Over at Finance and Development: Sluggish Future: You are reading this because of the long, steady decline in nominal and real interest rates on all kinds of safe investments, such as US Treasury securities. The decline has created a world in which, as economist Alvin Hansen put it when he saw a similar situation in 1938, we see “sick recoveries… die in their infancy and depressions… feed on themselves and leave a hard and seemingly immovable core of unemployment…” In other words, a world of secular stagnation. Harvard Professor Kenneth Rogoff thinks this is a passing phase—that nobody will talk about secular stagnation in nine years. Perhaps. But the balance of probabilities is the other way. Financial markets do not expect this problem to go away for at least a generation… Read MOAR at Finance and Development

My Draft: You are reading this right now because of the long, steady decline in safe interest rates at all maturities since 1990.(1)

In the United States, we have seen declines in short-term safe interest rates from 4% to -1.2% on the real side and from 8% to 0.5% on the nominal side. And we have seen the decline in long-term safe interest rates from 5% to 1% on the real side, and from 9% to 3% on the nominal side. The elusive Wicksellian “neutral” rate of interest—that rate at which planned investment equals desired full-employment savings—has fallen by more: the economy in 1990 had no pronounced tendency to fall short of full employment; the economy today has.

An economy suffers from “secular stagnation” when the average level of safe nominal interest rates is low and so crashes the economy into the zero lower bound with frequency. Thus, in the words of Alvin Hansen (1939): “sick recoveries… die in their infancy and depressions… feed on themselves and leave a hard and seemingly immovable core of unemployment…”(2)

Financial markets, at least, do not expect this problem to go away for at least as generation. That makes, as I have written, this current policy debate “the most important policy-relevant debate in economics since John Maynard Keynes’s debate with himself in the 1930s…”

I have heard eight different possible causes advanced for this secular fall in safe interest rates:

