What is going on with wage growth in the United States?

Fast wage growth is a key feature of a strong labor market. U.S. workers, and low-wage workers in particular, experienced exceptional wage growth over the past couple of years, which not only improved workers’ lives but also notably reduced wage inequality.

There are various ways that economists and policymakers measure U.S. wages, each capturing wage growth from different angles and influenced by different factors. Some common measures include:

- Average hourly earnings from the monthly Bureau of Labor Statistics’ jobs report, which are based on the earnings of whoever happens to be working in a given month. As a result, changes in the composition of the workforce or the mix of jobs can lead to changes in these measures of wage growth. For instance, because of a phenomenon sometimes called composition bias, measures of average hourly earnings often show wage growth increasing at the beginning of a recession, since the first people laid off tend to have systematically lower wages. This raises the average wage of people who remain employed and produces “growth” in wages, even if none of the workers remaining in the labor force got a raise.

- Measures of hourly compensation and unit labor costs published in the quarterly labor productivity release by BLS’s Office of Productivity and Technology. These estimates are based on aggregate data on output, hours worked, and compensation costs collected by other programs. Shifts in the composition of the workforce or the mix of jobs can also influence these aggregates, making these measures susceptible to composition bias as well.

- The Atlanta Fed’s wage growth tracker, which is based on the Current Population Survey and focuses on wage growth among people employed in the same month of consecutive years. As such, this measure is not affected by changes in the composition of the workforce but could be influenced, for instance, by workers shifting jobs across industries.

- The Employment Cost Index, which is published by the Bureau of Labor Statistics and is based on employers’ reports of the cost of employing workers in certain jobs. This makes it less likely to reflect shifts in the composition of workers or jobs, but also potentially makes it less reflective of wage growth arising from well-established career progressions that involve changing job types.

- Growth in posted wages, measured by the job listings board Indeed, which reflect employers’ wage offers when advertising vacancies rather than actual wages paid to workers. This measure may be influenced by a variety of factors, ranging from changes in the mix of jobs to employers’ recruiting strategies.

Recently, almost all of these important indicators of U.S. wage growth were updated with data through March or April of 2024 (technical changes to the underlying data have delayed the April update to the Atlanta Fed’s wage growth tracker). The new data paint a fairly consistent picture of gradually declining wage growth that, even as it goes down, remains elevated relative to pre-pandemic rates. (See Figure 1.)

