Must-Read: : Duncan Weldon on Globalization and Redistribution (with image, tweets) · delong · Storify:

Must-Read: Barry Ritholtz: How High Are Real House Prices?

Must-Read: : How High Are Real House Prices?

ObamaCare Increases the Salience of Antitrust in Health Insurance Markets

: ObamaCare Increases the Salience of Antitrust in Health Insurance Markets from “Important” to “Essential”: As the extremely-sharp Aaron Edlin has taught me, apropos of the current wave of proposed health insurance mergers–Aetna-Humana, Anthem-Cigna, and Centene-HealthNet:

The coming of ObamaCare makes any willingness on the part of antitrust authority to allow these mergers to go through extremely dangerous and destructive policy indeed.

The imposition of the individual mandate to purchase health insurance makes maintaining competition in health insurance markets significantly more important. Usually, the exercise of market power and the ability to easily collude implicitly or explicitly made possible by large market shares are curved by the possibility of exit. The ‘exit the market and buy something else’ option for consumers is the one competitor that the firm cannot acquire and merge with. It is the one competitor with which the firm cannot collude, implicitly or explicitly.

Imposing an individual mandate to purchase is a wise policy in a market place where the major market failure is adverse selection. It threatens to be a catastrophic policy in the marketplace where the major market failure is the exercise of sellers market power.

We see this flashpoint–and it is a dangerous flashpoint–in health insurance right now. But the issues are actually much broader. Here is the wise Kevin Drum:

: Our Four-Decade Antitrust Experiment Has Failed: “We have four airlines serving 80 percent of all passengers…

…We have four cable and Internet companies providing most of the nation’s cell-phone and television service. We have four big commercial banks, five big insurance companies (only three if two proposed mergers go through this year), and a handful of producers selling every major consumer product. Even when you think you have a choice, like in the array of online travel-booking sites, two companies (Expedia and Priceline) own all the subsidiaries…. Over the past few decades, America has undergone a sea change in antitrust law. It’s now all about ‘consumer welfare’—which means, in practice, that big mergers are fine as long as the mergees can make a credible case that the combined entity will be good for consumers. You will be unsurprised to learn that high-powered marketing departments are very good at collecting data to show exactly that, and that high-powered attorneys are extremely good at turning this data into bulletproof legal arguments. The result is that very few mergers are ever turned down.

But this siren call has led us down a long, blind alley. It turns out that in the short term, plenty of big mergers really can be good for consumers. In the longer term, though, very few are…. We’d be better off returning to an older, cruder rule: ensuring that there are plenty of competitors in every market and refusing to allow any single company to become too dominant. As near as I can tell, there’s a real tipping point around the number three or four. If a market is dominated by four companies or less, that’s when it starts to wither….

Needless to say, even a crude market share rule doesn’t make things simple. You’ll still have arguments over what counts as a single market (online advertising or the entire advertising industry?). You’ll have arguments over just how big a single company should be allowed to get (30 percent share or 50 percent share?). You’ll have industries where it’s not easy to have lots of competitors. And you’ll have some industries where the returns to scale to are so potent that small companies just flatly can’t compete. There’s no easy panacea. But ‘consumer welfare’ is an open invitation to thousand-page regulatory filings that dive deep down a rabbit hole and never come up for air…. Competition is the core engine of capitalism. If you have plenty of it, you can make do without a lot of other regulations. But once you allow competition to wither, there’s little choice left…. The federal government should do its best to ensure that markets have plenty of competition, and then it can afford to get out of the way and regulate fairly lightly. Other companies will do their work for them. What’s not to like?

U.S. labor market frictions and occupational licensing

Occupational licensing in recent years jumped out of obscurity into a prominent position in discussions about problems in the U.S. labor market. Between 25 and 30 percent of U.S. workers must have a license to work in their jobs, a five-fold increase since the 1950s. Such a big increase in licensing did increase wages for licensed workers, but the fear is that the gain for those workers comes at the expense of workers locked out of potential jobs. What’s more, occupational licensing might also be partially responsible for one of the most troubling trends in the U.S. labor market: declining labor market fluidity. State-by-state differences in licensing may stop workers from moving to a new job.

In fact, despite the good amount of policy conversation about the effects of licensing on geographic mobility in particular, there hasn’t been much research on the relationship. But that’s starting to change. New research on one particularly important licensed profession—nursing—indicates that licensing may not be as large a problem as some policymakers and economists have assumed.

Now, though, a new working paper released by the National Bureau of Economic Research investigates this very question. The new paper by Christina DePasquale of Emory University and Kevin M. Stange of the University of Michigan looks at the effect of a key policy reform to nursing licenses. The program, called the Nurse Licensure Compact, allows a nurse with a license in one state to go and work in another state that’s opted into the compact. Only 25 states have opted into the compact and their entrance has been staggered, so DePasquale and Stange can look at the differences in labor market outcomes between nurses in states that signed onto the compact and workers in bordering states who didn’t.

Furthermore, the two economists can run an analysis that does that comparison as well as comparing nurses to non-nurse health care workers to control for underlying differences that may have caused the state to join the Nurse Licensure Compact. When all is said and done, the researchers find a very small effect of this easing of licensing on nurse’s labor market outcomes.

