Good U.S. monetary policy can’t fix bad U.S. fiscal policy

This essay is part of Vision 2020: Evidence for a stronger economy, a compilation of 21 essays presenting innovative, evidence-based, and concrete ideas to shape the 2020 policy debate. The authors in the new book include preeminent economists, political scientists, and sociologists who use cutting-edge research methods to answer some of the thorniest economic questions facing policymakers today.

To read more about the Vision 2020 book and download the full collection of essays, click here.

Overview

In August 2018, Federal Reserve Chair Jerome Powell gave a speech in which he explained the macroeconomic “stars” that guide monetary policy.1 The three stars are the values for the unemployment rate (u), inflation (π), and the short-term interest rate (r), which together are consistent with long-run macroeconomic equilibrium. These three equilibrium variables are generally written with “stars”—as in u*, π*, and r*—in the mathematical representation of the New Keynesian macroeconomic models used by macroeconomists to discern the direction of economic activities. Powell stated in his speech that the stars were all aligned, with the exception that the Fed probably needed to continue gradually raising the federal funds rate, as in previous expansions.

U.S. stock markets became rattled shortly after Powell’s speech because the Fed continued to signal that it intended to move gradually to “normalize” (meaning raise) interest rates over the next few years. The steep decline in stock prices in October 2018 led to a change of tone by Fed officials by the end of 2018. Fed officials at first suggested there might be no need for future interest rate increases, and then completely switched direction and cut the target range for the federal funds rate by 50 basis points in 2019, from 2.25–2.5 to 1.75–2.0.

Many academic economists and other voices across the political spectrum argued that the Fed simply misjudged the value of r* (the equilibrium short-term interest rate, which in this essay will be used interchangeably) in recent years. John C. Williams, president of the New York Fed and vice chair of the Federal Open Market Committee, has long advanced the idea that r* has declined in recent decades.2 Williams is certainly not alone, with voices from both ends of the political spectrum arguing that maintaining low interest rates is crucial for continued economic expansion.3

In terms of the macroeconomic stars invoked by Fed Chairman Powell, there is widespread agreement that the U.S. economy today seems to be at or near full employment (u=u* in mathematical parlance) and that inflation is not rising (π ≤ π*). Therefore, higher interest rates would only do harm to an otherwise well-functioning economy. In contrast, fiscal policy (government revenues and spending) is holding back the U.S. economy because needed government investments in human capital, scientific research, or infrastructure are not happening.

This is the conundrum facing the monetary policymakers at the Fed. Lowering its benchmark federal funds rate will increase asset valuations and provide some economic stimulus, but without boosting potential long-run economic growth. The Fed may have little choice because fiscal policymakers, most of whom remain mistakenly fixated on rising government spending rather than on falling government revenue, will not support the government investments needed to boost long-term economic growth and prosperity. Should a recession occur, as one eventually will, Fed efforts to boost growth by lowering the short-term interest rate will be ineffective. Thus, in the event of a downturn, fiscal policymakers may once again be forced by events to provide short-term stimulus spending, but they will likely again fail to make the real investments necessary to boost long-run growth.

In this essay, I examine why a falling r* matters to the Fed, how lower interest rates increase asset valuations in the economy without boosting necessary investments, and then why fiscal policy has to change by recognizing that it is not rising government budget deficits that are a danger to future U.S. economic growth but rather falling government revenues. In short, I argue that appropriate monetary and fiscal policies in tandem will boost the income of the many—not just the value of assets owned by the few—to create the macroeconomic conditions most suitable for sustained and road-based economic growth.

Why has r* fallen, and why does it matter?

There is an active academic literature about a declining equilibrium short-term interest rate ( r* ) and the implications for Fed policy.4 The research on why r* has fallen mostly focuses on two key determinants: productivity growth and an aging population. Through the lens of New Keynesian macroeconomic models, when productivity growth slows, the demand for investment falls, and when populations age, the supply of saving rises. Declining demand for borrowed funds along with an increasing supply of saving pushes r* down.

