Must-Read: No, I do not know anyone who thinks this is correct. The Rubin wing of the Democratic Party thinks, today, that it paid much too little attention to policies to stem the growth of inequality in the 1990s, and that for the late 2010s and 2020s we need to focus on growth and distribution–on, in a phrase, equitable growth:

[Nick Timiraos:] Economic Policy Splits Democrats, WSJ: The old guard… that laid the groundwork for… a two-term president watches with unease…. That alarm shines through in a new 52-page report from centrist Democratic think tank the Third Way…. “The right cares only about growth, hoping it will trickle down,” says Jonathan Cowan, president of Third Way. The left, meanwhile, is too focused on “redistribution to address income inequality.”… “This country is in real trouble,” Ms. Warren said at the May event. “The game is rigged and we are running out of time.” That kind of rhetoric gives Mr. Cowan fits because he says it isn’t a winning political message…. Third Way cites the failures of main street icons such as Kodak, Borders Books and Tower Records as proof that new technologies and delivery systems, as opposed to a “stacked deck” in Washington, are primarily responsible for economic upheaval…

Tower Records explains inequality? Seriously?… So, should I adopt a message I don’t think is true because it sells with independents who have been swayed by Very Serious People?… I’d rather convince people of the truth that more growth and more wealth creation won’t solve the problem if we don’t address workers’ bargaining power at the same time than gain their support by patronizing their views…. Maybe politicians have to tell people what they want to hear, I’ll let them figure that out, but I will continue to call it as I see it…

Let me point out that, to the extent one recognizes even the possibility of hysteresis or superhystesis, obvious optimal control policy when you approach the zero lower bound is to dial up current monetary expansion to the max and call for more fiscal expansion as well. The long-run damage from not generating a V-shaped recovery in the short-run is then immense, and you always dial policy down to be less expansionary should it look like you were about to overshoot. Yet such arguments had no purchase in the Bernanke Fed or the Geithner Treasury, and little inside the Obama White House.

I must confess that I have never understood why people ever thought it reasonable to believe that the pace of potential output growth was the same in a low pressure as an high-pressure economy. And, indeed, it is not:

…than where output returns to trend. In other words ‘super hysteresis,’ to use Larry Ball’s term, is more frequent than ‘no hysteresis.’… We look at… recessions with different precursors. We find that even recessions that are associated with disinflationary monetary policies or the drying up of credit have substantial long-run output effects–suggesting the presence of hysteresis effects…. [Moreover,] fiscal policy changes have large continuing effects on levels of output suggesting the importance of hysteresis…

But we knew all this back in 1936, no? John Maynard Keynes:

…[is] the only practicable means of avoiding the destruction of existing economic forms in their entirety and as the condition of the successful functioning of individual initiative…. If effective demand is deficient, not only is [there] the public scandal of wasted resources… but the individual enterpriser… is operating with the odds loaded against him… many zeros, so that the players as a whole will lose if they have the energy and hope to deal all the cards. Hitherto the increment of the world’s wealth has fallen short of the aggregate of positive individual savings; and the difference has been made up by the losses of those whose courage and initiative have not been supplemented by exceptional skill or unusual good fortune. But if effective demand is adequate, average skill and average good fortune will be enough…

Only in a high-pressure economy, Keynes says, will the “increment of wealth”–the value of productive capital and organizations created–match “the aggregate of positive individual savings”–the amount of resources devoted to trying to boost productive capacity. In a low-pressure economy, a lot of investments that could pay off from a tastes-and-technologies standpoint won’t because of slack demand, and so perfectly-productive factories and organizations will be scrapped and shut down.

And we have to add on to this the perspective, derived from Granovetter, that a great deal of the societal resource-allocation capital of the labor market is the social network of loose ties generated that nobody gets paid for, and is thus a spillover; the perspective, derived from Saxenian, that a great deal of the societal resource-allocation capital of the value chain is the social network of overlapping communities of engineering practice generated that nobody gets paid for, and is thus a spillover; and the perspective derived from Hayek that a great deal of the societal resource-allocation capital of the price system is the revelation by market prices of societal scarcities and values that nobody could calculate on their own, and that nobody gets paid for generating, and is thus a spillover. Externalities all over the place here!