Specifically, the Nursing Licensure Compact neither increases nurses’ labor force participation and employment nor boosts the likelihood of them working across state lines. DePasquale and Stange find very minimal effects on nurses moving across state lines while the slight evidence they find for this effect is from young workers and it isn’t particularly strong in a statistical sense.

So what should policymakers take away from this research? First off, a reminder that this new paper looks only at the nursing labor market. Nursing is only one profession, so we shouldn’t jump to extrapolate these results to the whole labor market. Yet, as the two authors point out, nursing is the second-largest licensed profession after teachers. So perhaps their findings should make us more skeptical about occupational licensing being a major reason behind declining labor market fluidity. Licensing may have a role, but it may not be the main culprit.

Must-Read: Dani Rodrik: Brexit and the Globalization Trilemma

Must-Read: Time to fly my Neoliberal Freak Flag again!

I see this very differently than the extremely-sharp leader of the Seventh Social-Democratic International Dani Rodrik does. The Greek and the Spanish electorates vote loudly that they want to stay in the EU and even in the Eurozone at all costs, rather than threaten to exercise their exit option. The German electorate votes loudly that they want fiscal austerity at all costs. The policies are a result of those–democratic–decisions. The problem is not that Europe has too little democracy. The problem is that it has the wrong kind. Issues of fiscal stance are technocratic issues of economic governance in order to balance aggregate demand with potential output–to make the demand for safe, liquid, stores of value at full employment equal to the supply of such assets provided by governments with the exorbitant privilege of issuing reserve currencies and whatever other actors (if any) maintain credibility as safe borrowers. They are not properly what Angela Merkel and company have turned them into: things for the Germany electorate to vote on as it participates in what Dani Rodrik rightly calls a morality play about prudence and fecklessness. The monetary issue of whether to stay in the Eurozone or to pursue adjustment-through-depreciation is also a technocratic issue of economic governance in order to maximize speed and minimize the pain of structural adjustment. It is not properly what it has become: a thing for the Greek and Spanish electorates to vote on in a different morality play, one of whether the Mediterranean is or is not a full part of “Europe”.

Harry Dexter White and John Maynard Keynes were good democrats. Neither would say that Europe’s economic problems now are the result of a deficiency of democracy. They would say that it is the fault of their IMF–that their IMF should have blown the whistle, declared a fundamental disequilibrium, and required one of:

- the shrinkage of the eurozone and the depreciation of the peso and the drachma back in 2010

- a wipeout of Greek and Spanish external debts, and a fiscal transfer program from the German government to Greece and Spain and to German banks if German authorities wished to avoid such a shrinking of the eurozone.

We did not have such an IMF back in 2010. But that we did not have such an IMF is not the result of a deficiency of democracy in Europe.

Or so I think: I could be wrong here.

Dani:

: Brexit and the Globalization Trilemma: “My personal hope is that Britain will choose to remain in the EU…

…without Britain the EU will likely become less democratic and more wrong-headed…. Exit poses significant economic risk to Britain…. But there are also serious questions posed about the nature of democracy and self-government in the EU as presently constituted. Ambrose Evans-Pritchard (AEP) has now written a remarkable piece that… has little in common with the jingoistic and nativist tone of the Brexit campaign….

Stripped of distractions, it comes down to an elemental choice: whether to restore the full self-government of this nation, or to continue living under a higher supranational regime, ruled by a European Council that we do not elect in any meaningful sense, and that the British people can never remove, even when it persists in error…. We are deciding whether to be guided by a Commission with quasi-executive powers that operates more like the priesthood of the 13th Century papacy than a modern civil service; and whether to submit to a European Court (ECJ) that claims sweeping supremacy, with no right of appeal….

The trouble is that the EU is more of a technocracy than a democracy (AEP calls it a nomenklatura). An obvious alternative to Brexit would be to construct a full-fledged European democracy…. But as AEP says,

I do not think this is remotely possible, or would be desirable if it were, but it is not on offer anyway. Six years into the eurozone crisis there is no a flicker of fiscal union: no eurobonds, no Hamiltonian redemption fund, no pooling of debt, and no budget transfers. The banking union belies its name. Germany and the creditor states have dug in their heels….

Democracy is compatible with deep economic integration only if democracy is appropriately transnationalized as well…. The tension that arises between democracy and globalization is not straightforwardly a consequence of the fact that the latter constrains national sovereignty…. External constraints… can enhance rather than limit democracy. But there are also many circumstances under which external rules do not satisfy the conditions of democratic delegation…. It is clear that the EU rules needed to underpin a single European market have extended significantly beyond what can be supported by democratic legitimacy. Whether Britain’s opt out remains effective or not, the political trilemma is at work….

