- : Spring 2016 BPEA

- : Are Central Banks Really Out of Ammunition?

- : A World Stumped by Stubbornly Low Inflation

- : Reality Check for the Global Economy

Category: Equitablog

Must-read: Jan Eberly and Jim Stock: “Spring 2016 BPEA”

Must-Read: : Spring 2016 BPEA: “We have arranged the following program…

…Jesse Bricker [et al.]… on ‘Measuring Income and Wealth at the Top Using Administrative and Survey Data’. David M. Byrne [et al.]… on ‘Does the United States have a Productivity Problem or a Measurement Problem?’. Alberto Cavallo [et al.]… on ‘Learning from Potentially Biased Statistics: Household’s Inflation Perceptions and Expectations in Argentina’. Melissa Kearney… and Phillip Levine… on ‘Income Inequality, Social Mobility, and the Decision to Drop Out of High School’. Deborah Lucas… on ‘Credit Policy as Fiscal Policy’. Raven Molloy [et al]… on ‘Understanding Declining Fluidity in the U.S. Labor Market’…

Must-read: Adair Turner: “Are Central Banks Really Out of Ammunition?”

Must-Read: : Are Central Banks Really Out of Ammunition?: “The global economy faces a chronic problem of deficient nominal demand…

…But the debate about which policies could boost demand remains inadequate, evasive, and confused. In Shanghai, the G-20 foreign ministers committed to use all available tools – structural, monetary, and fiscal – to boost growth rates and prevent deflation. But many of the key players are keener to point out what they can’t do than what they can….

Central banks frequently stress the limits of their powers, and bemoan lack of government progress toward ‘structural reform’…. But while some [SR measures] might increase potential growth over the long term, almost none can make any difference in growth or inflation rates over the next 1-3 years…. Vague references to ‘structural reform’ should ideally be banned, with everyone forced to specify which particular reforms they are talking about and the timetable for any benefits that are achieved…. Central bankers are right to stress the limits of what monetary policy alone can achieve…. Negative interest rates, and… yet more quantitative easing… can make little difference to real economic consumption and investment. Negative interest rates… [may have the] the actual and perverse consequence… [of] higher lending rates….

Nominal demand will rise only if governments deploy fiscal policy to reduce taxes or increase public expenditure – thereby, in Milton Friedman’s phrase, putting new demand directly ‘into the income stream.’ But the world is full of governments that feel unable to do this. Japan’s finance ministry is convinced that it must reduce its large fiscal deficit…. Eurozone rules mean that many member countries are committed to reducing their deficits. British Chancellor of the Exchequer George Osborne is also determined to reduce, not increase, his country’s deficit. The standard official mantra has therefore become that countries that still have ‘fiscal space’ should use it. But there are no grounds for believing the most obvious candidates – such as Germany – will actually do anything….

These impasses have fueled growing fear that we are ‘out of ammunition’…. But if our problem is inadequate nominal demand, there is one policy that will always work. If governments run larger fiscal deficits and finance this not with interest-bearing debt but with central-bank money…. The option of so-called ‘helicopter money’ is therefore increasingly discussed. But the debate about it is riddled with confusions.

It is often claimed that monetizing fiscal deficits would commit central banks to keeping interest rates low forever, an approach that is bound to produce excessive inflation. It is simultaneously argued (sometimes even by the same people) that monetary financing would not stimulate demand because people will fear a future ‘inflation tax.’

Both assertions cannot be true; in reality, neither is. Very small money-financed deficits would produce only a minimal impact on nominal demand: very large ones would produce harmfully high inflation. Somewhere in the middle there is an optimal policy…. The one really important political issue is ignored: whether we can design rules and allocate institutional responsibilities to ensure that monetary financing is used only in an appropriately moderate and disciplined fashion, or whether the temptation to use it to excess will prove irresistible. If political irresponsibility is inevitable, we really are out of ammunition that we can use without blowing ourselves up. But if, as I believe, the discipline problem can be solved, we need to start formulating the right rules and distribution of responsibilities…

Must-read: Larry Summers: “A World Stumped by Stubbornly Low Inflation”

Must-Read: : A World Stumped by Stubbornly Low Inflation: “[The 1970s taught us that] allowing not just a temporary increase in inflation but a shift to above-target inflation expectations could be very costly…

…At present we are… in a world that is the mirror image…. Market measures of inflation expectations have been collapsing and on the Fed’s preferred inflation measure are now in the range of 1-1.25 per cent over the next decade. Inflation expectations are even lower in Europe and Japan…. The Fed’s most recent forecasts call for interest rates to rise almost 2 per cent in the next two years, while the market foresees an increase of only about 0.5 per cent. Consensus forecasts are for US growth of only about 1.5 per cent for the six months from last October to March. And the Fed is forecasting a return to its 2 per cent inflation target on the basis of models that are not convincing to most outside observers….