Accepting the proposition that r* has fallen does not mean the crucial monetary policy questions are all resolved. When r* is low, for example, monetary policymakers have to be more concerned about limits on nominal interest rates. The real interest rate—the nominal rate minus inflation—is what impacts real behavior in New Keynesian models. So, if inflation and real interest rates are both low when the economy is expanding, then there is little room for monetary policymakers to cut real rates in the event of a downturn, because zero is a natural lower bound on nominal rates.5

A second practical issue associated with lower r* is that the return to risk-free savings is reduced. Low risk-free rates of return are most important for securing retirement incomes for both individual savers and institutional funds with guaranteed pension benefits and other forms of annuities. Savers are forced to accept greater risks in order to get positive financial returns in a world with low r* or to compensate for low returns in some other way, such as saving even more.

One potential benefit in a low-r* economy is that the cost of borrowing is also lower, but that assumes the risk premium—the wedge between private and government borrowing costs—remains stable. Unfortunately, risk premia are not stable, and large increases in risk premia are generally associated with the end of an economic expansion. At the end of an expansion, investors become worried that growth will slow, and thus borrowers will have difficulty repaying their debts. Lenders are willing to supply less in the way of new loans to businesses and consumers at any given interest rate. Even if the Fed can lower the risk-free interest rate, movements in the actual cost of borrowing for businesses and consumers will depend on what is happening with risk premia.

Movements in risk premia and other economic fundamentals affecting r* point to a broader set of questions connecting risk, return, and asset values. In particular, the value of corporate stock is the discounted present value of the future profits the corporation is expected to earn. For a given stream of expected profits and a given risk premium to compensate for the uncertainty of those profits, a lower r* increases the value of a share of stock.6 If the owners of the corporation can borrow to fund their operations more cheaply, then their profits will be higher, everything else equal.

