- : The internet and the Productivity Slump

- : The Perils of Presidentialism

- : Yellen Pivots Toward Saving Her Legacy

Must-read: Gavyn Davies: “The internet and the Productivity Slump”

Must-Read: : The internet and the Productivity Slump: “How much would an average American, whose annual disposable income is $42,300…

…need to be paid in order to be persuaded to give up their mobile phone and access to the internet, for a full year? Would it be more, or less, than $8,400 for the year?… Chad Syverson… calculates that the productivity slowdown in the US is equivalent to about $2.7 trillion of lost output per annum by 2015. Even on the most generous method that he can find to calculate the extent of the underestimated consumer surplus from the digital economy, he reckons that only about one third of the productivity gap can be explained in this way…. He suggests, on prima facie grounds, that few people would value their access to the digital economy at one fifth of their disposable income. Maybe, but… most people are now extremely reliant upon, or addicted to, the internet, especially via their smartphones. Faced with the choice, I doubt whether they would be prepared to be transported back to the obsolete technology of a decade ago in exchange for an annual payment of less than, say, a few thousand dollars a year–i.e. far less than than the value currently accorded to digital activity in GDP…

Monday Smackdown: Robert Waldmann Marks Brad DeLong’s Beliefs about “The Return of Depression Economics” to Market

: Brad DeLong Marks His Beliefs about “The Return of Depression Economics” to Market: “Brad DeLong…reposted his review of Krugman’s ‘The Return of Depression Economics’ from 1999…

…’Just in case I get a swelled-head and think I am right more often than I am …’ Way back in the last century, Brad thought he had a valid criticism of Paul Krugman’s argument that Japan (and more generally countries in a liquidity trap) need higher expected inflation. I think the re-post is not just admirable as a self criticism session, but also shows us something about the power of Macroeconomic orthodoxy. Brad is just about as unorthodox as an economist can be without being banished from the profession, but even he was more influenced by Milton Friedman and Robert Lucas than he should have been…. Japan had slack aggregate demand at a safe nominal interest rate of 0–that i,s it was in the liquidity trap. Krugman argued that higher expected inflation would cause negative expected real interest rates and higher aggregate demand and solve the problem. Brad was unconvinced (way back then):

But at this point Krugman doesn’t have all the answers. For while the fact of regular, moderate inflation would certainly boost aggregate demand for products made in Japan, the expectation of inflation would cause an adverse shift in aggregate supply: firms and workers would demand higher prices and wages in anticipation of the inflation they expected would occur, and this increase in costs would diminish how much real production and employment would be generated by any particular level of aggregate demand.

Would the benefits on the demand side from the fact of regular moderate inflation outweigh the costs on the supply side of a general expectation that Japan is about to resort to deliberate inflationary finance? Probably. I’m with Krugman on this one. But it is just a guess–it is not my field of expertise–I would want to spend a year examining the macroeconomic structure of the Japanese economy in detail before I would be willing to claim even that my guess was an informed guess.

And there is another problem. Suppose that investors do not see the fact of inflation–suppose that Japan does not adopt inflationary finance–but that a drumbeat of advocates claiming that inflation is necessary causes firms and workers to mark up prices and wages. Then we have the supply-side costs but not the demand-side benefits, and so we are worse off than before.

As Brad now notes, this argument makes no sense. I think it might be hard for people who learned about macro in the age of the liquidity trap to understand what he had in mind. I also think the passage might risk being convincing to people who haven’t read enough Krugman or Keynes. The key problems in the first paragraphs are ‘adverse’ and ‘any particular level of aggregate demand’. Brad assumed that an increase in wage and price demands is an adverse shift. The argument that it is depends on the assumption that he can consider a fixed level of nominal aggregate demand (and yet he didn’t feel the need to put in the word ‘nominal’). The butchered sentence ‘would diminish how much real production and employment would be generated by any particular level of [real] aggregate demand.’ clearly makes no sense.