When I was asked to contribute to a special millennial issue of the Journal of Economic Perspectives… I viewed the EU as the only part of the world economy that could successfully combine hyperglobalization (‘the single market’) with democracy through the creation of a European demos and polity…. I now have to admit that I was wrong in this view (or hope, perhaps). The manner in which Germany and Angela Merkel, in particular, reacted to the crisis in Greece and other indebted countries buried any chance of a democratic Europe…. She treated it as a morality play, pitting responsible northerners against lazy, profligate southerners, and to be dealt with by European technocrats accountable to no one serving up disastrous economic remedies…. My generation of Turks looked at the European Union as an example to emulate and a beacon of democracy. It saddens me greatly that it has now come to stand for a style of rule-making and governance so antithetical to democracy that even informed and reasonable observers like AEP view departure from it as the only option for repairing democracy.

Must-Read: Judith Shulevitz: How to Fix Feminism

Must-Read: : How to Fix Feminism: “IN an important new book, ‘Finding Time’…

…Heather Boushey argues that the failure of government and businesses to replace the services provided by ‘America’s silent partner’–the stay-at-home wife–is dampening productivity and checking long-term economic growth. A company that withholds family leave may drive away a hard-to-replace executive. Overstressed parents lack the time and patience to help children develop the skills they need to succeed. ‘Today’s children are tomorrow’s work force,’ Ms. Boushey writes. ‘What happens inside families is just as important to making the economy hum along as what happens inside firms.’

Knowing that motherhood can derail a career, women are waiting longer and longer to have children…. I recently got into an argument with a professor friend about the plausibility of restructuring higher education and the professions so that women–and men–wouldn’t have to hustle for positions like partner or associate professor just as they reach peak fertility. Many universities, I said, now stop the tenure clock for a year when assistant professors have children. My friend laughed. A year is nothing when it comes to a baby, she said. She’d never have won tenure if she’d had her son first. I didn’t know what to say. At least she had a child, unlike friends who waited until too late….

What if child-rearing weren’t an interruption to a career but a respected precursor to it, like universal service or the draft?… American families, particularly low-income families, can’t do without a double income, given wage stagnation and the cost of children in a country that won’t help parents raise them. But having to work should not be confused with wanting to work…. Marissa Mayer, now chief executive of Yahoo, reported that when she was in Google’s employ, she slept under her desk, one disgusted feminist, Sarah Leonard, wrote, ‘If feminism means the right to sleep under my desk, then screw it.’… Feminism… should not mean… a politics of the possible. We’re fighting for 12 weeks of leave when we need to rethink the basic chronology of our lives…

This is, I would note, what Larry Summers said eleven years ago we should think very hard about, as an economy, as a society, and as a culture:

(2005): Remarks at NBER Conference on Diversifying the Science & Engineering Workforce: “[In] major corporations… [at] large law firms… [in] prominent teaching hospitals, and… [in] other prominent professional service organizations, as well as… in higher education…

…the story is fundamentally the same. Twenty or twenty-five years ago, we started to see very substantial increases in the number of women who were in graduate school in this field. Now the people who went to graduate school when that started are forty, forty-five, fifty years old. If you look at the top cohort in our activity, it is not only nothing like fifty-fifty, it is nothing like what we thought it was when we started having a third of the women, a third of the law school class being female, twenty or twenty-five years ago. And the relatively few women who are in the highest ranking places are disproportionately either unmarried or without children, with the emphasis differing depending on just who you talk to…. That is a reality…. What does one make of that?…

Speaking completely descriptively and non-normatively… the most prestigious activities in our society expect of people who are going to rise to leadership positions in their forties near total commitments to their work… a large number of hours in the office… a flexibility of schedules… a continuity of effort…. That is a level of commitment that a much higher fraction of married men have been historically prepared to make than of married women. That’s not a judgment about how it should be…. That expectation is meeting with the choices that people make and is contributing substantially to the outcomes that we observe….

What fraction of young women in their mid-twenties make a decision that they don’t want to have a job that they think about eighty hours a week? What fraction of young men make a decision that they’re unwilling to have a job that they think about eighty hours a week?… That has got to be a large part of what is observed.

Now that begs entirely the normative questions…. Is our society right to expect that level of effort from people who hold the most prominent jobs? Is our society right to have familial arrangements in which women are asked to make that choice and asked more to make that choice than men? Is our society right to ask of anybody to have a prominent job at this level of intensity?…

To buttress conviction and theory with anecdote, a young woman who worked very closely with me at the Treasury and who has subsequently gone on to work at Google highly successfully, is a 1994 graduate of Harvard Business School. She reports that of her first year section, there were twenty-two women, of whom three are working full time at this point. That may, the dean of the Business School reports to me, that that is not an implausible observation given their experience with their alumnae…

Tim Duy’s Five Questions for Janet Yellen

A very nice piece here from the very-sharp Tim Duy:

: Five Questions for Janet Yellen

Next week’s meeting of the Federal Open Market Committee (FOMC) includes a press conference with Chair Janet Yellen. These are five questions I would ask if I had the opportunity to do so in light of recent events.

(1) 1. What’s the deal with labor market conditions? You advocated for the creation of the Federal Reserve’s Labor Market Conditions Index (LMCI) to serve as a broader measure of the labor market and as an alternative to a narrow measure such as the unemployment rate. The LMCI declined for five consecutive months through May, the most recent release…. On June 6, however, you said that:

the job market has strengthened substantially, and I believe we are now close to eliminating the slack that has weighed on the labor market since the recession.

