How corporate governance strategies hurt worker power in the United States

Researchers studying the decades-long rise in earnings inequality and wage stagnation in the United States point to a number of reasons why the country’s income divide grew over the past 40 years or so. Declining union membership, racist labor policies, and changes in the industrial composition of the United States, for example, all have been found to be important drivers of economic disparities.

In addition to these trends and intentional policy choices that make workers worse-off, social scientists are studying how corporate governance affects workers’ wages, employment, and ability to bargain collectively. These researchers are also looking into how the rise of shareholder value as the main objective of U.S. corporations relates to income inequality, productivity, and labor’s share of economic growth in the United States. This research offers evidence that the rise in shareholder power reinforces the impacts of the decline of the U.S. labor movement—a decline that has had broad spillover effects across the country’s economy and has limited workers’ ability to share in the gains of the economic value they create.

In this issue brief, we examine a series of important changes to corporate governance in the United States between the 1970s and 1990s, the simultaneous decline in the country’s job quality and worker power, and the relationship between the two trends. Specifically, we discuss some of the academic evidence on the relationship between the rise of shareholder primacy, new management practices, and workers’ labor market outcomes. We then turn to policy recommendations that have the potential to strengthen labor vis-à-vis shareholders—a set of proposals that would rebalance bargaining power in the labor force, boosting productivity and promoting broadly shared economic growth.

How maximizing shareholder value became the main objective of U.S. corporate governance

“Shareholder primacy” is an economic and legal theory that proposes that maximizing wealth for shareholders should be the main, if not the sole, objective of publicly traded companies. This framework became the dominant model driving corporate governance in the United States beginning around four decades ago, gaining prominence as a number of economic, social, and academic shifts allowed it to displace the “managerialist” philosophy that guided public companies’ decision-making processes during the mid-20th century.

As legal scholar Lynn Stout explains, for most of the post-World War II era, large U.S. corporations generally thought of themselves as serving the interest of a wide variety of stakeholders—customers, suppliers, workers, and local communities. Yet between the 1970s and the 1990s, maximizing shareholder value came to trump every other corporate interest and priority.

A number of economic changes led to the growth of shareholder primacy. In the 1970s, for example, corporations began to look for new business models after facing several economic crises, alongside an increase in international competition in industries such as car manufacturing and consumer electronics, and poor performance as companies grew too big. At the same time, William Lazonick at the University of Massachusetts and Mary O’Sullivan at the University of Geneva propose, there was a shift in the distribution of stockholding away from households and toward large institutional investors. This occurred as the U.S. financial sector loosened restrictions on the extent to which life insurance companies and pension funds could own corporate equities. Indeed, the share of U.S. corporate equities held by institutions soared from 10 percent in the early 1950s to more than 60 percent in the early 2000s.

As shareholders in general—and institutional investors in particular—came to have greater influence over business operations, U.S. corporations underwent a series of changes. Executives and managers looked to maximize shareholder value by increasingly engaging in mergers, downsizing their workforces, deploying de-unionization tactics, and increasingly using corporate funds for shareholder payments in the form of stock buybacks and corporate dividends. As the interests of shareholders and executives became more tightly aligned through equity-based and other incentive pay schemes, the compensation of executives skyrocketed.

U.S. job quality and workers’ bargaining power simultaneously declines

Meanwhile, economic sociologists Neil Fligstein and Take-Jin Shin at the University of California, Berkeley write, the advent of shareholder primacy meant that publicly traded firms increasingly perceived workers as input costs rather than as contributors to be included or considered in the corporate decision-making process.

As such, overall job quality in the United States started to decline in the late 1970s. Real wages for nonsupervisory workers started to fail to keep up with productivity gains. Union membership shrunk from more than 20 percent in 1983 to 10 percent in 2021. A variety of factors, including international trade, ineffective labor laws, increasingly hostile labor-management relations, and deindustrialization and the decline of manufacturing, reinforced one another and exacerbated the decline of institutionalized worker bargaining power in the final decades of the 20th century.

Playing into this changing economic landscape, according to David Weil at Brandeis University, was a fundamental change in the way firms organized themselves and structured their workforces. This so-called fissuring of the workforce describes how big firms stopped directly employing workers that perform roles outside the core competency of their businesses. Janitorial services, for example, were largely transferred to a smaller network of firms through arrangements such as subcontracting and franchising, allowing large corporations to avoid the costs and obligations of traditional employment relationships with their janitorial staff. For workers, this shift generally resulted in lower compensation, less access to employer-provided benefits, fewer opportunities for career advancement, and greater vulnerability to labor law violations.

Similarly, Arne Kalleberg at the University of North Carolina at Chapel Hill and David Howell at the New School University argue that the rise of the financial sector and the prevalence of shareholder value strategies in the United States contributed to the erosion of labor market institutions, including the fall in the real value of the minimum wage, weakening union bargaining power, and the decline in the protective effect of laws and regulations that govern employment relationships.

