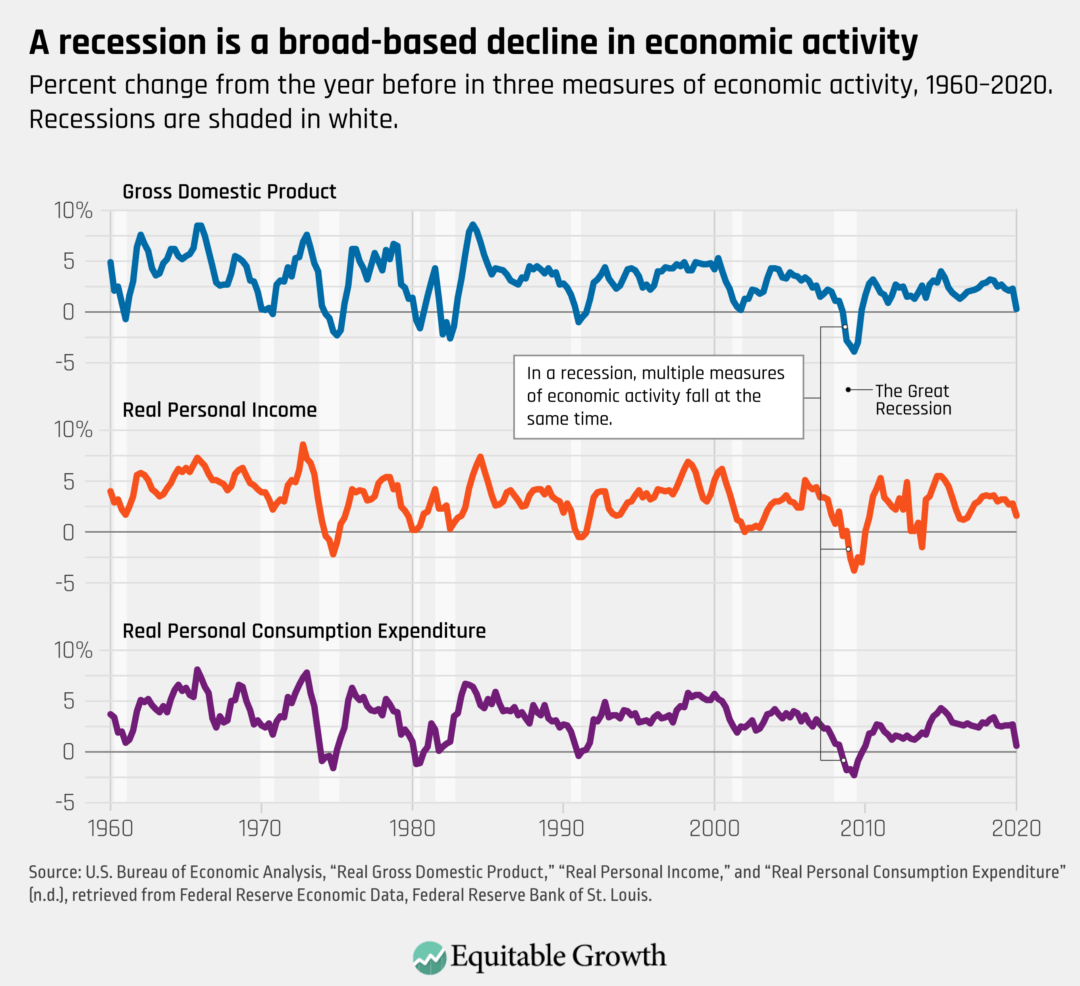

A recession is a broad-based decline in economic activity across the country. This general definition leaves substantial room for interpretation, however, and there is no hard rule for how big the drop in activity needs to be or how many different measures of economic activity need to fall. In identifying recessions, economists look for decreases in measures of activity such as production, personal income, employment, consumer spending, and retail sales, as well as increases in measures such as the unemployment rate. (See Figure 1.)

Figure 1

These measures of economic activity are better understood as different ways of looking at the same economy rather than entirely distinct measures of different things. If workers are laid off during a recession, they appear as unemployed workers when computing the unemployment rate and as a reduction in employment when computing total employment. The output they no longer produce appears as a reduction in output, and the income they no longer earn appears as a decline in personal income. The change in each statistic will differ based on exactly what it measures, but the decline in each statistic is a manifestation of the same underlying job losses.

The formal definition of a recession is the period when economic activity is decreasing. An expansion, or recovery, is when economic activity is increasing. This formal definition of a recession, however, does not capture the full extent of the economic suffering, which is generally a result of the depressed level of economic activity, not the rate of change.

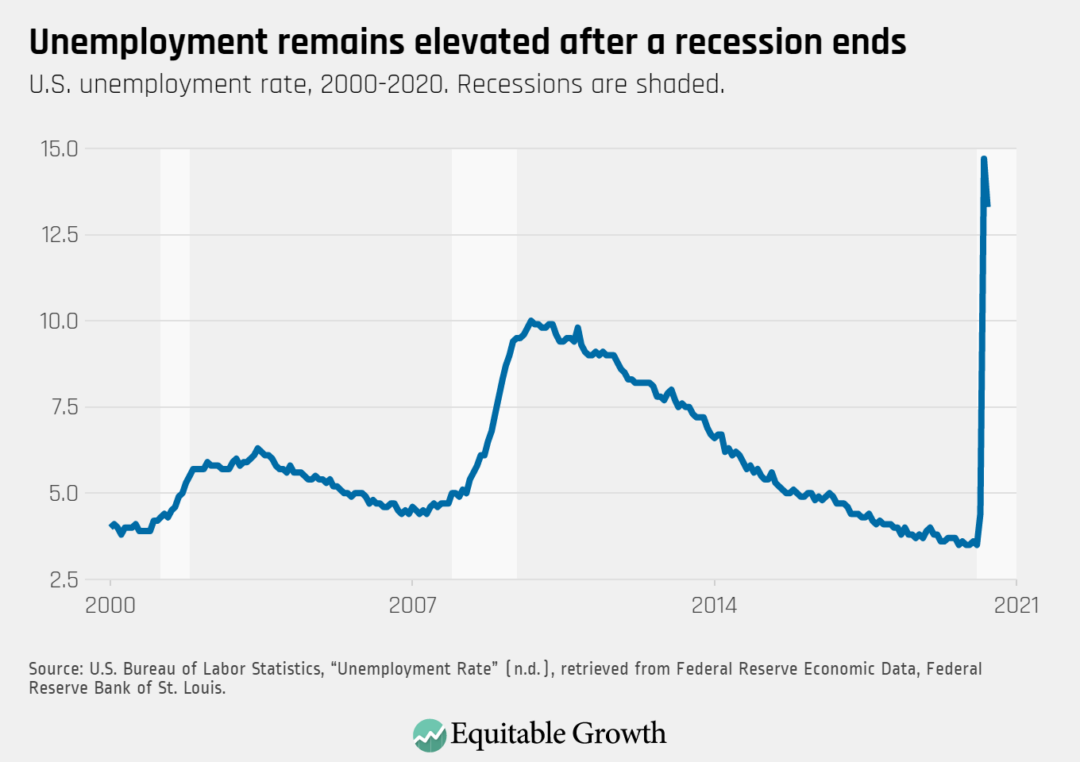

Unemployment, for example, typically remains elevated long after a recession ends. The Great Recession ended in June 2009, according to the formal definition, but unemployment peaked in October 2009 and remained higher in 2012 than it was during most of the recession. (See Figure 2.)

Figure 2

The persistence of suffering after a recession ends according to the formal definition is essential for understanding the current recession. The National Bureau of Economic Research recently announced its determination that the recession began in February 2020. The unemployment rate spiked between February and April, increasing from 3.5 percent to 14.7 percent, before falling to 13.3 percent in May. It’s possible—though certainly not guaranteed—that the decline in activity was concentrated in those 2 months. The formal recession might be both extremely short and extremely sharp.