In a world that is one major adverse shock away from a global recession, little if anything directed at spurring demand was agreed. Central bankers communicated a sense that there was relatively little left that they can do to strengthen growth or even to raise inflation. This message was reinforced by the highly negative market reaction to Japan’s move to negative interest rates. No significant announcements regarding non-monetary measures to stimulate growth or a return to target inflation were forthcoming, either…. Today’s risks of embedded low inflation tilting towards deflation and of secular stagnation… will require shifts in policy paradigms if they are to be resolved. In all likelihood the important elements will be a combination of fiscal expansion drawing on the opportunity created by super low rates and, in extremis, further experimentation with unconventional monetary policies.

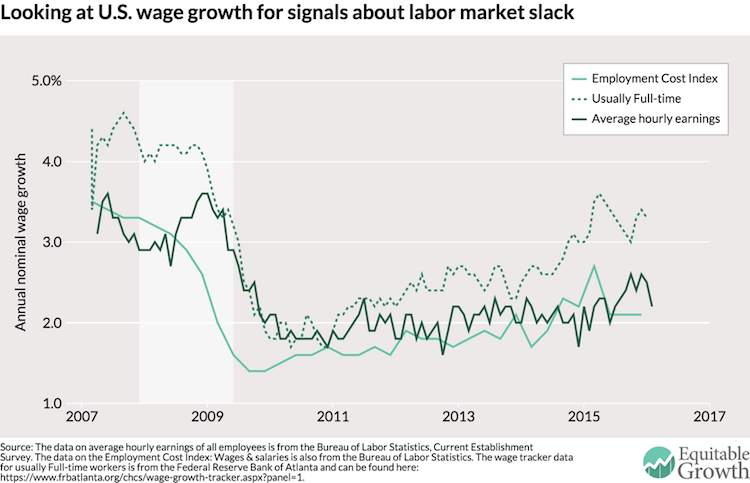

Is weak U.S. wage growth all because of who’s getting jobs?

The weak wage growth in the United States continues to confound some economists. Although the U.S. unemployment rate is under 5 percent—many economists’ estimate for the lowest possible rate of unemployment that won’t trigger accelerating inflation—U.S. wage growth is far from robust. And while the traditional Phillips curve would have us believe that high wage growth is right around the corner, it hasn’t arrived yet. Perhaps this is because the unemployment rate isn’t as good a measure of labor market slack as in the past. Or, as a new article from the Federal Reserve Bank of San Francisco argues, it may be because the composition of workers in the labor market is pushing down measured wage growth.

Why would the change in the composition of workers over time affect the measurement of wage growth? Consider the changes in the percentage of the workforce in certain occupations. Let’s say a lot of jobs are created in high-paying occupations over the course of an economic recovery. The workforce would then have a higher average wage, because more workers would be in higher-paying jobs, but that tells us nothing about the pace of wage growth within occupations. While the average wage growth would be high, wage growth for workers in those occupations might have been quite low.

Our nominal measures of wages and wage growth, such the Current Establishment Survey’s average hourly earnings, don’t account for changes in worker composition. But the Employment Cost Index tries to account for this issue by holding the occupational mix of workers constant at some ratio in the past and then measuring the pace of wage growth for that combination.

That’s not the only kind of compositional issue that might affect measured wage growth, however. In an economic letter for the San Francisco Fed, Mary Daly and Benjamin Pyle of the bank and Bart Hobijn of Arizona State University argue that other compositional effects need to be considered as well. First, there’s the Baby Boomers. The increase in retirement means that older workers, who are disproportionately higher-wage earners, are no longer included in the average wage, which will push down measured average wage growth. At the same time, many workers are moving from involuntary part-time work to full-time work. Because most of these new full-time jobs are relatively low-wage jobs, that will also pull down measured wage growth.

What should we look at then to understand wage growth? Daly, Hobijn, and Pyle argue for a measure that looks at the wage growth of workers who are continuously employed full-time. Luckily, the Federal Reserve Bank of Atlanta produces just such a metric. Note that this measure tracks a specific worker over time, so it’s not a cross-sectional measure like others that look at wage growth. The graph below shows annual wage growth according to the Atlanta Fed wage growth tracker for “Usually Full-time” workers, the Employment Cost Index, and the average hourly earnings for all private-sector workers from the Current Establishment Survey.

The wage tracker shows that wage growth ticked up in 2014 and is much higher than even the Employment Cost Index measure, which controls for the composition of occupations. Wage growth for usually full-time workers, however, seems to have decelerated in the second half of 2015. Also note that while the wage tracker data shows stronger wage growth, nominal wage growth for usually full-time workers is still below its pre-recession levels.