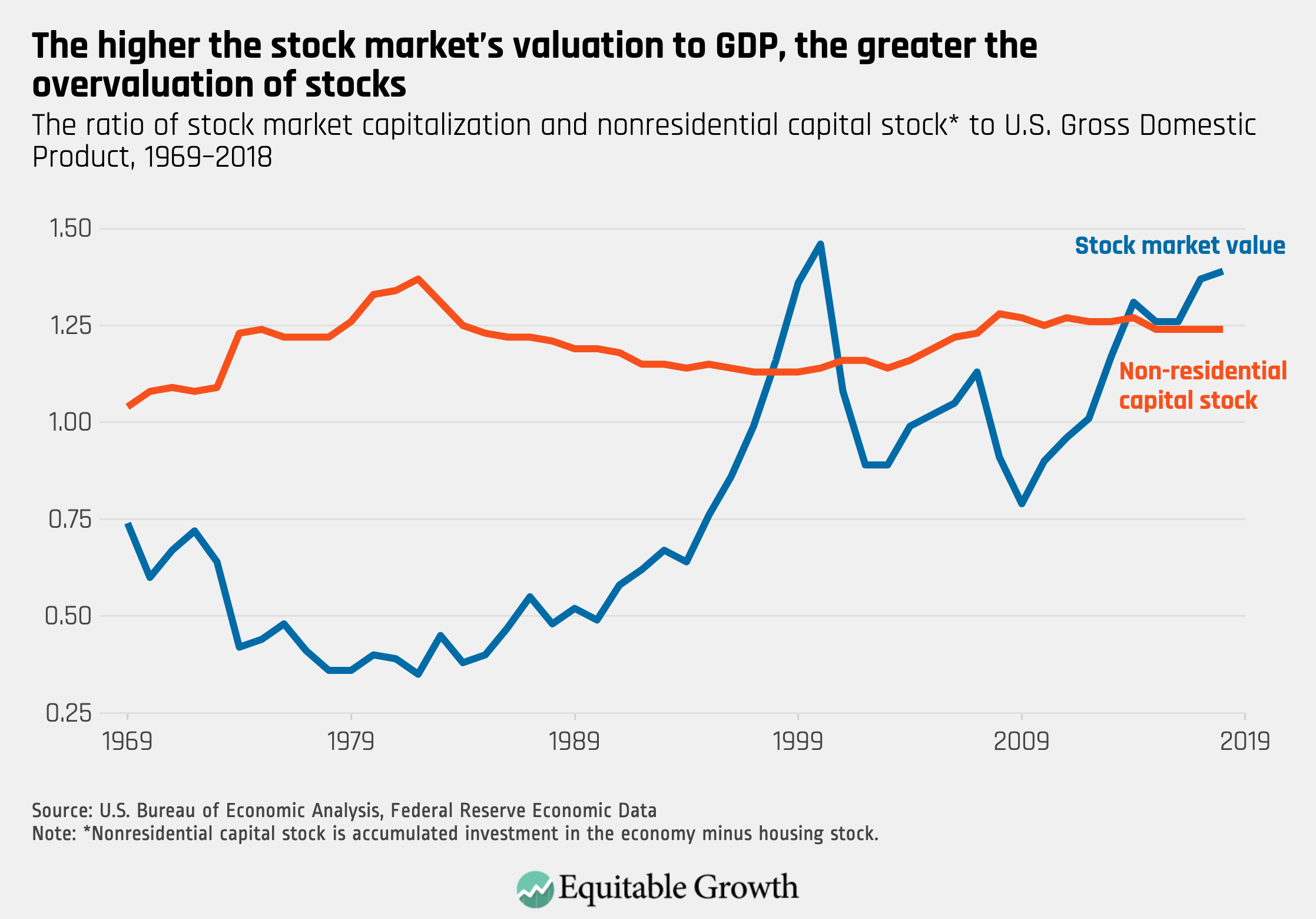

What can the current level of U.S. stock markets tell us about r* and other economic fundamentals? The famous value investor Warren Buffet has long advocated the following measure of stock market valuation: Add up all outstanding shares of corporate stock at current market values and divide by the size of the overall economy. A high ratio of stock market valuation to Gross Domestic Product indicates an overvalued market. At the end of 2018. the so-called Buffett Ratio was near the recent historical high that had occurred before the crash of 2000, and, in general, the ratio has been higher and much more volatile in recent decades. (See Figure 1.)

Figure 1

One possible explanation for a higher Buffett Ratio is more corporate investment, which will happen if people save more and capital markets convert that additional saving into real investment. Yet the other line in Figure 1 shows that accumulated investment in nonresidential capital stock relative to GDP has been stable. This means the level of interest rates and stock market valuations are not associated with greater real investments in the U.S. economy.

The share of national income going to corporate profits can also push up the Buffett Ratio because a higher profit share means the expected level of profits is higher. The ratio of measured corporate profits to GDP, however, cannot explain the increasing Buffett Ratio either, because there has been no corresponding increase in the corporate profits share.7

All of this evidence suggests that current stock market values are being maintained at historically high levels by the combination of low risk-free interest rates and low-risk premia. This ties the hands of the Fed because maintaining high asset-valuation ratios becomes essential for sustaining aggregate demand. Asset owners are willing to borrow, spend, and invest in productive capital when they feel wealthier. But if risk premia rise and asset values fall, then the resulting decreases in asset values will have disproportionate negative effects on spending and investment.8

Is U.S. monetary policy constrained by bad U.S. fiscal policy?

Evidence about asset valuation and asset price volatility suggests that describing economic fluctuations in terms of deviations from a New Keynesian equilibrium that ignores the risk premium is at best incomplete. The now-widespread belief that the Fed should simply acknowledge that r* has fallen goes hand in hand with accepting the inherent risk of keeping the economy growing by boosting the values of assets owned by the few, rather than boosting the incomes earned by the many.

This is where better fiscal policy becomes important. Although targeting a lower r* may be the best monetary policy given current fiscal policy, it is possible to change fiscal policy in ways that address the underlying reasons for declining r*. Better fiscal policy would make it possible for the Fed to conduct better monetary policy, meaning the Fed could achieve full employment and stable inflation—the U.S. central bank’s “dual mandate”—without the inherent financial market valuation issues and instability associated with a low r* equilibrium.

