…both from unemployment and lower future wages, will amount to about 6 percent of the agreement’s benefits…. The percentage gains for labor income from the TPP will be slightly greater than the gains to capital income. Households in all quintiles will benefit by similar percentages…. The agreement will confer net benefits to households at all levels of income and will certainly not worsen income inequality…

When it comes to tackling the United States’ large and growing achievement gap between high- and low-income children, today’s education policy entrepreneurs have increasingly adopted an accountability-and-evaluation mindset. Well-known policies including No Child Left Behind, Common Core standards, Race to the Top, and charter schools all stem from the conventional wisdom that we can’t just “throw money at the problem.”

But in the case of our national education policy, does this conventional wisdom hold true? Maybe not. New research by Julien Lafortune and Jesse Rothstein of the University of California, Berkeley, and Diane Whitmore Schanzenbach of Northwestern University finds that an increase in relative funding for low-income school districts actually has a profound effect on the achievement of students in those districts.

The researchers look at the impact of “adequacy”-based finance reforms, enacted by 27 states over the past 20 years. These reforms sought to ensure that low-income school districts had enough money to provide their students with a high-quality education, even if that meant that their costs exceeded that of high-income school districts—a focus on “adequacy” rather than “equity.” Within states that implemented the reforms, the funding gap between low-income and high-income districts was eradicated without cutting funds for wealthier school districts. Rather, across-the-board spending increases meant that by 2011, these states spent an average of $1,150 more per pupil in low-income districts compared to high-income districts. States that did not enact the reforms, however, maintained an $800 gap in favor of wealthier schools.

But did these increased funds for low-income districts reduce educational inequality? By comparing outcomes in the states that implemented these school finance reforms and those that did not, LaFortune, Rothstein, and Schanzenbach find that the reforms had a considerable impact on the achievement gap between high- and low-income school districts. They found that increasing funding per pupil by about $1,000 raises test scores by 0.16 standard deviations—roughly twice the impact as investing the same amount in reduced class sizes (according to data from Project STAR, a highly acclaimed study of Tennessee schools in the 1980s).