During the 80s, new Keynesian macroeconomists got into the habit of considering a fixed level of nominal aggregate demand when focusing on aggregate supply. Because it wasn’t the focus, they used the simplest existing model of aggregate demand the rigid quantity theory of money in which nominal aggregate demand is a constant times the money supply (which is assumed to be set by the monetary authority). This means that the aggregate demand curve (price level on the y axis and real gdp on the x axis) slopes down. This in turn means that an upward shift in the aggregate supply curve is an adverse shift.

More generally, the way in which a higher price level causes lower real aggregate demand is by reducing the real value of the money supply, but if the economy is in the liquidity trap the reduction in the real money supply has no effect on aggregate demand. In the case considered by Krugman, the aggregate demand curve is vertical. This means that he can discuss the effect of policy on real GDP without considering the aggregate supply curve. The second paragraph just repeats the assumption that higher expected inflation causes ‘costs’. There are no such costs (at least according to current and then existing theory) if the economy is in a liquidity trap. The third paragraph shows confusion about the cause of the ‘demand side benefits’. They are caused by higher expected inflation not by higher actual inflation. If there were higher expected inflation not followed by higher actual inflation, Japan would enjoy the benefits anyway. Those benefits would outweigh the non-existent costs.

Krugman actually did consider a model of aggregate supply, but it is so simple it is easy to miss. As usual (well as became usual as Krugman did this again and again) the model has two periods–the present and the long run. In the present, it is assumed that wages and prices are fixed. In the long run it is assumed that there is full employment and constant inflation. Krugman’s point is that all of the important differences between old Keynesian models and models with rational forward looking agents can be understood with just two periods and very simple math. The problem is that the math is so simple that it is easy to not notice it is there and to assume that he ignored the supply side.

I am going to be dumb (I am not playing dumb–I just worked through each step) and consider different less elegant models of aggregate supply. The following will be extremely boring and pointless:

- Fixed nominal wages, flexible prices and profit maximization (this is Keynes’s implicit model of aggregate supply). In this case, the supply curve gives increasing real output as a function of the price level. An ‘adverse’ shift of this curve would be a shift up. It would not affect real output in the liquidity trap since the aggregate demand curve is vertical. it would not impose any costs as the increased price level would reduce the real money supply from plenty of liquidity to still plenty of liquidity. This model of aggregate supply is no good (it doesn’t fit the facts). It is easy to fear that Krugman implicitly assumed it was valid when in a rush (at least this is easy if one hasn’t been reading Krugman every day for years–he doesn’t do things like that).

A fixed expectations-unaugmented Phillips curve which gives inflation as an increasing function of output. An ‘adverse’ shift of he Phillips curve would imply higher inflation. This would have no costs.

An expectations-augmented Phillips curve in which expected inflation is equal to lagged inflation–output becomes a function of the change in inflation. In a liquidity trap, there would be either accelerating inflation or accelerating deflation. For a fixed money supply accelerating inflation would reduce real balances until the economy would no longer be in a liquidity trap. The simple model would imply the possibility of accelerating deflation and ever decreasing output. This model is no good, because such a catastrophe has never occurred, Japan had constant mild deflation which did not accelerate, even during the great depression the periods of deflation ended.

An expectations augmented Phillips curve with rational expectations–oh hell I’ll just assume perfect foresight. Here both the aggregate demand and aggregate supply curves are vertical. If they are at different levels of output, there is no solution. The result is that a liquidity trap is impossible. This is basically a flexible price model. If there were aggregate demand greater than the fixed aggregate supply, the price level would jump up until the real value of money wasn’t enough to satiate liquidity preference. Krugman assumed that, in the long run, people don’t make systematic forecasting mistakes. So he assumed that the economy can’t stay in the liquidity trap for the long run. Ah yes, his model had everything new classical in the long run (this is the point on which Krugman has marked his beliefs to market).

