This has been available in full exclusively at the magnificent and well worth subscribing-to Talking Points Memo.

SEND TPM MONEY!!!!

But now let me let it out into the wild here–and promise to imminently (well, maybe in a month…) write about the whole symposium of which it is a part:

The Melting Away of North Atlantic Social Democracy: Hotshot French economist Thomas Piketty, of the Paris School of Economics, looked at the major democracies with North Atlantic coastlines over the past couple of centuries. He saw five striking facts:

- First, ownership of private wealth—with its power to command resources, dictate where and how people would work, and shape politics—was always highly concentrated.

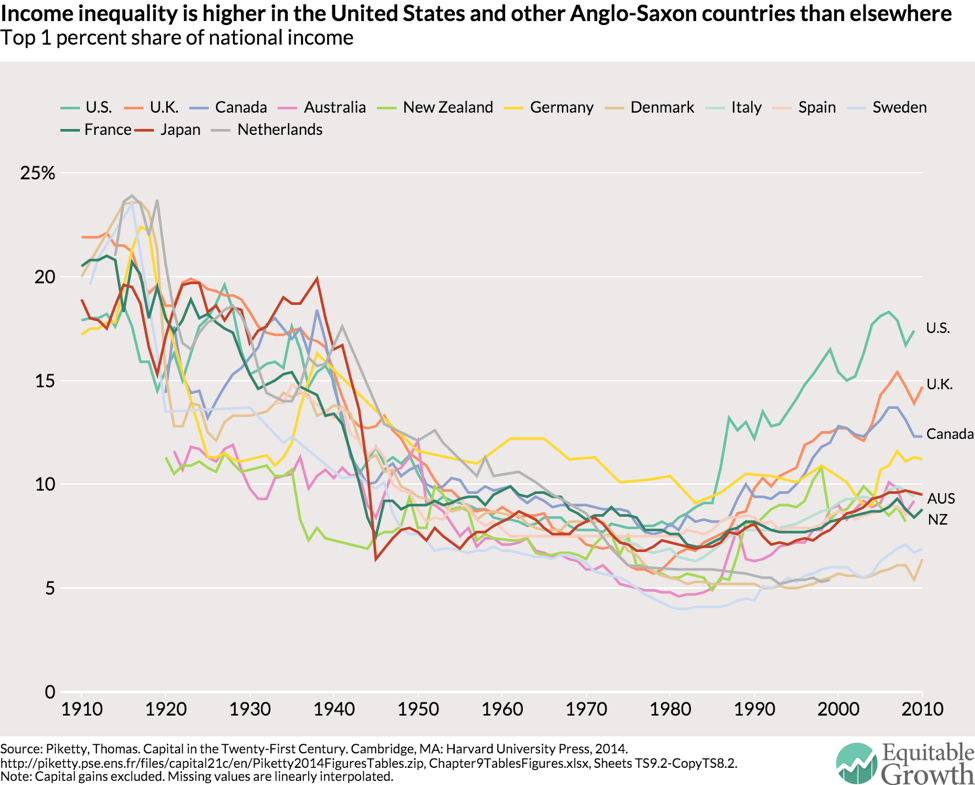

- Second, 150 years—six generations—ago, the ratio of a country’s total private wealth to its total annual income was about six.

- Third, 50 years—two generations—ago, that capital-income ratio was about three.

- Fourth, over the past two generations that capital-income ratio has been rising rapidly.

- Fifth, the flow of income to the owner of the dollar capital did not rise when capital was relatively scarce, but plodded along at a typical net rate of profit of about 5% per year generation after generation.

He wondered what these facts predicted for the shape of the major North Atlantic economies in the 21st century. And so he wrote a big book, Capital in the Twenty-First Century, that was published last year.

It has been a surprise bestseller. Thomas Piketty’s English-language translator, Art Goldhammer, reports that there are now 2.2 million copies in print and e-book form in 30 different languages scattered around the globe.

Piketty’s big surprise best-selling book has one central claim: Two generations ago the major North Atlantic economies were all four stable social democracies—relatively egalitarian places when viewed in historical perspective (for native-born white guys, at least), with political voice widely distributed throughout the population, the claims of wealth to drive political directions and shape economic structures not neutralized but kept within bounds. That was the North Atlantic economy that we lived in and had grown used to as recently as one generation ago. That, Piketty argues, was an unstable historical anomaly. It is now passing away.