The question is: why did people ever assume otherwise? Yes, a linear Phillips Curve is simple to work with. Yes, the assumption that the rate of inflation expected next year is simply actual inflation last year seems like a not unreasonable rule-of-thumb. But you have to put very great weight on both–weight that the past decade has conclusively proven they cannot bear–to even conclude the business cycles are fluctuations around rather than falls below sustainable levels of production. And you are still absolutely nowheresville with respect to the invariance of potential growth to cyclical conditions.

…of human capital. It is not at all clear that this kind of human capital can (or will) be created by MOOCs, self-study, or other forms of online learning that are being touted as replacements for college. In fact, right now it looks like the health-related human capital boost from college is all that is holding it together for our upper middle class.

Must-Read: It is genuinely surprising to me that Kevin Murphy thinks that Katz and Murphy (1992) is still close to the last word on inequality. And it is beyond genuinely surprising that Steve Durlauf thinks that Bill Gates’s wealth was acquired by merit and John D. Rockefeller’s by monopoly when they are both winners in gigantic winner-take-all natural-monopoly markets–a natural-monopoly created by economies of scale in refining and distribution in the case of oil, and by write-once run-everywhere protected by patent and copyright in the case of operating systems:

…with Jim Heckman acting as moderator…. [Murphy] thinks that his 1992 paper with Lawrence Katz, which tried to explain the dynamics of the college wage premium in the 1970s and 1980s with reference to the supply and demand for skilled labor in the form of workers with a college degree, constitutes the final word… [even though] its model fails at explaining… labor market outcomes… since… [and relies on the residual of] skills-biased technical change: the Ghost in the Free Market Economics Machine….

Piketty started things off by claiming that… globalization and skill-biased technical change… don’t explain the phenomena… closed with what I consider a profound restatement of why Capital in the 21st Century is such an important book:

The gap between [the] official discourse and what’s actually going on is enormous. The tendency is for the winner to justify inequality with meritocracy. It’s important to put these claims up for public discussion.

Durlauf… said, quite reasonably, that the key mechanism of inequality is segregation, because it translates individual inequality into entrenched deprivation, and that its policy implications are therefore to foster integration in a variety of contexts….

Murphy’s presentation was where the wheels came off, intellectually speaking. He declared… by regurgitating his 1992 paper… [saying] “that theory has done an amazing job,” including a cryptic statement about how it explains the rise of tail inequality “if you extrapolate,” whatever that means…. Murphy stepped forward once again to declare that the economy’s “natural supply response of supplying capital” will help workers by reducing the capital share and increasing their productivity…. Durlauf asserted in his JPE review of C21 that no one thinks like Clark anymore, with his quasi-moralistic view of the efficient functioning of capital formation and the adjustment of its rate of return. Unfortunately, Durlauf’s empirical prediction was falsified by Murphy right there on that stage…. Murphy added that in the absence of better education, “The march of technology over time means there’s little for someone with no human capital to do.”… Then things got weird. Durlauf… [said] what mattered was [Americans’] perception of [inequality’s] source: whether justified by merit, as in the case of Bill Gates, or extracted through monopolization, as with John D. Rockefeller. At that, Piketty quipped that Bill Gates certainly agrees….

