President Donald Trump is attempting to fire Federal Reserve Board Governor Lisa Cook, the first Black woman to serve in that role. He probably lacks the legal authority to do so, but that is for the courts to decide. Regardless, this unprecedented move by a U.S. president directly threatens the Fed’s independence—and therefore the stability of the U.S. economy.

We take central bank independence as a given, but it was not always that way. Until the end of the 1980s, central bank independence was the rare exception—mostly in Switzerland, (West) Germany, and the United States—not the rule. But since then, it has come to dominate both thinking and practice around the world.

There have been attacks on central bank independence before, both in the United States and in other countries, and the resulting economic pain was often severe. In this country, perhaps the most egregious example of the Federal Reserve doing the bidding of politicians came in the lead up to the 1972 presidential election, when then-President Richard Nixon and Federal Reserve Chairman Arthur Burns coordinated to expand both fiscal and monetary policy in tandem to boost the economy and thereby President Nixon’s reelection chances. It worked politically. But to contain the inflationary pressures these actions unleashed, the president was compelled in 1971 to put in place the only peacetime wage-price controls in U.S. history. They were a disaster.

It is unfair to blame Burns and his colleagues on the Fed for the entire extraordinary inflation that followed. Supply shocks, especially from food and energy, were important determinants of inflation starting in 1972. Ironically, the U.S. economy is now similarly facing several potential supply shocks—from tariffs, from the potential for current deportation policy to disrupt U.S. labor supply, and even from the possibility that the wars in Ukraine and the Middle East could affect oil prices.

Monetary policy is the primary policy tool for fighting inflation. While fiscal policy can boost demand, it has less ability to curb inflation—and is virtually never used for that purpose. What will happen if we face serious inflation, and the Federal Reserve does not respond with tighter monetary policy?

Again, we should look to the past for insight. Years after the unwise and coordinated expansionary fiscal and monetary policy mix of the early 1970s, the notable and strong-willed inflation hawk Paul Volcker was put in charge of the Fed and took to fighting inflation with high interest rates. The price of taming inflation was the twin recessions of 1980 and 1981–82, caused significantly by tight money and credit. Volcker’s policies worked and restored the Fed’s anti-inflation credibility. But the pain was palpable.

The supply shocks of the 1970s and 1980s, of course, were global. So were the recessions that followed. Today’s supply shocks in the United States—from tariffs and shrinkage of the labor force—are, by contrast, mostly homemade. If President Trump succeeds in his campaign to eviscerate the Fed, our main bulwark against inflation will be weakened, if not destroyed.

Policymakers in a central bank subject to short-term political influence may face pressures to overstimulate the economy to achieve short-term output and employment gains that exceed the economy’s underlying potential. Such gains may be popular at first, and thus helpful in an election campaign, but they are not sustainable and soon evaporate, leaving behind only inflationary pressures that worsen the economy’s longer-term prospects. Thus, political interference in monetary policy can generate undesirable boom-bust cycles that ultimately lead to both a less stable economy and higher inflation.

The Federal Reserve’s Open Market Committee is technocratic, not political. The seven governors are appointed by the usual political appointee process: nominated by the president and confirmed by the U.S. Senate. But they are expected to check their politics at the door—and they generally do. The 12 regional Reserve Bank presidents are not politically appointed.

These technocrats base their interest rate decisions on data, theory, and lessons from history, not on political calculations. That does not mean they never err. But it does mean that the Fed’s errors are not designed to help the party in power—which would generally mean setting lower interest rates no matter what. President Trump, for example, has been clamoring for a 1 percent federal funds rate for years, though markets do not believe that will happen. If they did, expected inflation, and hence interest rates, would be much higher right now.

If Congress and/or the courts do not stop the president from eviscerating the Fed’s independence, it stands to put the U.S. economy at risk of a 21st century version of the 1970s and ‘80s, with high inflation, high unemployment, and stagnant economic growth—a true recipe for economic disaster.

Did you find this content informative and engaging? Get updates and stay in tune with U.S. economic inequality and growth!

Correction: Freddie Mac and Udemy contacted the Washington Center for Equitable Growth on March 18, 2026 and April 2, 2026, respectively, to say they no longer had business relationships with Betterworks. Freddie Mac said Betterworks “provided technology project management” services and did not provide pay or surveillance practices. Udemy said that it “ceased being a Betterworks customer on May 30, 2024” and did not use AI-driven tools to set or influence employee wages. We have updated the piece to reflect this. The researchers’ methodology rigorously analyzed the products offered by AI early-stage companies that specialize in workforce management, employee monitoring, and labor performance and identified those at “high risk” for enabling algorithmic pay systems. They similarly identified employer characteristics, such as reliance on performance metrics, that would enable an employer to use algorithmic pay systems. The original piece included a lengthy list of companies across industries whose characteristics would allow for algorithmic pay systems that have or have had contracts with “high risk” AI vendors. Because we cannot confirm the specifics of these contracts, we have removed reference to specific companies.

Workers’ pay is increasingly shaped by opaque algorithms and artificial intelligence systems, shifting compensation decisions away from human managers, clear legal standards, and collective bargaining. This phenomenon—known as algorithmic wage discrimination1 or surveillance pay2—was first documented in app-controlled ride-hail and food-delivery work. Now, it is spreading to a range of other industries and services.

Our first-of-its-kind audit of 500 AI labor-management vendors suggests that traditional employers in industries including health care, customer service, logistics, and retail are now using automated surveillance and decision-making systems to set compensation structures and to calculate individual wages. Without policy interventions, we fear that these practiceswill become normalized, thus growing income uncertainty, entrenching bias, and eroding wage-setting transparency.

Government enforcement agencies and legislators working together should affirmatively and proactively prohibit these practices. This can be done by legislatively proscribing the use of real-time data to automate workforce compensation structures (such as tiered bonuses, performance-based incentives, or penalties for low productivity) and to automate wage calculations. To ensure a positive correlation between hard work and fair pay, wage-setting practices must be, at the very minimum, predictable and scrutable.

In this issue brief, we first examine how surveillance pay practices work and where they are increasingly deployed in the U.S. economy. We then present our audit findings in detail before turning to our policy recommendations to ensure fairness and transparency in setting and calculating workers’ pay.

How surveillance pay practices work and where they are becoming more prevalent in the U.S. economy

Nicole picked up a part-time job with ride-hailing firm Lyft Inc. to help cover her mortgage payments after its adjustable interest rate increased.3 After a long week of working at her regular day job in health care, she would wake up early on Saturday mornings and begin her second job—a ride-hail shift at Lyft. For a few weeks, Nicole would drive until she earned $200—the amount she needed to make her higher loan payment—and then go home.

Within 2 months, however, she found that it took her longer to earn that target amount of $200 per shift. For some inexplicable reason, her daily gig earnings dropped by as much as $50. Though she maintained a high driver score and worked harder than ever, over the course of the following year, Nicole’s Saturday wages dropped an additional $50. To make ends meet, she picked up a shift on Sundays, too. It seemed like the longer Nicole worked for Lyft, the less she earned.

On-demand workers such as Nicole were among the first to experience what has become known as algorithmic wage discrimination, also referred to as surveillance pay: digitalized wage-setting in which firms use large swaths of granular data, including data gathered in real time through automated monitoring systems, to establish compensation brackets and/or to calculate individual pay.4 Studies of on-demand workers dating back to 2016—including those initiated by workers themselves—have found that the introduction of these black box AI systems to determine remuneration has consistently led to low, erratic, and uncertain incomes for app-controlled ride-hail and food delivery workers. Perhaps unsurprisingly, this has led to increased worker stress, higher workplace injury rates, and decreased overall job satisfaction.5

Under surveillance wage systems, different people may be paid different wages for largely the same work, and individual workers cannot predict their incomes over time. These pay practices—especially those that rely on panoptic worker surveillance and on algorithmic intelligence or machine learning systems—invert the deeply held maxim that long, hard work steers toward higher wages and economic security. Not only has pay for app-controlled jobs, such as Nicole’s work for Lyft, decreased over time, suggesting shifting compensation brackets within firms, but industry research also affirms what workers like her have described: People who work longer hours are paid less per hour.

Alarmingly, this uncoupling of hard work and secure, fair pay is no longer just a concern for app-controlled or “gig” workers. The intense pace of funding for AI firms that specialize in labor management has fueled the growth and sale of automated products that aim to increase workforce efficiencies through the introduction of monitoring and decision-making systems that may affect or determine wages. But because software companies do not typically advertise their systems’ abilities to lower labor costs by generating dynamic wage structures and calculations, little is known about these products, their features, and the individual and social implications of their use.

Questions therefore abound. Which sectors of workers are experiencing disruptions in how they are monitored on the job, evaluated for their performances, and paid? What are the capabilities, limitations, and risks of these systems? And, critically, are these systems helping or hurting everyday workers?

To begin to fill this knowledge gap and identify the sectors most likely affected by algorithmic wage discrimination systems, we did a first-of-its-kind analysis of 500 AI vendors who market machine-learning products for use in labor management. Through a risk evaluation of these 500 firms, we then identified a subset of 20 vendors whose products are highly likely to use machine-learning systems to generate surveillance pay. To our knowledge, this is the first systematic study of the spread of algorithmic wage discrimination practices outside of the context of gig work.

Unlike set wages that are determined through contractual negotiations between employers and employees, wages determined by machine-learning systems are generated in real-time, rendering them variable, uncertain, and inscrutable to the workers who rely upon them. Despite this, the vast majority of products in our research detailed below also lacks any transparency or feedback mechanisms. Thus, though the experiences of people such as Nicole were once limited to app-controlled jobs, they are now likely to be spreading to other, more traditional sectors of employment, fundamentally changing the relationship between work and pay for workers across the U.S. labor market.6

The potential impacts of these findings are startling. The spread of surveillance pay practices to critical, human-centered industries such as health care and customer service not only changes the relationship between hard work and fair pay, but also meaningfully alters workplace norms and culture, impacting how patients are treated in hospitals and how consumer problems and interests are addressed. Lessons from research on app-controlled work suggests that the introduction of surveillance pay incentivizes workers to perform in ways that lower labor costs but may de-center patient well-being or customer satisfaction.

The potentially catastrophic consequences, then, of surveillance pay extend far beyond its implications for the insecurity and unpredictability of individual worker pay.

