How inequities in U.S. taxation can perpetuate systemic racism

The history of discriminatory taxation in the United States is long and storied. Writing on county governments in his in 1901 study, “The Negro Landholder of Georgia,” scholar W.E.B. Du Bois noted that “in most cases there are no tax assessors, but a county tax receiver, who receives the sworn statements of property holders as to their estates. This gives rise to wholesale undervaluation, especially in the case of the rich, and to overvaluation in the case of the very small estates of the poor.”

Du Bois also noted, according to historian Andrew Kahrl in an email exchange with me, that this problem was even more pronounced in counties where tax assessors were elected officeholders. As a result of Black disfranchisement in Georgia, Du Bois found that elected assessors were somewhat accountable to poor White landowners but entirely unaccountable to Black landowners, resulting in favoritism toward White people that, in turn, forced Black landowners to shoulder a comparatively heavier tax burden.

Local property taxation

While this favoritism might be less overt today, property tax systems still place a heavier burden on Black and Latinx property owners than on White property owners. In a working paper for Equitable Growth’s Working Paper series, economists Carlos Fernando Avenancio-León at Indiana University, Bloomington and Troup Howard at the University of California, Berkeley find that all else being equal, homeowners of color end up paying a 10 percent to 13 percent higher tax rate, on average, within the same local property tax jurisdiction than White homeowners.

In other words, Black and Latinx residents receive a higher property tax bill than homes of a similar value, paying a higher property tax rate for the same set of public goods and services. For the median Black or Latinx homeowner in the United States, this can translate to an extra $300 to $400 annually in additional property taxes. In communities with a higher concentration of people of color, the extra tax burden can be several times as large.

Though property tax laws intend for a homeowner’s payments to be proportional to the market value of their home, Avenancio-León and Howard find that the administration of home assessments leads to racially disparate outcomes in two ways.

First, they explain that when market prices and property assessments diverge, it isn’t driven by attributes of the home itself, such as the number of bedrooms or size of the home. Rather, the difference arises from neighborhood-level amenities, such as public parks or schools, which affect market prices but are inadequately reflected in property tax assessments.

Due to high degrees of residential racial segregation in the United States, Black and Latinx residents live, on average, in different neighborhoods than White residents—even within a single taxing jurisdiction. Continuing discriminatory policies have propelled White residents to tend to live in neighborhoods where amenities push market prices up, and these same policies drive Black and Latinx residents to live, on average, in areas that push market prices down. Since these amenities are not properly taken into account for property tax assessments, White homeowners end up undertaxed and Black and Latinx homeowners end up overtaxed.

Second, homeowners are typically able to contest the property assessment through filing an appeal. Avenancio-León and Howard find this process increases racial disparities because Black and Latinx residents are less likely to appeal their assessment, less likely to succeed once they have filed an appeal, and, even after succeeding, receive a smaller reduction.

Other biases in property taxation are described by Emory University School of Law professor Dorothy Brown, whose book, The Whiteness of Wealth, examines the ways tax law is far from race neutral. She notes, for example, that interest paid on mortgages are tax deductible whereas there is not a comparable deduction for renters, who tend to be disproportionately Black. This entrenched homeownership disparity is not mere happenstance, but rather a result of explicitly racist government policies such as redlining and lax enforcement that led to the 2008 foreclosure crisis.

Further, systemic racism in housing results in the homes of White residents appreciating at a faster rate than the homes of Black residents. This suggests that the value of a White-owned home will quickly outpace its property assessments. The gains made during resale are mostly tax-free, adding to an ever-growing tax break for White homeowners. Conversely, Black homeowners are more likely to lose money in their housing investment, and there is no tax deduction for these losses.