The LCMI signals that although the economy may be operating near full employment, it is now moving further away from that goal. Is it appropriate for the Fed to still be considering interest rate hikes when your measure is moving away from the goal of full employment? Or have you determined the LMCI is not a useful measure of labor market conditions?

(2) Has the effect of QE been underestimated? Since the Fed began and completed the process of ending quantitative easing (QE), the dollar has risen in value, the stock market rally has stalled, the yield curve has flattened, broader economic activity has slowed, and now we are experiencing a slowing in labor market activity. These are all traditionally signs of tighter monetary policy, but you have insisted that tapering is not tightening and that policy remains accommodative. Given these signs, is it possible or even likely that you have underestimated the effectiveness of QE and hence are now overestimating the level of financial accommodation?

(3) Optimal control or no? The Fed appears determined to hit its inflation target from below. In other words, the central bank is positioning policy to tighten despite inflation currently running below the 2 percent target in order to avoid an overshoot at a later date. In the past, however, you argued for an ‘optimal control’ approach that anticipated an explicit overshooting of the inflation target in order to more rapidly meet the Fed’s mandate of full employment. Under optimal control, it seems that given stalled progress on reducing underemployment, coupled with deteriorating labor market conditions, the Fed should now be explicitly aiming to overshoot the inflation target by keeping policy loose. Do you believe the optimal control approach you previously advocated is wrong? If so, what caused you to change your mind?

(4) An Evans Rule for all? Chicago Federal Reserve President Charles Evans remains concerned about asymmetric policy risks. Persistently below target inflation risks undermining the public’s belief that the Fed is committed to reaching its target. Such a loss of credibility hampers the ability to subsequently meet the central bank’s target. In contrast, the well-known effectiveness of traditional policy tools means there is less upside risk to inflation. Consequently, he argues for an updated version of the Evans Rule (or an earlier commitment to not hike rates as long as unemployment exceeded 6.5 percent and inflation was below 2.5 percent).

Specifically, Evans said:In order to ensure confidence that the U.S. will get to 2 percent inflation, it may be best to hold off raising interest rates until core inflation is actually at 2 percent. The downside inflation risks seem big — losing credibility on the downside would make it all that more difficult to ever reach our inflation target. The upside risks on inflation seem smaller.

Recall that in your most recent speech you indicated unease with inflation expectations and — at least implicitly — recognized the asymmetry of policy risks:

It is unclear whether these indicators point to a true decline in those inflation expectations that are relevant for price setting; for example, the financial market measures may reflect changing attitudes toward inflation risk more than actual inflation expectations. But the indicators have moved enough to get my close attention. If inflation expectations really are moving lower, that could call into question whether inflation will move back to 2 percent as quickly as I expect.

This — especially when combined with your past support for an optimal control approach to policy — suggests that you should be amenable to adopting Evans’ position. Do you support Evans’ proposal that the Fed should stand down from rate hikes until the inflation target is reached? Why or why not?

(5) Just how much do you care about the rest of the world? Earlier this year, Federal Reserve Governor Lael Brainard suggested that the many developed economies operating at or below zero percent interest rates reduces the central bank’s capacity for raising rates:

‘Financial tightening associated with cross-border spillovers may be limiting the extent to which U.S. policy diverges from major economies…

At last September’s FOMC press conference, you said that you thought the global forces were insufficient to restrain the path of U.S. monetary policy. In response to a question about ‘global interconnectedness’ preventing the U.S. from ever moving away from zero percent interest rates, you said:

I would be very surprised if that’s the case. That is not the way I see the outlook or the way the Committee sees the outlook. Can I completely rule it out? I can’t completely rule it out. But, really, that’s an extreme downside risk that in no way is near the center of my outlook.

Given the events of the past six months — especially the refusal of longer-term U.S. Treasury yields to rise despite repeated hints of monetary tightening — have you reassessed your opinion? Do you view the risks of such an outcome as greater or lower than your assessment made last September?

Bottom Line: Most of these questions try to push Yellen to explain her past positions in light of the current data and actions. I think understanding how and why her positions change is critical to understanding how the Fed reacts to the conditions facing it. Making the so-called ‘reaction function’ clear remains the most important piece of the Fed’s communication strategy.

These five questions–“What’s the deal with labor market conditions?… Has the effect of QE been underestimated?… Optimal control or no?… An Evans Rule for all?… Just how much do you care about the rest of the world?”–are the right questions to ask. And Tim’s bottom line–“Push Yellen to explain her past positions in light of the current data and actions. I think understanding how and why her positions change is critical…. Making the so-called ‘reaction function’ clear remains the most important piece of the Fed’s communication strategy”–is the right bottom line.

After all, does this look like an economy crossing the line of potential output in an upward direction with growing and substantial gathering inflationary pressures to you?

The Federal Reserve is simply not doing a good job of communicating its reaction function. It is not doing a good job of linking its model of the economy to current data and past events. Inflation, production, and employment (but not the unemployment rate) have been disappointingly low relative to Federal Reserve expectations for each of the past nine years. These events should have led to substantial rethinking by the Federal Reserve of its model of the economy. And yet the model set forward by Yellen and Fischer (but not Evans and Brainard) appears to be very much the model they held to in the late 1990s, which was the model they believed in in the early 1980s: very strong gearing between recent-past inflation and expected inflation, and a Phillips Curve with a pronounced slope, even with inflation very low.