The surveillance pay practices enabled by AI vendors and deployed by their customers

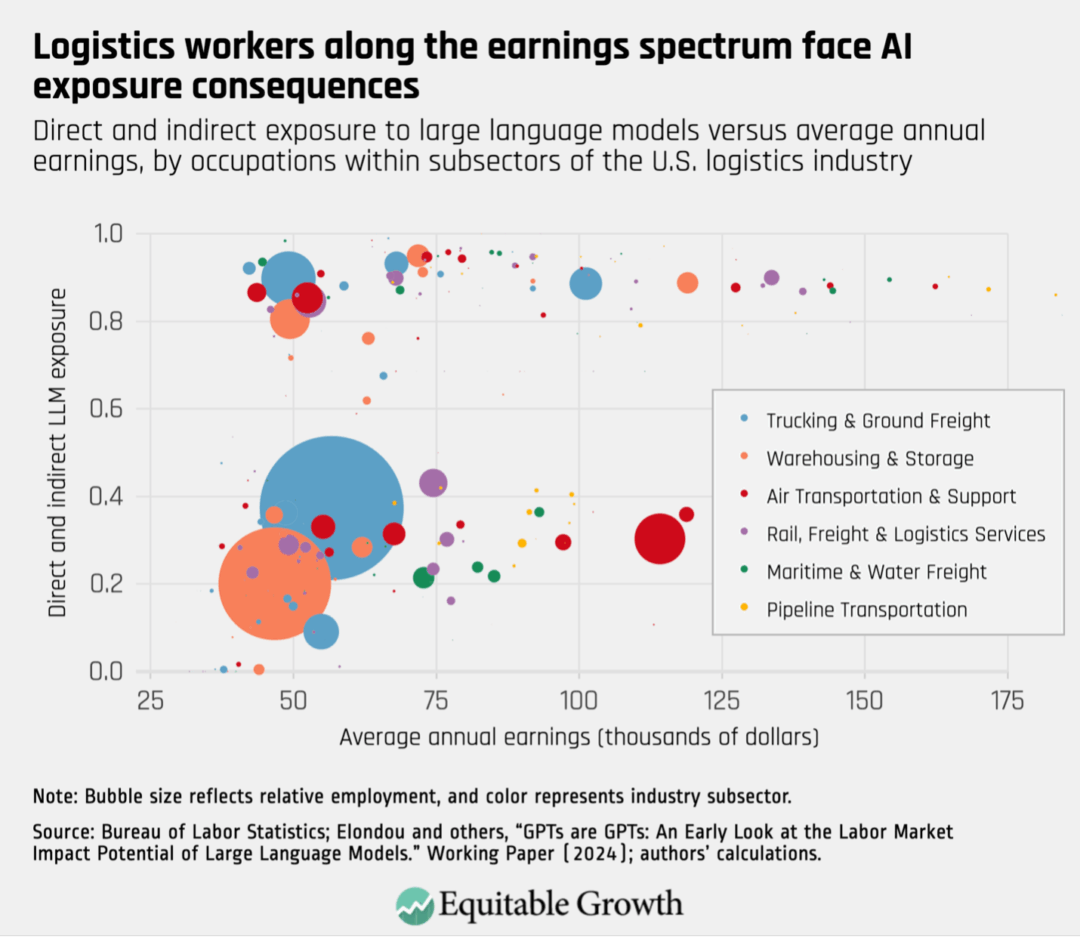

Analyzing the initial 500 AI firms using the parameters listed in our methodology (See Box above), we identified 20 vendors whose products we determined to be at high risk for producing algorithmic wage discrimination. While algorithmic pay practices began in the transportation and delivery sectors, our findings suggest that they have spread to workforce management in a number of industries, most prominently health care, customer service, logistics, and retail.

Of the 20 AI vendors at high risk for enabling surveillance-based wages, five created products specifically for customer serviceworkforce management (including one focused on call centers); four designed products for monitoring and managing workers inhealth care; one focused specifically on workforce management for last-mile delivery in logistics; and one targeted management in the manufacturing sector. The remaining nine vendors developed cross-sector tools that include platforms designed to be integrated across a range of industries, including retail, finance, education, transportation, and technology.

These vendors typically market their products as general-purpose workforce optimization or performance management systems. While not tied to a single sector, they are often deployed in metric and performance-intensive environments and can be integrated with existing HR and payroll systems, thus enabling algorithmic wage-setting across a wide range of workplaces. Overall, these cross-sector tools and platforms create a new standard of workforce surveillance, with plug-and-play solutions for performance monitoring, decision-making, and compensation management across diverse industries.

We found that some vendors embed into their platforms the ability to not only adjust workers’ pay in real time but also steer how pay tiers and bonus structures are set over time. These processes are frequently automated with limited-to-no human review.7 A vast majority of the vendors we reviewed (16 out of 20 firms) also links their products directly into payroll or HR systems. Most products give workers zero visibility into the data or logic behind pay calculations, and only a small subset offer built-in channels for employees to review or contest algorithmic decisions. Finally, we also found that many vendors apply identical performance benchmarks across diverse roles and contexts, ignoring factors such as task complexity, local market conditions, and worker accommodations (in possible violation of disability laws and protections).

Across the vendors and products we reviewed, we found that all relied on an extensive amount of data collected on and through their workforce and customer markets. Whether the firms quantified subjective metrics, such as performance and customer satisfaction, or whether they aimed to analyze real-time behavior for purposes of allocating tasks or determining quotas, the products all relied on data collection and processing. The systems did not provide a means for workers to access the personal or social data that are collected. They also lacked mechanisms to help workers understand and contest either the accuracy of the data collected or the decisions of the machine-learning systems.

The use of these products to suppress wages and produce variable income is concerning, as are the collateral effects. The collection and storage of these workforce data implicate workers’ privacy, ability to negotiate higher pay in this job or their next one, and their federally protected right to organize their workplaces.

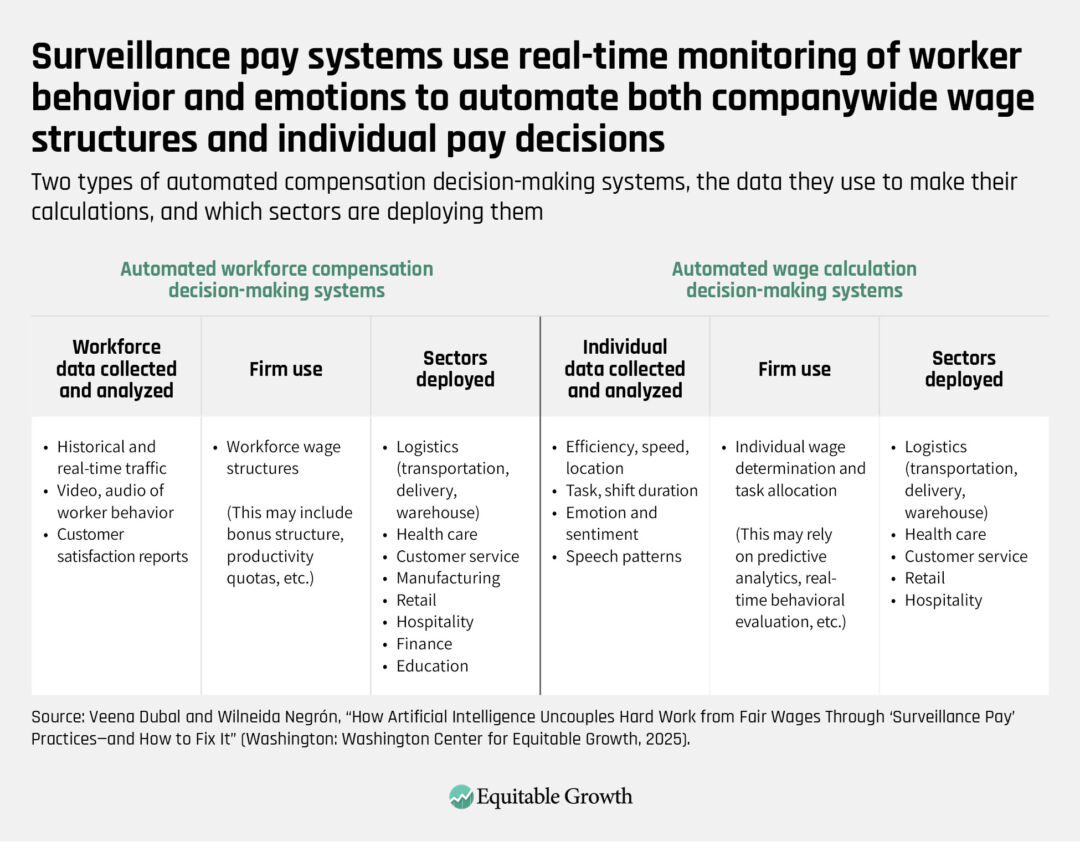

To better understand our findings—and the practices and harms that emerge—we propose a framework to understand surveillance pay systems. Some of these systems produce frameworks for automated workforce compensation, while others produce automated wage-calculation decisions, and still others do both. In our taxonomy, automated workforce compensation systems are those that create dynamic but broad frameworks affecting wage distribution and restrictions across a workforce. These automated systems are less likely to produce day-to-day variability for individual workers, but in so much as they yield wage bands or brackets, we expect that they are a driving factor in workforce wage suppression and wage discrimination.

Similarly, automated wage-calculation systems enable firms to make dynamic wage adjustments based on the system’s machine-learning analysis of an individual’s behavior, temporal and spatial market conditions, and other unknown factors. These systems can be integrated with automated workforce compensation systems. Both together and individually, these processes are likely to exacerbate the impacts of long-term wage stagnation and worker insecurity.

In Table 2 below, we further detail this taxonomy, the types of data both systems may rely on, how the data are used, and in what sectors the tools are currently deployed. The two AI surveillance processes are most likely to overlap when automated compensation structures are used to structure wages, such as worker-pay tiers, base rates, or compensation models based on performance, commissions, fixed or hourly pay, or salary, and where workers are simultaneously rewarded or punished through wage calculations based on a granular analysis of their performance, behaviors, and risk factors. (See Table 2.)

Table 2

Our analysis, for example, suggests that some AI vendors, such as med-tech startups Aidoc Medical Ltd and ARYAHealth, appear to focus more on using machine learning systems shape wage structures. Other AI vendors—among them call center-tech firm Level AI, governance and compliance-focused Cognitiveview, and conversation-analytics firm Uniphore—have developed products with notable workplace decision-making capabilities, including task allocation and performance-based reviews, which very likely result in automated wage calculations.

AI vendors that create and sell products that enforce strict productivity benchmarks, customer satisfaction metrics, and key performance indicators include Insightful, dba Workpuls, Netomi Inc., AssemblyAI, and kore.ai, as well as Level AI and Uniphore. But because these firms’ products are not integrated into metric-based pay systems, we suspect their customers use their products for automated workforce compensation decision-making.

Still other AI vendors, among them Symbl.ai, Betterworks Systems, Inc., and SupportLogic, offer products that enforce productivity benchmarks and key performance indicators and appear to integrate dynamic pay models with real-time metrics, such as performance-based compensation, bonuses, and penalties. Since earnings are frequently adjusted based on performance data, customer interactions, and behavioral analytics, this approach is likely to result in automated wage calculations, resulting in wage variability and unpredictability for workers.

Notably, our research finds that employers across the customer service, finance, manufacturing, computer science, and health care sectors have or have had contracts with these vendors, including major U.S. companies. Yet public visibility into how employer-vendor relationships function in practice is often limited. These tools can spread under conditions of opacity, limited disclosure, and weak worker visibility into how performance data may shape pay, scheduling, or discipline. This limitation is itself part of the accountability problem concerning AI-driven workforce systems.

How surveillance pay practices match up to existing U.S. labor laws and traditional workplace practices

In the United States, four major federal laws govern wages and working environments. Surveillance pay managed by algorithmic wage systems—both that set workforce structures and that automate wage calculations—may violate the letter and spirit of these laws. The impacts of low and variable wages on workplace safety and the ability of employers to use automated monitoring systems to detect worker organizing and punish it with low pay are instances in which surveillance pay practices may directly violate existing employment and labor laws.

Even in instances where the wage outcomes of automated compensation structures and automated wage calculations do not directly violate minimum wage laws, overtime regulations, labor protections, or anti-discrimination laws, their impacts offend the legislative intent behind wage regulations—namely, the creation of predictable, living wages, in which people are paid equally for equal work. In this section of our issue brief, we describe the federal laws that currently govern wages and the working environments produced through wage-setting practices and detail the ways that algorithmic wage-setting practices that power surveillance pay may be upending these protections and the norms they have produced.

Minimum wages and compensable time on the clock

The most widely known federal work law governs how long workers labor and how little they can be paid. In response to labor agitation created by widespread unemployment and poverty during the Great Depression nearly 100 years ago, Congress passed the Fair Labor Standards Act, a centerpiece of the New Deal legislation of the 1930s. The law sets minimum wages, overtime, and record-keeping laws and sets the floor (not the ceiling) for wages across the country. The federal minimum wage is set by Congress and has been a staggeringly low $7.25 per hour since 2009. In the face of congressional inaction and changing standards of living, many states and local municipalities have periodically passed legislation to set and raise the local minimum wage to near living wage levels of about double that amount.