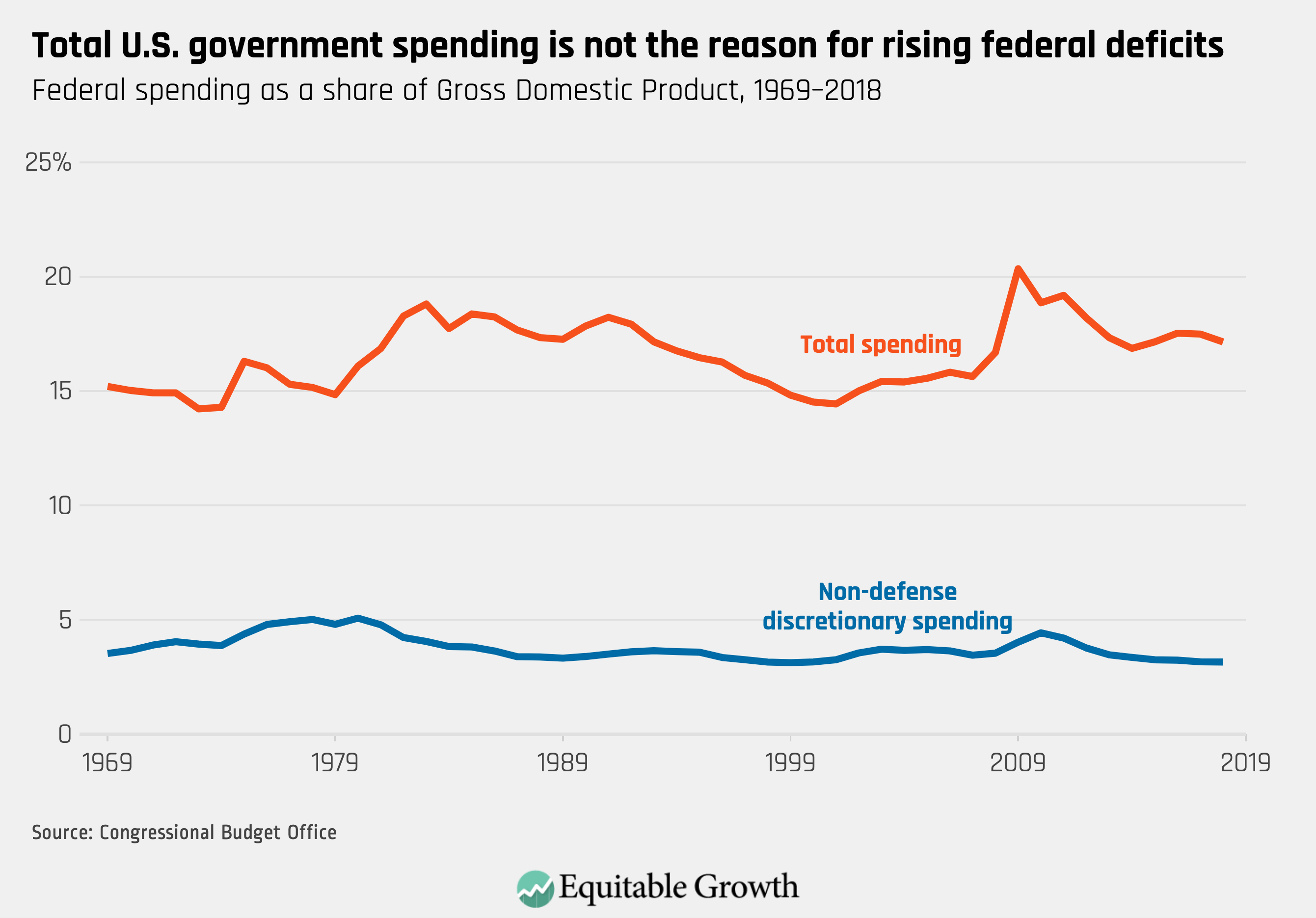

Examining the composition of federal spending and the composition of federal revenues relative to GDP can provide a high-level perspective on fiscal policy over the past 50 years. The data clearly reject the narrative that increased government spending is the primary reason for rising government deficits in recent years. Total spending, at about 20 percent of GDP in 2018, is close to its 50-year average. (See Figure 2.)