Figure 1

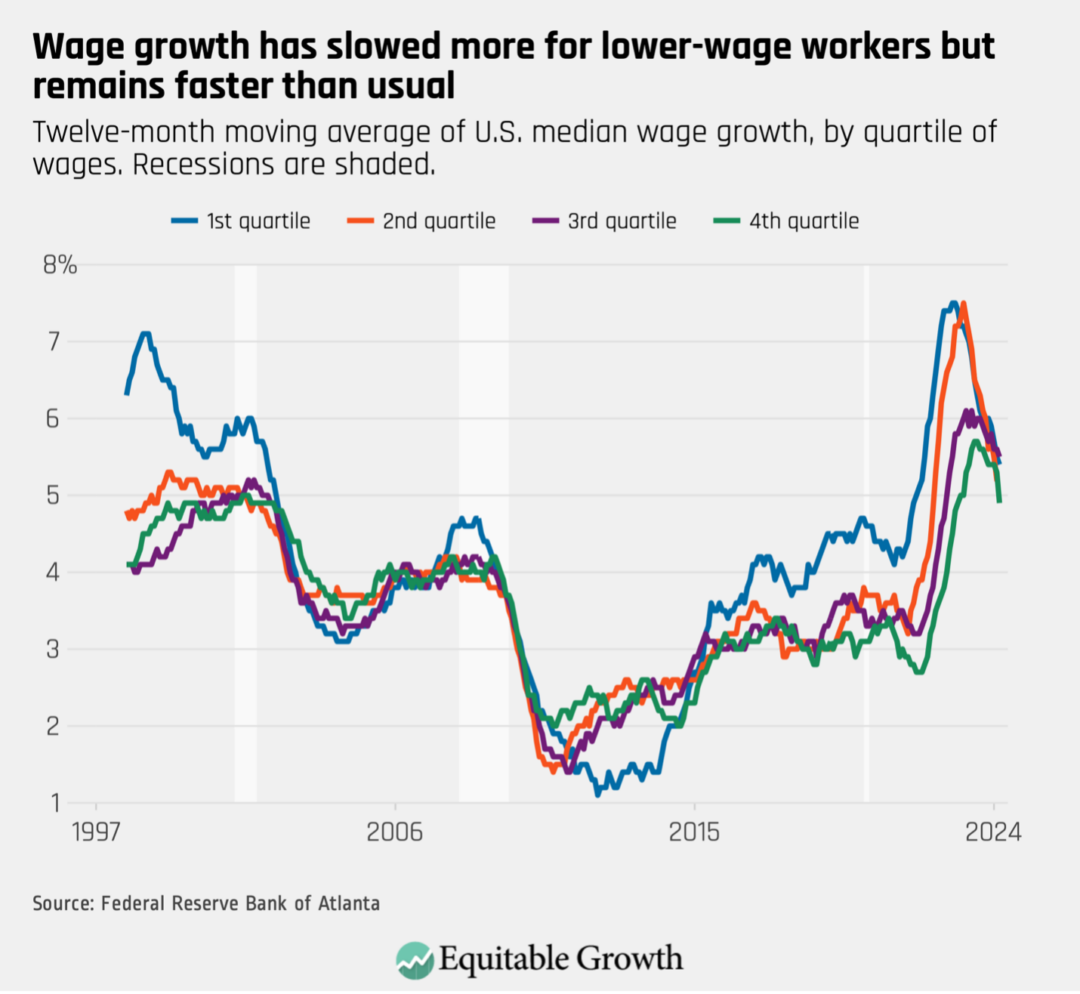

The data also show that wage growth has become somewhat less egalitarian than it was at the peak of the post-pandemic U.S. labor market, though it remains more equitable than it was prior to the pandemic. Lower-wage U.S. workers saw their wage growth accelerate relative to higher-wage workers in the second half of 2021, building on gains they made late in the recovery from the Great Recession; their wage growth is still faster than higher-wage workers, but the gap has closed. (See Figure 2.)

Figure 2

Likewise, earlier in the post-pandemic recovery, U.S. workers with only a high school diploma experienced faster wage growth than those with associate’s degrees, who, in turn, registered faster growth than those with bachelor’s degrees or higher. Now, all three groups see similar rates of wage growth, a departure from the usual advantage held by more-educated workers.

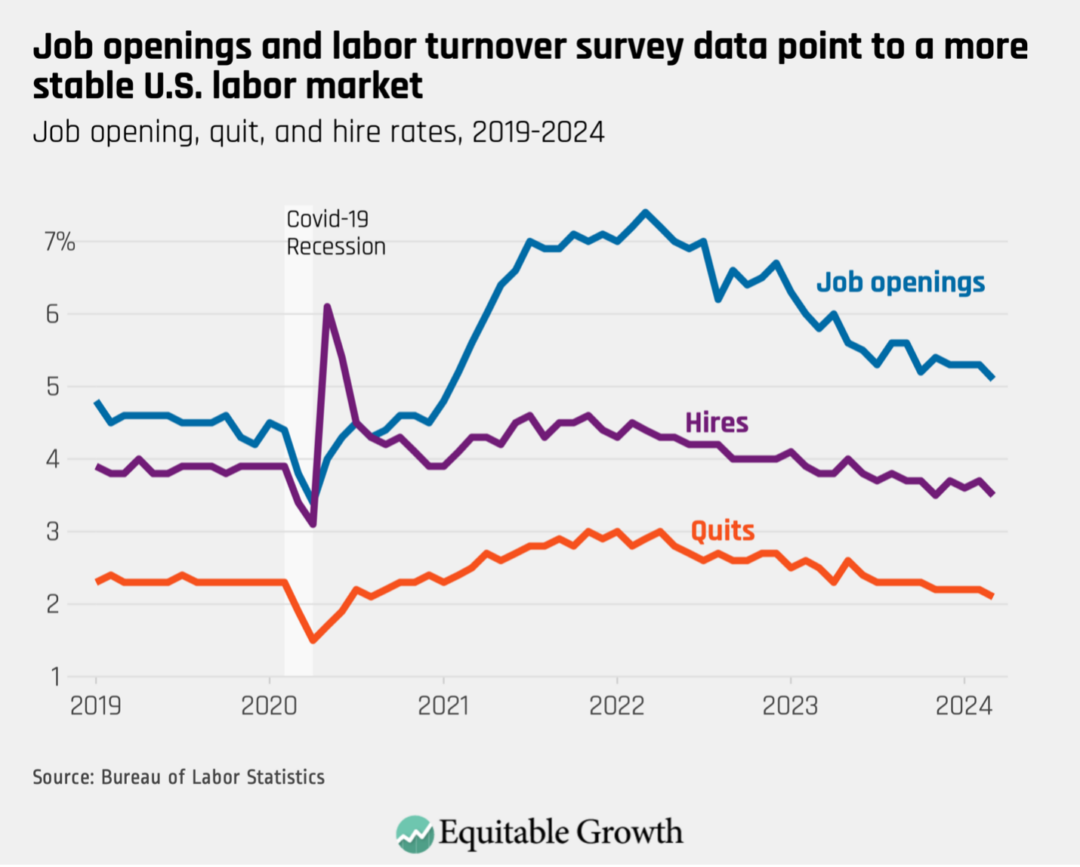

The current stability of the U.S. labor market probably makes the methodological differences between the wage measures less important, leaving each to reflect a similar underlying story of declining wage growth. Unlike over the past few years—which saw large shifts out of and back into the labor force, as well as some reallocation across job types, surrounding the onset of the COVID-19 pandemic—U.S. employment is now more stable. After peaking in 2021 and 2022, the number of open jobs is declining and the quit rate has returned to pre-pandemic levels, suggesting that workers now see fewer opportunities to change jobs than they did in the recent past. (See Figure 3.)