Unless my Visualization of the Cosmic All is grossly wrong along the relevant dimensions, this is not the right model of the current economy. There was never good reason to think that the bulk of the runup in inflation in the 1970s was due to excessive demand pressure and unemployment below the natural rate–it was, more probably, mostly due to supply shocks plus the lack of anchored expectations. Only if you highball the estimate of the Phillips Curve’s slope for the 1970s can you understand the fall in inflation in the early 1980s as due overwhelmingly to slack, rather than ascribing a component to the reanchoring of inflation expectations. Thus the way to bet is that the economy on its current trajectory will produce less upward pressure on current inflation and also on inflation expectations than the Federal Reserve currently projects.

But how will it react when the data once again disappoints Federal Reserve expectations–as it has? In June 2013, the Fed was predicting that annual GDP growth during the 2013-2015 period would average 2.9%, with longer-run growth of real potential GDP averaging 2.4%. Instead, annual growth has averaged 2.3% (or 2.2%, if estimates for the first half of 2016 are correct). Nor did it perform better on other measures. The Fed predicted an annual inflation rate, based on the personal consumption expenditures index, of 1.9% for 2015. The true number was 1.5%. Similarly, its average projection of the federal funds rate for 2015 was 1.5%. The figure is currently 0.25%. This three-year period, starting in 2013, in which the economy undershot the Fed’s expectations, follows a three-year period in which the economy likewise fell short of the Fed’s forecast. And that period followed a three-year period, starting in 2007, in which the Fed massively understated downside deflationary risks.

Yet the prevailing model does appear to be the model of the early 1980s. It continues to gear inflation expectations at unrealistically high levels based on past inflation. And it continues to rely on the unemployment rate as a stand-in for the state of the labor market, at the expense of other indicators. So the big questions are: Will that commitment break? What would make them revise their models of the economy? And how will those model revisions affect their policy reaction function map from data to interest rates?

In an environment of economic volatility like the one in which we find ourselves today, a prudent central bank should do everything it can to raise expected and actual inflation, in order to gain the ability to stabilize the economy in any direction. If interest rates were well above zero, the Fed would have scope to raise them further in case of overheating or to lower them in response to adverse demand shocks.

But the Fed continues to neglect asymmetry, considering it only a second- or third-order phenomenon. It is not pushing for inflation at or above its target, even as optimal-control doctrines that themselves neglect asymmetry call for such a trajectory. Instead, by tightening policy by an amount that it cannot reliably gauge, it is narrowing its room for maneuver.

Looking at the current composition of the FOMC does not add to confidence:

- On the left, Lael Brainard and Charles Evans certainly understand the situation–and have been right about almost everything they have opined on over the past eight years. Dan Tarullo shares their orientation, but these are not his issues.

-

On the right, Robert Kaplan and Patrick Harker replace hawks who were always certain, often wrong, and never open-minded–and are the products of failed searches: a job search is not supposed to choose a director of the search-consultant firm or the head of the search committee. Jeffrey Lacker and James Bullard and their staffs have been more wrong on monetary policy than the average FOMC member over the past eight years, but do not appear to have taken wrongness as a sign that their views of the economy might need a rethink. Esther George and Loretta Mester and their staffs feel the pain of a commercial banking sector in the current interest-rate environment, but I have never been convinced they understand how disastrous for commercial banks the medium- and long-term consequences of premature tightening and interest-rate liftoff would be.

-

In the neutral center, Jerome Powell does not appear to have views that differ from those of the committee as a whole. These are not Neel Kashkari’s issues: he is too good a bureaucrat to want to dissent from any consensus or near consensus on issues that are not his. And I simply do not have a read on Dennis Lockhart and his staff.

-

The active center is thus composed of Janet Yellen, Stanley Fischer, Bill Dudley, Eric Rosengren, and John Williams. Market risk and confusion is generated by uncertainty about their models of the economy, uncertainty about how they will revise their models as the data comes in, and uncertainty as to how they will react in committee, with six voices to their right calling for rapid interest-rate normalization and only three voices to their left worrying about asymmetric risks and policy traction.