Yet even if this turns out to be true, it will certainly be the case that the suffering will persist long after the formal recession ends. Moreover, there are important risks that this will not be the case, including if Congress allows critical relief enacted in March and April to expire over the next several months or if public health measures are unable to control the spread of COVID-19.

For this reason, the term recession is often also used to refer to the longer period of depressed activity that persists after the formal recession ends, even though the official definition of a recession is limited to the period of declining economic activity.

Defining recessions in terms of aggregate economic indicators also obscures disparate experiences for different populations. As noted above, the unemployment rate peaked in October 2009 following the end of the Great Recession several months earlier. This peak in overall unemployment coincided with the peak for White workers, but the peak for Black workers was not reached until March 2010, 6 months later. Similarly, the peak for men occurred in October 2009, but the peak for women was not reached until November 2010.

The economic pain from recessions compounds longstanding racial inequalities. Unemployment rates for Black and Latinx workers are persistently higher than unemployment rates for White workers.2 During recessions, the increases in the unemployment rate are consistently larger for Black and Latinx workers than they are for White workers. Moreover, wealth is a critical source of support for workers who lose their jobs during a recession, but Black and Latinx households have less wealth than White households.

Finally, economic activity is not an end in itself. What really matters about economic activity is the role it plays in determining families’ living standards. Put differently, the economic harmcaused by a recession is not the decline in Gross Domestic Product or any of the other measures used to identify a recession. The harm is the decline in families’ living standards.

This distinction is of relatively little importance when thinking about the harm resulting from a recession absent policy action as a recession causes simultaneous declines in economic activity and living standards. But it is critical for understanding the policy response. Public policies can have different impacts on living standards and economic activity. Restrictions on business activities, for example, may reduce economic activity even as they increase living standards by reducing the spread of disease. The appropriate focus of public policy is living standards, not economic activity per se.

What is the role of public policy during a recession?

During a recession, it becomes harder for people to find (and hold onto) jobs and business opportunities. The policy response can provide direct relief, moderate the decline in economic activity, and accelerate the recovery. Policies are typically categorized as either fiscal policies or monetary policies. The fiscal policy response consists of changes in taxation and spending. The monetary policy response consists of actions taken by the Federal Reserve through and in financial markets, such as influencing interest rates and lending.

On the fiscal side, public programs provide critical relief to people hurt by a recession and shorten the recession itself. Programs that automatically scale up during recessions and scale down during expansions are known as automatic stabilizers, and many of the United States’ most well-known social insurance and safety net programs function as automatic stabilizers.

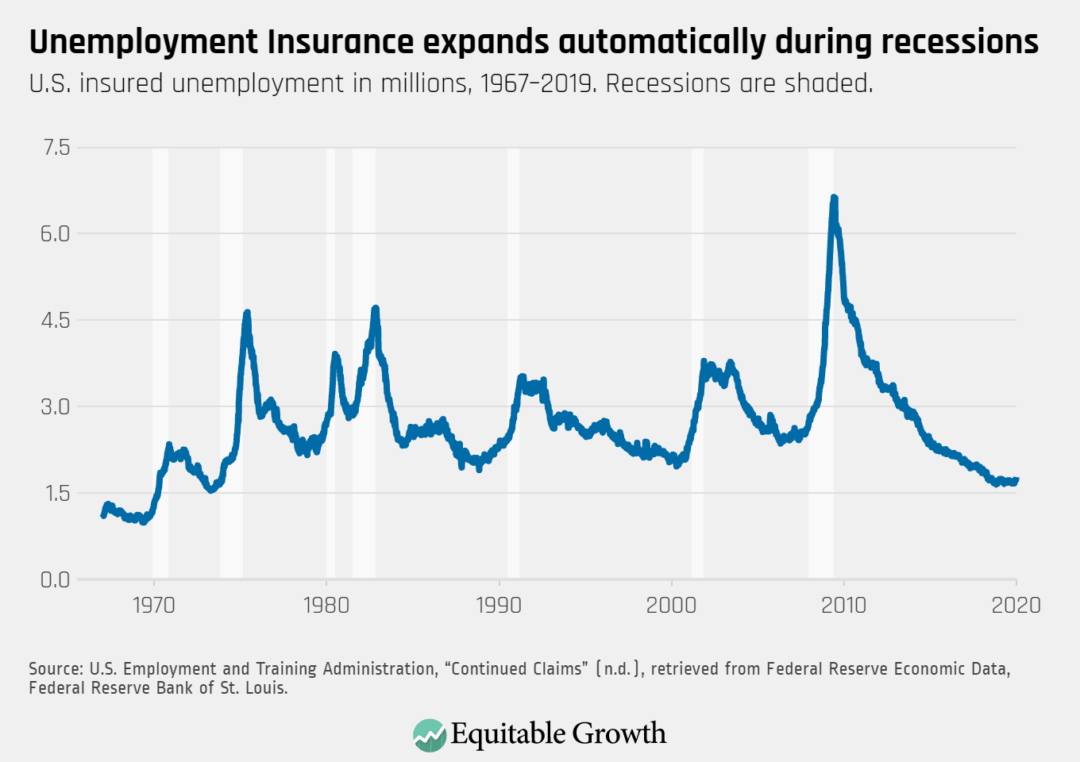

Unemployment Insurance provides cash to people who lose their jobs through no fault of their own, helping them maintain their standard of living. Even in relatively good times, some workers lose their jobs, and Unemployment Insurance serves this role. In bad times, Unemployment Insurance continues to serve this role while also short-circuiting the process by which cutbacks in spending by the newly unemployed spill over into reduced spending in other sectors, in turn causing even more job losses. Unemployment Insurance automatically scales up during recessions and down during expansions. (See Figure 3.)

Figure 3

Unemployment Insurance is perhaps the most prominent automatic stabilizer, but it is far from the only one. Medicaid provides health insurance to low-income families, automatically expanding during recessions, when incomes fall and more families become eligible. The Supplemental Nutrition Assistance Program provides assistance to low-income families in purchasing food and, like Medicaid, expands during recessions when incomes fall.

In addition to automatic stabilizers, Congress often responds to recessions by enacting additional policies specific to the recession. These new policies are known as discretionary fiscal policies, because they are enacted at the discretion of Congress. The American Recovery and Reinvestment Act of 2009 is an example of discretionary policy. The Recovery Act enhanced Unemployment Insurance, cut taxes, and provided financial support to state and local governments, including increased Medicaid payments, among other policies.

In addition to the fiscal policy response, the Federal Reserve responds to recessions using monetary and financial policy tools, which make it easier for people and businesses to borrow money. The logic is that this response will both prevent people and businesses unable to borrow funds from going bankrupt and encourage people and businesses to take on loans to support their purchases and investments, which will ramp demand back up to reverse the economic contraction.