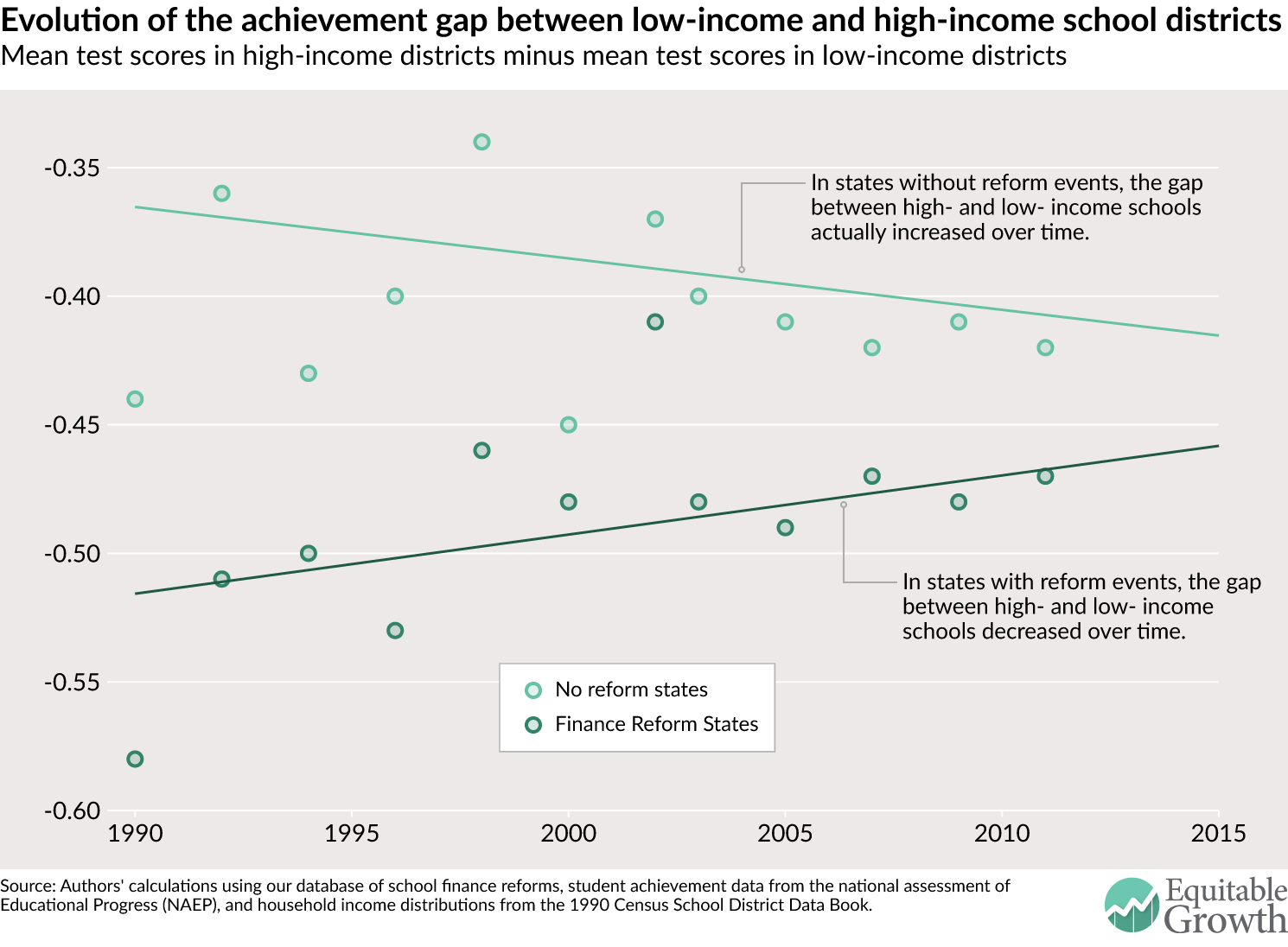

As seen in the figure below from an issue brief summarizing the authors’ findings, states that did not enact reforms saw the achievement gap between low- and high-income school districts widen substantially between 1990 and 2011, partially due to rising overall inequality over the same period.

Still, no single policy is a panacea. While school finance reforms made an impressive dent in the achievement gap between low- and high- income districts, the authors find that the reforms had no significant impact on the gap between individual rich and poor students. That’s because while poor students (and minority students as well) are slightly more likely to attend school in a low-income district, there are still many low-income and minority students educated in high-income districts. As a result, these reforms might not have had a sizable effect on the relative resources available to most minority or low-income students.

That aside, this research calls attention to the improvements in reducing educational disparities within the states that implemented school finance reforms, and points to a potential path forward on a national scale. As the authors note, taken together, state “school finance reforms are perhaps the largest national effort we have made to increase equality of educational opportunity since the school desegregation movement.”

While we still need to make progress as far as disparities between individual students, this research makes a compelling and evidence-based case for school finance reform on a federal level. Rather than “throwing money at the problem,” no-strings-attached funds may actually make a difference for the country’s most disadvantaged school districts.

Policymakers concerned with entrepreneurship at both the local and national level have long favored what economist Robert Litan dubbed a ‘shots on goal’ approach: Try to encourage as many startups as possible. Most of those companies will fail. Of the survivors, most will never grow into major economic engines. But statistically, a few will turn out to be the next Amazon, with huge rewards for their local economies…. Scott Stern and Jorge Guzman call that… into question. Startups as a whole may be declining, they find, but the kind of entrepreneurship that economists care the most about–fast-growing, innovative companies like Amazon–hasn’t shown the same downward trend… But all is not well…. The U.S. may have as many would-be Bezoses as ever, but it’s getting fewer Amazons…. ‘It’s a scaling problem,’ Stern said. ‘The machine that turned those kinds of companies into that kind of economic engine seems to be less robust today.’…

Ambitious startups share certain qualities. Their names, for example, tend to be shorter and are less likely to include the founder’s name. They tend to be set up as corporations… often incorporated in Delaware… often apply for patents early…. Stern and Guzman calculate what they call an Entrepreneurial Quality Index…. When it was founded, Amazon would have scored in the top 1 percent of all new companies on the index….