But it’s still not clear that only focusing on the constantly employed is necessarily a better indicator of labor market slack. If more workers are getting pulled into full-time employment, that’s a sign there’s still labor market slack. And the resulting lower wage growth would still be a sign of remaining labor market slack. Maybe these different wage measures are picking up the decline in different kinds of labor market slack, or stages of slack.

First, slack declines enough that already-employed workers start to see increases in their wages and earnings. That increase induces employers to find part-time workers who’d like a full-time job or even workers outside the labor force. Looking at measures like the Atlanta Fed’s may tell us about the progression through this first stage, and then the level of wage growth according to more traditional measures could tell us about the second stage. The first is a signal that slack is starting to abate, and the second is a signal that it’s mostly gone.

But when it comes to the most important question of the moment, most measures indicate that labor market slack still remains. The labor market is getting stronger, but it’s still not strong.

Must-read: Olivier Blanchard et al.: “Reality Check for the Global Economy”

: Reality Check for the Global Economy: “After five years of disappointing recovery throughout the major economies…

…almost everyone is ready to believe the worst. The widespread large declines in global asset prices indicate a significant divergence between what financial markets fear and what most mainstream macroeconomic forecasts are showing for the world economy. Having some clarity to distinguish between the more solid underlying economic outlook and the shadows thrown by financial puppetry is critical to avoid an unnecessary recession.

In this Briefing, a group of PIIE scholars came together to provide a reality check for the global economy. They set out what is known, both about macroeconomic dynamics and policy capabilities, in a context where distrust of both mainstream economic analysis and policymakers’ credibility has become excessive. Global economic fundamentals today are not so grim, though there is room for improvement in key areas including China, the United States, European banks, Brazil and Latin America, oil markets, global trade, and monetary policy options.

In particular, we argue: The relative forecasting ability of financial markets for the real economy has probably gone down postcrisis (Adam S. Posen). The US economy remains at a relatively low, though slightly elevated, risk of recession (David Stockton). The positive effects of the decline in the price of oil on the US economy have taken longer to materialize than was expected, but they will strengthen looking forward (Olivier Blanchard and Julien Acalin). Chinese economic growth is, at a minimum, well above current fear-driven estimates, and that growth is predominantly service sector–based and therefore sustainable (Nicholas Lardy). The slowdown in growth of global trade reflects weak global investment and a medium-term adjustment to the past creation of global supply chains and is not a harbinger of further contraction (Caroline Freund). The European banking system is in transition to a stronger state, and the problems evident in Italy are not enough to throw Europe’s economy off course (Nicolas Véron). Brazil’s economy while dysfunctional is far more likely to experience years of higher inflation than any overt fiscal or balance of payments crisis (Monica de Bolle). Latin America more generally has run into problems of slow productivity growth but is not doomed by the commodity cycle (José De Gregorio). Monetary policy remains potent, with multiple possible avenues for additional stimulus if needed, starting with effective quantitative easing on private assets (Joseph Gagnon).

What’s your college degree worth? It may depend on your parents’ income

Education is supposed to be a silver bullet. A great equalizer when it comes to income inequality, and a boost to flagging wages and incomes. But higher levels of education alone may not be able to reduce income inequality. While increasing the share of so-called “marginal students” attending college would have a positive return, it’s unclear just how large that return would be. And the return to higher education may also vary by how much a student’s parents earn.

In a column for the Brookings Institution, Brad Hershbein of the W.E. Upjohn Institute for Employment Research lays out some surprising results on the lifetime earnings of U.S. workers from different family backgrounds. Specifically, he and his colleagues looked at the lifetime earnings measured by the Panel Study of Income Dynamics for workers who grew up in families with incomes above and below 185 percent of the federal poverty level (about $45,000 for a family of four in 2016).

Unsurprisingly, workers with college degrees earn more than workers with just high school degrees, regardless of family background. College grads from families with incomes below 185 percent of the poverty line make more than than high school grads from the same income background, and the same for those from families well above the poverty threshold. But the boost from a college degree varies by background.

College grads from lower-income backgrounds (specifically families with incomes below the 185 percent threshold) earn 91 percent more over the course of their career than high school grads from the same background. But college grads coming from families that were well above poverty (or families earning above the 185 percent threshold) make 162 percent more than high school grads from the same background. So the return on a college degree is significantly higher for a student who grew up far away from poverty.

In other words, if you were to interpret these results as the causal effect of a college degree, a college degree boosts the earnings of students from low-income backgrounds, but college grads from higher-income backgrounds pull away from them as they get a larger boost. Incomes for both groups go up, but inequality rises.

Hershbein notes that he and his colleagues are now trying to dig into the reasons for this differential rate of return on college and making sure the trend holds up in other data sources. If the trend does hold up, understanding the causes will be incredibly important. If we want higher education to be a growth-enhancing and equalizing policy tool, we have to understand how to make sure that students from low-income backgrounds get the same—or perhaps even greater—rate of return.

