Why Americans need to know more about the Federal Reserve

What is the most important policy decision about the U.S. economy this week?

Arguably, it won’t be made in Congress or by the Trump administration. It’s the vote at the Federal Reserve tomorrow.

Tucked away quietly near the Lincoln Memorial, three women and seven men on the Federal Open Market Committee will decide whether to change interest rates. Chances are they will not, leaving the federal funds rate between 1.5 percent and 1.75 percent—a decision that should be good for people and businesses across the country. Supporting the economic expansion could lead to more jobs, higher wages, and broader economic well-being. The connection between this vote by a small group of unelected officials and workers’ paychecks may be surprising and even disconcerting.

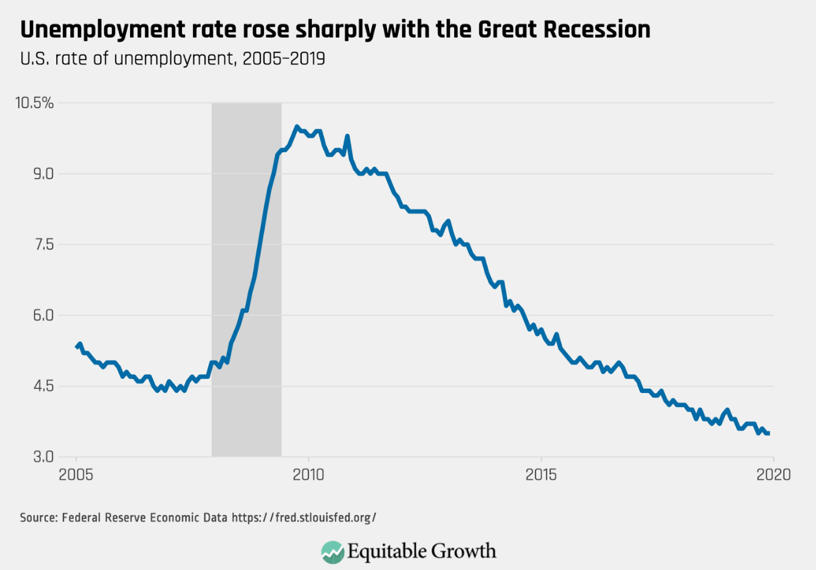

To set the stage for why tomorrow’s decision at the Federal Reserve is important for you, let’s start with some facts. Output, income, and jobs overall have increased for 10 years since the end of the Great Recession in mid-2009. That milestone is not as good as it sounds. The recession was very severe—with the unemployment rate reaching 10 percent in 2009. (See Figure 1.)

Figure 1

Furthermore, the recovery was slow and painful. Not until 2015 did the national unemployment rate return to its level at the start of the recession in 2007. More than 8 years to recover was extraordinarily long and destructive. The Federal Reserve does not deserve all the blame, but it did contribute to the policies’ failures. Most of you know the damage personally, even if you had not thought much about this source.

If in the Great Recession, you, a family member, or a friend lost their job, home, or business, I don’t need to tell you how damaging the recession and slow recovery were. Research backs you up. Losing a job creates immense strain on workers and their families at the time and has negative effects for years thereafter. Even if you were spared such losses, the widespread hit to the economy likely had negative effects for you too. Average raises have been meager, wealth remains below its pre-recession level for many households, and, with less financial support from their families, students often took out more college loans.

Now, let’s talk about policy. The Federal Reserve did act swiftly during the Great Recession, pushing the federal funds rate to zero. It acted as lender of last resort to keep financial markets going. It created new tools to support the economy. One can make the case that since the recession, it has done more than any other policymakers. One can also make the case that it missed the signs of the coming financial crisis in the early to mid-2000s and that it used the political capital it had to save Wall Street. Everyone in the country needs banks and financial institutions. Most Americans need jobs too. Here, the Federal Reserve fell short. It did not react with the same commitment to Main Street as Wall Street.