When I listen to this center, one vibe I get is that the asymmetries are really not that great. Janet Yellen this March:

One must be careful, however, not to overstate the asymmetries affecting monetary policy at the moment. Even if the federal funds rate were to return to near zero, the FOMC would still have considerable scope to provide additional accommodation. In particular, we could use the approaches that we and other central banks successfully employed in the wake of the financial crisis to put additional downward pressure on long-term interest rates and so support the economy–specifically, forward guidance about the future path of the federal funds rate and increases in the size or duration of our holdings of long-term securities. While these tools may entail some risks and costs that do not apply to the federal funds rate, we used them effectively to strengthen the recovery from the Great Recession, and we would do so again if needed…

Another vibe I get is more-or-less what Bernanke said back in 2009:

The public’s understanding of the Federal Reserve’s commitment to price stability helps to anchor inflation expectations and enhances the effectiveness of monetary policy, thereby contributing to stability in both prices and economic activity…. A monetary policy strategy aimed at pushing up longer-run inflation expectations in theory… could reduce real interest rates and so stimulate spending and output. However, that theoretical argument ignores the risk that such a policy could cause the public to lose confidence in the central bank’s willingness to resist further upward shifts in inflation, and so undermine the effectiveness of monetary policy going forward. The anchoring of inflation expectations is a hard-won success that has been achieved over the course of three decades, and this stability cannot be taken for granted. Therefore, the Federal Reserve’s policy actions as well as its communications have been aimed at keeping inflation expectations firmly anchored…

I cannot help but be struck by the difference between what I see as the attitude of the current Federal Reserve, anxious not to do anything to endanger its “credibility”, and the Greenspan Fed of the late 1990s, which assumed that it had credibility and that because it had credibility it was free to experiment with policies that seemed likely to be optimal in the moment precisely because markets understood its long-term objective function and trusted it, and hence would not take short-run policy moves as indicative of long-run policy instability. There is a sense in which credibility is like a gold reserve: It is there to be drawn on and used in emergencies. The gold standard collapsed into the Great Depression in the 1930s in large part because both the Bank of France and the Federal Reserve believed that their gold reserves should never decline, but always either stay stable of increase.

And I cannot help but be struck by the inconsistency between the two vibes. The claim that we need not worry about asymmetry because we are willing to undertake radical policy experimentation fits very badly with the claim that we dare not rock the boat because the anchoring of inflation expectations on the upside is very fragile. Combine these with excessive confidence in the current model–with a tendency to make policy based on the center of the fan of projected outcomes with little consideration of how wide that fan actually is–and I find myself with much less confidence in today’s Fed than I, four years ago, thought I would have today.