Individual income taxes

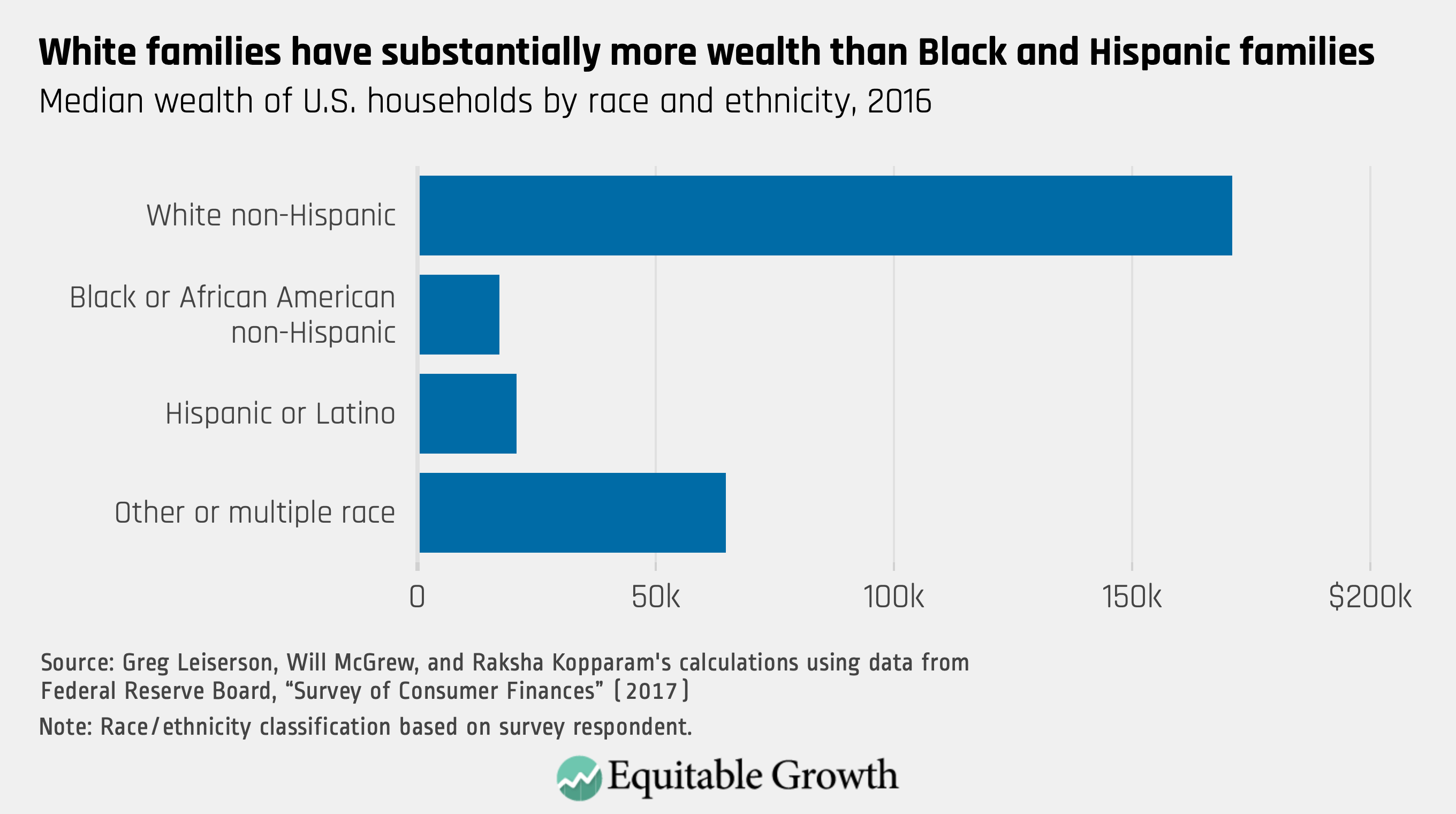

In state and federal income taxes, the value of tax breaks tends to increase as household income rises. Since White taxpayers tend to have higher incomes than Black and Latinx taxpayers, this means that White families disproportionally benefit from tax carve-outs that shield their income from the higher rates they would otherwise face. (See Figure 1.)

Figure 1

As the Center on Budget and Policy Priorities explains, the largest individual income tax expenditures in 2019 were on the provision that allows households to exclude from taxable income the value of employer-provided health insurance, the lower rates at which capital gains are taxed relative to earned income, tax breaks on owner-occupied housing, and the exclusion for employer-based retirement plans. Those who have 401(k)s are disproportionately White, while Black people are far less likely to have jobs that provide retirement benefits, healthcare, and flexible spending accounts, all of which are heavily subsidized by the tax code.

The relative lack of taxation on wealth in the United States further entrenches racial inequity. Wealth is disproportionately owned by White families because of the legacy of discrimination and inherited wealth. Income from wealth is taxed at lower rates than income from work through a variety of tax preferences, such as the lower rates on capital gains and for owner-occupied housing.

Unlike with regular income, when an investor’s wealth increases and they therefore experience a gain in income, they can legally choose not to pay taxes on that capital gain. Instead, wealthy investors can wait, even until death, at which time that income can be passed on to heirs completely tax-free because of the stepped-up basis tax exemption.

Recent efforts to weaken the estate tax in the Tax Cuts and Jobs Act of 2017 doubled the amount of dynastic wealth that can be passed on tax-free to heirs. And due to the racial wealth gap and discriminatory lending practices, people of color are less likely to own businesses, another form of wealth. This means that the majority of state and local tax benefits given to businesses tend to benefit White households.

Carl Davis, Misha Hill, and Meg Wiehe of the Institute on Taxation and Economic Policy explain that sales and excise taxes, often put forward as an alternative to the taxation of wealth or income, are the most regressive type of taxes that states levy. Low-income households, which are disproportionately households of color, must spend a larger share of what they earn to make ends meet. This therefore means that a larger share of their income is subject to consumption taxes, compared to high-income households.

In contrast, higher-income households, which are predominately White, can set aside much of their income as savings, therefore significantly delaying or entirely avoiding paying sales and excise taxes. A previous ITEP report found that in Tennessee, for example, both Black and Latinx households face average effective sales and excise tax rates (5 percent of income) that are 22 percent higher than the rate faced by White households (3.9 percent). When states rely on sales and excise taxes for revenue, they are worsening racial disparities in the state by taxing people of color more heavily than White households.

Dorothy Brown further notes that the fiction of Black people taking services and not paying taxes is widespread. This racist ideology is the very backbone of austerity economics and must be challenged head-on.

The enduring legacy of inequitable taxation requires more research and thinking into these questions, so that policymakers can address the problem directly. Policymakers will need to contend with the contours of the tax code and the ways it perpetuates systemic racism. Policy choices throughout U.S. history have contributed to racial disparities. Now, there is an opportunity to begin to make policy choices that confront these disparities.