Must-Read: Thomas Piketty on After Pikettyhttp://amzn.to/2qgPIRE. If I were running the publicity campaign for this book of ours, I would—today—broadcast two (or three) of the chapters for free in an attempt to excite interest while at the same time demonstrating that we are not simply broadcasting exciting teaser trailers from a boring movie—because each full chapter does have its own, complete, payoff. If it were up to me, I would probably grab our introduction and then either Goldhammer or Naidu, but that reflects my concerns right now rather than any objective government…

Since we are not doing that, let me broadcast an exciting teaser trailer from the last chapter of the book:

Thomas Piketty*: Lessons from “Capital in the Twenty-First Century”http://amzn.to/2qgPIRE: “I would like to see Capital in the Twenty-First Century as a work-in-progress of social science…

…Too much time is lost… on petty quarrels about boundaries and… sterile methodological positions…. The best way… is to address big issues and see how far we can take them, using whatever combination of methods and disciplinary traditions seems appropriate…. [Here] I would simply like to attempt to clarify a small number of issues… from the perspective of the multidimensional history of capital and power relations, and regarding the role played by belief systems and economic models in my analysis….

The primary ambition… was to present… historical material coherently… and [to] propose… an analysis of the economic, social, political, and cultural processes… to return the issues of distribution and the inequalities between social classes to the center of economic, social, and political thought… [as in] the works of Thomas Malthus, David Ricardo, and Karl Marx… motivated by the profound social changes they perceived around them…. Even though they did not have at their disposal systematic historical sources for studying such evolutions, these authors at least had the merit of asking the right questions.

Throughout the twentieth century, economists all too often sought to remove themselves from the social sciences (an illusory temptation, if ever there was one) and to pass over the social and political foundations of economics. Some authors—particularly Simon Kuznets and Anthony Atkinson—nonetheless patiently embarked on the meticulous task of collecting historical data on the distribution of income and wealth. My research directly stems from these studies and has largely consisted of extending the collection of historical data….

Furthermore, in Capital I tried to… simultaneously study the evolution of collective representations of social inequality and money in both public debates and political conflicts as well as in literature and cinema. I am convinced that such an analysis of the systems of representations and beliefs about the distribution of income and wealth… is essential…. This… central interaction between belief systems and inequality regimes… should be studied more extensively…. I plan to further study [it] in the years to come….

I tried, for example, to show that national identities and the representations each country has of its own economic and historical trajectory play an important role…. In particular, the “Social Democratic Age in the Global North (1945–1980)” (as it is aptly labeled by Brad DeLong, Heather Boushey and Marshall Steinbaum in their introductory essay) can certainly be viewed as an unstable historical episode, but it is also a product of deep transformations in belief systems about capitalism and markets.

I fully agree with Marshall Steinbaum (Chapter 18) when he stresses that the World Wars and the Great Depression were decisive, not so much in themselves, but because they “discredited the ideology of capitalism in a way mere mass enfranchisement had been unable to do so [in the decades preceding World War I].” The crisis of the 1930s and the complete collapse of the European inter-state competition system during the two World Wars led to the end of the nineteenth-century political regime, which was based upon the laissez-faire ideology and the quasi-sacralization of private property. This radical change in dominant belief systems is of course nothing else than the “Great Transformation” http://amzn.to/2pW8exV famously analyzed by Karl Polanyi in… 1944…

Heather Boushey, J. Bradford DeLong, and Marshall Steinbaum, eds.: After Piketty: The Agenda for Economics and Inequalityhttp://amzn.to/2qgPIRE (Cambridge: Harvard University Press: 0674504771).

Let’s see if I can maintain a post an hour today on this, shall we?

Here is my amazon review:

As one of the co-editors of this book, I know it very well. I am greatly pleased with how this project came out—we have very serious people, as Bob Solow would put it, writing very serious takes on what Thomas Piketty has accomplished, where he has gone wrong, and what gaps remain to be investigated by others. Social scientists thinking of citing on, working along lines related to, or drawing on Piketty should certainly read this book. People who have read Capital in the Twenty-First Century who are curious about how serious people are reacting to and assessing the book should read it as well.

New research shows the significant decline in lifetime income growth for most men in the United States over the past six decades and provides some evidence that the gains for women in the second half of the past century may soon be giving way to declining lifetime income growth, too. This is the main thrust of the paper by economists Fatih Guvenen of the University of Minnesota, Greg Kaplan of the University of Chicago, Jae Song of the Social Security Administration, and Justin Weidner of Princeton University, but they also present data on inequality of lifetime income in the United States.

The results of their research are surprising, given the trend in traditional snapshot figures such as the famous data on inequality compiled from data analyzed by economists Thomas Piketty at the Paris School of Economics and Emmanuel Saez at the University of California, Berkeley. Piketty and Saez show large increases in income inequality since the late 1970s, but this new research demonstrates that lifetime income inequality didn’t change that much, despite the significant increases in one-year income inequality. What could explain the difference between the two measures of income?

Digging into the data a bit more reveals that differences in gender make a bigger difference for lifetime income trends. The overall level of inequality didn’t rise much year on year, but inequality of lifetime income for each gender did. Remember that women across the income distribution saw increases in lifetime income while most men saw declines, which means there was a decrease in the inequality of lifetime income between the genders. This decrease was particularly pronounced for the bottom half of income distribution, as the convergence for men and women’s income was strongest there.

This decline in gender inequality counteracted the increase in inequality within each gender, leading to no increase in overall lifetime income inequality. So, even though the lifetime income of, say, a woman in the top 10 percent of income earners has increased much more than a woman with lifetime earnings at the median (the 50th percentile), and even though the lifetime income of a man among the top 10 percent also outpaced a man at the median, the overall distribution of lifetime income didn’t change much when we look at men and women together.

The income gains for women over the past several decades seem unlikely to be replicated in the future, so looking at the trends within genders may be useful for thinking about the future. The reasons for rising lifetime income inequality differ for men and women. Higher inequality of lifetime income could happen because the inequality of initial incomes has increased (more inequality when a person turns 25), or because there’s inequality in life trajectories (differences in earnings gains over the course of a working life), or some combination of the two.

For men, the rising inequality of lifetime income appears to be due to higher levels of initial inequality. Inequality for men is seemingly locked in for men around the time they turn 25. And that level of initial inequality has increased over the years. Understanding what’s driving the decline in lifetime inequality for men requires understanding why inequality at age 25 has been increasing.

For women, the story is a bit more complicated. Inequality at age 25 hasn’t changed that much, but trends in inequality over a work career have changed. But these trends haven’t been consistent over the several generations examined by Guvenen, Kaplan, Song, and Weidner. For earlier groups, the researchers find that inequality dropped over time, and for later groups inequality fell for a bit and then rose later in life.

The four co-authors admit they don’t have explanations for these trends and the forces behind them. The changing life-cycle trends for women will be particularly interesting and important to understand, as well as the force increasing inequality early in men’s careers. Hopefully some more fruitful research will come these findings.

Moderator: Gillian Tett, U.S. Managing Editor, Financial Times

Steven Ciobo, Minister for Trade, Tourism, and Investment, Australia

J. Bradford DeLong, Professor of Economics, UC Berkeley; Weblogger, Washington Center for Equitable Growth

John Hagel, Managing Director, Deloitte Consulting LLP; Co-Chairman, Center for the Edge

Alejandro Ramirez Magaña, CEO, Cinépolis

Stephen Schwarzman, Chairman, CEO and Co-Founder, Blackstone

In the 20 years leading up to the financial crisis, international trade grew at twice the rate of global output. Since then, trade has struggled to recover. Recent data is more worrying still, suggesting that trade’s share of global GDP is falling. With mainstream political support for multilateral trade deals diminishing and populist movements on the rise in the U.S. and Europe, it is time to examine the future of globalization. Panelists will consider the following questions:

Has international trade—and globalization more broadly—entered a period of stagnation or even reversal?

Once unleashed, can globalization ever reverse or are we just seeing a slowdown in a normal cycle?

What are the implications for the global economy and the international economic order?

Gillian Tett: Good afternoon, everybody, and welcome to this panel session entitled “Globalization in the Crosshairs”. That is the politically correct, slightly optimistic title. I would probably call it: “Are We Sliding Back to Protectionism and Nationalism? Is It ‘Back to the Future’—Like the 1930s?”

