Why antitrust enforcement and regulatory oversight in digital communications matter

Overview

Digital communications platforms, whether offered by a cable company, a telecommunications firm, or an Internet services provider, deliver the most important text and video content that powers our economy, educates our citizenry, and fuels our democracy. Yet the business dynamics of these platforms and the natural incentives of platform owners to overcharge consumers for their goods and services create enormous opportunities for competitive abuse—harming consumers and exacerbating economic inequality—unless vigorous public oversight corrects significant and pervasive market imperfections. These increasingly anti-competitive digital business practices also are a drag on our nation’s economic growth, causing consumers to overspend on these services far beyond what is necessary to induce any increased productive investments by firms in this key industry.

Download File

A communications oligopoly on steroids

Read the full PDF in your browser

Under U.S. law, antitrust enforcement is one critical element necessary to protect consumers and the competitive process. Yet antitrust by itself is not enough to ensure the marketplace benefits and potential progressive societal advancements that digital communications platforms offer. Antitrust enforcement can prevent the creation of monopolies and actions that diminish competition, but these laws are not designed to maximize competitive options or promote social policies such as expanded employment, equitable access to content, and overall freedom of expression. Only with appropriately focused regulatory oversight alongside strict antitrust enforcement can the service providers in the cable, telecommunications, wireless, and broadband industries be driven to offer competitive, nondiscriminatory, innovative, and socially beneficial video and broadband services that maximize consumer value and choice in both the economic market and the marketplace of ideas. These steps, in turn, will boost demand for these goods and services in the broader economy and spark more investments in innovation and new infrastructure.