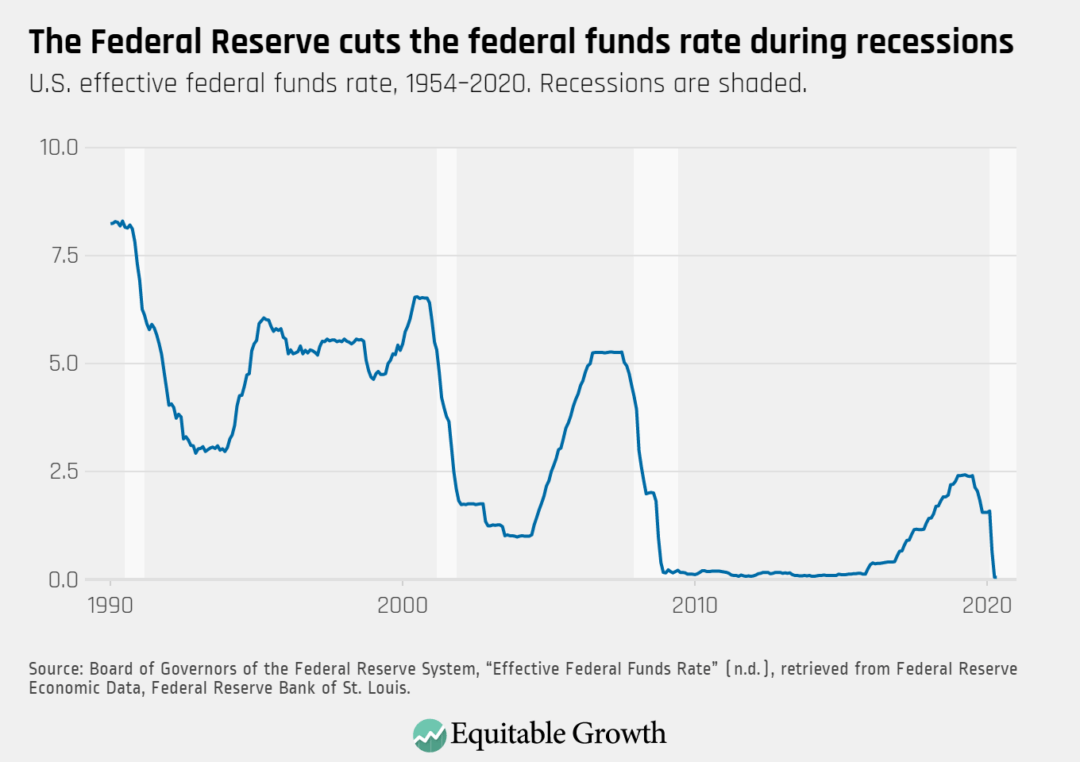

The traditional monetary policy tool is control of the federal funds rate, which is the interest rate at which banks lend money to each other overnight. In recent decades, the Federal Reserve has reduced the federal funds rate during recessions and increased it during expansions. (See Figure 4.) These changes in the federal funds rate make borrowing cheaper during recessions and more expensive during expansions.

Figure 4

In both the Great Recession and the current recession, control of the federal funds rate has been insufficient to fully address the recession. During and after the Great Recession, the Federal Reserve set the rate to nearly zero for 7 years. In part for this reason, the Federal Reserve has increasingly relied on other tools, such as lending programs and asset purchases, to stabilize the economy as well. These programs aim to ensure that the deterioration of financial market conditions does not create additional stresses for public- and private-sector employers, further exacerbating the recession.

How is this recession different?

The coronavirus recession shares many similarities with previous recessions but is also different in some key ways. First, this recession occurred with unprecedented speed due to the sudden emergence and spread of the novel coronavirus. Second, the virus has made economic activity more dangerous. Third, because the recession was caused by a virus, the decline in economic activity has occurred alongside an increase in morbidity and mortality.

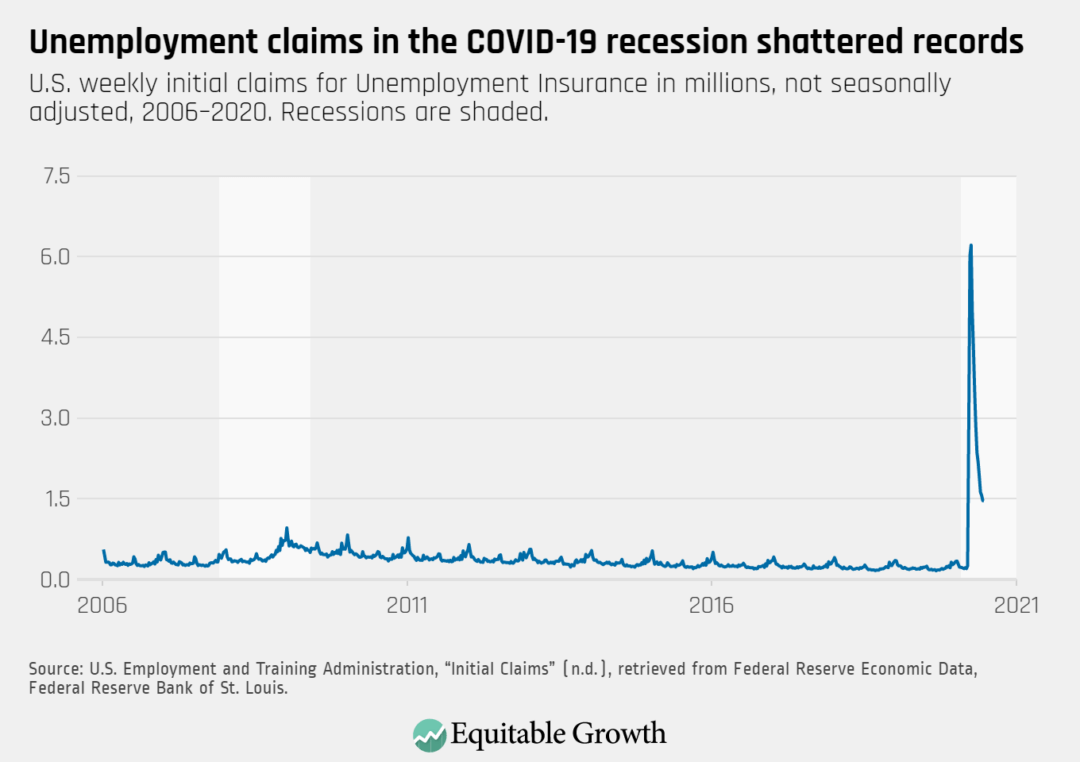

The onset of the coronavirus recession was sudden. In February 2020, U.S. unemployment was 3.5 percent. Employment stood at 152 million. In the week ending March 14, 250,000 people filed for Unemployment Insurance. Then, the recession began. The following week, 2.9 million people filed for Unemployment Insurance—by far the highest number on record and three times higher than the highest week during the Great Recession. The following week, 6 million people filed for Unemployment Insurance. And the filings have continued at a historic pace since then, with more than 40 million applications since mid-March. (See Figure 5.)

Figure 5

The rapidity of the coronavirus recession stands in sharp contrast to recessions more generally. Typically, unemployment is a lagging indicator; that is, it rises as firms lay workers off over time. For example, in December 2007, the month the Great Recession began, the unemployment rate was 5 percent. As the consequences of the financial crisis spread through the economy, it took 8 months for the unemployment rate to rise by 1 percentage point and another 4 months to rise by a second percentage point. In contrast, the unemployment rate rose 11 percentage points in 2 months in the coronavirus recession.

The speed with which the current recession began also is apparent in data on consumer spending and employment. Spending on travel, shopping, and entertainment plummeted in a matter of weeks. Overall, consumer spending fell by 19.6 percent between February 2020 and April 2020. Employment, particularly in jobs that involve close physical proximity, likewise fell sharply. About half of the jobs in leisure and hospitality were lost in March and April.

This brings us to the second distinguishing feature of this recession: The coronavirus has made economic activity more dangerous. In any other recession, being lucky enough to keep your job is almost certainly a good thing, but in the current recession, it’s more complicated. Being lucky enough to keep your job means you are much more likely to have maintained your income, but if you cannot perform your job remotely, it is also a risk factor for exposure to the coronavirus.

Existing patterns of occupational segregation in the United States play a critical role in determining who is hurt—and in what ways—by this unique feature of the coronavirus recession. Unemployment for Latinx workers, who are overrepresented in leisure and hospitality, has spiked more than for Black and White workers. Unemployment for Black workers, who had the highest pre-recession unemployment rate but are overrepresented in essential jobs, has increased dramatically but by a smaller amount.