Joining me today is a terrific broup of people to talk about these issues. On my far right, to your left, is Steven Ciobo, Minister for Trade, Tourism, and Investment for Australia. Next to him is Brad DeLong, Professor of Economics at Berkeley, one of my favorite economic bloggers. On my immediate left, your right, is John Hagel, Managing Director at Deloitte. Next to him is Alejandro Ramirez, CEO of Cinépolis, a large Mexican media group, and who is also Chairman of the Mexican Business Council. And at the very end is Steve Schwartzman, a man known well to most of you, CEO of Blackstone, and Chairman of the Strategy and Policy Forum at the White House. A great combination of people to talk about globalization, nationalism, protectionism, and the impact on business and the economy.

I would like to start with you, Steve, since you are now in this elevated role, speaking for business across America at the White House. You have built your career very much on the wave of globalization. Globalization has been good for you. Do you regard the president as a protectionist?

Steve Schwartzman: The way the president looks at himself is as someone who sets the table with equivalent tariff and other duties so that globalization goes ahead, but from the perspective of a certain type of equality. When you have the United States charging 1/3 duties and tariffs compared to three times that for the other country, the administration is saying: either you come down, or we will go up, and then let us let trade expand. It is really these in some cases enormous differences, as well as in some cases non-tariff barriers that make it very difficult for us to export our products. We look at it from the perspective of: How did we get into this situation? Why aren’t people letting there be equivalence, so the best products win, or the best services win? What you are seeing is an attempt at reciprocity, or equality, and then continue with globalization.

Right now the U.S. has the lowest fully-landed tariff borders, tariff plus VAT, in much of the world. It happened because of the U.S. dominance after World War II, when we had 70% of global GDP. And it has been allowed to continue. It’s not that the intent is to void or dampen globalization and the things we are all familiar with.

Gillian Tett: But do you around that table, the Strategy and Policy Council, strongly support these calls to renegotiate NAFTA. Are you concerned that this is part of an anti-globalization backlash that could end up damaging you?

Steve Schwartzman: I was at the G-20 in Hangzhou, and President Xi gave a big speech about the general anti-trade pattern. And everybody who measures these things has seen trade constricting around the world. You could look at, Gillian, in a few different ways:

As a simple correction, for equivalence.

Why is it coming up now? The theory is that these issues are being raised around the world.

But, really, this is an equivalence issue. These issues would all go away if barriers were more or less the same everywhere. We would not be having this panel.

Gillian Tett: OK. So it is not protectionism. It is “equivalence”. That is clearly going to be the new buzzword in Washington: “equivalence”. Alejandro, from where you are sitting…

Steve Schwartzman: Let me put it this way. If it were the reverse—if all these tariffs were upside down—what would other people think?

Gillian Tett: Well, let’s ask them. Alejandro, you come from Mexico…

Steve Schwartzman: As a curious item…

Gillian Tett: Well, that’s a great question to ask everyone on the panel. But, Alejandro, sitting in Mexico does what is happening in Washington look to you like an enlightened policy of “equivalence”, or does it look a bit more ominous? How do you read the current mood in Washington?

Alejandro Ramirez: We are very concerned in the Mexican private sector with what we do perceive as protectionist rhetoric in Washington. The fact that on Day 1 the U.S. withdrew from TPP. Last week there was, as you know, a leak saying that the White House was preparing to withdraw from NAFTA. That we are continuing on the path of renegotiating the trade deal. We are concerned because we think that NAFTA has been unduly vilified. We believe that NAFTA has brought many more benefits to all three countries than the trade deal has cost. Trade has more than tripled between the three countries. Bilaterally, between the U.S. and Mexico, trade has grown by more than sixfold since 1994.

Mexico has become the number two destination for U.S. exports. We trade over $500 billion every year. Around 6 million U.S. jobs depend on trade with Mexico. Of course, Mexico has also enormously benefited from trade with the U.S. In specific sectors, for example, more than 20 years ago when the trade deal was going to come into effect one of the most sensitive areas was agricultural markets on both sides. Today some of the biggest beneficiaries from NAFTA are the U.S. corn growers of the midwest and the Mexican growers of fruits and vegetables.

We are actually exporting very intelligently according to the relative comparative advantage of each country.

NAFTA has allowed us to strengthen the supply chains of North America, and strengthened the competitiveness of the region, so that we can produce more competitively in the world.

Gillian Tett: So when you hear someone like Steve Schwartzman saying, along with the White House, that what is needed is “equivalence”—we need a level playing field—do you think that is fair, or do you think that is protectionism under a new guise?

Alejandro Ramirez: I think part of what Steve was referring to was the policy of other countries that do not have a free-trade deal with the U.S. They may have disparate tariff rates. But Mexico—our average tariff was much higher than the U.S. back in 1994. We brought it down basically to zero. Both countries. The U.S. average tariff was below 5%. The Mexican average tariff was above 20%. I do not know about other countries, but I do know that with Mexico we are dealing with a level playing field. And yet the U.S. government has threatened repeatedly to withdraw from the deal.

I do, however, think that there is room for improvement. It is a 22-year old deal. Parts of the economy that did not exist back then—e-commerce. I think there is room for strengthening intellectual property rights. I think there is room for strengthening biotech. Other things we can add—labor, environment, anti-corruption.

There is room for modernizing it. But to call it the worst deal ever for the U.S. I do not think that is an accurate description of NAFTA.

Gillian Tett: Right, right. Just now that we are on NAFTA—we’ll get on the TPP in a minute—John: You have talked to a lot of CEOs. How concerned are they with rising protectionism—”equalization”, “trade modernization”, whatever you want to call it. Do you think we are in the middle of a protectionist backlash? Is that going to hurt companies that you talk to?

John Hagel: My sense is that there is increasing anxiety about the fact that we are at a pivot point, and about which way the world is going to fall. I think it reflects the paradox about globalization. At one level, globalization is creating expanding economic opportunity around the world. At another level, it is creating mounting performance pressure on all of us. It is intensifying competition on the individual level. We all face the possibility of loss of jobs. Wages are coming down because of international competition. At the corporate level, we are facing increasing competition, globally.

We have spent time—I run a research center called The Center for the Edge. We have looked at the long term forces making the global economy. The one metric that we think illustrates this mounting performance pressure—if I can show slide 1—the return on assets for all public companies in the United States:

From 1965 until today, if you look at return on assets for all public companies in the United States, it has basically collapsed, over a period of decades. There are short term cycles that correspond to the economic cycles. But the long term trend is very clear. And there is no sign of it leveling off. There is certainly no sign of it turning around.

Our belief is that that is an indicator not only of mounting performance pressure, but of the increasing inability of our institutions to respond to this pressure. This is public companies. But, based on the research we have done, we believe all institutions—educational institutions, government institutions, NGOs—are facing a similar kind of challenge.

Gillian Tett: That trend is going to hit zero around 2030, isn’t it?

John Hagel: This is not a sustainable trend. Clearly, something is going to have to change. Our belief, and this is being an optimist from Silicon Valley, is that this is going to be a catalyst to force us to reassess all of our institutions.

By the way, one of the key indicators of the failure of our institutions is “trust” metrics. We have study after study showing declining trust in every institution—not just companies, not just banks, not just government. Every institution around the world is collapsing! If that is not an indicator of a problem, what is? And our belief is that the problem is that we are unable to respond to mounting performance pressure, and unable to take advantage of the opportunity that is actually created by globalization.

Gillian Tett: Right. I am going to come back later and ask you what can be done. That is obviously a big question. And that is the point of these conferences: to assess what can actually be done. But before I do, I would like to turn to Brad, who has also come armed with a nice snappy chart. Brad, do you want to put this in a longer term historical term historical context.

Brad DeLong: OK. Let’s go!

Since 1800:

First Globalization—Trade between capital and resource rich regions, and huge amounts of migration of finance and labor to the resource rich regions.

Globalization Retreat—Faster progress in mass production than in transport makes it efficient to bring production back home; combined with the depressions on the interwar period encouraged governments to take steps to keep jobs at home and engage in beggar-thy-neighbor policies.

After World War II, Second Globalization—the enormous expansion of north-north intraindustry trade, as developed countries trade narrow slices of their industrial output with each other. This was the thing that explaining it won Paul Krugman his Nobel Prize.

Followed by the green line: Hyperglobalizion—in which the global south’s low wages give it a comparative advantage which can now be harvested for industrial-scale production because of the success in constructing internet and other communications-mediated intercontinental value chains.