Algorithmically determined wage structures and calculations do not necessarily violate minimum wage laws, but, to date, they have been used by firms to make it more difficult to identify violations and to enforce the law. In app-controlled ride-hail and food-delivery work in the United States, for example, firms have maintained that their workers are only entitled to pay after work is sent to them, not when they are waiting for work. This piece-pay practice disconnects time and pay, making it impossible for individual workers to know how much they might earn for work over any period of time.8

The Federal Labor Standards Act abolished piece-pay in many industries. Yet these algorithmic wage structures and calculations raise the problem anew by setting wages that are variable and difficult for workers and enforcement agencies to decipher.

What’s more, some of the firms that use digitalized piece-pay practices are trying and succeeding at amending state laws to make it legal to discriminate between workers in this way. In California, for example, the ride-hail and food-delivery firms with the largest market shares—Uber Technologies Inc., Lyft Inc., DoorDash Inc., and Maplebear Inc.’s Instacart—sponsored and won a 2020 referendum9 to cement their algorithmic wage discrimination practices into state law. Under the law, workers laboring for so-called transportation and delivery network companies are formally exempt from state minimum wage and hour protections and instead guaranteed 120 percent of the minimum wage of the area in which they are working—but only after they have been disseminated work, not while they are awaiting this work.

After this firm-sponsored law was enacted in 2020, a worker-led study found that Uber and Lyft drivers in California were making $6.20 per hour, with an hourly wage floor of about $4.20.10 In contrast, in 2025, the California minimum wage is $16.50 per hour.

Even the study’s authors were surprised by the low algorithmically determined earnings because they said that most drivers work until they hit a certain wage target, not accounting for the tolls, airport fees, gas, insurance, and vehicle depreciation costs that they incur in the process. And, in another California worker-led experiment, Uber and Lyft drivers themselves affirmed what they had long suspected—that they were being allocated different wages for the exact same work, a topic we turn to in the next section.11

Together, automated workforce compensation and calculation systems violate the spirit of local minimum wage laws and may also violate the Fair Labor Standards Act. In practice, the California model exists in many other states where local legislatures have cemented the status of ride-hail and food-delivery workers as “independent contractors” for the purposes of state law. But state laws do not preempt FLSA obligations. As of the time of writing, the federal government has not initiated an enforcement action in any state.

Equal pay for equal work

In response to social and labor movements and persistent age, disability, gender, and race-based wage gaps, Congress has passed laws over the past seven decades that, in theory, guarantee that workers doing broadly similar work earn the same wages for that work. The idea of “equal pay for equal work” emerged from the women’s movement and civil rights movement in the 20th century, and can be found most clearly in Title VII of the Civil Rights Act of 1964, the Age Discrimination in Employment Act of 1967, the Equal Pay Act of 1963, and the Americans with Disability Act of 1990.

Together, these laws prohibit differential pay becauseof race, color, religion, sex, national origin, age, or disability. They have been notoriously difficult to enforce, and identity-based wage gaps remain persistent in the U.S. labor market. Still, they create baseline aspirations for wage-setting in the labor market.

Algorithmic wage practices often violate the spirit of “equal pay for equal work” laws, and in some cases, they may also be violating the letter of the law. Indeed, wage-calculating AI is rooted in pay discrimination—differentiating between workers on the basis of any number of known and unknown factors, including, as discussed above, predictive analytics that attempt to determine a worker’s potential tolerance for low pay.

While some AI vendors claim their products enabling surveillance pay using their algorithmic wage-calculation software are based on objective analysis of workers’ performance, their systems often do not provide mechanisms for workers’ feedback or share clear information on how workers are evaluated in relation to their pay. Anecdotal evidence suggests that algorithmic performance analysis may also produce uncorrectable errors, resulting in unfair outcomes.

One case in point was included in the Biden administration’s “Blueprint for an AI Bill of Rights.” The White House Office of Science and Technology included the following example in the blueprint’s Safe and Effective Systems section: “A company installed AI-powered cameras in its delivery vans in order to evaluate the road safety habits of its drivers, but the system incorrectly penalized drivers when other cars cut them off or when other events beyond their control took place on the road. As a result, drivers were incorrectly ineligible to receive a bonus.”12

In turn, these undetectable and unfair errors may have devastating impacts on a worker’s ability to put food on the table or to pay rent for their homes. Studies suggest that low-income workers rarely contest wage violations in offline labor markets. If the wage errors themselves are inscrutable, then, by extension, workers in online labor markets would be even less inclined to do so.

These practices—in addition to resulting in discriminatory wages between any two workers doing broadly similar work at the same time and in the same way—may also exacerbate existing identity-based wage inequalities. Though Uber rarely shares pay data with third parties, research produced alongside Uber’s own chief economist, Jonathan Hall, found that “although neither the pay formula nor the dispatch algorithm for assigning riders to drivers depend on a driver’s gender,” women working for Uber make roughly 7 percent less than men.13 As one of us has argued elsewhere, “On its own terms, the publication of this finding signals a troubling moral shift in how firms understand the problem of gender discrimination and their legal responsibility to avoid it.”14

Collective organizing and bargaining

The National Labor Relations Act of 1935 created a nationwide industrial system in which collective worker organizing became a protected right for most workers and collective bargaining became systematized through national oversight.15 The law resulted both in the growth of labor power and, over time, a decrease in industrial unrest. Notably, at the behest of Southern Democrats at the time, who hoped to maintain the racialized nature of Southern plantation economies, the law excluded both domestic and agricultural workers from its protections, and Congress later also included a carveout for independent contractors.16

African American civil rights advocates at the time objected to the exclusion of these largely Black and minority workforces, understanding this exclusion as having devastating impacts on any post-Civil War gains made by these workers. They maintained that lower wages for Black workers would, in effect, “relegate … [African American workers] into a low wage caste,”17 and “destroy any possibility of ever forming a strong and effective labor movement.”18

The use of wage-calculating algorithms to differentially set wages in sectors comprised largely of workers of color, as is the case with platform-enabled ride-hail and food-delivery firms, has indeed had the impact of not only creating a second tier of wages—or, as one of us has called it, “a new racial wage code”—but it has also disrupted efforts at collective organizing. As one of our studies that explores the wage experiences of Uber drivers found, “The fact that different workers made different amounts for largely the same work was a source of grievance defined through inequities that often pitted workers against one another, leaving them to wonder what they were doing wrong or what others had figured out.”19 This, in turn, may be used as an employer tactic to violate the spirit of the National Labor Relations Act, making it more and more difficult for workers to collectively organize.

Additionally, algorithmic wage discrimination may be used to retaliate against workers for protected union-organizing activities. A union of Japanese workers, for example, has alleged that algorithmic wage-setting software has been used to target union organizers, effectively punishing those workers with lower wages.20 Of course, the nature of the black box systems that firms use to set wages and wage structures make it difficult to understand or to challenge an outcome such as this. In the United States, the use of an algorithmic wage-setting system to punish organizers would be unlawful retaliation under the National Labor Relations Act.

Safety and health standards at work

Workers in the United States have the broad and often-unrealized right to safe and healthy workplaces under the Occupational Safety and Health Act of 1970. Extant empirical evidence from around the globe suggests that algorithmic wage practices utilized by firms have resulted in high rates of psychosocial and physical injuries.21 These outcomes can be traced, in part, to the way workers are paid through algorithmic wage structures and setting systems.

Cornell University’s Worker Institute and the Worker’s Justice Project/Los Deliveristas Unidos together found that in New York City, 42 percent of delivery workers “reported non-payment or underpayment of their wages, with almost no recourse because of how the firms control them through digital machinery.”22 The under and non-payment of wages set and distributed by algorithms result in workers laboring in ways that make them vulnerable to risk-taking and injury. As one of us has argued elsewhere:

[T]he launch of ride-hailing companies in cities has been associated with a three-percent increase in the number of traffic fatalities. Working long and hard, with low wages and little predictability… may give rise to workplace dangers, including more crashes. A joint study of the California Public Utilities Commission and the California Department of Insurance found that ride-hailing accidents in that state alone generated 9,388 claims that resulted in a combined $185.6 million loss in 2014, 2015, and 2016.23

The low and unpredictable wages created through surveillance pay practices powered by these algorithmic systems can also result in emotional injuries. The fear of not earning enough, to accept all work without fail because not doing so will result in lower wages or termination, and working at great speeds to earn more can all cause psychosocial injuries. In a large study of workers who received algorithmically set wages in the European Union, researchers “found that workers suffered high rates of depression relative to other jobs.”24

Federal laws and some state protections place the responsibility on employers to create safe and healthy workplaces, but algorithmic wage-setting systems create new health and safety problems that have yet to be addressed robustly at the state or federal level.

Recommendations to ensure surveillance pay practices do not harm workers and depress their earnings

As detailed above, algorithmic wage discrimination practices are proliferating across an increasing number of sectors in the U.S. economy. The large body of evidence produced by researchers who study these practices in on-demand work settings suggest that firms that use these systems may risk violating the existing employment and labor protections detailed in the previous section. The practices may also violate antitrust and consumer laws.25

Yet, to date, few agencies have attempted to enforce these laws at the federal or state level. Opportunities to do so remain, however, even if wages do not fall below the minimum wage or state agencies do not have data to determine a violation of anti-discrimination laws. Why? Because if surveillance pay practices lend themselves to health and safety violations—for example, by incentivizing workers to labor longer in ways that cause physical and psychological injuries—then state and municipal agencies may enforce existing health and safety protections.

With the extraordinary speed of production of AI for workforce management, and the implications of algorithmic wage-setting practices across the U.S. labor market, we believe that both state and federal legislators are well-situated to step in. One approach, for which we advocate here, is to craft legislation to ban the use of real-time data to both automate workforce compensation structures and to automate wage calculations. Wage-setting has traditionally been transparent—at least to the workers receiving said wages—and the new opacity of wage structures and wage calculations creates new and alarming harms.

A second, less comprehensive approach, is for legislators to focus specifically on banning the use of automated wage calculation systems. Such laws should extend both to employers and hiring entities who use independent contractor labor and should apply to wages for all the time that their employees work and wait for work. In this context, providing for both private and public enforcement will make firms more reticent to engage in these practices.

Critically, we argue that legislation mandating transparency of algorithmic wage-setting systems alone will not do enough to mitigate these harms. Existing case studies of workers attempting to use their General Data Protection Regulation rights in the European Union to understand wage and termination practices underscore transparency’s limitations. These workers in the EU argue that even when they are given explanations for how they are paid, the systems change too frequently to effectively use this information to create income predictability. They also generally lack the power and technical expertise to use data releases to locate and correct violations of practice or law.26

Conclusion

Scholars, policy analysts, lawmakers, and labor advocates alike have raised significant concerns about the immediate and long-term financial insecurity of workers in the United States. Observers have identified macroeconomic trends, including historical wage stagnation,27 inflation’s effects on real wages,28 and widening structural and geographical wage disparities,29 as contributors to national problems of precarity and immobility. Despite significant productivity growth since the 1970s, most U.S. workers’ wages have stagnated, leading to a significant productivity-pay gap.30 This means workers have not benefited from productivity and efficiency gains arising from the growing use of technology for labor management.

More recently, these structural challenges have been compounded by the growing discretionary use of novel technologies at work. Developments in artificial intelligence and other digital machinery have led to well-documented problems, including worker displacement,31 reduced job quality,32 and the perpetuation of bias and discrimination in the labor market.

Across the political spectrum, workers and politicians agree that hard work should be positively correlated with fair pay. This essay has identified the empirical reality that machine-learning systems that very likely uncouple fair pay and hard work, leading to wage uncertainty, discrimination, and suppression, are rapidly spreading across the U.S. labor market. This should alarm analysts and lawmakers concerned about economic inequality.