Murphy[‘s]… idea seems to be that the poor, benighted though they are, will adopt the morally correct position of looking out for their own interest by acquiring an education, so long as the incentive to do so is preserved by avoiding progressive taxation. Usually the fallacy in the moral philosophy of economics… is to argue that whatever reality exists is for the best…. In this case, though, the “ought” is a priori: people should be selfish. For that reason, they probably will be, so long as the status quo is maintained as an instructive lesson in the disaster befalling anyone not born rich…. Durlauf made a final, inscrutable point… saying that we should directly address the harms caused by inequality, by which he was referring to capture of the political system by the wealthy…

Two weeks ago, New York University economist Michael Spence and former Federal Reserve governor Kevin Warsh published an op-ed in the Wall Street Journal about U.S. monetary policy that provoked a spirited response. They argued that quantitative easing—the Federal Reserve’s program of buying long-term bonds and mortgage securities—actually depressed business investment instead of boosting it. (Former Treasury Secretary Larry Summers and our own Brad DeLong were, in a word, confused by this line of thinking.)

While Spence and Warsh’s logic does seem flawed, business investment growth has been quite weak over the course of this recovery. Why this investment recovery has been so weak, however, may have less to do with monetary policy and rather the functioning of the financial market.

Earlier this year, John Jay College economist and Roosevelt Institute fellow J.W. Mason published a paper called “Disgorge the Cash,” arguing that the U.S. financial system has become less about funneling money to companies who invest it and more about getting cash out of firms. The paper received quite a bit of attention, both positive and negative, so Mason released a new paper last Friday expanding on the topic and answering some criticism.

One such criticism is the idea that business investment was fine during the past two decades, so there’s no need to worry about this disgorgement. Mason shows, however, that business investment growth has actually been very weak during this recovery. In fact, not only is the current investment recovery is the weakest on record, but the second-weakest recovery was the one immediately prior starting in 2001.

This weak growth is especially confusing given the trends in factors we might think would boost investment. For one, investment growth was quite weak even though long-term interest rates were on the decline during the 2000s. And if we think investment is more related to profits, then the weakness of investment growth is also confusing as corporate profits were quite high during this time period.

Mason points at the financial sector as a big culprit. Some have argued that the share buybacks Mason and others have highlighted are merely the recycling of funds from mature companies to new, dynamic firms that will use the funds more productively. But if you look at the sheer amount of shareholder payouts in 2014 ($1.2 trillion), it dwarfs the amount of money going to new companies in the form of initial public offerings and venture capital ($200 billion). For every dollar the system invests in these newer firms, it takes out $6 from older public firms.

Mason’s research paints a grim picture. A well-functioning financial system is supposed to channel savings to their most productive use. Instead, the U.S. system, in total, seems to be more interested in getting money out of firms and into the accounts of wealthy shareholders. As a companion Roosevelt Institute report also released Friday points out, it will take pulling on multiple policy levers to reverse this kind of massive trend. It seems we need to find many levers in order to move the financial world.

Peter Leyden: For those of you who do not know Brad DeLong, he is a professor of economics here at U.C. Berkeley and has been so for a while. He also did a stint at the U.S. Treasury Department in the 1990s in the Clinton administration, working under Larry Summers—which has gotten some stories behind that one…

Brad DeLong: As Gene Sperling once said: “Being Larry’s friend is never dull!”

Peter Leyden: “Is never dull.” Exactly. But I think most people outside of those circles know of him through his weblog, in which he delves deeply into economics and politics. He is quite prolific. He is quite into social media, which he is probably still banging at right now, as he sits on stage. So, Brad, one of the themes that has emerged here—particularly in some of the conversations I have had here, but also through the whole day—is a sense of technology, artificial intelligence, automation, robotics. We had drones here. There is a lot of sense of the how the technology is pushing us in different directions, and kind of disrupting life as we know it. It is continuing to push and disrupt it, and will potentially displace a lot of folks in the economy to come.

Peter Leyden: And so I think, just to open it up, given your economist’s perspective, why don’t you give us just a sense of how you think of the disruption that comes from a lot of these new technologies.

Brad DeLong: First, the industrial disruption has been ongoing for 225 years, at least. The pace at which people have been disrupted has been accelerating, yes. At the start of the eighteenth century the amount of technological progress we get in one year took twenty. By the start of the nineteenth century it was down to what we see in one year they saw in five. By the start of the twentieth century it was down to one in two.

But it has produced enormous dislocations for all 225 years.