Of these, perhaps the first example was the U.S.-Mexico division of labor in the automobile industry. My friends on the right and my friends on the left feared NAFTA back in 1992. They said NAFTA was going to kill the U.S. auto industry. The whole thing would move to Hermosillo. It did not. By outsourcing the most labor intensive parts of their production processes to Mexico, GM and Ford now find themselves in much more competitive positions vis-a-vis Toyota, BMW, and company than they would have found themselves had we not done NAFTA.

Gillian Tett: If you look at that chart, you have that lovely green arrow heading up towards the heavens, looking like it is going to go up forever. The last time I saw charts like that was in 2007 on the eve of the credit crisis. I have seen other charts like that showing what has happened over the past hundred years—to the credit cycle, to banking pay—that go up and down. The question I have is: I look at that, and I look at what we have just seen from John on returns from assets collapsing, and what makes you think that green arrow is going to continue to do up and not suddenly go down again?

Brad DeLong: It is always dangerous to make predictions, especially about the future. Yes, in an era of secular stagnation, with central bank-controlled interest rates kissing zero for large periods of time and governments loath to expand their purchases, one of the few tools left is to try to redirect its country’s spending to its own goods whenever it finds itself short of jobs. Yes, low wages are going to be a much less important player in the global division of labor as robots come and as labor productivity in manufacturing soars upward.

China is almost sure to be the last country that follows the successful industrialization recipe of becoming a lot richer by exporting low wage manufactures to the industrial core and so building up its communities of engineering practice. After China, low wage simple first line manufactures simply are not going to need enough workers to produce them for it to be worth much of anyone’s while.

Gillian Tett: Right. That is not entirely encouraging. On that note, it seems like a good moment to turn to Australia. You are in the position of being the only elected official, the only government official on the panel. You represent governments throughout the world, while Steve is singlehandedly representing American business. How do you read it? Do you think we are on the brink of an inexorable slide into protectionism? Do you see things like TPP unraveling as signposts of that trend? Or are you more optimistic?

Steven Ciobo: I am more optimistic. I was listening to the remarks that Steve made earlier. I will contrast them with our experience. In the 1980s, Australia unilaterally reduced its tariff barriers. most goods coming into Australia come in with zero tariffs. The maximum is 5%. We have free trade agreements with many countries which means, of course, that there are no tariff barriers at all. We are focused on non-tariff barriers so that they too are reduced over time.

We are now in our twenty-sixth year of consecutive positive economic growth, which is very good for a developed economy. In fact, we have the longest consecutive growth period that any developed economy has ever experienced.

Now I am not saying that that is all the consequence of our unilaterally reducing our tariff barriers. But we do know that they distort. They distort not only trade but the efficient allocation of capital.

Our experience as a country is that trade is driving, in many respects, we’ve seen it in the past twelve or twenty-four months, that trade is driving our economy and driving our employment. One of the points that people remark to me is that Australia has a different view and pattern of trade than other countries. In particular, they will focus on European countries. My observation is to say that may be the case, but if you look at Australia those industries that are particularly protected or subsidized tend to be in the agricultural sector. You see that in Europe. You see that in the United States. In Australia, in fact, it is our ag sector that has benefited from the fact that we have preferential market access to the fast growing Asian powerhouse economies of Japan, China, and Korea. This has really underscored the big price increases for ag products for Australia. There is quite a different view there. We had a lot of these battles thirty years ago. It caused pain. It caused disruption. But we have seen at the end of twenty-six years the benefits of having taken those decisions.

Gillian Tett: So if the White House is essentially saying that is not going to engage in multilateral deals, if TPP has essentially been torpedoed by the White House. Are you willing to say: the Americans are being protectionist; let them get on with it; we are going to go forward with, say, China, and do TPP by ourselves?

Steven Ciobo: I certainly believe that there is tremendous benefit from the TPP. Australia’s position is to continue to pursue all options that we can to bring the TPP into effect. As it is currently constructed, by definition the TPP cannot come into force without the USA. But there is an opportunity for the other eleven countries—we did this recently in Chile—to come together to have a conversation about the future of the TPP. Make a minor tweak so it can still come into force without the USA. That is what we are pursuing. I do not want to speak on their behalf, but I know a similar view is held by New Zealand, by Canada. Ultimately, the big player in this will be Japan. I was in Japan two weeks ago. I was particularly pleased that the Japanese government has given some indication that it is considering a TPP 11.

Now in time, whether China, the U.K., or some other country wants to join—that would be there decision. But meanwhile I think it would be an enormous missed opportunity for us not to do everything we can to bring the TPP into effect.

Gillian Tett: And are you willing to take the leadership in that role?

Steven Ciobo: Absolutely. Australia and Canada have been at the forefront of that discussion.

Gillian Tett: Right. Before I turn back to Steve, I would like to ask your reaction. Do you regard it now as wiser to spend more time building links with, say, China, than America given the way that politics is developing in America?

Steven Ciobo: For a long time, Australia’s view was that we considered ourselves a European country stuck in the wrong part of the world. The amazing thing is that good fortune has smiled on us. We live in the fastest growing region in the planet. So Australia has done a number of things. We have done a number of things. We have been pragmatic. We are very goods friends with the United States, with Japan, with Korea, with China. Now they haven’t all gotten along. But we have managed that process pretty effectively. We are not putting all of our eggs into one basket. We will continue to have a diversified approach. We know who are friends are in the United States. But we are focused on doing deals that are good for our country.

Gillian Tett: Spoken like a diplomat—a politician. Steve, I am curious: did you support TPP last year?

Steve Schwartzman: I thought it was a good thing. I believe it was a good thing. It was a shame that Democrats did not want to do it…

[General laughter from the panel and the audience]

Gillian Tett: I am not sure that is quite how history will write it. But go on:

[Continued laughter from Gillian Tett]

Steve Schwartzman: That is what happened.

Gillian Tett: Do you think it is a shame that the current administration does not want to do it?

Steve Schwartzman: I think it was DOA. The philosophy that the current group has. I’m in the private world. I’m not a government official.

Gillian Tett: That means you can speak freely.

Steve Schwartzman: The theory that the current administration has is that bilateral deals are better than multilateral deals. The way they come about that is—say, pretend you have a group of fifteen countries. You cut a deal with country number 1. They want certain things from you and you want certain things from them. You always hate giving up what you give up. But you give it up because the balance makes sense. And then you go to country number two which wants different things. And you cut a deal with them by giving up things. And you don’t want that. And let’s go to country number three and pretend they don’t want any of the things that countries one and two wanted. So now you have to give up more—different things to each one. But in a multilateral deal you give the same deal you didn’t want to give to country one, you give it to fifteen people…

Brad DeLong: But NAFTA is the ultimate bilateral—or, rather, trilateral—deal!…

Steve Schwartzman: Now, their view is: why would I give something away—why do I give the worst deal I could make with everyone? Why don’t I just give the deal I made with country one to country one. And then I do another deal with country two. It has been explained to me that when you do do that, you can get other benefits from the whole group on softer issues, labor issues. But the current group says: I just want to trade with each one, do the best deal I can, and do deals with each one of these countries.

Gillian Tett: Doesn’t it worry you that if Australia, Japan, China, the TPP will have something prepackaged, ready to go, ready to rock-and-roll very fast? The administration then trying to do negotiations with each of those eleven countries—wouldn’t that be time consuming, and perhaps leave American companies at a disadvantage?

[pause]

I can see Brad’s like…

Steve Schwartzman: I am not trade representative…

Gillian Tett: OK! The professor:

Brad DeLong: I…

Steve Schwartzman: However, I have not found anybody yet who takes the explanation that I have given—and I have checked with the heads of multilateral organizations—that is how it works. The administration doesn’t want to take the first bad deal and give it to all fifteen in a group, and then take the second bad deal and give it to all fifteen in a group. You could make the case, logically, that that makes some sense. You could make that case. And that is what they are pursuing.

Gillian Tett: The professor is dying to come in…

Brad DeLong: Steve Schwartzman is a brilliant genius. The organization he has played a principal role in constructing—Blackstone—is, we all know, outstripping even Warren Buffett’s vehicles in its α-generation for investors over the long run. It is an extraordinary capitalist accomplishment in finance of a truly astonishing magnitude.

Yet the argument Steve is making here this afternoon now against TPP is the ultimate argument for NAFTA—for a focused bilateral or rather trilateral agreement. And yet it was NAFTA that, according to First Son-in-Law Jared Kushner, President Trump was on the brink of abrogating six days ago. According to Kushner, if the President had abrogated NAFTA we would “have wound up in a pretty good place”.

