This is a weekly post we publish on Fridays with links to articles that touch on economic inequality and growth. The first section is a round-up of what Equitable Growth has published this week and the second is work we’re highlighting from elsewhere. We won’t be the first to share these articles, but we hope by taking a look back at the whole week, we can put them in context.

Equitable Growth round-up

There’s been quite a bit of theorizing that higher levels of inequality may cause lower levels of economic mobility. Up until now, there hasn’t been much evidence of a causal relationship. But a new paper finds a connection between higher levels of income inequality and higher high school dropout rates.

The effectiveness of monetary and fiscal policy in responding to the Great Recession has been one of the great economic debates of the past few years. But those debates overlook federal credit programs, which may have had a significant impact in countering the recession.

Earlier this week, Equitable Growth hosted economists David Card and Alan Krueger to discuss the impact of their book “Myth and Measurement” on our understanding of the minimum wage. In the 20 years since the book was published, the economics profession has changed its tune when it comes to the minimum wage.

Speaking of challenging the conventional wisdom, a new paper by Julien Lafortune and Jesse Rothstein of the University of California, Berkeley and Diane Whitmore Schanzenbach of Northwestern University argues that school finance reforms can boost student achievement. Their brief for Equitable Growth dives into their results.

Bridget Ansel takes their results and argues that our current education policy debate could be improved by considering these findings. “Rather than ‘throwing money at the problem,’” she writes, “no-strings-attached funds may actually make a difference for the country’s most disadvantaged school districts.”

Links from around the web

If you listen to the hype about technology companies, you’ll probably hear the word “disruption” quite often. New tech companies, in this telling, will upend old established companies. But Noah Smith floats the possibility that technology could help facilitate market concentration. [bloomberg view]

Since the end of the Great Recession, wage growth and productivity growth have been quite weak in both the United States and the United Kingdom. Are wages low because of low productivity? Or is productivity low because of low wages? Ryan Avent says yes. [the economist]

As I mentioned above, Equitable Growth hosted David Card earlier this week—an economist who has made a number of important contributions to the field of labor economics. Peter J. Walker profiles this “challenger” of conventional wisdom. [imf]

The U.S. labor force participation rate, after years of declining in the wake of the Great Recession, has ticked up in recent months. Whether or not this trend will continue is uncertain, but what’s behind this movement? Ernie Tedeschi digs into the numbers. [medium]

Free-floating fiat currencies are supposed to help countries avoid financial crises provoked by borrowing too much from abroad. But that really only works when a country’s currency is widely accepted by its trading partners. Otherwise, old problems can still arise according to Frances Coppola. [coppola comment]

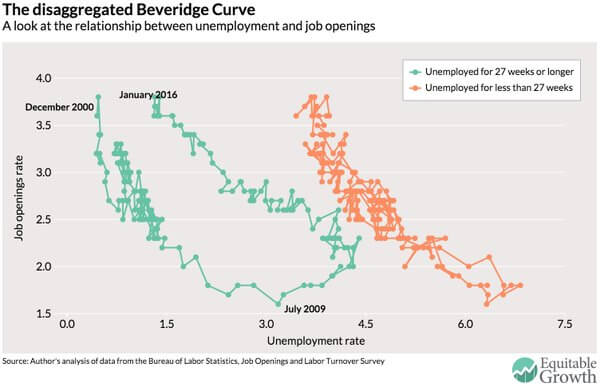

Friday figure

Figure created by Nick Bunker