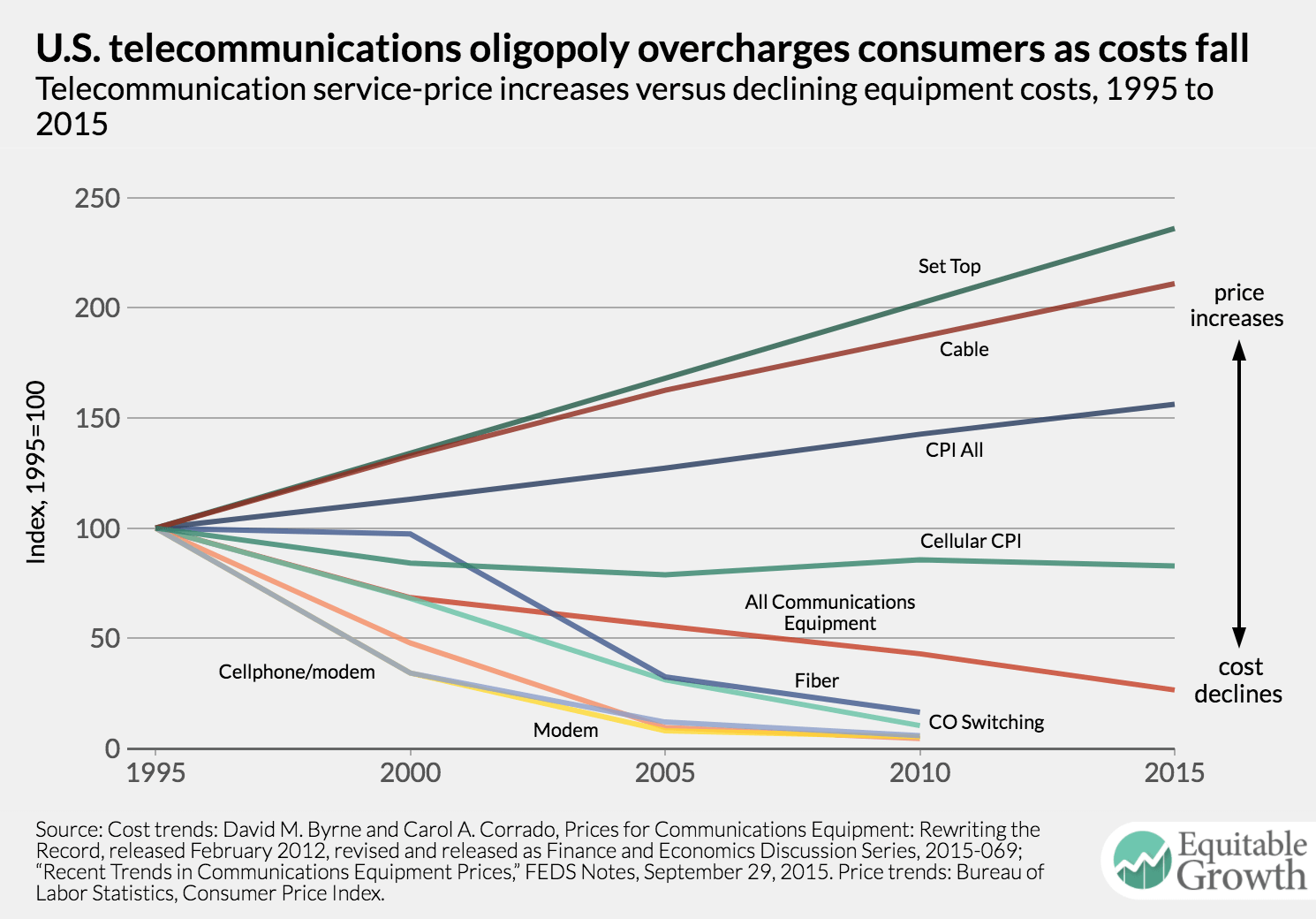

This paper details the state of these communications industries in the first dozen years after enactment of the 1996 Telecommunications Act, which opened the door to lax antitrust enforcement and excessive deregulation and led to highly concentrated oligopolistic markets that result today in massive overcharges for consumer and business services. 1 Prices for cable, broadband, wired telecommunications, and wireless services have been inflated, on average, by about 25 percent above what competitive markets should deliver, costing the typical U.S. household more than $45 per month, or $540 per year, for these services.2 This stranglehold over these essential means of communication by a tight oligopoly on steroids—comprised of AT&T Inc., Verizon Communications Inc., Comcast Corp., and Charter Communications Inc. and built through mergers and acquisitions, not competition—costs consumers in aggregate almost $60 billion per year, or about 25 percent of the total average consumer’s monthly bill.

The paper then examines the efforts by the Obama administration to arrest this uncompetitive trend by launching numerous regulatory interventions and enhanced antitrust enforcement.3 These efforts resulted in a change in course that was strongly positive for U.S. consumers and the economy. Alas, these actions could not address all of the structural harms caused by previous policy mistakes. What’s more, these ongoing antitrust problems in the communications sector are unlikely to be addressed by the new Trump administration, which has signaled that it will seek to reverse many of the gains to consumers achieved under the Obama administration.

Potential remedies, however, remain within reach of policymakers in Congress, at the Federal Communications Commission—the chief telecommunications regulatory agency in this business arena—and at the other two key federal antitrust enforcers, the Federal Trade Commission and the U.S. Department of Justice. In the pages that follow, this paper will explain these complex antitrust and regulatory processes in the telecommunications sector, trace how antitrust and regulatory actions have performed since the enactment of the 1996 Telecommunications Act, and then showcase a number of efforts made by the Obama administration to protect consumers and strengthen competition in the various communications industries—efforts that were partially successful but are now under threat under the new Trump administration.

Key Takeaways

- On average, prices for cable, broadband, wired telecommunications, and wireless services charged by the telecommunications oligopoly in the United States are inflated by about 25 percent above what competitive markets should deliver, costing the typical U.S. household more than $45 a month, or $540 a year.

- U.S. consumers in aggregate pay almost $60 billion per year to the telecommunications oligopoly due to inflated prices for cable, broadband, wired telecommunications, and wireless services.

- The concentration of four main U.S. telecommunications companies enables these firms to earn astronomical profits. Their earnings before interest, taxes, and depreciation and amortization, or EBITDA, a standard financial measure of profitability, are between 50 percent and 90 percent compared to the national average for all industries of just under 15 percent.

- The measure of market concentration of these four telecommunications firms based on the standard Herfindahl-Hirschman Index, or HHI, used by antitrust regulators, stands at between 2,800 and 6,600 compared to the currently acceptable market concentration level of 2,500.

- Due to rigorous antitrust enforcement in 2011 that blocked a proposed merger between AT&T and T-Mobile, the wireless services sector of the telecommunications industry is the only one with meaningful competition. By 2015, the average revenue per user accrued by wireless services providers was between $4-to-$5 less than it would have been, saving consumers in total more than $11 billion per year.

End Notes

1. This paper draws heavily on Gene Kimmelman and Mark Cooper, “Antitrust and Economic Regulation: Essential and Complementary Tools to Maximize Consumer Welfare and Freedom of Expression in the Digital Age,” Harvard Law & Policy Review 9-2 (2015): 403, available at http://harvardlpr.com/wp-content/uploads/2015/07/9.2_5_KimmelmanCooper.pdf; Mark Cooper, “Overcharged and Underserved: How a Tight Oligopoly on Steroids Undermines Competition and Harms Consumers in Digital Communications Markets.” Working Paper (Roosevelt Institute, 2016), available at http://rooseveltinstitute.org/wp-content/uploads/2017/02/Overcharged-and-Underserved.pdf.

2. See Cooper, “Overcharged and Underserved,” Chapter IX.

3. Ibid., Chapter I.

Related

Explore the Equitable Growth network of experts around the country and get answers to today's most pressing questions!