The principal reason Steve gave for why it might be desirable to “get tougher” on trade was that we face asymmetric non-tariff barriers. But I am not aware of any significant non-tariff barriers between the United States, Mexico, and Canada. Indeed, the only one I remember coming up when NAFT was being negotiated was Canada’s request for a cultural carve-out, so that its radio stations and other media could continue to give priority to Canada-themed entertainment—Celine Dion, and for some reason I do not understand, Lenny Kravitz’s “American Woman, Stay Away From Me!”

Gillian Tett: I am presuming a lot of French language Canadian entertainment as well.

You are essentially arguing that if we are moving toward a world with more bilateral than multilateral deals, that that is more dangerous?

Brad DeLong: It is certainly more complicated.

You either have one deal or you have N(N-1)/2 deals. You then have to be very very careful to keep track of what goods go where when with what components of value added covered by what rules of origin. What fraction of stuff coming in to the U.S. from Mexico under the terms of the Mexican-U.S. bilateral is transshipped from Australia where the Australia-Mexico leg is covered by the Mexico-Australia TPP deal. That would negate the idea that there is a bilateral deal between the U.S. and Australia that means anything.

Keeping track of that is an almost insuperable administrative task. It is an example of the reasons that Friedrich von Hayek concluded that central-planning micromanagement could not work. Micromanaging things at any detailed level, very soon—with the G-20, you would have 195 different bilateral trade agreements. It would be a wonderful full-employment thing for trade lawyers, and for those who could deploy the vast numbers of analysts to determine where the loopholes were. You could make serious money in that business. But I don’t think it would be good for the world economy.

Gillian Tett: Steve, how do you feel about moving toward more bilateral arrangements?

* Steven Ciobo*: We keep the full sweep. We are prepared to do a multilateral deal. We are prepared to do a sequence of bilateral deals. We do not believe in one size fits all. You have to cut the cloth to suit. The Holy Grail, as far as I am concerned, is multilateral. multilateral apply one set of rules across all countries. The biggest beneficiaries from a multilateral deal—for example the TPP—are the small-to-medium sized guys.

The big guys can always compete. They can hire the bevies of consultants and lawyers to make sure that the rules-of-origin and so forth are complied with. The little guy cannot. If you have ten different deals with ten different types of rules, the small exporter who is trying to navigate that noodle-bowl of rules really struggles. That is one of the major benefits of multilateral: you have that one set of rules that applies across all eleven countries in the case of a TPP-11 that you can comply with.

The other point I want to make. We get into the politics of this. I need to get votes. I need to get reelected to keep my job.

We took a decision as a government about three years ago to stop all subsidies to our automobile industry. Our automobile industry—tens of thousands of workers—but we could not justify a decision to continue to subsidize it to the tune of $5 billion every four years to maintain a small sector. Your frame of reference matters. I know that by doing that the car fleet in Australia is going to become younger—better for road safety, public health, and all of those things. We do not need a car industry. We were not competitive in it. Now we can focus on other industries where we do have competitive advantage.

The benefits, like always, are diverse, are spread, are small amounts over a large population. Versus a lot of noise that comes from the relatively small population employed in the industry that complains the loudest. That is the politics.

Gillian Tett: Right. Alejandro, you do not need to be reelected, but you are running a company that straddles borders. How would a renegotiation of NAFTA affect you? Do you see problems with trade access between the U.S. and Mexico in fields that you are operating in?

Alejandro Ramirez: Our company, Cinépolis, operates multiplexes in thirteen countries with just over five thousand screens. We are the second largest film exhibitor in the world in terms of admissions. 90% of the films that we show are American films, Hollywood films. Mexico is the fourth largest market in terms of movie admissions in the world, just after India, the U.S., and China. If we started a trade war between the U.S. and Mexico, the Mexican government could retaliate by raising tariffs on American cultural goods like films, including corn—we import all the corn for popcorn from Kansas and Iowa. We import all the amplifiers, servers, screens, popcorn warmers, the cheese—Mexico is the largest consumer of nachos in the world…

Gillian Tett: You are giving your Mexican consumers nachos made from American cheese…

Alejandro Ramirez: The cheese—we bring it from Wisconsin.

Gillian Tett: A fact that you did not know: you go to the cinema in Mexico and you are eating Wisconsin nachos…

Alejandro Ramirez: And popcorn! Mexico does not produce corn with the right expansion properties for popcorn. If there was a cancellation of NAFTA, it would become much cheaper for me to import the corn from Brazil or Argentina. They do have equivalent corn…

Gillian Tett: You can’t import Brad Pitt moves from Brazil, can you?

Alejandro Ramirez: You cannot. Our company is a good example of a NAFTA company. We have cinemas in the U.S. and Mexico, but also throughout Latin America, India. One of the main American exports is cultural goods. If NAFTA were repealed, where would both countries put new tariffs? How would it affect us?

One final point about your previous question: bilateral vs. multilateral. The main economic argument for multilateral is that the deal would include the most efficient producer if it were a multilateral producer. But with a bilateral deal you may well be excluding the most efficient producer. It would be trade diversion rather than trade creation. That is why it would be better to have a global multilateral deal under the WTO. But since Doha nothing has happened. Therefore since then we have had regional pushes. The Asia-Pacific region has pushed for TPP. We have the Pacific Alliance between Mexico, Chile, Columbia, and Peru. That is going very well, further integrating our economies and lowering tariff barriers.

Gillian Tett: Right. I am curious. I would like to ask each of you. If you were suddenly given a magic wand—were to become either the President of the United States, Steve, or the President of Mexico or the President of the WTO—what would you like to see happen over the next year? For you, Steve, would it be rapid “equalization”?

Steve Schwartzman: In the next year? That would be terrific! To resolve most of the major issues… I think NAFTA will be resolved in that time frame. I think you will have general agreement with China. It takes a long time to do trade agreements—working them all out. But the basic outlines of things—it would be great to get all that behind us in life, and have things be normalized.

Gillian Tett: That’s very encouraging! You think NAFTA will be broadly resolved in a year, and a new trade deal with China in the next year?

Steve Schwartzman: We all have our own opinions. I would be quite surprised if NAFTA is not successfully renegotiated. I think with China there is a desire for both countries to normalize trade relations and do it reasonably quickly, if it is possible. I am optimistic on that in spite of the rhetoric and other things of that type. It is in the interest of all of those countries.

Gillian Tett: Alejandro, what would you like to see? Would you like to see a renegotiation of NAFTA?

Alejandro Ramirez: Yes, I would like to see it speedily renegotiated. Hopefully we will have something done by the end of the year. Mexico has presidential elections next year. If this gets into that, it could be messy. So I want it done as soon as possible.

Steve Schwartzman: The biggest service that could be done for NAFTA is to have congress just release this document to authorize renegotiations. Elections are coming up. We could create our own problems as a group of three countries simply by having a document held up, which I think the administration wants to get going. This document is being held up by… I won’t say who… by a part of congress… It is not serving the purposes of the country or of Mexico.

Gillian Tett: John and Brad, what would you hope to see happening over the course of the next year to fell more encouraged?

John Hagel: Without diminishing the importance of these policy debates, I view policy debates as a second-order effect of much more fundamental forces. Unless we address those, the public policy will go beyond our control. The key thing to me is: what is our response to increasing performance pressure? I have spent considerable time studying the psychology of this. Very human things we do when we respond to mounting pressure:

We tend to maximize our perception of risk.

We discount our perception of reward.

We tend to shrink our time horizon: under pressure, we need to just think about today.

When we just think about today, we fall into what economists call a zero-sum view of the world: the resources are given, and the only choice is who is going to get them—you, or me?

The consequence of that is erosion of trust. You may seem like a real nice person, but I know that at the end of the day only one of us is going to get these resources, and it is going to be me. In that kind of environment, we are headed toward a very dysfunctional society. My belief is that at least in the U.S. both sides of the political system have fallen under a threat-based narrative: we are under attack. The enemy is coming at us. We all are going to die. We need to come together and fight, now. These narratives reinforce all those dysfunctional psychological reactions to increased pressure. Until and unless we can frame an opportunity-base narrative that gives a credible view of an opportunity that we can all come together to take advantage of that opportunity, our public policy will go in a dysfunctional direction.

Gillian Terr: And do you see any countries framing things this way at the moment?

John Hagel No.

Gillian Tett: Brad, what would you like to do if you were made president tomorrow. What would you like to do? What would you like to see happen?

Brad DeLong: Since I will not be president, what I hope for is that as little as possible gets broken, and as much knowledge as possible is acquired.