The American dream—however fraught and unreachable for many—is directly under attack. In this moment of income insecurity for most U.S. workers, legislators across the aisle should be motivated to write laws at both the federal and state level to address the problems endemic to the algorithmic wage-setting systems that power inequitable surveillance pay practices.

About the authors

Veena Dubal is a professor of law and legal anthropologist at the University of California Irvine School of Law. Her research focuses broadly on law, technology, and precarious workers, combining legal and empirical analysis to explore issues of labor and inequality.

Wilneida Negrón is a political scientist, technologist, and strategist whose work bridges labor rights, emerging technology, and public policy. As the architect behind field-defining initiatives on workplace surveillance and ethical innovation, she has shaped how funders, organizers, and policymakers address the future of work and tech accountability.

Did you find this content informative and engaging? Get updates and stay in tune with U.S. economic inequality and growth!

The Washington Center for Equitable Growth announced today that it has awarded funding to seven scholars seeking to better understand the effects of economic inequality in the United States and who are interested in engaging beyond academia to inform evidence-backed policymaking. These researchers are all in the early years of their careers, either currently enrolled in a Ph.D. program or those who received their degrees in the past 8 years.

The funded research projects range in topic, from the housing crisis to child care to supply chain resilience. Below, we detail each grant awarded funding in this year’s cycle.

Ph.D. students

The following projects are headed by students currently enrolled in Ph.D. programs at a U.S. university:

Market Power in Homebuilding and the U.S. Housing Shortage. Anna Croley at Yale University will study housing shortages and market power in the United States. She seeks to answer the question of whether market power among homebuilders can explain the undersupply of new housing, particularly entry-level units, or whether their economies of scale reduce costs.

Empirical Evaluations of Child Care Subsidy Policies. Serena Goldberg at Yale University aims to inform the policy design of child care subsidies for the U.S. child care sector to improve access to and affordability of high-quality care while also improving the wages of care workers. First, she will evaluate the effect of reimbursement-rate policies on local maternal labor force participation, child care worker wages, child care prices, and quality of care. Then, she will simulate the effects of counterfactual subsidy policies on parents’ use of child care, worker wages, mark-ups, and the distribution of quality.

Determinants of Irregular Worker Schedules. Whitney Zhang at the Massachusetts Institute of Technology will examine the impacts of schedule instability on workers. Utilizing third-party scheduling data that is well-suited to investigate schedule volatility, she seeks to document novel facts about worker schedules, evaluate the effect of predictive scheduling and minimum wage laws on schedule-related outcomes for firms and workers, and understand the welfare effects of the regulation of schedules on workers.

Pre-tenure academics

The projects below are led by early career scholars who received their Ph.D.s within the past 8 years:

The Distribution of Federally Insured Mortgages: 1935–1975 Evidence from Local Land Records.Omer Ali of the University of Pittsburgh seeks to create systematic data on the mortgage activity of the Federal Housing Administration and Veterans Administration—two federal agencies whose policies are understood to have contributed to racial disparities in homeownership, wealth, and neighborhood opportunity in the United States. He will digitize and publicly release a dataset of FHA-insured and VA-guaranteed mortgages issued between 1935 and 1975 to assess who received these loans, how they were distributed across neighborhoods, and whether FHA and VA insurance accelerated White flight and exacerbated segregation.

Corporate Governance and Labor Market Outcomes. Andrew Baker of the University of California, Berkeley will study a new potential explanation for the declining relative earnings of workers: changes in corporate governance. He will use the Longitudinal Employer-Household Dynamics, Longitudinal Business Databases, Census of Manufacturers, and the Annual Survey of Manufacturers to analyze changes generated by activist hedge fund investors, then changes in equity-based compensation of managers, and their impacts on worker outcomes.

Unlocking Opportunity: The Long-Term Effects of EITC-led Migration on Families and Intergenerational Mobility. Jacob Bastian of Rutgers University will evaluate the role of the Earned Income Tax Credit in supporting families’ decisions to move and outcomes for both parents and children. Leveraging detailed linked administrative data—including the American Community Survey, Current Population Survey, and individual tax records—the author will conduct a longitudinal analysis of U.S. families’ migration patterns and economic outcomes.

Supply Chain Resilience and Economic Growth: Evidence from Global Shipping Disruptions. Diego Känzig of Northwestern University will provide new causal evidence on the economic implications of supply chain disruptions. Leveraging the fact that global supply chains rely on maritime trade, which depends on a few critical choke points, he will identify disruptive incidents, which are plausibly exogenous to the U.S. economy, and then isolate the market impact of the disruption using high-frequency financial data. He will then use these shipping cost surprises to identify a structural supply chain shock.

Supporting the next generation of researchers

Equitable Growth is committed to seeding and supporting the next generation of economic and social science scholars, particularly those who are interested in how their research relates to policy. Preference in this year’s application process was given to those students and early career scholars eager to work with the media and policymakers to translate their findings for a broader audience and wider impact.

We thank all of this year’s applicants and are looking forward to following along as the recipients of these awards produce results that can help shape the U.S. policy environment for years to come.

Did you find this content informative and engaging? Get updates and stay in tune with U.S. economic inequality and growth!

Estimates in this brief were generated July 21, before the announcement of trade deals with Japan and the European Union. All data and code used in the Equitable Growth tariff analysis, including instructions to update the analysis with the latest tariff rates, can be found in our Github repository.

Overview

During his first term in office, President Donald Trump in 2018 made good on a campaign pledge to introduce new U.S. tariffs on imported goods33—steel and aluminum in particular—in a purported effort to protect domestic jobs and shrink the trade deficit. Those tariffs largely targeted products from China—the world’s second-largest economy, largest single source of U.S. imports, and the United States’ preeminent geopolitical rival.

In the subsequent administration, President Joe Biden maintained many of the Trump tariffs and enacted a series of new targeted trade restrictions intended to protect U.S. industry and national security.34 The moves reignited a popular debate about the function and fairness of tariffs—a debate that weighed the costs for U.S. consumers in the form of higher import prices against the benefits for U.S. workers in the form of increased demand for domestically produced goods.

Many economists argued that targeted tariffs, and specifically those on some auto imports, for example, could benefit domestic industry without pushing the overall consumer price level higher. That logic was upended, however, when President Trump returned to the White House for his second term, promising national “liberation” through a series of sweeping tariffs against countries deemed to cheat the United States in international markets.35

Rather than targeting a narrow industry or set of commodities, as he did in his first term, the second Trump administration’s tariff policy covers nearly all dutiable imports, with some limited exceptions. Energy and potash from Canada, for example, are subject to a lower tariff rate than the overall rate imposed on goods from Canada. Separately, U.S. automakers were awarded credits they can use to offset the cost of tariffs on imported materials, though these credits will be phased out within 3 years.36 (These commodity-specific exemptions are omitted from the baseline analysis in this issue brief due to limited public data on how industries source inputs.)

President Trump’s far-reaching tariff policy is sure to have deep and often contradictory economic consequences for the United States and the world. Some U.S. industries may indeed experience a revival, as their products become more competitive in domestic markets compared to tariffed imports. But it is unclear whether those potential benefits will outweigh the costs of tariffs, not only for consumers facing higher prices but also for U.S. workers themselves.

Retaliatory tariffs enacted by other countries on U.S. exports, for example, will harm U.S. workers as foreign demand for U.S. goods dries up. Also harmful to U.S. workers are the tariffs on intermediate inputs imported by domestic industries, such as the raw and finished metals used in auto assembly.

This Equitable Growth analysis focuses on the question of how tariffs on imported inputs could raise costs for U.S. industries and workers, and how those costs might be distributed geographically. More specifically, this analysis compiles data representing:

How U.S. industries use and import commodities as inputs

How a given tariff regime could impose additional input costs on U.S. industries

How those additional costs could impact employment in key industries and geographic regions

While it does not directly calculate the cost of tariffs or their effects on employment, it does draw an empirical picture of how tariff costs could be distributed across industries, relying on a few key assumptions drawn from the available data.

In the spirit of open and equitable research, this analysis is published alongside raw and finished datasets, as well as the Stata code required to reproduce this work and generate new datasets of interest. The code grants users the flexibility to compile datasets of interest by industrial and geographic specificity and produce metrics to judge industrial exposure to imports and tariffs. (More information on the Stata code can be found in the GitHub repository.37)

Tariffs pose a particular threat to U.S. manufacturing

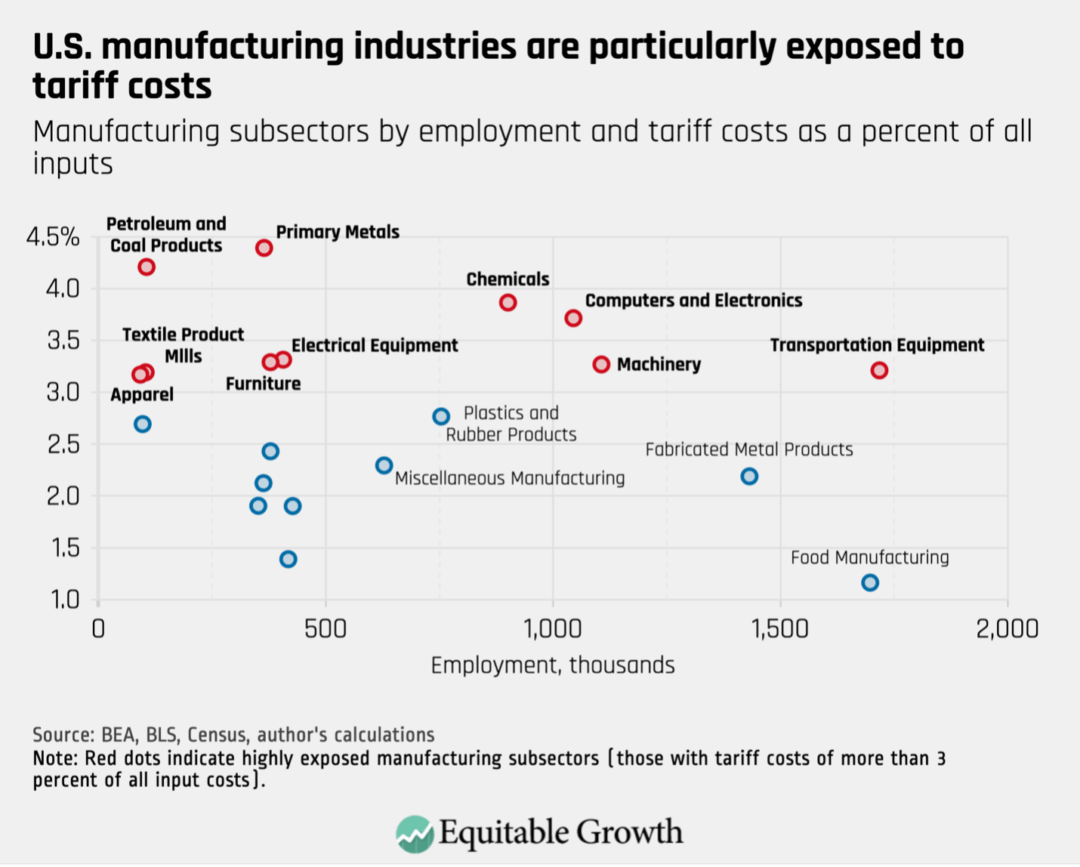

Our analysis finds that U.S. manufacturing industries are clearly more exposed to tariffs on intermediate inputs compared to other U.S. industries, undermining a key Trump administration argument about the effectiveness of tariffs. Manufacturing industries—including the politically and economically sensitive vehicle production sector—will face increased input costs imposed by the very tariff regime intended to boost their competitiveness with imported final goods (finished cars, in the vehicle production example).