The argument that Krugman would not have reached his conclusions about the economics of economies in liquidity traps if he had considered the supply side only makes sense if it includes the intermediate step that, if one considers the supply side, one must conclude that economies can never be in liquidity traps. This is no good as Japan was in the liquidity trap as are all developed countries at present.

I think the only promising effort here was (3)–a Phillips curve with autoregressive expectations. The problem is: why hasn’t accelerating deflation ever occurred? Way back in 1999, Krugman clearly thought that the answer was just that we had been lucky so far. He warned of the risk of accelerating deflation. Now he thinks he was wrong. Like Krugman, I think the reason is that there is downward nominal rigidity — that it is very hard to get people to accept a lower nominal wage or sell for a lower price. This depends on the change in the wage or price and not in that change minus expected inflation.

Clearly this rigidity isn’t absolute (Japan has had deflation and there were episodes of deflation in the 30s). But it is possible to get write a model in which unemployment is above the non accelerating inflation rate, but nominal wages aren’t cut. In this case expected inflation remains constant–actual deflation doesn’t occur so expected deflation doesn’t occur. The math can work. See here.

Must-read: Juan Linz: “The Perils of Presidentialism”

Must-Read: Juan Linz’s “The Perils of Presidentialism” is a rather good analysis of Richard Nixon and his situation, but a rather bad analysis of Barack Obama and his. In a way, the McConnell-Boehner-Ryan strategy, taken over from the Gingrich playbook, was based on Linz: Block everything Obama attempts, they decided, and then his supporters who have an exaggerated idea of his power will turn against him, and we will rise to power:

: The Perils of Presidentialism: “Given his unavoidable institutional situation…

…a president bids fair to become the focus for whatever exaggerated expectations his supporters may harbor. They are prone to think that he has more power than he really has or should have, and may sometimes be politically mobilized against any adversaries who bar his way. The interaction between a popular president and the crowd acclimating him can generate fear among his opponents and a tense political climate…. In the absence of any principled method of distinguishing the true bearer of democratic legitimacy,, the president may use ideological formulations to discredit his foes; institutional rivalry may thus assume the character of potentially explosive social and political strife….

This analysis of presidentialism’s unpromising implications for democracy is not meant to imply that no presidential democracy can be stable; on th contrary, the world’s most stable democracy–the United States–has a presidential constitution. Nevertheless… the odds that presidentialism will help preserve democracy are… less favorable…. The best type of parliamentary constitution… [needs] a prime-ministerial office combining power with responsibility… [to] help foster responsible decision-making and table governments… encourage genuine party competition without causing undue political fragmentation…. Finally… our analysis establishes only probabilities…. In the final analysis, all regimes… must depend… upon the support of society at large… a public consensus which recognizes as legitimate authority only that power which is acquired through lawful and democratic means… on the ability of their leaders to govern, to inspire trust, to respect the limits of their power, and to reach an adequate degree of consensus. Although these qualities are most needed in a presidential system, it is precisely there they are most difficult to achieve…

Looking at Obama’s 53% approval rating and contrasting it with GWB’s 28%, it has, obviously, not worked out that way. Instead, it is McConnell and Boehner and Ryan’s supporters–not the president’s–who had exaggerated expectations that were disappointed by reality, and have now turned against their putative leaders and representatives.

Must-read: Tim Duy: “Yellen Pivots Toward Saving Her Legacy”

Must-Read: Ever since the Taper Tantrum, it has seemed to me that the center of gravity of the FOMC has not had a… realistic picture of the true forward fan of possible scenarios.