Piketty believes that the rising inequality trends we have seen over the past generation and see now are simply returning us to what is the pattern of unequal income distribution and dominant plutocracy that is normal for an industrialized market economy in which productivity growth is not unusually fast. We had thought otherwise, and grown used to the social-democratic structure of two generations ago only because it came at the end of an era in which productivity growth had been unusually fast; the various political, depression, and revolutionary shocks to overturn established and inherited wealth had been atypically large.

The social democratic economy model the major North Atlantic economies followed as recently as a single generation ago had five salient features:

- For one, that labor was important relative to ownership of wealth as a source of income.

- Next, enterprise and savings were important relative to inheritance as a source of accumulated wealth.

- Opportunity, while constrained by race and gender, was not that constrained by class—there was upward mobility.

- Economic growth—both numbers of workers and the productivity of the average worker—was relatively rapid, with each generation clearly larger and more productive than its predecessor.

- And, finally, politics were relatively democratic, in that while the rich spoke with a louder voice, their concerns did not drown out the economic interests of others.

And Thomas Piketty’s central claim is that all five of these once-salient features of our social democracy are vanishing. We are, he believes, on a long-run historical trajectory to return us to a situation more like the nineteenth century, in which ownership of capital is more important relative to labor as a source of income; inheritance dominates enterprise and savings as a source of wealth; opportunity is tightly constrained by class of birth; economic growth is slow (both because of declining technological invention and birth rates on the one hand, and because established wealth, which is hostile to the creative destruction that drives economic growth, possesses a bigger voice in shaping the political economy); and politics is dominated by plutocrats.

Capital in the Twenty-First Century has struck a chord—hence its 2.2 million copies. And it has excited a fierce debate, with more and more people finding it worth arguing about both for the reasons that it struck a chord and because of the fact that it has struck a chord.

The first question is: Do we care?

Some—perhaps many—say that we do not care. There is one often-made thread of argument that we simply should not care about inequality, which is good as an engine of faster economic growth and not a problem for an economy, a society, or a country at all. What is a problem, this thread maintains, is poverty. And because we are now much richer than our predecessors of six generations ago, the amount of inequality that back then caused poverty and so was a problem does not cause poverty and so is not a problem today.

I think this is wrong. I think we do care.

- First, anyone who has looked at the distribution of medical care in the United States and our abysmal health outcome statistics relative to other rich countries cannot help but see that inequality is a factor that leads enormous investments of resources to deliver little of ultimate value in the sense of human well-being and human satisfaction. The point generalizes beyond the health sector: an unequal economy is one that is lousy at turning productive potential into societal well-being. We could be doing better—and with a more equal income and wealth distribution would be.

-

Second, as noted above, established wealth, especially inherited wealth, is by its nature hostile to the creative destruction that accompanies rapid economic growth, for it is established wealth that is creatively destroyed. Plutocrats and their ideologues like to claim that too equal an income distribution destroys incentives to work and turns us into a ‘nation of takers.’ But a return to the inequality levels of the 1960s would not turn us into Maoist China. In the relevant range of levels of inequality, it is much more likely that higher inequality will slow growth by depriving the non-rich of the resources to invest in themselves, their children, and their enterprises; It will further slow growth by focusing effort on helping the rich keep what they have at the cost of squelching the development of the new.

-

Third, a society in which plutocrats deploy their resources to have not just a loud but an overwhelming voice will be a society in which government sets about to solve problems of concern the plutocrats and not the people. And that is unlikely to be a good society.

So: Yes, we care.

The second, relevant, question is then: Is he right?

The only possible answer is ‘perhaps’.

Everything hinges on what ‘on our current political-economic trajectory’ means. So what might we take that phrase to mean? And under which interpretations of that phrase is Piketty right, and under which is he wrong?

Our Current Trajectory: Piketty’s View

Piketty’s view is that our current trajectory has five elements:

- For one thing, we now have a demographic pattern determined by literate women’s preference to have two or fewer children. Thus we have slow—or zero—population growth.