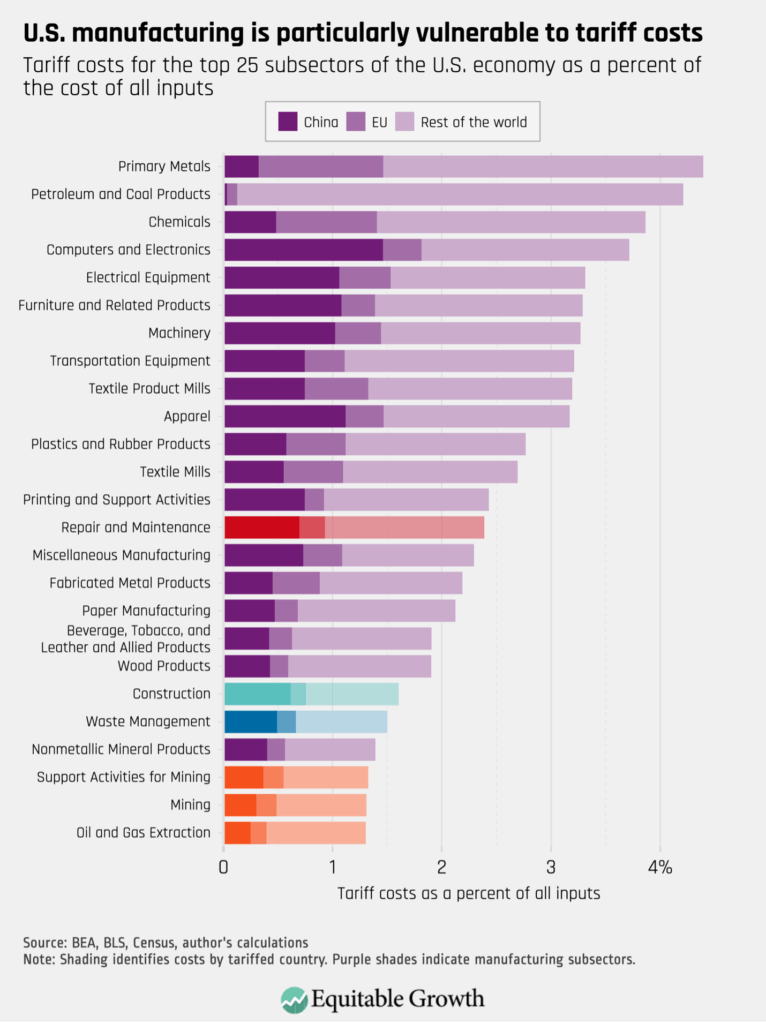

Importantly, manufacturing would likely be the most vulnerable industrial category regardless of the commodity or country specifics of a given tariff regime. Some manufacturing subsectors may be less harmed than others, but the overall reliance of the sector on imported inputs means manufacturing will face greater intermediate tariff costs compared to other industries. Indeed, of the top 25 subsectors of the U.S. economy that are most affected by tariffs, 19 are in manufacturing. (See Figure 1.)

Figure 1

Before diving into more detail, it is important to note that this analysis produces two distinct yet important metrics to predict or track the impacts of a given tariff regime:

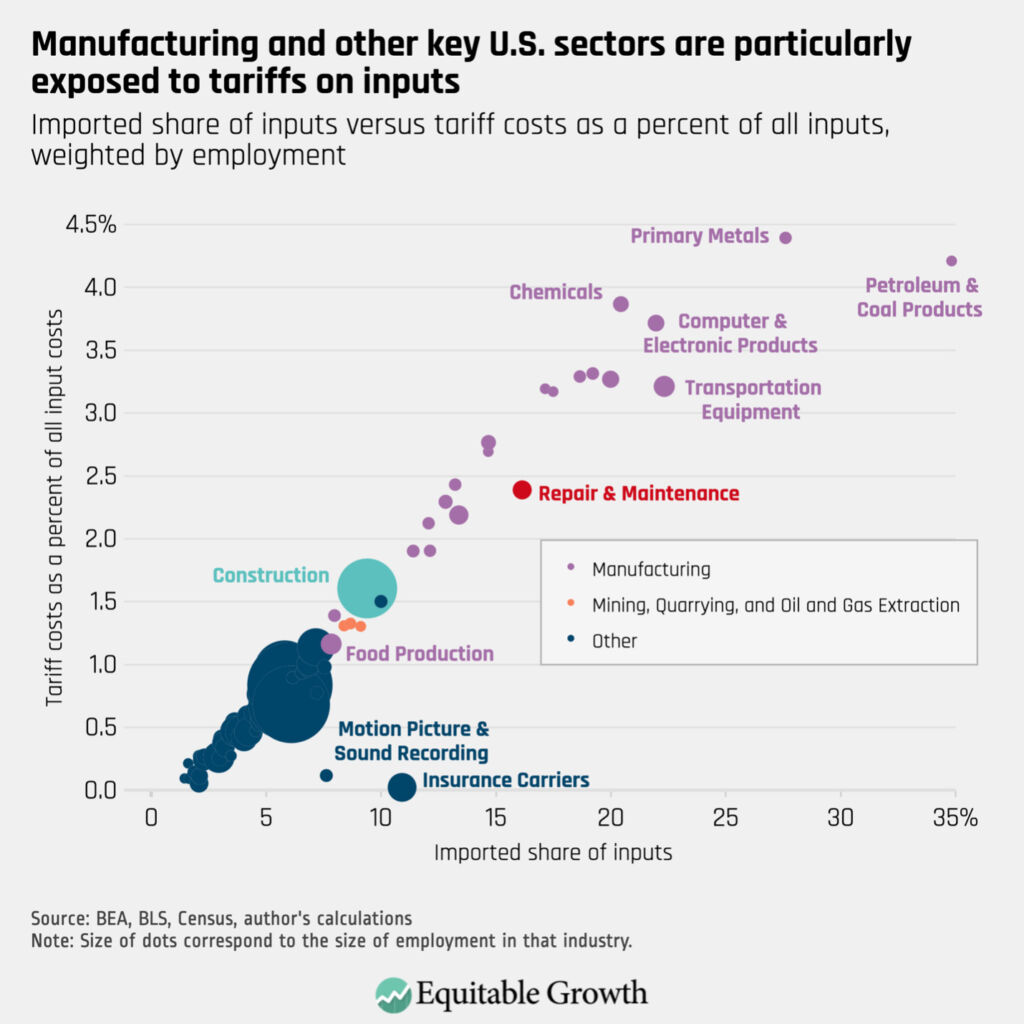

An industry’s imported share of inputs, or the fraction of that industry’s inputs that are sourced from outside the United States. This measure represents an industry’s exposure to tariffs generally, before the application of any specific trade policy. In this analysis, this import share value is first generated at the specific industry-commodity level, showing import intensity for each input, before being aggregated at the industry level.

Tariff costs as a percent of all input costs. After trade policy has been layered into the analysis, estimates of the costs of tariffs can be generated at the industry level, as a fraction of an industry’s total input costs. These tariff cost estimates are a representation of the hit to the profitability or bottom line of an industry as a result of a specific tariff regime. The baseline tariff regime modeled in this analysis includes all reciprocal tariffs due to come into effect in August, except those on Canada and Mexico (see the Appendix for further discussion).

Figure 2 below plots the exposure rate of certain industries to tariffs using each of these two measures. The tariff cost measure reflects tariffs both threatened and enacted by the Trump administration, as discussed further in the appendix section. The measures produce nearly identical pictures of industrial exposure to tariffs, as the diagonal plot line makes clear. As we can see, both measures show particular vulnerability for the manufacturing sector, with the tariff cost measure showing most manufacturing industries facing cost increases of 2 percent to 4.5 percent. (See Figure 2.)

Figure 2

A few outliers do exist, including the movie and sound recording industry and insurance carriers (the dark blue outliers on the bottom of the graph) and the petroleum and coal products industry (the purple dot in the upper right corner). The former two are more exposed in the import share measure compared to the tariff cost measure because while they import an unusually large amount of inputs, they are primarily nondutiable goods: Insurance products imported by insurance firms and foreign films imported by domestic movie companies. The latter is an outlier because the overwhelming majority of coal and petroleum imported inputs are sourced from countries (mostly Canada, but also Mexico and Saudi Arabia) that are subject only to the 10 percent base tariff rate, compared to the much higher reciprocal rates imposed on many other countries, including China.

Impact on upstream industries

The construction industry (the teal bubble in Figure 2) faces relatively lower tariff exposure compared to manufacturing subsectors but still substantially more than other industries. This is due in large part to imports of raw materials that are often sourced from China. The repair and maintenance industry (seen in red in Figure 2), which includes auto repair shops and commercial and household equipment repair, is also highly exposed to tariffs. Mining and fossil fuel extraction (marked in orange in Figure 2) are less exposed to tariffs than manufacturing but are meaningfully more exposed than the rest of the U.S. economy.

These three groups—construction, repair and maintenance, and mining and extraction—in addition to manufacturing, are upstream in the U.S. economy, meaning their products are often used as inputs by other industries further down a supply chain or are used as infrastructure in the facilitation of economic exchange broadly. Domestic vehicle parts manufacturers, for example, will face additional costs as they import raw metals and finished components to produce engines, transmissions, brakes, and other systems.

Some of those domestic vehicle parts will be sold (with a mark-up to account for the tariff cost) to domestic auto producers and the domestic repair and maintenance industry. This will impose additional costs on these domestic producers, on top of the tariffs they have to pay directly on their own imported inputs.

In the case of construction, additional costs of imported materials will burden the building of transportation infrastructure, as well as commercial and industrial facilities. It also means residential construction will become more expensive, and projects will slow or halt, constraining the supply of new housing and potentially putting upward pressure on housing prices. These second-order costs are not captured in this analysis but could be an important focus of future work.

Impact in highly exposed industries

The particularly high tariff exposure of manufacturing and construction industries is important for the U.S. economy not only because those industries are upstream but also because they employ large numbers of people. More than 8 million workers were employed in construction in an average month in 2025, while nearly 13 million people were employed in manufacturing industries—more than 1 in 10 U.S. workers.38

Numerous factors outside the purview of this analysis will dictate how domestic employers pass down tariff costs to workers, including union coverage, gender and race, and other workforce characteristics. The U.S. Bureau of Labor Statistics says, for example, that more than 10 percent of construction workers and 7.9 percent of manufacturing workers are covered by a union contract,39 meaning those workers might be marginally more protected against tariff-caused job losses, compared to the average worker in the U.S. private sector, where the union coverage rate is 5.9 percent.