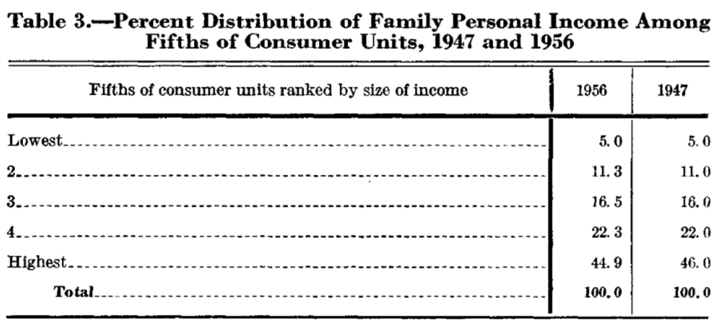

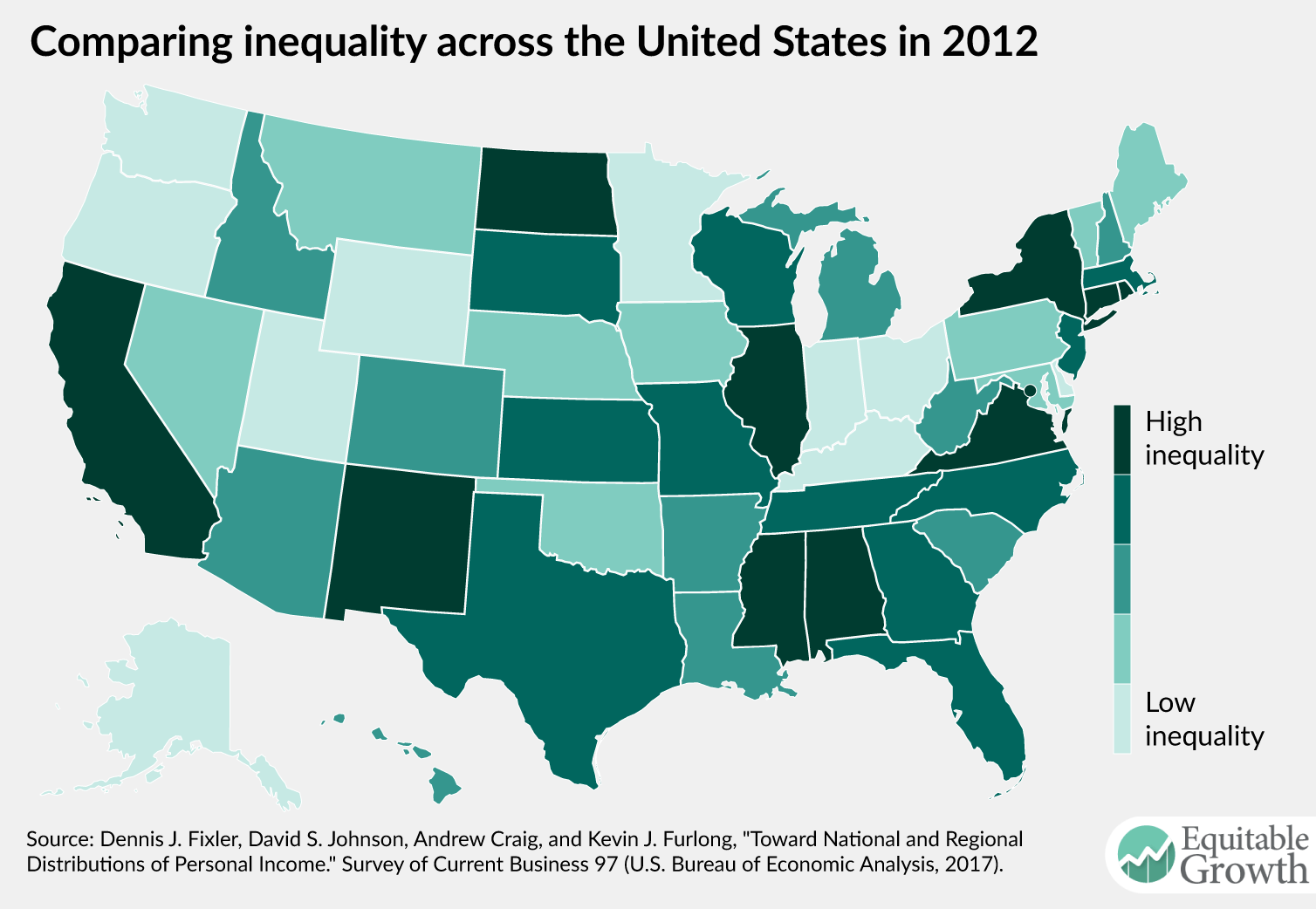

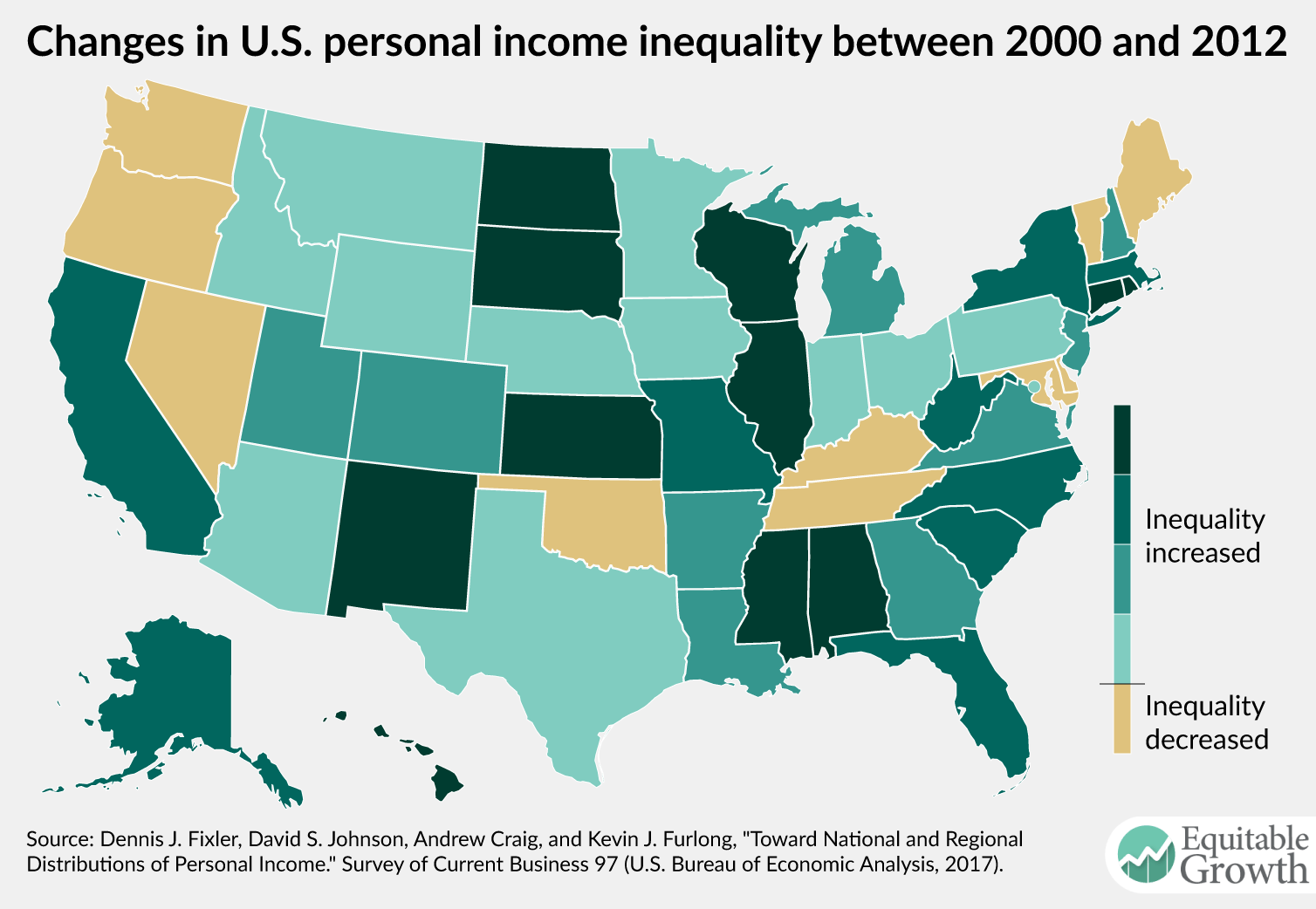

- High income inequality, which boosts savings too much because the rich can’t think of other things they’d rather do with their money.

- Technological and demographic stagnation that lowers the return on investment and pushes desired investment spending down too far.

- Non-market actors whose strong demand for safe, liquid assets is driven not by assessments of market risk and return but rather by political factors or by political risk.

- A collapse or risk-bearing capacity as a broken financial sector finds itself overleveraged and failing to mobilize savings, thus driving a large wedge between the returns on risky investments and the returns on safe government debt.

- Very low actual and expected inflation, which means that even a zero safe nominal rate of interest is too high to balance desired investment and planned savings at full employment.

- Limits on the demand for investment goods coupled with rapid declines in the prices of those goods, which together put too much downward pressure on the potential profitability of the investment-goods sector.

- Technological inappropriateness, in which markets cannot figure out how to properly reward those who invest in new technologies even when the technologies have enormous social returns—which in turn lowers the private rate of return on investment and pushes desired investment spending down too far.

- Increased technology- and rent seeking-driven obstacles to competition which make investment unprofitable for entrants and market-cannibalizing for incumbents.