Andrew Carnegie’s father was sitting at home in Scotland making a pretty-good living as a skilled handloom weaver. All of a sudden technological improvements three hundred miles south in the form of the power loom destroys his livelihood. I don’t remember whether he starves to death or whether simply his children’s immune systems are so badly compromised by poor nourishment that they die like flies. But Andrew makes it to America. He promptly gets an entry-level job in the high-tech industry of that day as one of the first telegraph operators, one of the first people who makes it their business to sit in front of their telegraph and communicate via the code of Samuel Morse with others across hundreds of miles at lightspeed. And we are off and running.

This has been going on for quite a while. What has done most to illuminate in my mind, with the force of a thousand atomic bombs, was an article—an article that I was discussing this morning with other economists up at the QualComm Cafe on the Berkeley campus—a Wired article of long ago, an article by Neal Stephenson about the submarine telegraph cables of the nineteenth century, a brilliant article called “Mother Earth, Motherboard”. I just discovered in the green room that Peter edited it. And I must say that to edit Neal Stephenson so that not only is every paragraph a diamond of prose but the thing has a proper beginning, middle, and end—that demonstrates true genius.

Peter Leyden: Thank you.

Brad DeLong: If you want to take the really long sweep of history, the argument is this: Up until 6000 years ago by and large the kind of things that we invented were things that allowed us to use all of our human capabilities to do what we had done but do what we did better and more effectively. Spears allow us to hunt large animals—as opposed to throwing rocks at rabbits and hoping you get a lucky hit. Picking the pieces of grass that have really big seeds—what we turn into wheat—allows us to harvest and gather a lot more calories in our daily gathering if we have been lucky or smart enough to have scattered some of the seeds by the riverbank the year before. The invention of the loom allows us to actually weave grasses into cloth much more effectively. But we are are using all of our standard paleolithic human capacities to do so.

Then, in 4000 BC or so, something different happens, something unusual. We domesticate the horse. All of a sudden having people pull things is economically obsolete. Strong human backs and strong thighs are very useful whenever you have big things to move around. But once you have got a horse, a horse can do it better. Horses are much more useful. Horses make human backs and human thighs technologically obsolete as far as moving heavy objects is concerned.

Thus over the past six thousand years, the argument continues, first slowly and then more rapidly, we have had more and more places where things that used to be in the province of human excellence become activities that our draft animals, our domesticated animals, and our machines can and are doing better. The horse takes care of backs and thighs. We get the spinning jenny and the assembly line. They largely take care of fingers—of fine manipulation. We are no longer economically competitive moving things around with our big muscles or, for the most past, finely-manipulating things with our small muscles and nimble fingers. I find that on this iPhone here, in terms of nagging me to actually move around, the Withings App is significantly better than asking somebody to tell me to move around once an hour—not least because the Withings App does not have feelings of its own—not yet. And I cannot snap at the iPhone no matter how many frowny faces it shows me.

Peter Leyden: But do you think that the next generation—the AI brainpower robotics—will take it to the next level? Do you think there is any material difference in this?

Brad DeLong: Up until now, it has been the case that, every time we have domesticated an animal or invented a machine, it has removed the market value from some human excellences. But every such animal or machine or device is not intelligent. Every one requires a cybernetic control mechanism. The human brain is a supercomputer that fits in a breadbox and draws only 50W of power. That is a very impressive cybernetic control mechanism. And so—up until now—whenever you have a horse-guiding task or machine-running task or a machine-programming task or an accounting task, you had to have a human brain in the loop to control what the machines and what the software and what the animals were actually going to do. Now, however, for the first time, we can dimly envision the coming of an age in which machines will be smart enough to run themselves. They will no longer need human minders in the loop to control them.

