Every parent hopes that their children will have a better standard of living than their own: it is a defining feature of the American Dream. Yet this opportunity is fading for many Americans. New research by Raj Chetty, David Grusky, and Maximillian Hell (Stanford University), Nathaniel Hendren and Robert Manduca (Harvard University), and Jimmy Narang (University of California-Berkeley) shows that “absolute income mobility”—the fraction of children that are earning more than their parents—has declined over the past half century due to rising inequality. Here are some key facts from their analysis.

Download File

The-fading-American-dream

Read the PDF in your browser

Absolute income mobility has declined for Americans across the entire income spectrum

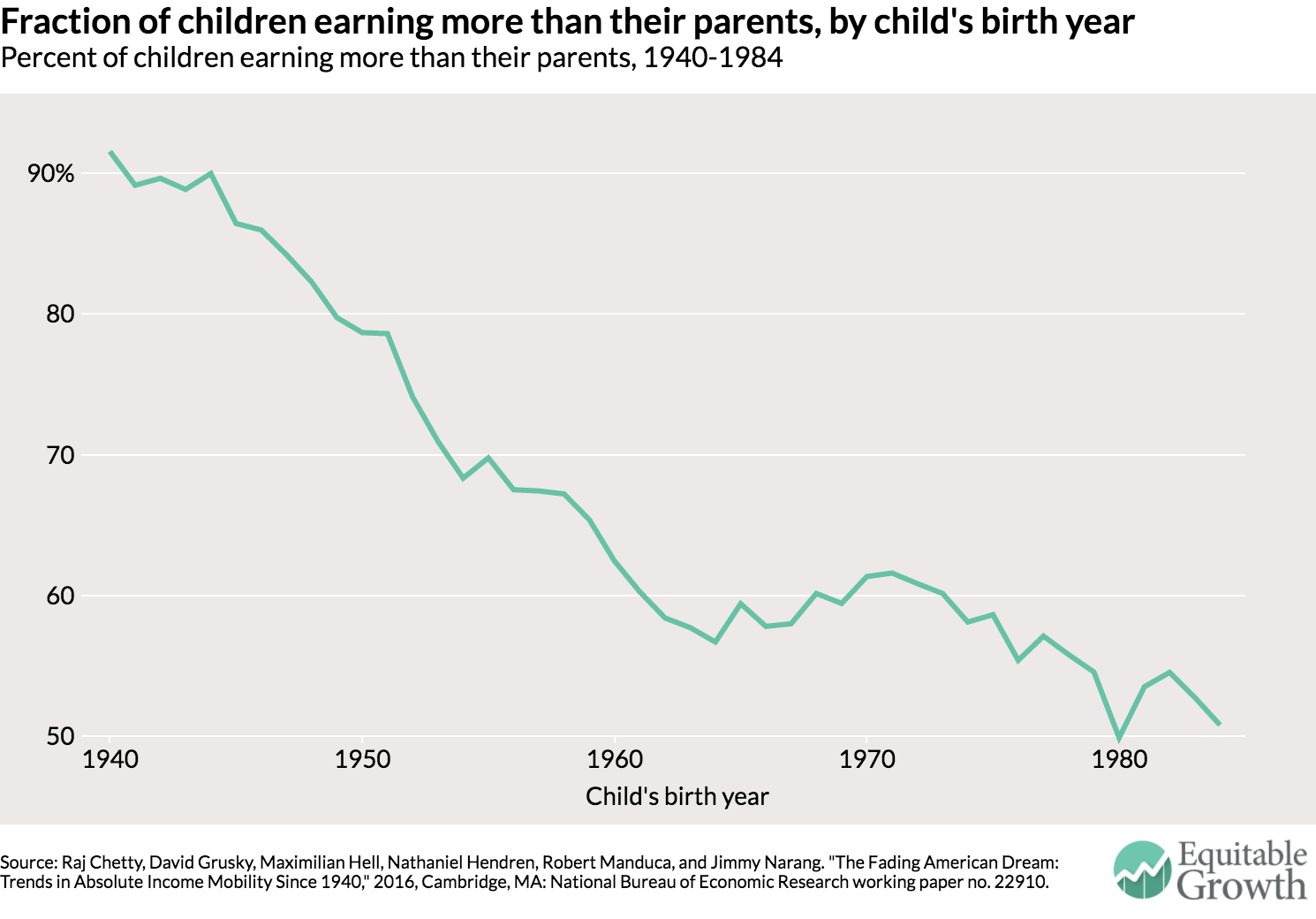

Rates of absolute income mobility in the United States have fallen sharply since 1940. Ninety-two percent of children born in 1940 earned more than their parents in inflation-adjusted terms. In contrast, only 50 percent of children born in 1984 earned more than their parents. (See Figure 1.) The downward trend in absolute mobility persists when using alternate inflation adjustments, accounting for taxes and transfers, measuring income at later ages, and adjusting for changes in household size.