Figure 2

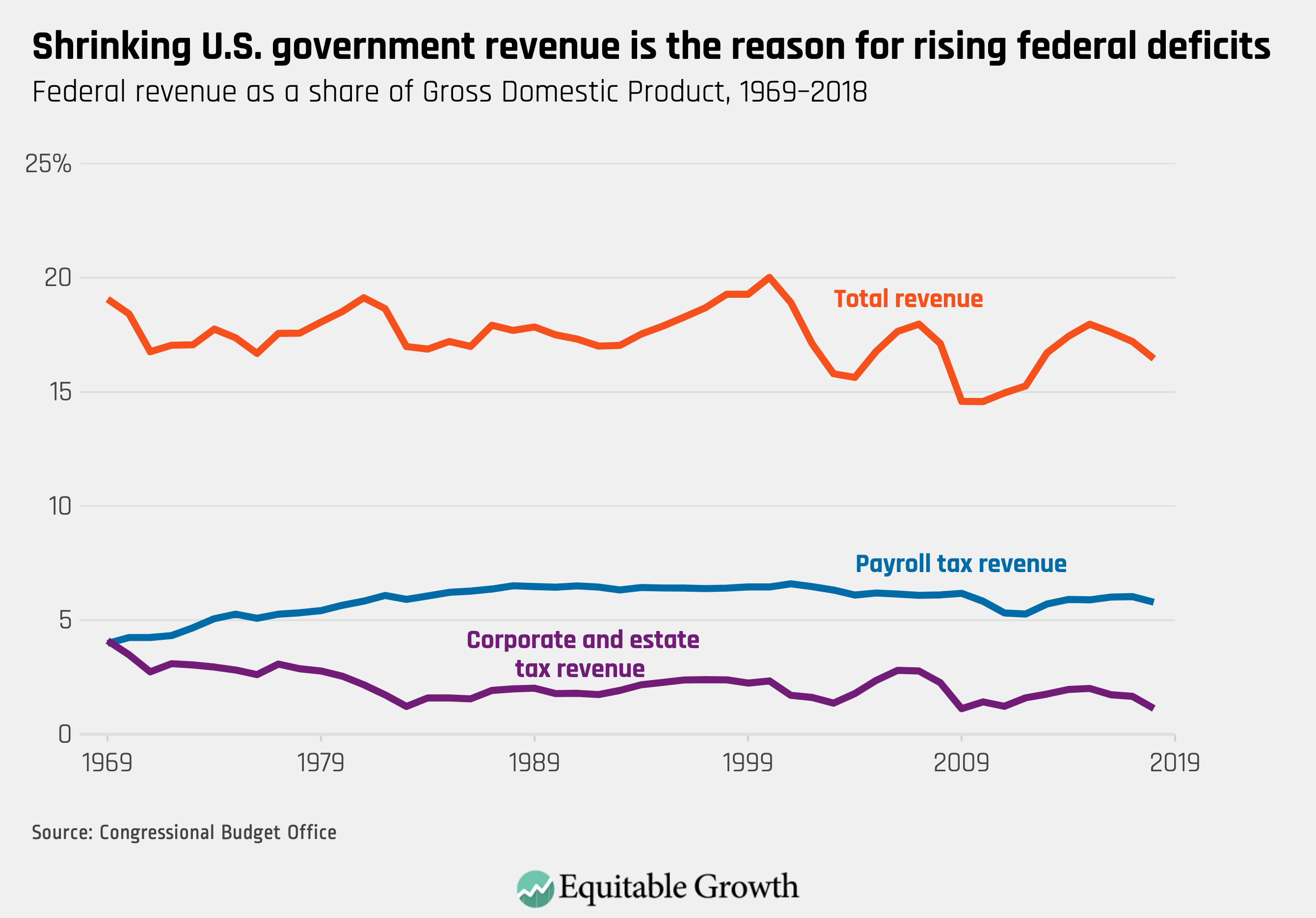

In contrast, total federal revenue relative to GDP is well below its 50-year average. (See Figure 3.)