The increased danger of economic activity changes the goals for the policy response. A typical recession does not change the cost-benefit analysis of working. In the coronavirus recession, the relative costs and benefits of work have changed for many jobs. This unique characteristic of the coronavirus recession required policymakers to act in unusual ways. Across the country, states and cities prohibit many types of economic activity to stop the spread of the coronavirus, shutting down businesses and asking—in some cases requiring—people to maintain greater physical distance from each other.

In principle, these shutdown orders could have induced the recession. Yet state closures appear to be responsible for only a modest portion of the decline in economic activity. Economic activity began to fall in early-closing states before closures began—and this gap is even more pronounced in late-closing states. In other words, people and organizations began to respond to the risks associated with the coronavirus before state orders took effect. In addition, a similar decline in economic activity is observed in states that did not issue formal stay-at-home orders. For the same reason, even as state orders have been relaxed, economic activity has remained substantially depressed.

Because the coronavirus makes economic activity more dangerous, a core focus of the policy response in this recession should be making jobs and other activities of economic life safer. Needless to say, in a typical recession, this is not a concern in the same way. By reconfiguring our economic life to improve safety, we lay the groundwork for the future economic expansion. The longer we delay addressing this task and the less we focus on it, the more severe the consequences of the coronavirus pandemic will be.

The third and final distinguishing feature of the coronavirus recession is the accompanying increase in mortality and morbidity attributable to the virus that caused the recession. More than 115,000 people have died from COVID-19 and more than 2million people have been confirmed infected in the United States. Moreover, there remains much we don’t know about the virus and the disease it causes, including how long the effects of COVID-19 will persist in those who recover, and how severe they will be afterward.

Existing inequalities continue to shape the health consequences of the coronavirus and COVID-19. Severe outbreaks occurred and continue to occur in prisons, nursing homes and other care facilities, and at worksites such as meat-packing plants. Mortality rates for Black people and for Latinx people far exceed those for White people, especially at younger ages. These differences likely reflect, in part, the fact that many of the jobs that rely on close physical proximity and have been deemed essential are held by Black and Latinx workers, as noted above.

How have policymakers responded to the COVID-19 recession?

Because the COVID-19 recession is caused by the emergence of a new virus, the most important response to the crisis is the public health response. But the Trump administration’s response has been ineffective and poorly managed. The United States lagged on testing throughout early 2020, which contributed to the undetected spread of the novel coronavirus.

The administration also failed to facilitate a coordinated response to the crisis in terms of managing supply chains, organizing or directing production of needed supplies, or providing clear guidance to people and businesses on appropriate health and safety measures. Numerous journalists have provided detailedaccounts of this ineffective executive branch response. This failure exacerbated the spread of the virus, and deepened the recession and will undermine the recovery.

For its part, Congress enacted four major bills in response to the COVID-19 crisis that President Donald Trump signed into law. First came the Coronavirus Preparedness and Response Supplemental Appropriations Act, on March 6; then, the Families First Coronavirus Response Act on March 18; then, the Coronavirus Aid, Relief, and Economic Security, or CARES, Act on March 27; and then, the Paycheck Protection Program and Health Care Enhancement Act on April 24.

The Coronavirus Preparedness and Response Supplemental Appropriations Act provided emergency appropriations to federal agencies to respond to the crisis and made changes to Medicare rules for telehealth services. The price tag was only $8 billion—by far the smallest response legislation.

The Families First Coronavirus Response Act provided a more substantial response. The legislation required public and private insurers to provide free coronavirus testing, provided increased Medicaid funding to states, created a paid leave program for employers with more than 50 and fewer than 500 employees, provided additional funding to pay for SNAP benefits, provided administrative funding for Unemployment Insurance programs, and provided supplemental appropriations for a variety of purposes. The estimated cost was $192 billion.

The major federal legislative response came with the CARES Act. It had a price tag of $1.7 trillion. (The legislation is estimated to increase the federal deficit by $1.7 trillion; it is sometimes described as a $2.2 trillion package because that is the gross amount of spending, tax cuts, and loan guarantees.) This legislation offered direct payments to most families, sharply but temporarily increased Unemployment Insurance benefits and expanded eligibility for the program, created multiple business loan programs, and cut and deferred a range of business taxes, among other provisions.

Finally, about a month later, the Paycheck Protection Program and Health Care Enhancement Act provided additional funding for the Paycheck Protection Program (one of the small business loan programs created by the CARES Act), additional funding for healthcare providers, and made additional appropriations.

The Federal Reserve also took unprecedented actions to address the economic fallout due to the coronavirus pandemic. The Fed cut the federal funds target rate by 1.5 percentage points in two steps in March. It also announced an open-ended commitment to purchase Treasury debt, government-guaranteed mortgage-backed securities, and commercial mortgage-backed securities. It also created and expanded several programs that lend to financial-sector institutions in an effort to ensure the smooth functioning of financial markets.

In addition, the Fed created new programs that lend directly to businesses, relying in part on funds appropriated by Congress in the CARES Act for this purpose, and started lending directly to state and local governments. Finally, the Fed is lending dollars to foreign central banks.

Why should Congress expand automatic stabilizers?

Nobody knows for sure how long the coronavirus recession will last or exactly how severe it will be. The uncertainty that would exist when confronting any recession is compounded by the uncertainty about the nature and consequences of the coronavirus itself, including the number of people who will die from COVID-19 now and in the future, the short- and long-term health impacts of the virus on those who recover, the pace at which treatments and vaccines will be developed, and the quality of the public health response.

As with any fiscal policy response, automatic stabilizers support household incomes and spending during recessions. Crucially, however, automatic stabilizers continue as long as they are needed without requiring further legislative action. If the recession is deeper and longer, then the response grows. If the recovery is quicker, then the response shrinks.

The coronavirus recession is the most severe economic downturn since the Great Depression. Yet key provisions of the congressional response to the pandemic are either scheduled to expire or were made available only in a fixed amount. The $600 increase in weekly Unemployment Insurance benefits expires at the end of July, for example, and state and local governments are facing a looming budget crisis but have received only a modest amount of aid.

The United States is currently experiencing a severe recession attributable to the emergence of a new virus. Unemployment jumped at a record-breaking pace, and daily life swiftly changed in radical ways. Policymakers responded quickly but insufficiently. Their response headed off the worst of the recession to this point, but Congress should move immediately to extend necessary relief and make it automatic by tying it directly to economic conditions.

COVID-19 shines a bright light on the role of crucial care work undertaken by some of the most marginalized workers.

The displays of solidarity among Black Lives Matter protesters and frontline healthcare workers across the United States over the past month demonstrate the underlying links between multiple crises involving public health, the economy, and racial justice. The COVID-19 pandemic shines a bright light on the role of crucial care work undertaken by some of the most marginalized workers—in particular, the overrepresentation of women, and especially women of color, among low-wage healthcare workers on the frontlines, including home health aides, nurses, and nursing assistants. And the historic marginalization of populations along lines of race, gender, and class, particularly for Black and Latinx populations, limits how our nation provides for and values care work in the United States.

The gendered dimensions of these crises also are present in our homes. Women still do more of the unpaid work of caring for their families and communities compared to men. Black women are more likely to be breadwinners while also being responsible for caregiving. The COVID-19 pandemic increases the need for family caretaking not only because of the closing of schools and childcare facilities, but also because more people are sick and need care.

Together, these crises experienced in our homes and our workplaces point a spotlight on the foundational role of care in our society: caring for each other in our families and communities, as well as caring for the health of society, including those low-wage workers such as nursing assistants, whose jobs are crucial to the functioning of health systems but earn near-poverty wages. Yet the work of care is undervalued and often invisible.

The foundation of this profound inequality lies in the traditions and structures of patriarchy, where unpaid or low-paid domestic duties have been the purview of women for millennia. Even as some of this work increasingly entered the marketplace through professional care jobs such as nurses and childcare workers, it is still perceived by society as having low value. And the lowest paid careworkers often are Black and Latinx women workers facing multiple structural barriers in the economy.