Stern and Guzman used business-registration data from 15 states to calculate both quality and success indexes for different metro areas. Some, like Silicon Valley, showed both high rates of entrepreneurship and successful growth. Others, like Miami, have seen a steep drop in the number of high-potential startups in recent years. Perhaps not coincidentally, cities with high rates of startup activity have also experienced faster economic growth over the past decade…

…we may well at present be seeing the first stirrings of an increase in the inflation rate…

Fed Governor Lael Brainard perches on the right, whispering:

…there are risks around this baseline forecast, the most prominent of which lie to the downside.

Yellen is caught in a tug of war between Fischer and Brainard. At stake is the Fed chair’s willingness to embrace a policy stance that accepts the risk that inflation will overshoot the U.S. central bank’s target. At the moment, Brainard has the upper hand in this battle. And she has a new weapon on her side: increasing concerns about the stability of inflation expectations….

Fischer’s not alone. In his group sit Federal Reserve Bank of San Francisco President John Williams, Kansas City Fed President Esther George, and Cleveland Fed President Loretta Mester. And Yellen is believed to be reasonably sympathetic to this camp. She’s repeatedly voiced her support of a Phillips curve view of the world—or the idea that, after accounting for the temporary impacts of a strong U.S. dollar and weak oil, inflation will rise as unemployment rates fall…. Indeed, a Phillips curve view is fairly common among monetary policymakers….

So, given the Phillips curve framework’s consistency among policymakers, why delay further rate hikes?… The challenge for further rate hikes is that recent financial instability has exposed the downside risks to the forecast… New York Fed President William Dudley, Philadelphia Fed President Patrick Harker, and Boston Fed President Eric Rosengren…. Financial instability certainly gives the Fed reason to stand still this week. And it gives reason for the Fed to continue to be cautious…

…even though economic forecasters disagree. When the next recession arrives, will fiscal and monetary policy be able to respond? If so, how? The Federal Reserve is holding short-term interest rates near zero and faces resistance, internally and externally, to reviving large-scale purchases of assets. The federal debt is larger, as a share of the economy, than at any time since the end of World War II and is projected to climb further. On March 21, the Hutchins Center on Fiscal and Monetary Policy will consider which fiscal and monetary policy tools will be available in the event of a recession—and which won’t—and how effective additional fiscal and monetary stimulus is likely to be, along with new ideas to make fiscal policy more effective…. David Wessel… Wendy Edelberg… Ben Spielberg… Phillip Swagel… Richard Clarida… Jon Faust… Louise Sheiner… Jared Bernstein

The achievement gap between rich and poor students in the United States is large—roughly twice as large as the gap between black and white students—and growing. On average, children from low-income families have lower test scores and rates of high school and college completion, and eventually lower earnings than their peers from higher income families. Addressing these disparities is key to breaking the cycle of poverty and inequality across generations.

Recent education policy discussions have started from the premise that one can’t just “throw money at the problem.” Instead, solutions to the achievement gap must come from accountability, school choice, or other reforms designed to obtain better outcomes using a fixed set of resources. But largely outside of the public eye, a number of states have made dramatic changes to their finance systems to redirect funding to low-income school districts. Taken together, these reforms are the largest anti-inequality education effort in this country since school desegregation. Are school finance reforms merely a waste of effort? Or does money really matter, and does funding reform have the ability to make a dent in the achievement gap?

Our recent paper, “School Finance Reform and the Distribution of Student Achievement,” explores these questions. We examine the impacts of so-called “adequacy”-based finance reforms, designed to ensure that low-income schools have adequate funding to achieve desired outcomes. These reforms began in 1990 in Kentucky, with the Kentucky Education Reform Act. Since then, 26 additional states have enacted their own reforms. We draw on rarely used student-level data from the National Assessment of Educational Progress, or NAEP, to identify the effects of these reforms on the relative achievement of students in high- and low-income school districts.

The importance of additional school resources for student achievement has long been debated, with many researchers arguing that school resources do not matter much in explaining differences in student achievement between schools, and therefore that money does not matter. But these studies have generally compared districts or states that spent more to those spending less, without the ability to control for the factors that determined the disparities in funding. As a result, the estimated effect of resources is confounded by other factors (such as student need) and may not identify the true causal effect of additional funding. By examining state-level reforms, we are able to identify the causal effects of funding through reform-induced changes in the resources available to districts. Importantly, these changes in funding are driven by shifts in state policy rather than unobserved local determinants that might confound the effect of funding. We are therefore able to identify the policy-relevant effect of funding: What is the impact of changes in state policies that send funding to low-income districts, often with few or no strings attached?