Already we have had President Trump say that he did not know what he was talking about last year on the campaign trail when he said that NATO was “obsolete”. He now agrees that NATO is indeed not obsolete—but the pillar of security for the western alliance.

I would like Donald Trump to say that he did not know what he was talking about when he claimed that the TPP was a job-destroying trade deal that would rob Americans of good manufacturing jobs.

I would like him to say that the TPP would further strengthen market integration across the Pacific to the benefit of the U.S. economy, and that the United States had struck a very good deal with respect to intellectual property in the TPP. Very much so. When I was tending toward “no” on the TPP, it was largely because I did not think that it was fair that the Vietnamese be charged through the nose for pharmaceuticals. They are poor. We bombed them for ten years. We could at least let them buy pharmaceuticals cheaply.

In the best of all possible worlds is one in which people realize that a free trade agreement is a free trade agreement. There are no tariff barriers in NAFTA. To talk about “equalization” of tariffs… There is nothing to be renegotiated. There are no large substantial issues. The issues are, as I said, on the order of those (a) the United States has been consistently in violation of its NAFTA obligations to Canada in the lumber sector over the past 25 years, (b) the United States has, I believe, been consistently in violation of its NAFTA obligations to Mexico in transport services, and (c) the Canadian cultural thing—Lenny Kravitz, Celine Dion. Should we let Hollywood wipe them off the Canadian airwaves?

Gillian Tett: When Secretary Ross suddenly makes lumber and milk key trade issues, is that justified under NAFTA or is that just plucked out of thin air?

Brad DeLong: That is just plucked out of thin air. Admittedly, there have for a long time been many congressmen and senators in the United States who have been upset about the implications of NAFTA. I remember a conversation in the buffet line at Jackson Hole with the chief of staff of one of the Democratic senators. Is it really worth taking a stand here? There response was: yes—we have our lumber and cheese producers, a lot of them, whose interests we need to advance.

That was the thing we had hoped to get away from with free trade. Agreements that were simple, global, comprehensive, and grew the economy so that even the losers from the individual provisions would acknowledge that they had gained more than enough to compensate them from the greater market scale. The spillovers from faster and greater economic growth would make it win-win in five years even if it were a shock now.

The reverse? We know what happens then, too. The spider-diagram from Charlie Kindleberger’s The World in Depression. The collapse of world trade in the early 1930s.

Gillian Tett: The chart that you put up there showing globalization going up like a rocket. Have you tried to calculate what that means for world GDP and so forth? How serious would it be if protectionism does come in?

Brad DeLong: Trade does lead to big redistributions. It leads to big movements of goods and services. But if everything had to be produced at home, prices of most things would not go up by all that much. Australia could run an automobile industry, but at something like 30% subsidies, a 30% cost increase. 10% of the economy in manufacturing that is foreign value added—a 3% hit to global GDP from a coming of some form of protectionism. You can say that’s not very much: 2 years of global north economic growth. But with a world GDP of $80 trillion—that’s a $240 billion a year loss. We do not have a world—you would know it in this room, at this hotel, in this conference—but we do not have a world in which everybody is incredibly rich. We live in a world in which a quarter of our number live lives very much like our pre-industrial ancestors, save that they do have some access to the village smartphone. Fear about where the food is going to come from next week is still a thing for a quarter of humanity.

Only a tenth of humanity has what those of us in this room would regard as a normal, even a bare-bones standard of living.

In that context, $240 billion a year of lost production would be seriously felt by a lot of people. It is not enough to derange an entire economy or to grossly destabilize global asset prices. But there are a lot of people out there whom it would seriously hurt.

Gillian Tett: Steve, when you look at things, is it just business as usual? Do you just try to push ahead with TPP? Or is there something else you can do to promote more globalization?

Steven Ciobo: The outcomes of this global discuss has been an empowering of pro-globalization advocacy. I may feel it more keenly than others. But in the context of myself and the other members of the government, we feel emboldened to stress the benefits of free trade. When you feel under siege, you have to talk about history. You have to talk about how from the 1960s on trade growth was about double GDP growth. We know that trade drives growth. We know that trade drives jobs. I will use illustration after illustration, companies, businesses, and others, that our benefiting from tree trade. This may not be a uniform media environment—but often it is—they will always put the factory closure on the front page and talk about how many workers have lost their jobs. They will never put the business expansion and the extra employment to meet international orders. We have to be realistic. The world is more global than it has ever been. Labor is global. Capital is global. We are kidding ourselves if we do not appreciate that, for the generations coming through now, national boundaries, especially in the western world, mean less than they have ever meant before. That is what we need to tap into.

Gillian Tett: So when you look ahead a couple of years from now, do you see us operating in a climate of more protectionism or less protectionism?

Steve Ciobo: Well, if we are operating in an environment of more protectionism in a decade’s time, we will all be more impoverished. Full stop.

Gillian Tett: How about you, Brad? Do you think that we will be having more protectionism in a decade’s time or less protectionism?

Brad DeLong: I think more. But not significantly more. The secular stagnation issues—that governments are unwilling to increase their purchases, that central banks are largely tapped out and have pushed the pedal to the floor, that redirecting spending to domestically-produced goods is a lever that can and might create jobs—some governments will decide that they have to pull that lever. So there will be some increase in protectionism.

There will also be some reduction in intercontinental value chains. Nike will bring some production back from Vietnam to outside of Boston. It will figure out how to build robots that can handle not just rigid metal and plastic but flexible leather and fabric, and sew shoes. They will get it. Something like a return of the mass production era reshoring, the implications of secular stagnation and aggregate demand pressures, with the burbling underlying political pressures. Lots of people think something is going wrong, lots of politicians are looking for somebody to blame, and the best person for a politician to blame is a foreigner who does not go to the voting booth when they run for reelection. That’s an easy way to go—whether it is true or not.

Gillian Tett: Right. John, do you expect more protectionism? Or less?

John Hagel: In the short term I do expect more protectionism. As an optimist, I view it as a catalyst to force us to reassess our institutions. Broadly, the shift that we see that we need to make is to shift from a model of institutions—and I am not talking about companies alone but all institutions—built on a model of scalable efficiency, thank you Ronald Coase, to a model of scalable learning that will help all of us to learn faster and achieve more of our potential and that will bring us back to more of a globalized mindset.

Gillian Tett: Right. Well, trust the Silicon Valley boys to be more optimistic. Silver linings. Alejandro: more or less protectionism in a few years time?

Alejandro Ramirez: Slightly more, at the global level. But I am an optimist and I hope we will see less after this time that is a little bit turbulent. Mexico, for instance, is trying to open up or strengthen trade relationships with the rest of the world. 80% of our trade is with the U.S. Reach out to Latin America. Modernize and deepen our free trade agreement with the European Union. Open up to Asia. My hope is that we will see less protectionism.

Gillian Tett: Steve. I have chucked many hard questions at you. Only fair to let you have the last word. More protectionism or less?

Steve Schwarzman: Gee. I don’t know whether I want the first word, or the last word.

Gillian Tett: You can have both.

Steve Schwarzman: You will probably see in a historical context a little more. But this is a cycle we are going through. Once you get through the cycle you will have a new baseline and move on to other things. John is right: this is just one part of a very complex set of circumstances, with technology a leader in terms of putting pressure on government and people, and trade gets mixed up with that to some degree as do other political factors. We as a society are going to have to work our way through these things. We have to find a way to deal with technology, with education, which at least in the United States has steadily been declining. We are now number 27 in the world. You cannot deal with important issues like technology putting pressure on margins, returns, job creation expressed through different types of unhappiness with trade and other things without the educational aspect. We used to be in the top three in the world. To become 27 is a remarkable achievement in 25 years. If you do not address that, this will not be the only panel that has not completely cheerful things to say.

Gillian Tett: Right. I think the clear consensus is, by about 4.5 votes, short term pessimism—you are an elected politician so you cannot be short term pessimism—but medium to long term hopes, hopes that this is a cycle. That rocket diagram graph that Brad presented is one quite optimistic framing. Let’s hope that that rocket keeps going up.

Thank you all very much indeed for your time. And best of luck.

This is a weekly post we publish on Fridays with links to articles that touch on economic inequality and growth. The first section is a round-up of what Equitable Growth published this week and the second is the work we’re highlighting from elsewhere. We won’t be the first to share these articles, but we hope by taking a look back at the whole week, we can put them in context.

