Well, that was a very interesting election night. Our failure in 2000 to introduce into the running code (as opposed to the specification document) of our constitution that electors switch votes so that the national popular vote winner wins the electoral college cost us dear in 2000, and may cost us even more today…

You may ask: How is one to judge what to do in such times? The answer is clear: As one has ever judged. Good and evil have not changed since yesteryear, nor are they one thing among Elves and another among Men. It is a human’s part to discern them, as much in the Golden Wood as in his own house. What would have been good policy yesterday would still be good policy today. What would have been bad policy yesterday would still be bad policy today. So we play our position.

I therefore set forth seven principles that should govern good technocratic fiscal policies that promise to enhance America’s societal well-being :

- Preserve Our Credit

- Our National Debt a National Blessing

- Right Now Our National Debt Is too Low

- International Agencies Agree

- Benefits from a Higher Deficit If We Are at Full Employment

- Benefits from a Higher Deficit If We Are Not at Full Employment

-

A Strong Argument for More Government Purchases Rather than Tax Cuts for the Rich

-

Preserve Our Credit: President-elect Donald Trump has been told by many that our national debt is too high and dangerous. He has responded as one would expect a real estate developer would respond. He has proposed taking steps to shake the confidence of our creditors, and then to buy back our debt, at a heavy discount, thus removing the danger. This is a substantial misreading of the situation. Market confidence in the credit worthiness of the United States of America is an extremely valuable asset, from which we derive much benefit, and which it would be folly to throw away.

-

Our National Debt a National Blessing: In fact, at the moment, with interest rates where they are now and are expected to be for the foreseeable future, our national debt is not a burden but a blessing. It is not a drain on the Treasury but a source of wealth for the Treasury. If we do our accounts using a reasonable benchmark–setting our goal to be keeping our available physical space constant–we find that, at the levels of interest rates we see now and expect to see for the foreseeable future, a lower national that would not allow us to lower but would require us to raise taxes in order to maintain the given level of spending. The United States right now is not in the position of a cash-strapped borrower forced to pay interest. The United States right now is, rather, in the position of something like the medieval Medici bank, which people pay to safeguard their money.

-

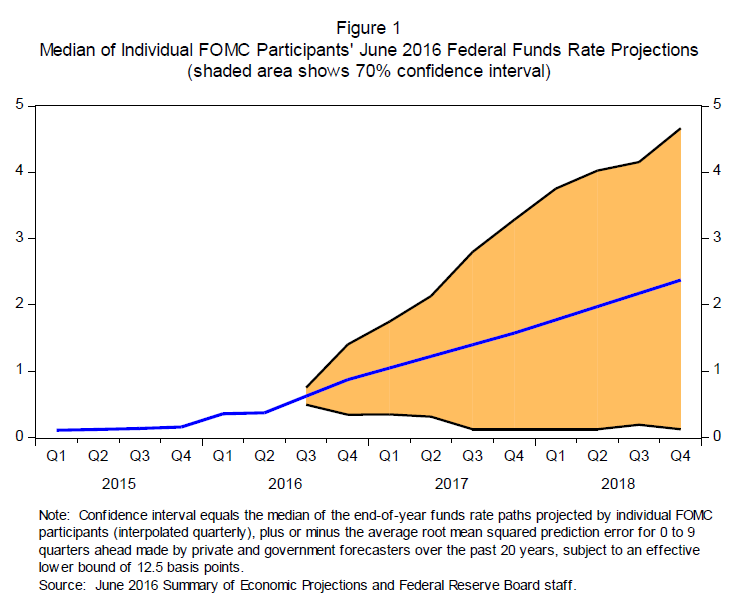

Right Now Our National Debt Is too Low: The fact is that our national debt, right now, is not a burden but a profit center. That implies that, whatever you think of the long-term multi-generational fiscal outlook, right now our national debt is not too high but too low. That is the case unless one confidently anticipates a rapid and substantial increase in interest rates in the relatively near future. This was, in fact, one of the major lesson of the big article that Larry Summers and I wrote for the Brookings Institution back in 2012.

-

International Agencies Agree: Note that, after four years of argument, the IMF and other international agences agree with Larry and my technocratic judgment that right now our national debt is too low, and thus that good economic policy requires higher deficits right now, not budget balance.

-

Benefits from a Higher Deficit If We Are at Full Employment: Right now, only the extremely rash would definitely claim to know one way or the other whether the United States is at full employment–whether further increases in the employment-to-population ratio would (1) start an inflationary spiral and require the Federal Reserve to raise interest rates to lower employment back down to its current level, or (2) bring large numbers of discouraged workers back into the labor force and make America richer. If the answer is (1), there are still substantial benefits to an economic policy stance, right now and for the foreseeable future as long as the global configuration of savings supply and investment demand is not transformed, with a larger deficit and tighter money and hence higher interest rates. Higher interest rates would restore the health of the banking sector. Higher interest rates might discourage the blowing of potentially dangerous bubbles. The drawback of raising interest rates–the reason that the Federal Reserve has not done so–is that it lowers employment. But if that reduction in employment is offset by an increase in the deficit that boosts employment, hit becomes a no-drawbacks policy.

-

Benefits from a Higher Deficit If We Are Not at Full Employment: Right now, only the extremely rash would definitely claim to know one way or the other whether the United States is at full employment–whether further increases in the employment-to-population ratio would (1) start an inflationary spiral and require the Federal Reserve to raise interest rates to lower employment back down to its current level, or (2) bring large numbers of discouraged workers back into the labor force and make America richer. If the answer is (2), there are massive benefits to an economic policy stance of running larger deficits–the benefit of raising employment and making people richer, and making those people richer who have suffered the most since the subprime crisis and crash of 2008.

-

A Strong Argument for More Government Purchases Rather than Tax Cuts for the Rich: If America does decide to run larger deficits, there are large benefits from choosing to do so by increasing government purchases than by cutting taxes, especially for the rich. Increasing government purchases puts to work and improves the lot of the people who have suffered the most since the subprime crisis and crash of 2008. And cutting taxes–especially for the rich–has much smaller effects on the balance between savings and the capital inflow on the one hand and investment and government borrowing on the other. Since the effectiveness of the policy in putting people to work and in creating space for the Federal Reserve to raise interest rates to a healthy level without harming employment depends on this investment-savings balance, there is much more bang for a buck of government purchases than from a buck of tax cuts.

{kind=link}