Figure 3

Declining U.S. wage growth is of particular interest because of its potential influence on inflation and the role it could play in informing how the Federal Reserve conducts monetary policy. Because one of the Fed’s two main goals is to maintain price stability, it quickly raised interest rates in 2022 and early 2023 in an attempt to counteract inflationary pressure in the U.S. economy. Leaving rates high after those pressures have abated, however, could risk a recession that could devastate the U.S. labor market.

From the perspective of wanting to avoid such a monetary-policy-induced recession, high wage growth (and any attendant inflationary pressure) is concerning, and so slower wage growth could be encouraging for monetary policymakers—to a point. Low-wage workers would likely bear the brunt of a recession caused by tight monetary policy aimed at reducing wage growth. Sacrificing the aspects of the current labor market that benefit these workers in the name of avoiding the possibility of a downturn would not be ideal.

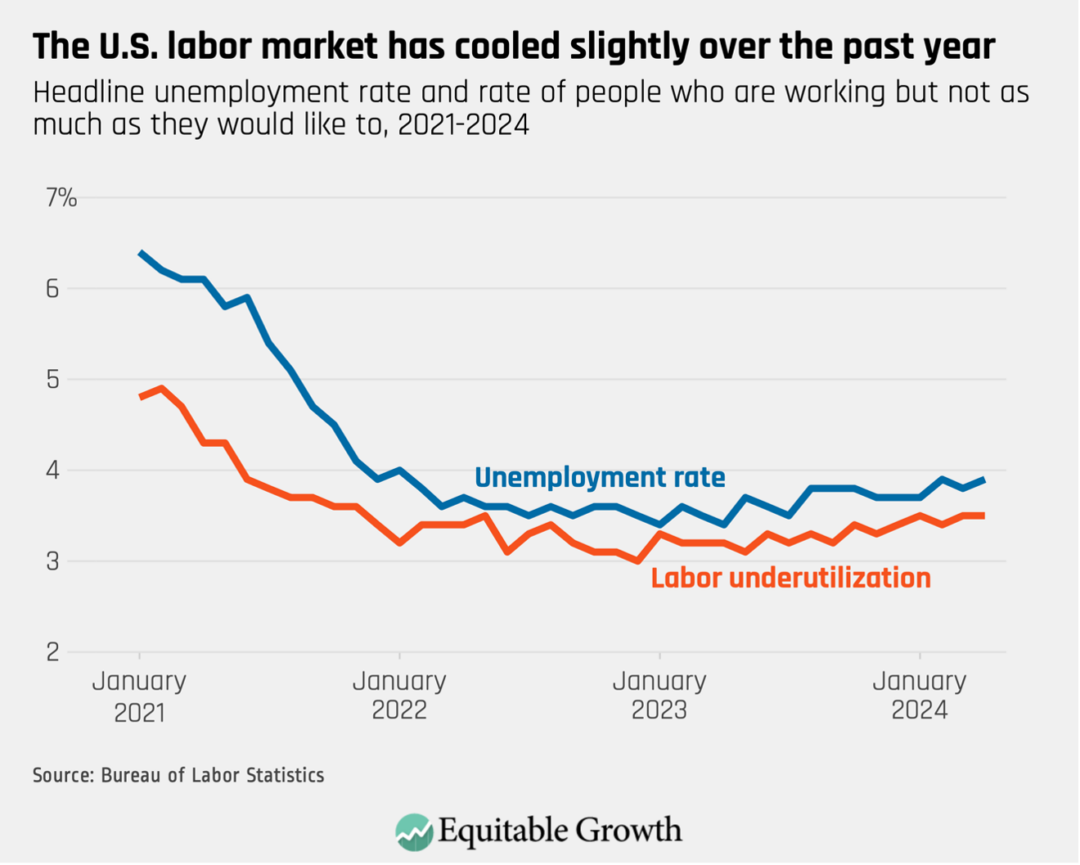

In this context, current labor market dynamics support the prospect of wage growth continuing to slow across the U.S. economy. While still low, U.S. unemployment has ticked up over the past several months, and the pool of workers not counted as unemployed but also not working as much as they would like to also has grown. (See Figure 4.)