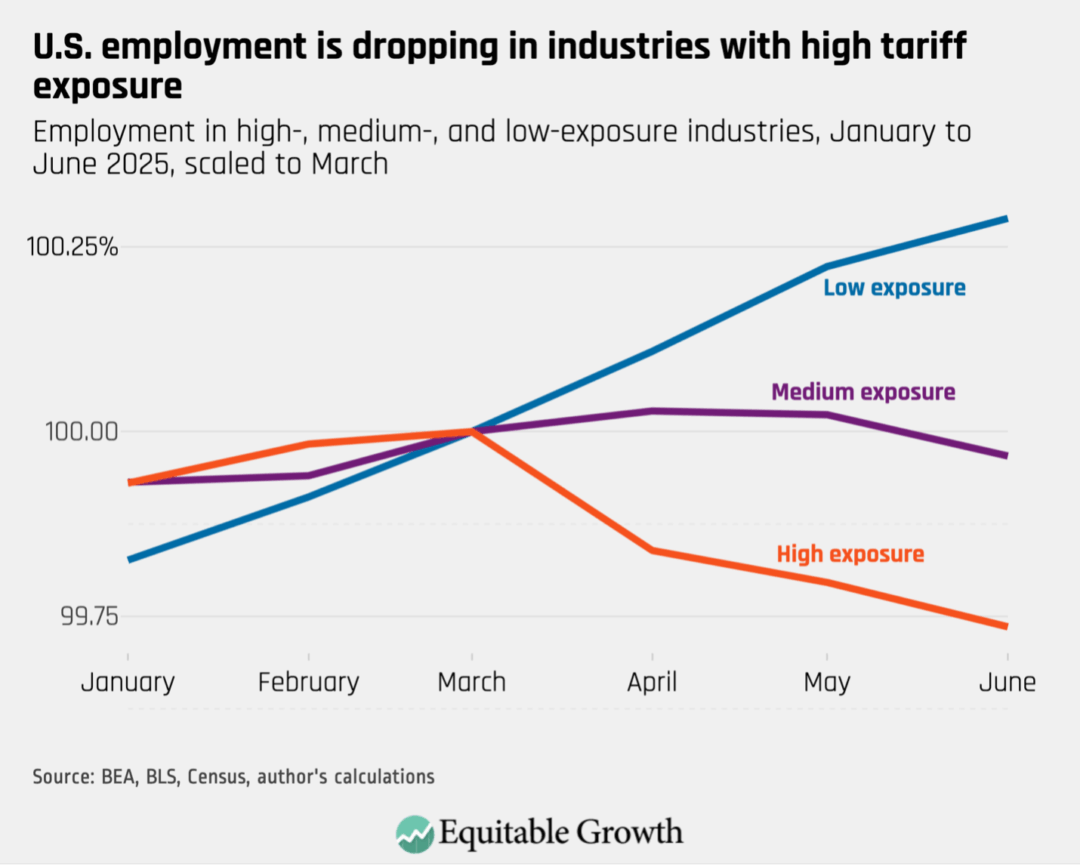

It is unclear whether those protections will be sufficient for firms facing estimated tariff-related hits to their bottom lines of 2 percent to 4.5 percent, as is the case in most manufacturing industries shown in Figure 2. Already, seasonally adjusted employment in highly tariff-exposed industries is beginning to decline. (See Figure 3.)

Figure 3

Many highly exposed industries also are important to the stated national security goals of this and prior administrations—namely, the protection and cultivation of a domestic semiconductor and computer tech industry, including AI development, and reinvigoration of domestic energy production. Without targeted tariff carveouts, as the Trump administration has sporadically attempted, these nationally strategic industries will suffer.

Computer and electronic product manufacturing, for example, is one of most highly exposed subsectors of the U.S. economy, importing more than 20 percent of its inputs and facing an estimated more than 3.5 percent increase in total input costs because of the current tariff regime. Similarly, though domestic energy production is less exposed—a little less than 10 percent of inputs are imported and estimated cost increases are close to 1.5 percent—even a modest shrinking of profit margins could disrupt production in an industry known for its high sensitivity to prices. (See Figure 4.)

Figure 4

While these industries important to national security may see a boon in tariffs on competitor goods, those same tariffs will increase input costs and mitigate—or even eliminate—any leg up in the market, creating political complications for the Trump administration.

Geographic impact of tariffs

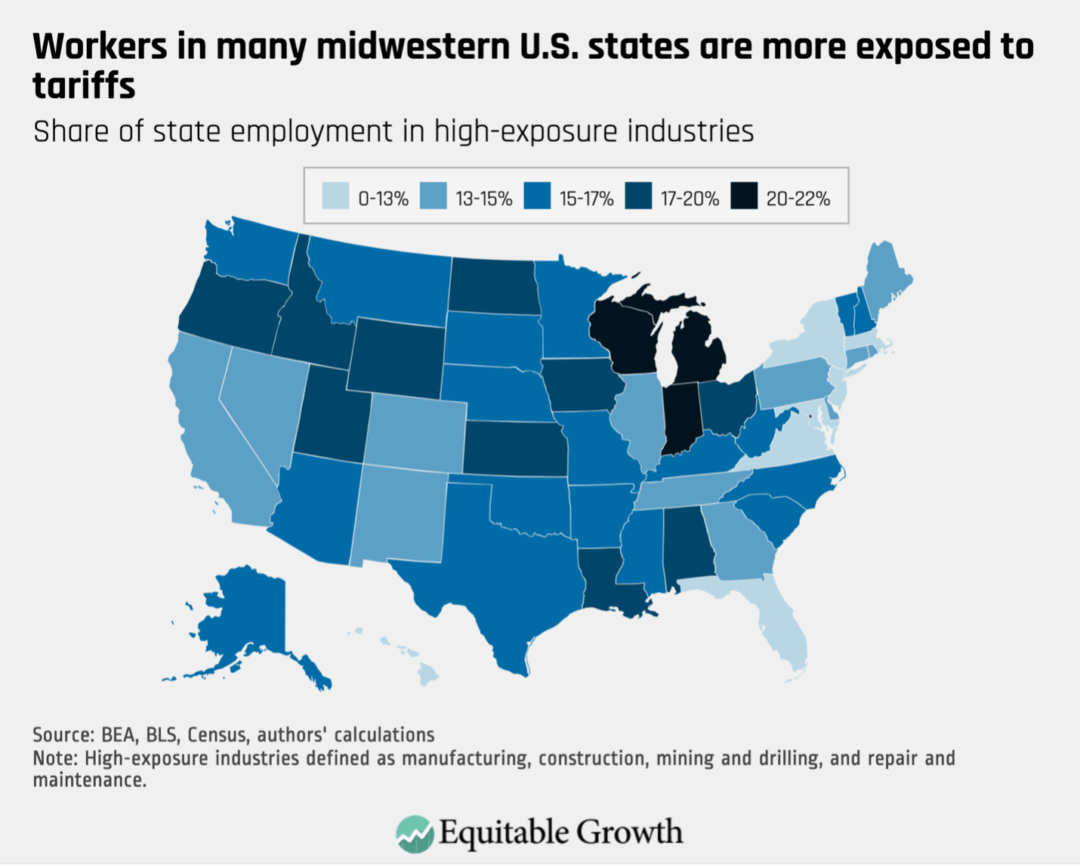

Also likely to produce political complications for President Trump is the geographic incidence of tariffs. A core limitation of this analysis is that U.S. Census Bureau import data only captures a shipment’s initial destination rather than its final destination, so it is difficult to know how states will be directly impacted by tariffs on various countries or commodities.

To paint a general picture of how states could be differently impacted by the current tariff regime, we use employment by industry in each state to construct a measure of relative industrial employment compositions. We determine states to be highly exposed to tariffs if a large share of state employment is in industries with high tariff exposure. Using this metric, we find that midwestern states, including Michigan, Wisconsin, and Indiana, will likely face higher tariff costs compared to other states. (See Figure 5.)

Figure 5

These high tariff costs could put pressure on many workers and their families in these politically important states, where votes on the margin have swung elections for one candidate or another in recent elections.

Areas for future research

This analysis should be seen as a foundation or a framework for estimating the potential industry-level effects of a given tariff and trade policy regime, providing several avenues for further research. The first option would be to combine this analysis of tariffs on intermediate inputs with comparable industry-level estimates of the effects of tariffs on final goods—both U.S. tariffs on imported competitor products and retaliatory tariffs imposed by other countries on U.S. industries’ exports.

Similarly, the positive effects of import substitution on domestic industry—for example, when U.S. steel producers see higher revenue as steel-consuming domestic industries reshore supply chains—are not captured by this analysis and could similarly be incorporated to provide a more complete picture of tariffs’ effects on the U.S. economy.

Additionally, tariff policy does not exist in a vacuum. The recently passed Republican budget reconciliation law will have broad and deep impacts on the U.S. economy, including on industries impacted by tariff policy.40 Many of the industries likely impacted by the budget law, including hospitals and doctors’ offices hurt by $1 trillion in Medicaid cuts,41 are not particularly exposed to tariffs directly. But the medical equipment and supplies manufacturing industry is both highly exposed to tariffs and potentially harmed by the law’s Medicaid cuts due to slowing demand for equipment from hospitals and doctors across the country.

As discussed above, workforce characteristics—including union coverage, race and gender identity, and immigration status—could determine how easily U.S. employers pass down tariff costs to workers in the form of stagnant wages, layoffs, or firm closures. Incorporating industry-level workforce characteristics from the Current Population Survey or other data sources would greatly improve the predictive capacity of this analysis.

Conclusion

This baseline prediction of how U.S. industries will be impacted by tariffs on imported inputs finds the manufacturing sector is highly exposed to tariffs, despite some exemptions granted by the Trump administration. Also relatively vulnerable to tariffs are construction, mining and energy production, and repair and maintenance.

The more than 23 million people employed in 2024 in these more exposed industries could face wage stagnation or even job losses as their employers seek to pass down the costs of tariffs onto workers. Considering the geographic concentration of the impact of the tariffs in midwestern and other electorally important states, the impact of the Trump “liberation” tariffs could reach beyond the economy or the specific industries most vulnerable to trade policy shifts.

Future research is needed to expand and further detail the potential impacts of tariffs and trade policy. This analysis can be used as a stepping off point for many avenues of future study, as it offers a novel interlinked dataset and code accessible to other researchers.

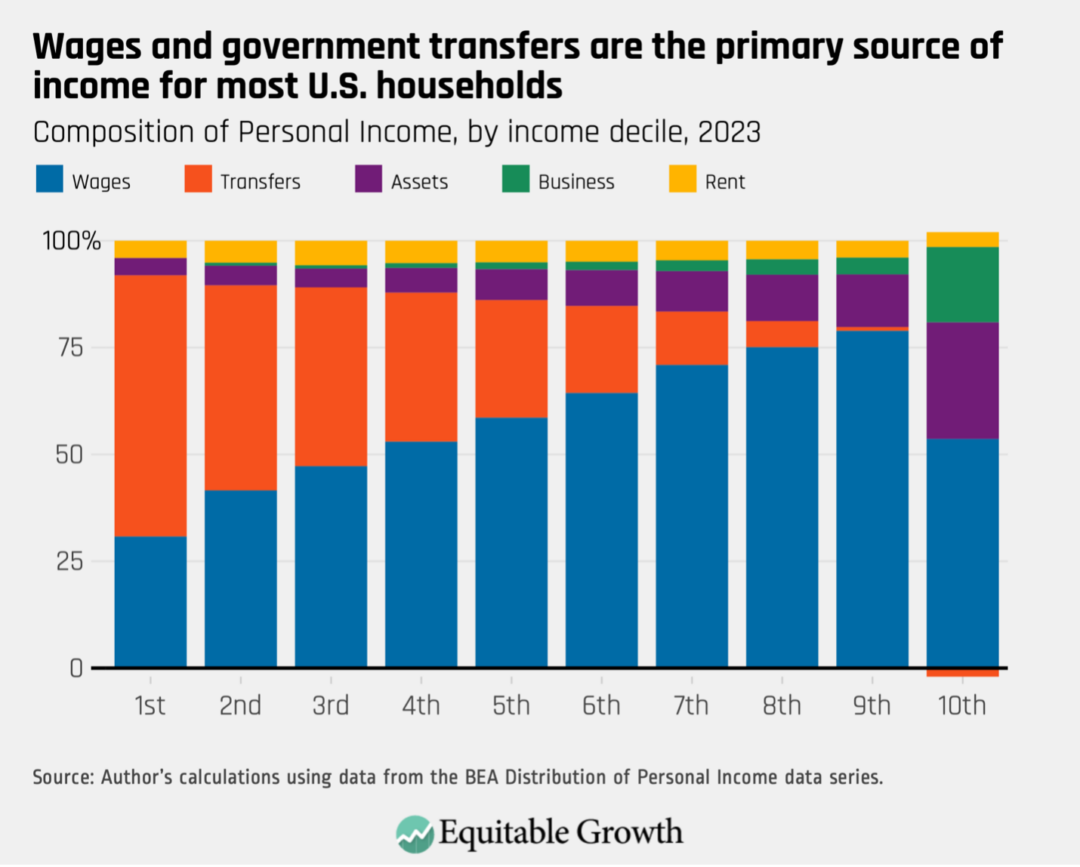

The Washington Center for Equitable Growth’s recently launched U.S. Inequality Tracker uses data from the U.S. Bureau of Economic Analysis to show how income and wealth inequality have evolved in the 21st century. Our analysis of the data through 2023 shows that income inequality has been relatively stable over this time span, while wealth inequality has grown in that same period.