Christopher Kollmeyer at the University of Aberdeen and John Peters at Laurentian University likewise find evidence that between the early 1970s and the early 2010s, U.S. corporate governance strategies that shrunk labor costs and redirected resources away from productive investment contributed to the decline in union density in a number of high-income countries, including the United States.

To be sure, firms’ growing concern with maximizing shareholder value was not the only important change in U.S. business strategies between the 1970s and 1990s, let alone in the U.S. economy writ large. Yet there is evidence that the advent of shareholder value as the most important concern for corporate governance had important effects on wage growth, income inequality, and workers’ ability to bargain for better workplace conditions in the United States.

Empirical evidence demonstrates that shareholder primacy lowers workers’ wages and worsens employment outcomes

While several scholars have long proposed that the rise of shareholder power affects workers, recent empirical studies contribute to the academic understanding of the size and importance of shareholder power’s effect, and the precise mechanisms through which shareholder primacy influences labor market outcomes.

For example, an analysis by José Azar of the University of Navarra, Yue Qiu of Temple University, and Aaron Sojourner of the Upjohn Institute finds that greater common ownership in a labor market—or the concentration of investment positions of public companies in the hands of a few large institutional shareholders—is associated with both lower wages and a lower employment-to-population ratio. With about 1 in 3 U.S. private-sector workers employed in publicly traded firms, the concentration of shareholders across firms through common ownership by institutional investors could play a significant role in the overall structure of the labor market.

Likewise, in a new working paper, Antonio Falato of the Federal Reserve Board, Hyunseob Kim at the Federal Reserve Bank of Chicago, and Till von Wachter at the University of California, Los Angeles examine the relationship between shareholder power and workers’ earnings and employment. The authors find that as establishments experience an increase in ownership by institutional shareholders, they also experience a decline in employment and payroll costs. This finding holds both at the establishment and the industry level.

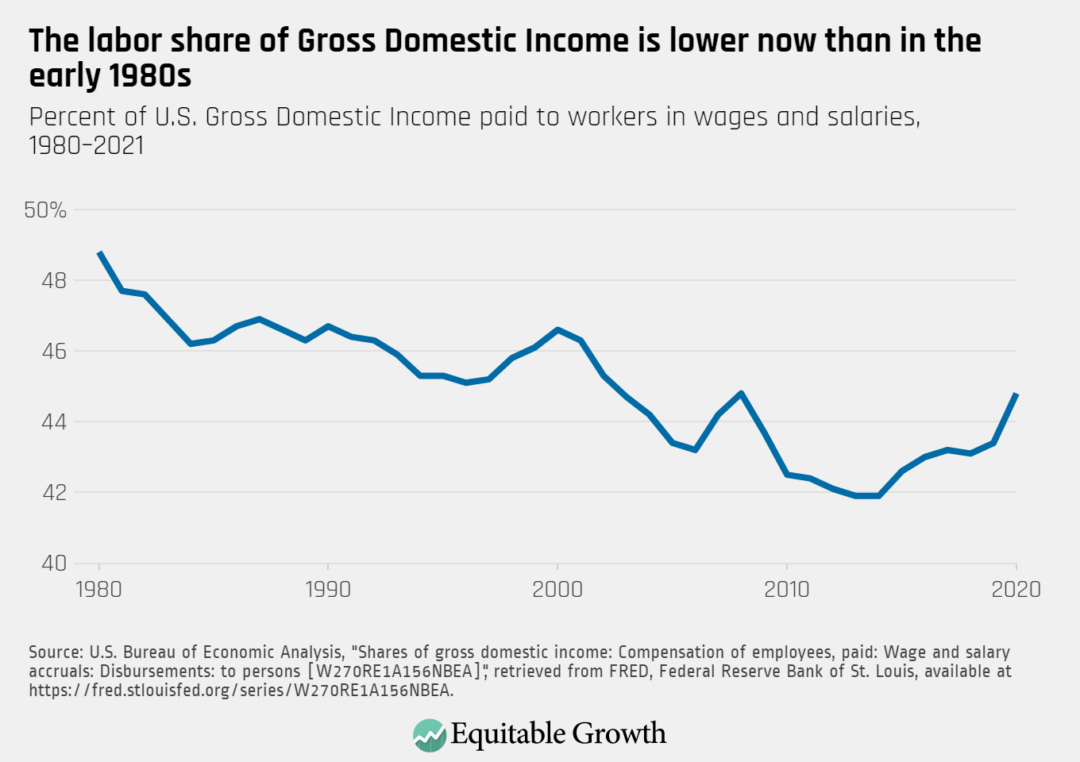

Moreover, Falato, Kim, and Von Wachter find that an increase in ownership by institutional shareholders explains about a quarter of the decline in the ratio of total wages and salaries to Gross Domestic Income—a metric that has seen an important drop in the past four decades— between 1980 and 2014. (See Figure 1).