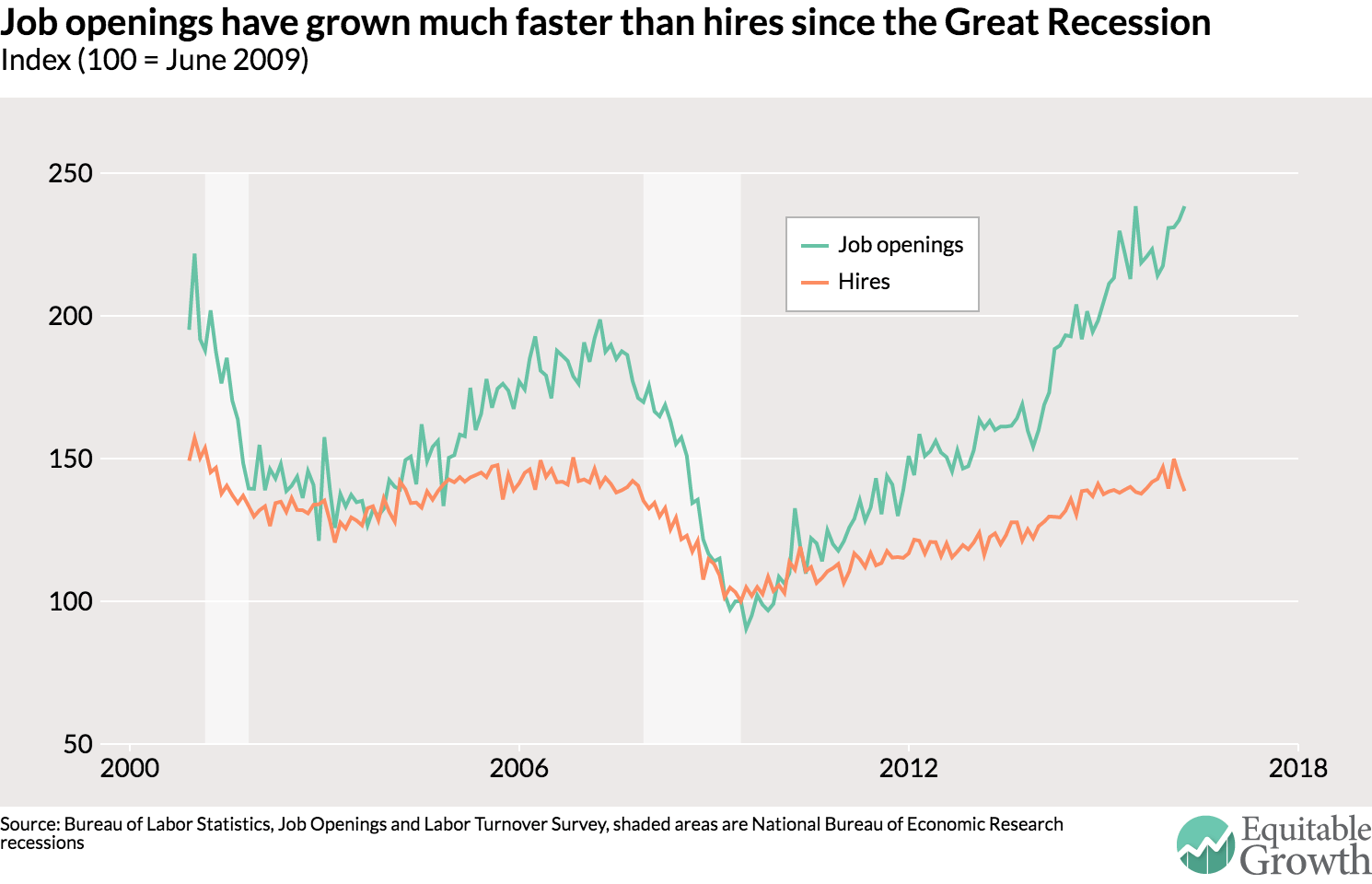

The open questions about the rise of U.S. job openings

One of the more disconcerting trends in the U.S. labor market since the end of the Great Recession is the divergence between the rate of hiring and the rate at which employers are offering jobs. Since June 2009, the number of hires has grown by 39 percent while the job openings have grown by 138 percent. (See figure 1.)

Figure 1

If we think of job openings as a sign of labor demand, then why aren’t firms actually hiring the number of people that they seem to indicate they need based on their job postings? Some economists and writers have interpreted this divergence as a sign that employers want to hire, but they can’t find the right workers for the job. But there are other interpretations of this data that point to the change being related more to employers, rather than employees.

If we think of job openings as a sign of labor demand, then why aren’t firms actually hiring the number of people that they seem to indicate they need based on their job postings? Some economists and writers have interpreted this divergence as a sign that employers want to hire, but they can’t find the right workers for the job. But there are other interpretations of this data that point to the change being related more to employers, rather than employees.

First, let’s make the quick point about the “skills-shortage” argument, that would have us believe the relative dearth of hiring is because workers don’t have adequate skills. For this to be true, we’d expect employers to bid up the price of scarce workers and we’d see rising wage growth. But openings have been growing faster than hires since mid-2010 and wage growth has not been accelerating over that time. So it seems unlikely that something on the worker side is a major part of this divergence.