This is partly because of the difficulty in conceptualizing and measuring the long-term benefits of providing quality care, which is at least partly why this type of work was left out of most of the history of economics. But this also is because structural sexism and misogyny still influences how society perceives what jobs are worthy of fair payment and acknowledgement.

Research and analysis of these harmful trends is left out of most of academic economics and sidelined in economic policy in the United States. But paid and unpaid care work has been central to the development of a subfield of economics called feminist economics. These economic scholars bring to light valuable lessons centered in feminist thought to demonstrate the value of care and guide policy to improve the well-being of care workers and care recipients alike. Women’s physical and mental health—and, by extension, the societies that rely on women and this work they are doing—are at stake.

Our own research shows that the COVID-19 pandemic exposes how gender roles are embedded in the U.S. labor market and within families and communities, ultimately leading to more work from women than from men. Black feminist economist scholar Nina Banks argues that community work is both racialized, as well as gendered, so Black women are creating social and economic value through caring for others in their communities. This community care work is more crucial now than ever. Although many of the challenges for women are not unique to this time, the COVID-19 pandemic exacerbates their impacts, making this an important moment to recognize the gendered and racial structures underlying this work and advocate for policies that support their well-being and security.

Any comprehensive response to the COVID-19 crisis must recognize this gendered work as an integral part of an economic system that promotes human well-being for all. A call for a feminist economic agenda for the World Health Organization ran recently in medical journal The Lancet. A leader to take this approach is Hawaii’s Department of Human Services, which has issued a Feminist Economic Recovery Plan for COVID-19. It is the first time an official U.S. state agency has developed an explicitly feminist plan to deal with this pandemic. Priorities include building the state’s social infrastructure and supporting job creation in green industries.

This is a model worth emulating. Economic policy should be constructed within a broader, feminist framework of human well-being and justice. Economic policy that has been solely concerned with the achievement of output-based metrics such as financial stability and Gross Domestic Product growth have always been inadequate in addressing how patriarchy and structural racism determine economic outcomes. This is now more clear than ever.

Americans are protesting racial injustice nationwide during a pandemic that has affected people very differently based on who they are and what jobs they have. The federal government continues to plan another economic recovery package of uncertain size and scope. Both the American public and policymakers in Washington need to embrace a comprehensive response to the COVID-19 crisis that emphasizes the importance and value of care work within families and communities and in the labor market as an integral part of the economic system. We must judge the success of policy responses by how they promote human well-being for all.

New analysis shows that while Congress was busy debating the parameters of federal paid leave to families dealing with the COVID-19 pandemic, state paid leave programs in Rhode Island and California were already at work providing much-needed support to affected workers. Because of longstanding paid family and medical leave programs in these two states, workers were able to access paid leave benefits sooner and for a wider variety of reasons than their peers in states without paid leave social insurance programs.

This column summarizes the key findings from this analysis—an empirically grounded starting place for understanding how workers are accessing paid leave during these public health and economic crises. It continues with a roadmap for researchers, including potential data sources and priority research questions identified by paid leave experts and advocates, interested in examining how state and federal programs supported workers during the COVID-19 pandemic and the recession it caused. Such research has important short- and long-term implications for policymakers developing an equitable, accessible, and permanent federal option for the nation’s paid leave needs.

Paid leave policy in the United States when the COVID-19 pandemic hit

Even before the onset of the COVID-19 pandemic, addressing conflicts between family and job responsibilities without access to paid family and medical leave was a challenge for U.S. workers. The current public health crisis and related illnesses and school and business closures exacerbate this challenge. While some workers can count on their employers to provide them with paid leave, it is rare: Only 18 percent of private-sector workers have paid family leave and 44 percent have paid personal leave though their jobs. Access to these benefits drops precipitously for lower-income and part-time workers.

Filling these gaps, eight states and the District of Columbia have developed their own paid leave social insurance systems, expanding leave access to most of their states’ private-sector employees. Five of these states—California, New Jersey, Rhode Island, New York, and Washington state—are currently paying out claims, while the remaining states and the District of Columbia will begin paying benefits in 2020–2023.

When the COVID-19 pandemic hit, these five states had the infrastructure in place to support workers’ time-off needs immediately, while families elsewhere were left to scramble with these new work-life challenges. Then, Congress, recognizing the importance of paid leave during a public health emergency, passed the Families First Coronavirus Response Act. Signed into law on March 18 and implemented on April 1, 2020, the new law provides the first federal guarantee to U.S. private-sector workers for paid sick days, which cover a short time away from work to deal with an illness, and paid family leave, which covers longer absences from work to care for a loved one.

This is an historic development for working families, but it is an imperfect solution. The law is temporary, carves out a wide swath of employees who cannot access paid leave, and only offers paid family leave for parents whose regular childcare provider is unavailable. This is a necessary benefit for those parents, but it leaves out many other reasons workers need time off, such as caring for a relative recovering from COVID-19.

While more data on the new federal paid leave system are surely forthcoming, the existing state-level programs offer important immediate insights into how paid leave can support workers during a period of crisis. These state systems were available from the onset of the pandemic and offer workers a wider array of benefits than the federal alternative. How they responded in the early days of the pandemic is an important lesson for policymakers considering a permanent and comprehensive federal paid leave program.

As COVID-19 spread, California and Rhode Island’s paid leave systems responded

A new analysis by the Urban Institute’s Chantel Boyens sheds light on how state systems responded to the increasing need for paid leave as COVID-19 spread. Boyens’ analysis of paid family and medical leave systems in California and Rhode Island, the two states that publicly release timely claims data, shows a sizable increase in new claims following the World Health Organization’s March 11 declaration of a global pandemic. Workers filing these initial claims accessed benefits weeks before the Families First Coronavirus Response Act was implemented.

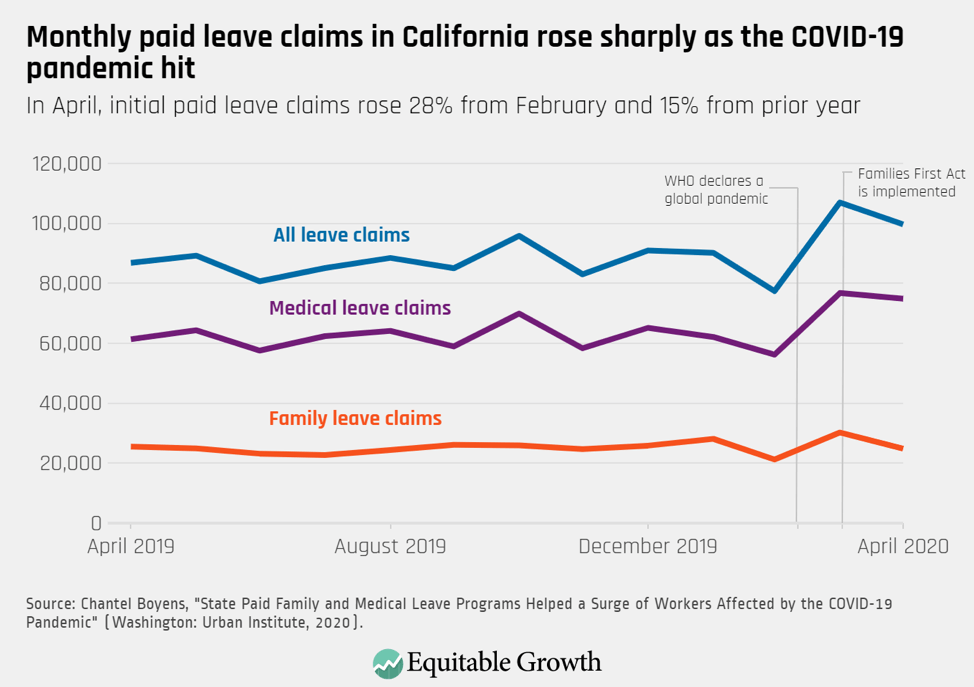

In California, 106,989 new paid family and medical leave claims were filed in March 2020 and 99,695 were filed in April 2020. In March, the first month of the pandemic, claims rose by 29,601—or 38 percent—from the month prior, representing a 16 percent increase from March 2019. The majority of these new claims were for medical leave, but family caregiving claims also exhibited a 43 percent February to March increase and a 13 percent increase from the year prior. By April, medical leave claims remained 22 percent higher than the year prior, but family caregiving claims fell to prepandemic levels. (See Figure 1.)