Now Tim Duy sees signs that the center of the FOMC’s distribution is moving closer to mine. Of course, I still do not see the FOMC taking proper account of the asymmetries, but at least their forecast of central tendencies no longer seems as far awry to me as it had between the Taper Tantrum and, well, last month:

: Yellen Pivots Toward Saving Her Legacy: “Janet Yellen… [would] her legacy… amount to being just another central banker…

…who failed miserably in their efforts to raise interest rates back into positive territory[?] The Federal Reserve was set to follow in the footsteps of the Bank of Japan and the Riksbank, seemingly oblivious to their errors. In September… a confident Yellen declared the Fed would be different…. ANN SAPHIR…. “Are you worried… that you may never escape from this zero lower bound situation?” CHAIR YELLEN…. “I would be very surprised if that’s the case. That is not the way I see the outlook or the way the Committee sees the outlook…. That’s an extreme downside risk that in no way is near the center of my outlook.”…

Bottom Line: Rising risks to the outlook placed Yellen’s legacy in danger. If the first rate hike wasn’t a mistake, certainly follow up hikes would be. And there is no room to run; if you want to ‘normalize’ policy, Yellen needs to ensure that rates rise well above zero before the next recession hits. The incoming data suggests that means the economy needs to run hotter for longer if the Fed wants to leave the zero bound behind. Yellen is getting that message. But perhaps more than anything, the risk of deteriorating inflation expectations – the basis for the Fed’s credibility on its inflation target – signaled to Yellen that rates hike need to be put on hold. Continue to watch those survey-based measures; they could be key for the timing of the next rate hike.

Weekend reading: April Fool’s Day edition (but no joke, this is good reading)

This is a weekly post we publish on Fridays with links to articles that touch on economic inequality and growth. The first section is a round-up of what Equitable Growth has published this week and the second is work we’re highlighting from elsewhere. We won’t be the first to share these articles, but we hope by taking a look back at the whole week, we can put them in context.

Equitable Growth round-up

The U.S. labor share has declined quite a bit over the past 15 years. But it’s actually increased since 2012, in part due to the continued economic recovery. Does this mean we can return the labor share to its old levels through strong economic growth alone?

Social insurance isn’t just a form of redistribution. It is, unsurprisingly, also a form of insurance. Programs like Medicaid don’t just insure against the risk of deprivation, but also encourage workers to move into riskier yet higher-paying jobs.

You’ve almost certainly heard of the gig economy. But you probably haven’t heard concrete numbers on its size or importance to the labor market. New research shows that reality is far from the caricature we often hear about Uber and its ilk.

The number of good-paying union jobs and manufacturing jobs have fallen sharply in the United States over the past several decades. Ben Zipperer explains why this downturn has hurt African American workers more than white workers.

Links from around the web

Discussions of higher education among policymakers and the media are dominated by talk about the experiences and challenges that students have when they apply to and attend selective four-year universities. But the typical college-going American has a very different experience. Ben Casselman describes how this skews the public debate about higher ed. [fivethirtyeight]

Larry Summers works through why record-high corporate profits may be a problem. “Suggestive evidence of increases in monopoly power,” he writes, “makes me think that the issue of growing market power deserves increased attention from economists and especially from macroeconomists.” [larrysummersdotcom]

There’s been a significant rise in the number of contractors and temps over the past decade, larger than the rise in overall employment from 2005 to 2015. This trend poses a number of big questions—specifically about the state of social insurance and how much of it will be shifted onto workers, writes Neil Irwin. [the upshot]

The Federal Reserve has a large impact on the U.S. economy, but you wouldn’t know that by the debates presidential candidates are having about the state of the economy. The public would be better served by the candidates talking about the role of the central bank. Narayana Kocherlakota, former president of the Minneapolis Fed, offers some questions on the topic. [bloomberg view]

Speaking of the Federal Reserve, some commentators have worried that Congress is increasingly posing a threat to the independence of the central bank. But is that sense borne out by the data? Carola Binder takes a look and says it doesn’t look like it does. [quantitative ease]

