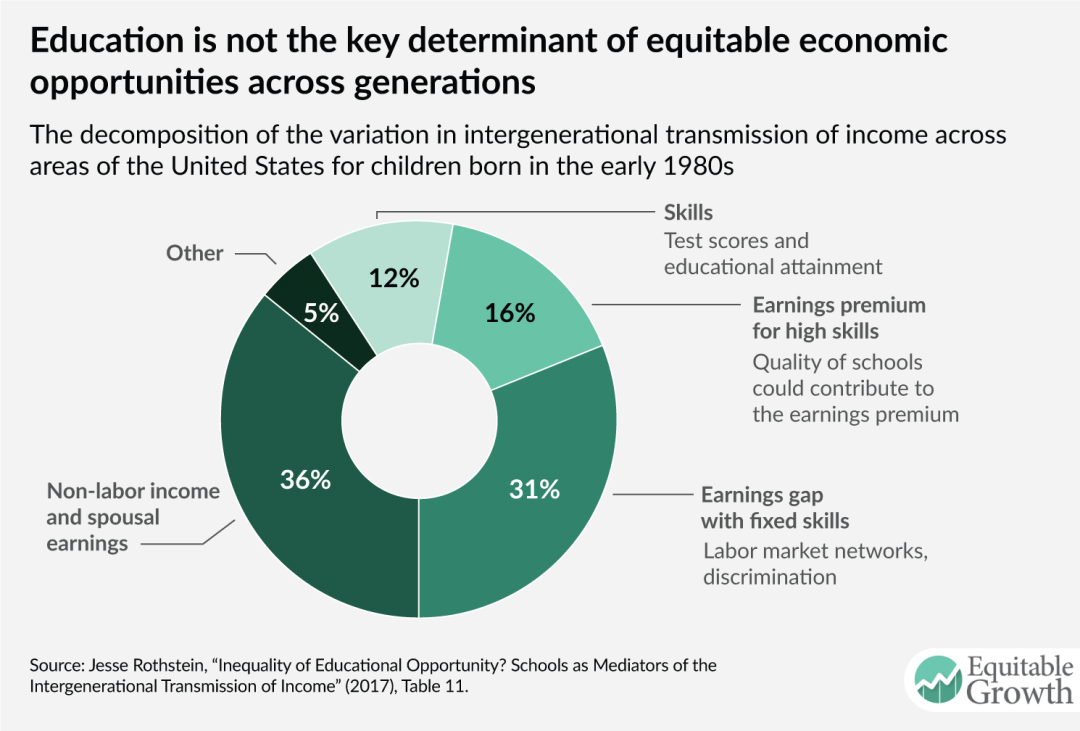

- Jesse Rothstein: Inequality of educational opportunity? Schools as mediators of the intergenerational transmission of income: “Chetty et al. (2014) show that children from low-income families achieve much better adult outcomes… in some places than in others… https://equitablegrowth.org/working-papers/inequality-of-educational-opportunity-schools-as-mediators-of-the-intergenerational-transmission-of-income/

- Will Dobbie and Jae Song: Targeted debt relief and the origins of financial distress: Experimental evidence from distressed credit card borrowers: “We identify the separate effects of the payment reductions and debt write-downs using variation from both the experiment and cross-sectional differences… https://equitablegrowth.org/working-papers/targeted-debt-relief-and-financial-distress/

- Drew Conway: The Data Science Venn Diagram http://www.dataists.com/2010/09/the-data-science-venn-diagram/: “The primary colors of data: hacking skills, math and stats knowledge, and substantive expertise…

- Fardels Bear: Was James Buchanan a Racist? Libertarians and Historical Research: “Today’s libertarians face a similar problem that Morley faced half a decade ago… https://altrightorigins.com/2017/07/13/was-james-buchanan-a-racist-libertarians-and-historical-research/

- Sarah Kliff: Top Democratic, Republican health experts agree on this plan to fix Obamacare: “‘This package is no one’s conception of what is perfect health reform’, says Ron Pollack… of… Families USA, an ardent defender of the ACA… https://www.vox.com/policy-and-politics/2017/8/9/16119244/bipartisan-plan-fix-obamacare