We already know that a simple computer with the proper big-data regression underneath it could do a significantly better job at choosing which people to admit as graduate students in economics who are likely to succeed. And the faculty committees we currently hand this task to do not do that good a job. Faculty committees are always struck by stories that resonate with them. And such stories always lead them to place too-high a weight on replicating themselves in the next generation of professors, and giving too high a weight to the recommendations from their friends in their social network. The computer is an intelligence, vast and cool and unsympathetic, that does not suffer from such biases. We have reached the stage where it can crunch the data as well as—better than—I can.

Perhaps we are approaching “peak human”. Our last remaining really-strong comparative advantage was the ability of our brains to serve as cybernetic control mechanisms for dumb animals and dumb machines. Perhaps that is coming to an end.

Peter Leyden: But that does not seem to worry you. We were chatting about this before. A lot of that is taken away. How can this play out?

Brad DeLong: There are two roads: First is the road in which we genuinely have Turing-class machines and software assistants that can do for us everything that a human can do. They will serve as super-intelligent Jeeveses to our more-or-less inept [Bertie Woosters29. They will keep the trains running. They will keep us—with our inept bumbling lack of knowledge—from creating chaos and catastrophe. They will keep us from alienating our rich Aunt Agathas from whom we hope for large legacy inheritances, plus low-interest liquidity in the meantime. That road is very much that of the science-fiction novels of the alas!, late genius Iain M. Banks. In his “Culture” universe, every person has a robotic artificially-intelligent personal drone that follows them around and makes sure that their life doesn’t crash into chaos. And the drones—smarter than the humans—do this more-or-less as a hobby. It amuses them. It gives them something to do in the real world, while they use the rest of their brain power to do whatever else they want to do communicating with the other AIs and carrying out whatever projects the AIs have.

Brad DeLong: Second is the road that is well-marked not by science-fiction novels but rather by Regency Romance novels. Down this road, it is Regency Romances that present us with the image of our own future. In the works of Georgette Heyer—riffing off of Jane Austen in a peculiar way—wrote about a social class in a condition of material comfort that had absolutely no productive economic role to perform whatsoever. Even in Austen, neither Mr. Bingley nor Mr. Darcy have or ever will do a lick of socially-productive work in their lives in return for their £5000 or £10000 a year in income, respectively. And nobody expects either of them to a lick of socially-productive work. And everybody thinks that they are wonderful people because they have inherited £5000 or £10000 a year. They are good masters. They will bring you a basket down from the manor house if you are sick. Maybe they will forgive your rent for two months if you break a leg.

This is a society of material abundance for the upper class. Thus the entire narrative force of privation—of desperately trying to get the crops in before the hail smashes them or the grasshoppers eat them so the family of the Little House on the Prairie can survive The Long Winter—is absent. Material scarcity vanishes. So what do people then do? Well, look at what’s displayed at the supermarket checkout line. What people are interested in are: first, avoiding violent death, especially for their children; second, material subsistence, comfort, and fashion; and, third, who’s sleeping with whom. If you manage to greatly reduce the risks of the first and take worry about finding material subsistence away, what you are left with as the primary motive springs of human action and society are:

The social dance that decides who is going to sleep with whom.

The display of human excellence and the acquisition of status via the appreciation and exercise of comfort and fashion.

This is the Regency Romance world. Everyone in it—everyone in the Bon Ton of England in 1820—appears to be very happy engaging in this world. Wearing the right coat, wangling an invitation to Almacks, spending two hours a day tying their cravat so that it looks like they tied it carelessly in a hurry and yet it came out fine, choosing a gown color that compliments rather than clashes with their eyes. Combine that with the great mating-and-affection dance. The characters in Regency Romances manage to keep themselves very busy and occupied indeed. They do not feel like their lives are empty.

Peter Leyden: That assumes, of course, that society allowed for the very top to act like that. If we had this more mechanized society that would take care of material wants, the economy would have to be reorganized differently. In the near term, however, how do you deal with placing people? There has been some creative thinking about that. From the right, we have seen proposals for guaranteed incomes and other things that would essentially liberate people from the spur of material necessity and its trauma.