But the Bureau of Economic Analysis does not keep track of capital gains in the U.S. economy, or increases in the value of an asset, such as stocks and property. When an asset is sold, the profits or losses on that asset are called realized capital gains, whereas when an asset increases or decreases in value but is not sold off, it is referred to as unrealized capital gains. Capital gains in the United States are large and are distributed very unequally along the income distribution, with the bulk of them going to the very top.

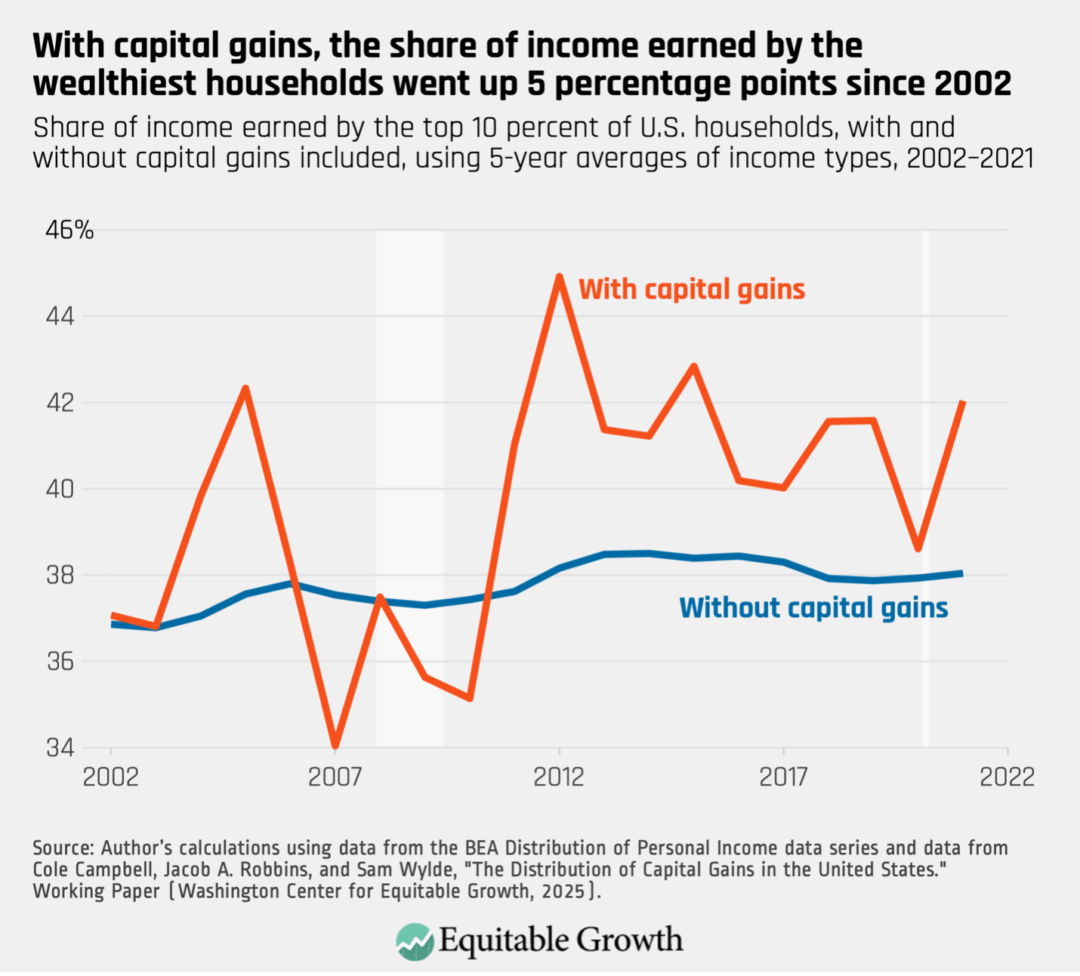

Indeed, we find that adding capital gains to the BEA income series shows that the share of income earned by the top 10 percent of households between 2002 and 2021 actually increased by 5 percentage points, rather than the 1.1 percentage points shown in the BEA data alone.

To reach this finding, we worked with a team of economists—the Federal Communications Commission’s Cole Campbell and the University of Illinois at Chicago’s Jacob Robbins and Sam Wylde—who recently put out a working paper tracking capital gains. Their team shared estimates of U.S. capital gains from 2002 to 2021 for three income groups: the bottom 50 percent of households, the upper 40 percent of households (those in the 50th percentile to 90th percentile), and the top 10 percent of households. Their measure, which they call pure capital gains, includes both realized and unrealized capital gains.

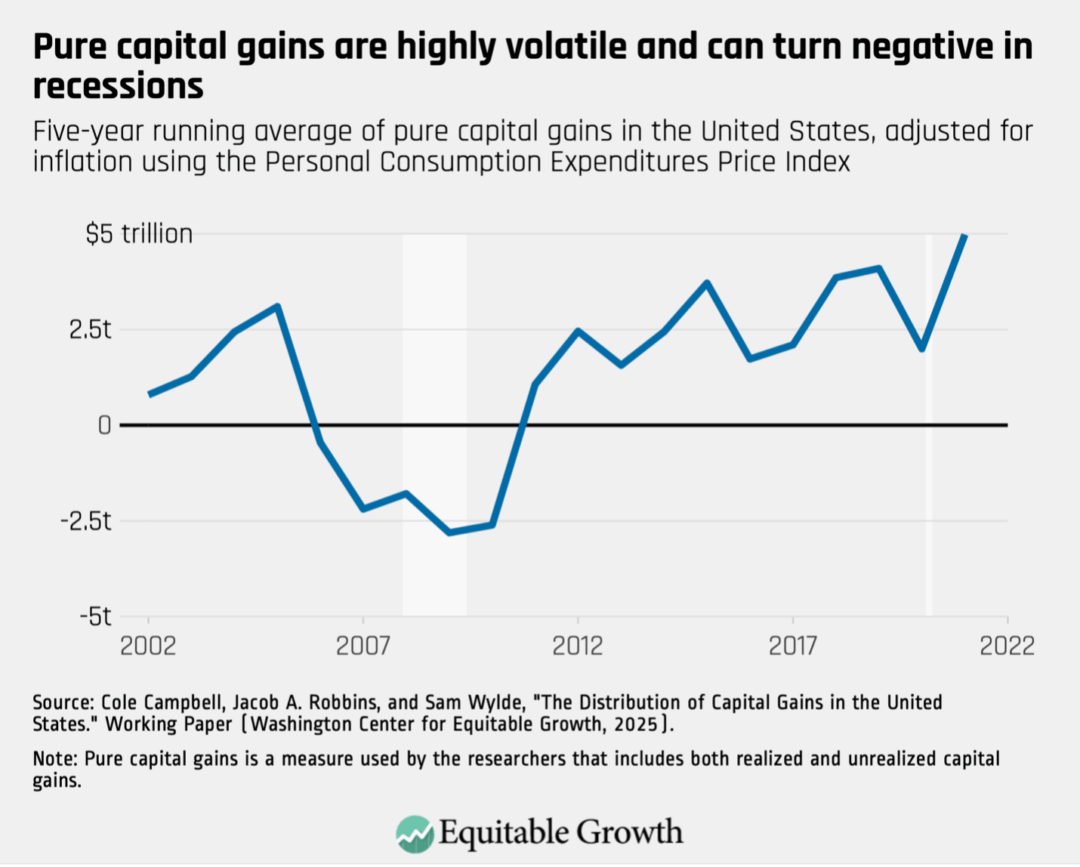

In 2021, pure capital gains on assets held by U.S. households came in at $16.2 trillion, making them the single largest component of income in that year. But capital gains are highly volatile because of conditions in the stock market and can sometimes yield enormous losses, particularly amid economic downturns. Adding capital gains to other forms of income can thus both increase and decrease inequality. During recessions, when asset values plunge, adding capital gains to income measures will tend to decrease income inequality, with the reverse happening during booms.

To create more stable and interpretable income trends, we used the 5-year running average of pure capital gains to make our calculations about their impact on income inequality. Yet even this measure is volatile, as shown in Figure 1. During the Great Recession of 2007–2009, for example, they reached lows exceeding -$2.5 trillion in 2017 dollars, while they reached highs of close to $5 trillion in 2022. (2017 is the index year for the Personal Consumption Expenditures Price Index, which is a key measure of U.S. inflation and the official deflator for BEA’s Personal Income series, which we use here.) (See Figure 1.)

Figure 1

Figure 2 below shows the share of income earned by U.S. households in the top 10 percent over time, both with and without pure capital gains. To make the numbers comparable, we use a 5-year running average of other forms of income as well, which greatly reduces the variation in this series.

When capital gains are not included, the share of income earned by the top 10 percent increased 1.1 percentage points over the two decades studied, from 36.9 percent to 38 percent. With capital gains, the difference is more pronounced, with the share of income earned by the top 10 percent of households increasing from 37.1 percent in 2002 to 42.1 percent in 2021. (See Figure 2.)

Figure 2

As Figure 2 shows, the series with capital gains included was quite volatile over this time, with the top 10 percent’s share dipping as low as 34 percent before bouncing back in the early 2010s. Unsurprisingly, this was a result of asset values crashing during the Great Recession.

These findings echo estimates from the Congressional Budget Office’s distribution of income report. This report, which is currently only updated through 2021, also tracks U.S. income inequality over time but uses a different income concept than the Bureau of Economic Analysis and includes realized capital gains. In the CBO data series on income after taxes and transfers, the top 10 percent’s share of income increased by 5 points between 2002 and 2021.