- Nick Bunker: Weekend reading: “Jolting news this week!” edition: “Estimates of the potential growth rate of U.S. gross domestic product have declined… https://equitablegrowth.org/equitablog/weekend-reading-jolting-news-this-week-edition/

- Barry Eichengreen: Hyperglobalization Is Over, But Globalization Is Still with Us: “Hyperglobalization is over… international trade… growing faster than the world economy… has drawn to a close… https://neo.ubs.com/shared/d1JfrUS5WO79UD/9e9d7589-d888-4435-98fc-4792ff141323.pdf

- Chris Dillow: Stumbling and Mumbling: Reinventing the wheel: “In both the UK and US, wage inflation has stayed low despite apparently low unemployment–to the puzzlement of believers in the Philips curve… http://stumblingandmumbling.typepad.com/stumbling_and_mumbling/2017/07/reinventing-the-wheel.html

- Guillermo Gallacher: Manufacturing employment, trade and structural change: “Calls for a return of manufacturing jobs… how feasible is such a goal in light of structural changes in the U.S. economy?… https://equitablegrowth.org/person/guillermo-gallacher/

- Economist: Who will be the next chair of the Federal Reserve?: “The interest-rate opinions of the favourite to succeed her are less clear. Mr Cohn… https://www.economist.com/news/finance-and-economics/21726081-gary-cohn-leading-candidate-replace-janet-yellen-who-will-be-next

- Fabio Ghironi: Micro Needs Macro: “An emerging consensus on the future of macroeconomics views the incorporation of a role for financial intermediation, labor market frictions, and household heterogeneity in the presence of uninsurable unemployment risk as key needed extensions to the benchmark macro framework… http://faculty.washington.edu/ghiro/GhiroFuture.pdf

- Nancy MacLean: Democracy in Chains: The Deep History of the Radical Right’s Stealth Plan for America http://amzn.to/2voi3qD: “As 1956 drew to a close, Colgate Whitehead Darden Jr., the president of the University of Virginia, feared…

Interesting Reads:

- Note to Self: Data Science Reading List

- John Tukey: The Future of Data Analysis: “Large parts of data analysis are inferential… but only parts…. Large parts… are incisive…. Some parts… are allocative… dude its in the distribution of effort…” http://projecteuclid.org/DPubS?service=UI&version=1.0&verb=Display&handle=euclid.aoms/1177704711

- Leo Breiman: Statistical Modeling: The Two Cultures: “The data are generated by a given stochastic data model… [vs.] algorithmic models… treat[ing]… the data mechanism as unknown. The statistical community[‘s]… commit[ment]… to… models… has led to irrelevant theory, questionable conclusions, and has kept statisticians from working on a large range of interesting current problems…” http://projecteuclid.org/euclid.ss/1009213726

- Ben Fry: computational information design: “Fields such as information visualization, data mining and graphic design… each solv[e]… an isolated part of the specific problem but fail… in a broader sense…. This dissertation proposes that the individual fields be brought together as part of a singular process titled Computational Information Design…” http://benfry.com/phd/

- Hal Varian: How the Web challenges managers: “There’s already been a big revolution in how we view intellectual property…. It’s not so much the question of what’s owned or what’s not owned. It’s a question of how can you leverage the assets you have to realize the most value…. Disseminating content… has become intensely competitive…” http://www.mckinsey.com/industries/high-tech/our-insights/hal-varian-on-how-the-web-challenges-managers

- Drew Conway: The Data Science Venn Diagram http://www.dataists.com/2010/09/the-data-science-venn-diagram/: “The primary colors of data: hacking skills, math and stats knowledge, and substantive expertise…”

- Gil Press: A Very Short History Of Big Data: “1944 Fremont Rider… publishes The Scholar and the Future of the Research Library…: https://www.forbes.com/sites/gilpress/2013/05/09/a-very-short-history-of-big-data/#6e3a8ee465a1