- For another, the pace of technological progress may well be slowing from its 20th-century white-heat intensity. Thus slower population and slower productivity growth combine to produce slower overall growth, and so wealth accumulated in the past when the economy was smaller looms larger in the present than it would were the economy expanding more rapidly.

- In addition, ever since—even before—the start of the Industrial Revolution, we have seen the system of property rights continually tweaked, via a politics in which money talks loudly, in order to keep the rate of profit on wealth roughly at 5% per year. The British economist John Maynard Keynes was one of many who thought that a world of more wealth accumulation would also be one of a more equal income distribution. As capital accumulated, he thought, that capital would have to bid for the services of workers to operate it. It would do that by offering to accept a lower rate of profit in order to pay higher wages and salaries. The profit rate would, he thought, fall more rapidly than the stock of capital would grow, and we would have what he called the ‘euthanasia of the rentier’: even though the rich might be very rich indeed in terms of assets, their relative share of income would, over time, fall. But, Piketty documents, this seems to be wrong: The overall profit rate did not rise when economies went from the wealth-to-annual income ratio of six that it was six generations ago to the one of three that it was two generations ago. The overall profit rate has not fallen as wealth-to-annual-income ratios have risen.

- Yet another factor is the concentration of savings among the rich, for—contrary to economists’ standard life-cycle theories—the proportion of income saved does not decline with increasing wealth. And so a higher stock of wealth does not induce forces that tend to spread it around, but rather induces forces that concentrate it.

- And, last, Piketty sees money as talking even louder in politics than it used to and thus preventing, with increasing strength over time, the implementation of policies that might redistribute wealth and so keep the social-democratic political-economic order alive.

In Piketty’s view, we are now more than a full generation into this process of the passing away of North Atlantic social democracy.

This process, however, has not yet come to an end. It will, he thinks, take another two generations or more for the logic he sees driving us on our current trajectory to work itself through to its completion. We haven’t, in Piketty’s view, seen anything yet, at least support as far as plutocracy is concerned.

The Demand for Bad Critiques of Piketty

A substantial number of critics have offered differing strongly negative views of Piketty’s theories.

There is, for example, Greg Mankiw from Harvard and his (2015) ‘Yes, r > g. So What?’:

There is… good reason to doubt… the ‘endless inegalitarian spiral’ that concerns Piketty…. The worrisome ‘endless inegalitarian spiral’… [requires] the return on capital r to exceed the economy’s growth g by at least 7 percentage points per year…. There is no ‘endless inegalitarian spiral’…’

I presume Mankiw picked up the phrase ‘endless inegalitarian spiral’ from Piketty’s introduction, where the phrase is not a prediction of the necessary consequences that follow from r > g. It is, instead, a description of what the data Piketty has compiled and analyzed tells us about the pre-WWI Belle Époque:

1870–1914 is at best a stabilization of inequality at an extremely high level, and in certain respects an endless inegalitarian spiral…

Mankiw’s critique was pre-butted not just in Capital in the Twenty-First Century, but also in Piketty’s (2015) ‘Putting Distribution Back at the Center of Economics’ in which he explicitly refers critics to Stanford economist Charles Jones and to Piketty’s online appendix. An economy with a larger gap between the rate of profit r and the rate of economic growth g will indeed be an economy with more concentrated wealth. Mankiw’s implicit claim that we should remain unconcerned with wealth inequality and concentration unless and until it is growing without bound toward infinity—even among a brazen goalpost-moving exercises, that is a remarkably brazen one.

There is also, for example, a paper from Daron Acemoglu of MIT and James Robinson of Chicago (2015), ‘The Rise and Decline of General Laws of Capitalism’. It claims that the theoretical mechanisms stressed by Piketty cannot be seen in the real world. To this Piketty responds by arguing that they are looking at changes over much too short a time period to see what is and will in the future be going on:

The process of intergenerational accumulation and distribution of wealth is very long-run process, so looking at cross-sectional regressions between inequality and r − g may not be very meaningful…

There is Stanford’s Allan Meltzer, and his 2014 ‘The United States of Envy’:

The Obama administration has drawn the political discussion away from its unpopular and flawed… Obamacare… income redistribution… based heavily on research by two French economists named Thomas Piketty and Emanuel Saez. The two worked together… at MIT, where the current research director of the IMF, Olivier Blanchard, was a professor…. He is also French. France has, for many years, implemented destructive policies…

There is Clive Crook’s 2014 ‘The Most Important Book Ever Is Wrong’, which I will leave to the Economist’s Ryan Avent:

You don’t even have to read hundreds of pages to get the qualification Mr. Crook wants; you can start with the page on which r>g is first mentioned…. I suppose if you only read the book’s conclusion you could miss these details, but who would do that?’

