Executive actions to coordinate federal countercyclical regulatory policy

This factsheet has been adapted from Yair Listokin’s Vision 2020 essay and his 2019 book, Law and Macroeconomics: Legal Remedies to Recessions.

Overview

Traditional macroeconomic tools—fiscal policy from the U.S. Congress and monetary policy from the Federal Reserve—are critical but not sufficient responses to the current coronavirus recession. To round out the federal government’s actions to deal with the ongoing economic downturn, executive agencies should consider how their regulatory power can be aggressively leveraged to provide a much-needed, countercyclical boost to the ailing U.S. economy. Regulatory actions that encourage banks to lend, firms to invest, and consumers to spend can increase demand and reduce unemployment.

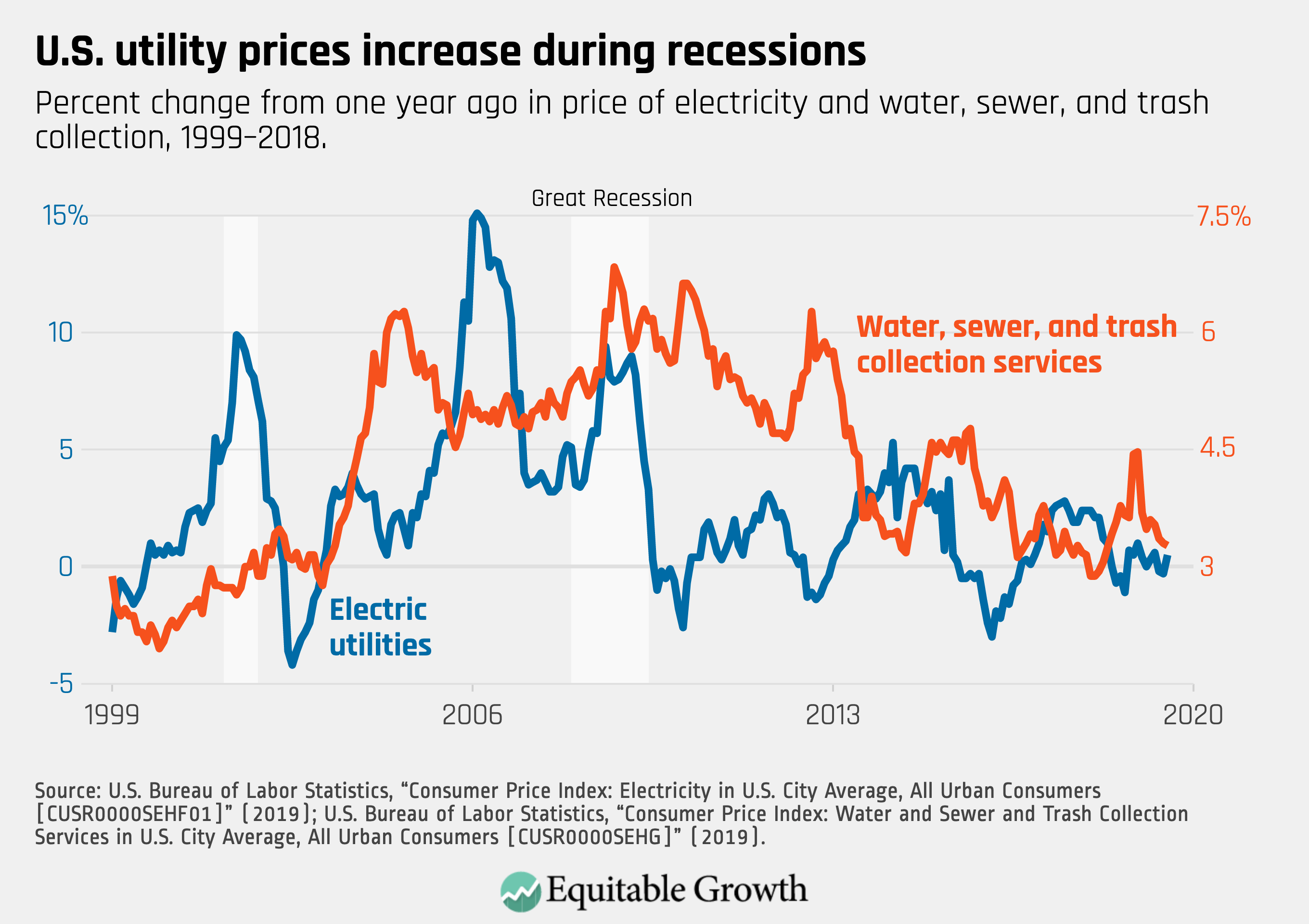

One case in point is the current regulation of utilities, implemented jointly by federal and state regulators. These rules tend to affect private-sector spending pro-cyclically by allowing for rate increases to compensate for reduced profits during recessions. As a result, retail prices for electricity, water, and trash collection increased during recent recessions. (See Figure 1.)

Figure 1

This pro-cyclical pricing effectively amounts to a tax increase on low- and middle-income families, which have a high propensity to consume, and is the exact opposite of how a smart recession-fighting, countercyclical policy would be designed. A better regulatory framework from a macroeconomic perspective would hold utility prices down during recessions but allow for higher utility prices—and profits—during economic expansions. This kind of regulation could be supported by guidance from the Federal Energy Regulatory Commission or state regulators. The state of Connecticut is pursuing a similar idea.

Other examples of regulatory actions the federal government could take to fight the coronavirus recession and other future economic downturns include:

- The Federal Housing Administration, Fannie Mae, and Freddie Mac could reduce guarantee fees on government-backed mortgages or increase allowable loan amounts in order to jumpstart mortgage origination during economic downturns. The Biden administration also could reduce interest rates or pause payments for existing homeowners with government-backed mortgages.

- The U.S. Department of Education could use its authority under the Higher Education Act to take a number of steps to reduce the burden of student loan debt during a recession, boosting the ability of otherwise struggling borrowers to spend. This could take the form of pausing payments or potentially cancelling some amount of outstanding student debt by executive action.

These two debt-focused examples build off arguments made by the authors of House of Debt: How They (And You) Caused the Great Recession, and How We Can Prevent It from Happening Again. Economists Atif Mian at Princeton University and Amir Sufi at the University of Chicago make the case that reducing consumers’ debt obligations can mitigate economic slumps because debtors are more likely to spend as a result of having more flexibility in their personal budget than are creditors.

Executive action

But knowing which of these, or other, countercyclical regulations to pursue, and predicting how the regulations will affect the macroeconomy demands expertise. Every regulator and administrator acting across many different sectors of the U.S. economy cannot be expected to have that needed expertise. As a result, effective countercyclical regulatory policy requires a coordinating office staffed by a mix of experts in macroeconomics and regulation.

President Joe Biden should create such an office, to be housed at the White House National Economic Council, by modifying the executive order that established the NEC. This new countercyclical regulatory policy office within the NEC would, in conjunction with macroeconomic experts throughout government:

- Evaluate macroeconomic conditions and the ability of discretionary fiscal and monetary policies to respond to the business cycle

- Instruct regulators to identify and implement countercyclical regulatory programs, including the reform of unintentionally pro-cyclical regulations

Importantly, the office’s purview would be limited to evidence-based, countercyclical regulations so as to not morph into a tool for indiscriminate deregulation.

Conclusion

Every federal regulatory program affects the business cycle. Countercyclical regulatory policy offers an infinite variety of macroeconomic policy options that are not subject to the constraints of monetary and fiscal policy. By paying attention to these effects and managing them through a new office within the National Economic Council, the Biden administration could stimulate the U.S. economy during the current recession and lay the groundwork for future administrations to do so as well.