Figure 1

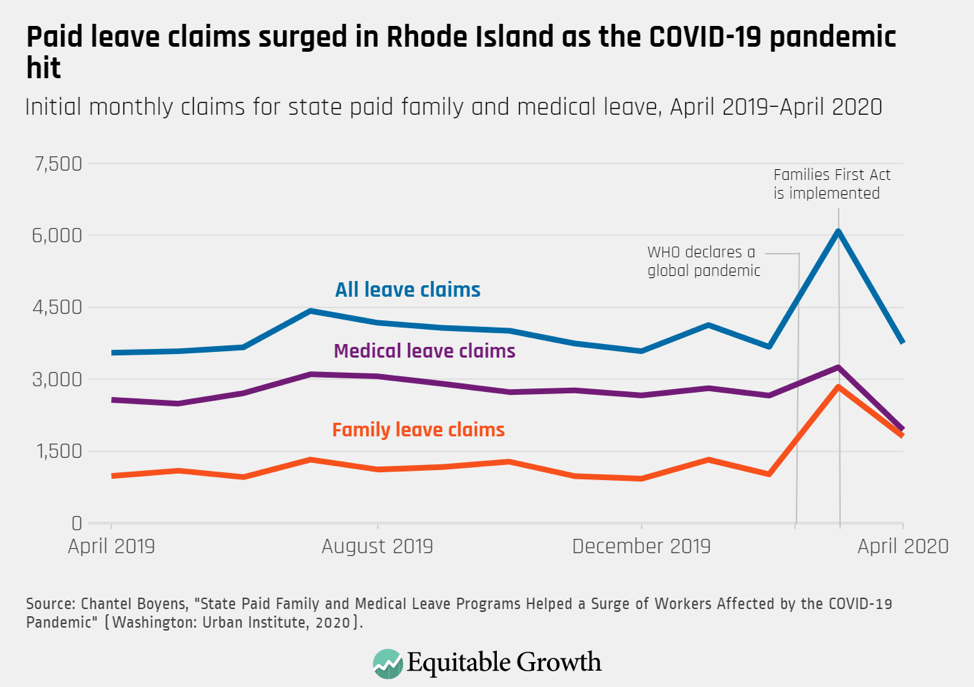

On the other side of the country, data from Rhode Island tell a similar story, with one key difference. According to Boyens’ analysis, new family caregiving claims in Rhode Island nearly tripled from February to March—an increase from 1,016 to 2,841 new claims, or 180 percent. Medical leave claims also rose in March to 3,248 from 2,659, representing a 22 percent bump from the prior month. Claims in April did return to roughly prepandemic levels, though this drop was not uniform across all types of leave. (See Figure 2.) Unlike California, Rhode Island’s decline in claims was largely driven by a fall in medical leave claims, but family caregiving claims remained 84 percent higher than in April 2019.

Figure 2

In Rhode Island, the spread of COVID-19 remained low in the first half of March, but policymakers worked quickly to prepare the state’s paid leave system for the crisis. March 12, 2020, just one day after the WHO declared a pandemic, Governor Gina Raimondo (D) approved executive action that expanded the reasons individuals could quality for leave, waived waiting periods, and loosened medical certification requirements for those with a COVID-19-related illness. This effort to push workers toward the state’s paid leave system appears successful, particularly in the weeks before the federal program was accessible.

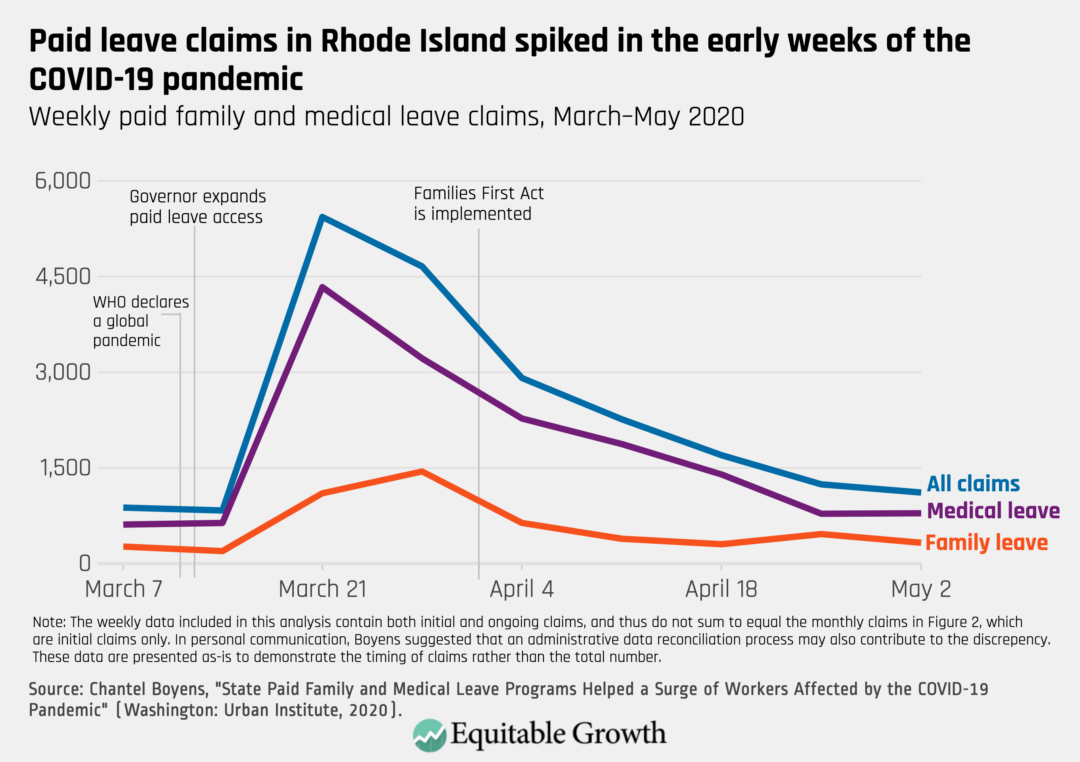

Boyens finds that the largest spike in claims occurred in Rhode Island in the second half of March, following the WHO’s declaration and Gov. Raimondo’s emergency order. The weekly peak of claims for family caregiving leave occurred later than that for medical leave, possibly due to the timing of statewide childcare center closures on March 16 or a lag in the public’s awareness of these benefits. (See Figure 3.)

Figure 3

Rhode Island’s weekly data include initial and continuous claims, so the number of claims presented in the weekly numbers exceeds the monthly data detailed in Figure 2. Still, the pattern in these data is clear: The number of workers requesting new leave or continued time away from work rose dramatically in the early weeks of the pandemic. These workers accessed benefits relatively early in the public health crisis.

Research on paid leave during the pandemic could offer valuable insight during the current public health crisis and beyond

Boyens’ analysis is an early glimpse into how the paid family and medical leave systems in two states responded in the beginning months of what is shaping up to be a protracted public health and economic crisis. More research is needed, however, to understand the accessibility and use of paid leave during this pandemic, not just in California and Rhode Island but also in the other jurisdictions with paid leave programs and the rest of the country accessing paid leave for the first time via the federal Families First Coronavirus Response Act.