If there is a worst critique of Piketty from a technical economics standpoint, it is made by Per Krusell of Gothenberg and Anthony A. Smith of Yale in their 2015 ‘Is Piketty’s ‘Second Law of Capitalism’ Fundamental?’. They assume—without presenting evidence or data—that their key parameter is 10% per year when Piketty documents that it appears to be less than 2% per year. When challenged, they write only:

DeLong’s main point is that the rate we are using is too high (we use 10% in one place and 8% in another place…. (We conducted a quick survey among macroeconomists at the London School of Economics, where Tony and I happen to be right now, and the average answer was 7% [per year]…

This response seems to me to be remarkably weak. This response seems to me to indicate only that the macroeconomists they talk to have neither carried out aggregate growth-accounting calculations nor reflected on what share of society’s productive assets are machines that depreciate at 7% per year, as opposed to land, buildings, and infrastructure that depreciate much more slowly.

When I look at these—and other—critiques of Piketty and assess their quality, I find myself quite surprised. And I find myself strongly tempted to agree with what Piketty said at the January 2015 American Economic Association meeting about billionaires:

We know something about billionaire consumption, but it is hard to measure some of it. Some billionaires are consuming politicians, others consume reporters, and some consume academics…

The Demand for Piketty

I do find it disappointing that so many critiques, indeed what appear to me to be the standard critiques, of Piketty, do not look much like academic analyses. Instead, they look more like things designed to reassure standard billionaires hoping to establish a dynasty. If Piketty is wrong, it is important to figure out why. For his book has definitely struck an immense nerve: people want answers to questions, and they hope Piketty will provide them.

So let me turn to Capital in the Twenty-First Century as a sociological-intellectual phenomenon.

I did not expect Capital in the Twenty-First Century to go, in a sense, viral.

I expected the book to sell ten copies to libraries and professors here at Berkeley, and a couple hundred copies to students here—10,000 copies worldwide.

Art Goldhammer quotes William Sisler, head of Piketty’s English-language publisher, Harvard University Press, as being more optimistic and expecting total sales in the 10-20,000 copy range ‘if we were lucky’.

Capital in the Twenty-First Century does indeed have many excellences. Its logic is clear and powerful. It is comprehensively documented by very skillful extraction and presentation of the data. It deals with very big and important questions. It takes a broad historical and moral-philosophical view.

But I thought it would be a book for a narrow audience: myself and a few others.

You had to like mathematical economic growth theory, economic history, going deep into the weeds of data construction, plus have read Balzac and Jane Austen to be comfortable in the intellectual world of the book. It seemed to me that there were very few people whose interests were as broad as Thomas Piketty’s. Given that the book makes few concessions to and demands much of its audience, I expected that audience to be small—not large.

Better Critiques of Piketty

So it is in a way fortunate that there are some better critiques of Piketty’s argument out there. An MIT graduate student has mounted the best sustained critique: Matthew Rognlie points to a set of considerations that John Maynard Keynes called the ‘euthanasia of the rentier’:

- As capital accumulation proceeds, more and richer people seek to entrust their larger and larger wealth to entrepreneurs to buy machines relative to the number of workers who seek to be hired by entrepreneurs to work the machines.

- Thus by simple supply-and-demand the rate of profit declines.

- Thus increasing wealth accumulation enriches workers-their productivity at the margin rises and entrepreneurs are willing to bid more for their services.

- And increasing wealth accumulation does not impoverish the wealthy, but it does make their wealth less salient as a source of income.

Thomas Piketty’s response to this is, roughly: Rognlie’s argument sounds very good in neoclassical economic theory, but fails in historical practice. Supply-and-demand tells us that when the economy’s wealth-to-annual income ratio varies, the rate of profit should vary in the opposite direction. But history tells us that the rate of profit sticks at 5% per year, across eras with very different wealth-to-annual-income ratios.

Piketty, however, does not tell us why.