- Gil Press: A Very Short History Of Data Science: “The term “Data Science” has emerged only recently to specifically designate a new profession that is expected to make sense of the vast stores of big data. But making sense of data has a long history and has been discussed by scientists, statisticians, librarians, computer scientists and others for years…” https://www.forbes.com/sites/gilpress/2013/05/28/a-very-short-history-of-data-science/#3a3f6c7955cf

- Jean Mark Gawron: Python for Social Science http://gawron.sdsu.edu/python_for_ss/course_core/book_draft/index.html

- Lucy Hornby: Chinese crackdown on dealmakers reflects Xi power play: “Beijing aims for more control over the economy by curbing outbound M&A, while helping the president erode the support of rivals…” https://www.ft.com/content/ed900da6-769b-11e7-90c0-90a9d1bc9691

- Adrianna McIntyre, Allan M. Joseph, M.P.H., and Nicholas Bagley: Small Change, Big Consequences — Partial Medicaid Expansions under the ACA http://www.nejm.org/doi/full/10.1056/NEJMp1710265

- Simon Wren-Lewis: Real wages are mainly a macro issue https://mainlymacro.blogspot.co.uk/2017/08/real-wages-are-mainly-macro-issue.html

- Gillian Tett: The next crash risk is hiding in plain sight: “If we want to avoid a replay of 2007, we must keep questioning our assumptions—and peering at the parts of the system that seem ‘boring’, ‘geeky’ and ‘dull’…” https://www.ft.com/content/a859449e-7daf-11e7-ab01-a13271d1ee9c

- Information Technology and the Future of Society http://www.bradford-delong.com/2017/08/information-technology-and-the-future-of-society.html

- Live from Cyberspace: The elective affinity between fantasy and computer programming: Paul Dourish: THE ORIGINAL HACKER’S DICTIONARY: “WIZARD n. 1. A person who knows how a complex piece of software or hardware works…” http://www.bradford-delong.com/2017/08/live-from-cyberspace-the-elective-affinity-between-fantasy-and-computer-programming-paul-dourish-the-original-hac.html

- Weekend Reading: Paul Romer (2016): The Trouble with Macroeconomics: “Macroeconomic theorists dismiss mere facts by feigning an obtuse ignorance about such simple assertions as ‘tight monetary policy can cause a recession’. Their models attribute fluctuations in aggregate variables to imaginary causal forces that are not influenced by the action that any person takes…” http://www.bradford-delong.com/2017/08/weekend-reading-paul-romer-2016-the-trouble-with-macroeconomics.html

- Note to Self: “Data Science” as an Ephemeral Term: There was a time—perhaps a century, maybe a bit more, certainly not much less—ago, when the high-tech bleeding edge electricity sector was an important but discrete part of the “economy”… http://www.bradford-delong.com/2017/08/note-to-self-_data-science-as-an-ephemeral-term_there-was-a-timeperhaps-a-century-maybe-a-bit-more-certainly-not.html

- Note to Self: I am told that what we are doing here is something called “data science”: I find myself feeling somewhat surprised—like the “Middle-Class Aristocrat” title character in 1600s-era French playwright Moliêre’s Le Bourgeois Gentilhomme…” http://www.bradford-delong.com/2017/08/note-to-self-i-am-told-that-what-we-are-doing-here-is-something-called-data-science.html

- Note to Self: Data Science Reading List http://www.bradford-delong.com/2017/08/note-to-self-data-science-reading-list-john-tukey-the-future-of-data-analysis-large-parts-of-data-analysis-ar.html

- Note to Self: View jupyter notebook from dropbox (or other) links: Dropbox: change: “https://www.dropbox.com/” to: “http://nbviewer.jupyter.org/urls/dl.dropbox.com/”; then load the url… Else: change: “https://” to “http://nbviewer.jupyter.org/”; then load the url… http://www.bradford-delong.com/2017/08/note-to-self-view-jupyter-notebook-from-dropbox-or-other-links-dropbox-change-httpswwwdropboxcom-to-ht.html