The first of these was John A. Hobson’s explanation a century ago for the economic distress that had led to the rise of imperialism.(3) The second was, of course, Hansen’s, echoed today by Robert Gordon.(4) The third is Ben Bernanke’s global savings glut.(5) The fourth is Ken Rogoff’s debt-supercycle.(6)

The fifth notes that, while safe real interest rates are higher than they were in the 1980s and 1990s, that is not the case for the 1960s and 1970s. It thus attributes the problem to central banks’ inability to generate the boost from expected and actual inflation a full-employment flex-price economy would generate naturally.(7)

(6), (7), and (8) have always seemed to me to be equally plausible as potential additional factors. But the lack of communication between industrial organization and monetary economics has deprived them of scrutiny. While Gordon, Bernanke, Rogoff, Krugman, and many others have covered (1) through (5), (6), (7), and (8) remain undertheorized.

In general, economists have focused on a single individual one of these causes, and either advocated policies to cure it at its roots or waiting until the evolution of the market and the polity removes it. By contrast, Lawrence Summers(8) has focused on the common outcome. And if one seeks not to cure a single root cause but rather to neutralize and palliate the deleterious macroeconomic effects of a number of causes working together, one is driven—as Larry has been—back to John Maynard Keynes (1936)(9):

A somewhat comprehensive socialisation of investment… [seems] the only means of securing an approximation to full employment… not exclud[ing] all manner of compromises and of devices by which public authority will cooperate with private initiative…

Summers has, I think, a very strong case here. Ken Rogoff likes to say that nine years from now nobody will be talking about secular stagnation.

Perhaps.

But if that is so, it will most likely be so because we will have done something about it.

Notes:

(1) For considerably overlapping and much extended versions of this argument, see J. Bradford DeLong (2016): Three, Four… Many Secular Stagnations! http://www.bradford-delong.com/2017/01/three-four-many-secular-stagnations.html; (2015): The Scary Debate Over Secular Stagnation: Hiccup… or Endgame? Milken Review http://tinyurl.com/dl20170106m

(2) Alvin Hansen (1939): Economic Progress and Declining Population Growth American Economic Review https://www.jstor.org/stable/1806983

(3) John A. Hobson (1902): Imperialism: A Study (New York: James Pott) http://files.libertyfund.org/files/127/0052_Bk.pdf

(4) Robert Gordon (2016): The Rise and Fall of American Growth http://amzn.to/2iVbYKm

(5) Ben Bernanke (2005): The Global Saving Glut and the U.S. Current Account Deficit http://www.federalreserve.gov/boarddocs/speeches/2005/200503102/

(6) Kenneth Rogoff (2015): Debt Supercycle, Not Secular Stagnation http://www.voxeu.org/article/debt-supercycle-not-secular-stagnation

(7) Paul Krugman (1998): The Return of Depression Economics http://tinyurl.com/dl20170106r

(8) Lawrence Summers (2013): Secular Stagnation http://larrysummers.com/imf-fourteenth-annual-research-conference-in-honor-of-stanley-fischer/ ; https://www.youtube.com/watch?v=KYpVzBbQIX0&ab_channel=JamesDecker; (2014): U.S. Economic Prospects: Secular Stagnation, Hysteresis, and the Zero Lower Bound http://link.springer.com/article/10.1057%2Fbe.2014.13; (2015): Rethinking Secular Stagnation After Seventeen Months http://larrysummers.com/wp-content/uploads/2015/07/IMF_Rethinking-Macro_Down-in-the-Trenches-April-20151.pdf;(2016): The Age of Secular Stagnation http://larrysummers.com/2016/02/17/the-age-of-secular-stagnation/

(9) John Maynard Keynes (1936): The General Theory of Employment, Interest and Money https://www.marxists.org/reference/subject/economics/keynes/general-theory/ch24.htm

This File: http://www.bradford-delong.com/2017/04/sluggish-future-no-longer-fresh-over-at-finance-and-development.html

Edit This File: http://www.typepad.com/site/blogs/6a00e551f08003883400e551f080068834/post/6a00e551f08003883401b7c8db1dcc970b/edit

Pages: https://www.icloud.com/pages/0FTAYBVrR3N8H4mtJ8FqbDMiQ#2017-01-09_Sec_Stag_for_F.D_.6x812pt