Must-read: Justin Fox: “The U.S. Could Use a New Economic Strategy”

Must-Read: Some very nice thoughts about our Concrete Economics from the extremely-sharp Justin Fox:

: The U.S. Could Use a New Economic Strategy: “In his four-plus years as the country’s first treasury secretary…

…Alexander Hamilton crafted an economic strategy that helped the U.S. rise from agrarian former colony to global economic power… [write] Stephen S. Cohen and J. Bradford DeLong write in their brand-new book, Concrete Economics: The Hamilton Approach to Economic Growth and Policy…. No U.S. leader since has articulated and then put in place an all-encompassing economic plan in quite the way Hamilton did. But the country has always followed some sort of economic strategy, even if it has seldom been clearly defined…. It is at least possible that this last era has come to an end…. It’s not at all clear, though, what’s going to replace it.

DeLong… and Cohen… simply recommend that discussion of economic policy focus on the concrete–what works…. Still, it’s not easy to figure out what the U.S. should do next. Nations playing catch-up… have concrete examples…. But the U.S. of 2016 is the biggest economy on the planet…. In the latest World Economic Forum global competitiveness rankings, for example, it trailed only Switzerland and Singapore. There is surely much we can learn… but… the U.S. remains largely sui generis. I’m almost certain that more infrastructure investment would be a smart part of any new U.S. economic strategy. But I’m not so sure what should be built and where, or what else…. Got any suggestions?…

I would say that our book has two big lessons to teach. The first is that, in America, economic policy has been successful when it has been pragmatic. Hamilton is our first example. But “Hamiltonianism” is not the right economic policy configuration for the ages. The United States did not stay with Hamilton’s policy configuration. The post-Civil War Gilded Age’s focus on homesteading, truly massive infrastructure subsidies, and mass immigration had little to do with Hamilton’s debt, finance, bank, tariff, and manufacturing focus. The Progressive Era had different concerns and policies. As did the other Roosevelt’s New Deal. As did Eisenhower. And our recent age–which Justin Fox calls “financialization”, but which we might as well call “neoliberalism” (it’s what everyone else calls it)—has been broadly unsuccessful not because it has deviated from Hamiltonianism but because it has been ideological.

Must-reads: March 9, 2016

- : Uncertainty Principles: ‘The End of Alchemy’, by Mervyn King

- : The ‘Strong Case’ Critically Examined

- : A New Deal for Europe

- : Fiscal and Financial Crises

- : Asian Growth in Turbulent Times

- : The Economics of Analyzing the TPP

- : “The speed at which producer surplus changes to consumer surplus has accelerated since software is non rival & non excludable.”

- : Demographics and Productivity

- : Google discovers the key to good teamwork is being nice

Must-read: John Plender: Uncertainty Principles: ‘The End of Alchemy’, by Mervyn King

Must-Read: : : “King’s hugely ambitious aim in his book is to put an end to the alchemy…

…that has made financial crises a permanent feature of the landscape and allowed money — a public good — to become the byproduct of credit creation by private-sector banks. Above all, he argues that the crisis of 2007-09 reflected not just a failure of individuals or institutions, but a failure of the ideas that underpin current economic policymaking…. King argues that in a world of what economists now call ‘radical uncertainty’… there is simply no way of identifying the probabilities of all future events and no set of economist’s equations that describe people’s attempts to cope with that uncertainty…. In King’s terms, the coping strategy of households, businesses and investors involved adopting a narrative of stability while the level of spending ran at unsustainably high levels….

Western consumers’ urge to spend was not strong enough to offset the greater urge of northern Europeans and Asians to save, [so] global interest rates fell. Banks then satisfied investors’ desperate search for income by creating increasingly complex and risky financial products…. Bank balance sheets grew explosively…. The financial crisis changed the narrative. In King’s estimation, policymakers were right to adopt a Keynesian stimulatory response in 2008-9…. They averted a repetition of the Great Depression but, in doing so, created what King calls a paradox of policy. Interest rates today, he says, are too high to permit rapid growth of demand in the short run but too low to be consistent with a proper balance between spending and saving in the long run….

King argues that Bagehot’s famous dictum on central bank crisis management — lend freely on good collateral at penalty rates — is out of date because bank balance sheets today are much larger and have fewer liquid assets than in the 19th century. Central banks are thus condemned in a crisis to take bad collateral in the shape of risky, illiquid assets on which they will lend only a proportion of the value, known as a haircut…. King suggests this lender of last resort role should be replaced by what he calls, with a pleasing irreverence towards central banking mystique, a pawnbroker for all seasons…. Banks would decide how much of their asset base to lodge in advance at the central bank to be available for use as collateral. For each asset, the central bank would calculate a haircut…. The system would displace what King regards as a flawed risk-weighted capital regime ill-suited to addressing radical uncertainty…