Doctor checking blood pressure of his patient by mangostock, veer.com

One of the promises of economic growth and advancement is that things will get better for everyone. A rising tide is supposed to lift all boats, even if we’ve acknowledged that some boats have risen higher lately. But a new study shows that this promise isn’t always fulfilled—and that sometimes, things can actually get worse. The paper, written by Princeton University economists Anne Case and Angus Deaton (the recent winner of the Nobel Prize), shows an increasing mortality rate for white Americans ages 45 to 54 since 2000. In other words, a middle-aged white person was more likely to die in 2013 than they were in 1999. This alarming new health trend coincides with a multitude of economic data documenting increasing economic insecurity over this same period—something the authors comment on in their paper and in reports about their findings.

Indeed, this health reversal stands in stark contrast to the trends in mortality prior to the start of this century. According to Case and Deaton, the mortality rate fell considerably for middle-aged Americans from 1978 to 1998. For middle-aged whites, the rate fell on average by 2 percent a year. This trend was quite similar to declines in other high-income economies like those in Western Europe. But in 1999, the mortality rates for middle-aged white workers in the United States begin to increase, in contrast to their European counterparts whose death rates continued to fall.

What’s more, the self-reported rate of morbidity—the frequency of sickness or disease—has also increased among American middle-aged white workers since 1999. They are much more likely to report their physical health as “not good” and that they are in pain. Such health problems put these men more at risk for mental health problems and heavy drinking.

What’s at the root of these huge problems for middle-aged white Americans? A likely cause, which Case and Deaton flagged, is a rise in general chronic pain among this population. The same time period (1999–2013) saw an increase in the use of opioids, first in the form of prescription drugs and increasingly in the form of heroin. The report doesn’t specify, however, whether the increase in self-described pain came first or if the increased use of opioids did. Either way, the increased amount of pain also shows up in higher suicide rates and alcohol abuse.

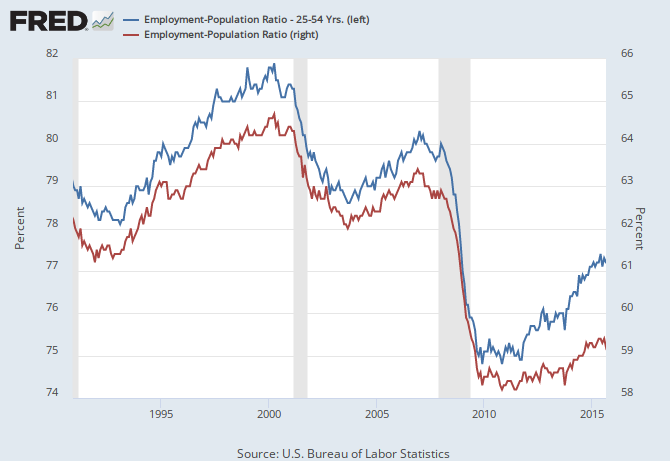

It’s very likely that increased economic insecurity since 1999 has been a factor in driving these health problems. In a Wall Street Journal article this week, Case notes that the inflation-adjusted median household income for high-school educated whites peaked in 1999. The downward trend in median household income that followed isn’t just for those with a high school degree—the median household income for all white Americans peaked in 2000, and the median market income for all households peaked in 1999 according to the Congressional Budget Office. At the same time, the share of white 45- to 54-year-olds with a job reached its zenith in 2000, just like the overall U.S. employment rate and the employment-to-population ratio for all prime-age workers. Of course, these declines in income and employment are happening to all racial groups, so they can’t be the sole cause of rising mortality for whites. But they certainly seem to be a major contributor.

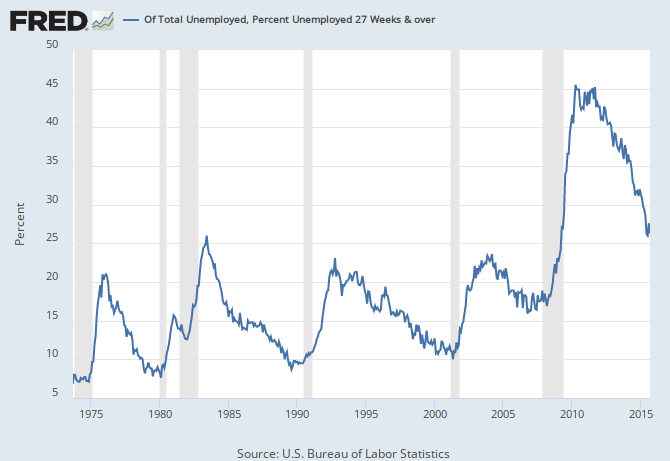

This last trend and the increased pain among the U.S. population could also help explain both the rising number of workers on disability insurance and part of the decline in the U.S. labor force participation rate. Case and Deaton’s results, if they hold up, would show that rising disability claims aren’t due to workers being attracted to more generous benefits, but rather because they are increasingly unable to actually work.

On a number of fronts, the startling results from Case and Deaton’s research should cause us to think deeply about what’s been happening in the U.S. economy during this new century.

{kind=link}

{kind=link}