Figure 3

A closer look at the composition of spending in Figure 2 cuts further against the narrative about rising government spending. The component of spending associated with direct government intervention in the real economy—nondefense discretionary spending—has fallen as a share of GDP in recent decades. The fastest growing categories of outlays are for programs such as Social Security, Medicare, and Medicaid, all of which are government programs generally financed by payroll taxes on the same group of low- and moderate-wage earners who also are the beneficiaries of these programs. The increase in payroll taxes used to fund these programs is evident in Figure 3. Thus, another crucial takeaway from this high-level perspective is that the overall decline in total revenues relative to GDP is because corporate, estate, gift, and income taxes have fallen even more than payroll taxes have increased.

Most analysis of fiscal policy focuses on the economic effect of deficits, without regard for why the deficits were created. The trends in the composition of spending and revenue shown above are suggestive that all deficits are not created equal. A deficit created by increased nondefense discretionary spending focused on investment in human capital, scientific research, or infrastructure has positive effects on aggregate demand and boosts productivity. Such policies have the potential to reverse the downward pressure on r*.

A deficit generated by reducing taxes on capital incomes, in contrast, has only short-run effects on aggregate demand, mostly through increased asset prices. Indeed, the effect of such fiscal policies is to reinforce a low-r* equilibrium because the after-tax return from owning stock is higher, and thus standard asset-valuation models tell us the stock should be worth more. Yet experience with those sorts of policies over the past two decades shows they do not lead to the sorts of investments that will make the U.S. economy grow and help alleviate the downward pressure on r*.9

The recent history of fiscal and monetary policies suggests that bad fiscal policy and constrained monetary policy have increasingly reinforced each other in recent decades, contributing to a slowdown in overall U.S. economic growth alongside rising income and wealth inequality and financial instability. Fiscal policymakers have abdicated their responsibility to make the investments in people, technology, and infrastructure that private investors cannot and will not make.

The good news is that a continued slowdown in economic growth and lower r* is not inevitable. Understanding how to reverse the decline in r* just involves a deeper understanding of the proper role of government in today’s economy.

Download FileGood U.S monetary policy can’t fix bad U.S. fiscal policy

Policies for the next Congress and administration

Bad fiscal policy has increasingly constrained monetary policy, and thus the first set of policies to embrace involve rethinking government intervention more broadly. On the spending side, the federal government needs to step up and identify areas where more investment is warranted in human capital, science and technology, and infrastructure. Federal investment in these areas will not be displacing private investments because those investments are simply not happening now. These sorts of investments will increase productivity growth, providing a direct offset to the otherwise-declining r*.

Increasing government investment may involve deficit spending in the short run, thus the second policy recommendation is to transform the way policymakers and the public think about spending and taxes. When a private citizen makes an investment, the payoff is in the form of profits, dividends, or interest. When government makes an investment, the fiscal payoff is in the form of higher taxes on the additional income that is generated. Most of the policy discussion about taxes involves the negative consequences of taxing some positive outcomes, but policymakers need to remember that those positive outcomes are, sometimes in large part, the payoff on public investment. Our tax system is increasingly allowing those who have benefitted the most from public investments in science and technology to pay less in taxes.

Although better fiscal policy is the key to better monetary policy, there are some monetary policy principles the Fed can and should embrace if economic conditions deteriorate. Economic shocks generally involve both financial effects and real effects in the economy, with the wealthy experiencing declines in their net worth but the less wealthy experiencing job losses. In the past, the Fed has focused on propping up the financial system—for example, bailing out mortgage lenders but not mortgage borrowers. The Fed needs to expand their policy purview if the fiscal authorities won’t act in the interests of all the people, and make sure the next round of Quantitative Easing—Fed speak for the central bank’s purchase of financial securities in the marketplace to boost liquidity in the economy—or other extraordinary monetary policy actions do not simply rescue those who benefitted from the mistakes that led to problems in the first place.

—John Sabelhaus is a visiting scholar at the Washington Center for Equitable Growth. Previously, from 2011 to mid-2019, he was assistant director in the Division of Research and Statistics at the Board of Governors of the Federal Reserve System, and prior to that, his roles at the Federal Reserve Board included oversight of the Microeconomic Surveys and Household and Business Spending sections, including primary responsibility for the Survey of Consumer Finances.

End Notes

1. Jerome H. Powell, “Montary Policy in a Changing Economy,” speech given at Changing Market Structure and Implications for Monetary Policy Symposium, August 24, 2018, available at https://www.federalreserve.gov/newsevents/speech/powell20180824a.htm.

