Ireland’s spectacular economic growth reveals a stark truth about corporate tax avoidance

If you were tuning in to the world economy for the first time, last Tuesday’s release from Ireland’s Central Statistics Office would probably convince you that the Irish economy is booming. According to the Irish agency’s annual national income statistics, the domestic economy in 2015 grew a staggering 26.3 percent in real terms (after accounting for inflation). These are numbers you don’t even see in developing countries. They are unheard of in an advanced economy. And far from experiencing healthy, robust growth, most advanced economies are struggling to generate even low single-digit economic growth. So these numbers should raise an eyebrow.

Ireland’s gross domestic product growth rate isn’t a lie, but it highlights a peculiar thing about the country—its status as a tax haven. GDP measures the total value of everything produced within the country. But in Ireland’s case, a lot of very big companies, many in the high technology and pharmaceutical industries, like to say all of their intellectual property rights exist in Ireland for tax purposes. When companies in these industries design a new product they can avoid paying U.S. corporate tax by transferring their intellectual property—such as patents and brands—to an Ireland-based subsidiary. Strategies to avoid taxation can get quite complex, including such “tax-efficiency” maneuvers as the “Double Irish” and the “Dutch Sandwich.”

Whatever the maneuver, profits from the sales of those items in the United States and around the world accrue to these firms’ Irish-based subsidiaries, resulting in a significantly reduced tax burden on those profits. This artificially inflates the size of the Irish economy and creates some wild gyrations in the country’s reported growth rate.

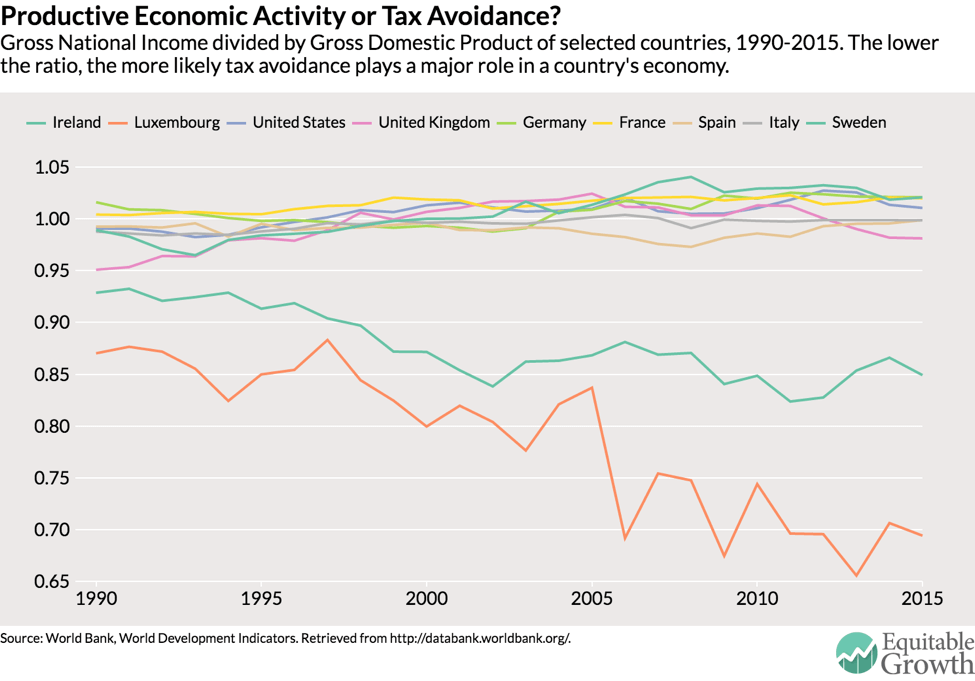

One way to show the severity of this issue in countries such as Ireland and other offshore tax havens is to divide their gross domestic product by an alternative measure of an economy’s size—gross national income, a measure of all the things produced by nationals of a country. An Irish person’s wages when working in the United States, for example, registers as Irish national income (while simultaneously registering in U.S. GDP figures). Gross national income also excludes foreign-owned earnings, including that intellectual property owned by U. S. companies that are located in tax havens.

The ratio of these measures in normal, non-tax haven countries usually hovers around one. The earnings of foreign-owned capital and labor and domestic-owned capital and labor deployed in foreign countries usually nets out. In tax-haven countries, however, this ratio can be extremely lopsided. In Ireland, the ratio as of 2015 was 0.85. In Luxembourg, the difference is even starker, coming in at 0.69. And these ratios have been trending downward as the level of tax avoidance in the world economy explodes. (See Figure 1.)

Figure 1

Now, there are other reasons why gross national income and gross domestic product can differ. The workforce of Luxembourg consists of many foreign residents and workers from nearby countries. But nonetheless, Luxembourg is widely known as a tax haven and some portion of this differential can be attributed to its role as one.

Now, there are other reasons why gross national income and gross domestic product can differ. The workforce of Luxembourg consists of many foreign residents and workers from nearby countries. But nonetheless, Luxembourg is widely known as a tax haven and some portion of this differential can be attributed to its role as one.

In his 2015 book “The Hidden Wealth of Nations: The Scourge of Tax Havens,” author Gabriel Zucman of the University of California-Berkeley estimates just how much money is being shifted around the world for purposes such as sheltering money from the tax authorities. He calculates that 55 percent of the $650 billion of foreign profits earned by U.S. companies in 2013 were booked in just six low-tax countries: The Netherlands, Bermuda, Luxembourg, Ireland, Singapore, and Switzerland. For U.S. companies, this comes out to about 18 percent of all U.S. corporate profits “earned” in tax havens, and results in lost tax revenue of about $130 billion a year. Kim Clausing of Reed College calculated similarly—about $100 billion a year in lost tax revenue.

Putting an end to international tax-avoidance is now a major focus of organizations such as the Organisation for Economic Co-operation and Development, which now boasts its “Base erosion and profit shifting” program. But more work needs to be done so that U.S. companies are not able to skirt their obligations. International coordination alongside smart business tax reform here in the United States could help put an end to corporate tax avoidance.