Equitable Growth round-up

Three years after Thomas Piketty’s “Capital in the Twenty-First Century” became a surprise best-seller, “After Piketty: The Agenda for Economics and Inequality,” edited by Heather Boushey, Brad Delong, and Marshall Steinbaum, takes a deeper look at what Piketty’s work means for our current era. The volume, to be released next week, brings together the written reactions of a diverse group of scholars and helps set the research agenda moving forward. We provide an excerpt here.

We all know the role that debt can play in recessions, but what about credit? Nick Bunker writes about research that shows that an increase in an economy’s credit is a better predictor of how severe a recession will be compared to the level of debt.

A recent paper shows that corporations in high-income countries have all increased their savings rate, and are now lending more to the global economy than they are investing in their own corporations.

How has income inequality changed over time? Nick Bunker highlights recent research that looks at data spanning from 1957 to 2013 and finds that the median lifetime income for men has fallen by a stunning 10 percent to 19 percent. And while the results for women are less frightening, the data for the most recent groups show a stagnation.

Links from around the web

Dylan Matthews takes a closer look at the American Health Care Act, and shows why it reverses the reductions in income inequality that Obamacare created and more, leaving many people, especially the poor, worse off than they were before the Affordable Care Act. [vox]

Men’s declining labor force participation isn’t just a short-term economic issue. Andrew L. Yarrow argues that it’s harming today’s kids in a way that may exacerbate the intergenerational transmission of inequality. [san francisco chronicle]

Research shows that noncompete agreements can lower wages, reduce employee motivation, and stymie innovation. This is a sizeable problem considering that 1 in 6 workers are subject to these contracts. Orly Lobel, a University of San Diego Law Professor, argues that we should ban noncompetes, at least for low-wage workers. [new york times]

New research shows that educated workers are much likelier to receive disability insurance benefits compared to workers with a high school degree or less. Kathy Ruffing takes a closer look at why this is considering the outsize benefits of disability insurance for less-educated workers. [cbpp]

Alexia Fernández Campbell wrote about a survey of renowned economists done last week in which every single one rejected the notion that the draft Trump tax plan will pay for itself. [vox]