We show that school resources play a major role in student achievement, and that finance reforms can effect major reductions in inequality between high- and low-income school districts. Accordingly, while states that did not implement reforms have seen growing test score gaps between high- and low-income school districts over the last two decades, states that implemented reforms saw steady declines over the same period. The effect is large: Finance reforms raise achievement in the lowest-income school districts by about one-tenth of a standard deviation, closing about one-fifth of the gap between high- and low-income districts. There is no sign that the additional funds are wasted. On the contrary, our estimates indicate that additional funds distributed via finance reforms are more productive than funds targeted to class size reduction.

School finance reforms increase school spending in low-income districts

Traditionally, U.S. public schools have been funded through local property taxes. Because wealthy families tend to live in communities with larger tax bases and fewer needs, their children’s schools have typically spent much more per student than have schools in poor districts.

Beginning in the 1970s, many states reformed their school finance systems to address this inequality. Often reacting to mandates from courts that found local finance systems unconstitutional, states have moved away from funding based primarily on property taxes and have implemented state aid formulas that direct more money to low-income and low-tax-base school districts.

These reforms can be divided into two waves:

In the 1970s and the 1980s, state school finance reforms were focused on equity, or on reducing funding gaps between districts. These reforms often involved redistribution from high income or high tax base districts to low income or low tax base districts. They have been much studied, and some scholars have argued that they induced political dynamics that led to reduced funding across the board.

In 1989, the Kentucky Supreme Court ruled in Rose v. Council for Better Education that “each child, every child … must be provided with an equal opportunity to have an adequate education.” This set off a second wave of reforms, beginning in Kentucky and followed by 26 other states, focused on “adequacy” rather than on “equity.” The goal was to ensure an adequate level of funding in low-income school districts, regardless of whether that was more than, the same as, or less than funding levels in high-income districts. As a consequence, states facing adequacy standards were much less prone to achieve equality by reducing overall funding; instead, they were forced to raise absolute and relative funding in the poor districts. However, there has been little evidence available about their actual impacts. Our new paper helps to close that gap.

Average revenue per pupil in elementary and secondary schools in the United States amounts to roughly $13,000 a year. In 2011, low-income districts spent an average of 8 percent more per pupil than did high-income districts in states that have implemented reforms. This is a dramatic reversal from historical experience—as recently as 1990, low-income districts in these states averaged 9 percent less than high-income districts.

In order to estimate how much adequacy-based school finance reforms have contributed to this reduction, we use an “event study” design, which essentially looks at the result of three successive differences for each school finance reform. We compare outcomes in high-income and low-income districts (difference #1), in states where school finance reforms have been implemented and where reforms haven’t been implemented (difference #2), and before and after the reform (difference #3). This identification strategy allows us to disentangle the impact of school finance reforms from other contemporaneous changes in school funding and from other differences between states that did and did not implement finance reforms.

The following interactive provides a state-by-state look at how funding gaps between high- and low-income school districts evolved from 1990 to 2011. Specifically, it shows what low-income districts in each state received in funding per pupil relative to high-income districts over those two decades.

Separate panels show revenues received from the state government and total revenues. Low-income districts in Ohio, for example, received $1.41 in state aid for each dollar that high-income districts received in 1990. By 2011, state aid was more progressive: For every $1 of state aid for high-income districts, low-income districts received $1.94. The progressivity of state aid in Ohio offset local revenues, which in Ohio and elsewhere are quite regressive. Combining all sources, low-income districts received 75 percent as much funding as high-income districts in 1990, and 101 percent as much in 2011.

Choose a state:

Note: Low income districts are those with average household-income in the bottom 20% of all in the same state districts. High-income districts are those with average household-income in the top 20% of all districts in the same state. Hawaii was excluded as there is only one school district in Hawaii. "Progressive" school funding means that a state's low-income districts are receiving more funding per student than high-income districts. "Regressive" school funding means that a state's low-income districts are receiving less funding than the high-income districts.

Source: Authors' calculations using our database of school finance reforms, district level finance data from the National Center for Education Statistics' Common Core of Data school district files, the Census of Governments, demographics from the CCD school universe files, and household distributions from the 1990 Census.