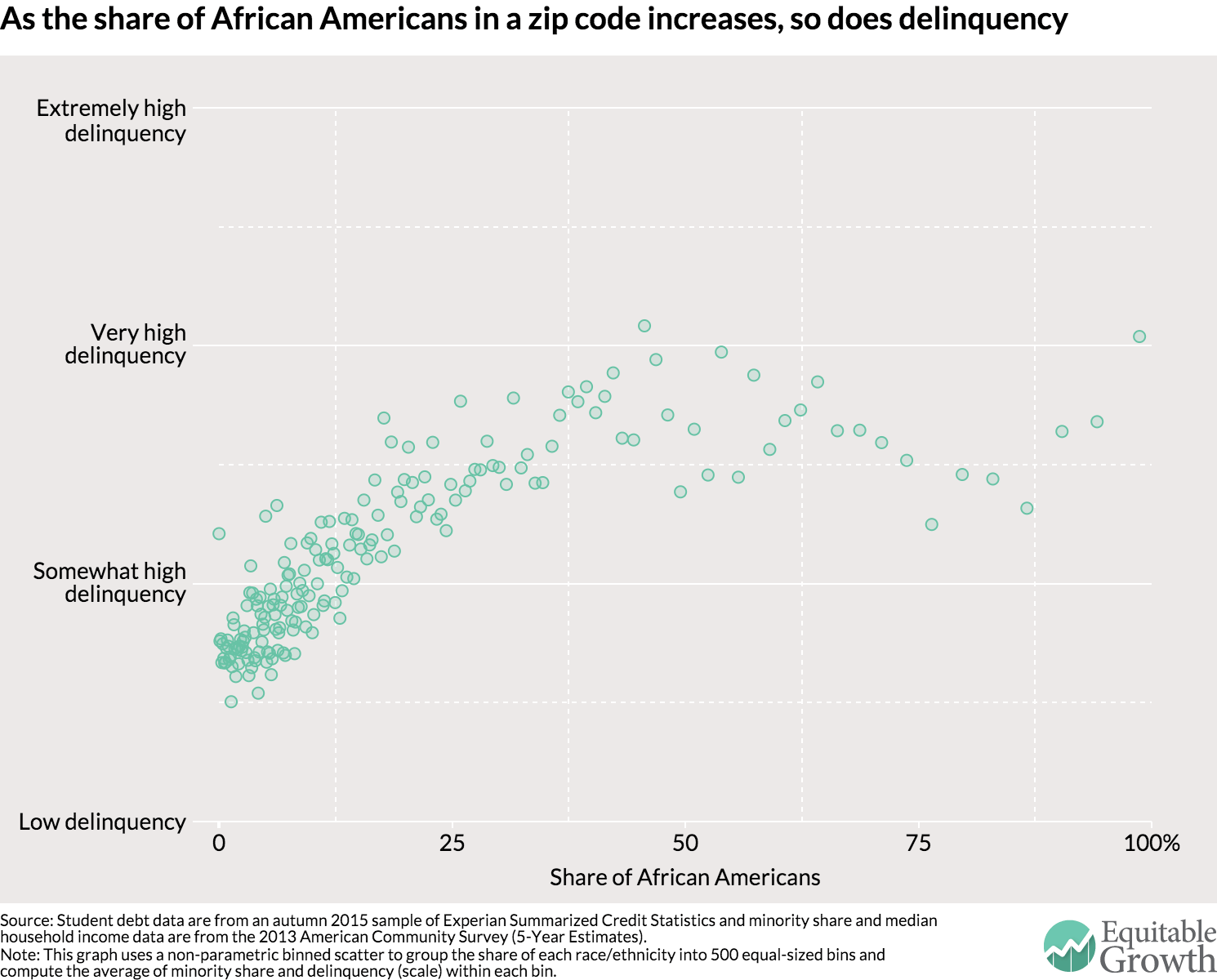

Friday figure

Figure from “How the student debt crisis affects African Americans and Latinos” by Marshall Steinbaum and Kavya Vaghul.

Must-reads: April 1, 2016

Must-read: Dean Baker: “Prime-Age Workers Re-Enter Labor Market”

Must-Read: The Federal Reserve is looking at the past six months and seeing significant improvement in the labor market. It is also looking at financial markets and seeing increased pessimism about inflation. It is having a difficult time reconciling these two.