2. In addition to leading the research on the topic, Williams has been very outspoken in public about declining r*. For example, in May 2019, he gave a speech titled “When the Facts Change…” which lays out the case for why r* has fallen and what that implies for Fed policy. See John C. Williams “When the Facts Change…,” speech given at High-Level Conference on the International Monetary System, May 14, 2019, available at https://www.newyorkfed.org/newsevents/speeches/2019/wil190514.

3. In general, the argument for raising interest rates when the economy comes out of a recession is based on preventing higher inflation down the road, an approach often characterized as “hawkish” and usually associated with more conservative political philosophies. The lack of price inflation in recent decades has dampened those arguments, and thus very few observers are willing to argue that the Fed should be targeting a higher r*.

4. The empirical literature is well captured in a paper by Kathryn Holston, Thomas Laubach, and John C. Williams, “Measuring the natural rate of interest: International trends and determinants,” Journal of International Economics, (108): S59–S75. A good example of the theory that can explain declining r* is in a paper by Gauti B. Eggertsson, Neil M. Mehrotra, and Jacob A. Robbins, “A Model of Secular Stagnation: Theory and Quantitative Evaluation.” Working Paper 23093 (National Bureau of Economic Research, 2017).

5. One approach to avoiding the ZLB in a low r* environment is to increase the nominal inflation target (π*). See the recent paper by Philippe Andrade and others, “The Optimal Inflation Target and the Natural Rate of Interest.” Papers on Economic Activity (The Brookings Institution, 2019).

6. The formulas relating the present value of a share of corporate stock to expected dividends, the risk-free interest rate, and the risk premium are well-described in the Wikipedia entry on the “Dividend discount model,” available at https://en.wikipedia.org/wiki/Dividend_discount_model (last accessed October 30, 2019). A very useful site with data on stock value fundamentals is Robert Shiller’s repository built around his book, Irrational Exuberance, “Online Data Robert Shiller,” available at http://www.econ.yale.edu/~shiller/data.htm (last accessed October 30, 2019).

7. Although much is made of declining labor income shares in recent decades, the offset has not been reflected in increasing corporate profit shares, which, in principle, is the key input into stock price valuation models. Rather, the offset to declining measured labor income seems to be mostly in noncorporate business income, including returns to labor at the very top of the income and wealth distributions. See Matthew Smith and others, “Capitalists in the 21st Century.” Working Paper 25442 (National Bureau of Economic Research, 2019). On the other hand, the measured profit share of GDP may be biased over time, suggesting that decreased competition and rising markups may be at least in part the source of an increasing Buffet Ratio. See, for example, Simcha Barkai, “Declining Labor and Capital Shares” (London Business School, 2017).

8. The asymmetric relationship between asset values and aggregate demand could be due to pure wealth effects or the sorts of “financial accelerator” principles advanced by researchers such as Ben Bernanke and Mark Gertler, as described in the Wikipedia entry, “Financial accelerator,” available at https://en.wikipedia.org/wiki/Financial_accelerator (last accessed October 30, 2019). Corporate equities are only one of various types of assets owned by households where prices matter, and indeed, the boom and bust in house prices generally gets more attention than stock prices in discussions about the post-2000 period. It is important to note that house prices are subject to the same sorts of valuation principles as stocks, with the rental value of a house serving as the counterpart to the flow of future profits in determining what a house is worth. Indeed, slowing economic growth and a declining r* would have likely been more evident sooner had it not been for the boom and bust in housing.

9. The 2017 Tax Cuts and Jobs Act reduction in corporate tax rates was just the most recent example of indefensible tax base erosion or tax rate reductions affecting capital incomes. Beginning in 1997 with the Taxpayer Relief Act, Congress has acted several times to reduce effective taxes on various forms of capital incomes, repeatedly justifying the cuts based on promises of future macroeconomic benefits that never materialize. The history of tax law changes in recent decades is well-described by the Tax Policy Center, “Laws and Proposals,” available at https://www.taxpolicycenter.org/laws-proposals (last accessed October 30, 2019).