Figure 4

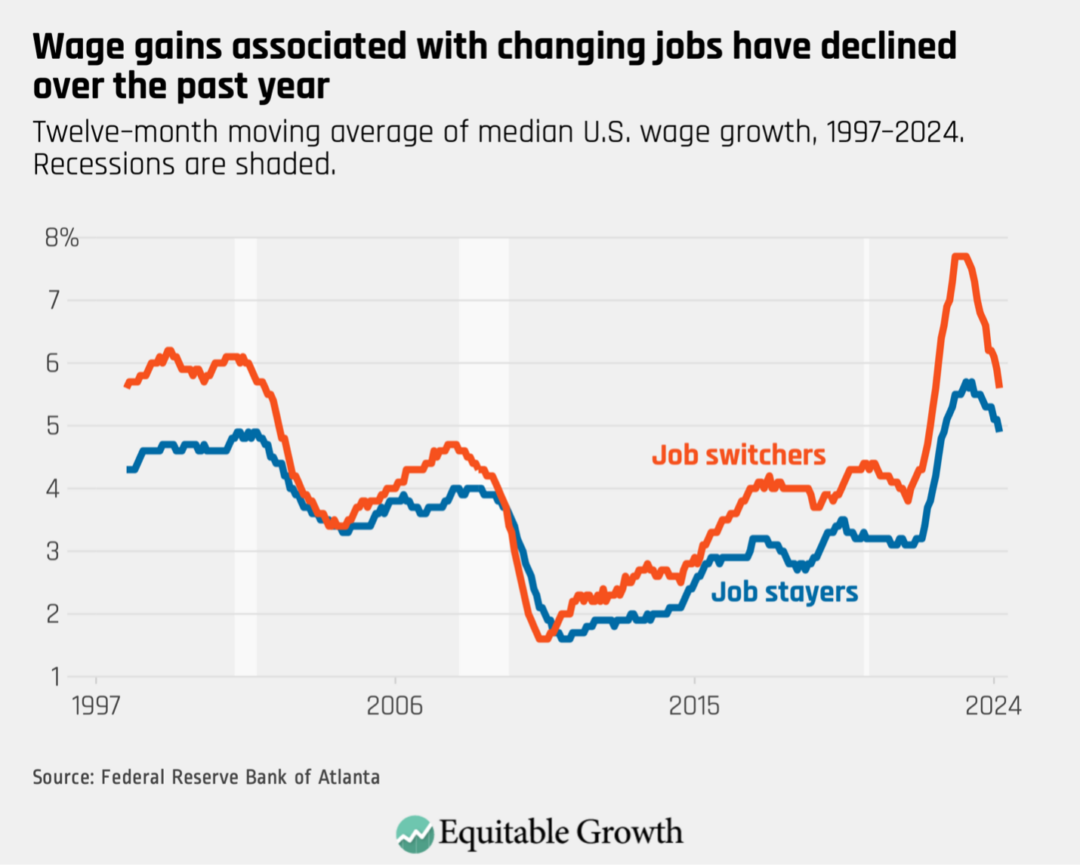

This larger group of available or underutilized workers may point toward employers not feeling the need to offer wage increases as large as they had in recent years to attract employees to their job openings. This is reflected directly in the decline in Indeed’s posted wage growth measure. The declining quit rate also could be a reflection of workers’ reduced ability to secure higher wages by changing jobs, and the Atlanta Fed’s wage tracker shows that the typical wage gain experienced by job changers has declined substantially over approximately the past year.(See Figure 5.)

Figure 5

Increased labor productivity may also be limiting some inflationary pressure from current levels of wage growth. That’s because the faster productivity grows, the faster wages can grow without adding to inflation.

Productivity growth has now rebounded, as shown in Figure 1, after substantially lagging behind wage growth for much of 2021 and 2022. The gap between wage growth and productivity growth is at roughly the levels seen in the years preceding the pandemic, when inflation was low and stable. Yet productivity growth can be volatile, and it remains to be seen whether its relationship with wage growth will fully normalize going forward.

A wide range of workers benefit from the current full employment labor market. Yet with inflation still running above the Fed’s target despite ticking down in April, there could be some tension between the benefits of the faster wage growth it creates for workers and inflationary pressures that wage growth may produce. That said, a broad range of indicators show that wage growth is declining, and rebounding productivity growth further reduces potential contributions to inflation from wage growth.

This suggests that further weakening in the U.S. labor market is not necessary to control inflation. Current labor market fundamentals are in line with those seen in 2019, a period with low and stable inflation. Sustaining this labor market should be a primary goal of policymakers. As the Federal Reserve considers when and how to adjust interest rates, it should take care to avoid unnecessarily weakening it. High interest rates are already hurting poorer workers and families. A policy-induced recession would make that pain much more widespread.

Did you find this content informative and engaging?

Get updates and stay in tune with U.S. economic inequality and growth!