Figure 1

The middle class saw the largest rate of decline. Absolute income mobility fell across the entire income spectrum, but the middle class experienced the largest declines in the likelihood of children earning more than their parents.

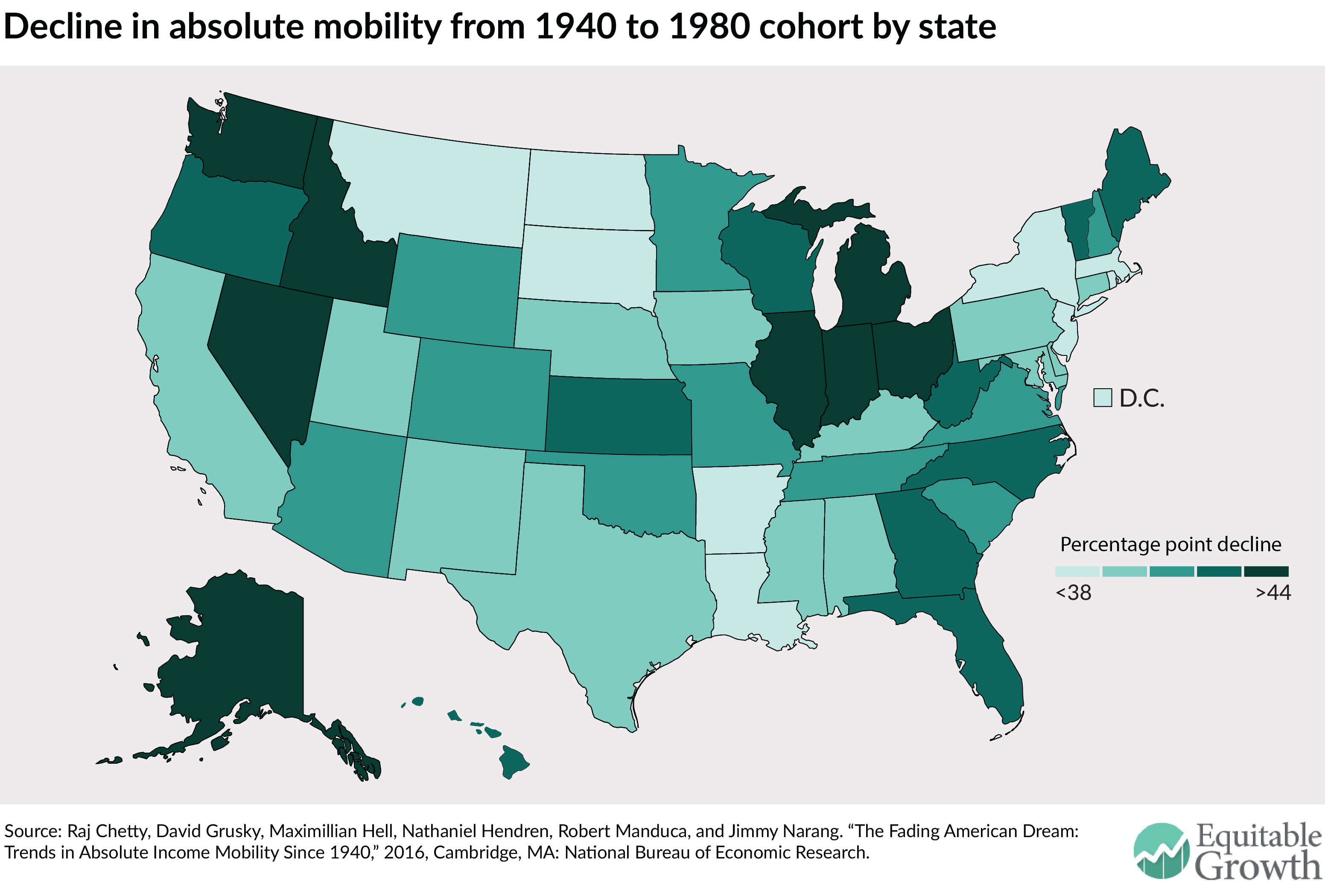

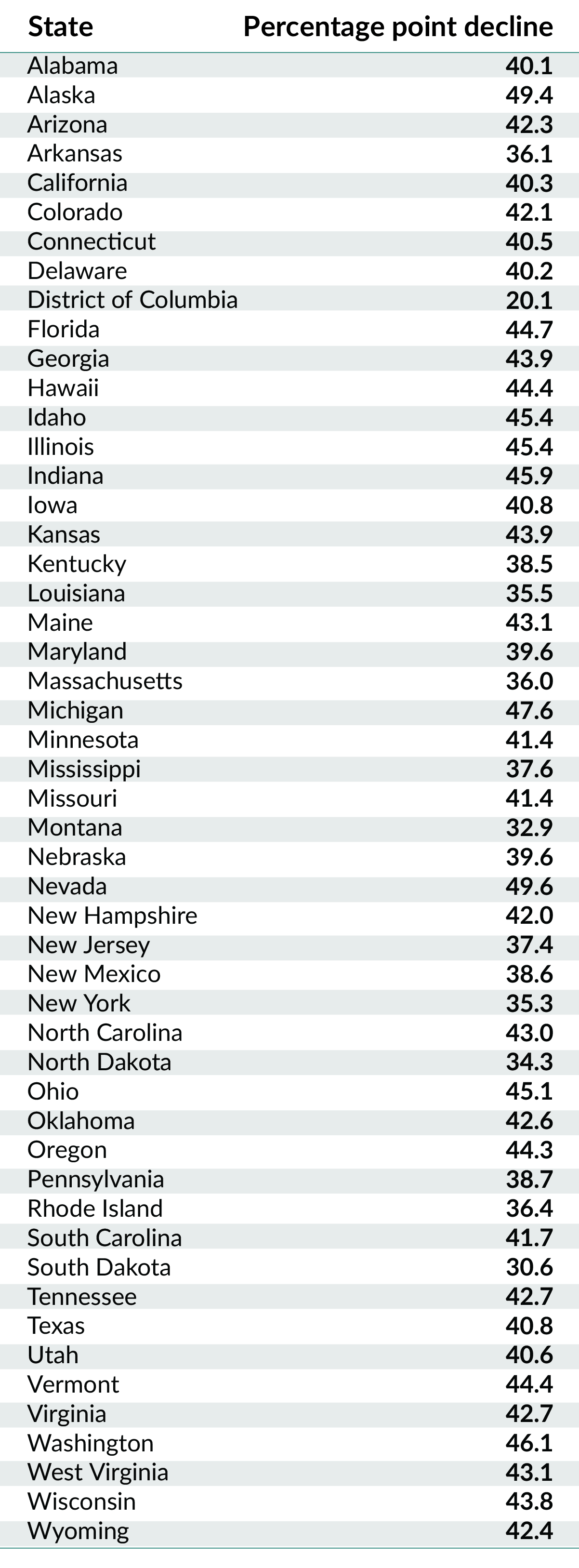

The largest declines are concentrated in Rust Belt states. Absolute income mobility fell in all 50 states and the District of Columbia, but the largest declines were concentrated in the Rust Belt states, such as Michigan and Indiana (which registered 49 and 46 percentage-point declines, respectively). The smallest declines occurred in Massachusetts, New York, and Montana, which recorded absolute mobility declines of approximately 35 percentage points. (See Figure 2 and table, below.)

Figure 2

Men’s economic prospects declined dramatically. Ninety-five percent of men born in 1940 earned more than their fathers compared to 41 percent in 1984 (a 54 percentage-point decline). The fraction of daughters earning more than their fathers fell from 43 percent of women born in 1940 to 26 percent of women born in 1984.

In order to revive the American dream, we must address inequality

The decline in absolute mobility is driven by inequality and the unequal distribution of economic growth. Children born in 1980 experienced lower growth in gross domestic product, the broadest measure of economic growth, compared to those in the 1940s and 1950s, but the authors find that the decline is absolute income mobility was driven primarily by the increasingly unequal distribution of GDP growth rather than by the slowdown in aggregate economic growth.

Higher growth rates alone are insufficient to restore absolute mobility. Because a large fraction of economic growth goes to a smaller fraction of high-income households today compared to the 1940s and 1950s, higher GDP growth does not automatically increase the number of children who earn more than their parents.

Restoring GDP growth rates to the levels experienced in the 1940s and 1950s while distributing GDP across income groups as it is distributed today (much more unequally) would increase the likelihood of children earning more than their parents to only 62 percent, reversing less than one-third of the reduction in mobility relative to what in was for children born in 1940 (92 percent).

Maintaining GDP growth at its current level but distributing it as it was distributed for children born in the 1940s would increase the likelihood that children earn more than their parents to 80 percent, thereby reversing more than two-thirds of the decline in absolute mobility.