The reconciliation is, I think, that financial markets now believe that the Phillips Curve is flatter and that the NAIRU is lower than they thought two years ago–and they are likely to be right:

: Prime-Age Workers Re-Enter Labor Market: “The economy added 215,000 jobs in March…

…with the unemployment rate rounding up to 5.0 percent from February’s 4.9 percent. However, the modest increase in unemployment was largely good news, since it was the result of another 396,000 people entering the labor force. There has been large increase in the labor force over the last six months, especially among prime-age workers. Since September, the labor force participation rate for prime-age workers has increased by 0.6 percentage points. This seems to support the view that the people who left the labor market during the downturn will come back if they see jobs available. However even with this rise, the employment-to-population ratio for prime-age workers is still down by more than two full percentage points from its pre-recession peak.

Another positive item in the household survey was a large jump in the percentage of unemployment due to voluntary quits. This sign of confidence in the labor market rose to 10.5 percent, the highest level in the recovery, although it’s still more than a percentage point below the pre-recession peaks and almost four percentage points below the levels reached in 2000.

While the rate of employment growth in the establishment survey was in line with expectations, average weekly hours remained at 34.4, down from 34.6 in January. As a result, the index of aggregate hours worked is down by 0.2 percent from the January level. This could be a sign of slower job growth in future months.

Must-read: Ben Thompson: “Andy Grove and the iPhone SE”

Must-Read: Invest like mad in your technology drivers–even if it looks as if they are not the most profitable. But, conversely, don’t keep pouring money into things that used to be technology drivers but are no longer. And keep your mind open and place many bets as to what your future true technology drivers will be:

: Andy Grove and the iPhone SE: “While [Gordon] Moore is immortalized for having created ‘Moore’s Law’…

…the fact that the number of transistors in an integrated circuit doubles approximately every two years is the result of a choice made first and foremost by Intel to spend the amount of time and money necessary to make Moore’s Law a reality… and the person most responsible for making this choice was Grove…. Grove [also] created a culture predicated on a lack of hierarchy, vigorous debate, and buy-in to the cause (compensated with stock)…. Intel not only made future tech companies possible, it also provided the template for how they should be run….

Grove’s most famous decision…. Intel was founded as a memory company… the best employees and best manufacturing facilities were devoted to memory in adherence to Intel’s belief that memory was their ‘technology driver’…. The problem is that by the mid-1980s Japanese competitors were producing more reliable memory at lower costs (allegedly) backed by unlimited funding from the Japanese government…. Grove soon persuaded Moore, who was still CEO to get out of the memory business, and then proceeded on the even more difficult task of getting the rest of Intel on board; it would take nearly three years for the company to fully commit to the microprocessor….

Intel today is still a very profitable company…. [But] the company’s strategic position is much less secure than its financials indicate, thanks to Intel’s having missed mobile. The critical decision came in 2005…. Steve Jobs was interested in… the XScale ARM-based processor… [for] the iPhone. Then-CEO Paul Otellini….

We ended up not winning it or passing on it, depending on how you want to view it. And the world would have been a lot different if we’d done it…. You have to remember is that this was before the iPhone was introduced and no one knew what the iPhone would do…. At the end of the day, there was a chip that they were interested in that they wanted to pay a certain price for and not a nickel more and that price was below our forecasted cost. I couldn’t see it. It wasn’t one of these things you can make up on volume. And in hindsight, the forecasted cost was wrong and the volume was 100x what anyone thought.

It was the opposite of Grove’s memory-to-microprocessor decision: Otellini prioritized Intel’s current business (x86 processors) instead of moving to what was next (Intel would go on to sell XScale to Marvell in 2006), much to the company’s long-term detriment…

Must-read: Narayana Kocherlakota: “Information in Inflation Breakevens about Fed Credibility”

Must-Read: Whenever I look at a graph like this, I think: “Doesn’t this graph tell me that the last two years were the wrong time to give up sniffing glue the zero interest-rate policy”? Anyone? Anyone? Bueller?