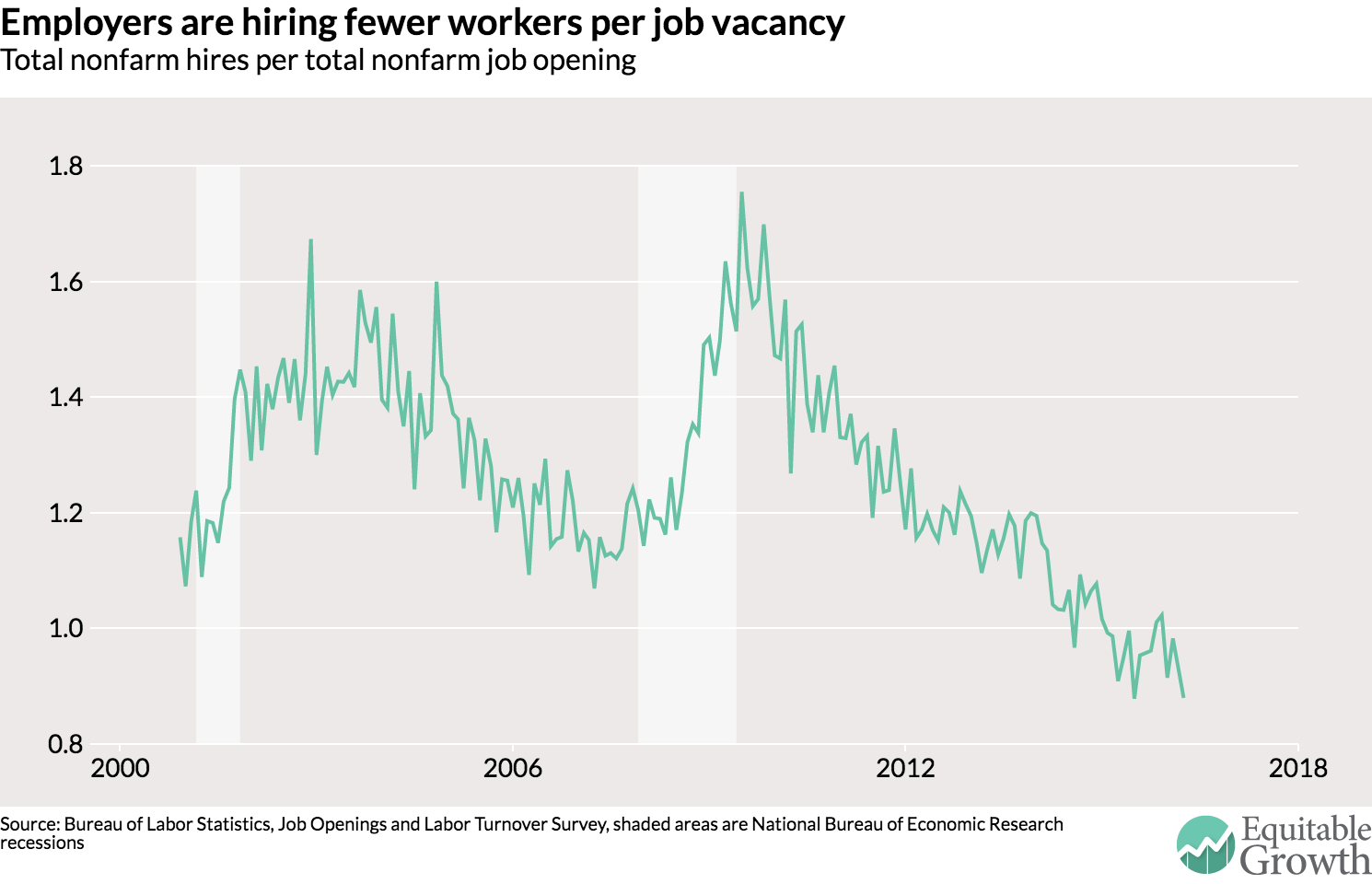

Another way to look at the hires-to-openings divergence is to look at what economists Steven J. Davis of the University of Chicago, R. Jason Faberman of the Federal Reserve Bank of Chicago, and John Haltiwanger of the University of Maryland call the vacancy yield, which is the number of hires per job opening in the economy. The vacancy yield actually jumps up during recessions as there are more unemployed workers to potentially hire and then declines during expansions. As of April 2016, there was only 0.88 hires for every one job opening. (See figure 2.)

Figure 2

The yield for a vacancy is now quite low. Why is it so low? Looking at changes in the yield since the end of the Great Recession, Davis, Faberman, and Haltiwanger find that a lot of it is due to a decline in recruiting intensity by employers. In other words, employers are doing less to actually fill the vacancies they are posting out there in the labor market.

Ben Casselman points out this change might have to do with changes in how companies recruit. The cost of a job posting—simply throwing up an add on a website—may have declined thanks to the internet, so it’s much easier to post jobs than to complete the process of filling them. Or perhaps the reduction in the cost of a job posting is because firms are more profitable now and know the relative cost of employing another worker isn’t that high anymore. Furthermore, this reduction in job filling may be due to the consolidation of companies, as the paper by Davis, Faberman, and Haltiwanger shows that vacancy yields are lower at bigger firms.

These research findings and hypotheses indicate there may have been a change in the labor market since the end of the Great Recession. But rather than a change among the sellers of labor—workers—it may have more to do with the buyers of labor: employers. More thought should be focused on how firms have changed their hiring practices over the past seven years or perhaps since the mass adoption of internet job hunting. This effort may have a higher yield than other research investments.

Must-Reads: June 13, 2016

- : Why Hasn’t the Productivity Crisis Caused a Bear Market (Yet)?

- : Evolution Not Revolution: Rethinking Policy at the IMF

- : Mergers in the Healthcare Sector: Why You’ll Pay More

Should Reads:

- : China’s Rustbelt Revamp Leaves Millions of Jobs at Risk

- : Market deregulation and optimal monetary policy in a monetary union

- Must-Attend: June 15, 2016: 7 PM :: @Booksincberk :: 1491 Shattuck Ave, Berkeley, CA: Manu Saadia: Join us for #Trekonomics

Must-Read: Gavyn Davies: Why Hasn’t the Productivity Crisis Caused a Bear Market (Yet)?

Must-Read: This by the very sharp Gavyn Davies seems to me to be wrong. An ebbing of the current shortage of risk-bearing capacity would produce a further boom in equities. Central banks’ focus on a 2%/year inflation target makes it very difficult to envision any improvement in the economy leading to be a rapid increase in the wage share. Some unknown future negative shock to the economy could certainly produce a large bear market in equities. But a return to more normal risk attitudes in markets and a continuation of business-as-usual are very unlikely to do so:

: Why Hasn’t the Productivity Crisis Caused a Bear Market (Yet)?: “The 2016 calendar year may well see productivity growth in the US economy slumping to around 0.5 per cent, a catastrophic outcome…

…The productivity slowdown has often been called a ‘puzzle’, because it has coincided with a period of rapid technological change in the internet sector…. [But] many of the obvious benefits of the internet revolution appear to increase human welfare without leading to increases in market transactions and nominal GDP. Furthermore, there are several other plausible reasons for the productivity slowdown, including low business investment and a loss of economic dynamism since the financial crash. There is however a different puzzle connected to the productivity slowdown. Given that it has greatly reduced the level and expected growth rate in nominal GDP, why has it had so little apparent impact on equities, an asset class that depends on the level and expected future growth of corporate earnings?…

The conclusion is that the damaging impact of the productivity slump on the S&P 500 has so far been masked by other factors, but there are signs that this might be changing…. The drop in productivity growth has been accompanied by a decline in the yield on safe assets (government bonds), so the discount rate to be applied to future corporate earnings and dividends has declined…. There are however some other reasons…. The share of profits in the economy has risen to historic peak levels, and the dividend payout ratio has also increased…. So does this mean that investors can sit back and relax in the face of a productivity crisis that will clearly damage the outlook for the global economy very seriously? I doubt whether this aberration can last forever. The decline in the real bond yield may be reaching its limits…. And the sharp falls in the unemployment rate, especially in the US, could cause greater wage pressure and a decline in the profit share in GDP…