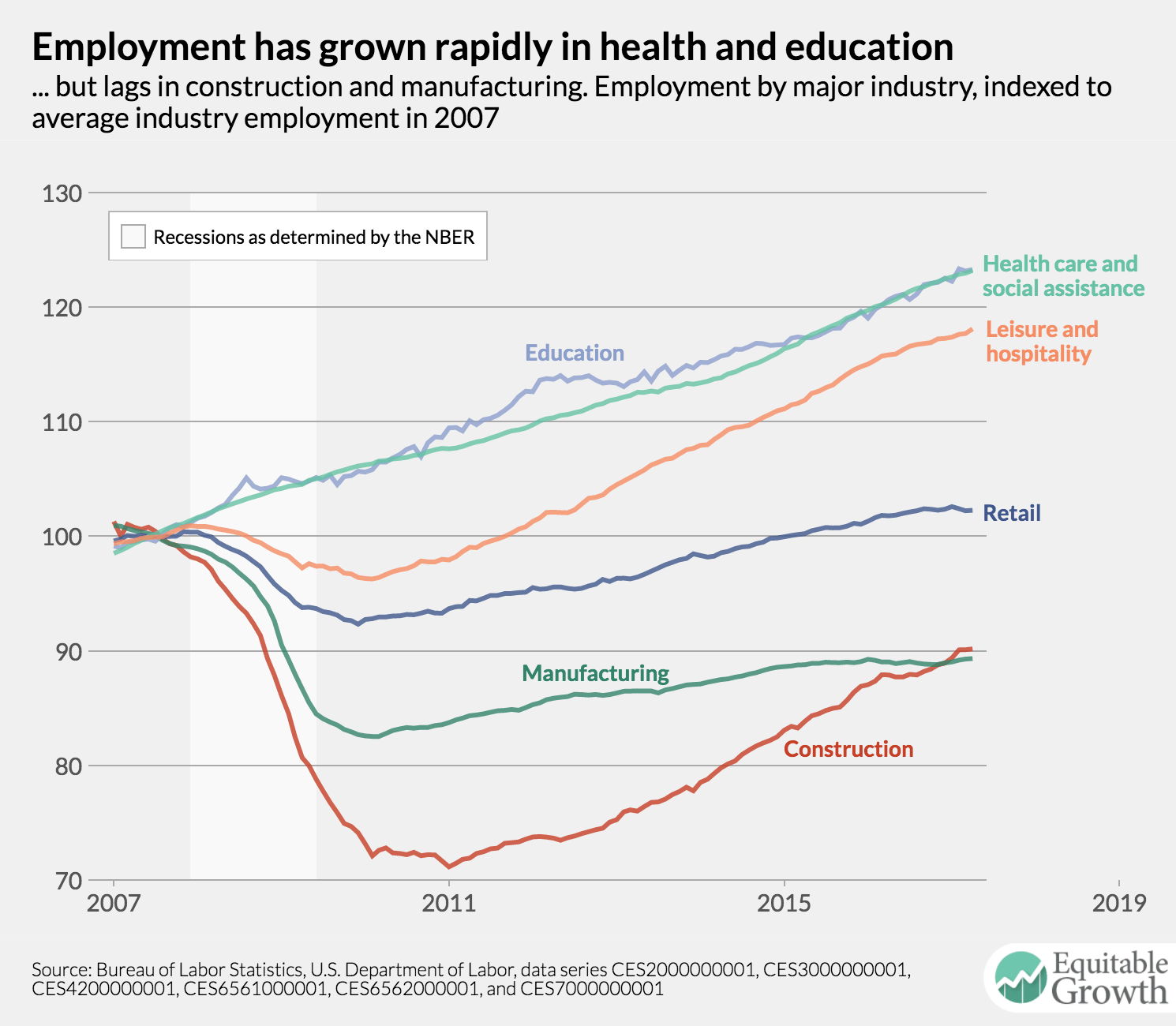

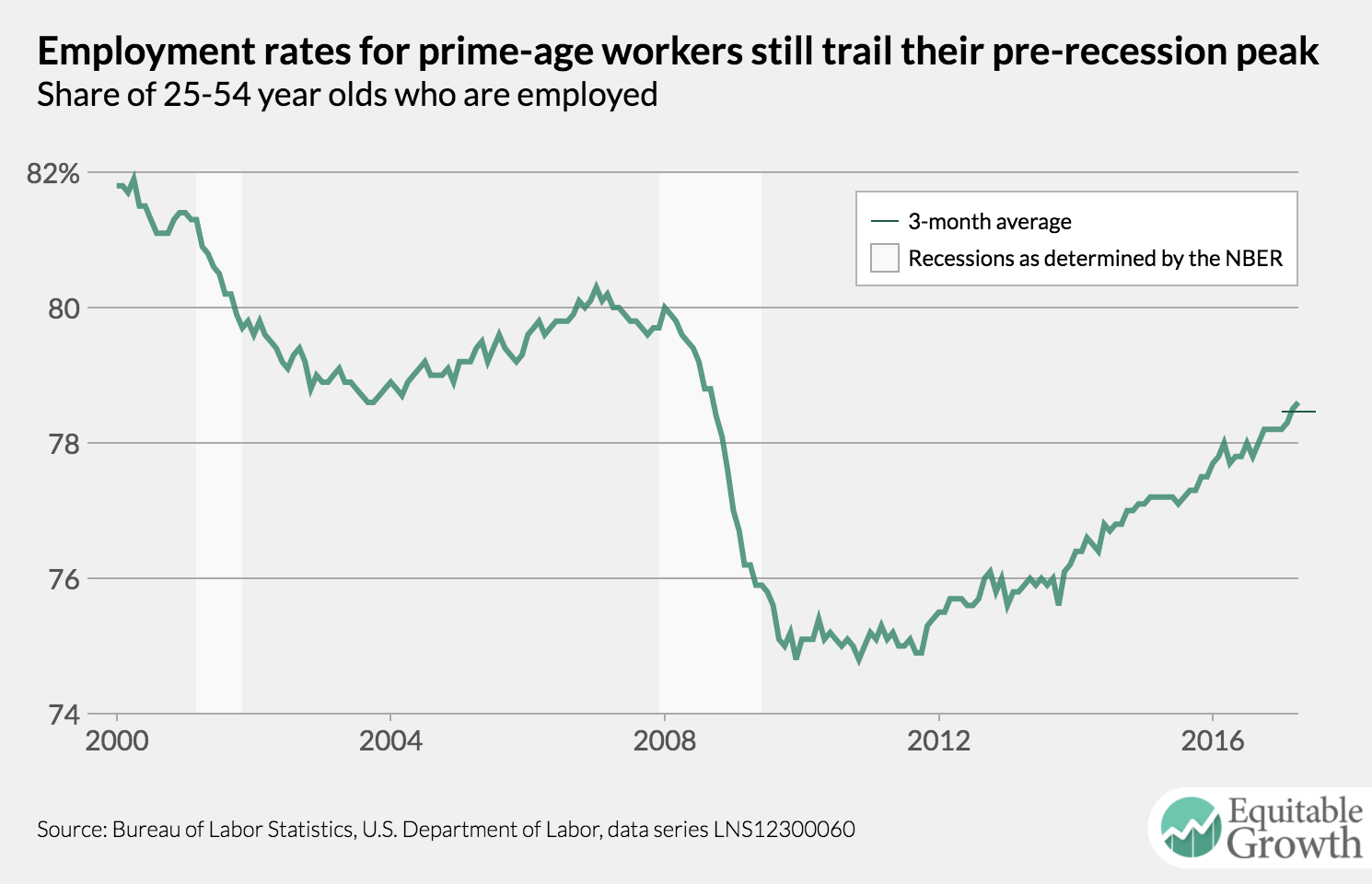

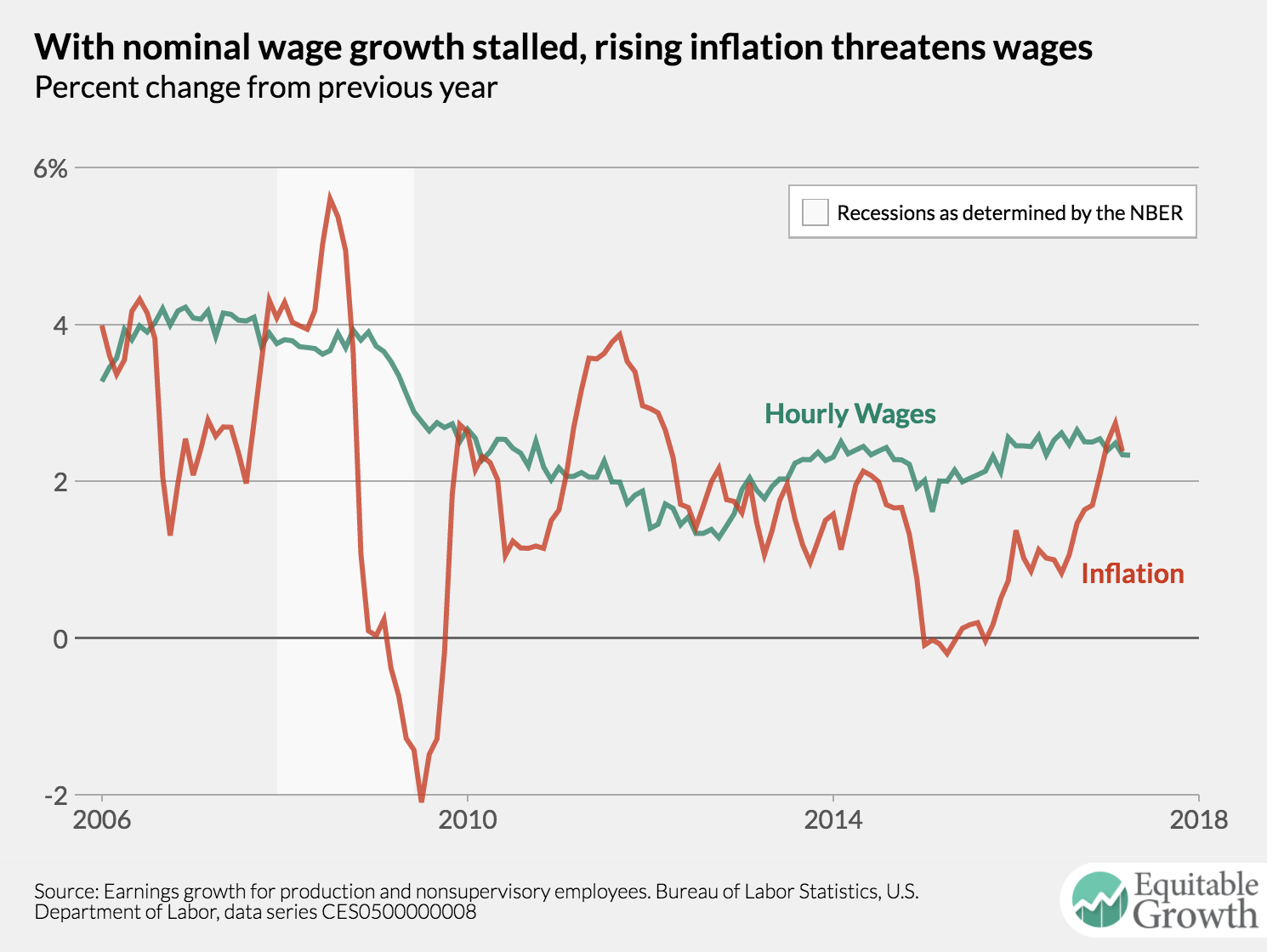

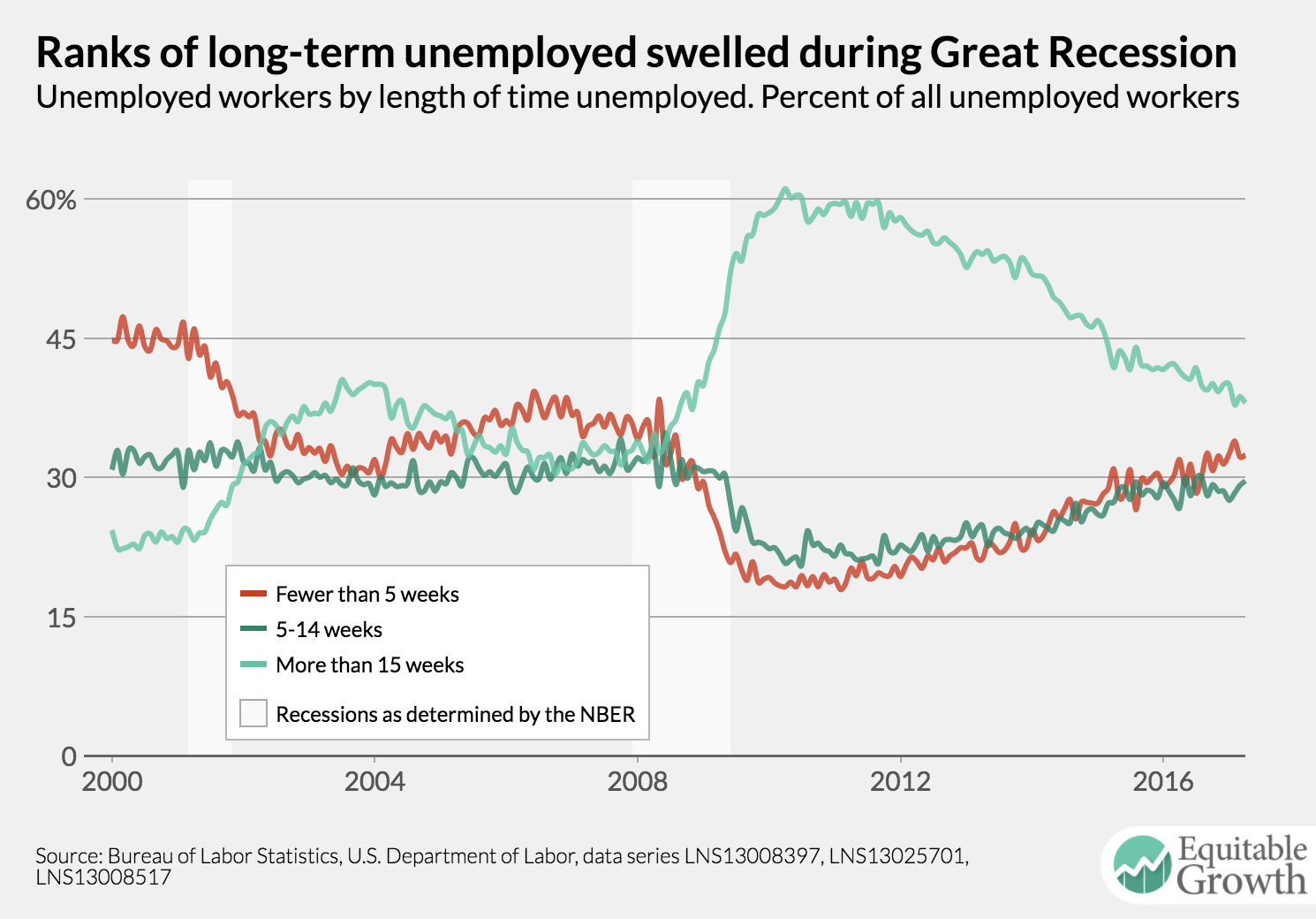

Earlier this morning, The U.S. Bureau of Labor Statistics released new data on the U.S. labor market during the month of April. Below are five graphs compiled by Equitable Growth staff highlighting important trends in the data.