And Narayana Kocherlakota agrees, and makes the case:

: Information in Inflation Breakevens about Fed Credibility: “The Federal Open Market Committee has been gradually tightening monetary policy since mid-2013…

…Concurrent with the Fed’s actions, five year-five year forward inflation breakevens have declined by almost a full percentage point since mid-2014. I’ve been concerned about this decline for some time (as an FOMC member, I dissented from Committee actions in October and December 2014 exactly because of this concern). In this post, I explain why I see a decline in inflation breakevens as being a very worrisome signal about the FOMC’s credibility (which I define to be investor/public confidence in the Fed’s ability and/or willingness to achieve its mandated objectives over an extended period of time).

First, terminology. The ten-year breakeven refers to the difference in yields between a standard (nominal) 10-year Treasury and an inflation-protected 10-year Treasury (called TIPS). Intuitively, this difference in yields is shaped by investors’ beliefs about inflation over the next ten years. The five-year breakeven is the same thing, except that it’s over five years, rather than 10.

Then, the five-year five-year forward breakeven is defined to be the difference between the 10-year breakeven and the five-year breakeven. Intuitively, this difference in yields is shaped by beliefs about inflation over a five year horizon that starts five years from now. In particular, there is no reason for beliefs about inflation over, say, the next couple years to affect the five-year five-year forward breakeven.

Conceptually, the five-year five-year forward breakeven can be thought of as the sum of two components:

1. investors’ best forecast about what inflation will average 5 to 10 years from now

- the inflation risk premium over a horizon five to ten years from now – that is, the extra yield over that horizon that investors demand for bearing the inflation risk embedded in standard Treasuries.

(There’s also a liquidity-premium component, but movements in this component have not been all that important in the past two years.)There is often a lot of discussion about how to divide a given change in breakevens in these two components. My own assessment is that both components have declined. But my main point will be a decline in either component is a troubling signal about FOMC credibility.

It is well-understood why a decline in the first component should be seen as problematic for FOMC credibility. The FOMC has pledged to deliver 2% inflation over the long run. If investors see this pledge as credible, their best forecast of inflation over five to ten year horizon should also be 2%. A decline in the first component of breakevens signals a decline in this form of credibility.

Let me turn then to the inflation-risk premium (which is generally thought to move around a lot more than inflation forecasts). A decline in the inflation risk premium means that investors are demanding less compensation (in terms of yield) for bearing inflation risk. In other words, they increasingly see standard Treasuries as being a better hedge against macroeconomic risks than TIPs.

But Treasuries are only a better hedge than TIPs against macroeconomic risk if inflation turns out to be low when economic activity turns out to be low. This observation is why a decline in the inflation risk premium has information about FOMC credibility. The decline reflects investors’ assigning increasing probability to a scenario in which inflation is low over an extended period at the same time that employment is low – that is, increasing probability to a scenario in which both employment and prices are too low relative to the FOMC’s goals.

Should we see such a change in investor beliefs since mid-2014 as being ‘crazy’ or ‘irrational’? The FOMC is continuing to tighten monetary policy in the face of marked disinflationary pressures, including those from commodity price declines. Through these actions, the Committee is communicating an aversion to the use of its primary monetary policy tools: extraordinarily low interest rates and large assetholdings. Isn’t it natural, given this communication, that investors would increasingly put weight on the possibility of an extended period in which prices and employment are too low relative to the FOMC’s goals?

To sum up: we’ve seen a marked decline in the five year-five year forward inflation breakevens since mid-2014. This decline is likely attributable to a simultaneous fall in investors’ forecasts of future inflation and to a fall in the inflation risk premium. My main point is that both of these changes suggest that there has been a decline in the FOMC’s credibility.

To be clear: as I well know, in the world of policymaking, no signal comes without noise. But the risks for monetary policymakers associated with a slippage in the inflation anchor are considerable. Given these risks, I do believe that it would be wise for the Committee to be responsive to the ongoing decline in inflation breakevens by reversing course on its current tightening path.