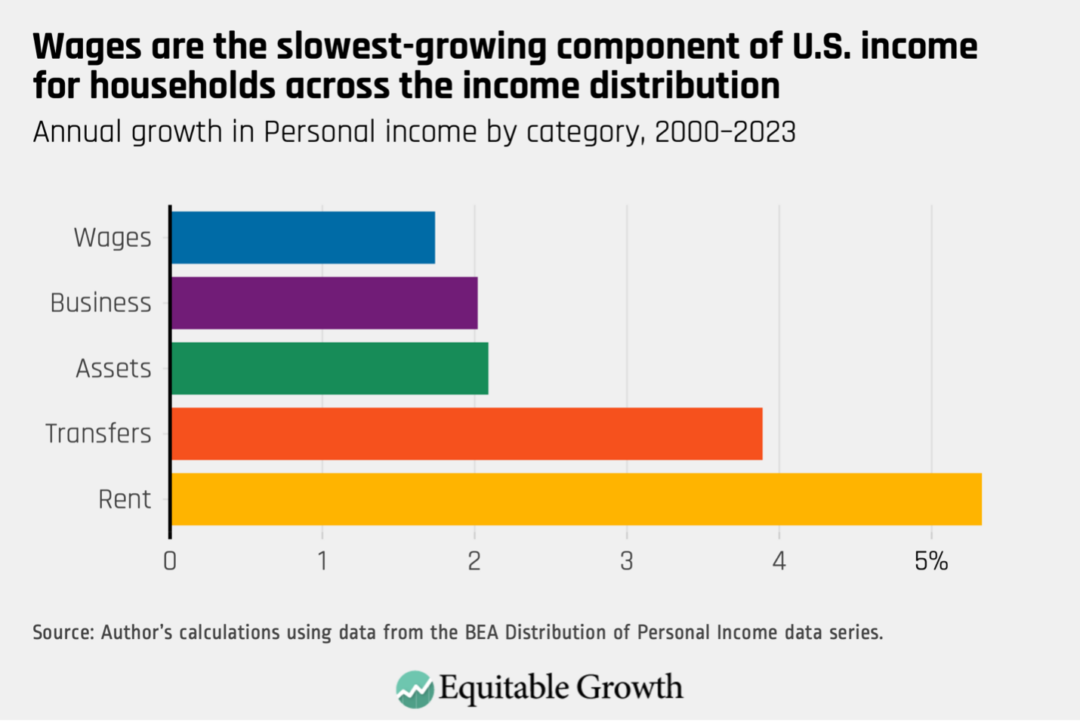

Overall, these findings reinforce that income inequality has been high but stable through the 21st century—but there are serious warning signs just beneath the surface. We pointed to two such warning signs in our initial analysis: First, income support programs have propped up U.S. households in a period of weak wage growth, and second, that these government transfers have been increasing as a share of income, implying that economic welfare has increased much more slowly for the bottom 50 percent than for the top of the distribution.

Rising levels of capital gains wealth is another warning sign. Capital gains significantly increase the wealthiest households’ share of income and are growing over time. All these warning signs suggest U.S. income inequality will rise further in coming years.

Did you find this content informative and engaging? Get updates and stay in tune with U.S. economic inequality and growth!

The 2025 budget reconciliation law that was enacted earlier this month is a sprawling piece of legislation, touching almost every corner of the federal budget and the U.S. economy. It will take years for all the consequences of the law to be fully felt and understood.

A preliminary economic analysis, however, reveals 10 especially harmful policies that were included in the final bill and which run counter to the evidence on what spurs equitable economic growth. Below, we detail each of them and their implications for Americans and economic growth over the next decade and beyond.

Phony populism

Though the so-called populist tax provisions in the new law—partial deductions for tip income, overtime income, auto loan interest payments, and a larger standard deduction for some seniors—got a lot of attention, they are overly complicated, will benefit few U.S. workers, and will expire after 2028. These tax provisions are not pro-growth because very few workers will be able to work more in order to qualify (find a job in the right industry, for instance, or have the right amount of income and tax liabilities, and have control over their hours and pay).

In fact, by making these provisions effective in 2025, the bill’s authors are rewarding economic decisions that have already been made—the definition of a tax windfall—which simply generates a (small) political treat for favored constituencies. That is, of course, assuming an under-resourced IRS can quickly get these policies up and running while protecting against any game-playing, including attempts to recategorize ordinary income as tip income, which will be a challenge.

Slashing the Affordable Care Act

The 2010 Affordable Care Act ushered in a new era for health care in the United States: protection for those with preexisting conditions, state marketplaces with affordable insurance options, and an expansion of Medicaid. The result was near-universal coverage and a bent cost curve, freeing up space in families’ and governments’ budgets for other productive investments.

While the ACA insurance reforms and marketplaces are both still intact, the reconciliation law cut Medicaid by $1.15 trillion, a 15 percent reduction in federal spending on the program. Enhanced premium tax credits for marketplace plans also were allowed to expire, which will lead to a spike in premiums for millions of middle-income families. These provisions will lead to an estimated 16 million Americans losing their health insurance coverage over the next decade—11.8 million from Medicaid cuts and 4.2 million from the failure to extend the premium tax credits.

Increased hunger

Similar to the Medicaid cuts, the reconciliation law severely curtails the federal government’s contribution to the Supplemental Nutrition Assistance Program, which, in 2023, provided food stamps to an average of 42 million Americans per month. It is unlikely that states will be able to make up for the $186 billion reduction in federal aid. The official estimate is that more than 22 million families will lose some or all of their SNAP benefits, effectively raising food costs for many families already struggling under high prices.

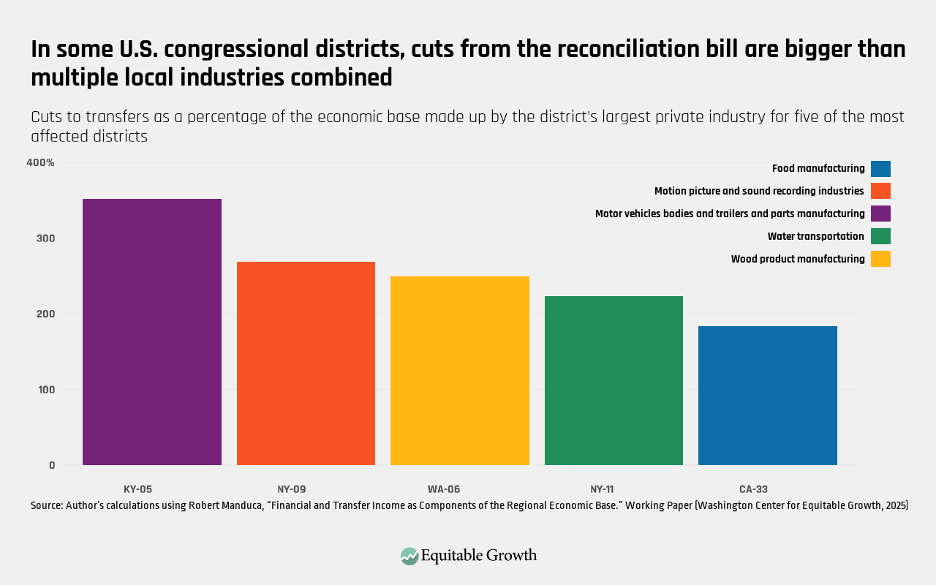

It is not just SNAP beneficiaries who will suffer; their local economies will feel the ramifications as well. Recent research from Equitable Growth grantee Robert Manduca of the University of Michigan finds that nutrition assistance and Medicaid are a major contributor to the economic base of local communities, or the portion of its economy that brings money into a region from the outside world and then circulates locally, creating jobs and additional economic activity.

Indeed, Manduca finds that the cuts in the reconciliation bill are the economic equivalent for many states and congressional districts of losing a big chunk of their largest private industry. (See Figure 1.)

Figure 1

Large tax cuts for the wealthy

Instead of using the savings from cuts to Medicaid and nutrition assistance to, say, pay down the multitrillion dollar federal debt, the law uses the money to partially offset a huge tax cut that disproportionately benefits the rich. The bill’s authors in the Republican-led U.S. Congress didn’t just extend the expiring provisions of the 2017 Tax Cuts and Jobs Act, which was the stated rationale for the reconciliation bill, but instead went on a tax-cutting spree, doling out more than $5 trillion in tax cuts over the next 10 years—not including the added cost of interest payments on the debt or the potential cost of a future Congress extending temporary tax breaks, which often happens.

The signature provision was a $2.2 trillion cut to marginal income tax rates. The top bracket, for example, is now permanently set at 37 percent, rather than the 39.6 percent from the Obama and Clinton eras. Indeed, the richest Americans are some of the law’s biggest winners. The average household in the top 0.1 percent of earners, making more than $2 million annually, will get a $308,763 tax cut in 2027. Millionaires receive 21 percent of the tax benefits that year, which amount to more than $113 billion—roughly equal to the average annual cut to Medicaid.

This combination of tax cuts for the tippy top of income earners and spending reductions for programs that aid low-income Americans makes the new law the largest upward transfer of wealth in a tax and budget bill in at least the past 40 years.

Indefensible tax giveaways

The budget law also gifted the wealthiest Americans additional, completely unjustified hand-outs. Three of the most egregious examples, which Equitable Growth has written about elsewhere, are a permanent extension of the 199A qualified business income deduction, a permanent increase in the estate tax exemption, and an enhanced qualified small business stock exclusion. Almost all of the benefits of these three policies—which have a total combined cost of $966 billion—accrue to those in the top decile of income earners, and a large majority of the benefits go to the top 1 percent.

In particular, pass-through business owners, including venture capital investors, are some of the law’s biggest winners, since they are uniquely positioned to take advantage of these tax breaks. What’s more, the two most concrete proposals from President Trump on raising taxes on the rich—crackdowns on the carried interest loophole and on a tax break used by owners of sports teams—both fell out of the final bill.

Even worse, while the law severely restricts eligibility for many social programs, creating onerous layers of administrative burdens, the legislation’s authors made qualifying for these tax breaks easier for the rich. Their explanation is that these cuts will spur investment and eventually trickle down to workers, but these views fundamentally misunderstand how economic growth works.

Budget gimmicks

While the sausage-making of legislating has always been messy, the Republican-led Congress took an especially untransparent approach to this law that will likely further erode adherence to institutional norms and ultimately reduce trust in Congress. Most notably, the Senate deployed a novel “current policy baseline” to fraudulently conceal $3.8 trillion in tax cut extensions. This unprecedented abuse of the budget reconciliation process—a process originally designed to reduce long-term deficits—paves the way for a permanent deficit-financed tax cut that will heighten the fiscal risk facing the nation for decades to come.

These and other budget gimmicks send an unfortunate signal to investors and consumers here and abroad about the United States’ ability to responsibly manage its fiscal affairs and remain the leader of the global financial system.

Underappreciated macroeconomic consequences

There has been a lot of focus lately on the Federal Reserve keeping interest rates elevated because of inflationary pressure from tariffs. Meanwhile, there has been less attention on how a budget bill that adds $3.4 trillion to the deficit over the next 10 years will also put upward pressure on prices and could cause even higher interest rates. Spending on this scale while the U.S. economy is at near full employment is a recipe for a short-term economic sugar-high but long-term weakness.

This is just one reason why economic modelers don’t expect the tax cuts to be pro-growth—despite their proponents’ arguments—because any increase in economic activity will be counteracted by the risk of inflation and the Fed reacting accordingly by raising its prime rate. As much as President Trump wants Fed Chair Jerome Powell to lower interest rates, in the face of tariffs and a massive tax cut, the Fed’s hands will be tied.

At the same time, the reconciliation law provides roughly $170 billion for the Trump administration’s mass deportation efforts, including an unprecedented budget increase for U.S. Immigration and Customs Enforcement. Economic evidence demonstrates a labor force contraction of the scale currently planned by the Trump administration will have negative effects on native-born workers and the economy as a whole, reducing total employment and economic growth.

Missed opportunity on child care

The Section 45F tax credit for employer-provided child care is a flawed policy that has not effectively expanded access to affordable child care. Fixing the broken child care market in the United States requires more than an employer subsidy or a modest and selective increase in the Child Tax Credit. Rather, a comprehensive approach that includes higher wages for child care workers and more high-quality child care facilities is needed.

Unfortunately, the budget law makes just a few small improvements to the 45F tax credit and to the nonrefundable Child and Dependent Care Tax Credit, as well as expanding a different tax credit for paid family and medical leave—a woefully inadequate effort for addressing the scale of the problem.

One especially clear example of how this works is in the pharmaceutical industry, which took advantage of outsourcing loopholes embedded in the 2017 Tax Cuts and Jobs Act. Loosening taxes on outsourcing is part of this administration’s larger, misguided goal of unwinding the global tax deal negotiated by the Biden administration, which would have created a long-overdue global minimum tax on multinational corporations.

Politically targeted ‘pay-fors’

Despite the reconciliation law being an overall tax cut,some unlucky constituencies will see their taxes raised by the legislation. These politically targeted “pay-fors” include research universities, legal immigrants, blue-state homeowners, and clean energy producers, investors, and consumers.