Brad DeLong: If not—if people have to earn their daily bread by the sweat of their brow by doing something economically-valuable—then we have an immense problem. We have needed a guaranteed income here in the North Atlantic since 1800 or so. Whenever we have not had a social-insurance system, the results of technological change in producing social terror and distress have been enormous. And we economists have more often than not been the bad guys on this.

My most unfavorite line from a nineteenth-century economist comes from Alexis de Tocqueville’s friend Nassau Senior, the first Professor of Political Economy at Oxford. I was, in fact, just an hour ago reciting this line to one of our brand-new assistant professors here at Berkeley, the brilliant young Danny Yagan, who we have been very lucky to hire. Senior was well-known for taking the position that the government of the United Kingdom should not spend any money relieving the distress of Andrew Carnegie’s father and the other handloom weavers whose livelihoods had collapsed out from underneath them with the invention of the power loom. Why not? Because the spur of material privation was necessary to induce them to shift occupations and find other jobs. And if you fed them in idleness to keep them from dire material deprivation and possible death, they wouldn’t search so hard for work. It would take them longer to find other jobs. And in the end the government would waste a great deal of money on outdoor relief without diminishing the total sum of misery created by technological displacement. Misery was the spur needed to induce people to get on their bikes and look for jobs.

The story is this: The Irish Potato Famine created by monoculture and blight stuck. The six million people of Ireland start to starve. It’s pretty clear that the comfortably-sustainable population of Ireland given mid-nineteenth century technology is more like four million or so. One million people, we think, die in the course of the Irish Potato famine. Classicist Benjamin Jowett, Master of Balliol College, distressed, asks Senior about what is going on—how disastrous will it be. Senior replies: “A million Irishmen will die—and that is not nearly enough.”

Peter Leyden: Let’s say we want…

Brad DeLong: Senior says: “We need another million to die to get Ireland down to a comfortably-sustainable population of four million.” What you should say is: We should give them an income—Britain is rich enough to pay. Or: We should move them to Britain, where there are plenty of jobs. Or: We should pay to ship them to Australia, Argentina, Canada, the United States—where there is a great deal of land that can be farmed, of trees that can be cut to build houses, a great deal of work in general to be done productively. People are useful and ingenious. You should give them the power and ability to be so—rather than concluding that they are social waste.

Peter Leyden: Now, this guaranteed income. It is not just a progressive thing. There are roots in conservative thinking too. There is some possibility that…

Brad DeLong: Well… There is, but that was an earlier generation of conservatives than we have here and now. There were roots in conservative thinking. Milton Friedman was always a very big backer of a simple negative income tax—something like the Earned Income Tax Credit we currently have, but more generous and not tied to your having a job. The one that Russell Long started and that Bill Clinton expanded his this property: you have to have a job, you have to work to receive it. Friedman thought it was profoundly undignified and unfree for people to have to justify to the welfare office or the IRS why they qualified for their benefit check. The overwhelming proportion of what we produce, he thought, was the joint collective product of everyone who has come before us and handed us our knowledge. That is our collective inheritance. That has all been given us for free by our predecessors, starting even before the people of Catal Huyuk noticed that the plant that was to become wheat had a really big and tasty seed, continuing with the guy named Ish-Baal or whatever in Phoenecia in 1200 BC who saw that a stylized picture of an ox could represent the phoneme “b” and thus invented the alphabet, on down to here and now. A good society, Friedman thought, would be a relatively unequal society, but it would not have a bottom extreme of dire poverty and people who were unfree because of the harsh spur of absolute material necessity.

But that was an earlier generation of conservatives.

Brad DeLong: That is vanishing from the right. That is, especially, vanishing from the right if the people who are kept out of poverty by social insurance are the wrong kind of people.