Perhaps this is because at a technological level capital does not empower and complement but rather competes with and thus substitutes for labor. Perhaps this is because of successful rent-seeking by the rich who control the government and get it to award them monopoly rents. Perhaps it is because of a social structure that leaves wealth holders believing that a 5% per year is the ‘fair’ rate of profit and are unwilling to underbid each other. Piketty is agnostic here.

This makes his argument both difficult to criticize, and less than fully satisfactory. For, Rognlie points out, the big news so far in the accumulation of wealth and the surge in income received by wealth holders comes from housing, which has risen from 3% of total income to 8% of total income here in the U.S. since World War II. Similar forces are at work in England and France: simply look at rents these days in central London or central Paris. And the collapse of the wealth of European Belle Époque elites after 1900—though not of American Gilded Age elites—owed a lot to the falling value of their broad-acre agricultural-land estates as globalization and rapid improvements in farm productivity enriched the economy as a whole but left agriculture relatively impoverished. In Rognlie’s view, the connection between wealth inequality and income inequality is largely a reflection of the dynamics of housing prices—and, I would add, in Europe agricultural land values. And, in Rognlie’s and Piketty’s view, the rise in U.S. income inequality at the top up until now is only tangentially related to the concentration of wealth. Rather, it is the superincomes of corporate executives, anesthesiologists and allied specialties, and financiers that we have seen so far—and they have not had to have much wealth of their own to grasp these prizes. (Although, of course, their children will then start out with a great deal of wealth.)

There are additional complaints that I regard as serious:

- First, as James K. Galbraith has most aggressively noted, Piketty tacks back-and-forth between a market value—the capitalized current value of all claims on income that are not brow-sweat—and a physical quantity conception of capital in a way that cannot be completely legitimate.

- Second, I would be much more comfortable with a framework in which, instead of talking about ‘tendencies’ that can be counteracted by ‘special factors,’ Piketty included the ‘special factors’ in the model and then forecast the economy’s destiny.

- And, third and most important of all, Piketty badly needs a political-economic theory of the constancy of the rate of profit that he finds in his data. He does not have one.

I think these critiques have force, all of them: from the ‘euthanization of the rentier’ as a possibility that needs to be considered, to the need to understand housing and agriculture separately rather than lumping them into ‘wealth,’ the need to be clear about the units—dollars on the one hand or acres and machines on the other—of measurement, my economist’s preference for predictions of equilibrium points rather than identification of tendencies, and the need for a political economy-based theory of how government capture by the rich means that wealth accumulated is not spent invested in projects that make us richer, but rather in better ways of raising the share of a constant-sized pie that is carved up for the rich.

Assessment

When I try to evaluate the state of the debate over Thomas Piketty’s Capital in the Twenty-First Century two years after its first (French) publication, I find myself driven to three conclusions. The factors that Piketty identifies as leading to the melting-away of the social-democratic North Atlantic economy are operating, but so far their effects on income and wealth inequality have been smaller than other largely-unrelated factors that have been operating in the past generation and generating the rise of housing as a source of wealth and the rise of the super-incomes. Piketty’s factors have been supercharged by other forces over the past generation, but that does not mean that they are not at work—and, in fact, reinforces the chances that Piketty’s inequality-driving factors will be of decisive importance over the next seventy years. The question of whether our road leads to Piketty (2014)—a new Belle Époque plutocracy—or Keynes (1936)—a euthanization of the rentier in which the wealth of the rich is outlandish but their incomes are not due to low rates of profit—hinges on our politics. And our politics is something we can control.

We as a civilization could decide that we are not willing to let money talk so loudly in politics. We could keep our politics from being one of establishing monopoly after monopoly and rent-extraction chokepoint after rent-extraction chokepoint. If we manage that, then the forecasts of Keynes (1936) and Rognlie (2015 will come true, and a rise in wealth accumulation will carry with it a fall in the rate of profit, and a highly-productive not-too-unequal society.

But right now money talks very loudly indeed. And I leave the Piketty debate more depressed about our ability to keep it from talking so loudly. What makes me more depressed? The Piketty debate itself does: The eagerness of so-many economists to aggressively make so many shoddy arguments that Piketty does not know what he is talking about–that makes me think that Piketty does indeed know what he is talking about.