In the short term, such research could inform programmatic tweaks to the Families First Coronavirus Response Act and other related programs. The new federal law constructed a paid leave system during a crisis and was unable to benefit from the existing infrastructure and public awareness available in states such as California and Rhode Island. More research on how the program is working in real time will help policymakers and regulators make necessary adjustments. For example, analyses that examine benefit eligibility and access by demographic groups may reveal opportunities for targeted public education. Further, any evidence that paid leave has positive public health implications or health system cost implications may encourage policymakers to expand the benefits offered through the Families First Coronavirus Response Act or extend the program beyond 2020.

In the longer term, research on how access to paid sick leave and paid family and medical leave supported workers during the COVID-19 pandemic will be instructive for policymakers designing a permanent system at the federal level. Already, existing research provides valuable insight into how such a system could be designed. Still, the Families First Coronavirus Response Act and ancillary programs are an opportunity to study alternative benefit models and delivery systems and learn from their successes or inefficiencies. Some important research questions include:

How are state paid leave programs, unpaid leave programs, and the Families First Coronavirus Response Act serving the needs of workers affected by COVID-19? How do these program compare in terms of:

The demographic and socioeconomic status of people served?

The eligible population’s awareness of the programs?

The sizes and characteristics of firms where employees are accessing leave?

The reasons for taking leave?

The duration and timing of leave-taking?

The return-to-work rate after the leave period?

Barriers to leave-taking?

Take-up rates?

The impacts on key outcomes, including health, material hardship, care recipient well-being, COVID-19 diagnoses, public health, hospital admissions, health insurance continuation, and health systems costs?

How do these paid leave programs compare to other programs that workers may have used for wage replacement when not able to work during the pandemic? Other programs include:

Unemployment Insurance

Workers compensation

Stimulus payments

Wages covered by businesses that accessed the Paycheck Protection Program

Wages covered by businesses that did not access the Paycheck Protection Program

Employer-provided paid time off

Unpaid time off

Private charitable contributions

For workers taking family caregiving leave, which family members are they caring for? How is this impacted by the definition of a “family member” included in the applicable paid leave program?

How does leave-taking behavior vary by the level of job protection (no job protection, anti-retaliatory protection, full job protection) included in the applicable paid leave program?

How does leave-taking behavior vary in jurisdictions that mandate employer-provided sick leave? Is paid family and medical leave being used to substitute sick days for workers without this benefit?

Does paid leave access impact the rate of COVID-19 infections? If so, how?

How have claims to state leave systems been impacted by the implementation of the Families First Coronavirus Response Act?

How are workers sequencing benefits during this crisis?

What is the leave-taking behavior of workers carved out of Families First Coronavirus Response Act? Are they foregoing leave, taking unpaid leave, accessing alternative benefits, using pandemic unemployment benefits, leaving work, or something else entirely?

For researchers interested in these or related questions, some potential data sources include:

State systems’ administrative data. California and Rhode Island share monthly leave data going back years, and New Jersey produces useful annual reports. Other states may be willing to negotiate data-sharing agreements with researchers.

The U.S. Census Bureau’s Household Pulse Survey, which includes several questions on paid leave use, caregiving needs, and other measures of economic security and well-being during the coronavirus pandemic.

The COVID Impact Survey, available from the University of Chicago’s National Opinion Research Center, which asks a variety of questions on respondents’ well-being, economic security, food security, physical health, and interactions with one’s community and social network during the coronavirus pandemic.

The Household Pulse Survey allows for the most direct comparison between workers with caregiving or health needs by paid leave access. If the survey continues, researchers may be able to study the impact of states implementing their own paid leave systems in the coming months. The District of Columbia will start paying benefits in July 2020, and Massachusetts will begin in January 2021. The COVID Impact Survey does not include a specific measure for paid leave access, but researchers can leverage variation in paid leave eligibility by state of residence or size of employer to generate intent-to-treat estimates.

Conclusion

Researchers have been studying the impact of paid leave for decades, but the coronavirus recession and the diversity of federal, state, and local responses raises new research questions about workers’ demand for paid family and medical leave and the most effective government response. Continuing to build upon the existing paid leave research base will inform a stronger federal solution that supports families, employers, and the economy during the remainder of this pandemic and beyond.

This past March, as a coronavirus relief measure, Congress suspended payments on a lion’s share of federally owned student loans for 6 months. When this temporary loan forbearance expires on September 30, it should be extended—permanently.

Many borrowers will not be prepared to begin making payments that soon. But more importantly, none of these student loan borrowers should ever have to make another payment. Cancelling these debts would benefit the U.S. economy, reduce the massive racial wealth divide, and create new opportunities for a generation of college graduates whose hopes the economy has wiped out twice in a dozen years.

The Coronavirus Aid, Relief, and Economic Security, or CARES Act places federal student loans in administrative forbearance. That means debtors still owe their full debt but need not make any payments, and no interest will accrue on the loan during this period. It’s a good idea to provide relief to the more than 40 million borrowers in our country, many of whom face staggering levels of debts, not to mention helping to sustain an otherwise bleak economy by putting some money in the pockets of consumers.