Consider what I saw crossing my desk last week. I was in Kansas City, MO, just across State Line Road from Samuel Brownback’s Kansas. Governor Brownback denounced the liberal churches of Kansas and the meager and powerless Democratic Party of Kansas for pushing for Kansas to expand Medicaid. Medicaid expansion is, at the state level, a true no-brainer. The people of Kansas are paying taxes to the federal government for Medicaid expansion all over the country. If they don’t expand Medicaid in Kansas, their tax money will go to pay for medical care for the poor and disabled and elderly disabled here in California and in New York and in Colorado and Arkansas and Illinois, and now Pennsylvania. If they do expand Medicaid they get value back for those federal taxes they are going to pay anyway. As long as Medicaid does not make its recipients sicker and the doctors, nurses, and hospitals who collect it worse off—which it does not—it is a true no-brainer.

Yet Brownback said that he was not going to do it. Why not? Because Medicaid expansion was Barack Obama’s Trojan Horse to keep alive “big city” hospitals that ought to close, and that were going to going to close.

Now, first, this is false. The big-city hospitals of Kansas City, KS, of Topeka, and of Wichita are in better shape than the rural hospitals.

It is small rural hospitals that are going to close. It’s small rural hospitals that white people go to that are under threat. But the only argument Brownback could think to make sotto voce was that Medicaid expansion gives free stuff to urban people who carry ghetto blasters. They are the ones who are going to benefit. And, Brownback hints to his audience of supporters: “We really don’t like that, do we?”

It is scary out on the prairie.

Peter Leyden: We do not have a lot of time here. And there are some interesting questions here. We have been talking about the long-term displacement from technology through a big picture lens. Right now, however, the pressing issue around here now is income inequality. This idea of our politics being trapped, and unable to deal with this. Any thoughts on what could be done relatively quickly, knowing what we know now or what we need to know soon, to shift gears on this and make some substantial progress?

Brad DeLong: First: higher taxes on the rich; more benefits for the poor. That is the first and most obvious plan. We have the least progressive tax-and-transfer system in the North Atlantic. There is no reason why we should. We are still one of the richest. So we should have a somewhat more progressive tax-and-transfer system than the average. We do not.

Second: Back at the start of the 1970s, I think we made a large collective mistake in deciding that we should charge for public colleges. At the time, that decision make some sense. People who are going to college colleges and graduate wind up being richer than average. Why should you tax the average taxpayer in order to subsidize the education of those who are going to, say, Berkeley who will be substantially richer than the average? That makes little sense—or so we thought back in the 1970s. The upper middle class do not need more subsidies.

Third: We have an enormous problem with figuring out how to work our technology. George Eastman was a marvelous inventor and innovator. He produced Kodak as we knew it, and brought middle-class prosperity to 50,000 engineers and to the surrounding city of Rochester New York for generations. Larry Page and Sergei Brin also had truly genius ideas. They grabbed Eric Schmidt to make their company run smoothly—who had grown up a lot since his days writing the Berkeley UNIX clone in the basement of Evans Hall. But Google has not produced broad-based middle-class prosperity for its workers anywhere. It has created a much-smaller group of very, very well-paid engineers, plus a few billionaires. Why did high-tech do one thing in the case of Kodak and another thing in the case of Google? Hell if I know. I wish I did.

Peter Leyden: It could be a very different kind of technology. Unfortunately, we have run out of time. We could probe your brain for a long time here. He gave us a lot of food for thought that we can continue to think about for the rest of the conference for the next couple of days. Thank you.

Adam Posen: To talk about misallocation of capital and added financial risk at great length without mentioning “regulation” once. And to talk about how quantitative easing has greatly added to systemic risk when its principal disappointment has been the failure of quantitative easing to persuade pension funds and corporations to extend themselves out the yield curve.

The argument that ultra-low interest rate policies add to systemic risk seems to be based on a view that they do both of:

inducing people to create more long-duration assets

increasing the duration of existing assets.

And that a world with a lot of long-duration assets is one of great systemic risk.

As we move into our post-December world, the Federal Reserve will have three levers to control 2.5 dimensions of policy:

The federal funds rate.

The rate of interest on reserves.

The size of its balance sheet.

What is our thumbnail measure of monetary policy in such a world?

