Larry Summers by J. Scott Applewhite, Associated Press

After the worst of the Great Recession seemed to have passed in early 2010, policymakers, concerned with the run-up in public debt caused by the recession and policies intended to fight it, turned to fiscal consolidation, better known as austerity. Their thinking was that the response to the financial crises and the resulting recession had done what it could, and that governments across the globe should pull back from boosting growth through fiscal policy.

More than five years later, however, that turn to austerity so early during the recovery seems to have been premature. In fact, some economists are starting to wonder if we should have ever stopped the fiscal stimulus.

One of the arguments against continued fiscal stimulus, or any stimulus at all, was Say’s Law. Named after the early economist Jean-Baptiste Say, the “law” states that supply creates its own demand. According to this thinking, the government doesn’t need to be concerned about boosting demand during recessions because the system will equilibrate on its own. But this doesn’t hold up in the short run. In fact, the inverse of Say’s Law seems to be the case, at least in our current situation.

Austerity, according to a new paper by former U.S. Treasury Secretary and Harvard University economist Larry Summers, and INSEAD economist Antonio Fatas, seems to have actually hurt potential output, measured as our estimates of future gross domestic product. In other words, the amount of demand in the present very much has an effect on the economy’s future potential. Not putting the current resources of the economy to their full use can result in a poorer future.

This insight is important when thinking about the potential problem of secular stagnation. Early in the Great Recession, many economists, including Paul Krugman, thought that problem for macroeconomics was hastening the arrival of the recovery. A return to normal economic conditions would come around, but fiscal and monetary policy could get the economy there quicker. But now, after rethinking the case of the Japanese economy, Krugman is considering whether it’s possible for an economy to be in a state of constant demand deficiency.

If the natural rate of interest is permanently below zero, then policy has to be permanently stimulative. Whether this means the central bank pushes inflation permanently higher or policymakers run fiscal deficits in perpetuity, policymakers can’t just wait for the recovery to show up. To paraphrase Larry Summers, there will be no deus ex machina ending. Recovery needs to be brought about proactively.

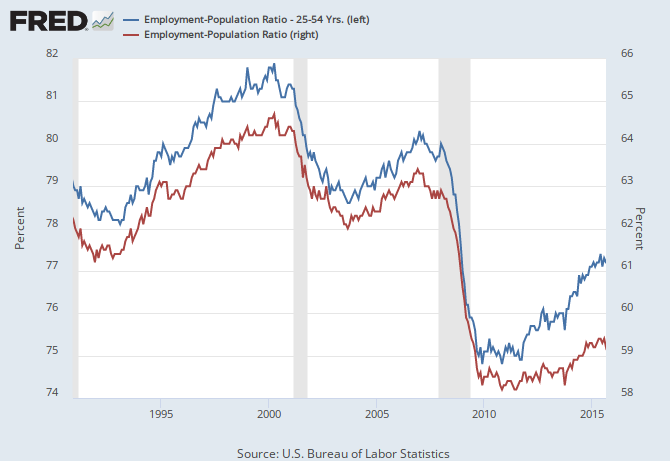

And the costs of inaction would be tremendous. Even if the demand deficit were a temporary phenomenon, the costs of not accelerating recovery would still be large. But if it is a permanent problem, then the lack of demand would have larger and far-reaching costs in terms of supply as well. If workers aren’t employed in the short run, maybe they won’t be employed in the future. If high unemployment reduces the earnings of young workers early in their careers, that cost will project forward as well. If companies hold back on investment due to weak growth, that’ll impact future potential supply as well. A lack of urgency about the present could do major damage to the future.

{kind=link}