The U.S. macroeconomic data of the past 40 years have produced a number of surprising, and indeed puzzling, facts about economic growth and rising income and wealth inequality. Five of the most salient are:

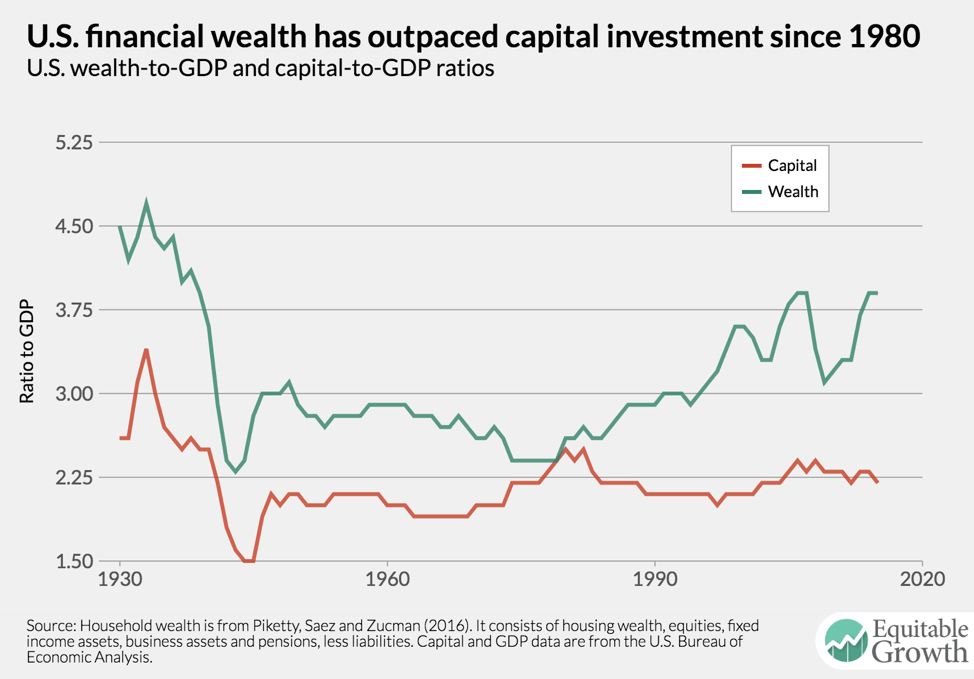

- Financial wealth has increased rapidly despite no real increase in the amount of investment in the economy.

- The financial value of many firms now is permanently higher than the cost of their assets.

- At the same time, these more valuable firms haven’t invested more in their own operations or workforces despite higher profits and low interest rates.

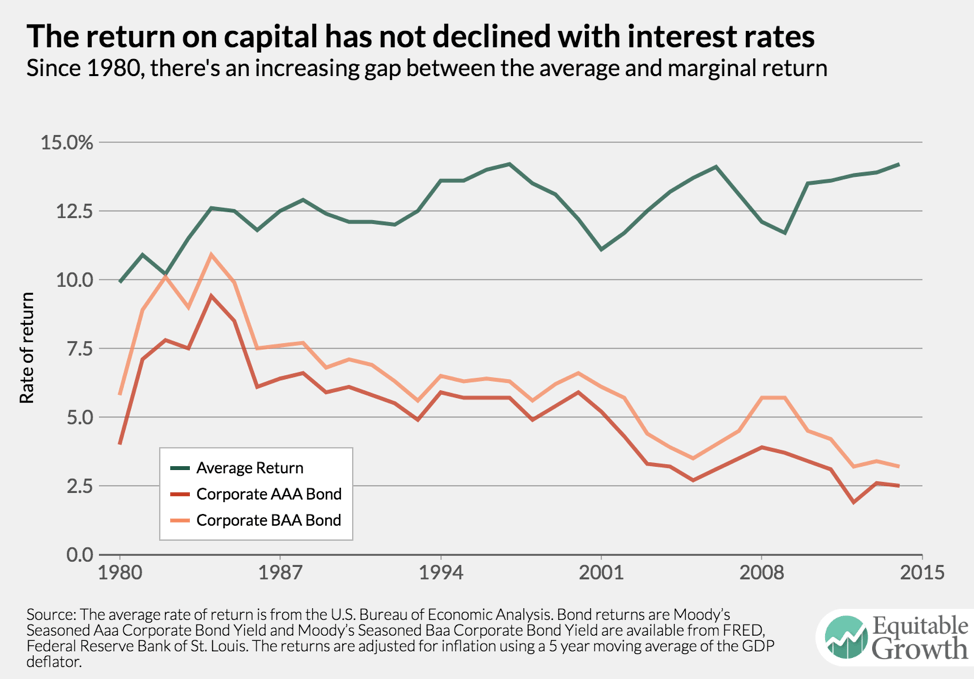

- The average rate of return on capital has stayed steady while interest rates have dropped.

- The share of income going to labor (in the form of wages, salaries, and other kinds of compensation for work) has declined as the share of income going to profits has increased.

In a new Equitable Growth working paper, Gauti Eggertsson, Ella Getz Wold, and I at Brown University argue that these diverse trends are closely connected, and that the driving force behind them is an increase in monopoly power together with a decline in interest rates.

These new facts are particularly puzzling from the point of view of the standard neoclassical economic model, in which markets are perfectly competitive. In this view, profits should not persist over the long run, let alone enable the owners of corporations to increase their share of income over time. The standard model, however, cannot address many of the fundamental changes that have occurred in the U.S. economy over the past 40 years.

In order to explain these new trends, I and my co-authors make several modifications to the standard model, among them positing imperfect market competition, financial assets based on monopoly profits, and the possibility that the natural rate of interest can change. With these parsimonious modifications, our model can explain the data in ways the old model cannot.

Here’s how it works: An increase in firms’ market power leads to an increase in monopoly rents-economic parlance for profits in excess of competitive market conditions-and thus an increase in the market value of stocks (which hold the rights to these rents). This leads to an increase in financial wealth and to what’s known as Tobin’s Q, the ratio of a firm’s financial value (market capitalization) to the value of its assets (book value). (See Figure 1.)

Figure 1

An increase in monopoly rents will tend to drive up the average return on capital, since the measurement of this return includes pure profits. To generate a constant average return, which is evident in the macroeconomic data, our paper contends there needs to be a decline in interest rates, which pushes down the average return on capital. These two forces cancel each other out, leading to a constant average return on capital. (See Figure 2.)

Figure 2

With an increase in market power, the share of income consisting of pure rents increases, while the labor and capital shares both decrease. Finally, the greater monopoly power of firms leads them to restrict output. In restricting their output, firms decrease their investment in productive capital, even in spite of low interest rates.

If there has been a sizeable increase in monopoly power, this trend would not only deepen our understanding of how the economy works but also lead to important implications for public policy. Greater monopoly power tends to depress economic growth and increase income and wealth inequality. With high levels of monopoly profits, it may be optimal to have higher taxes on corporate income than would be suggested by analyses that assume perfect market competition. Figuring out just how pervasive this monopoly power is in the U.S. economy is an important endeavor moving forward.

-Jacob A. Robbins is a Ph.D. candidate in economics at Brown University and a doctoral fellow at the Washington Center for Equitable Growth.