This is a weekly post we publish on Fridays with links to articles that touch on economic inequality and growth. The first section is a round-up of what Equitable Growth has published this week and the second is work we’re highlighting from elsewhere. We won’t be the first to share these articles, but we hope by taking a look back at the whole week, we can put them in context.

Equitable Growth round-up

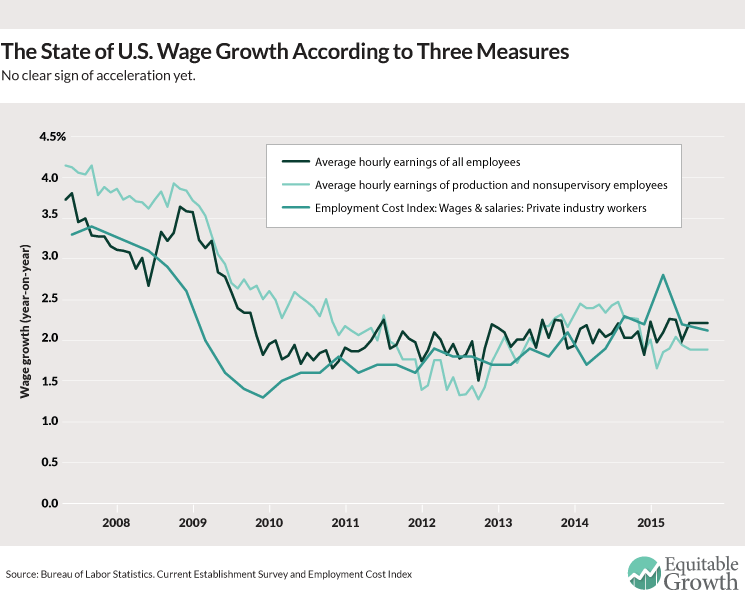

Last week, we got fresh data on U.S. wage and compensation growth for the third quarter of 2015, which showed no pick-up in wage growth. And while wage growth seemed to pick up in today’s employment situation report for October, there’s still no conclusive evidence of accelerating wage growth.

One of the major concerns about the post-Great Recession labor market has been that the millions of workers out of a job for 27 weeks or longer would be locked out of future jobs. But a new study used fake resumes to show that length of unemployment isn’t a detriment (for some workers) for getting called for an interview.

A new report by economists Anne Case and recent Nobel Prize winner Angus Deaton shows an alarming increase in mortality among middle-age whites in the United States. The reasons for this increase aren’t definitively known, but economic insecurity seems like a likely culprit.

Looking back at the efforts to rein in budget deficits so soon after the Great Recession shows the many problems with that approach. In fact, it may have hurt the potential growth of gross domestic product. And that has important implications for our conversations about secular stagnation.

Following this morning’s jobs report, Ben Zipperer takes a look at the stagnation of the employment rate for prime-age workers and links that to the new report from Case and Deaton.

Links from around the web

Jeff Guo looks at research as to why women are sometimes hesitant to compete against men, and comes away with a new argument for hiring quotas. This form of affirmative action can increase the number of qualified women who apply for a job. [wonkblog]

When accelerating wage growth shows up, will the acceleration be gradual or quick? Adam Ozimek looks at the relationship between unemployment and the Employment Cost Index among U.S. metro areas and finds that the acceleration will likely be smooth and steady. [moody’s]

When talking about how economic instability abroad threatens the U.S. economy, economists often mention that the United States is a relatively closed economy. But that might not be the case anymore, and that has important implications for when the Federal Reserve raises interest rates, according to Menzie Chinn. [econbrowser]

A new Pew Research Center survey shows the amount of stress that working parents experience. Claire Cain Miller discusses how, while both parents working is increasingly becoming the norm, “public policy, workplace structure and mores have not seemed to adjust.” [the upshot]

Household debt growth has remained tepid, at least compared to last decade, but who is this new credit flowing to? Four economists from the Federal Reserve Bank of New York find that most household debt is flowing more to higher-income households, with the major exception of student debt. [liberty street economics]

{kind=link}