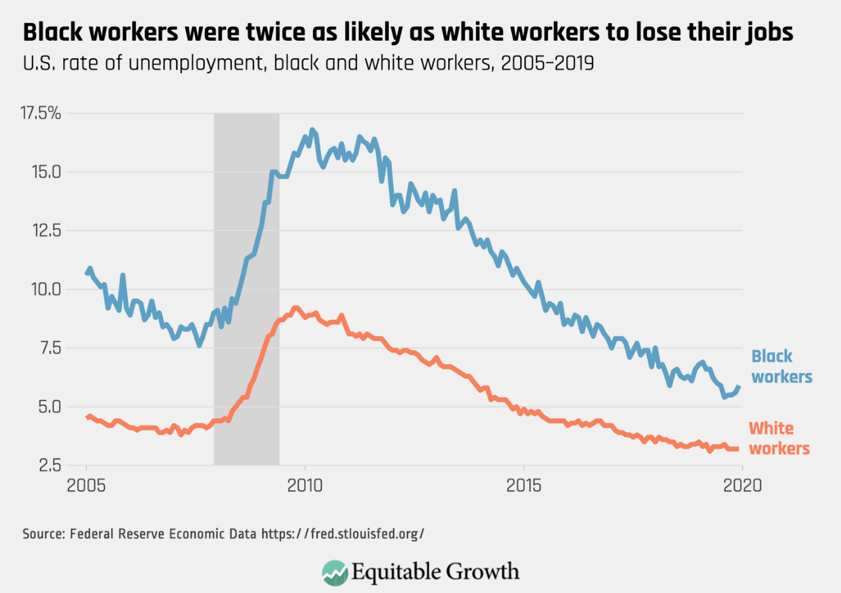

The harm from policymakers not doing everything they could did not affect everyone in the same way. Experiences of Americans, on average, mask the greater distress among some of their fellow citizens. Many groups of people and specific communities were hit harder in the recession and were slower to recover. One glaring example is among many people of color. The unemployment rate among black workers peaked at almost 17 percent, nearly twice the rate of white workers. (See Figure 2.)

Figure 2

Moreover, these disparate outcomes have existed for decades, in good times and bad.

The Federal Reserve has had a dual mandate from Congress since 1977 to pursue stable prices and maximum employment. Its mandate applies to the entire country. But policymakers know—mainly due to the efforts by community groups—that some Americans are less likely to have a job when they want a job. Black and Hispanic workers are among those people who often are not fully employed. Here again, the Federal Reserve could do better. It was not until September 2010 that “maximum employment” was in a statement after its vote. That mention came three decades after Congress set that mandate.

In contrast, every statement mentions inflation. For years, in its policy meetings, there was hardly any discussion about worse outcomes among some groups of workers. Narayana Kocherlakota, a former Federal Reserve official, called attention to this failure. More discussion of the unequal effects of monetary policy has occurred in recent years—both on the committee and in the economics profession. It is hard to point to any actions at the Federal Reserve.

Fast forward to today. The national unemployment rate was 3.5 percent in December 2019. For black workers, it was down to about 6 percent. By the unemployment rate alone, the labor market looks its best in 50 years. Of course, the economy today is not the economy of the 1960s. Too many workers remain on the sidelines. Even so, with inflation stable and low, the Federal Reserve can allow the economy to push forward. The unemployment rate is less today than it thinks it will be over the longer run.

The typical forecast among Federal Reserve officials is for it to move gradually back to 4.1 percent. That’s their best guess; they could be wrong. They have consistently underestimated how low unemployment can go over this expansion. They could be wrong now. No one has a crystal ball, but they should think harder about their systematic mistakes.

I will close on a positive note. They are thinking harder. The Federal Reserve is reviewing its approach to monetary policy. It began the efforts last year. As part of the introspection, it held Fed Listens events across the country. It brought in people from community groups, businesses, colleges, and academia. Federal Reserve officials are still in discussions. They plan to release the findings in June. Tomorrow at the press conference, we might get some glimpses from Fed Chair Jerome Powell as to where they are currently.

The Federal Reserve has a history of halfheartedly pursuing maximum employment. Even so, it is thinking now and will tell us where that thinking may lead. This is progress. Most importantly for all of us, it believes it may need to change how it does monetary policy. It can do better.