1.

The share of prime-age workers with a job increased slightly in April, once again reaching a new high for this recovery. But it remains below pre-recession levels.

a

2.

Wage growth for non-managerial workers continues to stagnate in the face of inflation near two percent.

a

3.

Retail employment was muted in April, adding only 6,000 jobs, but that was a welcome change from declines in previous months.

a

4.

As unemployment continues to decline, the share who’ve been unemployed for 15 weeks or more also continues to decline.

a

5.

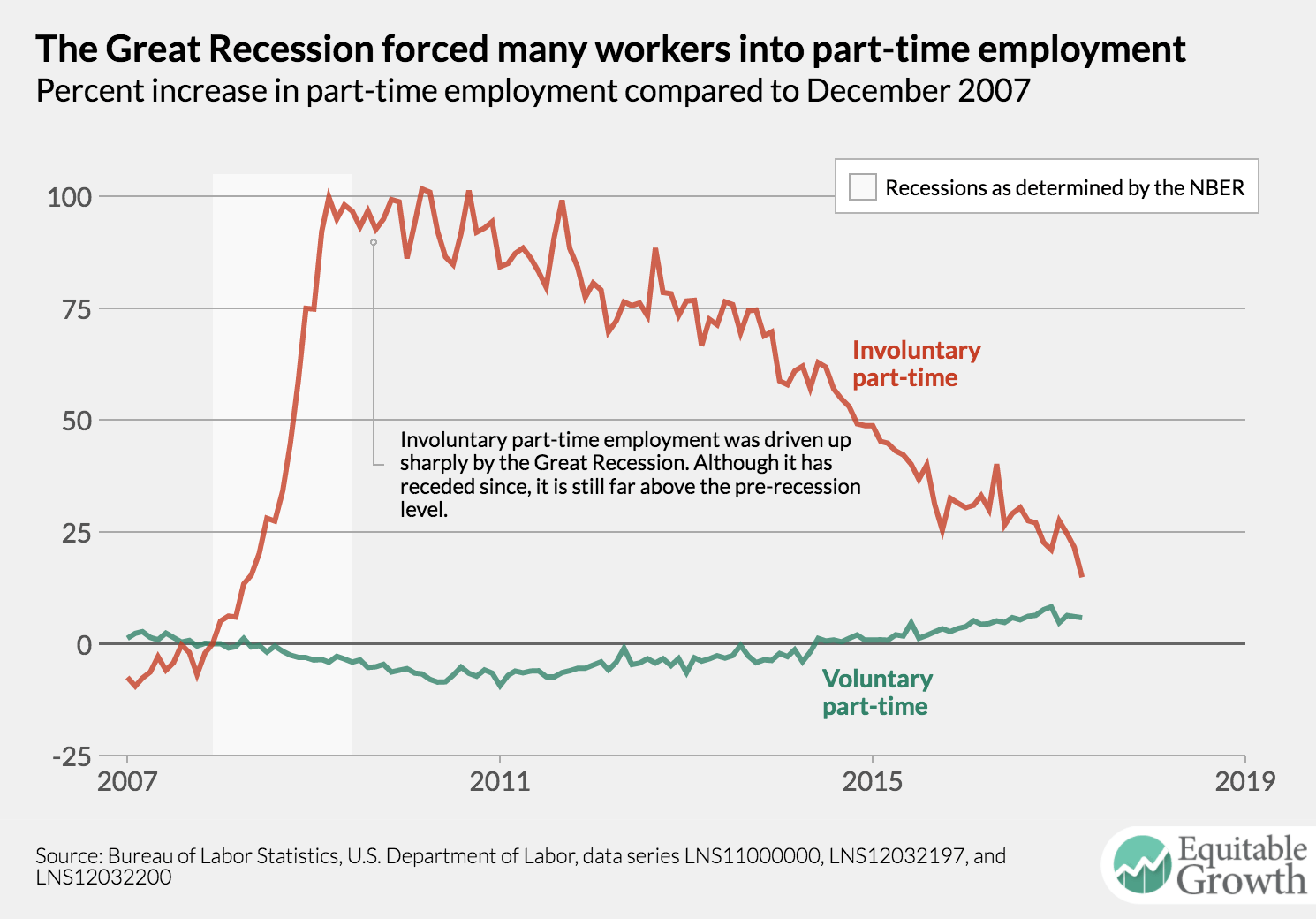

The increase in part-time workers who’d like to work full-time is abating, but the number of these workers is still above pre-recession levels.

…to rates of absolute mobility in the 1940s…. Because a large fraction of GDP goes to a small fraction of high-income households today, higher GDP growth does not substantially increase the number of children who earn more than their parents…. [But] changing the distribution of growth naturally has smaller effects on absolute mobility when there is very little growth to be distributed. The key point is that increasing absolute mobility substantially would require more broad-based economic growth…. Absolute mobility has declined sharply in the US over the past half century primarily because of the growth in inequality. If one wants to revive the American Dream of high rates of absolute mobility, one must have an interest in growth that is shared more broadly across the income distribution…

Tamim Bayoumi and Barry Eichengreen: Shocking Aspects of European Monetary Unification: “Data on output and prices for 11 EC member nations… http://www.nber.org/papers/w3949

Neil Ericsson, David Hendry, and Stedman Hood: Milton Friedman and data adjustment: “Milton Friedman more than doubled the observed initial stock of money to account for a ‘changing degree of financial sophistication’…. His data adjustment dramatically reduced apparent movements in the velocity of circulation of money, and it adversely affected the constancy and fit of his estimated money demand models…” http://voxeu.org/article/milton-friedman-and-data-adjustment

Kris Mitchener and Gonçalo Pina: Pegxit Pressure: “Markets [may] expect countries to abandon pegs and devalue their currencies [because of] shocks to the value of their output. During the classical gold standard era commodity price fluctuations determined expected devaluation…” http://voxeu.org/article/pegxit-pressure

“After Piketty” Excerpthttp://www.bradford-delong.com/2017/05/after-piketty-excerpt.html: “While we will not repeat the cultural dominance of property of the 1870–1914 Belle Époque French Third Republic, we do look to be engaged in the process of echoing many of its main characteristics…”

Should-Read: Tamim Bayoumi and Barry Eichengreen (1992): Shocking Aspects of European Monetary Unification: “Data on output and prices for 11 EC member nations… http://www.nber.org/papers/w3949

…aggregate supply and demand disturbances… a VAR decomposition…. Underlying shocks are significantly more idiosyncratic across EC countries than across US regions, which may indicate that the EC will find it more difficult to operate a monetary union. However a core… Germany and her immediate neighbors… shocks of similar magnitude and cohesion as the US regions. EC countries also exhibit a slower response to aggregate shocks than US regions, presumably reflecting lower factor mobility…

…exclud[ing] the US and other TPP members from the Americas. But it adds Cambodia, China itself, India, Indonesia, South Korea, Laos, Myanmar, the Philippines and Thailand. Including the world’s two most populous states, RCEP’s members generate some 31 per cent of world exports and its aggregate GDP is bigger than that of the TPP. Though less ambitious than the accord abandoned by President Trump, the RCEP could form the basis of a future free trade area of Asia and the western Pacific, but one with China, not the US, as the hub….

China’s “One Belt, One Road” initiative… might accelerate the emergence of such a market… us[ing] China’s capital and organisational abilities to enhance the supply of infrastructure…. The infrastructure needs of the Asia-Pacific region are so vast that additional Chinese resources should be helpful.

The world, and so Asia, is now in an unstable balance between globalisation and deglobalisation and between US and Chinese leadership. The US is turning its back on its postwar role, once so vital to Asia’s economic success. Will what takes its place be chaos and confusion or a new order built around China? Optimists might consider this a time of opportunity. Pessimists can consider it a time of danger. It is in fact both.