Equitable Growth hosts Hill briefing on proliferation and taxation of U.S. pass-through businesses

On March 7, the Washington Center for Equitable Growth hosted a briefing—part of a series we call “Econ 101”—for Hill staffers curious about the proliferation of pass-through businesses and how tax breaks for such businesses could affect start-up investment, job creation, and workers’ earnings in the United States. The briefing was led by Equitable Growth’s Senior Fellow for Tax and Regulatory Policy David S. Mitchell and Max Risch, assistant professor at Carnegie Mellon University.

Lawmakers are engaged in fierce ongoing debates related to expiring provisions of the Tax Cuts and Jobs Act of 2017, including tax deductions for pass-through business owners. These pass-through firms have become increasingly common in the United States in recent decades, and a concurrent decline in IRS resources means the audit rate for pass-throughs has dropped to historic lows.

Mitchell began the briefing with an explanation of the basics of pass-throughs, contrasting their various types—sole proprietorships, S-corporations, and partnerships—and showing how legislative changes since 1986 have promoted their use. Partnerships in particular have grown rapidly as a preferred form of firm organization for finance and real estate investors seeking to take advantage of complex ownership networks to reap tax benefits. Partnerships account for at least a quarter of U.S. net business income, while pass-throughs altogether comprise more than half of net income.

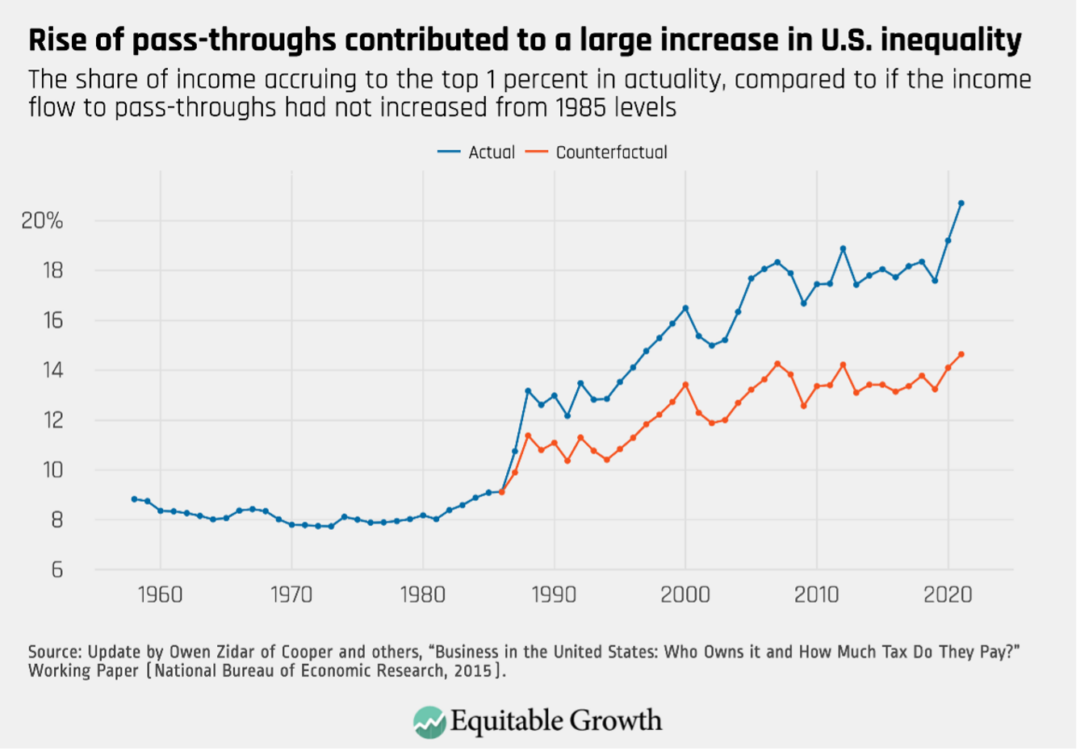

The essential feature of pass-throughs—that firm tax costs and benefits are funneled to owners rather than assessed at the firm level—means changes to the personal income tax regime could directly address distributional issues caused by the proliferation of partnerships. As Risch explained in the briefing, partnerships are often large businesses—nearly 40 percent are firms with more than 100 employees—whose gains accrue overwhelmingly to the top 1 percent of U.S. earners. In fact, income inequality would be significantly lower without the proliferation of pass-through businesses, as they account for about a quarter of the growth in income share accruing to the top 1 percent. (See Figure 1.)

Figure 1

The briefing then focused on key legislative provisions of the expiring Trump tax cuts, including the qualified business income deduction, also known as Section 199A, which almost exclusively benefitted top U.S. earners and businesspeople. Mitchell highlighted several pieces of recent research showing how the introduction of Section 199A incentivized unproductive tax game-playing, including artificially modifying salaries to maximize income tax deductions. Other key provisions addressed by Mitchell include payroll taxes and carried interest—both of which are highly gameable within the partnership legal framework. Many of these tax strategies work to keep pass-through businesses artificially small and capital-constrained, with questionable value for the broader U.S. economy.

Finally, Risch tackled the questions of tax evasion and avoidance, showing how changes to reporting requirements for large complex partnerships could improve the federal fiscal outlook and reduce inefficient gaming of tax rules. Risch also spoke in favor of fully funding the IRS, particularly its Pass-Through Compliance Unit and Large Partnership Compliance Program, and introducing a user fee for partnerships above a certain level of complexity.

The Econ 101 event was the first of two business-tax-themed briefings for Hill staffers amid the ongoing tax and budget debate in 2025. The second, scheduled for March 28, will focus on taxing multinational corporations. These events follow a series of Econ 101s hosted in the fall of 2024 on the complexities of the U.S. tax code and the implications of tax policy for economic growth.

Review the presentation slides from the March 7 Econ 101 to learn more.

Did you find this content informative and engaging?

Get updates and stay in tune with U.S. economic inequality and growth!