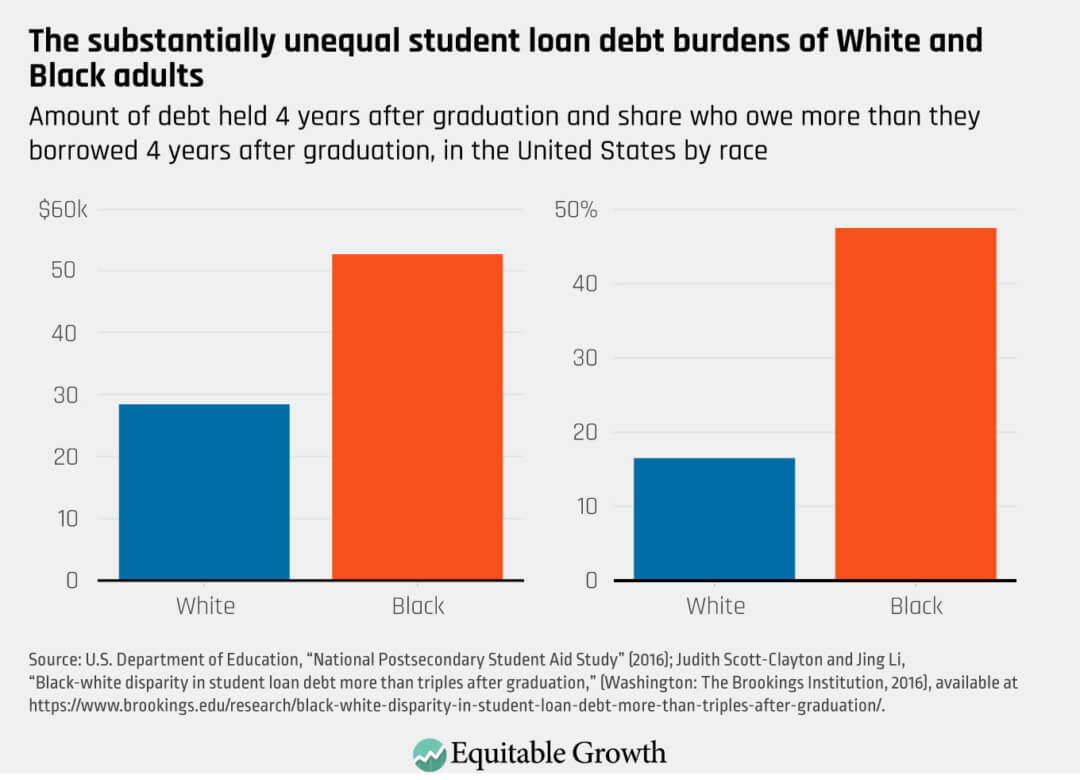

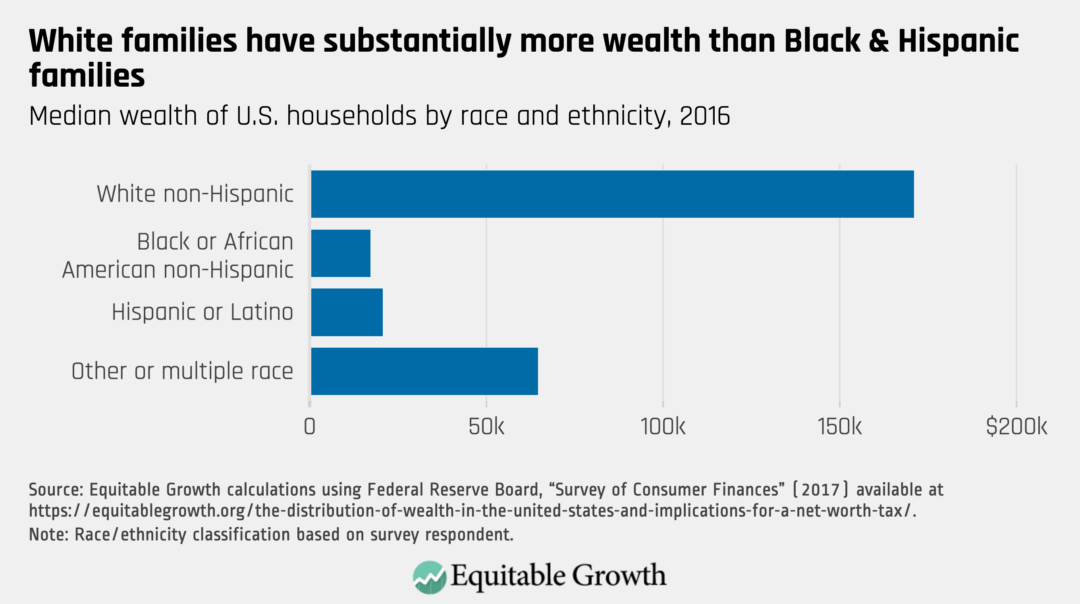

But this measure doesn’t go nearly far enough. This debt should not merely be suspended but cancelled entirely. Even before the coronavirus pandemic, federal student loan debt was crushing the financial and career aspirations of millions of borrowers. With college costs consistently rising faster than inflation and federal grant aid to students not keeping up, the aggregate amount of student debt is more than triple its level just 13 years ago—revealing the systemic nature of the trap created by a system of debtor’s education. Debt levels are especially high for Black students, who, 4 years after graduation, have an average obligation of more than $50,000, compared to less than $30,000 for the average White student. (See Figure 1.)

Figure 1

This higher debt load stems, in part, from the extraordinary gap in wealth between White and Black families. The median White household has 10 times the assets of the average Black family. (See Figure 2.)

Figure 2

Receiving less protection from parental wealth, Black students take on higher debt loads. Then, upon entering the labor market as young adults, these students face a harder time paying off their loans in a labor market characterized by racial discrimination. Evidence suggests that student debt has significant social impacts on the most vulnerable borrowers, including impeded family formation and poorer mental health. While student debt has conventionally been thought of as “good debt,” the investment generates widely disparate rates of return by race, given the prevailing social framework of unequal housing and Kindergarten through 12th grade education, predatory finance, and labor market discrimination.

The past decade and a half were especially cruel to college graduates. The scarring effect of the Great Recession of 2007–2009 is well-known. Those who graduated during that recession and immediately after will, on average, earn less throughout their careers. Yet, in part because of legislation permitting higher federal student borrowing, overall student borrowing began to skyrocket, surpassing credit card debt for the first time in 2010.

In addition, during the Great Recession, adults were encouraged to wait out the poor labor market and advance their career prospects by furthering their education. Many accrued more student loan debt but not all returned to the workforce with a degree or with the substantial improvement in earnings potential needed to pay off their debt. College costs are continuing to rise faster than overall inflation and federal grant aid is lagging, causing a significant portion of the millennial generation and its immediate successors to pursue adult lives with a millstone around their necks.

Cancelling student debt during the coronavirus recession and going forward with tuition-free universities would provide the greatest benefit to those who are suffering the most today. It is well-documented that people of color are contracting and dying from COVID-19 in numbers far out of proportion to their share of the population. Those service-sector jobs that don’t require a college degree, where Black workers and immigrants are overrepresented, are also less likely to provide access to insurance coverage or paid sick leave than other sectors. As the saying goes, when America gets a cold, Black people get the flu, but when America gets the flu, Black folks are far more likely to die. The anger we are seeing on the streets of cities across the nation is due not only to the violence imposed on Black Americans by discriminatory law enforcement but also is inextricably intertwined with social, educational, and economic injustices all created by the same society.

The concept of cancelling federal student debt is not a new one. Congress enacted loan forgiveness programs with Presidents George W. Bush and Barack Obama. The Bush program, initiated in 2007, focused on teachers and other public servants, as well as those working for nonprofit organizations, but it is exceedingly complex. Since loans became eligible for forgiveness in 2017, fewer than 3,400 borrowers have been approved for forgiveness, though nearly 200,000 have applied.

The Obama plan, which began in 2010, aimed at a far broader swath of borrowers. It enables borrowers to make payments based on a percentage of income. It also allows for cancellation of loans, but only after 20–25 years of payment. It is too early to tell how many borrowers will be aided by the cancellation element of the program, but, as with the Bush program, the Trump administration is showing that much can be done through administrative efforts to undermine this program’s intent by making it difficult for borrowers to qualify.

Cancellation of student debt was among the focal points of the recent Democratic Party presidential nomination campaigns. While some presidential candidates supported full student debt cancellation, former Vice President Joe Biden recently made a more modest proposal to forgive all undergraduate loan debt for borrowers who attended public colleges and universities, as well as historically Black colleges and universities, private minority-serving institutions, and for-profit colleges that disproportionately enroll Black students. Only those earning up to $125,000 would be eligible for forgiveness. In addition, Vice President Biden supports $10,000 in across-the-board loan forgiveness as a response to the coronavirus crisis.

There’s no question this proposal goes a long way and would cancel the loans of many millions of borrowers. Loan forgiveness, however, must be complete. Partial proposals—whether they limit the amount of cancellation, limit the source of debt to undergraduates, establish income ceilings, or distinguish between public and private institutions—leave us with the same mess of rules, income verification, and administrative burdens plaguing the previous, wildly ineffective attempts and will not protect young Black people seeking to use education as a tool for social mobility. Partial forgiveness would keep in place the unfair burden carried by this generation of borrowers, who were hit hard by higher debt and a double whammy of now-two recessions. Full cancellation is simple. It doesn’t pose administrative barriers, and it avoids the stigma associated with means testing.

Moreover, full cancellation leads naturally to what we consider to be the logical next step. Once Congress cancels all student debt, it should not stop there. Just as free public elementary education has effectively been a universal (though unevenly applied) economic right since the 19th century, free higher education should become the standard in the 21st century. Most young people have little choice but to pursue a college education if they wish to raise their socioeconomic standing beyond where they started out in life. And for many, higher education is a necessary step to earning a living wage. Providing tuition-free public higher education to all Americans would eliminate the social and psychological stigma associated with the current system of financial aid and eliminate the need for future generations to carry burdensome debts.

The coronavirus pandemic, the ensuing recession, and the community response to the police killing of George Floyd and far too many other Black Americans in 2020 and beyond bring into sharp focus the barriers American society places in front of today’s generation of Black students—barriers as old as our nation that continue to this day. Student loan debt exacerbates the challenges facing young Black Americans trying to establish careers and begin families. Eliminating this debt would be an important step toward reducing racial and economic inequality in the United States and bringing about the globally competitive, educated workforce that will unleash the country’s overall productive potential. As Congress and American voters facing a presidential election think about big solutions to America’s very big problems, this is one of the most important and effective actions we can consider.