This is a weekly post we publish on Fridays with links to articles that touch on economic inequality and growth. The first section is a round-up of what Equitable Growth published this week and the second is the work we’re highlighting from elsewhere. We won’t be the first to share these articles, but we hope by taking a look back at the whole week, we can put them in context.

Equitable Growth round-up

Weak U.S. productivity growth has been one of the most troubling trends since the Great Recession. Is it just a coincidence that productivity has been weak since the crash? Or did the recession have an impact?

The conventional wisdom about encouraging entrepreneurship is that policymakers should increase the return to starting a business. But increasing evidence shows that we should be concerned about reducing the cost of a failing business as well.

The permanent income hypothesis is an important tool for thinking about how people react to drops or boosts to their income. The idea, however, has some flaws and doesn’t hold up for the entire U.S. population.

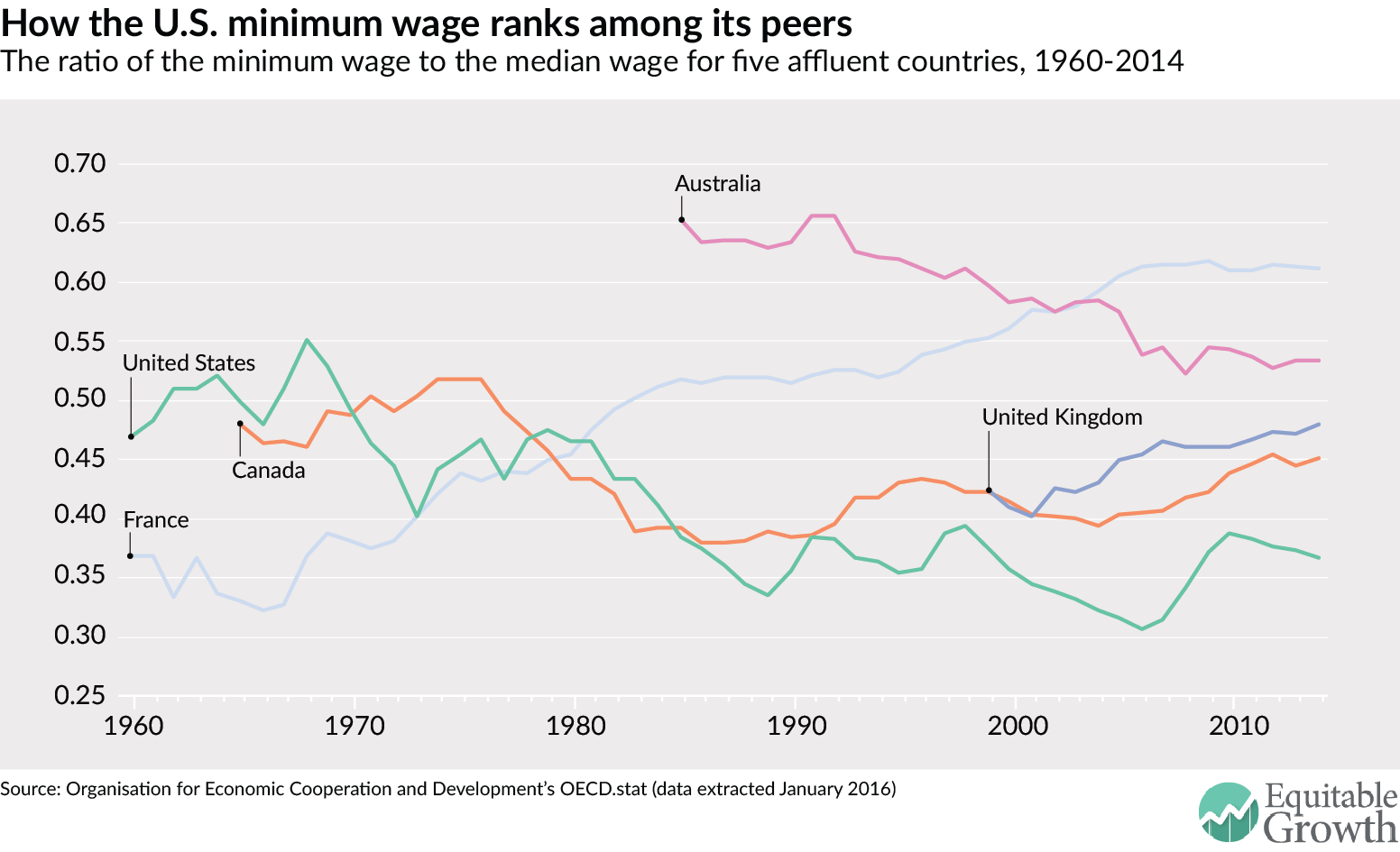

With the policy conversation centered on proposals to raise the minimum wage to rates unseen in the United States, it’s hard to tell how such an increase would play out in the United States. New School economist and Equitable Growth grantee David Howell takes a look at the international data for answers. And Bridget Ansel pulls out some of the key graphs and takeaways from Howell’s brief.

Links from around the web

The Federal Reserve kept U.S. interest rates steady at its most recent meeting this week. Ylan Mui writes that the central bank is coming around to the view that U.S. economic growth in the future will be much weaker than it previously thought. [wonkblog]

Because the Federal Reserve has kept U.S. interest rates so low for so long, some economists have thrown out the idea that low interest rates are causing low inflation despite the established view that low interest rates increase inflation. Noah Smith reports on a new paper that tries to settle the question that has quite interesting results. [bloomberg view]

Speaking of unconventional monetary policy, the prospect of “helicopter money” becoming a real world policy is starting to sink in among economists and policy analysts. Neil Irwin gives some background on the idea. [the upshot]

How important is the U.S. government to economic growth and economic policy writ large? Mike Konczal reviews two books on the topic with very different opinions on the matter. [boston review]

“Red tape no doubt prevents some firms from making growth-boosting investments. But bigger gains might come from creating an economy in which firms found themselves needing to compete to attract workers.” Ryan Avent writes on the increase evidence that economic sclerosis in high-income countries is related to inequality and insufficient demand. [the economist]

Friday figure

Figure from “The employment effects of a much higher U.S. federal minimum wage: Lessons from other rich countries” by David Howell