Figure 1

Lenore Palladino at Smith College also studies the relationship between profits, shareholder payments, and wage growth, finding that as shareholder payments as a percent of companies’ profits grew, the share of profits that went to workers’ wages declined. In addition, through firm-level empirical analysis and accounting for macroeconomic factors and a number of firm-specific characteristics, Palladino shows that as shareholder payments as a portion of operating expenses increased between 1984 and 2017, wages paid to workers fell.

Evidence also shows that as shareholder primacy and the financialization of the U.S. economy more broadly influence workers’ outcomes, these trends also contribute to widening racial and gender inequality in the U.S. labor market. Indeed, a team of researchers finds that between the 1980s and the 2010s, the pay for workers in managerial occupations did not only outpace the pay of workers in other types of jobs, but White and Latino men also have benefited disproportionately from this financial and managerial wage premium.

Business practices that lead from shareholder primacy to inefficient and inequitable workplace outcomes

What mechanisms underlie the effect of shareholder primacy on workplace outcomes? One body of research looks at the role of managers and management practices. Indeed, it appears as though the rise of the shareholder primacy ethos, as taught in business schools, has reduced any tendency toward rent-sharing with workers. Following the guidance of economist Milton Friedman, who proclaimed “the social responsibility of businesses is to increase profits,” business school philosophy tends to view workers as costs rather than stakeholders.

For example, Daron Acemoglu of the Massachusetts Institute of Technology, Alex He of the University of Maryland, and Daniel le Maire of the University of Copenhagen investigate how the rising number of managers with business degrees affects wages within workplaces in both the United States and Denmark—a research strategy that isolates policy and institutional landscapes across two different countries. The authors find that a greater proportion of managers with business degrees is associated with lower worker wages.

Acemoglu, He, and le Maire also are able to causally estimate this impact by looking at scenarios in which there is a retirement or death and a manager without a business degree is replaced by another person with a business degree. In the United States, the authors find that the appointment of a manager with a business degree results in a 6 percent decline in wages in the following 5 years. The authors estimate that these dynamics explain 15 percent of the slowdown in wage growth and 20 percent of the decline in the labor share in the United States since 1980.

What’s more, the increasing preponderance of managers with business degrees is not associated with higher firm output or productivity.

Policy proposals to return bargaining power to workers and foster broadly shared economic growth

Most evidence shows that efforts to maximize shareholder value do not just hurt workers’ labor market outcomes and lead to an increase in economic inequality, but also do little to increase firm profitability. Further, research suggests the shift toward shareholder primacy is a drag on economic growth. In Equitable Growth-funded research, for example, Florian Ederer of Yale University and Bruno Pellegrino of the University of Maryland find that common ownership—an ownership arrangement where a few institutional investors hold investment positions in a number of competing firms—reduces competition between firms, similar to monopolization, and decreases overall economic welfare across the U.S. economy.

The promise of broadly shared growth in a market-based economy can only be realized in a legal, economic, and institutional context that supports worker power to offset the inefficient tendency toward inequality and wealth-hoarding under financial capitalism. In the current environment of shareholder primacy, research shows that these tendencies result in declining wages, deadweight loss, and a distorted distribution of economic value.

Measures to reinforce countervailing worker power include policies that will restore the strength and presence of unions in the United States. The decline of unions is associated with a variety of deleterious impacts for the U.S. economy. Reforming labor law to make worker organizing easier—such as provisions in the Protecting the Right to Organize, or PRO, Act that protect the right to strike, ensure union elections are fair, and make it harder for companies to misclassify their workers as independent contractors—would help restore union density.

Another effective measure is to increase worker and union representation on corporate boards. Research by Simon Jäger of the Massachusetts Institute of Technology, Benjamin Schoefer of the University of California, Berkeley, and Jörg Heining of the German Institute for Employment Research finds that so-called co-determination—or when workers have secured spots on company boards—does not diminish firm performance but does, in fact, diminish the likelihood that a firm will outsource work, without impacting wage levels.

Sectoral bargaining, where multiemployer groups bargain with unions for an entire employment sector in a specific location, and wage boards that include union representation would also provide a much-needed counterbalance to corporate strategies that push managers to cut wages and exploit workers.

Another piece of the puzzle for restoring balance in the economy and ensuring robust, broadly shared growth is reforms that diminish the exploitative power of finance. This would set the U.S. economy on a path toward a system of so-called stakeholder capitalism, in which corporate strategy is reoriented toward the interests of all relevant stakeholders, including workers, suppliers, and local communities.

To accomplish these goals, limiting stock buybacks and establishing board fiduciary duty to stakeholders would help reshape corporate governance away from shareholder primacy. This, in turn, may help ensure that workers can share in the value they create, as well as offset the potential for negative externalities, such as environmental costs.

These proposals would go a long way to fostering equitable economic growth in the United States by boosting worker power and shifting corporate strategies away from policies that center shareholder primacy.